1) The use of debt is sometimes described as financial leverage because debt can have

the effect of increasing the return on equity.

2) The direct materials section of a job cost sheet shows the materials costs assigned to

a job, but the direct labor section only shows the total hours of labor allocated to the

job.

3) An advantage of common-size statements is that they reflect the dollar magnitude

(size) of the different companies under analysis.

4) The manufacturing budgets include the sales budget and the budgeted income

statement.

5) A purchase of land in exchange for a long-term note payable is reported in the

investing section of the statement of cash flows.

6) Expenses related to accounting, human resource management, and financial

management are known as selling expenses.

7) One section of the process cost summary describes the equivalent units of production

for the department during the reporting period and presents the calculations of the direct

materials and conversion costs per equivalent unit.

8) Companies that have a relatively large amount invested in assets to generate a given

level of sales are considered capital-intensive.

9) If a bond’s interest period does not coincide with the issuing company’s accounting

period, an adjusting entry is necessary to recognize bond interest expense accruing

since the most recent interest payment.

10) When evaluating the days’ sales uncollected ratio, generally the higher the

receivables balance, the better the ratio.

11) General-purpose financial statements include the (1) income statement, (2) balance

sheet, (3) statement of stockholders’ equity (or statement of retained earnings), (4)

statement of cash flows, and (5) notes to these statements.

12) The cash flow on total assets ratio compared to the total assets ratio can be used as

an indicator of earnings quality.

13) The price-earnings ratio is calculated by dividing:

A.Market value per share by earnings per share.

B.Earnings per share by market value per share.

C.Dividends per share by earnings per share.

D.Dividends per share by market value per share.

E.Market value per share by dividends per share.

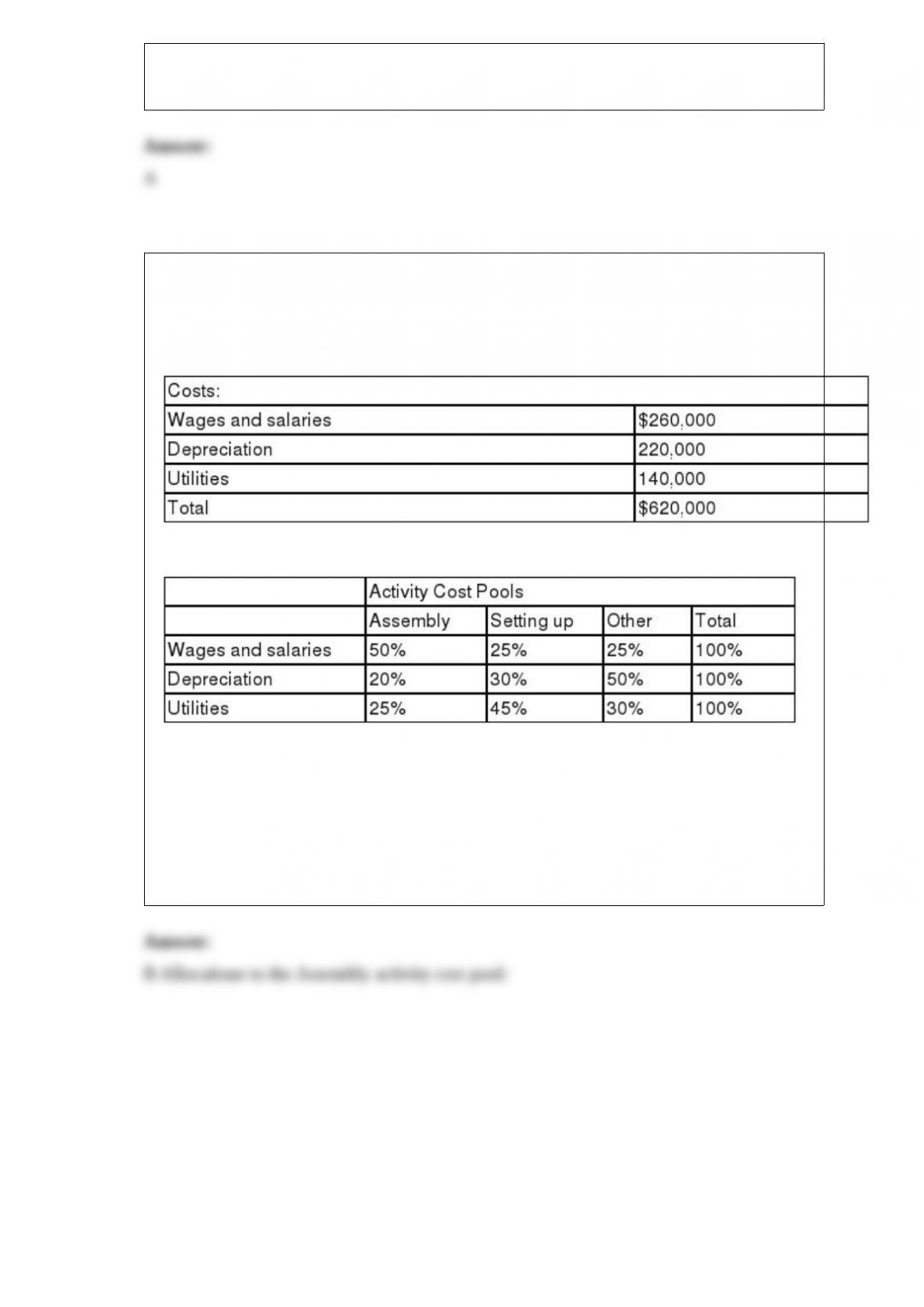

14) Borden Corporation uses an activity-based costing system with three activity cost

pools. The company has provided the following data concerning its costs and its activity

based costing system:

Distribution of resource consumption:

How much cost, in total, would be allocated in the first-stage allocation to the Assembly

activity cost pool?

