1) Bonds issued by a company remain on their books as a liability, but are considered

constructively retired when

A) the company borrows money from unaffiliated entities to re-purchase its own bonds

at a gain

B) The company borrows money from an affiliate to re-purchase its own bonds at a

gain

C) The company’s parent or subsidiary purchases the bonds from outside entities

D) The company borrows money from an affiliate to repurchase its own bonds at a gain

or at a loss

2) In 2011, Parla Corporation sold land to its subsidiary, Sidd Corporation, for $38,000.

It had a book value of $24,000. In the next year, Sidd sold the land for $41,000 to an

unaffiliated firm.

The 2011 unrealized gain from the intercompany sale

A) should be recognized in consolidation in 2011 by a working paper entry

B) should be eliminated from consolidated net income by a working paper entry that

credits land for $14,000

C) should be eliminated from consolidated net income by a working paper entry that

debits land for $14,000

D) should be eliminated from consolidated net income by a working paper entry that

credits gain on sale of land for $14,000

3) The town of Mayberry receives a gift of $500,000 in bonds. The contributor instructs

that the principal should remain intact, but the annual interest income of $50,000 can be

used for the maintenance of the zoo animals.

When the interest income of $50,000 is received, what account should be credited?

A) Other Financing Sources

B) Other Financing Uses

C) Deferred Revenue

D) Revenue

4) Voluntary health and welfare organizations (VHWO) measure contributions at fair

value unless

A) fair value is less than the original cost of the item

B) the contributed item is not intended to be re-sold by the VHWO

C) fair value cannot be reasonably determined

D) the contributions are not in cash or cash equivalents

5) On January 1, 2011, Pardy Corporation acquired a 70% interest in the common stock

of Salter Corporation for $7,000,000 when Salter’s stockholders’ equity was as follows:

10% cumulative, nonparticipating preferred stock,

$100 par, with a $105 liquidation preference,

callable at $110$ 1,000,000

Common stock, $10 par value6,000,000

Additional paid-in capital1,500,000

Retained earnings2,500,000

Total stockholders’ equity$11,000,000

There were no preferred dividends in arrears on January 1, 2011 . There are no book

value/fair value differentials.

Assume Salter’s net income for 2011 is $220,000. No dividends are declared or paid in

2011 . What is the change in Pardy’s Investment in Salter for the year ending December

31, 2011?

A) $ 84,000

B) $119,000

C) $154,000

D) $189,000

6) On December 31, 2010, Giant Corporation’s Investment in Penguin Corporation

account had a balance of $500,000. The balance consisted of 80% of Penguin’s

$625,000 stockholders’ equity on that date. Giant owns 80% of Penguin. On January 2,

2011, Penguin increased its outstanding common stock from 15,000 to 18,000 shares.

Assume that Penguin sold the additional 3,000 shares directly to Giant for $150,000 on

January 2, 2011. Giant’s percentage ownership in Penguin immediately after the

purchase of the additional stock is

A) 66-2/3%

B) 80%

C) 83-1/3%

D) 86-2/3%

7) Palomba Corporation allocates consolidated income taxes to its 90%-owned

subsidiary using the percentage allocation method. Under this method, consolidated

income tax expense will be allocated to a subsidiary

A) on the basis of the agreement between the parent and subsidiary

B) on the basis of the subsidiary’s pretax income as a percentage of consolidated pretax

income

C) on the basis of the income taxes remitted to the IRS

D) 90% to the subsidiary

8) According to the segmented markets theory of the term structure

A) bonds of one maturity are close substitutes for bonds of other maturities, therefore,

interest rates on bonds of different maturities move together over time

B) the interest rate for each maturity bond is determined by supply and demand for that

maturity bond

C) investors’ strong preferences for short-term relative to long-term bonds explains why

yield curves typically slope downward

D) because of the positive term premium, the yield curve will not be observed to be

downward-sloping

9) On December 5, 2010, Unca Corporation, a U.S. firm, bought inventory items from

Skagerrak Corporation of Norway for 1,000,000 Norwegian kroner when the spot rate

for kroner was $0.166. The purchase was denominated in kroner. At Unca’s fiscal year

end, December 31, 2010, the spot rate was $0.171. On January 4, 2011, Unca purchased

1,000,000 kroner for $167,500 and paid the invoice. How much gain or (loss) did Unca

report in its 2010 and 2011 income statements, respectively?

