During its first year of operations, Brown Company incurred the following product

costs:

Direct materials used in production $200,000

Direct labor $175,000

Manufacturing overhead $145,500

Brown Company’s ending Work in Process Inventory amounted to $35,000 at the end of

the year. What is the company’s cost of finished goods manufactured for the year?

A. $200,000.

B. $375,000.

C. $485,500.

D. $520,500.

All things being equal, if investors expect earnings to increase substantially from

current levels, the price/earnings ratio will:

A. Be quite low.

B. Be quite high.

C. Not change.

D. Not be affected by income expectations.

A 2-for-1 stock split:

A. Is accounted for in the same way as a 100% stock dividend.

B. Increases the number of outstanding shares of common stock, but par value per share

remains the same as before the split.

C. Is recorded by transferring the par value of additional shares from retained earnings

to the common stock account.

D. Should logically cause the market price per share to drop by approximately 50%.

Refer to the information above. Which of the following is the largest payroll-related

expense incurred by Girard?

A. Group health insurance premiums.

B. Income taxes expense.

C. The employer’s share of social security taxes.

D. Wages and salaries expense.

When net cash flow from operating activities is presented by the direct method, the

statement of cash flows is accompanied by a supplementary schedule reconciling:

A. Net cash flow from operating activities with net sales.

B. Net income with the net increase or decrease in cash and cash equivalents.

C. Net income with net cash flow from operating activities.

D. Net cash flow from operating activities shown in the statement with that which

would result from use of the indirect method.

The changes in financial statement items from a base year to following years are called:

A. Money changes.

B. Trend percentages.

C. Component percentages.

D. Ratios.

A company failed to make an adjusting entry in the prior year to accrue earned revenue.

To correct this they should:

A. Correct last year’s statement by increasing net income.

B. Correct this year’s statements with a prior period adjustment increasing beginning

retained earnings.

C. Correct this year’s statements with a prior period adjustment decreasing beginning

retained earnings.

D. Correct this year’s statements with a prior period adjustment increasing ending

retained earnings.

The par value of the common stock of a large listed corporation:

A. Tends to establish a ceiling for the market price of the stock.

B. Tends to establish a floor for the market price of the stock.

C. Represents legal capital and is not related to the market price of the stock.

D. Is increased by net income and decreased by dividends.

Capital budgeting proposals often require input from all of the following stakeholders

except:

A. Managers.

B. Employees.

C. Shareholders.

D. Directors.

Manufacturing overhead is best described as:

A. All manufacturing costs other than direct materials and direct labor.

B. All period costs associated with manufacturing operations.

C. Indirect materials and indirect labor.

D. All operating expenses other than selling expenses and general and administrative

expenses.

The contribution margin is calculated by:

A. Subtracting fixed costs from sales.

B. Subtracting variable costs from sales.

C. Subtracting fixed and variable costs from sales.

D. Subtracting common costs from sales.

During the month of January, Sundown Corporation had sales of $300,000 and a cost of

goods available for sale of $600,000. The company consistently earns a gross profit rate

of 45%. Using the gross profit method, the estimated inventory at January 31 amounts

to:

A. $135,000.

B. $435,000.

C. $165,000.

D. $465,000.

During the current year, the assets of Quality Stairs increased by $175,000 and the

liabilities decreased by $15,000. If the owners’ equity in the business is $475,000 at the

end of the year, the owners’ equity at the beginning of the year must have been:

A. $335,000.

B. $285,000.

C. $665,000.

D. $615,000.

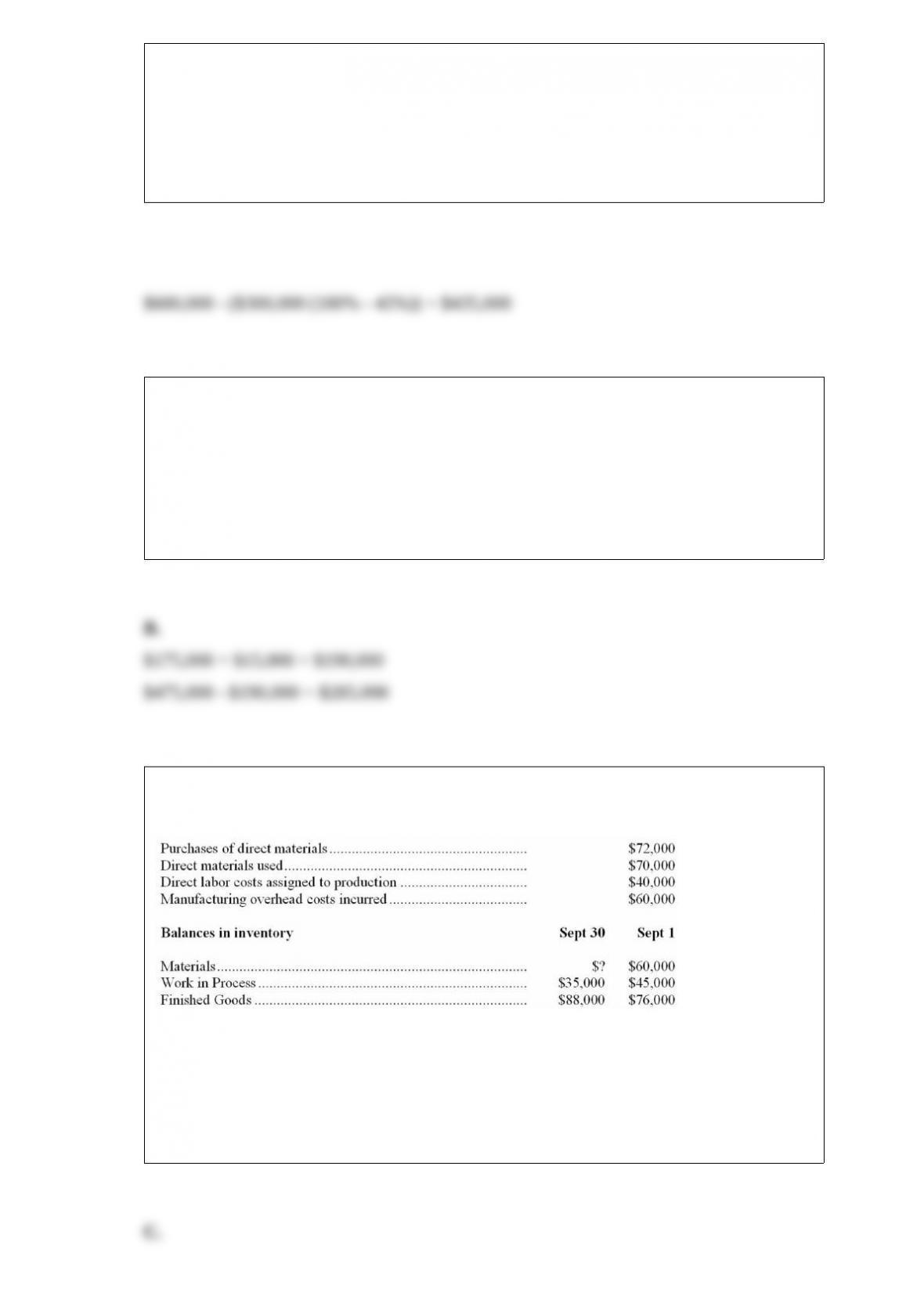

The following information has been taken from the perpetual inventory system of

Imperial Mfg. Co. for the month ended September 30:

Refer to the above data. The total amount of inventory to be included in Imperial’s

September 30th balance sheet amounts to:

A. $255,000.

B. $123,000.

C. $185,000.

D. Some other amount.

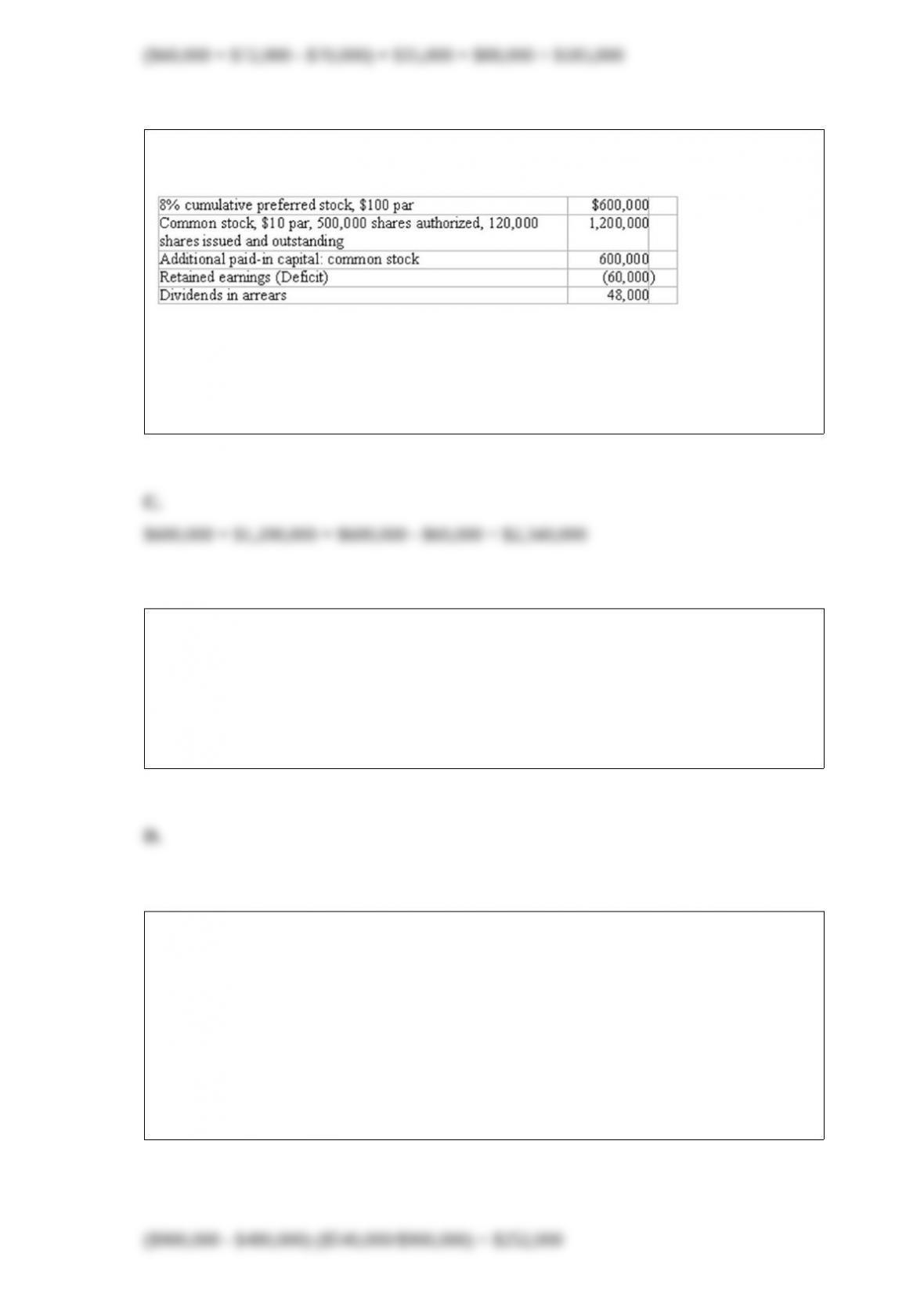

Shown below is information relating to the stockholders’ equity of Reeve Corporation

as of December 31, 2015:

Refer to the information above. Total stockholders’ equity is:

A. $2,400,000.

B. $2,460,000.

C. $2,340,000.

D. $2,292,000.

Retained Earnings represent:

A. The profits of the company.

B. The investments of the owners.

C. The profits of the company plus the investments of the owners.

D. The total earnings of the company, less the dividends distributed to the owners and

less any losses.

Garden World uses the retail method to estimate its monthly cost of goods sold and

month-end inventory. At May 31, the accounting records indicate the cost of goods

available for sale during the month (beginning inventory plus purchases) totaled

$540,000. These goods had been priced for resale at $900,000. Sales in May totaled

$480,000. The estimated inventory at May 31 is:

A. $540,000.

B. $252,000.

C. $420,000.

D. $288,000.

The adjusting entry to record interest that has accrued on a note payable to the bank will

cause an immediate:

A. Increase in liabilities and reduction in net income.

B. Decrease in liabilities and reduction in net income.

C. Decrease in assets and reduction in net income.

D. Increase in assets and increase in net income.

If a company wanted to evaluate the manager’s ability to control costs, the company

would probably look at the:

A. Performance margin.

B. Responsibility margin.

C. Contribution margin.

D. Segment margin.

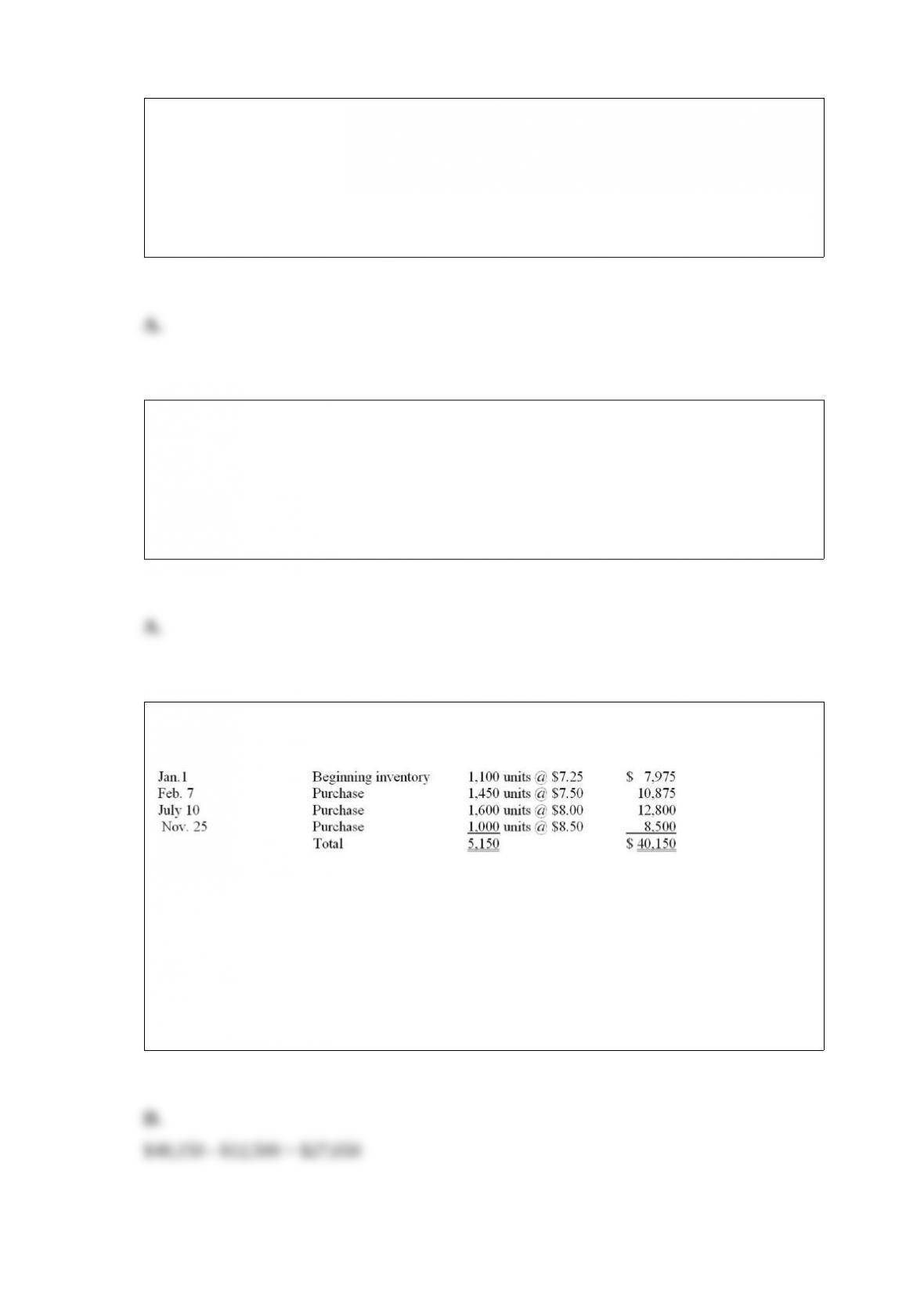

Harding Systems, Inc. uses a periodic inventory system. The purchases of a particular

product during the year are shown below:

At December 31 the ending inventory consisted of 1,500 units.

Refer to the information above. Compute the cost of goods sold for the current year

based on the FIFO method of inventory valuation.

A. $12,500.

B. $29,175.

C. $10,975.

D. $27,650.

Which of the following accounts will be closed to Income Summary?

A. Prepaid Expenses.

B. Unearned Revenue.

C. Dividends.

D. Depreciation Expense.

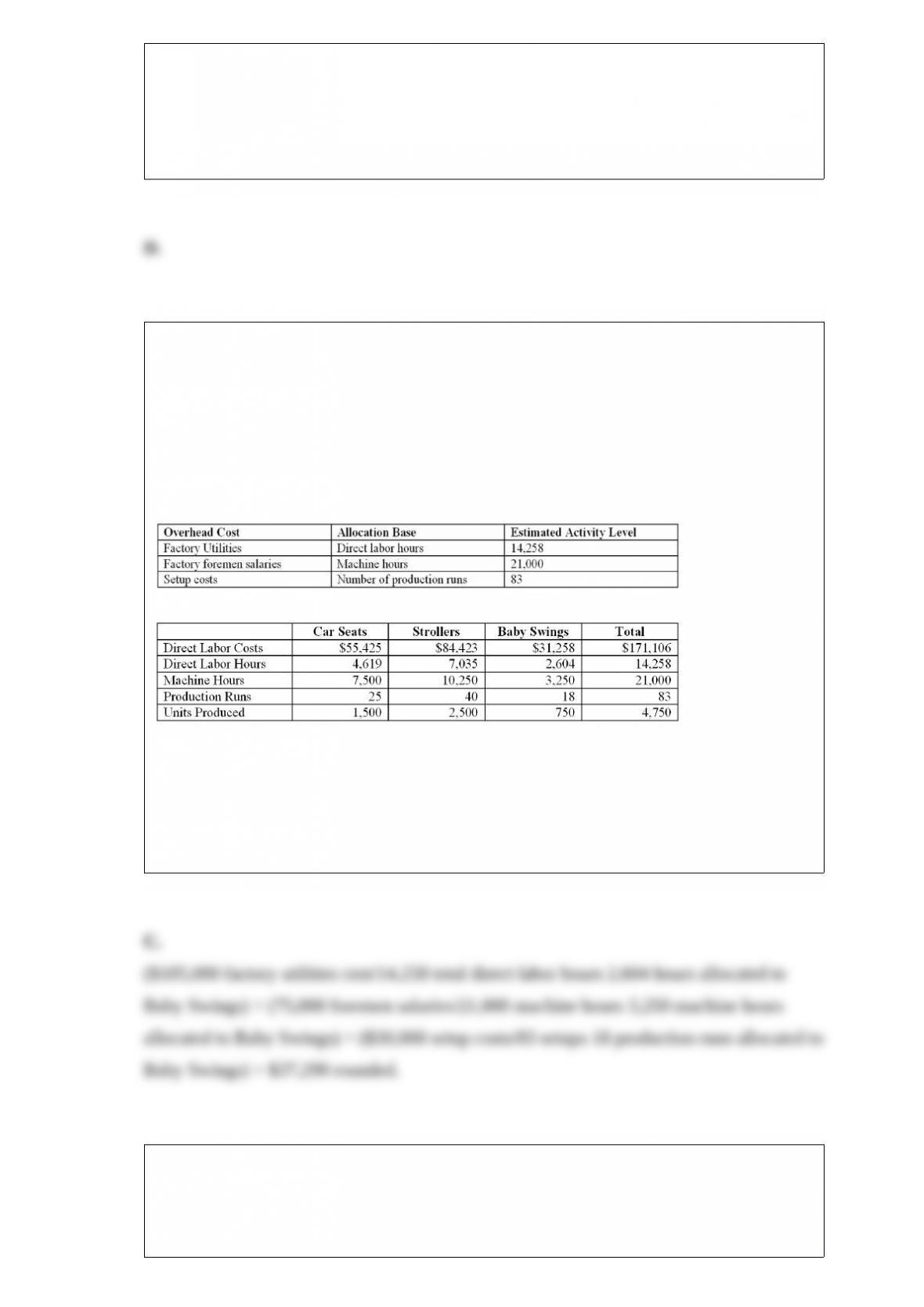

Starbright manufactures children car seats, strollers, and baby swings. Starbright’s

manufacturing costs are budgeted as follows:

Factory utilities $105,000

Factory foremen salaries $75,000

Machinery setup costs $30,000

Total manufacturing overhead $210,000

The company uses activity-based costing to allocate its manufacturing overhead costs to

products based on the following schedule:

During the current month, the following levels of activities were incurred:

What are the total manufacturing overhead costs allocated to the Baby Swings for the

current month?

A. $69,837.

B. $102,873.

C. $37,290.

D. $210,000.

From the viewpoint of stockholders or potential investors, which of the following cash

flow measurements would be of least importance?

A. The dollar amount of net cash flow from operating activities for the current year.

B. The trend in net cash flow from operating activities from year to year.

C. The corporation’s free cash flow for the current year.

D. The dollar amount of overall increase or decrease in cash for the current year.

After preparing the financial statements for 2015, the accountant for the Dawson

Corporation discovered that a prior period adjustment had been omitted from the 2013

financial statements. Which of the following is most likely to require correction as a

result of this oversight?

A. Earnings per share as originally computed.

B. Net income for 2015 as originally reported.

C. Ending retained earnings at December 31, 2015.

D. Extraordinary items as originally reported.

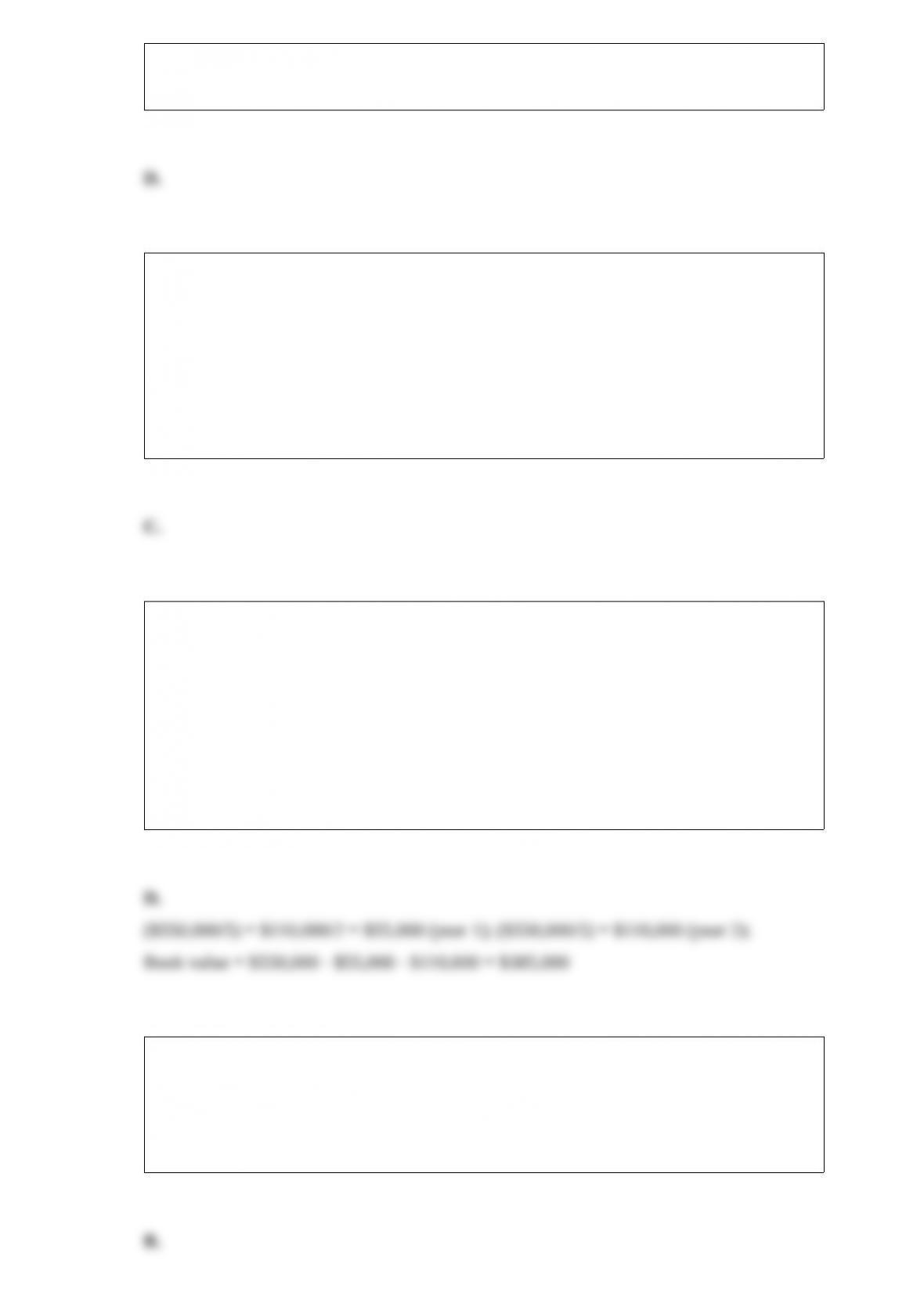

On March 2, 2014, Glen Industries purchased a fleet of automobiles at a cost of

$550,000. The cars are to be depreciated by the straight-line method over five years

with no salvage value. Glen uses the half-year convention to compute depreciation for

fractional periods. The book value of the fleet of automobiles at December 31, 2015,

will be:

A. $165,000.

B. $330,000.

C. $495,000.

D. $385,000.

Net income from the Income Statement appears on:

A. The Balance Sheet.

B. The Retained Earnings Statement.

C. Neither the Balance Sheet nor the Retained Earnings Statement.

D. Both the Balance Sheet and the Retained Earnings Statement.

Sultan Company produces a single product. The selling price is $50 per unit, and

variable costs amount to $20 per unit. Sultan’s fixed costs per month total $80,000.

Refer to the information above. What is the monthly sales volume in dollars necessary

to break-even? (Rounded)

A. $320,000.

B. $106,667.

C. $200,000.

D. $133,333.

An annual report filed with the Securities and Exchange Commission must include a

section called “Management Discussion and Analysis” (MD&A).

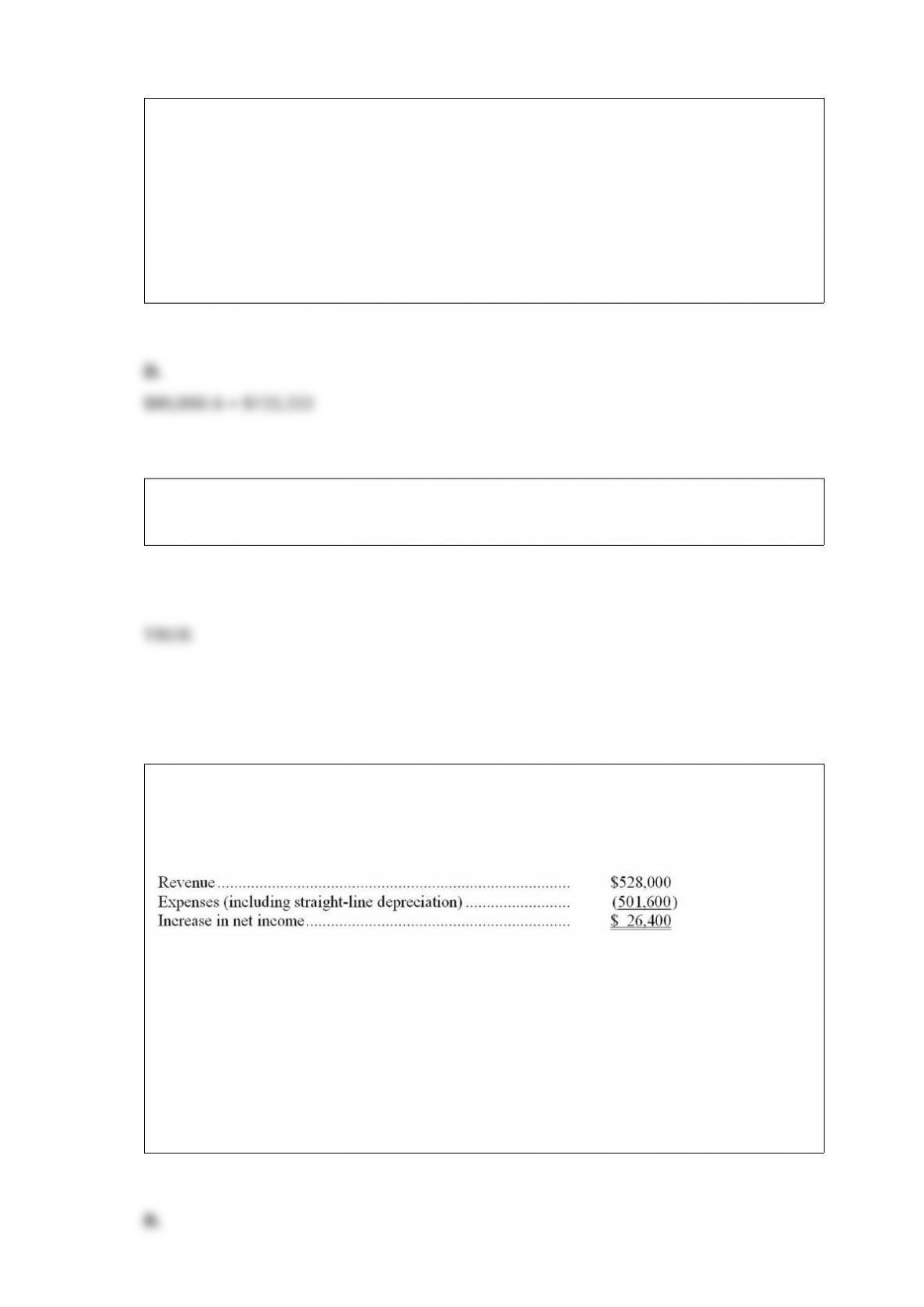

Helicopter Gear is planning to expand its product line, which requires investment of

$475,200 in special-purpose machinery. The machinery has a useful life of six years

and no salvage value. The estimated annual results of offering the new products are as

follows:

All revenue from the new products and all expenses (except depreciation) will be

received or paid in cash in the same period as recognized for accounting purposes.

Refer to the information above. Compute the net present value of this proposed

investment, using a discount rate of 12%. (An annuity table shows that the present

value of $1 received annually for six years, discounted at 12%, is 4.111.)

A. ($105,600).

B. ($41,078).

C. $369,600.

D. $434,121.

On October 12, 2014, Neptune Corporation invested $700,000 in short-term

available-for-sale marketable securities. The market value of this investment was

$730,000 at December 31, 2014, but had slipped to $725,000 by December 31, 2015.

Refer to the information above. Assuming Neptune does not sell this investment, the

fair value accounting adjustment necessary at December 31, 2015, includes:

A. A $5,000 debit to Unrealized Holding Gain on Investments.

B. A $25,000 credit to Unrealized Holding Gain on Investments.

C. A $5,000 debit to Investments in Marketable Securities.

D. A $725,000 debit to Investments in Marketable Securities.

In a periodic inventory system, recording a sale on account involves debiting which of

the following accounts?

A. Only Accounts Receivable.

B. Accounts Receivable and Inventory.

C. Accounts Receivable and Cost of Goods Sold.

D. Accounts Receivable, Cost of Goods Sold, and Inventory.

During the year 2015, Tosco Corporation suffered an $800,000 loss when its factory

was destroyed in a flood. Assuming the corporate income tax rate is 36%, what amount

will Tosco report as an extraordinary loss on its income statement for 2015? Assume

floods are not common in this area.

A. $800,000.

B. $512,000.

C. $288,000.

D. Nothing, since this does not qualify as an extraordinary item.

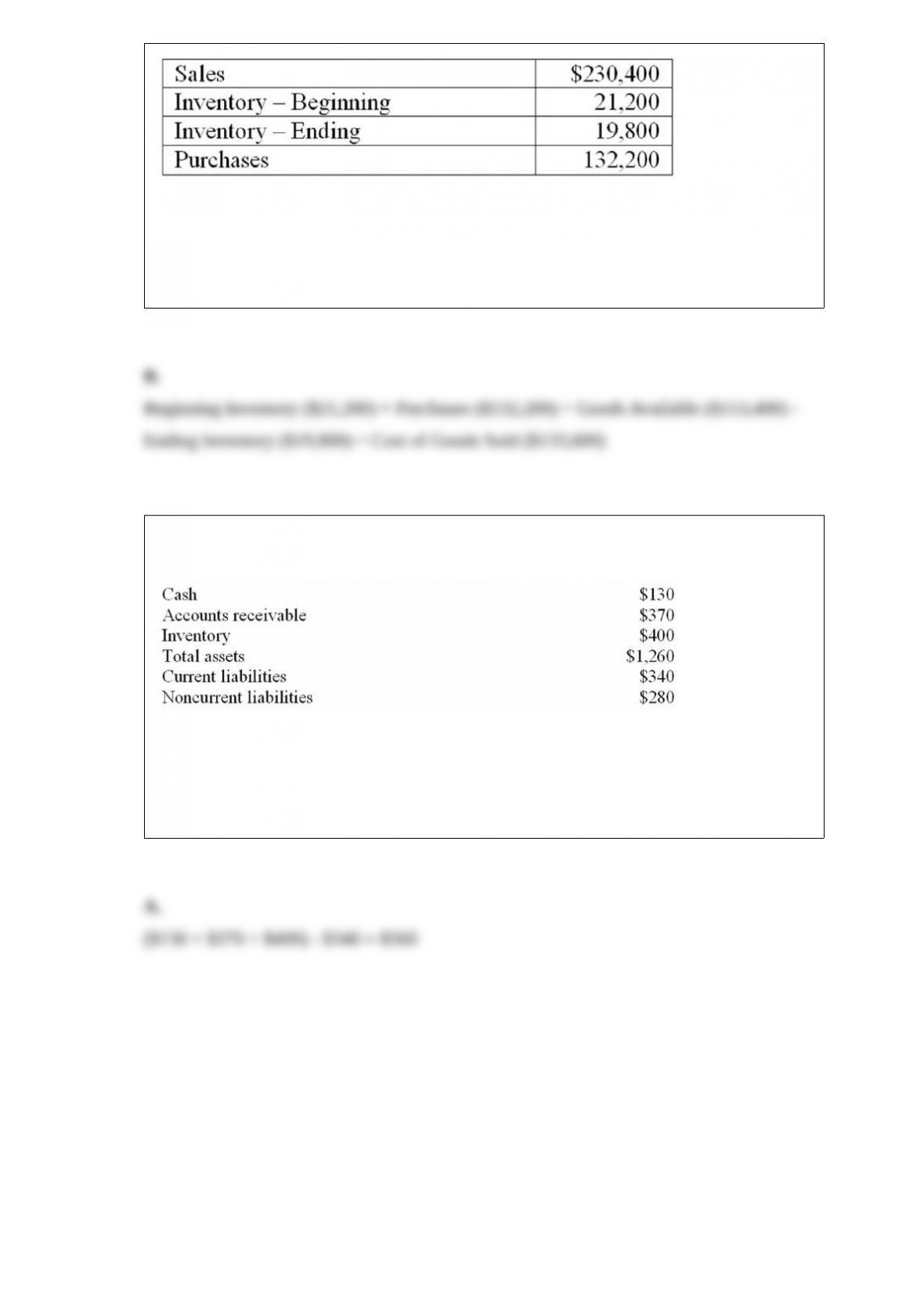

Bremmer uses a periodic inventory system and the following information is available:

Refer to the information above. What is the cost of goods sold?

A. $96,800.

B. $133,600.

C. $132,200.

D. $230,400.

Shown below are selected data from the balance sheet of Bill’s Auto Parts, a retail store

(dollar amounts are in thousands):

Refer to the information above. Working capital equals:

A. $560,000.

B. $530,000.

C. $270,000.

D. $900,000.