47. During 2012, Smithson Corp. had the following cash flows: receipt from customers,

$10,000; receipt from the bank for long-term borrowing, $6,000; payment to suppliers,

$5,000; payment of dividends, $1,000, payment to workers, $2,000; and payment for

machinery, $8,000. What amount would be reported for financing cash flows on the

Statement of Cash Flows?

48. Cash paid for financing activities would include cash paid for:

49. Cash received from issuing common stock would be classified in which section of the

Statement of Cash Flows?

50. Which of the following would be classified as an investing cash flow?

51. During 2012, Victoria Group: (1) received cash of $5,000 billed to a customer in 2011; (2)

earned $20,000 of net income; (3) paid interest of $6,000 on a corporate bond issued; (4) paid

dividends of $8,000 to its stockholders; (5) borrowed $40,000 from a local bank; and (6)

purchased its own shares of common stock for $10,000. What is Victoria Group’s cash flow

from financing activities in 2012?

52. The following information pertains to Alpha Computing at the end of 2012:

Alpha Computing’s Retained Earnings account had a zero balance at the beginning of 2012.

What amount of dividends did the company pay in 2012?

53. The balance sheet of Sound Designs reports total assets of $750,000 and $800,000 at the

beginning and end of the year, respectively. Sales revenues are $1.5 million ($1.2 million in

the previous year), net income is $150,000, and net cash flows from operating activities are

$175,000. What is Sound Designs’ cash return on assets?

54. The balance sheet of Sound Designs reports total assets of $750,000 and $800,000 at the

beginning and end of the year, respectively. Sales revenues are $1.5 million ($1.2 million in

the previous year), net income is $150,000, and net cash flows from operating activities are

$175,000. What is Sound Designs’ cash flow to sales?

55. The balance sheet of Sound Designs reports total assets of $750,000 and $800,000 at the

beginning and end of the year, respectively. Sales revenues are $1.5 million ($1.2 million in

the previous year), net income is $150,000, and net cash flows from operating activities are

$175,000. What is Sound Designs’ asset turnover?

56. The balance sheet of Tech Track reports total assets of $400,000 and $500,000 at the

beginning and end of the year, respectively. Sales revenues are $1.1 million ($0.8 million in

the previous year), net income is $40,000, and net cash flows from operating activities are

$50,000. How does Tech Track’s cash return on assets compare to the industry average of

10%?

57. The balance sheet of Tech Track reports total assets of $400,000 and $500,000 at the

beginning and end of the year, respectively. Sales revenues are $1.1 million ($0.8 million in

the previous year), net income is $40,000, and net cash flows from operating activities are

$50,000. How does Tech Track’s cash flow to sales ratio compare to the industry average of

5%?

58. The balance sheet of Tech Track reports total assets of $400,000 and $500,000 at the

beginning and end of the year, respectively. Sales revenues are $1.1 million ($0.8 million in

the previous year), net income is $40,000, and net cash flows from operating activities are

$50,000. How does Tech Track’s asset turnover compare to the industry average of 2.4 times?

59. We can separate cash return on assets into:

60. We calculate cash return on assets as

61. Which of the following statements is not true relating to cash flow analysis?

62. The balance sheet of Storage Solutions reports total assets of $300,000 and $350,000 at

the beginning and end of the year, respectively. The cash return on assets for the year is 10%.

What is Storage Solutions’ net cash flows from operating activities for the year?

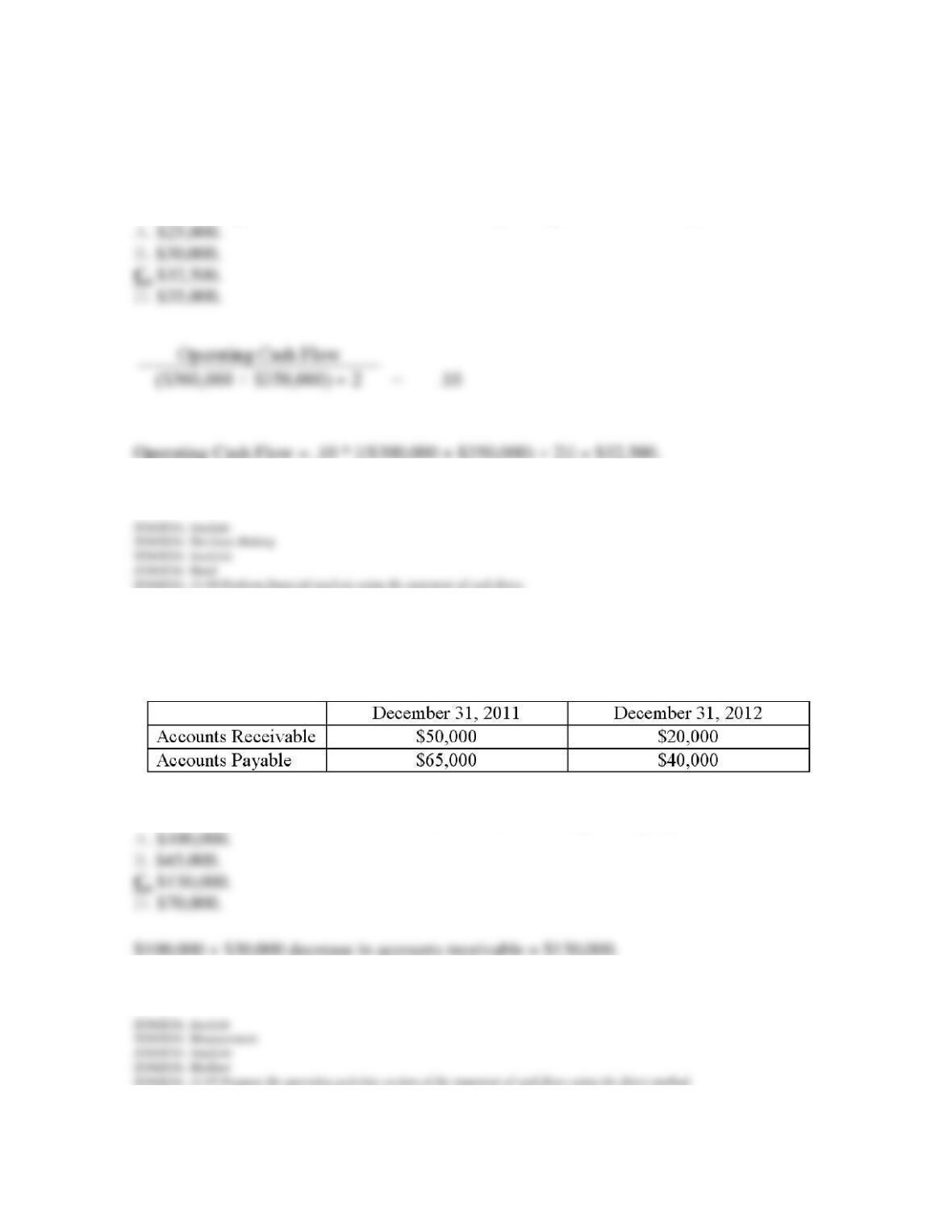

63. In 2012, Hope Company incurred sales on account of $100,000. The company also has the

following information:

What is the amount of cash received from customers for Hope Company in 2012?

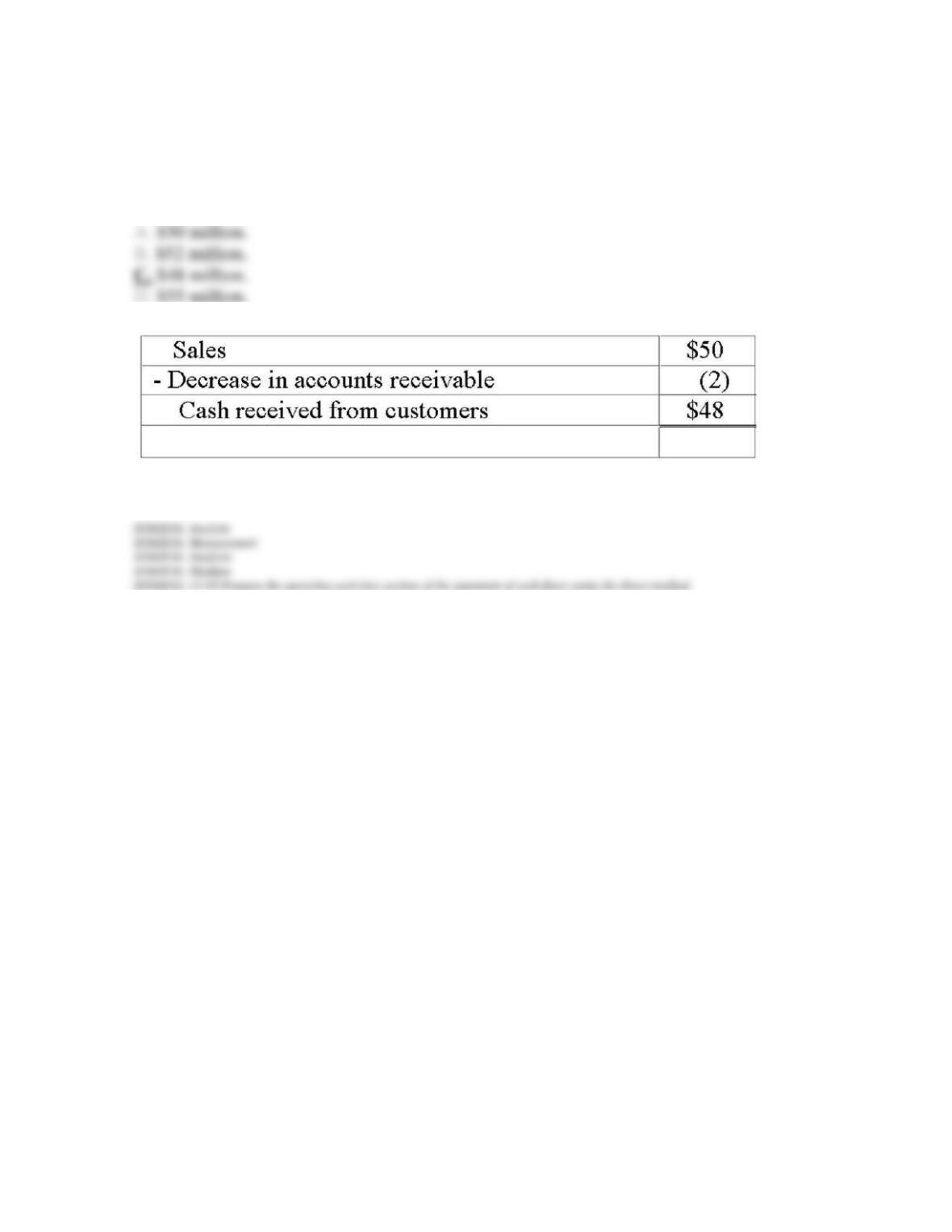

64. Wireless Technologies reports sales of $50 million. Accounts receivable at the beginning

and end of the year are $5 million and $7 million, respectively. What is the amount of cash

received from customers?

65. Wireless Technologies reports cost of goods sold of $40 million. Inventory at the

beginning and end of the year are $4 million and $3 million, respectively. Accounts payable at

the beginning and end of the year are $3 million and $6 million, respectively. What is the

amount of cash paid to suppliers?

66. Wireless Technologies reports operating expenses of $2 million. Operating expenses

include rent expense. Prepaid rent at the beginning and end of the year are $20,000 and

$70,000, respectively. All other operating expenses were paid in cash as incurred. What is the

67. Wireless Technologies reports income tax expense of $800,000. Income tax payable at the

beginning and end of the year are $50,000 and $70,000, respectively. What is the amount of

cash paid for income taxes?

68. Data Solutions reports sales of $100 million. Accounts receivable at the beginning and

end of the year are $6 million and $9 million, respectively. What is the amount of cash

received from customers?

69. Data Solutions reports cost of goods sold of $75 million. Inventory at the beginning and

end of the year are $8 million and $9 million, respectively. Accounts payable at the beginning

and end of the year are $5 million and $3 million, respectively. What is the amount of cash

paid to suppliers?

70. Data Solutions reports operating expenses of $5 million. Operating expenses include rent

expense. Prepaid rent at the beginning and end of the year are $120,000 and $80,000,

respectively. All other operating expenses were paid in cash as incurred. What is the amount

of cash paid for operating expenses?

71. Data Solutions reports income tax expense of $1,700,000. Income taxes payable at the

beginning and end of the year are $250,000 and $370,000, respectively. What is the amount of

cash paid for income taxes?

72. Schneider Inc. purchases its inventory from suppliers on account. During the year, its

Inventory account increased by $10 million and its accounts payable to suppliers decreased by

$3 million. Cost of goods sold was $440 million, its cash outflows to inventory suppliers

totaled:

73. A company’s Income Tax Payable account decreased from $14 million to $12 million

during the year. If its income tax expense was $80 million, what would be shown as cash paid

for income taxes under the direct method?

74. Which of the following items is not reported in the operating section of the statement of

cash flows using the direct method?

75. Which of the following items is reported in the statement of cash flows using the direct

method?

76. A statement of cash flows provides a summary of cash inflows and cash outflows during

the reporting period.

77. The three primary categories of cash flows are cash flows from operating activities, cash

flows from investing activities, and cash flows from financing activities.

78. Financing activities include cash receipts and cash payments for transactions relating to

revenue and expense activities.

79. Investing activities include cash transactions involving the purchase and sale of long-term

assets and current investments.

80. Operating activities are both inflows and outflows of cash resulting from the external

financing of a business.

81. We report interest and dividends received from investments with investing activities.

82. We report interest paid on bonds or notes payable with operating activities rather than

financing activities.

83. We record dividends received as a financing activity.

84. We record dividends paid as a financing activity.

85. Transactions that don’t increase or decrease cash, but that result in significant investing

and financing activities, are reported either directly after the cash flow statement or in a

separate note to the financial statements as noncash activities.

86. The purchase of long-term assets by issuing debt is recorded as both an investing activity

and a financing activity.

87. The total net cash flows from operating activities differ between the direct and indirect

methods.

88. Using the indirect method, we begin with net income and then list adjustments to net

income in order to arrive at operating cash flows.

89. Using the direct method we adjust the items on the income statement to directly show the

cash inflows and outflows from operations.

90. Since depreciation expense reduces net income, companies will add depreciation expense

back to net income as a step in arriving at net cash flows from operations under the indirect

method.

91. We need to add back to net income any loss on sale of long-term assets in the operating

section of the statement of cash flows in order to eliminate the noncash component of net

income.