A) $(5,000) and $1,500

B) $0 and ($1,500)

C) ($5,000) and $3,500

D) $0 and ($3,500)

10) Match the following fund balance descriptions for a General Fund with the proper

classification for a fund balance. Each classification may be used more than once.

A.Nonspendable Fund Balance

B.Restricted Fund Balance

C.Committed Fund Balance

D.Assigned Fund Balance

E.Unassigned Fund Balance

_____1> Amounts can only be spent for the specific purposes determined by a formal

action of the government’s highest level of decision-making authority.

_____2> Amounts can only be spent for the specific purposes stipulated by constitution,

external resource provider or enabling legislation.

_____3> Residual classification of funds for the General Fund.

_____4> Dollar amount of Ending Inventory.

_____5> Amounts intended to be used by the government for specific purposes but do

not meet the criteria of restricted or committed.

_____6> Dollar amount of endowment principal

11) Under the Uniform Partnership Act, loans made by a partner to the partnership are

treated as

A) liabilities to the partnership for which interest shall be paid from the date of the

advance

B) advances to the partnership that are carried in the partners’ capital accounts

C) Accounts Payable of the partnership for which interest is paid

D) advances to the partnership for which interest does not have to be paid

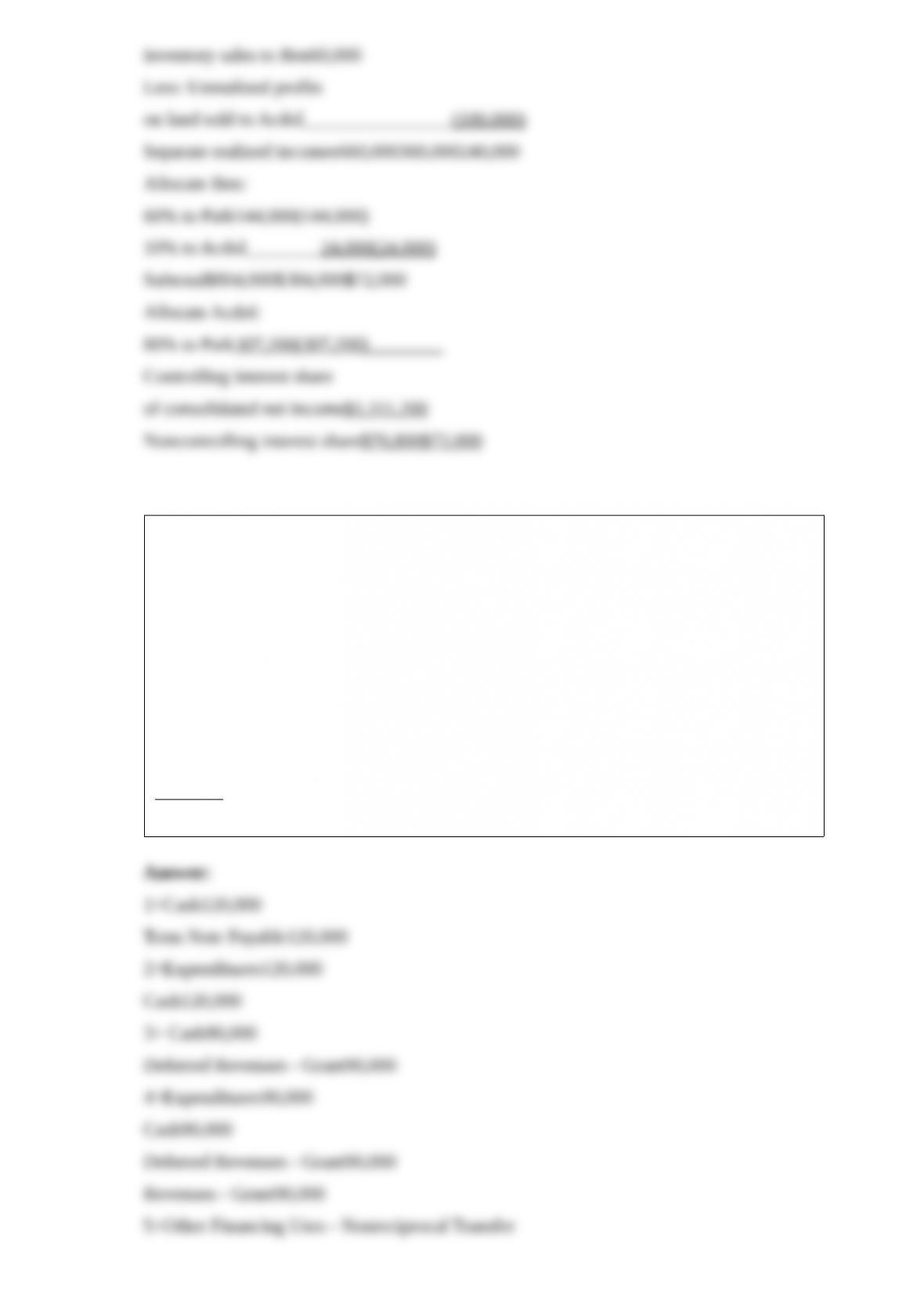

12) The executor or administrator of a will is required to prepare and file an inventory

of property owned by the deceased within what time period?

A) One month of appointment

B) Two months of appointment

C) Three months of appointment

D) 45 days of appointment

13) If the partnership agreement provides a formula for the computation of a bonus to

the partners, the bonus would be computed

A) next to last, because the final allocation is the distribution of the profit residual

B) before income tax allocations are made

C) after the salary and interest allocations are made

D) in any manner agreed to by the partners in the partnership agreement

14) John Doe’s will states that all assets he had should be transferred to a trust to cover

living expenses for his spouse, who he feels will not be able to handle her own financial

affairs without advice and supervision. Upon his spouse’s passing, the trust will be

converted to cash and distributed to their only daughter, Jane. The probate court already

ruled on which assets could be excluded from the estate, and all tax issues were

addressed, leaving the following inventory of assets from the estate:

Required:

Prepare the journal entry for the creation of the trust.

15) Based upon the flow information provided below for the year ending December 31,

2011, prepare a cash flow statement for the Downtown City Motor Pool, an internal

service fund.

Cash received from customers$830,000

Cash received from General Fund (noncapital loan)20,000

Interest revenue received1,000

Cash received from short-term note payable (not used for capital assets)40,000

Payments to employees450,000

Payments to suppliers250,000

Cash paid to the General Fund – noncapital loan65,000

Payments for capital improvements60,000

Interest paid on short-term note payable above2,000

Principal paid on capital debt50,000

Interest paid on capital debt5,000

Unrestricted Cash (and cash equivalents), January 1, 201113,000

16) On January 1, 2010, Palgan, Co. purchased 75% of the outstanding voting common

stock of Somil, Inc., for $1,500,000. The book value of Somil’s net equity on that date

was $2,000,000. Book values were equal to fair values except as follows:

BookFair

Assets & LiabilitiesValuesValues

Inventory$ 225,000$ 253,000

Building850,000750,000

Note payable320,000304,000

Required:

Prepare a schedule to allocate any excess purchase cost to specific assets and liabilities.

17) Paik Corporation owns 80% of Acdol Corporation and 60% of Ben Corporation.

Acdol Corporation owns 10% of Ben Corporation. All subsidiary investments were

acquired at book value. There are no fair value/book value differentials associated with

each investment. Separate net incomes (excluding investment income) of the affiliated

companies for 2011 are:

Paik:$600,000 which includes $60,000 unrealized losses on inventory items sold to Ben

Acdol:$360,000

Ben:$340,000 which includes $100,000 unrealized profit on land sold to Acdol

Required:

Determine controlling interest share of consolidated net income and noncontrolling

interest shares for Paik Corporation and Subsidiaries for 2011 .

18) The City of Electri entered the following transactions during 2011:

1>Borrowed $120,000 for a six-month term, to be paid upon receipt of property tax

payments which were previously billed.

2>Used the funds borrowed to purchase a new fire truck. The truck is expected to have

a 15-year useful life, and a $5,000 residual value.

3>Received $90,000 cash from a state grant. Funds are restricted for the purchase of a

second fire truck.

4>Used the grant funds received to purchase a second fire truck. The truck is expected

to have a 15-year useful life, and a $5,000 residual value.

