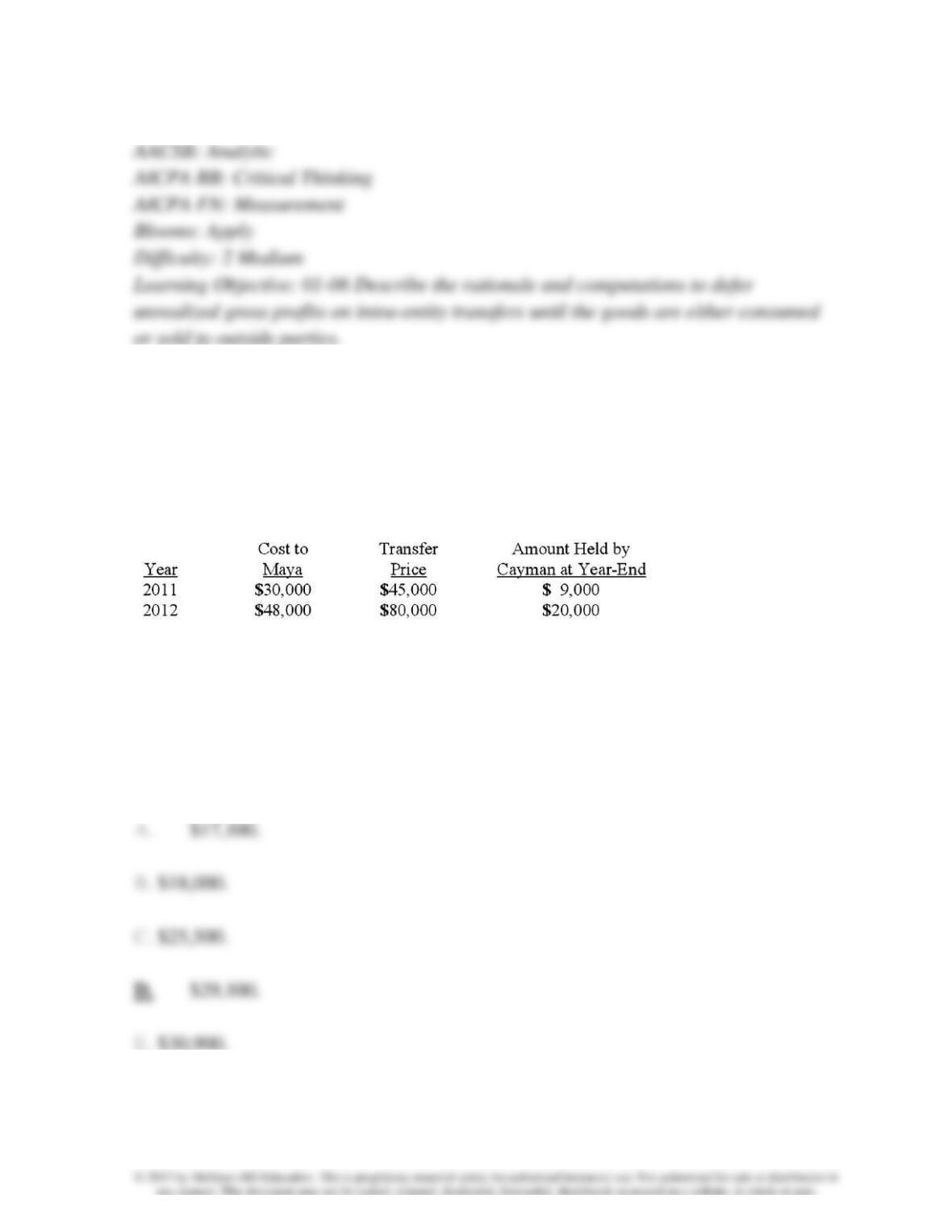

79. Cayman Inc. bought 30% of Maya Company on January 1, 2011 for $450,000.

The equity method of accounting was used. The book value and fair value of the net

assets of Maya on that date were $1,500,000. Maya began supplying inventory to

Cayman as follows:

Maya reported net income of $100,000 in 2011 and $120,000 in 2012 while paying

$40,000 in dividends each year.

What is the Equity in Maya Income that should be reported by Cayman in 2011?

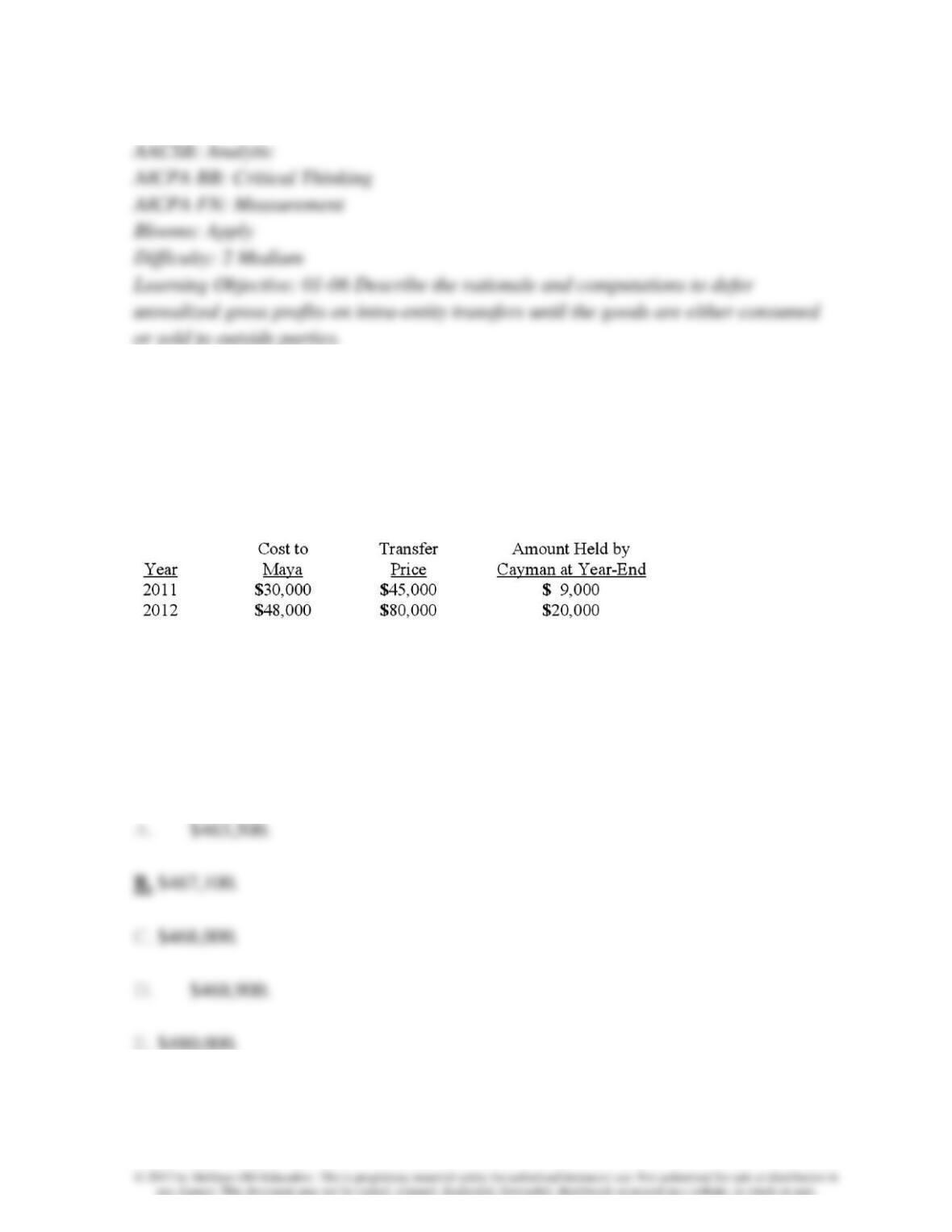

80. Cayman Inc. bought 30% of Maya Company on January 1, 2011 for $450,000.

The equity method of accounting was used. The book value and fair value of the net

assets of Maya on that date were $1,500,000. Maya began supplying inventory to

Cayman as follows:

Maya reported net income of $100,000 in 2011 and $120,000 in 2012 while paying

$40,000 in dividends each year.

What is the balance in Cayman‘s Investment in Maya account at December 31, 2011?

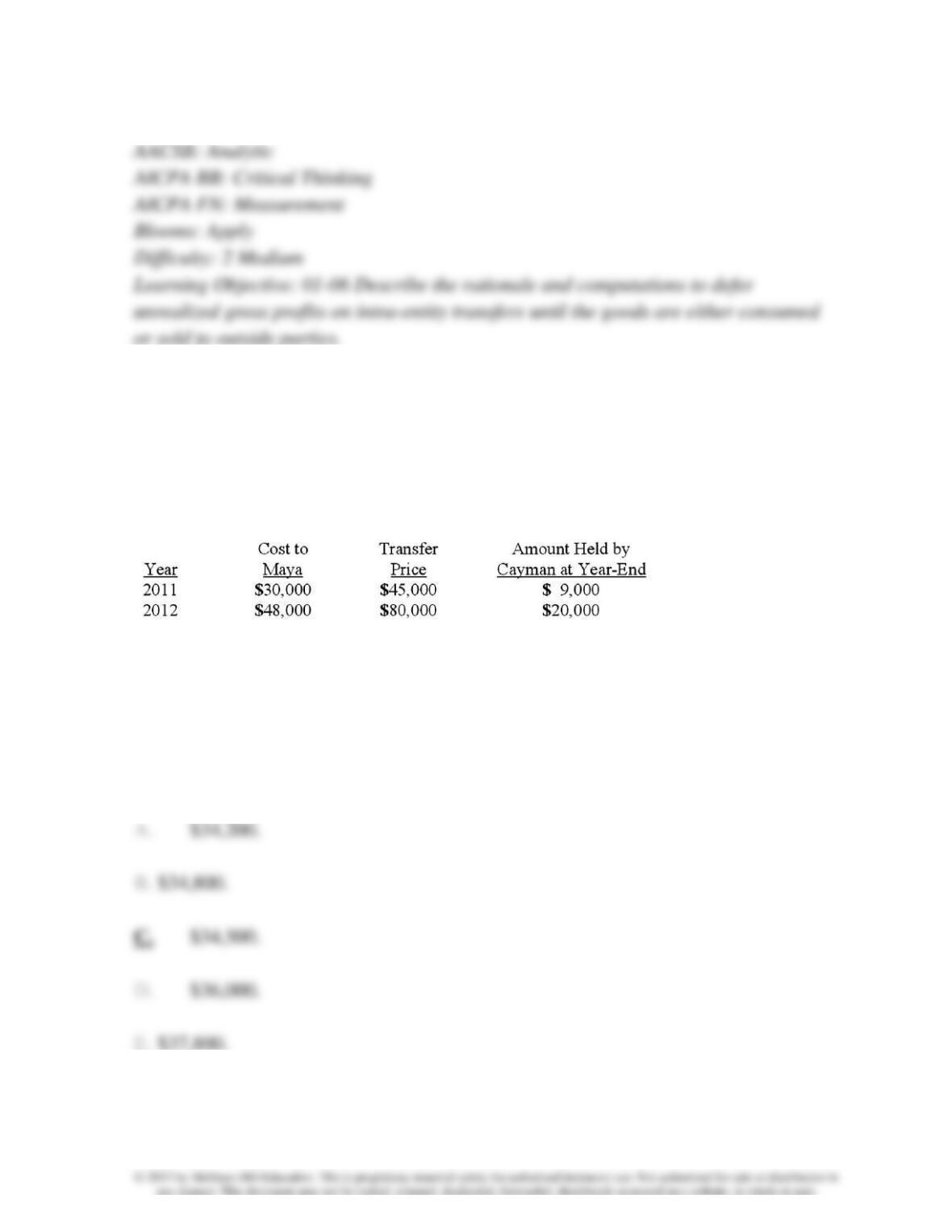

81. Cayman Inc. bought 30% of Maya Company on January 1, 2011 for $450,000.

The equity method of accounting was used. The book value and fair value of the net

assets of Maya on that date were $1,500,000. Maya began supplying inventory to

Cayman as follows:

Maya reported net income of $100,000 in 2011 and $120,000 in 2012 while paying

$40,000 in dividends each year.

What is the Equity in Maya Income that should be reported by Cayman in 2012?

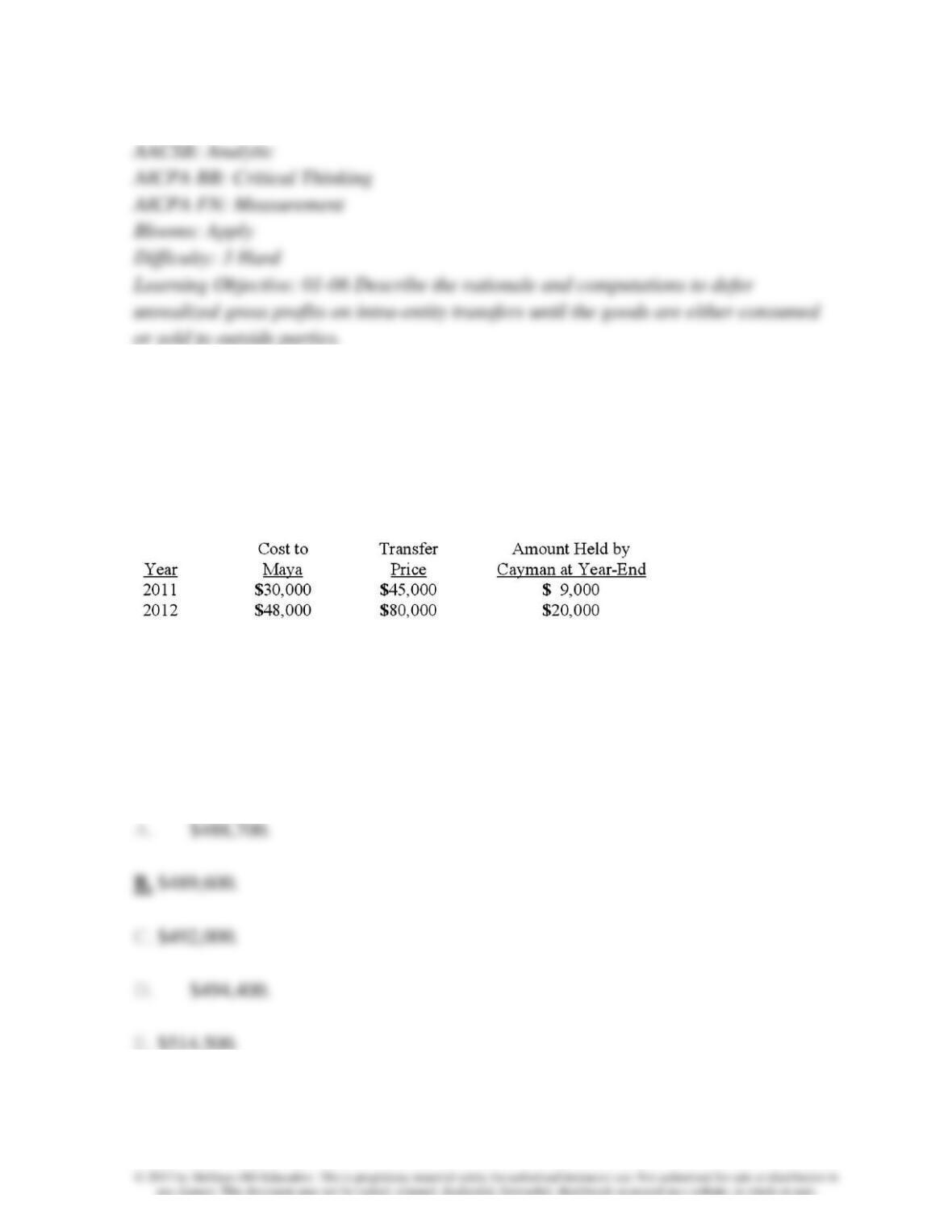

82. Cayman Inc. bought 30% of Maya Company on January 1, 2011 for $450,000.

The equity method of accounting was used. The book value and fair value of the net

assets of Maya on that date were $1,500,000. Maya began supplying inventory to

Cayman as follows:

Maya reported net income of $100,000 in 2011 and $120,000 in 2012 while paying

$40,000 in dividends each year.

What is the balance in Cayman‘s Investment in Maya account at December 31, 2012?

83. Which of the following results in a decrease in the investment account when

applying the equity method?

84. Which of the following results in an increase in the investment account when

applying the equity method?

85. Which of the following results in a decrease in the Equity in Investee Income

account when applying the equity method?

86. Which of the following results in an increase in the Equity in Investee Income

account when applying the equity method?

87. Renfroe, Inc. acquires 10% of Stanley Corporation on January 1, 2010, for

$90,000 when the book value of Stanley was $1,000,000. During 2010, Stanley

reported net income of $215,000 and paid dividends of $50,000. On January 1, 2011,

Renfroe purchased an additional 30% of Stanley for $325,000. Any excess of cost over

book value is attributable to goodwill with an indefinite life. During 2011, Renfroe

reported net income of $320,000 and paid dividends of $50,000.

How much is the adjustment to the Investment in Stanley Corporation for the change

from the fair-value method to the equity method on January 1, 2011?

88. Renfroe, Inc. acquires 10% of Stanley Corporation on January 1, 2010, for

$90,000 when the book value of Stanley was $1,000,000. During 2010, Stanley

reported net income of $215,000 and paid dividends of $50,000. On January 1, 2011,

Renfroe purchased an additional 30% of Stanley for $325,000. Any excess of cost over

book value is attributable to goodwill with an indefinite life. During 2011, Renfroe

reported net income of $320,000 and paid dividends of $50,000.

What is the balance in the Investment in Stanley Corporation on December 31, 2011?

89. On January 4, 2010, Trycker, Inc. acquired 40% of the outstanding common

stock of Inkblot Co. for $2,400,000. This investment gave Trycker the ability to

exercise significant influence over Inkblot. Inkblot’s assets on that date were recorded

at $8,000,000 with liabilities of $2,000,000. There were no other differences between

book and fair values.

During 2010, Inkblot reported net income of $500,000 and paid dividends of

$300,000. The fair value of Inkblot at December 31, 2010 is $7,000,000. Trycker

elects the fair value option for its investment in Inkblot.

How are dividends received from Inkblot reflected in Trycker’s accounting records for

2010?

90. On January 4, 2010, Trycker, Inc. acquired 40% of the outstanding common

stock of Inkblot Co. for $2,400,000. This investment gave Trycker the ability to

exercise significant influence over Inkblot. Inkblot’s assets on that date were recorded

at $8,000,000 with liabilities of $2,000,000. There were no other differences between

book and fair values.

During 2010, Inkblot reported net income of $500,000 and paid dividends of

$300,000. The fair value of Inkblot at December 31, 2010 is $7,000,000. Trycker

elects the fair value option for its investment in Inkblot.

At what amount will Inkblot be reflected in Trycker’s December 31, 2010 balance

sheet?

91. For each of the following numbered situations below, select the best letter

answer concerning accounting for investments:

(A.) Increase the investment account.

(B.) Decrease the investment account.

(C.) Increase dividend revenue.

(D.) No adjustment necessary.

(1.) Income reported by 40% owned investee.

(2.) Income reported by 10% owned investee.

(3.) Loss reported by 40% owned investee.

(4.) Loss reported by 10% investee.

(5.) Change from fair-value method to equity method. Prior income exceeded

dividends.

(6.) Change from fair-value method to equity method. Prior income was less than

dividends.

(7.) Change from equity method to fair-value method. Prior income exceeded

dividends.

(8.) Change from equity method to fair-value method. Prior income was less than

dividends.

(9.) Dividends received from 40% investee.

(10.) Dividends received from 10% investee.

(11.) Purchase of additional shares of investee.

(12.) Unrealized ending intra-entity inventory profits using the equity method.

92. Jarmon Company owns twenty-three percent of the voting common stock of

Kaleski Corp. Jarmon does not have the ability to exercise significant influence over

the operations of Kaleski. What method should Jarmon use to account for its

investment in Kaleski?

93. Idler Co. has an investment in Cowl Corp. for which it uses the equity method.

Cowl has suffered large losses for several years, and the balance in the investment

account has been reduced to zero. How should Idler account for this investment?

94. Which types of transactions, exchanges, or events would indicate that an

investor has the ability to exercise significant influence over the operations of an

investee?

95. You are auditing a company that owns twenty percent of the voting common

stock of another corporation and uses the equity method to account for the investment.

How would you verify that the equity method is appropriate in this case?

96. How does the use of the equity method affect the investor’s financial

statements?

97. What is the primary objective of the equity method of accounting for an

investment?

98. What is the justification for the timing of recognition of income under the

equity method?