1. Fixed costs should not be included in a performance report because fixed costs are not

controllable.

2. A flexible budget can be used to determine what costs should have been at a given level of

activity.

3. If activity is higher than expected, total variable costs should be higher than expected. If

activity is lower than expected, total variable costs should be lower than expected.

4. When a flexible budget is used in performance evaluation, actual costs are compared to

what the costs should have been for the actual level of activity during the period rather than to the

static planning budget.

5. An activity variance is due solely to the difference between the level of activity assumed in

the planning budget and the actual level of activity used in the flexible budget.

6. The activity variance for revenue is favorable if the actual level of activity for the period

exceeds the planned level of activity.

7. The activity variance for revenue is unfavorable if the revenue in the flexible budget is less

than the revenue in the static planning budget.

8. The revenue and spending variances are the differences between the static planning

budget and the actual results for the period.

9. A revenue variance is favorable if the revenue in the static planning budget exceeds the

revenue in the flexible budget.

10. A spending variance is the difference between how much a cost should have been, given

the actual level of activity, and the actual amount of the cost for the period.

11. A favorable spending variance occurs when the actual cost exceeds the amount of that

cost in the flexible budget.

12. A flexible budget performance report contains both activity variances and revenue and

spending variances.

13. While fixed costs should not be affected by a change in the level of activity within the

relevant range, they may change for other reasons.

14. Flexible budgets cannot be used when there is more than one cost driver (i.e., measure of

activity).

15. Directly comparing static budget costs to actual costs only makes sense if the costs are

fixed.

16. If the actual level of activity is 4% more than planned, then the variable costs in the static

budget should be increased by 4% before comparing them to actual costs.

17. The purpose of a flexible budget is to:

18. A static budget:

19. Which of the following comparisons best isolates the impact of a change in activity on

performance?

20. Which of the following would not appear on a flexible budget performance report as

shown in the text?

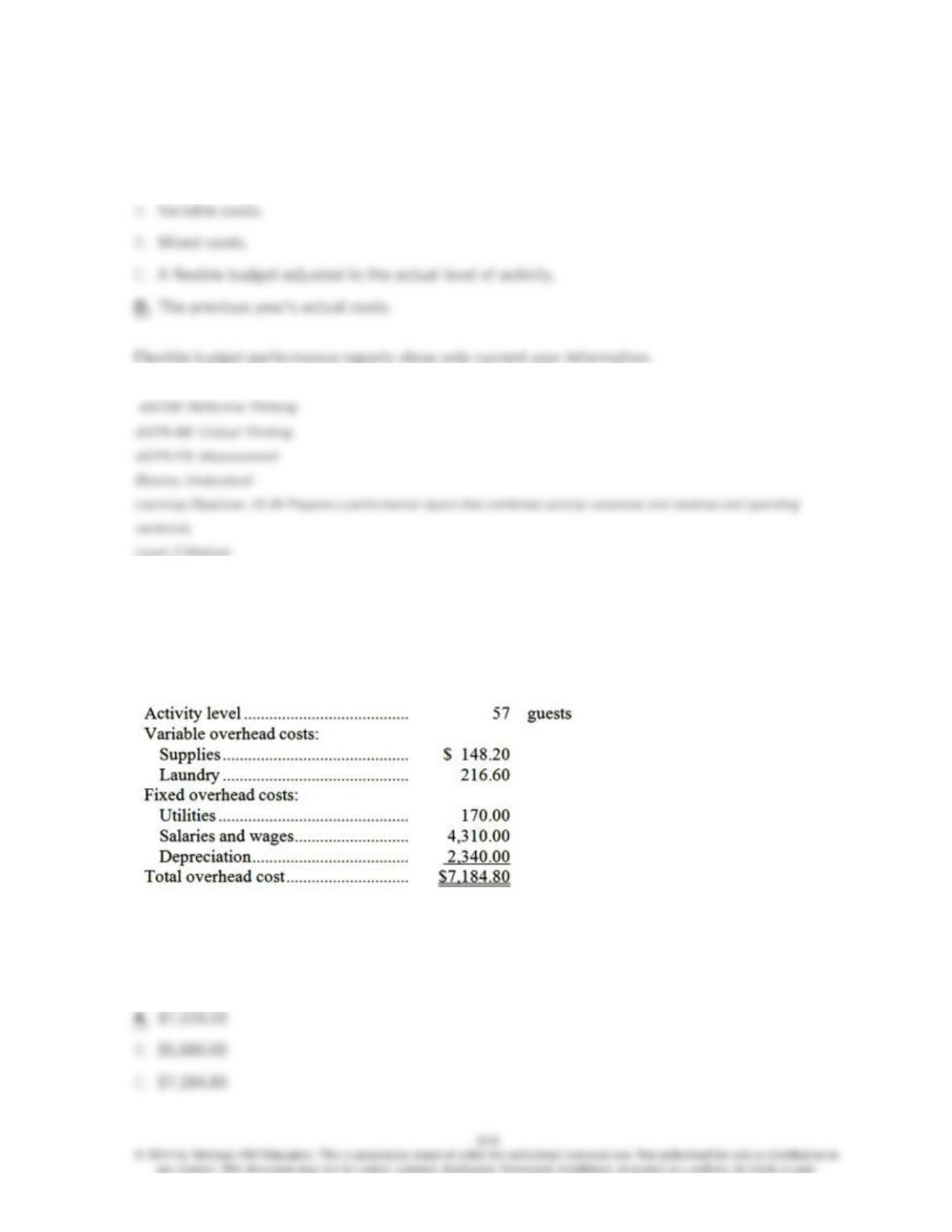

21. Salyers Family Inn is a bed and breakfast establishment in a converted 100-year-old

mansion. The Inn’s guests appreciate its gourmet breakfasts and individually decorated rooms.

The Inn’s overhead budget for the most recent month appears below:

The Inn’s variable overhead costs are driven by the number of guests.

What would be the total budgeted overhead cost for a month if the activity level is 53 guests?

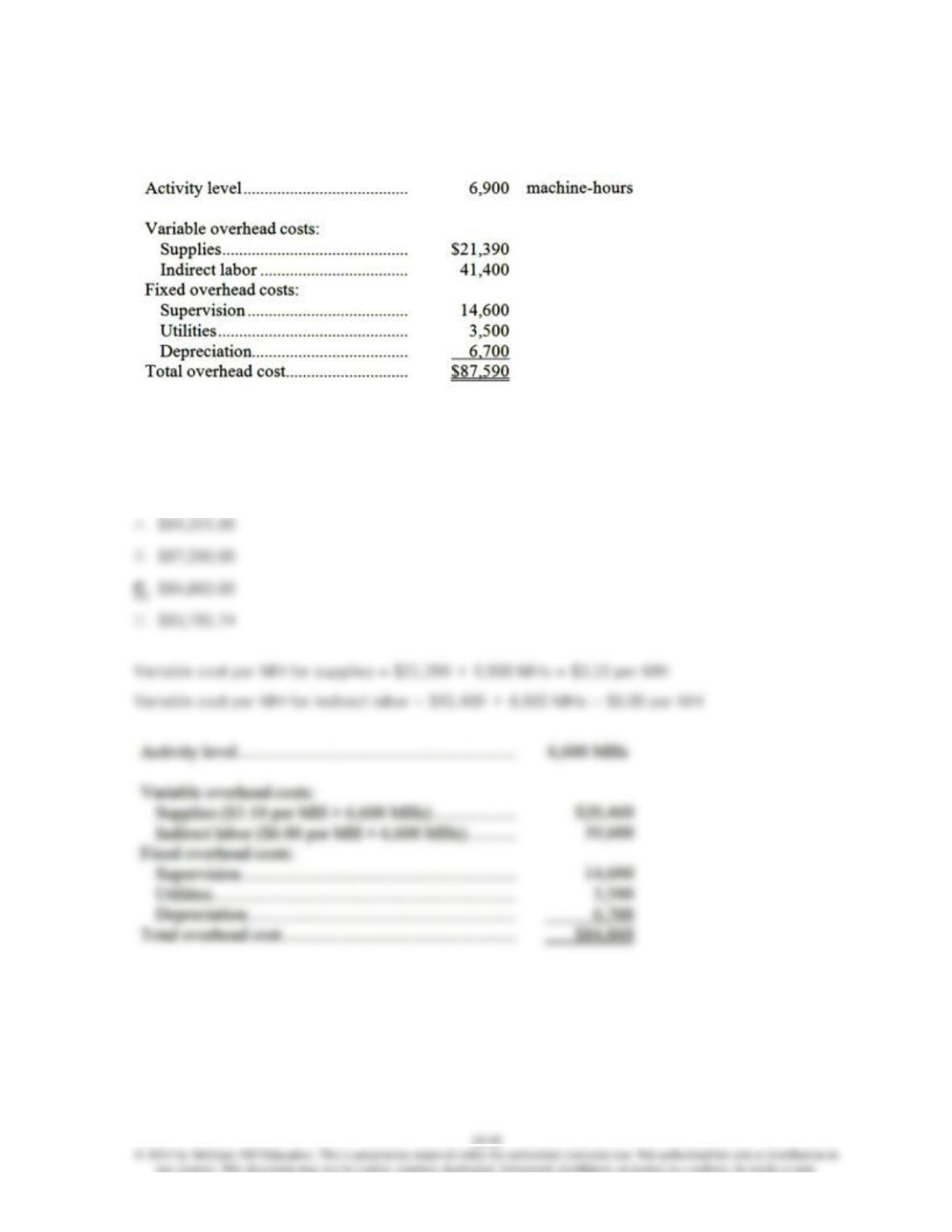

22. Stock Manufacturing Corporation has prepared the following overhead budget for next

month.

The company’s variable overhead costs are driven by machine-hours.

What would be the total budgeted overhead cost for next month if the activity level is 6,600

machine-hours rather than 6,900 machine-hours?

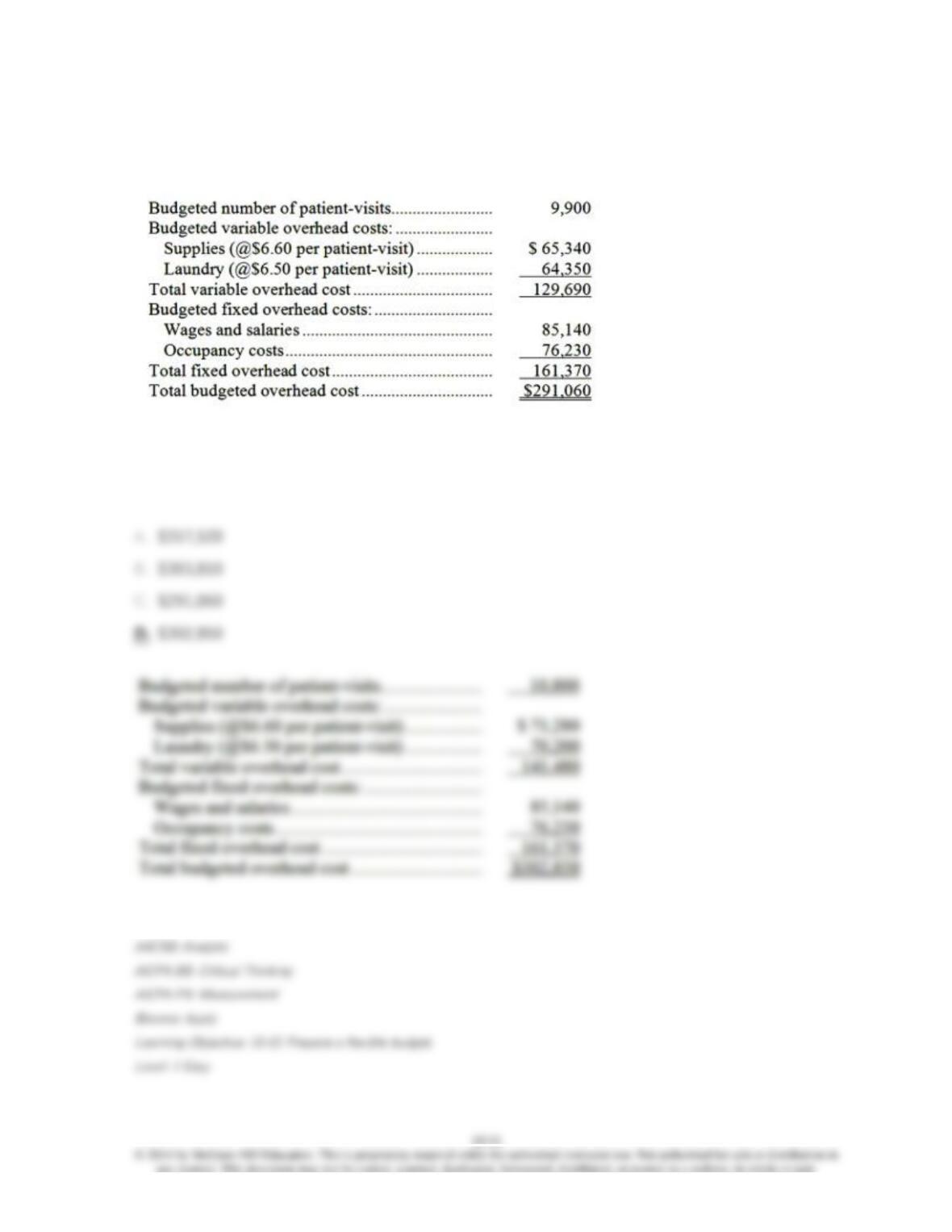

23. Gummer Hospital bases its budgets on patient-visits. The hospital’s static budget for

February appears below:

The total overhead cost at an activity level of 10,800 patient-visits per month should be:

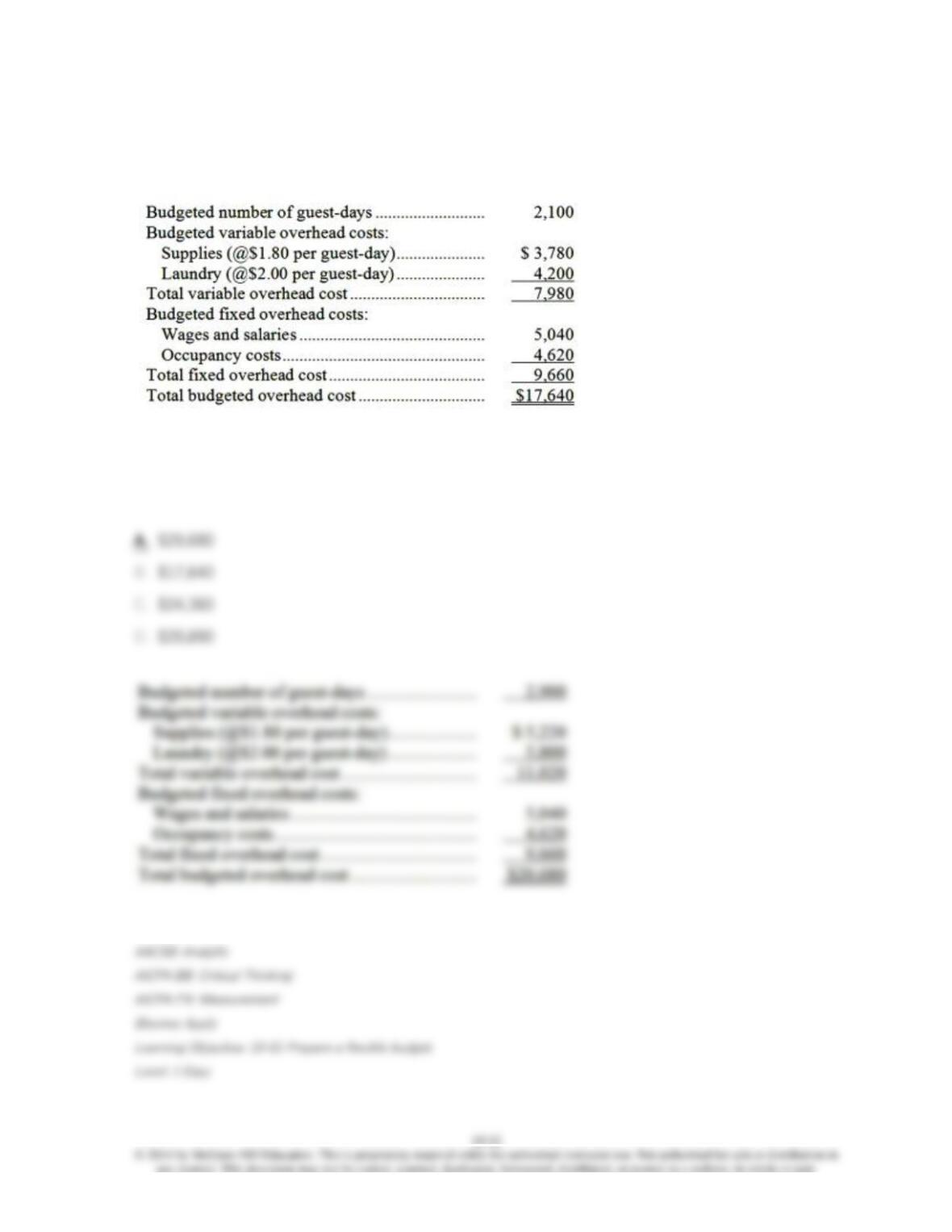

24. Scarfo Hotel bases its budgets on guest-days. The hotel’s static budget for December

appears below:

The total overhead cost at an activity level of 2,900 guest-days per month should be:

25. Wadhams Snow Removal’s cost formula for its vehicle operating cost is $1,900 per month

plus $430 per snow-day. For the month of December, the company planned for activity of 16

snow-days, but the actual level of activity was 21 snow-days. The actual vehicle operating cost for

the month was $11,470. The vehicle operating cost in the planning budget for December would be

closest to:

26. Petersheim Snow Removal’s cost formula for its vehicle operating cost is $1,750 per

month plus $484 per snow-day. For the month of November, the company planned for activity of

15 snow-days, but the actual level of activity was 14 snow-days. The actual vehicle operating cost

for the month was $8,360. The vehicle operating cost in the flexible budget for November would

be closest to:

27. Oscarson Midwifery’s cost formula for its wages and salaries is $2,720 per month plus

$351 per birth. For the month of September, the company planned for activity of 121 births, but

the actual level of activity was 119 births. The actual wages and salaries for the month was

$43,380. The wages and salaries in the planning budget for September would be closest to:

28. Clovis Midwifery’s cost formula for its wages and salaries is $2,680 per month plus $245

per birth. For the month of September, the company planned for activity of 118 births, but the

actual level of activity was 121 births. The actual wages and salaries for the month was $33,290.

The wages and salaries in the flexible budget for September would be closest to:

29. Gradert Framing’s cost formula for its supplies cost is $1,540 per month plus $12 per

frame. For the month of September, the company planned for activity of 668 frames, but the

actual level of activity was 666 frames. The actual supplies cost for the month was $9,980. The

supplies cost in the planning budget for September would be closest to:

30. Bargas Framing’s cost formula for its supplies cost is $2,240 per month plus $6 per frame.

For the month of May, the company planned for activity of 808 frames, but the actual level of

activity was 810 frames. The actual supplies cost for the month was $7,090. The supplies cost in

the flexible budget for May would be closest to:

31. Stuchlik Catering uses two measures of activity, jobs and meals, in the cost formulas in its

budgets and performance reports. The cost formula for catering supplies is $430 per month plus

$80 per job plus $14 per meal. A typical job involves serving a number of meals to guests at a

corporate function or at a host’s home. The company expected its activity in January to be 20 jobs

and 190 meals, but the actual activity was 21 jobs and 194 meals. The actual cost for catering

supplies in January was $4,850. The catering supplies in the planning budget for January would be

closest to:

32. Whit Catering uses two measures of activity, jobs and meals, in the cost formulas in its

budgets and performance reports. The cost formula for catering supplies is $380 per month plus

$94 per job plus $11 per meal. A typical job involves serving a number of meals to guests at a

corporate function or at a host’s home. The company expected its activity in October to be 20 jobs

and 216 meals, but the actual activity was 19 jobs and 221 meals. The actual cost for catering

supplies in October was $4,790. The catering supplies in the flexible budget for October would be

closest to: