Name:

Class:

Date:

chapter 1

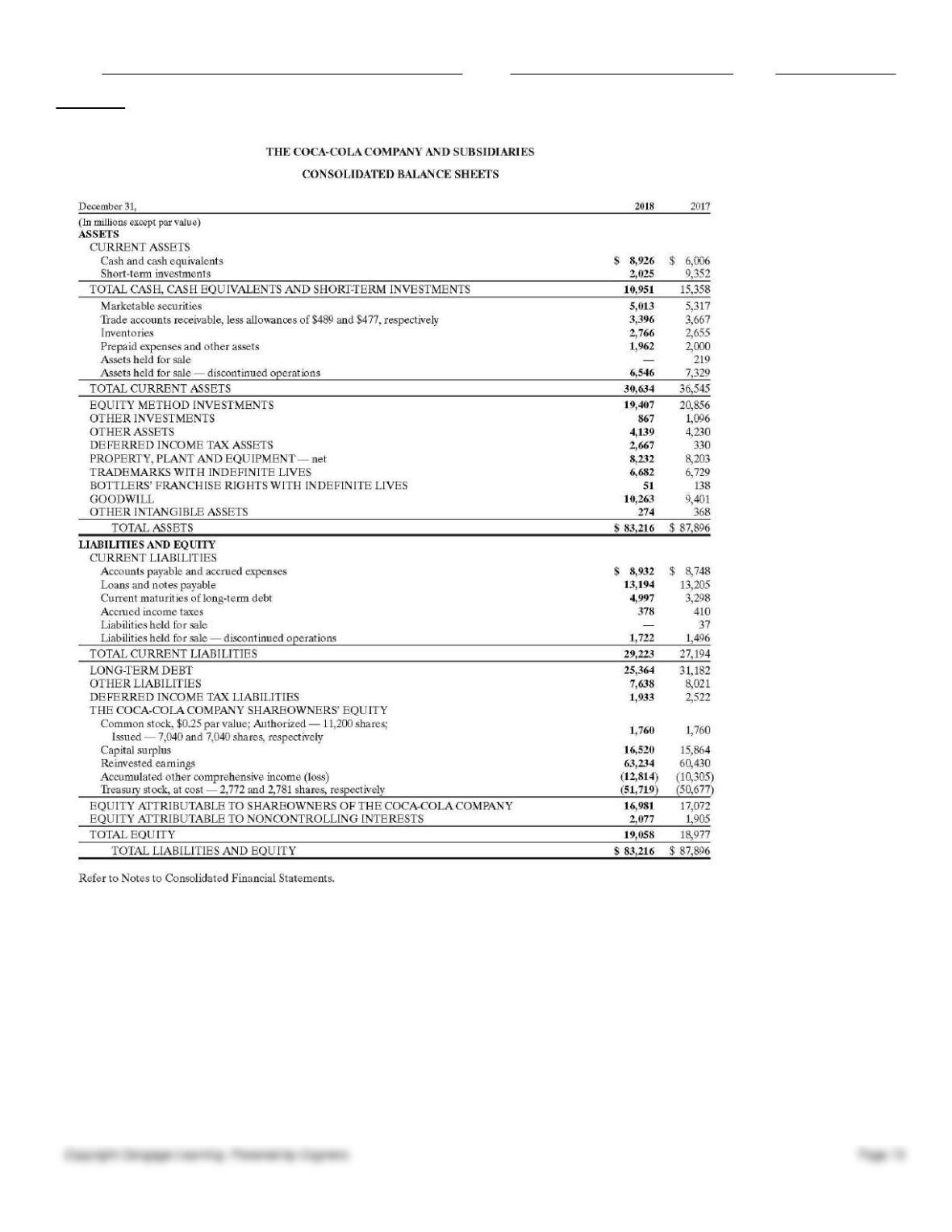

88. Review Coca-Cola’s financial statements and answer the following questions:

(1) What is Coke’s percent of current assets to total assets on its December 31, 2018 balance sheet?

(2) What is Coke’s percentage of current liabilities to total stockholders’ equity on its December 31, 2018, balance

sheet?

(3) What is the percentage increase in cash and cash equivalents from 2017 to 2018?

(4) What percentage did total assets decrease from 2017 to 2018?

Name:

Class:

Date:

chapter 1

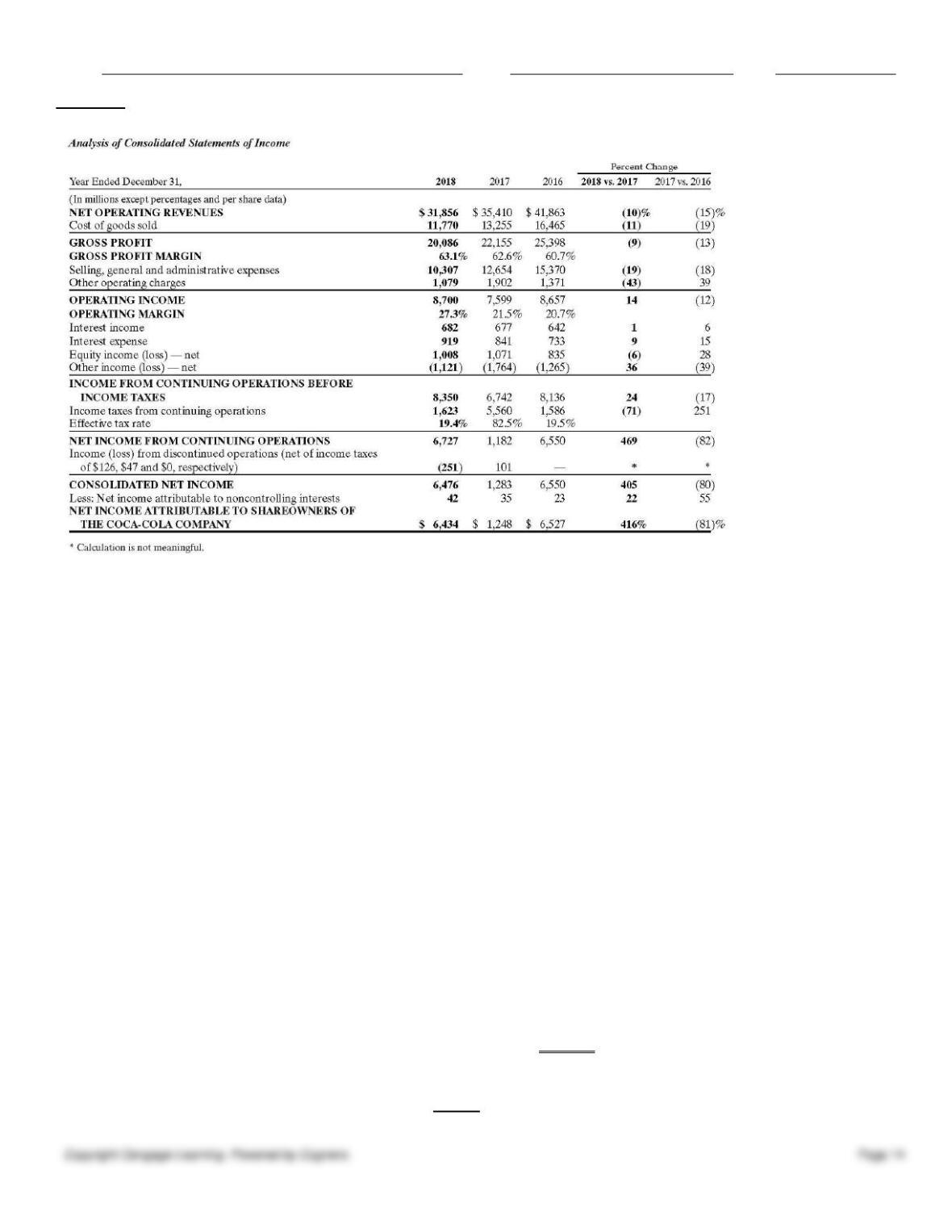

89. Review Coca-Cola’s financial statements and answer the following questions:

(1) How are Coke’s numbers reported (in what denomination)?

(2) What is Coke’s net operating revenue for 2018?

(3) What is Coke’s cost of goods sold for 2018?

(4) What is Coke’s net income for 2018?

(5) What is Coke’s percent of interest expense to net operating revenue on its 2018 income statement?

(6) What is Coke’s percent of increase in net operating revenue from 2017 to 2018?

90. Name and describe the three forms of businesses and their advantages and disadvantages (if any).

91. Fill in the missing amounts of the following balance sheet.

Prova Company

Balance Sheet

December 31, 20Y8

Assets

Cash $ 3,300

Accounts Receivable 2,400

Supplies (a)

Inventory 5,700

Equipment 7,400

Land 9,250

Total Assets $32,550

Liabilities

Accounts Payable $ 850

Notes Payable (b)

Total Liabilities $ (c)

Name:

Class:

Date:

chapter 1

Stockholders’ Equity

Common Stock $18,500

Retained Earnings 4,200

Total Stockholders’ Equity 22,700

Total Liabilities and Stockholders’ Equity $ (d)

92. What is the basic accounting equation, and which financial statement is prepared from this equation?

93. The following are the financial statement data for Degen Temporary Services at December 31, 20Y8. Prepare Degen’s

income statement.

Accounts Payable $ 850

Accounts Receivable 780

Cash 425

Common Stock 600

Dividends 200

Insurance Expense 75

Office Equipment 1,500

Retained Earnings, January 1, 20Y8 370

Salaries Expense 525

Notes Payable 40

Service Revenue 1,750

Inventory 35

Supplies Expense 50

Degen Temporary Services

Income Statement

For the Year Ended December 31, 20Y8

94. For each of the following companies, identify whether it is a service, merchandising, or manufacturing business.

A. Dillards

B. Time Warner Cable

C. Kohl’s

D. Ford Motor Co.

E. Applebee’s

Name:

Class:

Date:

chapter 1

G. Best Buy

H. GAP

I. H & R Block

95. How do businesses make money? What strategies can they use to gain a competitive advantage?

96. Match the following items with the appropriate financial statement.

a. Income statement

b. Balance sheet

c. Retained earnings statement

d. Statement of cash flows

(1) Cash

(2) Salary expense

(3) Unearned revenue

(4) Depreciation expense

(5) Capital stock

(6) Cash flows from operating activities

(7) Accounts receivable

(8) Beginning balance of retained earnings

(9) Notes payable

(10) Accounts payable

(11) Changes in current assets and current liabilities

(12) Total expenses

97. Indicate whether each of the following activities would be reported on the statement of cash flows as an operating

activity, an investing activity, a financing activity, or does not appear on the statement of cash flows.

(a) Cash paid for building

(b) Cash paid to suppliers

(c) Cash paid for dividends

(d) Cash received from customers

(e) Cash received from the sale of capital stock

(f) Cash received from the sale of a building

(g) Borrowed cash from a bank

98. Describe business stakeholders. State the classification of business stakeholders.

99. Classify the following as an asset, liability, revenue, or expense.

(1) Unearned revenue

(2) Office equipment

(3) Wages payable

(4) Salary expense

(5) Dividends payable

(6) Art fees earned

(7) Prepaid rent

(8) Accounts receivable

(9) Income tax expense

(10) Office supplies

Name:

Class:

Date:

chapter 1

100. On May 31, 20X8, Deana’s Services Company had account balances as follows:

Accounts payable $ 9,900

Accounts receivable 26,950

Cash 11,390

Fees earned 70,800

Insurance expense 1,475

Land 74,400

Miscellaneous expense 1,510

Prepaid insurance 2,000

Rent expense 8,000

Salary expense 35,300

Dividends 15,100

Supplies 950

Supplies expense 825

Utilities expense 3,800

Capital stock 81,000

Retained earnings (beginning balance on May 1, 20Y8) 20,000

Present, in good form, (a) an income statement for May, (b) a statement of shareholders’ equity for May, and (c) a balance

sheet as of May 31.

101. Match each statement with the appropriate accounting concept. (Some items may not be used. Others may be used

more than once.)

a. Accounting period concept

b. Adequate disclosure concept

c. Business entity concept

d. Cost concept

e. Going concern concept

f. Matching concept

g. Objectivity concept

h. Unit of measure concept

(1) Owners’ transactions are separate from business transactions.

(2) Financial statements are prepared at the end of each year.

(3) Land purchased for $50,000, 10 years ago, is reported on the Balance Sheet at $50,000.

(4) December rent expense paid in January is reported with the December revenues.

(5) All transactions are recorded and reported in dollars.

(6) This provides a summary of significant accounting policies.

(7) This assumes that IBM will continue as a corporation forever.

(8) The length of time left on debt obligations is shown.

Name:

Class:

Date:

chapter 1

Answer Key

Name:

Class:

Date:

chapter 1

Name:

Class:

Date:

chapter 1

Name:

Class:

Date:

chapter 1

Name:

Class:

Date:

Name:

Class:

Date:

chapter 1

Name:

Class:

Date:

chapter 1