A.$196,333

B.$209,000

C.$310,000

D.$155,000

E.$200,000

15) Pepper Department store allocates its service department expenses to its various

operating (sales) departments. The following data is available for its service

departments:

The following information is available for its three operating (sales) departments:

What is the total expense allocated to Department B?

A.$29,375.

B.$30,462.

C.$30,500.

D.$30,775.

E.$32,160.

16) Products that are in the process of being manufactured but are not yet complete are

called:

A.Raw materials inventory.

B.Conversion costs.

C.Cost of goods sold.

D.Work in Process inventory.

E.Finished goods inventory.

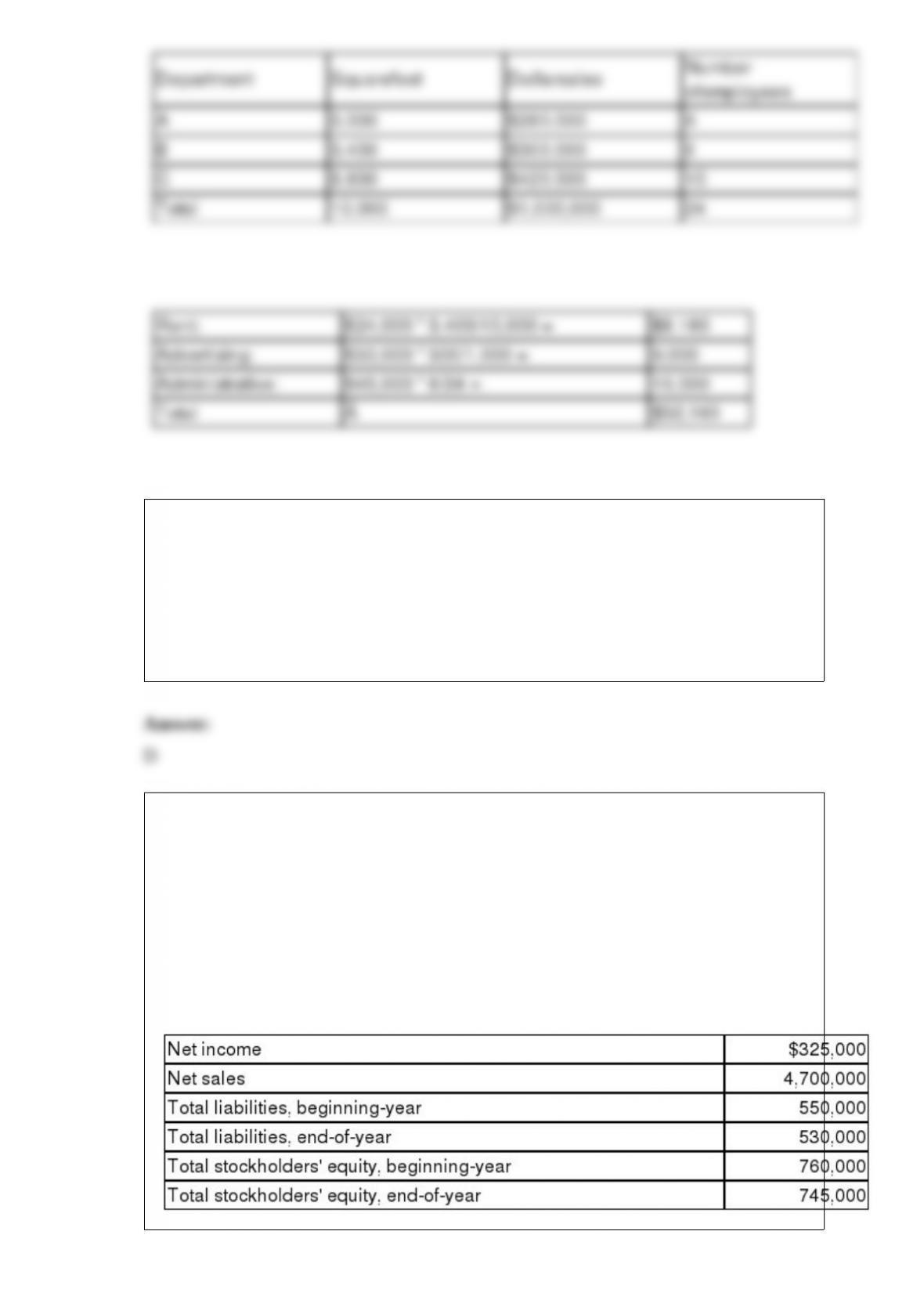

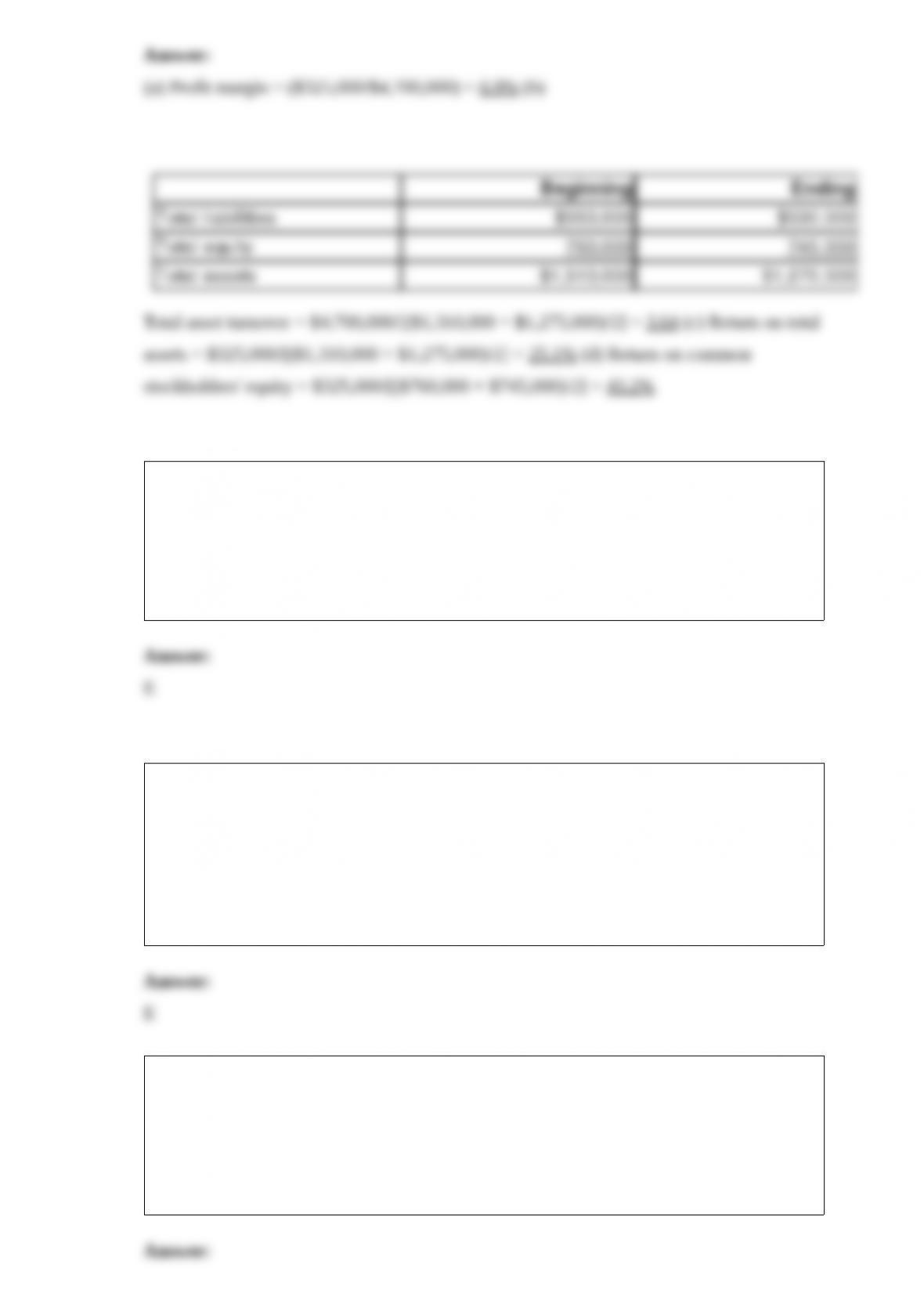

17) Selected current year end financial information for a company is presented below.

Calculate the following company ratios:

(a) Profit margin.

(b) Total asset turnover.

(c) Return on total assets.

(d) Return on common stockholders’ equity (assume the company has no preferred

stock).

18) Return on investment can be split into which of the following two measures?

A.Investment center income and profit margin.

B.Profit margin and net income.

C.Investment center average assets and investment turnover.

D.Residual income and operating income.

E.Profit margin and investment turnover.

19) If an issuer sells bonds at a date other than an interest payment date:

A.This means the bonds sell at a premium.

B.This means the bonds sell at a discount.

C.The issuing company will report a loss on the sale of the bonds.

D.The issuing company will report a gain on the sale of the bonds.

E.The buyers normally pay the issuer the purchase price plus any interest accrued since

the prior interest payment date.

20) Period costs for a manufacturing company would flow directly to:

A.The income statement as an expense.

B.Factory overhead.

C.The balance sheet as inventory.

D.Cost of goods sold on the income statement.

E.The current schedule of cost of goods manufactured.

21) Eastline Corporation had 10,000 shares of $10 par value common stock outstanding

when the board of directors declared a stock dividend of 3,000 shares. At the time of the

stock dividend, the market value per share was $12. The entry to record this dividend is:

A.Debit Retained Earnings $36,000; credit Common Stock Dividend Distributable

$36,000.

B.Debit Retained Earnings $36,000; credit Common Stock Dividend Distributable

$30,000; credit Paid-In Capital in Excess of Par Value, Common Stock $6,000.

C.Debit Common Stock Dividend Distributable $36,000; credit Retained Earnings

$36,000.

D.Debit Retained Earnings $30,000; credit Common Stock Dividend Distributable

$30,000.

E.No entry is needed.

22) Depreciation:

A.Measures the decline in market value of an asset.

B.Measures physical deterioration of an asset.

C.Is the process of allocating the cost of a plant asset to expense.

D.Is an outflow of cash from the use of a plant asset.

E.Is applied to land.

23) In preparing a budgeted balance sheet, the amount for Accounts Receivable data

can be derived from:

A.The purchases budget and schedule of cash payments.

B.The sales budget and the schedule of cash receipts.

C.The capital expenditures budget and purchases budget.

D.The budgeted income statement and budgeted balance sheet.

E.The selling expenses budget and the schedule of cash receipts.

24) Jervis sells $75,000 of its accounts receivable to Northern Bank in order to obtain

necessary cash. Northern Bank charges a 5% factoring fee. What entry should Jervis

make on to record the transaction?

A.Debit Cash $71,250; debit Factoring Fee Expense $3,750; credit Accounts

Receivable $75,000

B.Debit Accounts Receivable $71,250; debit Factoring Fee Expense $3,750; credit Cash

$75,000

C.Debit Cash $75,000; credit Factoring Fee Expense $3,750; credit Accounts

Receivable $75,000

D.Debit Cash $71,250; credit Accounts Receivable $71,250

E.Debit Accounts Receivable $75,000; credit Factoring Fee Expense $3,750; credit

Cash $71,250

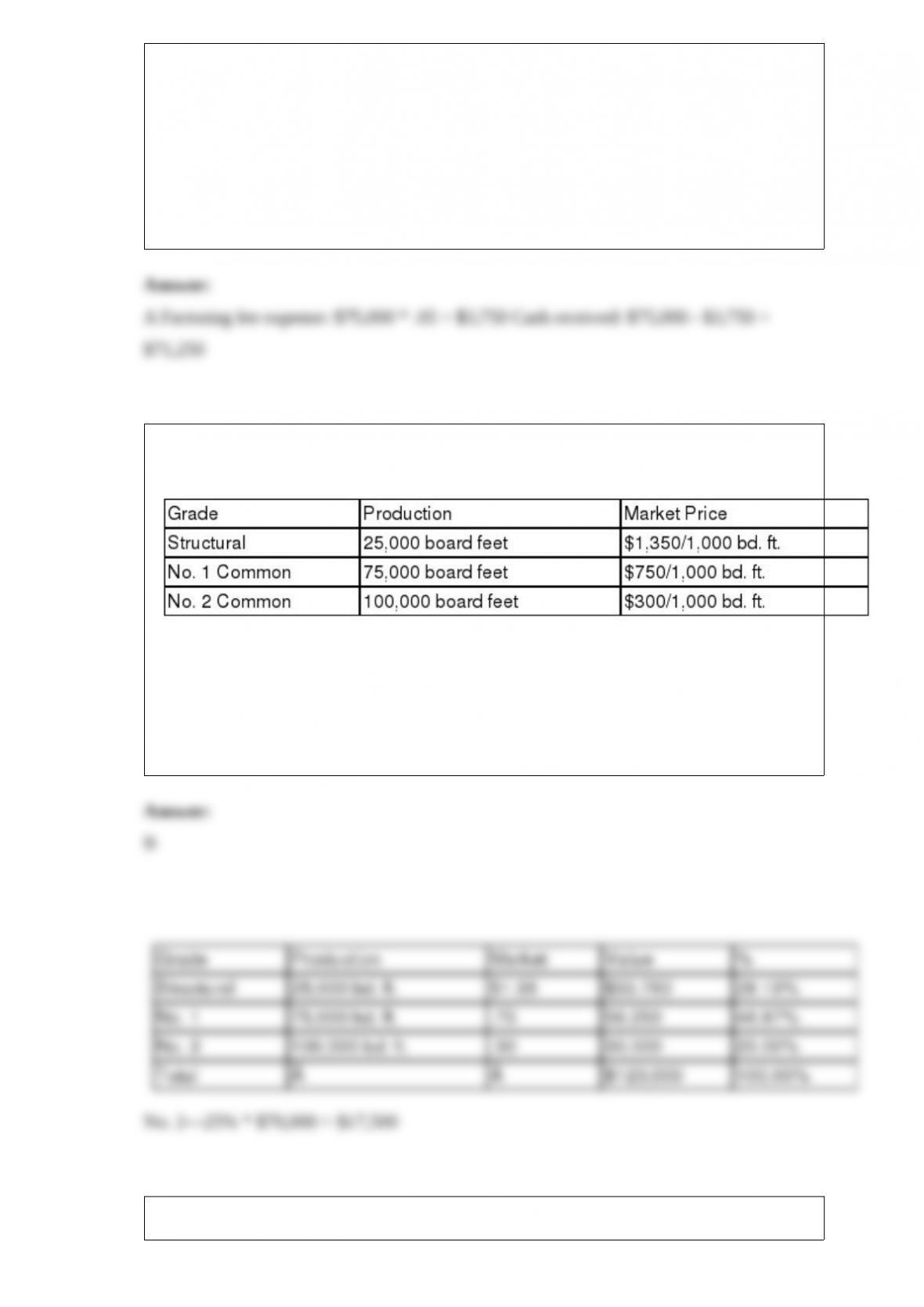

25) A lumber mill paid $70,000 for logs that produced 200,000 board feet of lumber in

3 different grades and amounts as follows:

Compute the portion of the $70,000 joint cost to be allocated to No. 2 Common.

A.$0.

B.$17,500.

C.$23,333.

D.$35,000.

E.$70,000.

26) List the five basic components of accounting information systems and give an

example of each.

