On June 30, 2016, Prego Equipment purchased a precision laser-guided steel punch that

has an expected capacity of 300,000 units and no residual value. The cost of the

machine was $450,000 and is to be depreciated using the units-of-production method.

During the six months of 2016, 24,000 units of product were produced. At the

beginning of 2017, engineers estimated that the machine can realistically be used to

produce only another 230,000 units. During 2017, 70,000 units were produced. Prego

would report depreciation in 2017 of:

a. $135,230.

b. $126,000.

c. $108,000.

d. $105,000.

Accrued liabilities:

a. Are generally paid in services rather than cash.

b. Result from payment before services are received.

c. Result from services received before payment.

d. Are deferred charges to expense.

The corporate charter of Llama Co. authorized the issuance of 10 million, $1 par

common shares. During 2016, its first year of operations, Llama had the following

transactions:

January 1 sold 8 million shares at $15 per share

June 3 purchased 2 million shares of treasury stock at $18 per share

December 28 sold the 2 million shares of treasury stock at $20 per share

What amount should Llama report as additional paid-in capital in its December 31,

2016, balance sheet?

a. $122 million

b. $116 million

c. $112 million

d. $ 74 million

Washburn Co. spent $10 million to purchase a new patented technology, debiting an

intangible asset and crediting cash. Washburn uses SYD depreciation on its depreciable

assets and plans to amortize the intangible asset on a straight-line basis. The appropriate

accounting treatment is that:

a. Washburn is not required to make any accounting adjustments.

b. Washburn is required to adjust a change in accounting estimate prospectively.

c. Washburn has made a change in accounting principle, requiring retrospective

adjustment.

d. Washburn needs to correct an accounting error.

Z Company acquired a subsidiary several years ago that was appropriately excluded

from consolidation last year. This year Z has consolidated the subsidiary in its financial

statements. This results in:

a. An accounting change that should be reported prospectively.

b. A correction of an error.

c. An accounting change that should be reported by restating the

financial statements of all prior periods presented.

d. Neither an accounting change nor a correction of an error.

For a leased asset under a lease that qualifies as a capital lease because of a bargain

purchase option, the depreciation period used by the lessee must be:

a. The same period that was used by the lessor.

b. The useful life to the lessee.

c. The term of the lease regardless of the lease provisions.

d. The remaining life of the asset at the time the lease agreement took effect.

Priscilla’s Exotic Pets discounted a note receivable without recourse and the sales

criteria were met. The discounting is recorded as:

a. A secured borrowing.

b. Only note disclosure of the arrangement is required.

c. A sale.

d. None of these answer choices are correct.

JRE2 Inc. entered into a contract to install a pipeline for a fixed price of $2,200,000.

JRE2 recognizes revenue upon contract completion.

In 2015, JRE2 would report (rounded to the nearest thousand) gross profit (loss) of:

a. $0.

b. $(100,000).

c. $ 56,000.

d. $ 73,000.

When the amount of revenue collected in advance decreases during an accounting

period:

a. Accrual-basis revenues exceed cash collections from customers.

b. Accrual-basis net income exceeds cash-basis net income.

c. Accrual-basis revenues are less than cash collections from customers.

d. Accrual-basis net income is less than cash-basis net income.

An example of a contra account is:

a. Depreciation expense.

b. Accounts receivable.

c. Sales revenue.

d. Accumulated depreciation.

Important elements of an internal control system for cash disbursements include each of

the following except:

a. Only authorized personnel should sign checks.

b. All expenditures should be authorized before a check is prepared.

c. All disbursements, other than very small disbursements, should be made by check.

d. The same person that prepares the check should also record it in the proper journal.

Espana Corporation purchased $100,000 of Hales Inc. 6% bonds at par and classifies its

investment as available for sale. Unfortunately, a combination of problems at Hales and

in the debt market caused the fair value of the Hales investment to decline to $70,000

during 2016. Wang views this decline as an other-than-temporary impairment. Wang

calculates that, of the $30,000 drop in fair value, $10,000 of it relates to credit losses

and $20,000 relates to non-credit losses. If Wang accounts for the Hales bonds under

IAS No. 39, before-tax net income for 2016 will be reduced by: a. $0.

b. $10,000.

c. $20,000.

d. $30,000.

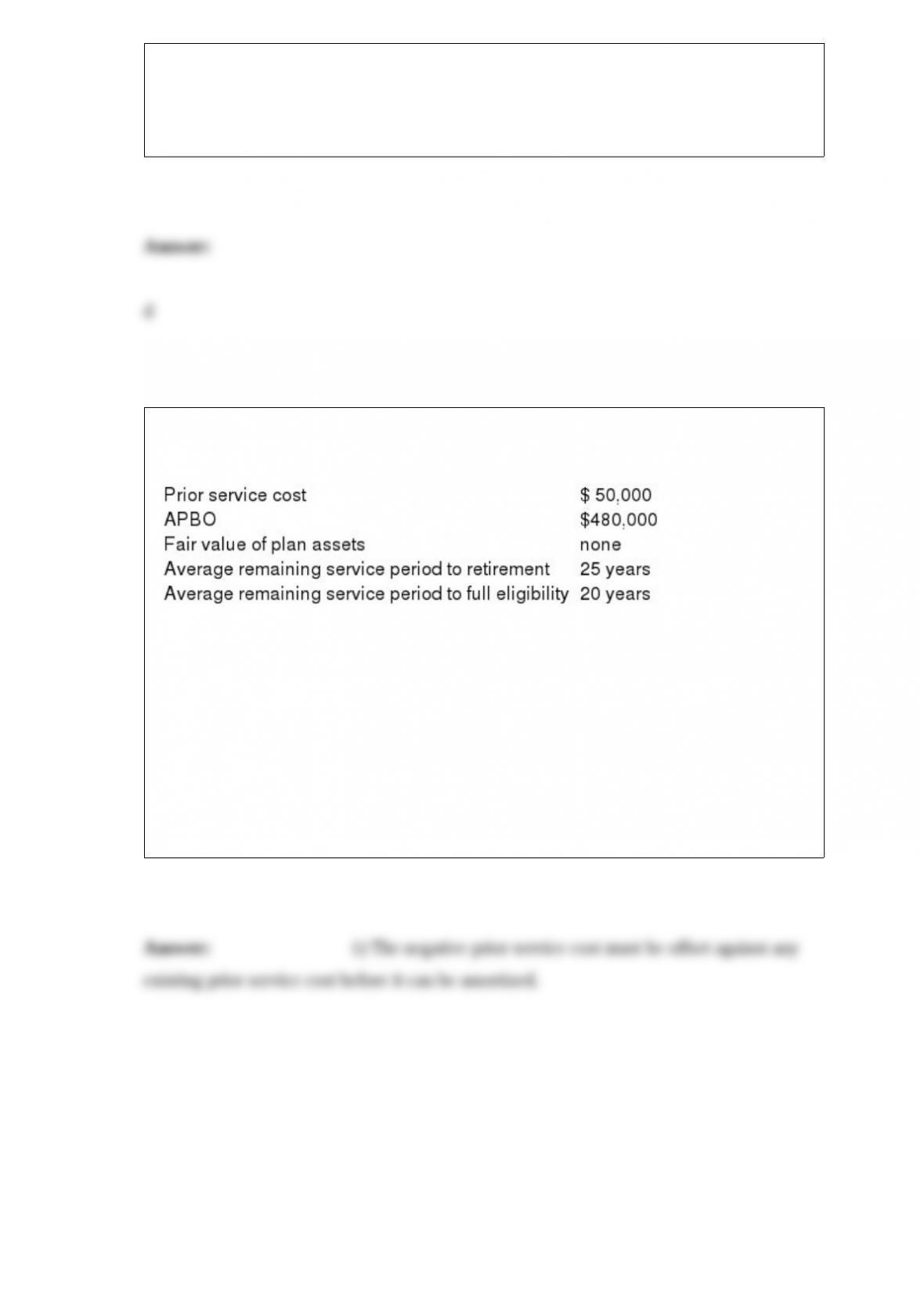

Brown Industries provides postretirement health care benefits to employees. On January

1 of the current calendar year, the following data were available.

Management amortizes prior service cost on a straight-line basis. The interest rate is

10%. Service cost for the current year is $95,000.

Required:

1) Calculate the prior service cost amortization for the current year.

2) Calculate the postretirement benefit expense for the current year.

3) Prepare the entry to record the postretirement benefit expense for the current year.