5>Nonreciprocal transfer of $50,000 to the Debt Service Fund to be used toward

repayment of the note.

Required:

Prepare the journal entries in the General Fund for the transactions.

19) Pittle Corporation acquired a 80% interest in Seel Corporation at a cost equal to

80% of the book value of Seel’s net assets several years ago. At the time of purchase,

the fair value and book value of Seel’s assets and liabilities were equal. Pittle purchases

its entire inventory from Seel at 150% of Seel’s cost. During 2011, Seel sold $490,000

of merchandise to Pittle. Pittle’s beginning and ending inventories for 2011 were

$72,000 and $66,000, respectively. Income statement information for both companies

for 2011 is as follows:

PittleSeel

Sales Revenue$ 820,000$440,000

Investment income from Sitt145,600

Cost of Goods Sold(460,000)(165,000)

Expenses(120,000)(95,000)

Net Income$ 385,600$ 180,000

Required:

Prepare a consolidated income statement for Pittle Corporation and Subsidiary for

2011 .

20) On January 1, 2011, Jeff Company acquired a 90% interest in Marian Company for

$198,000 cash. On January 1, 2011, Marian Company had the following assets and

liabilities:

Book ValueFair Value

Cash$5,000$5,000

Accounts Receivable30,00035,000

Inventory40,00050,000

Plant Assets60,00080,000

Total Assets$135,000$170,000

Liabilities$25,000$25,000

Capital Stock100,000

Retained Earnings10,000

Total Liabilities &

Stockholders’ Equity $135,000

Push-down accounting is used for the acquisition.

Required:

1> Assume both companies use the entity theory. Prepare the elimination entry(ies) on

consolidating work papers on January 1, 2011 .

2> Assume both companies use the parent company theory. Prepare the elimination

entry(ies) on consolidating work papers on January 1, 2011 .

21) Parkview Holdings owns 70% of Skyline Corporation. On January 1, 2011, Skyline

acquires half of the $2,000,000 of bonds originally issued by Parkview on January 1,

2006 . The bonds were issued at a stated rate of 5% for 10 years, for $1,920,000.

Skyline purchased them for $950,000. Assume that both Parkview and Skyline will use

the straight-line method for any bond-related amortization. Annual interest is paid on

December 31 .

Required: Prepare the entries required for the consolidating worksheet for the years

ended December 31, 2006 through December 31, 2016 .

22) Pacini Corporation owns an 80% interest in Abdoo Corporation, acquired on

January 1, 2010 for $700,000 when Abdoo’s stockholders’ equity consisted of $600,000

of Capital Stock and $200,000 of Retained Earnings.

Abdoo Corporation acquired a 60% interest in Bach Corporation on July 1, 2010 for

$180,000 when Bach had Capital Stock of $200,000 and Retained Earnings of $50,000.

On January 1, 2011, Abdoo acquired a 70% interest in Cabo Corporation for $270,000

when Cabo had Capital Stock of $250,000 and Retained Earnings of $100,000.

No change in outstanding stock of any of the affiliated companies has occurred since

the investments were made. All cost-book value differentials are goodwill. There are no

fair value/book value differentials. The stockholders’ equity section of the separate

balance sheets of Abdoo, Bach, and Cabo at December 31, 2011 are as follows:

AbdooBachCabo

Capital Stock$600,000$200,000$250,000

Retained Earnings280,000140,000130,000

Total stockholders’ equity$880,000$340,000$380,000

Required:

1> Compute the amount at which goodwill should be shown in the consolidated balance

sheet of Pacini Corporation and Subsidiaries at December 31, 2011 .

2> Pacini and Abdoo have applied the equity method correctly. Determine the balances

of the three investment accounts at December 31, 2011 .

23) The City’s municipal golf course had the following transactions.

1>Received a beautification(operating) grant from the state for $600,000. Received

cash of $600,000.

2>Incurred and paid qualifying expenses under the state grant program in (1) above of

$280,000.

3>Incurred and paid construction costs on an uncompleted clubhouse for $1,200,000.

4>Received $1,000,000 cash from a grant to assist with construction costs for the

clubhouse.

Required:

Given that the golf course is operated based on user fees for upkeep, prepare the

necessary journal entries for each of these transactions.