1) The purpose of phase 3 in the “process for understanding internal control and

assessing control risk” is to:

A) design, perform and evaluate tests of controls

B) obtain and document an understanding of internal control design an operation

C) assess control risk

D) decide planned detection risk and substantive tests

2) After a purchase requisition is approved, a ________ must be initiated to purchase

the goods or services.

A) purchase order

B) vendor order

C) call order

D) vendor invoice

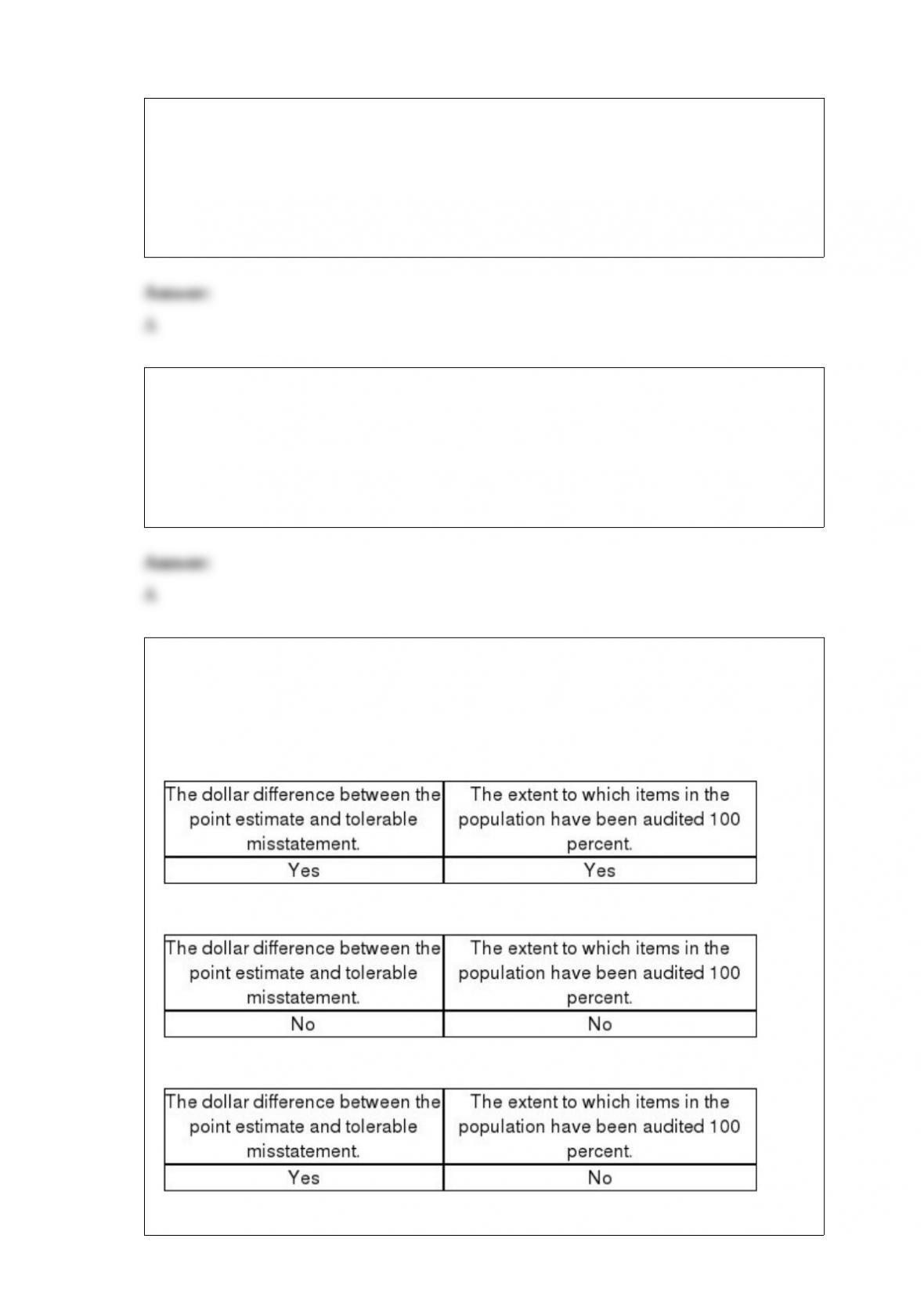

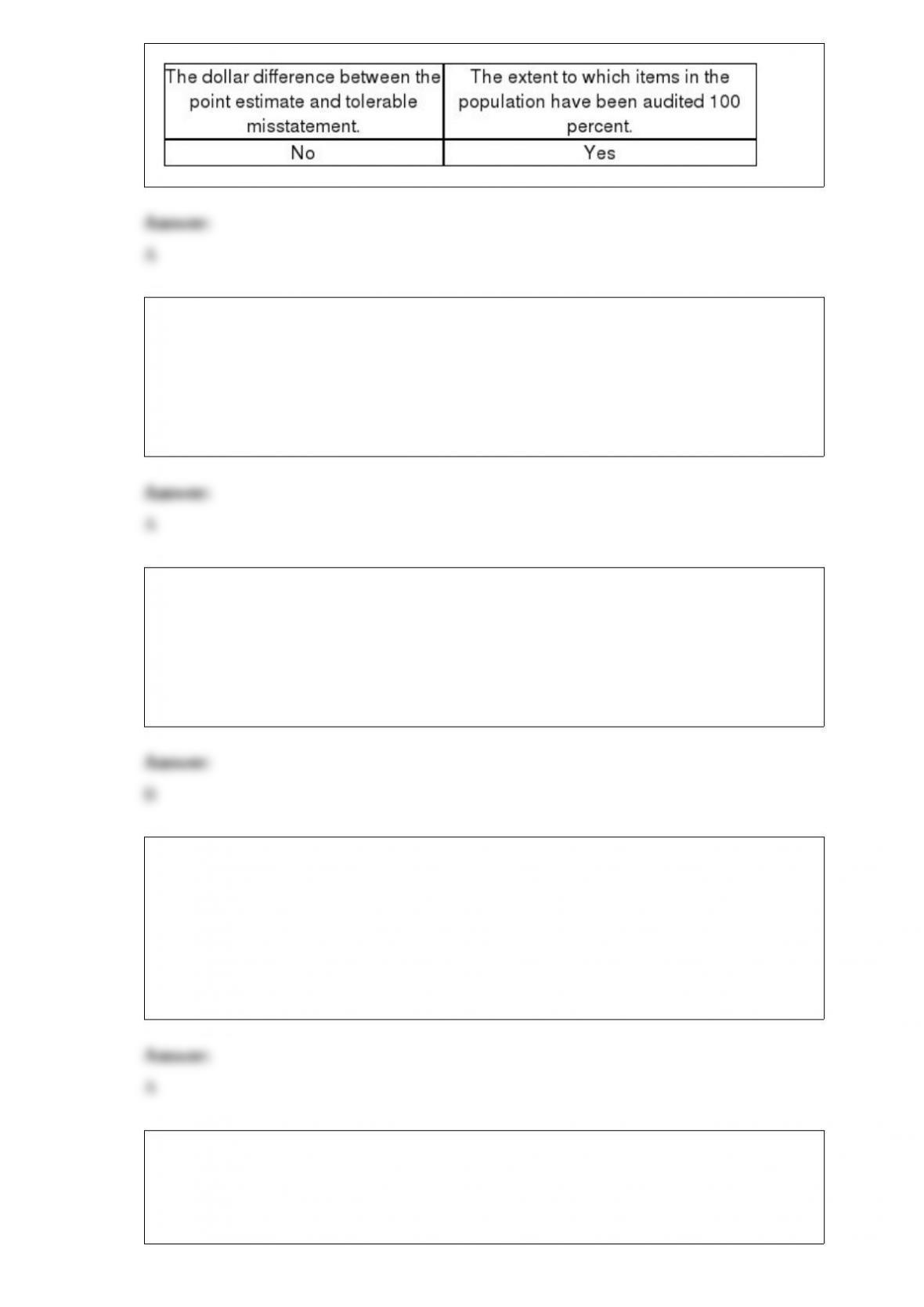

3) An auditor using nonstatistical sampling cannot formally measure sampling error and

therefore must subjectively consider the possibility that the true population

misstatement exceeds a tolerable amount. Which of the following factors should be

considered by the auditor in making this assessment?

A)

B)

C)

D)

4) Which one of the following best describes the auditors responsibilities regarding

appropriate authorizations in the sales/collections cycle?

A) B, C, and D should all be of concern to the auditor

B) Credit must be authorized before the sale

C) Goods must be shipped after the authorization

D) Prices must be authorized

5) Auditor tests of the physical controls over raw materials, work in process, and

finished goods are generally limited to:

A) observation and confirmation

B) observation and inquiry

C) inquiry and reconciliation

D) observation and reconciliation

6) Non-probabilistic selection methods are not based on mathematical probabilities;

therefore:

A) the extent to which a sample is representative of the population may be difficult to

determine

B) they are discouraged by the

C) they are not allowed by the Statements on Auditing Standards

D) they are not as effective as statistical sampling

7) A written purchase order is a contractual document that is:

A) an offer to buy

B) not enforceable if it is not in writing

C) a binding agreement between purchaser and vendor

D) an acceptance of a vendor’s catalog offer to sell

8) The main difference between job order and process costing systems is that:

A) one accumulates costs by materials issued and the other by labor incurred

B) one accumulates costs by individual jobs and the other by particular processes

C) one emphasizes costs accumulated in completed products and the other emphasizes

costs associated with work-in-process

D) one emphasizes costs adding value to the product and the other emphasizes costs

incurred because of waste, scrap, and obsolescence

9) The document used to indicate to the customer the amount of a sale and payment due

date is the:

A) sales invoice

B) bill of lading

C) purchase order

D) sales order

10) Which of the following statements regarding types of operational audits is likely

incorrect?

A) A functional audit has the advantage of permitting specialization by auditors

B) An advantage of functional auditing is its ability to evaluate interrelated functions

C) The emphasis in an organizational audit is on how efficiently and effectively

functions interact

D) Special operational auditing assignments arise at the request of management

11) Negative assurance is not permissible in:

A) reports based upon a review engagement

B) letters required by security underwriters for data pertinent to SEC registration

statements

C) reports based on an audit of interim financial statements of a closely held business

entity

D) reports relating to the results of agreed-upon procedures to one or more specified

elements, accounts, or items of financial statement

12) Which of the following statements is most correct concerning audit risk?

A) Audit risk can be quantified with a reasonable degree of certainty

B) Audit risk cannot be quantified with certainty

C) Audit risk is the same for all audit client in the same industry

D) Audit risk can be eliminated by having the correct audit procedures

13) The payroll and personnel cycle begins with which of the following events?

A) interviewing job candidates

B) hiring a new employee

C) existing employees submitting requests for payment for work performed

D) issuance of paychecks

14) Auditors are required to evaluate the going concern assumption as part of each

audit.

A) True

B) False

15) As a client’s information system becomes more complex, it is likely that an auditor

will increase reliance on controls and decrease substantive tests to support a control risk

assessment.

A) True

B) False

16) A) True

B) False

17) The audit procedure referred to as proof of cash receipts is particularly useful to

test:

A) time lags in making deposits

B) whether all recorded cash receipts have been deposited in the bank

C) whether there are cash receipts that have not been recorded in the journals

D) the client’s reconciliation between cash receipts and bank deposits

18) Monetary-unit sampling is not particularly effective at detecting:

A) overstatements

B) understatements

C) errors in current assets

D) errors in noncurrent assets

19) The WebTrust service requires that a CPA update its testing of the e-commerce

aspects of a entity’s Web site at least every:

A) ninety days

B) month

C) six months

D) twelve months

20) Oehlers, CPA, is a staff auditor participating in the engagement of Capital Trust,

Inc. Which of the following circumstances impairs Oehlers independence?

A) Oehlers sister is an internal auditor employed part-time by Capital Trust

B) Oehlers friend, and employee of another local accounting firm, prepares the tax

return of Capital Trust’s CEO

C) Oehlers and Capital Trust’s 401K plan own stock with the same corporation

D) During the period of professional engagement, Capital Trust gave Oehlers tickets to

a football game worth $75

21) You are performing an audit of Hawk Company. In evaluating the accounts payable

balance you are concerned with the completeness assertion. Which of the following

audit procedures best satisfy your concern?

A) send confirmations to only vendors with large balances

B) send confirmations to vendors with large, active, zero balance accounts and a

representative sample of all others

C) send confirmations to vendors chosen from sample stratified by the dollar balance

D) send confirmations to all vendors

22) The responsibility for the preparation of the financial statements and the

accompanying footnotes belongs to:

A) the auditor

B) management

C) both management and the auditor equally

D) management for the statements and the auditor for the notes

23) In auditing payroll, which of the following procedures will normally require the

least amount of auditor time under normal circumstances?

A) Tests of controls

B) Substantive tests of transactions

C) Analytical procedures

D) Tests of details of balances

24) An auditor who is testing IT controls in a payroll system would most likely use test

data that contain conditions such as:

A) time tickets with invalid job numbers

B) overtime not approved by supervisors

C) deductions not authorized by employees

D) payroll checks with unauthorized signatures

25) The only parties who can recover from auditors under the Securities Act of 1933 are

original purchasers of securities.

A) True

B) False

26) A control that relates to all parts of the IT system is called a(n):

A) general control

B) systems control

C) universal control

D) applications control

27) In job cost systems, costs are accumulated by individual jobs.

A) True

B) False

28) Inherent risk and control risk:

A) are inversely related to each other

B) are inversely related to detection risk

C) are directly related to detection risk

D) are directly related to audit risk

29) Which of the following is not an application control?

A) preprocessing authorization of sales transactions

B) reasonableness test for unit selling price of sale

C) post-processing review of sales transactions by the sales department

D) logging in to the company’s information systems via a password

30) The auditor receives the client’s schedule of recorded disposals and then performs

detail tie-in tests of the recorded disposals schedule. What procedures does the auditor

perform on the client’s schedule of recorded disposals?

31) In certain circumstances, an auditor will issue modified unqualified report. Discuss

each of the five circumstances when an auditor would issue an unqualified report with

an explanatory paragraph or modified wording.

32) What is the key advantage and disadvantage associated with systematic sample

selection? How must auditors address this disadvantage?

33) Certain principles dictate the proper design and use of documents and records.

Briefly describe several of these principles.

34) Distinguish between internal documentation and external documentation as types of

audit evidence. Give two examples of each. Which type is considered more reliable?

35) What are two important procedures that companies should implement to prevent

misstatements in owners’ equity?

36) Discuss the auditor’s responsibilities for inventory maintained in public warehouses

or with other outside custodians.

37) Auditors examine supporting documentation for cash disbursements subsequent to

the balance sheet date in order to determine whether the cash disbursement was for a

current period liability.

Describe at least two audit procedures the auditor would perform to provide evidence

that the cash disbursement was made for a current period liability.

38) In designing substantive audit procedures for tests of transactions for sales the

auditor needs to test for evidence of misstatements due to errors or fraud. Describe at

least 2 potential errors (unintentional) and at least 1 intentional (fraud).

39) In auditing depreciation expense one the auditors concerns is on determining that

the client’s calculations are correct. In determining that the auditor must weigh which

four considerations?