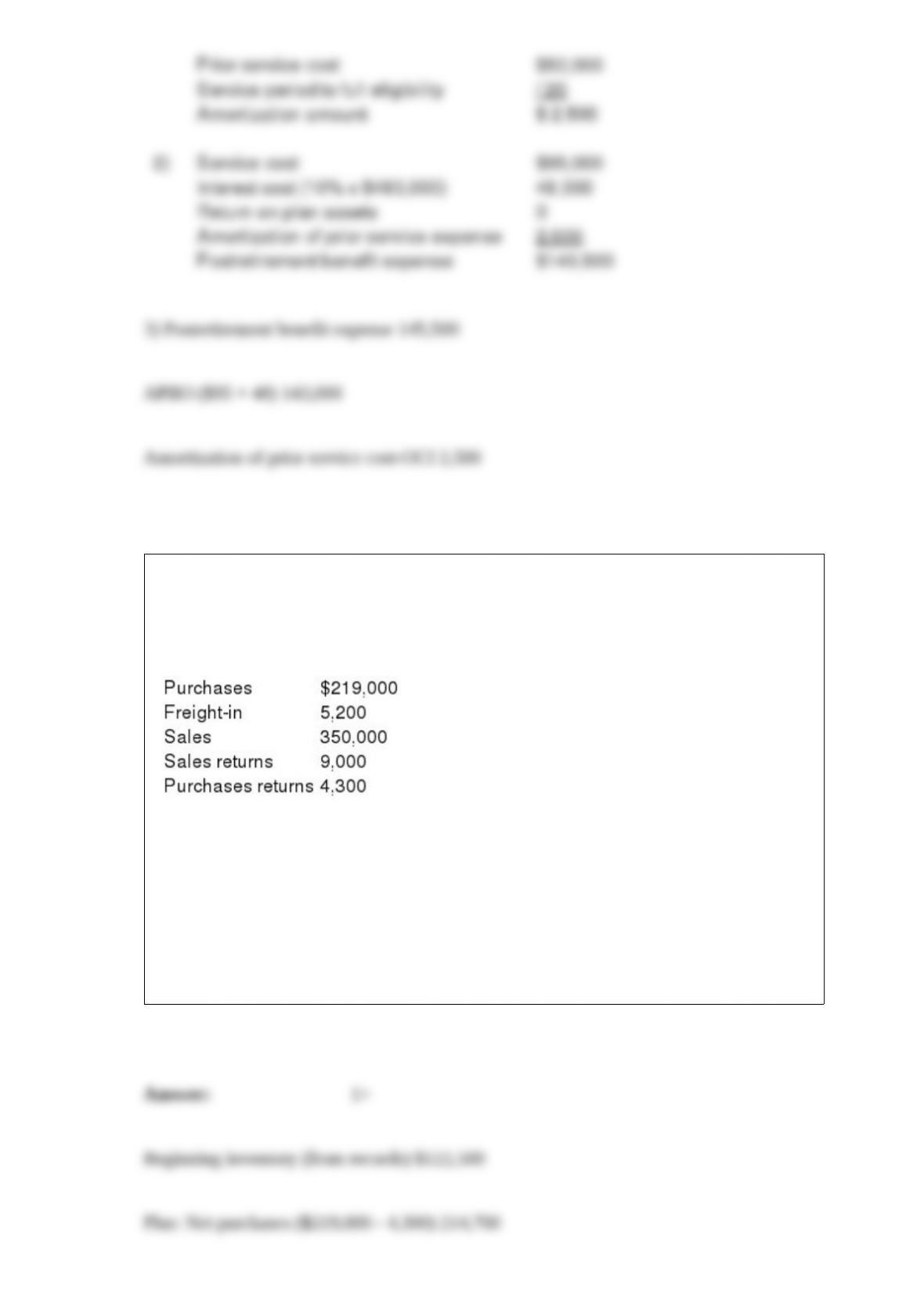

Henderson Company uses the gross profit method to estimate ending inventory and cost

of goods sold when preparing monthly financial statements required by its bank.

Inventory on hand at the end of July was $122,500. The following information for the

month of August was available from company records:

In addition, the controller is aware of $10,000 of inventory that was stolen during

August from one of the company’s warehouses. Required:

1> Calculate the estimated inventory at the end of August, assuming a gross profit ratio

of 30%.

2> Calculate the estimated inventory at the end of August, assuming a markup on cost

of 25%.

Silica Corporation constructs highly specialized communication satellites. A customer

in Hong Kong recently placed an order for a cable TV satellite at a price of $20 million.

The order was placed in April 2016, and the satellite is to be delivered in one year. The

customer has guaranteed to pay in full at the end of 2016, regardless of progress or

cancellation. Silica uses “proportion of time” as its measure of progress toward

completion.

Required: When should Silica recognize revenue: at completion, or as the construction

is performed?

Romano Services provides room cleaning arrangements for hotels in Ohio. On April 1,

Silvia Hotels & Resorts signed an agreement to outsource its room cleaning functions to

Romano. The contract specifies the service fee to be $15,000 per month, and all

payments are to be made shortly after the end of each quarter. It also specifies that

Romano will receive an additional quarterly bonus of $3,000, if during that quarter,

Silvia receives no more than five complaints from customers about room cleanliness. –

On April 1, based on historical experience, Romano estimated that there is a 75%

chance that it will earn the quarterly bonus.

– On May 5, Romano learned that, during March, there were two complaints from

customers related to room cleanliness. Based on this new information, Romano revised

its estimate downward to 40% that it would earn the quarterly bonus.

– On June 30, Silvia notified Romano that, for the quarter ended, there were four

complaints associated with room cleanliness, so Romano would receive the bonus. Two

days later, Romano received all payments due for all services rendered in the second

quarter, including the bonus. Romano bases estimates of variable consideration on the

expected value of the consideration it expects to receive.

Prepare Romano’s May 30 journal entry to record the revenue earned in May, as well as

any appropriate adjustments to the revenue earned in April.

When an investor owns 20% to 50% of the voting stock of an investee company, the

investor is presumed to exercise significant influence over the investee unless there is

evidence to the contrary.

Required:

(1.) What factors could be evidence of significant influence?

(2.) What factors could be evidence of lack of significant influence?

Pension plans typically require some minimum period of employment before benefits

vest. What is the 1974 federal law governing vesting (as well as other aspects of

pensions)? What are the vesting rules?