141

122) Millonzi Corporation manufactures one product. It does not maintain any beginning or

ending Work in Process inventories. The company uses a standard cost system in which

inventories are recorded at their standard costs and any variances are closed directly to Cost of

Goods Sold. There is no variable manufacturing overhead. The company’s balance sheet at the

beginning of the year was as follows:

Millonzi Corporation

Balance Sheet

January 1

Assets

Cash

$1,170,000

Raw materials inventory

52,725

Finished goods inventory

81,060

Property, plant, and equipment (net)

601,000

Total assets

$1,904,785

Liabilities and Equity

Retained earnings

$1,904,785

Total liabilities and equity

$1,904,785

The standard cost card for the company’s only product is as follows:

Inputs

Standard

Quantity

or Hours

Standard Price

or Rate

Standard

Cost

Direct materials

3.7

liters

$9.50

per liter

$35.15

Direct labor

0.90

hours

$18.50

per hour

16.65

Fixed manufacturing overhead

0.90

hours

$17.50

per hour

15.75

Total standard cost per unit

$67.55

The company calculated the following variances for the year:

Materials price variance

$16,800

F

Materials quantity variance

$950

F

Labor rate variance

$5,484

U

Labor efficiency variance

$3,700

F

Fixed manufacturing overhead budget variance

$11,100

F

Fixed manufacturing overhead volume variance

$152,775

U

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing

overhead of $236,250 and budgeted activity of 13,500 hours.

142

During the year, the company completed the following transactions:

a. Purchased 21,000 liters of raw material at a price of $8.70 per liter.

b. Used 19,510 liters of the raw material to produce 5,300 units of work in process.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash)

worked 4,570 hours at an average cost of $19.70 per hour.

d. Applied fixed overhead to the 5,300 units in work in process inventory using the predetermined

overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs

for the year were $225,150. Of this total, $165,150 related to items such as insurance, utilities, and

indirect labor salaries that were all paid in cash and $60,000 related to depreciation of

manufacturing equipment.

e. Transferred 5,300 units from work in process to finished goods.

f. Sold for cash 5,500 units to customers at a price of $108.90 per unit.

g. Completed and transferred the standard cost associated with the 5,500 units sold from finished

goods to cost of goods sold.

h. Paid $27,000 of selling and administrative expenses.

i. Closed all standard cost variances to cost of goods sold.

143

Required:

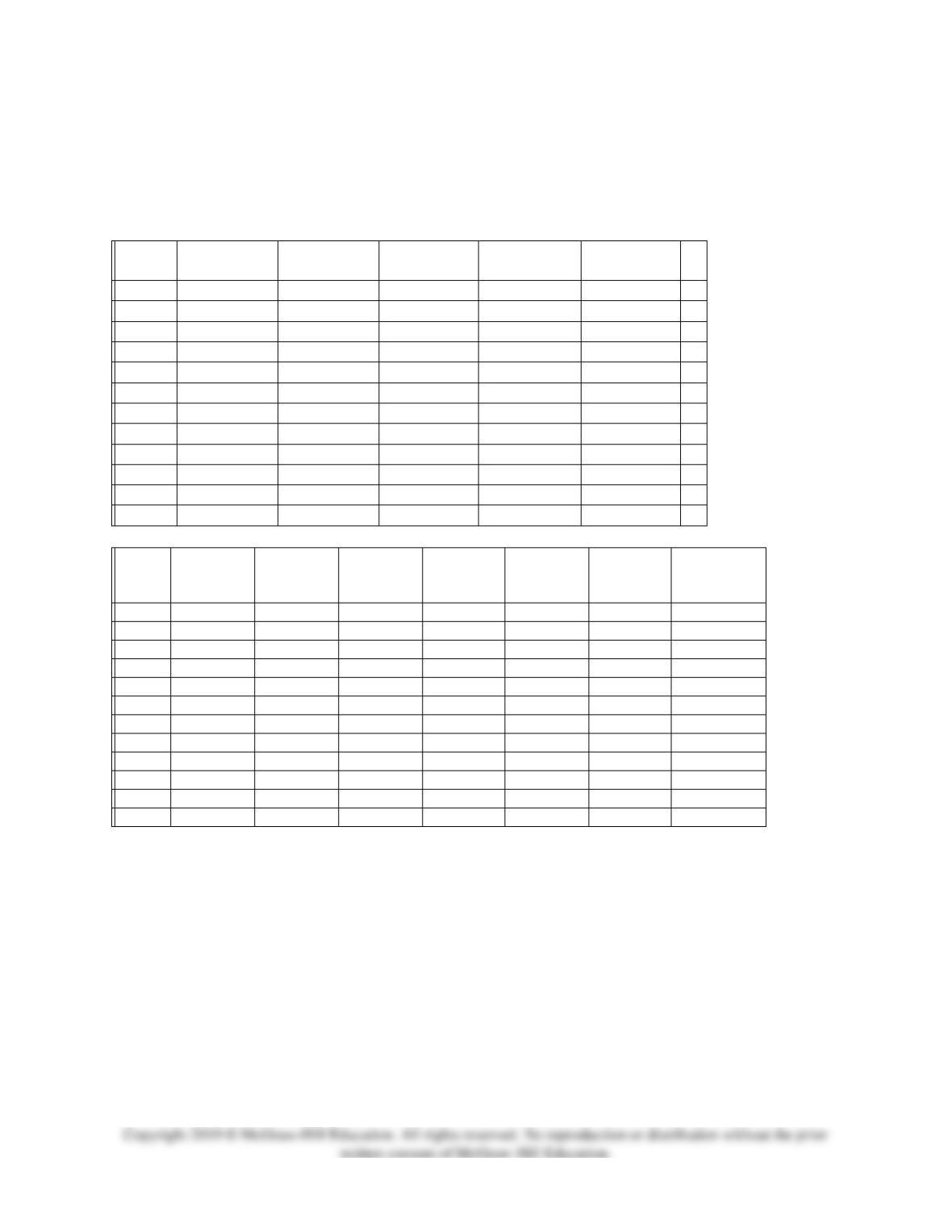

1. Enter the beginning balances and record the above transactions in the worksheet that appears

below. Because of the width of the worksheet, it is in two parts. In your text, these two parts would

be joined side-by-side to make one very wide worksheet.

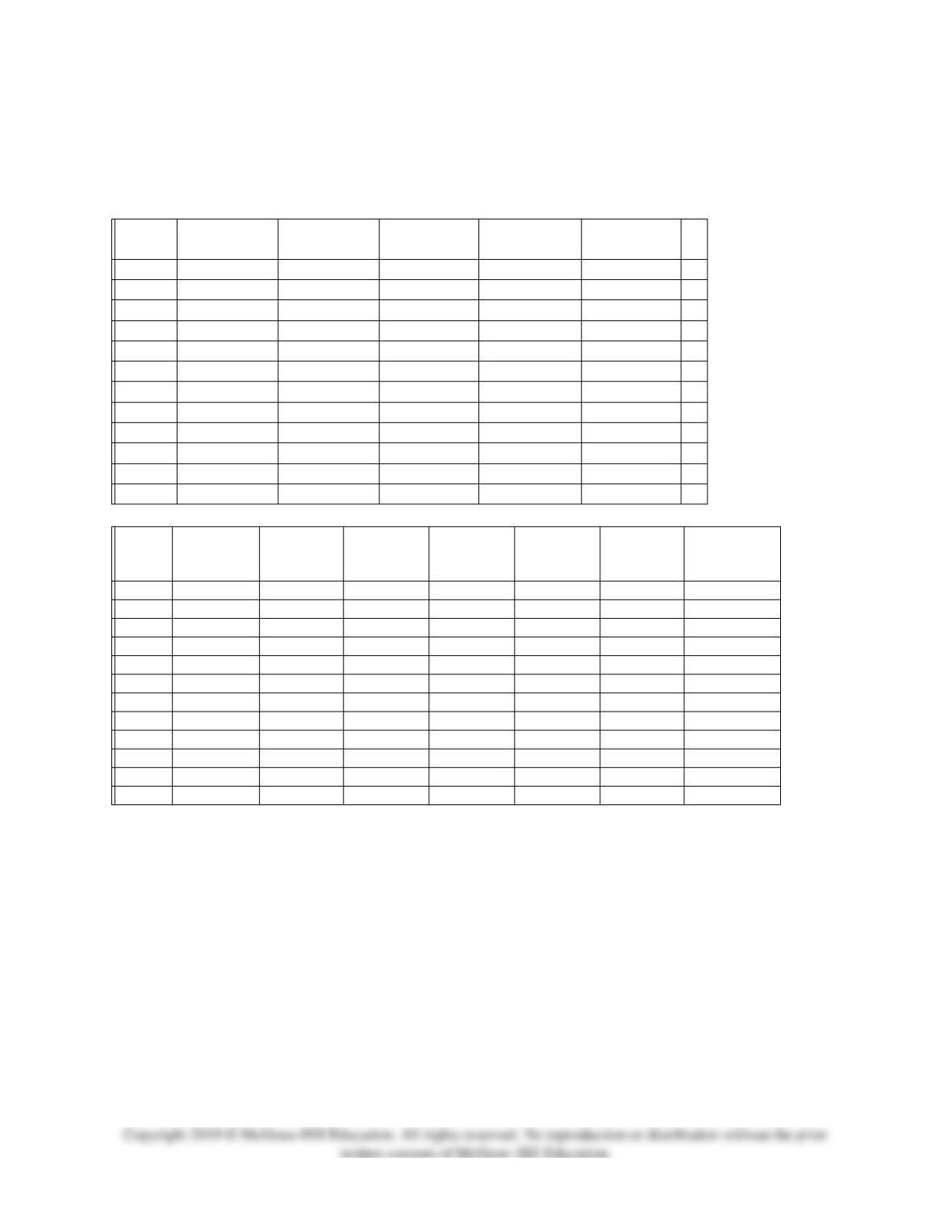

Cash

Raw Materials

Work in

Process

Finished

Goods

PP&E (net)

=

1/1

=

a.

=

b.

=

c.

=

d.

=

e.

=

f.

=

g.

=

h.

=

i.

=

12/31

=

=

Materials

Price

Variance

Materials

Quantity

Variance

Labor Rate

Variance

Labor

Efficiency

Variance

FOH Budget

Variance

FOH

Volume

Variance

Retained

Earnings

1/1

a.

b.

c.

d.

e.

f.

g.

h.

i.

12/31

2. Determine the ending balance (e.g., 12/31 balance) in each account.

144

146

123) Gathman Corporation manufactures one product. It does not maintain any beginning or

ending Work in Process inventories. The company uses a standard cost system in which

inventories are recorded at their standard costs and any variances are closed directly to Cost of

Goods Sold. There is no variable manufacturing overhead. The company’s balance sheet at the

beginning of the year was as follows:

Gathman Corporation

Balance Sheet

January 1

Assets

Cash

$

1,000,000

Raw materials inventory

27,500

Finished goods inventory

72,485

Property, plant, and equipment (net)

784,300

Total assets

$

1,884,285

Liabilities and Equity

Retained earnings

$

1,884,285

Total liabilities and equity

$

1,884,285

The standard cost card for the company’s only product is as follows:

Inputs

Standard

Quantity

or Hours

Standard Price or

Rate

Standard

Cost

Direct materials

2.5

pounds

$

5.00

per pound

$

12.50

Direct labor

0.90

hours

$

22.00

per hour

19.80

Fixed manufacturing overhead

0.90

hours

$

6.50

per hour

5.85

Total standard cost per unit

$

38.15

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing

overhead of $117,000 and budgeted activity of 18,000 hours.

147

During the year, the company completed the following transactions:

a. Purchased 36,300 pounds of raw material at a price of $4.70 per pound.

b. Used 32,100 pounds of the raw material to produce 12,800 units of work in process.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in

cash) worked 12,520 hours at an average cost of $21.00 per hour.

d. Applied fixed overhead to the 12,800 units in work in process inventory using the

predetermined overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed

overhead costs for the year were $132,700. Of this total, $27,700 related to items such as

insurance, utilities, and indirect labor salaries that were all paid in cash and $105,000 related to

depreciation of manufacturing equipment.

e. Transferred 12,800 units from work in process to finished goods.

f. Sold for cash 12,600 units to customers at a price of $52.10 per unit.

g. Completed and transferred the standard cost associated with the 12,600 units sold from

finished goods to cost of goods sold.

h. Paid $73,000 of selling and administrative expenses.

i. Closed all standard cost variances to cost of goods sold.

148

Required:

1. Compute all direct materials, direct labor, and fixed overhead variances for the year.

2. Enter the beginning balances and record the above transactions in the worksheet that appears

below. Because of the width of the worksheet, it is in two parts. In your text, these two parts would

be joined side-by-side to make one very wide worksheet.

Cash

Raw

Materials

Work in

Process

Finished

Goods

PP&E (net)

=

1/1

=

a.

=

b.

=

c.

=

d.

=

e.

=

f.

=

g.

=

h.

=

i.

=

12/31

=

=

Material

Price

Variance

Material

Quantity

Variance

Labor

Rate

Variance

Labor

Effici.

Variance

FOH

Budget

Variance

FOH

Volume

Variance

Retained

Earnings

1/1

a.

b.

c.

d.

e.

f.

g.

h.

i.

12/31

3. Determine the ending balance (e.g., 12/31 balance) in each account.

4. Prepare an income statement for the year.

149

152

153

124) Lanciotti Corporation manufactures one product. It does not maintain any beginning or

ending Work in Process inventories. The company uses a standard cost system in which

inventories are recorded at their standard costs and any variances are closed directly to Cost of

Goods Sold. There is no variable manufacturing overhead. The standard cost card for the

company’s only product is as follows:

Inputs

Standard Quantity

or Hours

Standard Price

or Rate

Standard

Cost

Direct materials

2.6

pounds

$6.50

per pound

$16.90

Direct labor

0.80

hours

$20.00

per hour

16.00

Fixed manufacturing overhead

0.80

hours

$11.50

per hour

9.20

Total standard cost per unit

$42.10

The company calculated the following variances for the year:

Materials price variance

$44,040

F

Materials quantity variance

$650

F

Labor rate variance

$52,308

U

Labor efficiency variance

$54,000

F

Fixed manufacturing overhead budget variance

$10,200

F

Fixed manufacturing overhead volume variance

$89,240

F

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing

overhead of $276,000 and budgeted activity of 24,000 hours.

During the year, the company completed the following transactions:

a. Purchased 110,100 pounds of raw material at a price of $6.10 per pound.

b. Used 103,120 pounds of the raw material to produce 39,700 units of work in process.

c. Assigned direct labor costs to work in process. The direct labor workers (who were paid in cash)

worked 29,060 hours at an average cost of $21.80 per hour.

d. Applied fixed overhead to the 39,700 units in work in process inventory using the predetermined

overhead rate multiplied by the number of direct labor-hours allowed. Actual fixed overhead costs

for the year were $265,800. Of this total, $198,800 related to items such as insurance, utilities, and

indirect labor salaries that were all paid in cash and $67,000 related to depreciation of

manufacturing equipment.

e. Transferred 39,700 units from work in process to finished goods.

f. Sold for cash 34,600 units to customers at a price of $50.90 per unit.

g. Completed and transferred the standard cost associated with the 34,600 units sold from finished

goods to cost of goods sold.

h. Paid $150,000 of selling and administrative expenses.

i. Closed all standard cost variances to cost of goods sold.

154

Required:

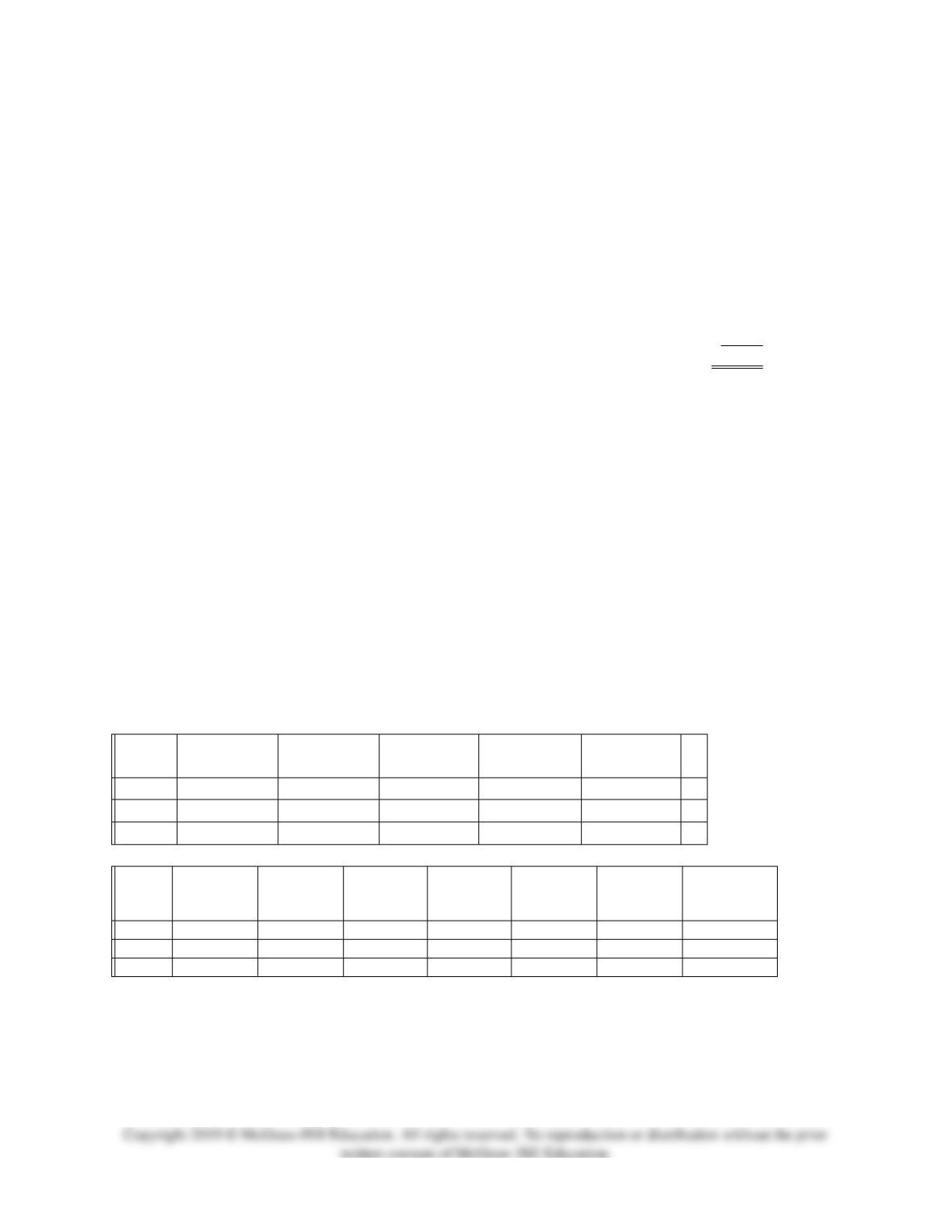

1. Record the above transactions in the worksheet that appears below. Because of the width of the

worksheet, it is in two parts. In your text, these two parts would be joined side-by-side to make one

very wide worksheet. The beginning balances have been provided for each of the accounts,

including the Property, Plant, and Equipment (net) account which is abbreviated as PP&E (net).

Cash

Raw Materials

Work in

Process

Finished

Goods

PP&E (net)

=

1/1

$1,020,000

$52,390

$0

$84,200

$538,800

=

a.

=

b.

=

c.

=

d.

=

e.

=

f.

=

g.

=

h.

=

i.

=

12/31

=

=

Materials

Price

Variance

Materials

Quantity

Variance

Labor Rate

Variance

Labor

Efficiency

Variance

FOH Budget

Variance

FOH

Volume

Variance

Retained

Earnings

1/1

$0

$0

$0

$0

$0

$0

$1,695,390

a.

b.

c.

d.

e.

f.

g.

h.

i.

12/31

2. Determine the ending balance (e.g., 12/31 balance) in each account.

3. Prepare an income statement for the year.

155

157

158

125) Herriot Corporation manufactures one product. It does not maintain any beginning or ending

Work in Process inventories. The company uses a standard cost system in which inventories are

recorded at their standard costs and any variances are closed directly to Cost of Goods Sold. There

is no variable manufacturing overhead. The standard cost card for the company’s only product is as

follows:

Inputs

Standard Quantity

or Hours

Standard Price

or Rate

Standard

Cost

Direct materials

3.7

pounds

$7.50

per pound

$27.75

Direct labor

0.90

hours

$18.50

per hour

16.65

Fixed manufacturing overhead

0.90

hours

$19.00

per hour

17.10

Total standard cost per unit

$61.50

The standard fixed manufacturing overhead rate was based on budgeted fixed manufacturing

overhead of $598,500 and budgeted activity of 31,500 hours.

During the year, the company applied fixed overhead to the 37,500 units in work in process

inventory using the predetermined overhead rate multiplied by the number of direct labor-hours

allowed. Actual fixed overhead costs for the year were $609,000. Of this total, $549,000 related to

items such as insurance, utilities, and indirect labor salaries that were all paid in cash and $60,000

related to depreciation of manufacturing equipment.

Required:

Completely record the transactions involving fixed overhead, including any variances, in the

worksheet that appears below. Because of the width of the worksheet, it is in two parts. In your

text, these two parts would be joined side-by-side to make one very wide worksheet. The

beginning balances have been provided for each of the accounts, including the Property, Plant, and

Equipment (net) account which is abbreviated as PP&E (net).

Cash

Raw

Materials

Work in

Process

Finished

Goods

PP&E (net)

=

1/1

$1,030,000

$58,275

$0

$86,100

$475,300

=

=

=

Materials

Price

Variance

Materials

Quantity

Variance

Labor Rate

Variance

Labor

Efficiency

Variance

FOH Budget

Variance

FOH Volume

Variance

Retained

Earnings

1/1

$0

$0

$0

$0

$0

$0

$1,649,675

160

126) Obenshain Corporation manufactures one product. The company uses a standard cost system

in which inventories are recorded at their standard costs. The standard cost card for the company’s

only product is as follows:

Inputs

Standard

Quantity

or Hours

Standard Price

or Rate

Standard

Cost

Direct materials

2.7

liters

$9.00

per liter

$24.30

Direct labor

0.80

hours

$21.00

per hour

16.80

Fixed manufacturing overhead

0.80

hours

$16.00

per hour

12.80

Total standard cost per unit

$53.90

During the year, direct labor workers (who were paid in cash) worked 12,880 hours at an average

cost of $20.00 per hour on 17,600 units. These units were started and completed during the year.

Required:

Completely record the direct labor costs, along with any direct labor variances, in the below

worksheet. Because of the width of the worksheet, it is in two parts. In your text, these two parts

would be joined side-by-side to make one very wide worksheet. The beginning balances have been

provided for each of the accounts, including the Property, Plant, and Equipment (net) account

which is abbreviated as PP&E (net).

Cash

Raw

Materials

Work in

Process

Finished

Goods

PP&E (net)

=

1/1

$1,010,000

$34,020

$0

$48,510

$721,000

=

=

=

Materials

Price

Variance

Materials

Quantity

Variance

Labor Rate

Variance

Labor

Efficiency

Variance

FOH Budget

Variance

FOH

Volume

Variance

Retained

Earnings

1/1

$0

$0

$0

$0

$0

$0

$1,813,530