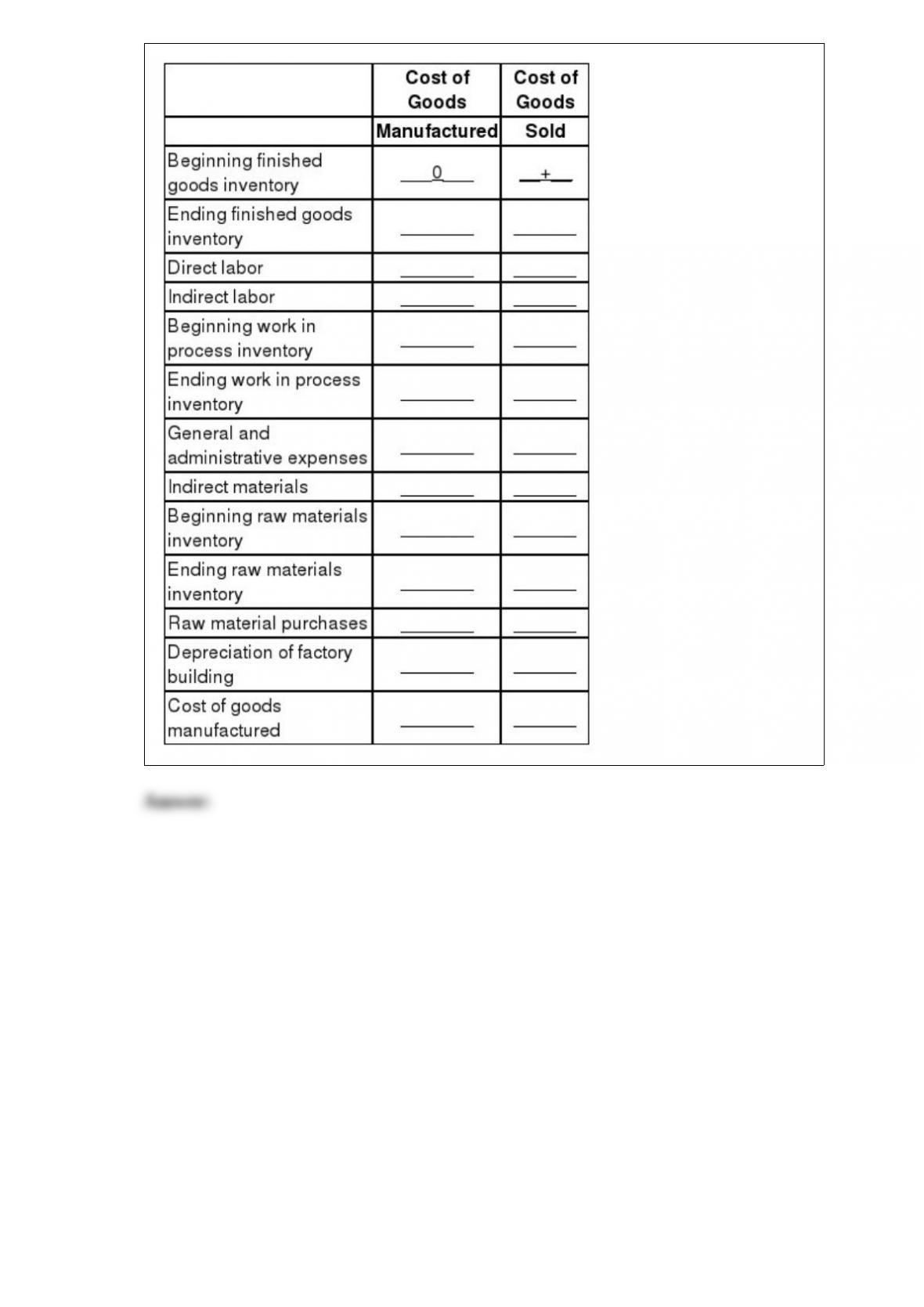

27) The following items for Neptune Company are used to compute the cost of goods

manufactured and the cost of goods sold. Indicate how each item should be used in the

calculations by filling in the blanks with “+” if the item is to be added, “-” if the item is

to be subtracted, or “0” if the item is not used in the calculation. The first item is

completed as an example.

28) A company purchased a delivery van on October 1 of the current year at a cost of

$40,000. The van is expected to last six years and has a salvage value of $2,200. The

company’s annual accounting period ends on December 31.

1) What is the depreciation expense for the current year, assuming the straight-line

method is used?

2) What is the book value of the van at the end of the first year?

29) In preparing flexible budgets, the costs that remain constant in total are

_______________ costs. Those costs that change in total are _______________ costs.

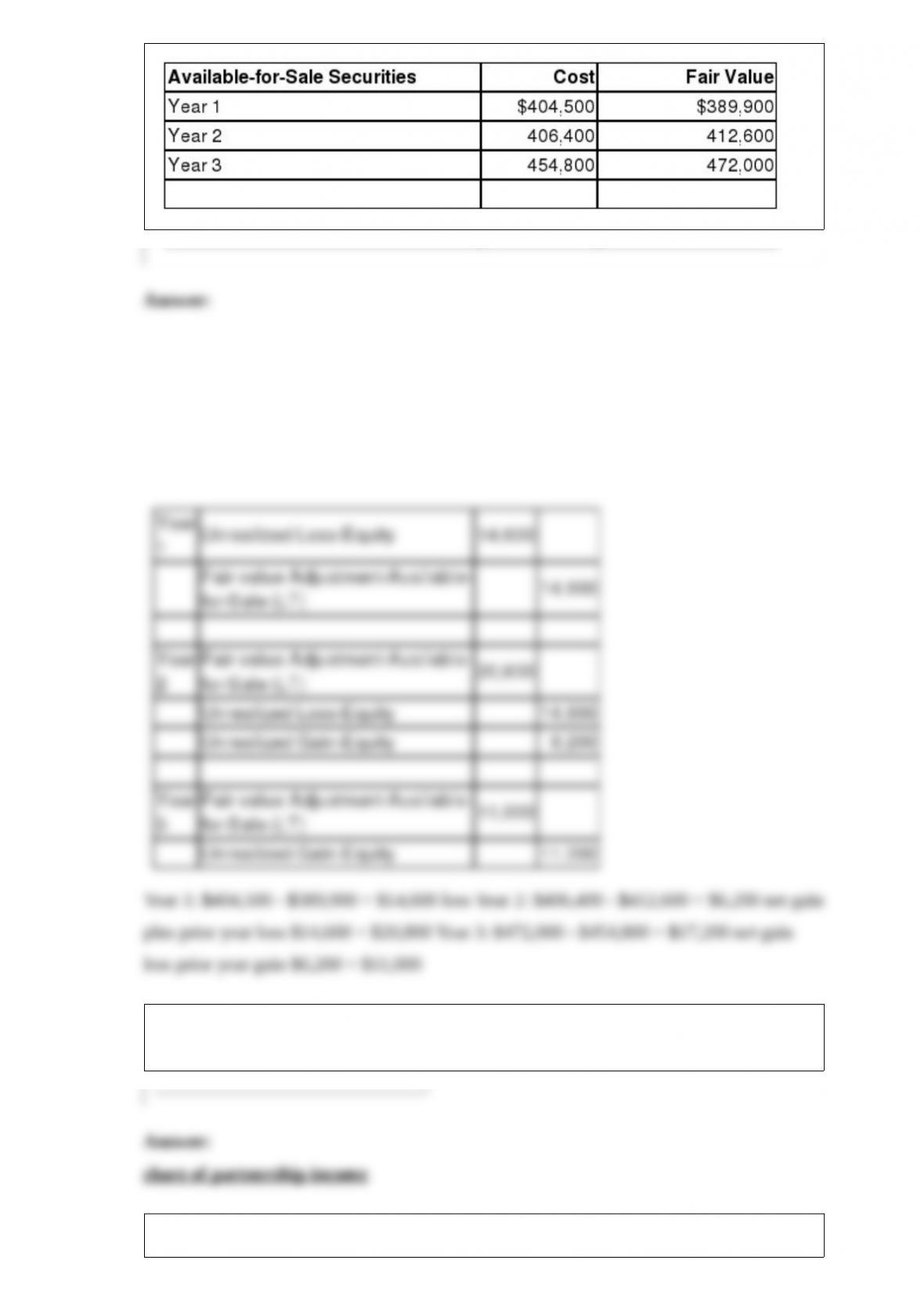

30) Element Company had the following long-term available-for-sale securities in its

portfolio at December 31 for each of the years listed. The year-end cost and fair values

for its portfolio follow. Beginning with Year 1, prepare the appropriate journal entry to

record each year-end market adjustment for these securities.

31) Partners in a partnership are not taxed on their withdrawals, but rather on

_____________________________.

32) A company is considering purchasing a machine for $85,000. The machine is

expected to generate a net after-tax income of $11,250 per year. Depreciation expense

would be $8,500. What is the payback period for this machine?

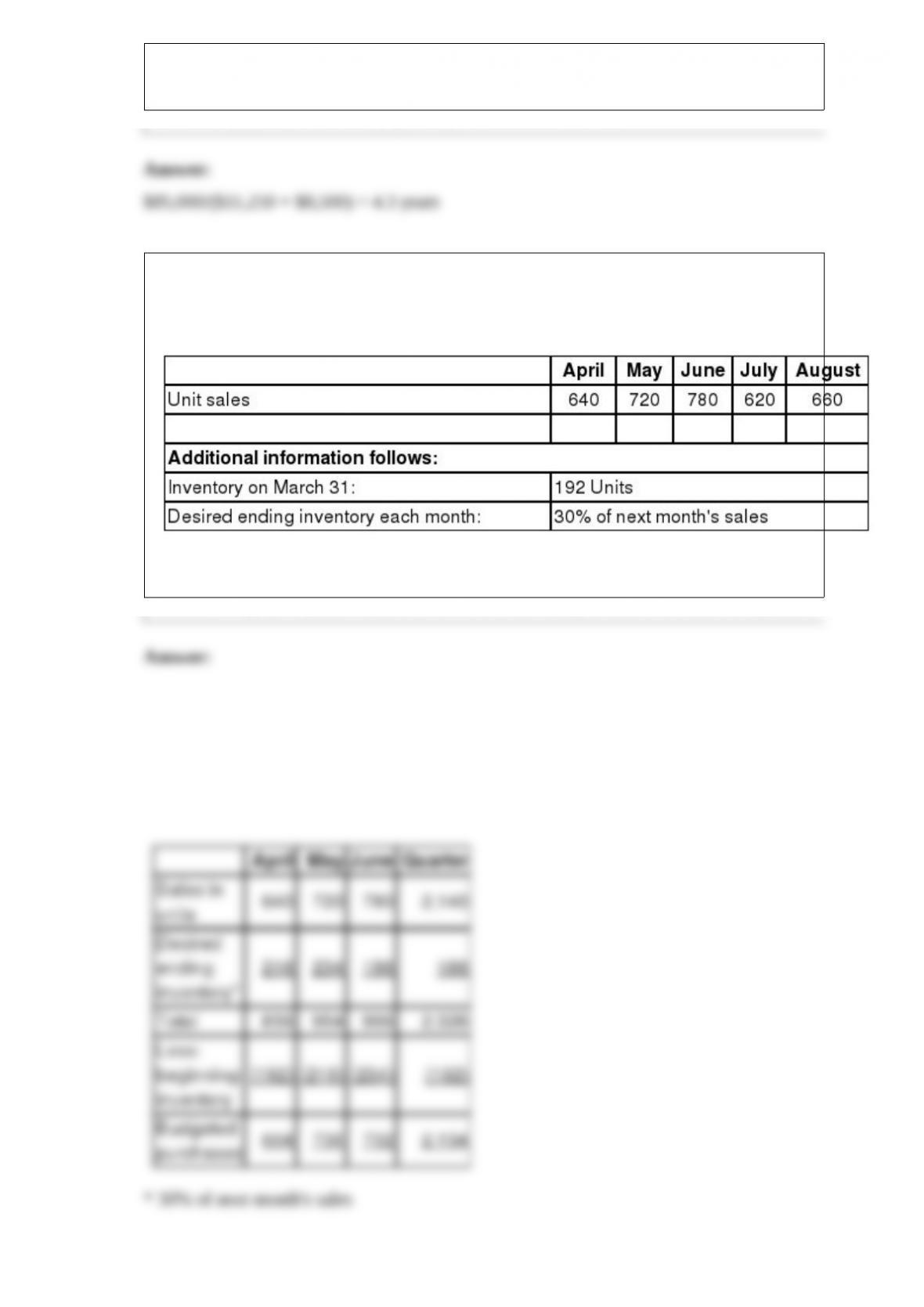

33) Dado, Inc. is preparing its budget for the second quarter. The following sales data

have been forecasted:

Prepare a merchandise purchases budget for the total units to be purchased in the

months of April, May, and June, as well as the total unit purchases for entire the quarter.

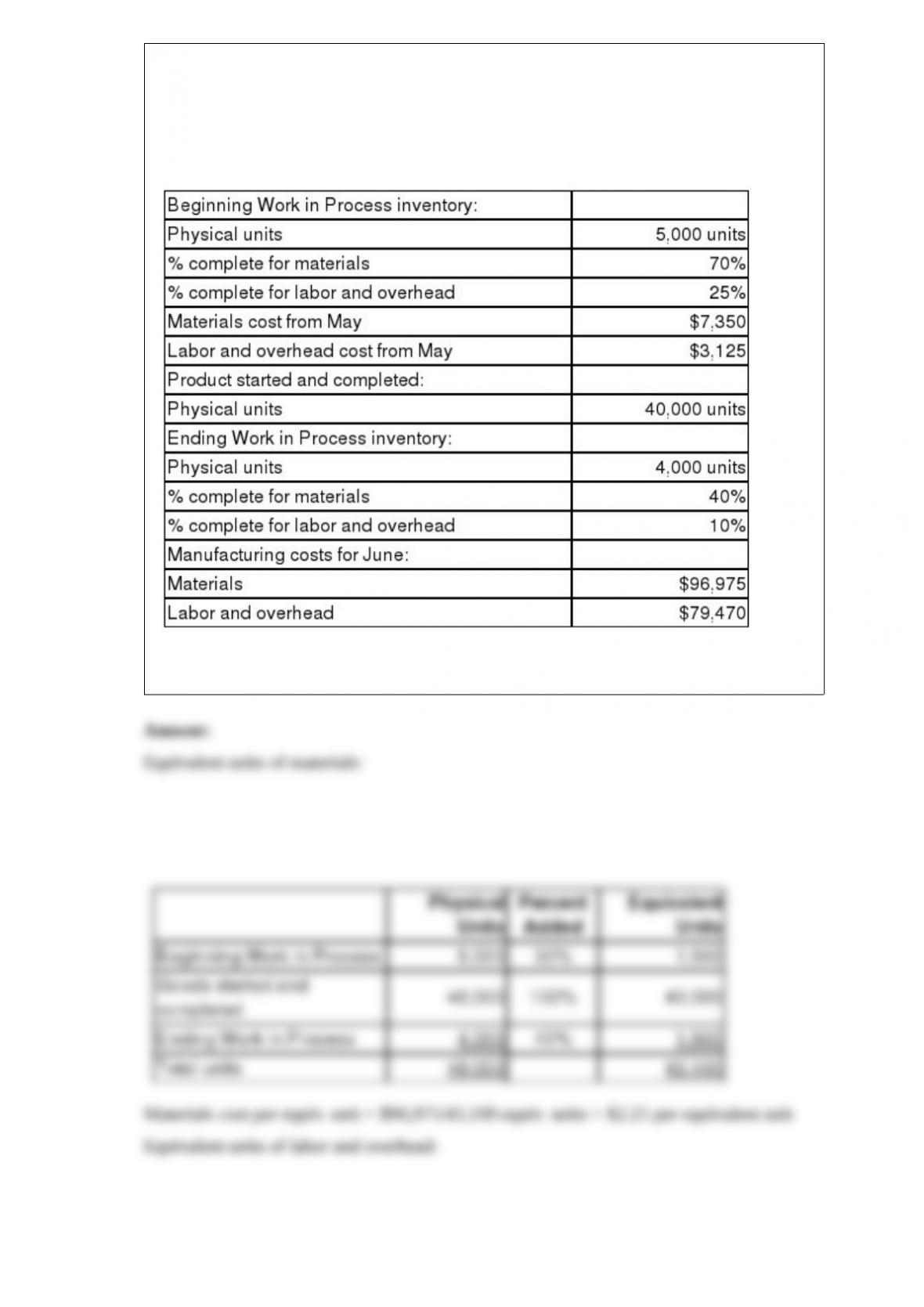

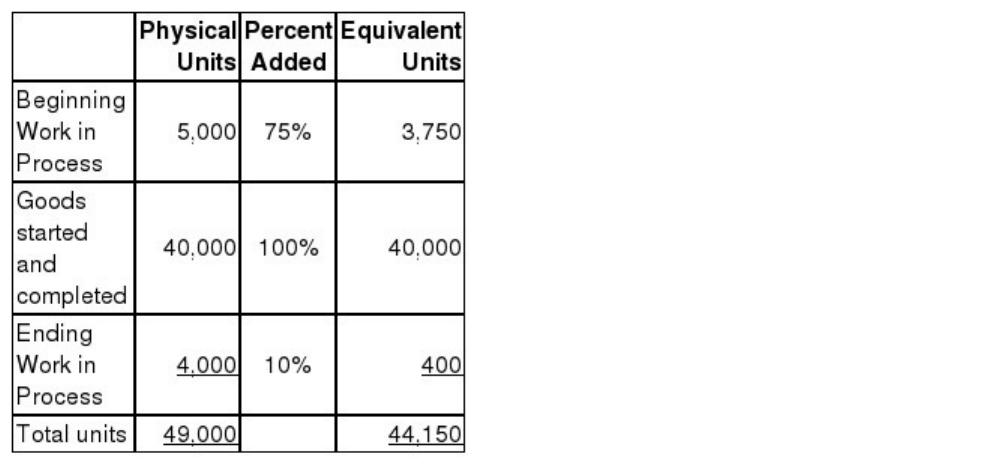

34) Refer to the following information about the Finishing Department in the Davidson

Factory for the month of June. Davidson Factory uses the FIFO method of inventory

costing.

Compute the total cost of all units that were completed and transferred to finished

goods during June. Compute the total cost of the ending Work in Process inventory.

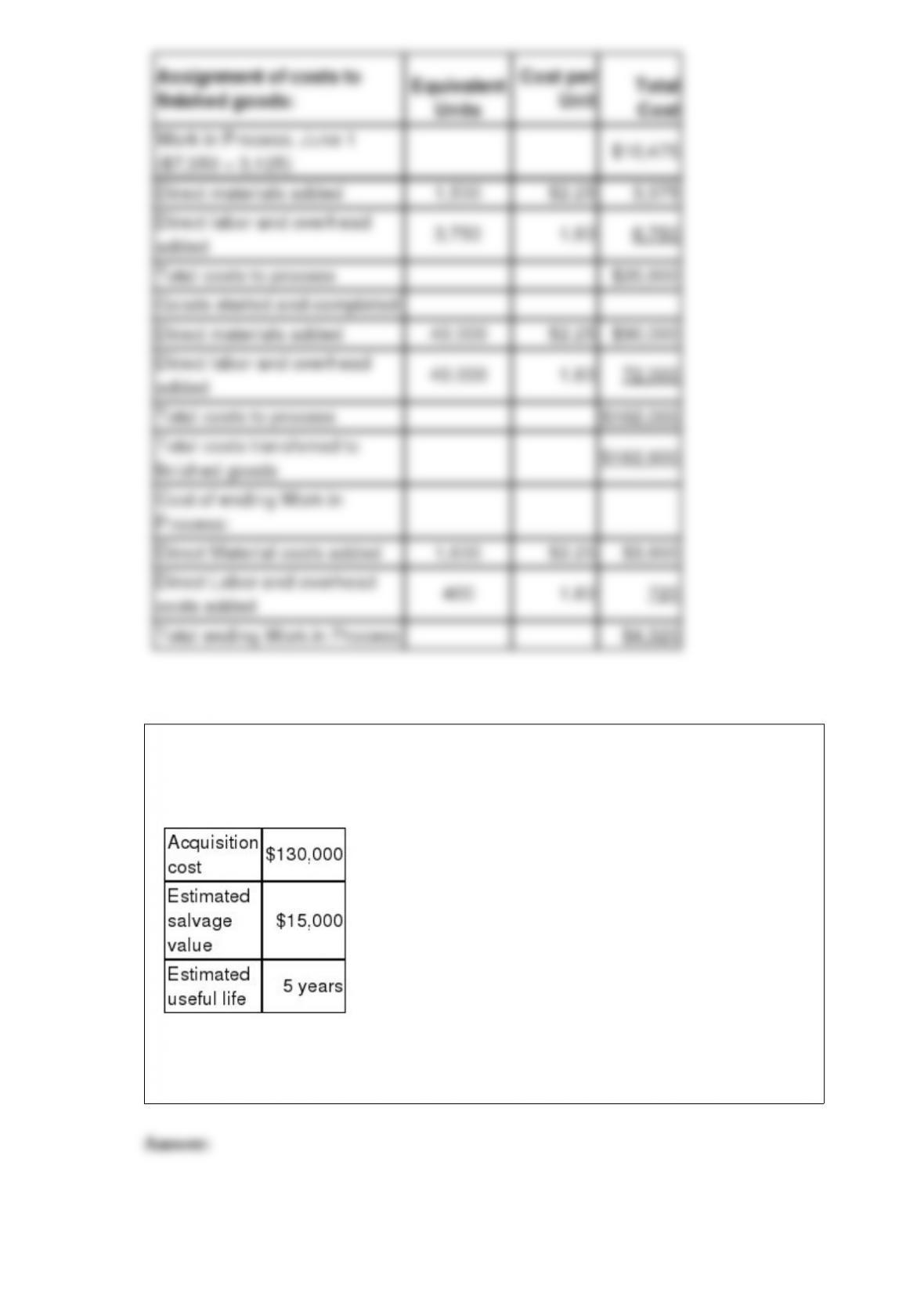

35) On April 1, Year 1, Raines Co. purchased and placed a plant asset in service. The

following information is available regarding the plant asset:

Make the necessary adjusting journal entries at December 31, Year 1, and December 31,

Year 2 to record depreciation for each year under the double-declining balance

depreciation method: