The probability that the customer will pay the seller does not affect whether a contract

exists for purposes of revenue recognition.

Most, but not all, liabilities are monetary liabilities.

Payment terms, interest rates, and other details of long-term liabilities usually are

reported in disclosure notes.

If a company’s capital structure includes convertible bonds, diluted EPS might be

reduced even if the bonds are not actually converted during the year.

The statement of cash flows summarizes transactions that caused cash to change during

a reporting period.

In a bank reconciliation, adjustments to the book balance could include adding or

subtracting company errors.

Vendor-specific objective evidence of separate sales prices is required for

multiple-element software contracts, but estimated selling prices can be used for other

multiple-element contracts under U.S. GAAP.

Generally speaking, cash flows from operating activities include the elements of net

income reported on a cash basis.

In a bill-and-hold arrangement, revenue only can be recognized after the sale of the

goods to the end user.

Monetary assets include only cash and cash equivalents.

For long-term construction contracts, the cost recovery method under IFRS requires

recognizing equal amounts of revenue and cost until all costs are recovered.

The physical life of a depreciable asset is bounded by its service life.

The criterion of 75% of economic life for classifying a lease as a capital lease is

consistent with the basic premise that most of the risks and rewards of ownership occur

during the first 75% of an asset’s life.

Sales tax paid on equipment acquired for use in the business is not capitalized.

Holding gains and losses on trading securities are included in earnings because:

a. They measure the success or failure of taking advantage of short-term price changes.

b. The IRS mandates the inclusion.

c. The SEC mandates the inclusion.

d. They measure the book value of the securities in the balance sheet date.

Cash flows from investing activities do not include:

a. Proceeds from issuing bonds.

b. Payment for the purchase of equipment.

c. Proceeds from the sale of marketable securities.

d. Cash outflows from acquiring land.

Lundholm Company purchased a machine for $100,000 on January 1, 2014. Lundholm

depreciates machines of this type by the straight-line method over a 10-year period

using no salvage value. Due to a change in sales patterns, on January 1, 2016,

management determines the useful life of the machine to be a total of five years. What

amount should Lundholm record for depreciation expense for 2016? The tax rate is

40%.

a. $20,000.

b. $16,000.

c. $17,778.

d. $26,667.

A note receivable Mild Max Cycles discounted with recourse was dishonored on its

maturity date. Mild Max would debit:

a. A loss on dishonored receivable.

b. A receivable.

c. Dishonored note expense.

d. Interest expense.

Which of the following is true about accounting for a troubled debt restructuring?

a. If a receivable becomes impaired, it is remeasured at the discounted present value of

the cash flows that were originally expected to be collected, but at a revised discount

rate.

b. Receivables are not remeasured; instead, fair values are obtained from reliable

factors.

c. If a receivable is continued, but with modified terms, a loss is typically recorded.

d. Receivables are never settled outright at the time of a restructuring.

In its 2016 income statement, WME reported a $40,000 loss on the sale of equipment.

In its reconciliation schedule, WME should:

Each year, White Mountain Enterprises (WME) prepares a reconciliation schedule that

compares its income statement with its statement of cash flows on both the direct and

indirect method bases.

a. Report a $40,000 cash outflow for the direct method.

b. Show a $40,000 positive adjustment to net income under the indirect method.

c. Show a $40,000 negative adjustment to net income under the indirect method.

d. None of these answer choices is correct.

The net postretirement benefit liability (APBO minus plan assets) is increased by:

a. Service cost.

b. Expected return on plan assets.

c. Amortization of net gain.

d. Cash contributions to plan assets.

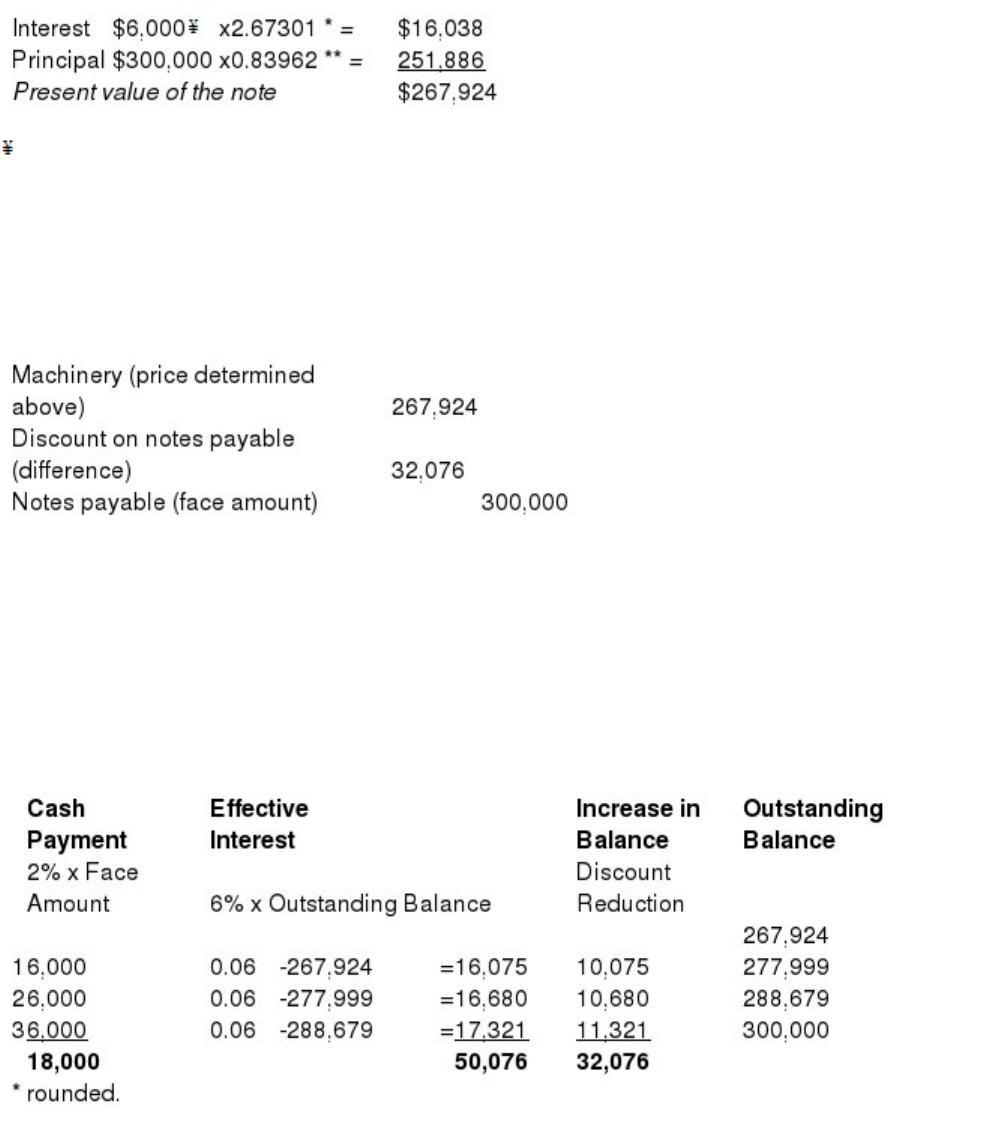

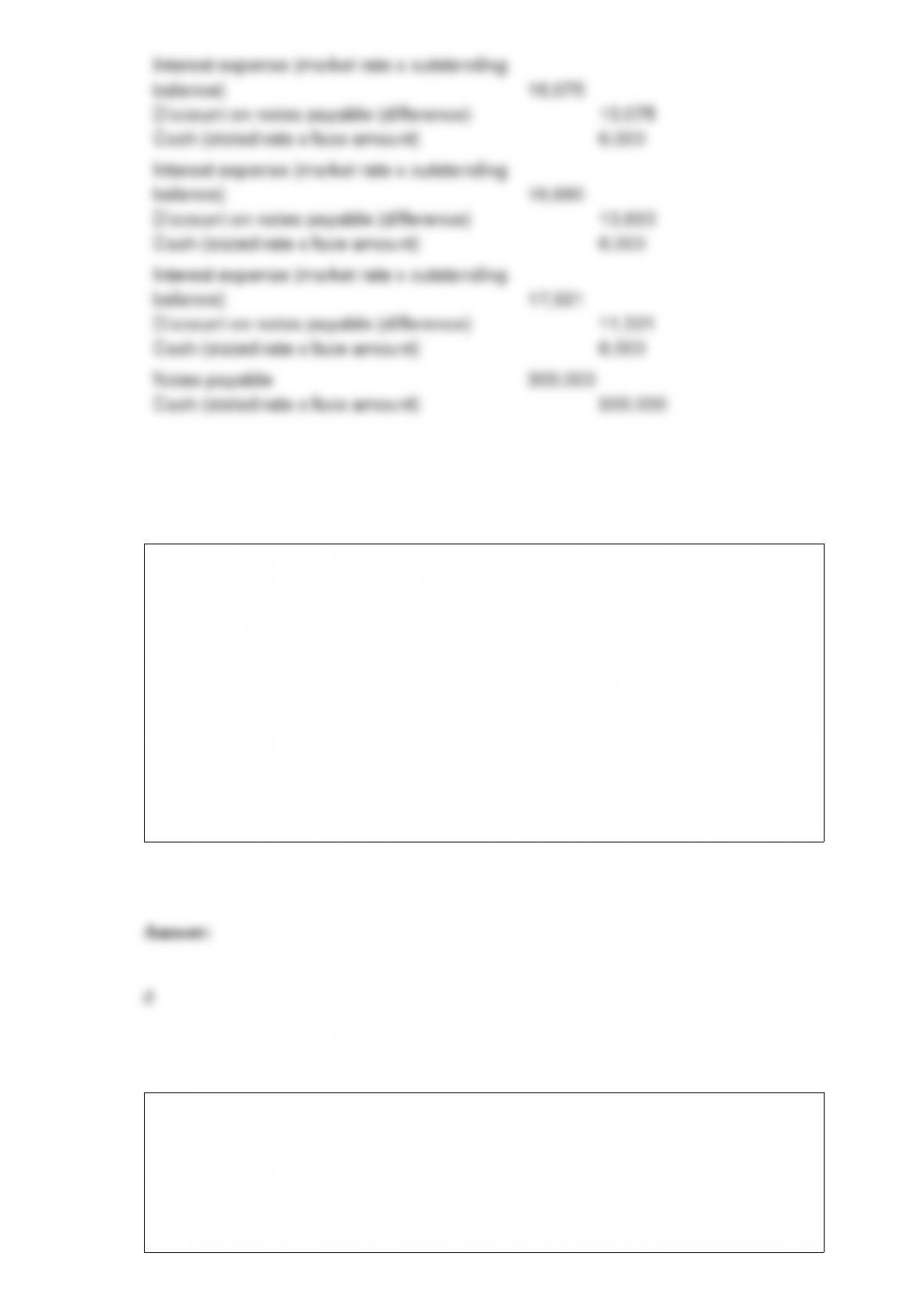

() Prepare the journal entries to record (a) interest for each of the three years and (b)

payment of the note at maturity.

When the investor’s level of influence changes, it may be necessary to change from the

equity method to another method. When the level of ownership falls from a range of

20% to 50% to less than 20%, the equity method typically would be discontinued and

the investment account balance would be carried over at:

a. Amortized cost on the date of ownership change.

b. Fair value on the date of ownership change.

c. Discounted present value on the date of ownership change.

d. The current balance, and this balance would serve as the new “cost.”

When bonds are sold at a discount, if the annual straight-line amortization amount is

compared to the annual effective interest amortization amount over the life of the bond

issue, the annual amount of the straight-line amortization of discount is:

a. Higher than the effective interest amount every year.

b. Higher than the effective interest amount in the early years and less than the effective

interest amount in the later years.

c. Less than the effective interest amount in the early years and more than the effective

interest amount in the later years.

d. Less than the effective interest amount every year.

An investor purchases a 20-year, $1,000 par value bond that pays semiannual interest of

$40. If the semiannual market rate of interest is 5%, what is the current market value of

the bond?

a. $ 828.

b. $ 893.

c. $1,000.

d. $1,686.

If Pop Company owns 15% of the common stock of Son Company, then Pop Company

typically:

a. Would record 15% of the net income of Son Company as investment income each

year.

b. Would record dividends received from Son Company as investment revenue.

c. Would increase its investment account by 15% of Son Company income each year.

d. All of these answer choices are correct.

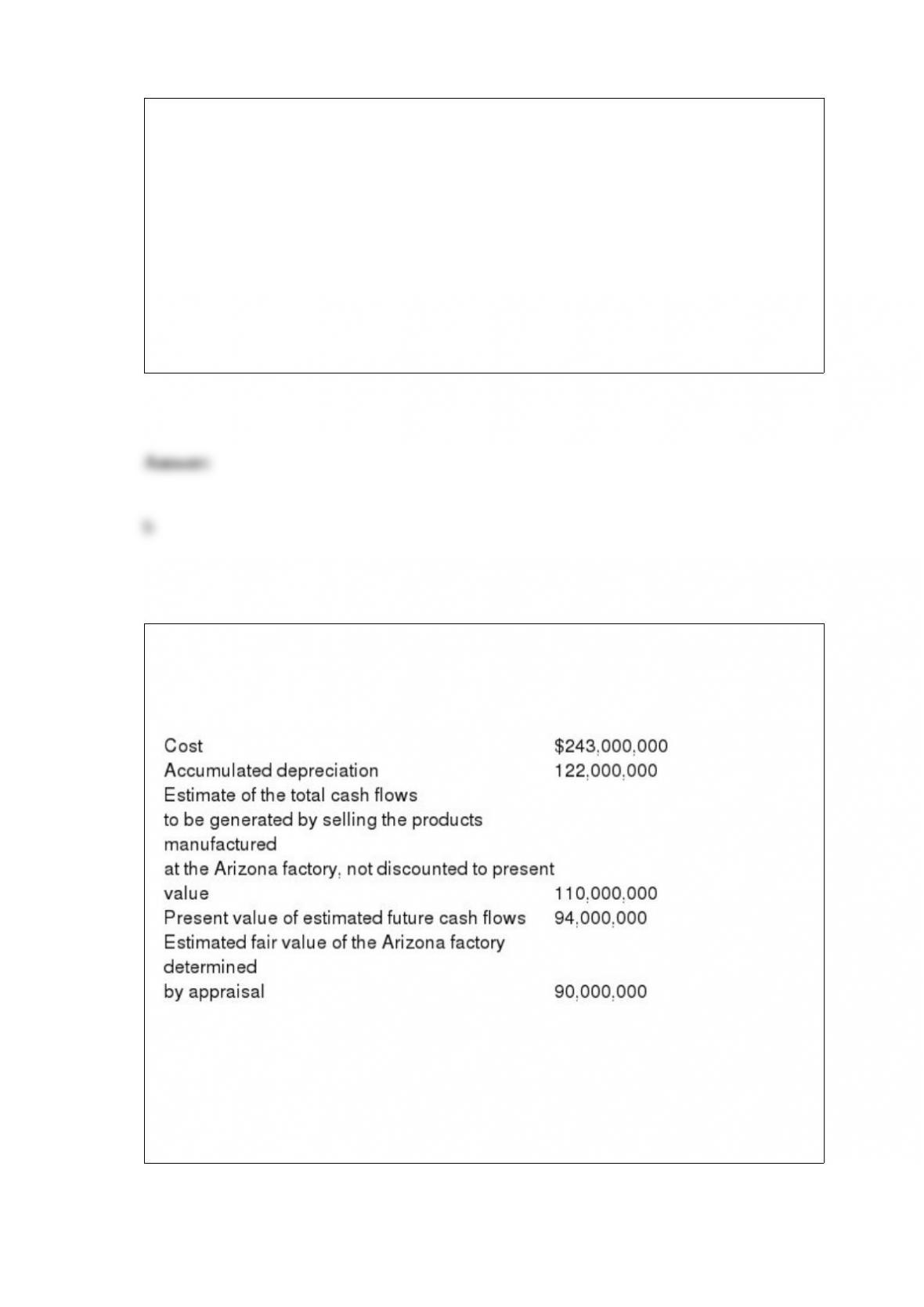

Sanders Corporation operates a factory in Arizona. Due to a change in business climate,

an impairment test is deemed appropriate. Management has acquired the following

information for the assets at the plant:

Required:

1> Determine the amount of impairment loss, if any.

2> If a loss is indicated, prepare the entry to record the loss

3> Repeat requirement 1 assuming that Sanders prepares its financial statements

according to 4> International Financial Reporting Standards (IFRS). Also assume that

the estimated fair value of the factory approximates fair value less costs to sell.

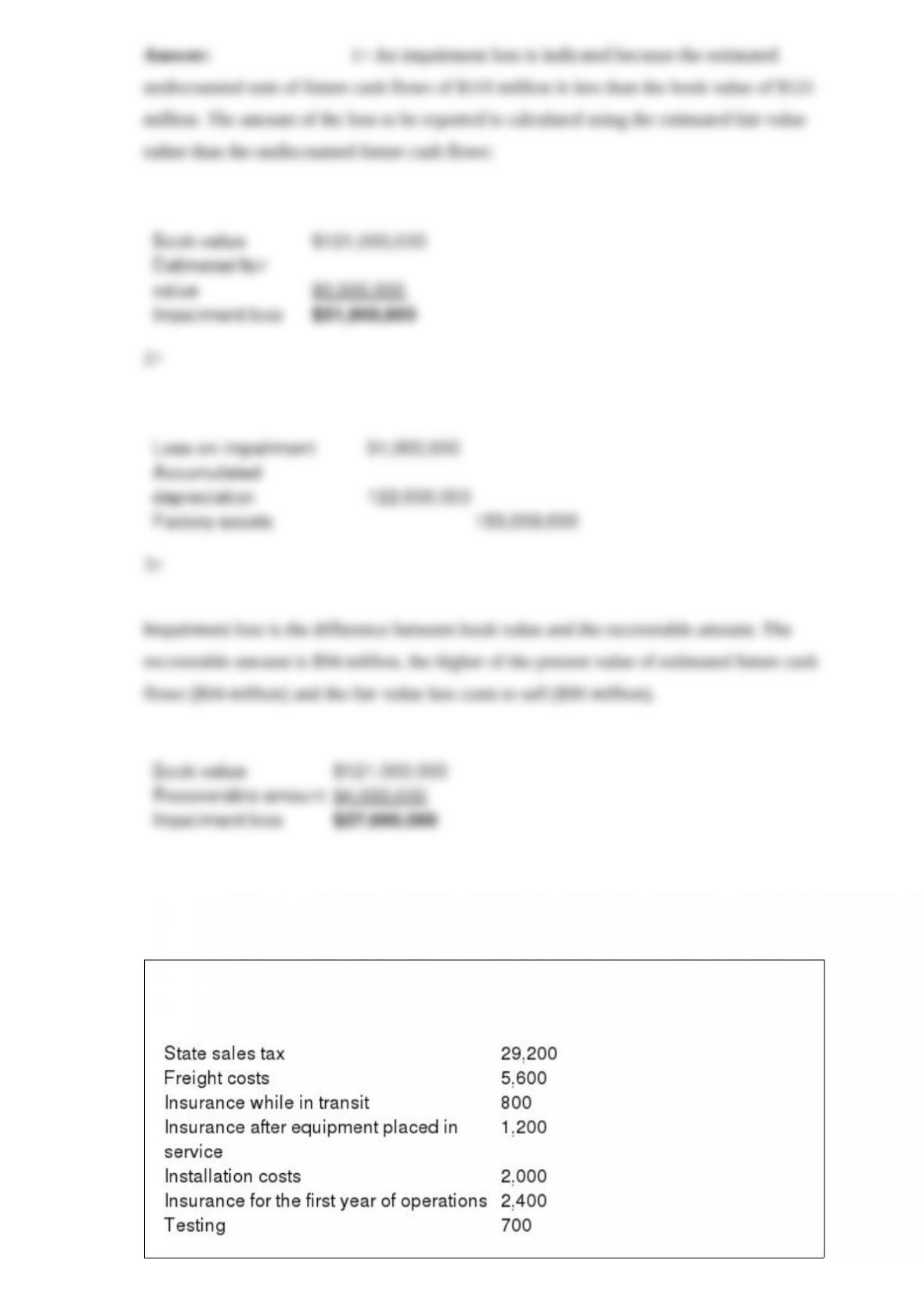

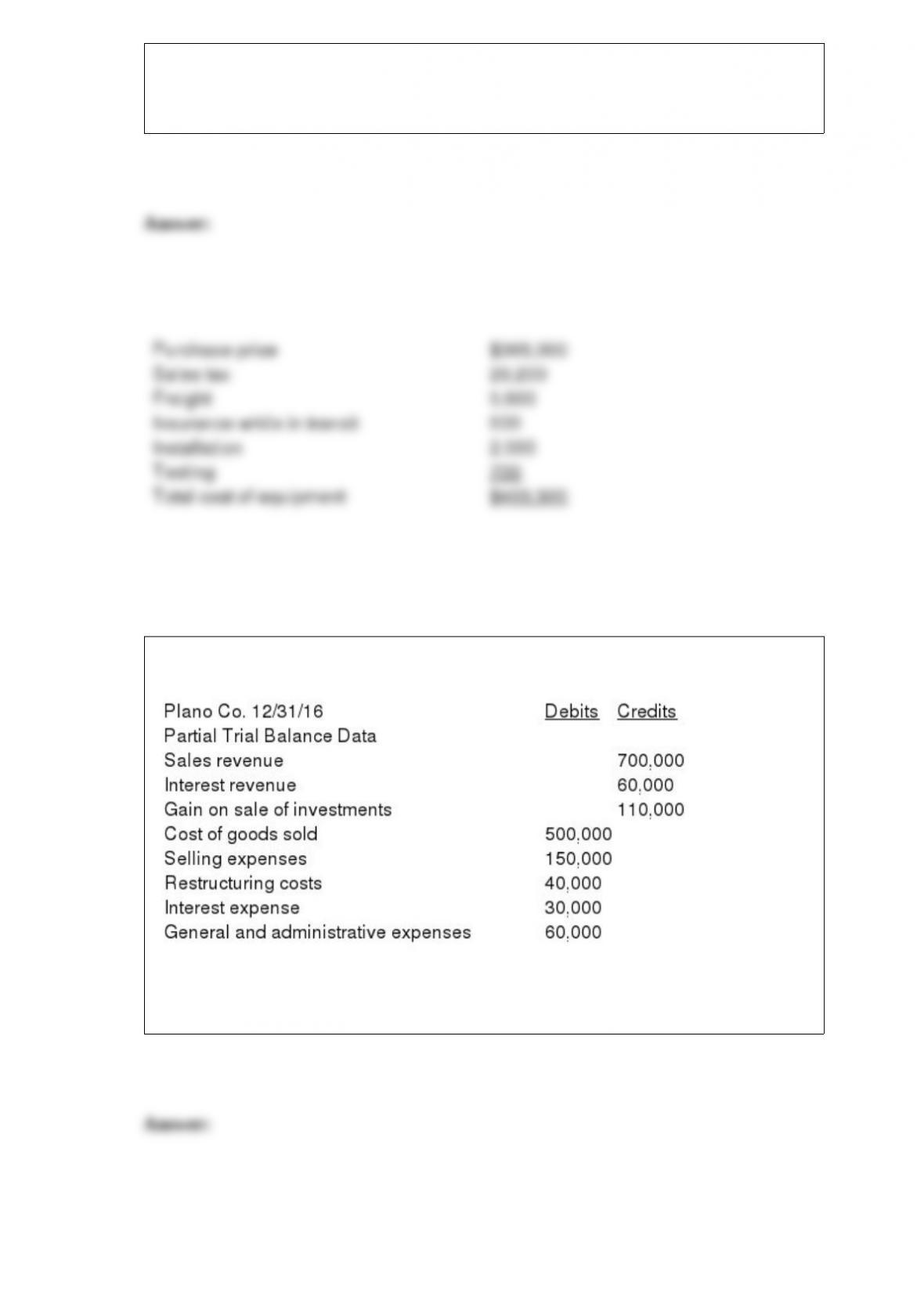

Mad Hatter Enterprises purchased new equipment for $365,000, terms f.o.b. shipping

point. Other costs connected with the purchase were as follows:

Required:

Determine the capitalized cost of the equipment.

Plano had 50,000 shares of stock outstanding throughout the year. Income tax expense

has not yet been accrued. The effective tax rate is 30%.

Required: Prepare a multiple-step income statement with earnings per share disclosure.

On February 1, 2016, Stealth Trucks sold a diesel rig to Kansas Transports for

$250,000, receiving a $50,000 down payment and a 12-month, 10% note for the

balance. Principal and interest are due at maturity, and the 10% interest rate reflected

the market rate of interest at the time of sale. On August 1, 2016, Kansas Transports

discounted the note without recourse at the First South Bank at 12% interest.

Required:

Prepare all required journal entries at August 1 to recognize interest revenue and the

discounting of the note.

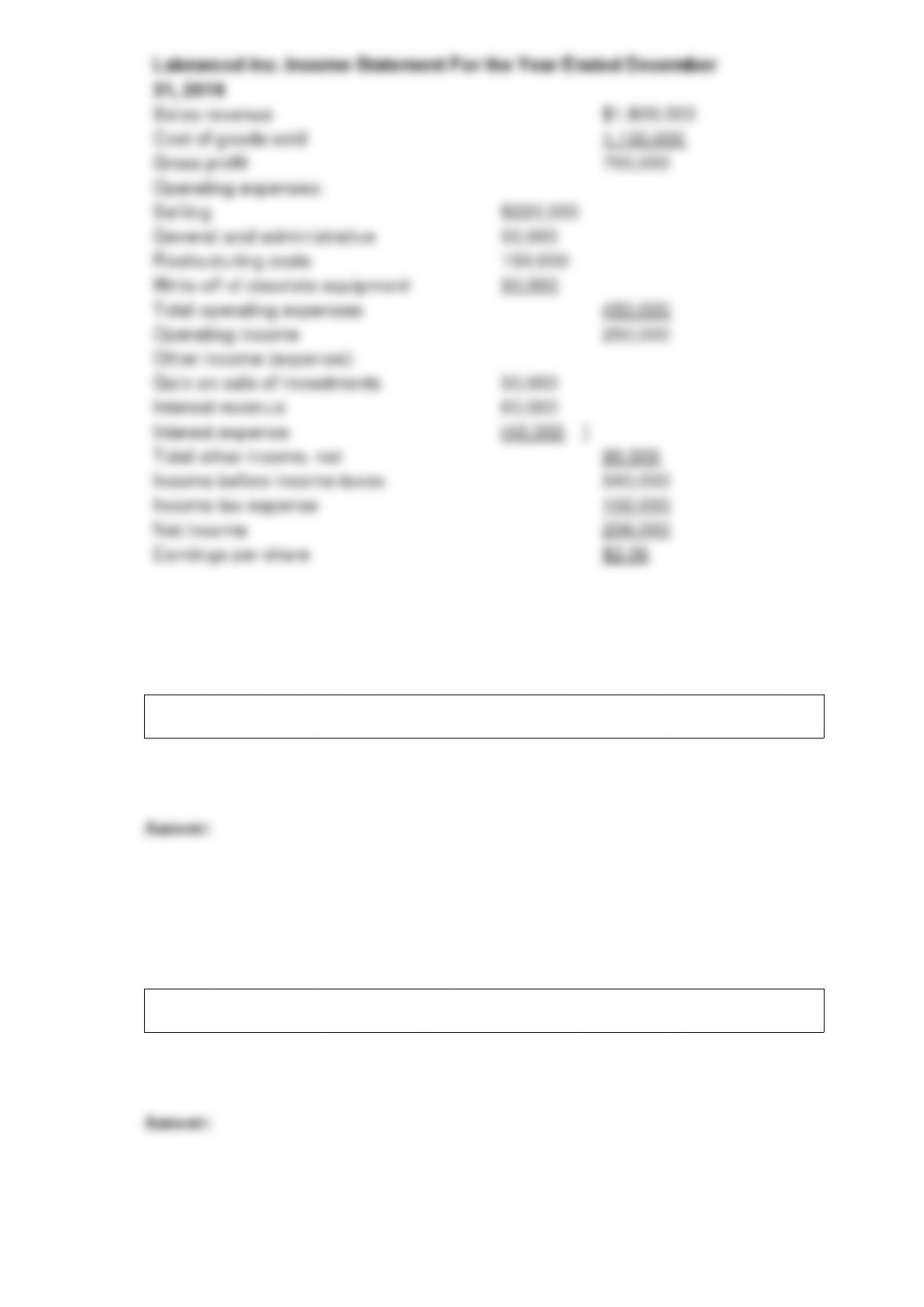

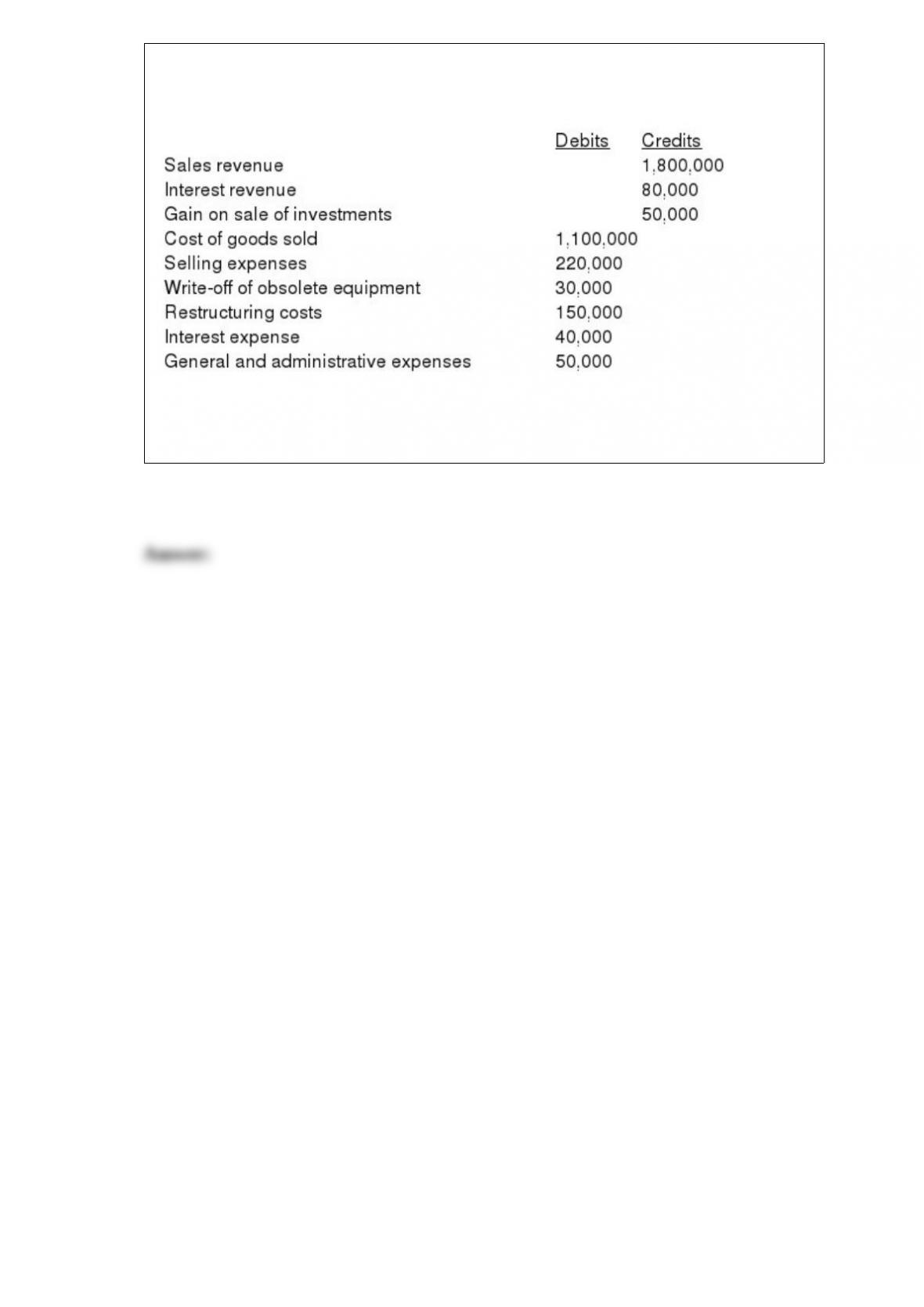

The trial balance of Lakewood Inc. included the following accounts as of December 31,

2016:

Lakewood Inc. had 100,000 shares of stock outstanding throughout the year. Income tax

expense has not yet been accrued. The effective tax rate is 30%.

Required: Prepare a multiple-step income statement with earnings per share disclosure.