A decrease in cash dividends payable means that dividends declared were less than

dividends paid.

Dilutive convertible bonds affect both the numerator and the denominator in computing

diluted EPS.

Comprehensive income is the total change in shareholders’ equity that occurred during

the period.

If an investment is accounted for under the equity method, the investor reduces

investment income and the investment account for amortization of goodwill acquired in

the investment.

If the seller is a principal, the seller typically is not vulnerable to risks associated with

delivering the product or service.

The interest expense on an installment note decreases with each periodic payment.

The relative fair values are used to determine the valuation of individual assets acquired

in a lump-sum purchase.

Compensation expense must be adjusted during the service period to reflect changes in

the fair value of options caused by changes in the market price of the underlying

shares.

Cost of goods on consignment is included in the consignee’s inventory until sold.

If the seller is a principal, the seller has primary responsibility for delivering a product

or service.

Depreciation:

a. Is always considered a period cost.

b. Could be a product cost or a period cost depending on the use of the asset.

c. Is usually based on the declining-balance method.

d. Per books is usually higher than MACRS in the early years of an asset’s life.

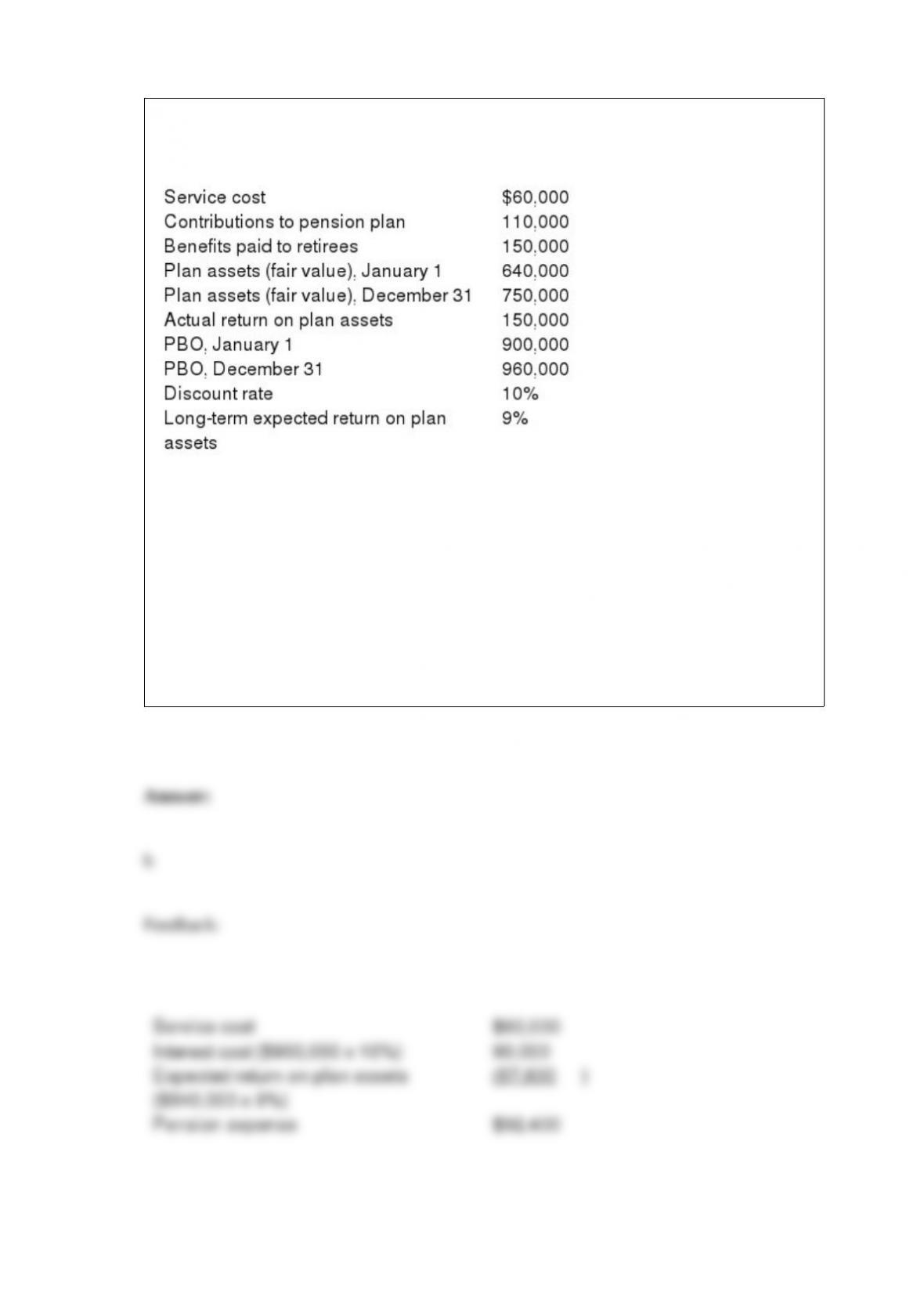

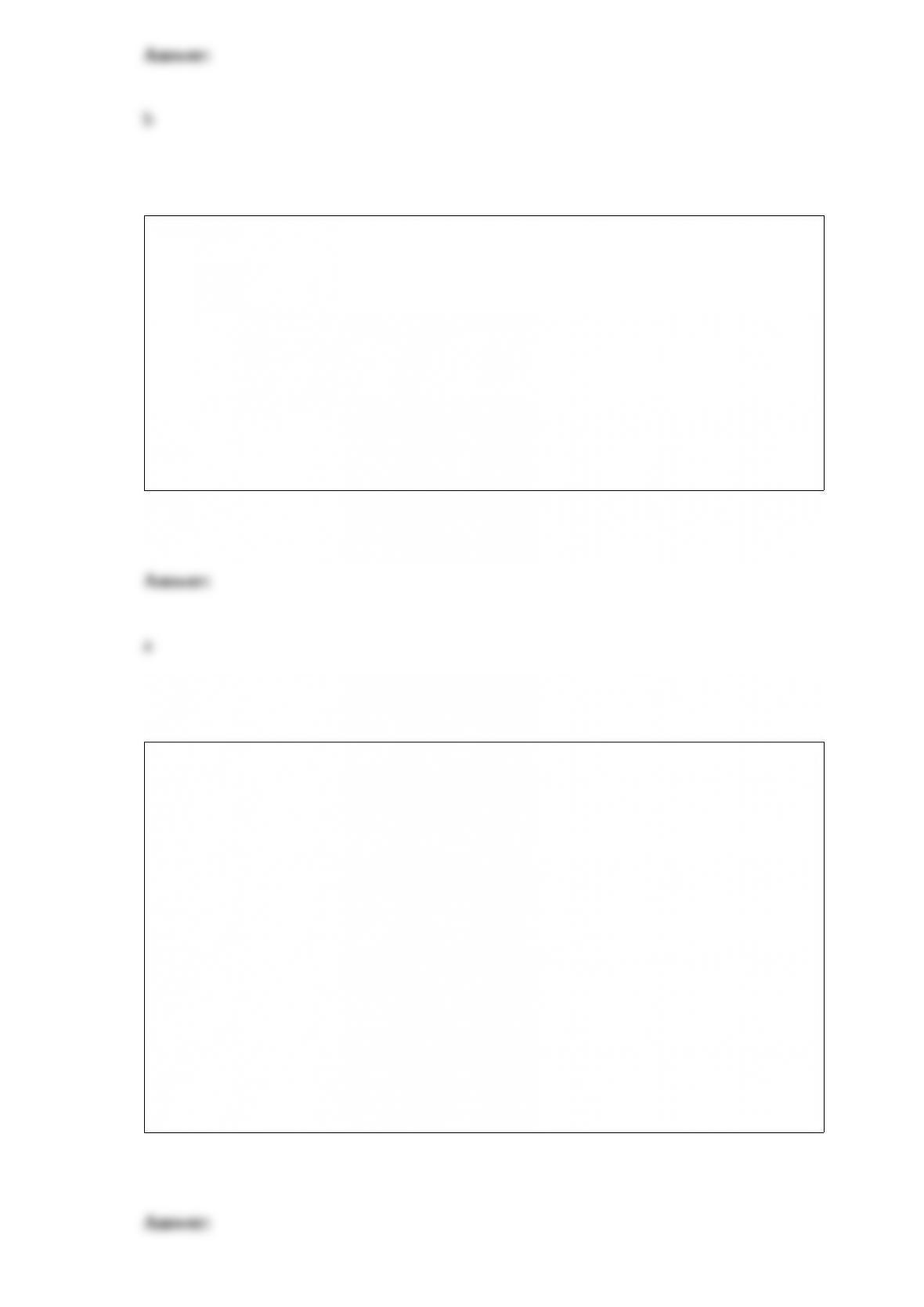

The following information is related to the defined benefit pension plan of Dreamworld

Company for the year:

Assuming no other relevant data exist, what is the pension expense for the year?

a. $190,000.

b. $ 92,400.

c. $ 60,000.

d. $170,000.

Kellogg Company and its subsidiaries are engaged in the manufacture and marketing of

ready-to-eat cereal and convenience foods. In its annual report to shareholders, Kellogg

disclosed the following:

DISPOSITIONS

Last year, the Company sold certain assets and liabilities of the Lender’s Bagels

business to Aurora Foods Inc. for $275 million in cash. As a result of this transaction,

the Company recorded a pretax charge of $178.9 million ($119.3 million after tax or

$.29 per share). This charge included approximately $57 million for disposal of other

assets associated with the Lender’s business, which were not purchased by Aurora.

Disposal of these other assets was completed during the current year. The original

reserve of $57 million exceeded actual losses from asset sales and related disposal costs

by approximately $9 million. This amount was recorded as a credit to other income

(expense), net during the current year.

Required:

Explain how the Kellogg transactions described could be interpreted as an example of

earnings management.

Hawk Corporation purchased 10,000 shares of Diamond Corporation stock in 2013 for

$50 per share and classified the investment as securities available for sale. Diamond’s

market value was $60 per share on December 31, 2014, and $65 on December 31, 2015.

During 2016, Hawk sold all of its Diamond stock at $70 per share. In its 2016 income

statement, Hawk would report:

a. A gain of $ 50,000.

b. A gain of $150,000.

c. A gain of $200,000

d. A gain of $300,000.

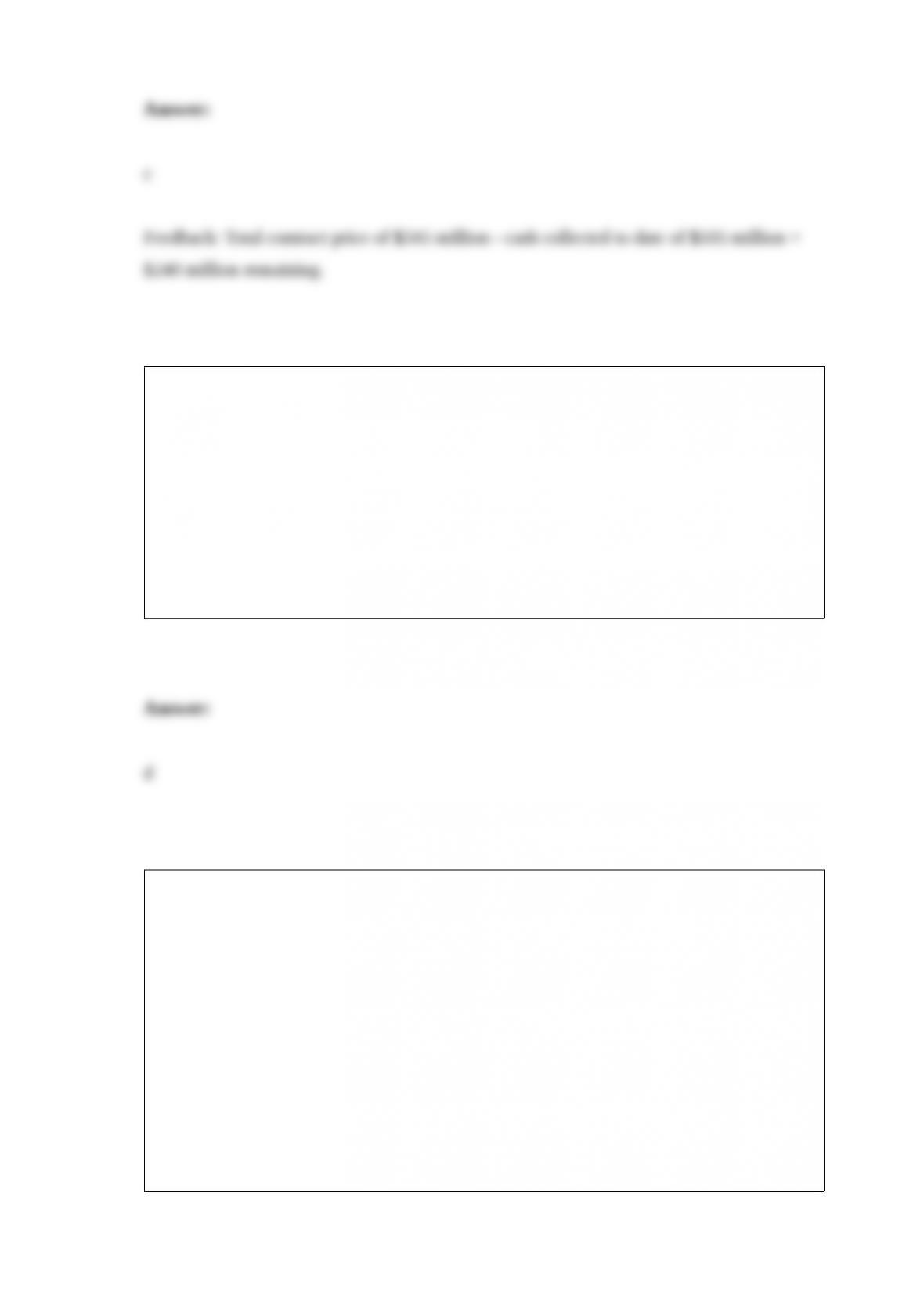

Lake Co. receives nonrefundable advance payments with special orders for containers

constructed to customer specifications. Related information for 2016 is as follows ($ in

millions):

What amount should Lake report as a current liability for advances from customers in

its Dec. 31, 2016, balance sheet?

a. $0.

b. $80.

c. $125.

d. $170.

On June 1, 2016, Emmet Property Management entered into a 2-year contract to

oversee leasing and maintenance for an apartment building. The contract starts on July

1, 2016. Under the terms of the contract, Emmet will be paid a fixed fee of $50,000 per

year and will receive an additional 15% of the fixed fee at the end of each year provided

that building occupancy exceeds 90%. Emmet estimates a 30% chance it will exceed

the occupancy threshold, and concludes the revenue recognition over time is

appropriate for this contract.

Assume that Emmet accrues revenue each month, and estimates variable consideration

as the most likely amount. On November 1, Emmet revises its estimate of the chance

the building will exceed the 90% occupancy threshold to a 70% chance. What is the

total amount of revenue Emmet should recognize on this contract in November of

2016?

a. $3,125

b. $4,167

c. $4,792

d. $7,291

Hot Springs Marine borrowed $20 million cash on December 1, 2016, to provide

working capital for year-end inventory. Hot Springs Marine issued a 4-month, 9%

promissory note to Third Bank under a prearranged short-term financing arrangement.

Interest on the note was payable at maturity. Each firm’s fiscal period is the calendar

year. Required:

1> Prepare the journal entries to record (a) the issuance of the note by Hot Springs

Marine and (b) Third Bank’s receivable on December 1, 2016.

2> Prepare the journal entries by both firms to record all subsequent events related to

the note through March 31, 2017.

3> Suppose the face amount of the note was adjusted to include interest (a

noninterest-bearing note) and 9% is the bank’s stated “discount rate.” Prepare the

journal entries to record the issuance of the noninterest-bearing note by Hot Springs

Marine on December 1, 2016. What would be the effective interest rate?

For a bond issue that sells for more than the bond face amount, the effective interest

rate is:

a. The rate printed on the face of the bond.

b. The Wall Street Journal prime rate.

c. More than the rate stated on the face of the bond.

d. Less than the rate stated on the face of the bond.

Which of the following statements is true as to GAAP regarding accounting for income

taxes, and its use of the asset and liability approach?

a. Considerable flexibility is permitted in the balance sheet classification of deferred tax

amounts.

b. The approach recognizes the time value of money.

c. The approach is consistent with a balance sheet emphasis of U.S. GAAP and the

International Financial Reporting Standards (IFRS).

d. The approach is consistent with cash basis accounting.

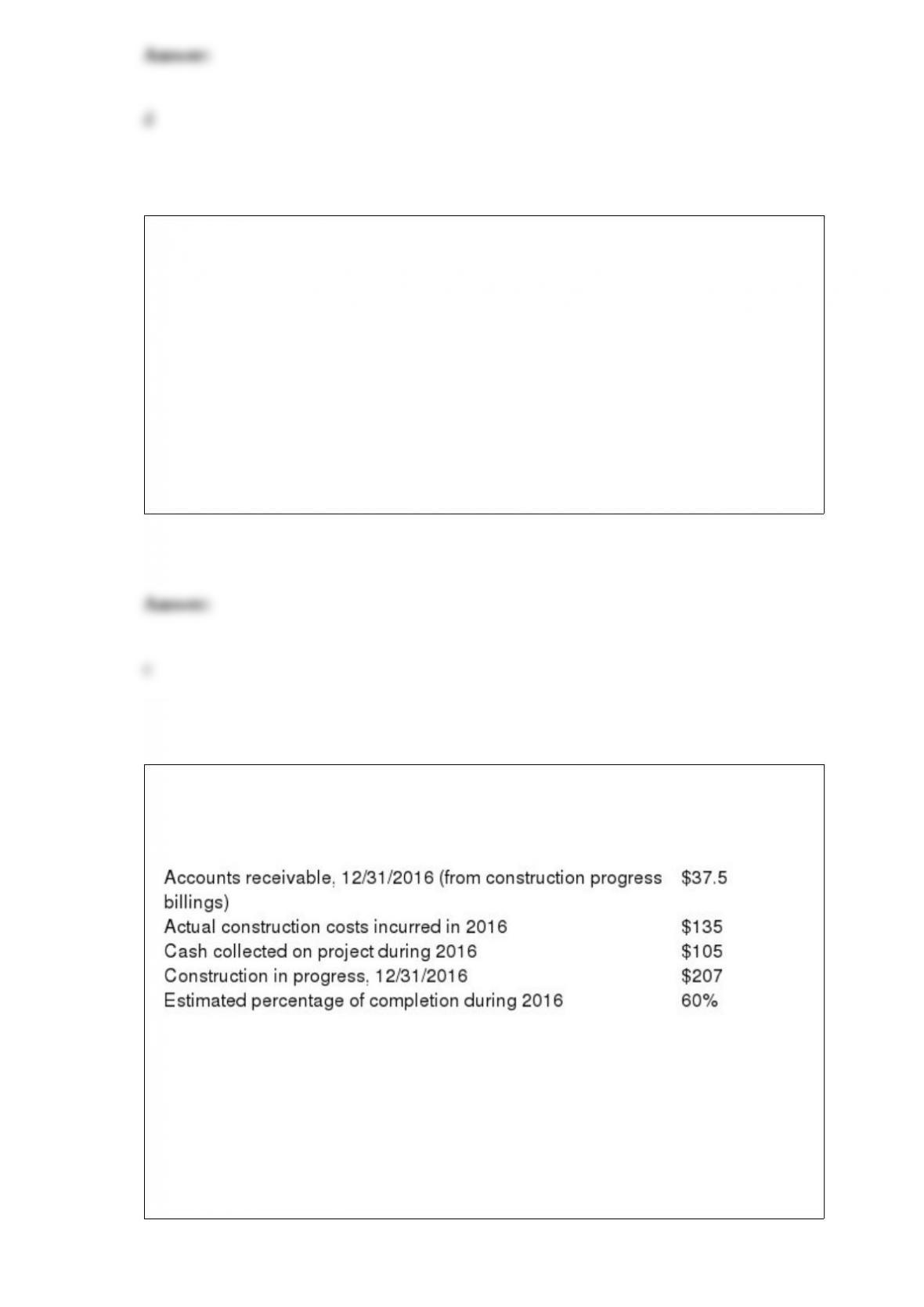

In 2016, Cupid Construction Co. (CCC) began work on a two-year fixed price contract

project. CCC recognizes revenue over time according to percentage of completion for

this contract, and provides the following information (dollars in millions):

How much cash remains to be collected by CCC on the project?

a. $70 million.

b. $202.5 million.

c. $240 million.

d. Cannot be determined from the given information.

The cost recovery method of accounting for long-term construction contracts under

IFRS is sometimes referred to as the:

a. “Sales-neutral approach.”

b. “Completed contract method.”

c. “Multi-step approach.”

d. “Zero profit method.”

If the fair value of a held-to-maturity investment declines for a reason that is viewed as

“other than temporary” because the company intends to sell the investment:

a. The investment is not written down to fair value.

b. The investment is written down to fair value, and the entire impairment loss is

recognized in net income.

c. The investment is written down to fair value, and the entire impairment loss is

recognized in accumulated other comprehensive income.

. d. The investment is treated the same way it would be treated if the decline in fair

value was viewed as temporary.

When preparing the statement of cash flows using the indirect method for determining

net cash flows from operating activities, depreciation is added to net income because:

a. It was deducted as an expense on the income statement, but does not require cash.

b. It was deducted as an expense on the income statement and affects the amount of

cash.

c. It is a significant portion of the year’s expenses.

d. It represents a source or inflow of cash.

If the fair value of a debt investment that is classified as an available-for-sale

investment declines for a reason that is viewed as “other than temporary” because it is

viewed as “more likely than not” that the investor will be required to sell the investment

prior to recovering the amortized cost of the investment less any credit losses arising in

the current year:

a. The investment is not written down to fair value.

b. The investment is written down to fair value, and the impairment loss is recognized

in net income.

c. The investment is written down to fair value, and the impairment loss is recognized

in accumulated other comprehensive income.

. d. The investment is written down to fair value, and only the noncredit loss is included

in net income.

Like other assets, the cost of a leasehold improvement is allocated as depreciation

expense over its useful life to the lessee, which will be:

a. The shorter of the physical life of the asset or the lease term.

b. The physical life of the asset.

c. The lease term.

d. A time period determined by management.

In testing for recoverability of property, plant, and equipment, an impairment loss is

required if the:

a. Asset’s book value exceeds the undiscounted sum of expected future cash flows.

b. Undiscounted sum of its expected future cash flows exceeds the asset’s book value.

c. Present value of expected future cash flows exceeds its book value.

d. All of these answer choices are incorrect.

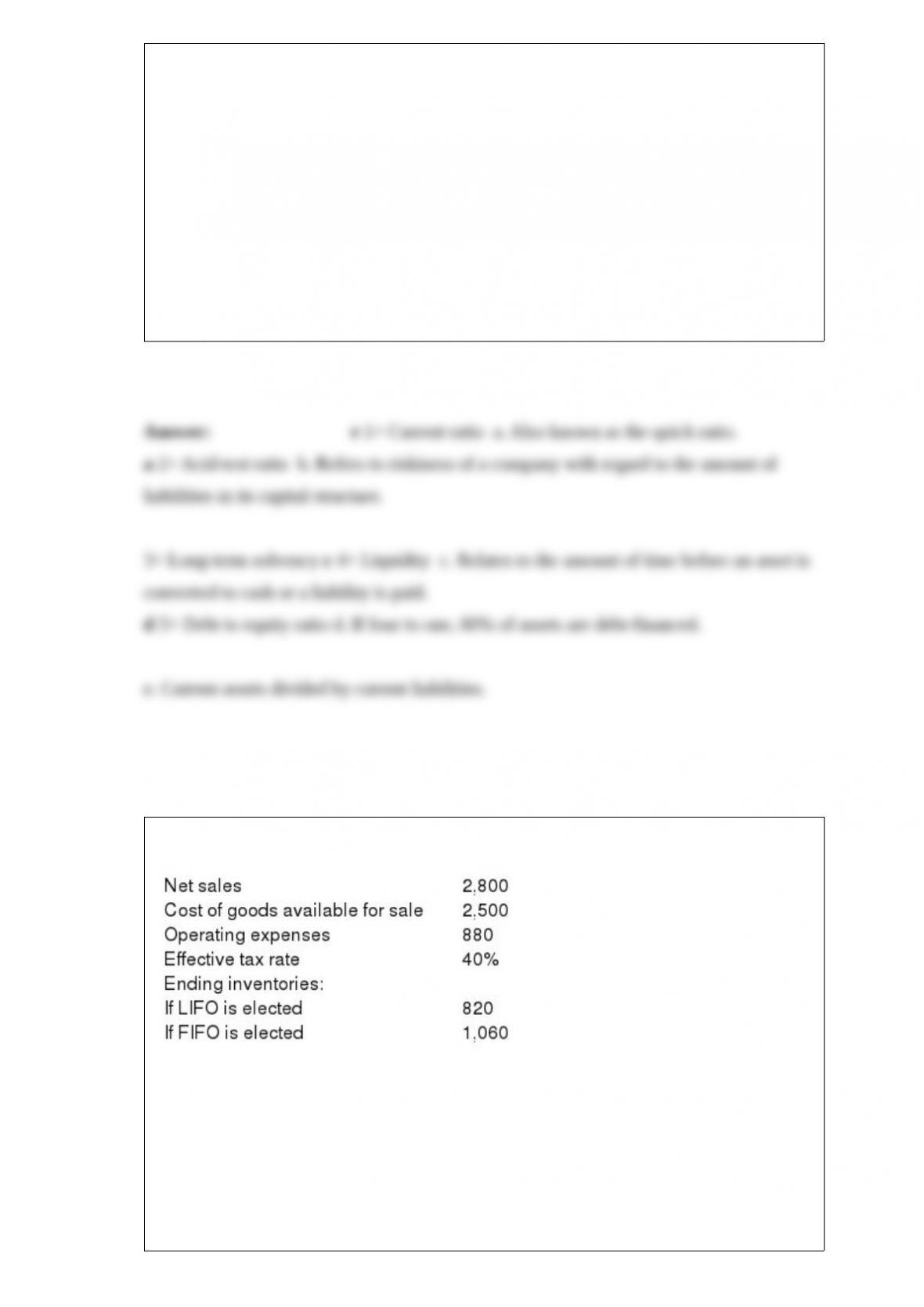

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term.

1> Current ratio a. Also known as the quick ratio.

2> Acid-test ratio b. Refers to riskiness of a company with regard to the amount of

liabilities in its capital structure.

3> Long-term solvency 4> Liquidity c. Relates to the amount of time before an asset

is converted to cash or a liability is paid.

5> Debt to equity ratio d. If four to one, 80% of assets are debt-financed.

e. Current assets divided by current liabilities.

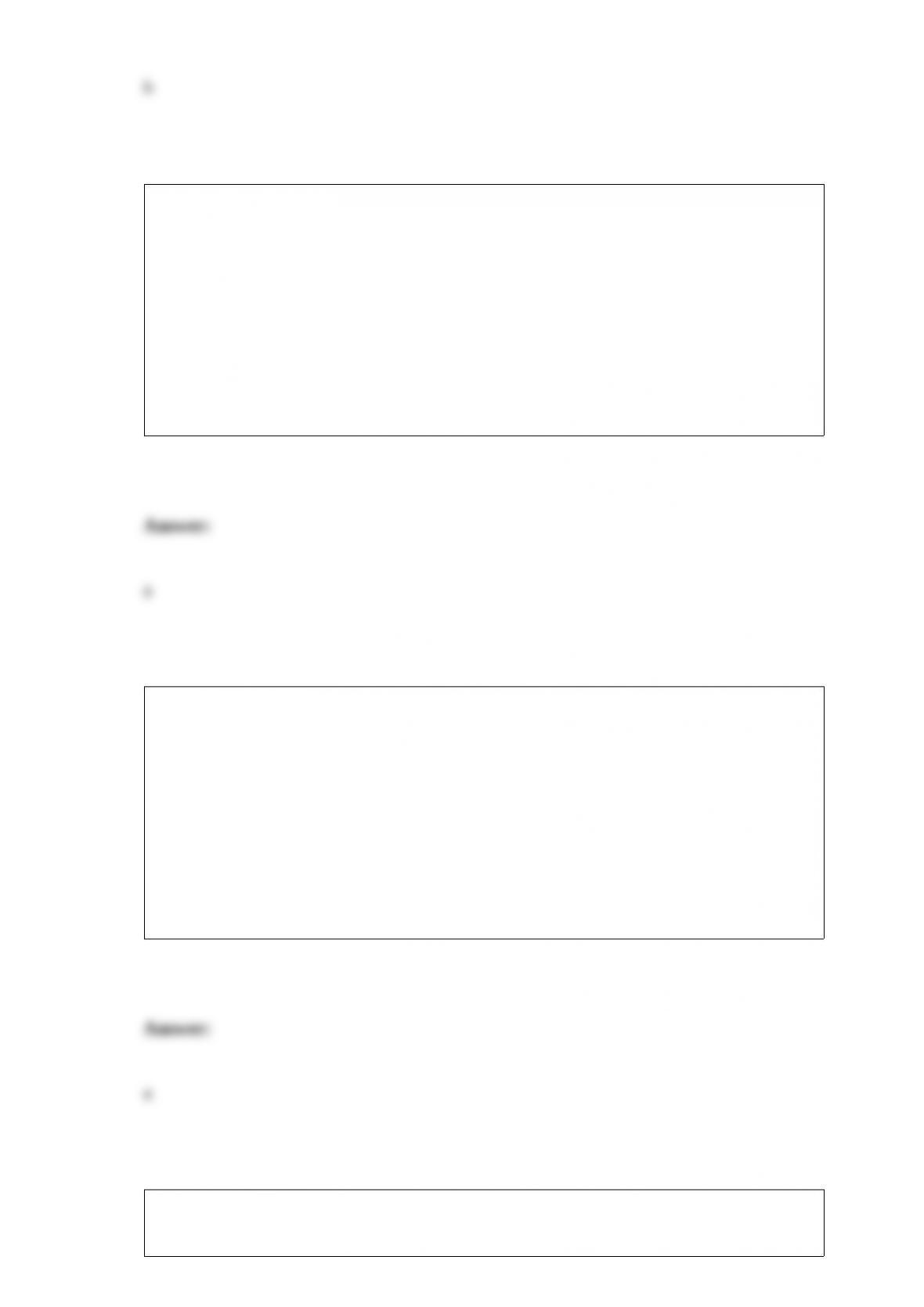

Nu Company reported the following pretax data for its first year of operations.

What is Nu’s net income if it elects LIFO?

a. $288.

b. $144.

c. $240.

d. $480.

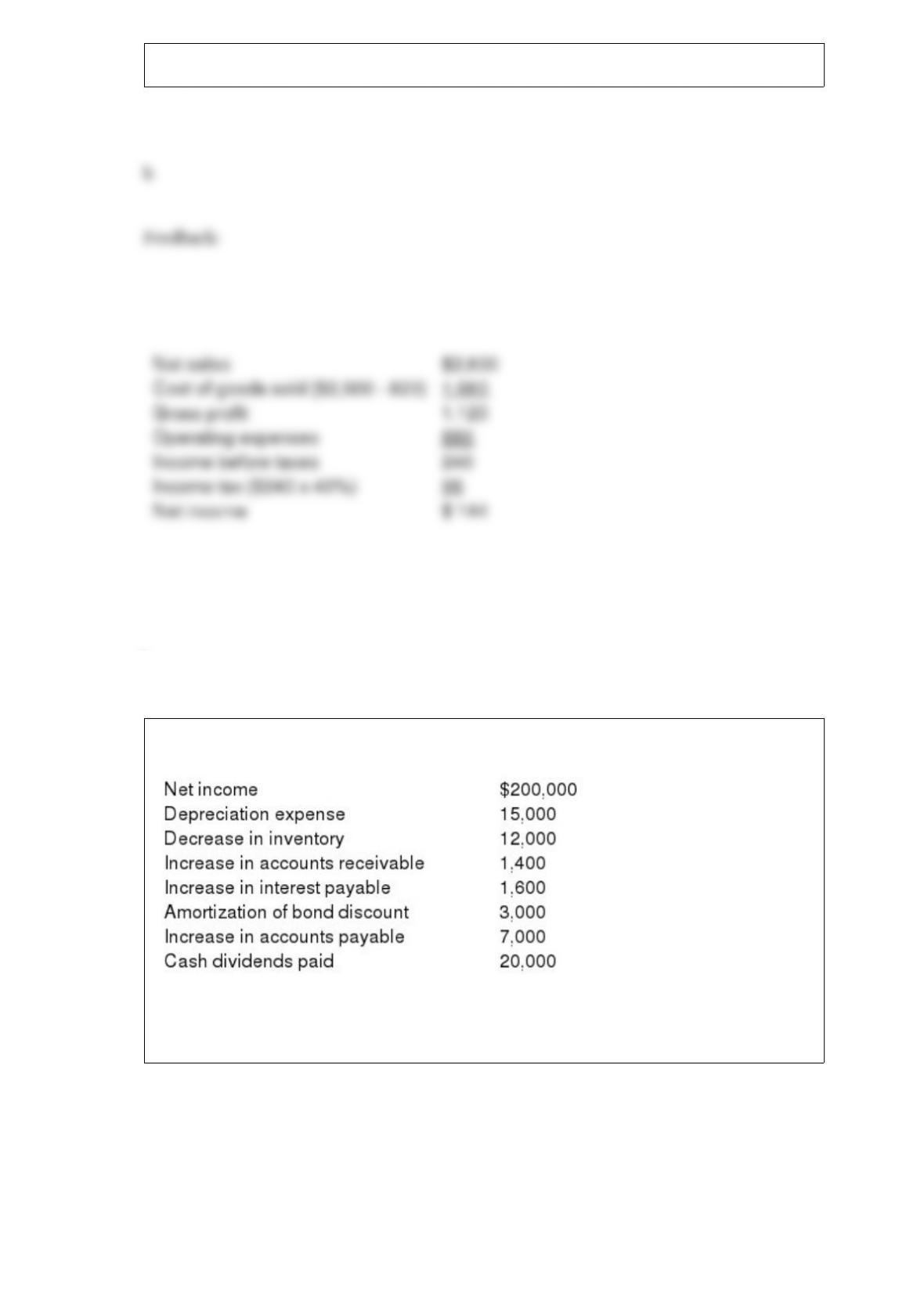

The accounting records of Westlake Industries provided the data below.

Required:

Prepare a reconciliation of net income to net cash flows from operating activities.

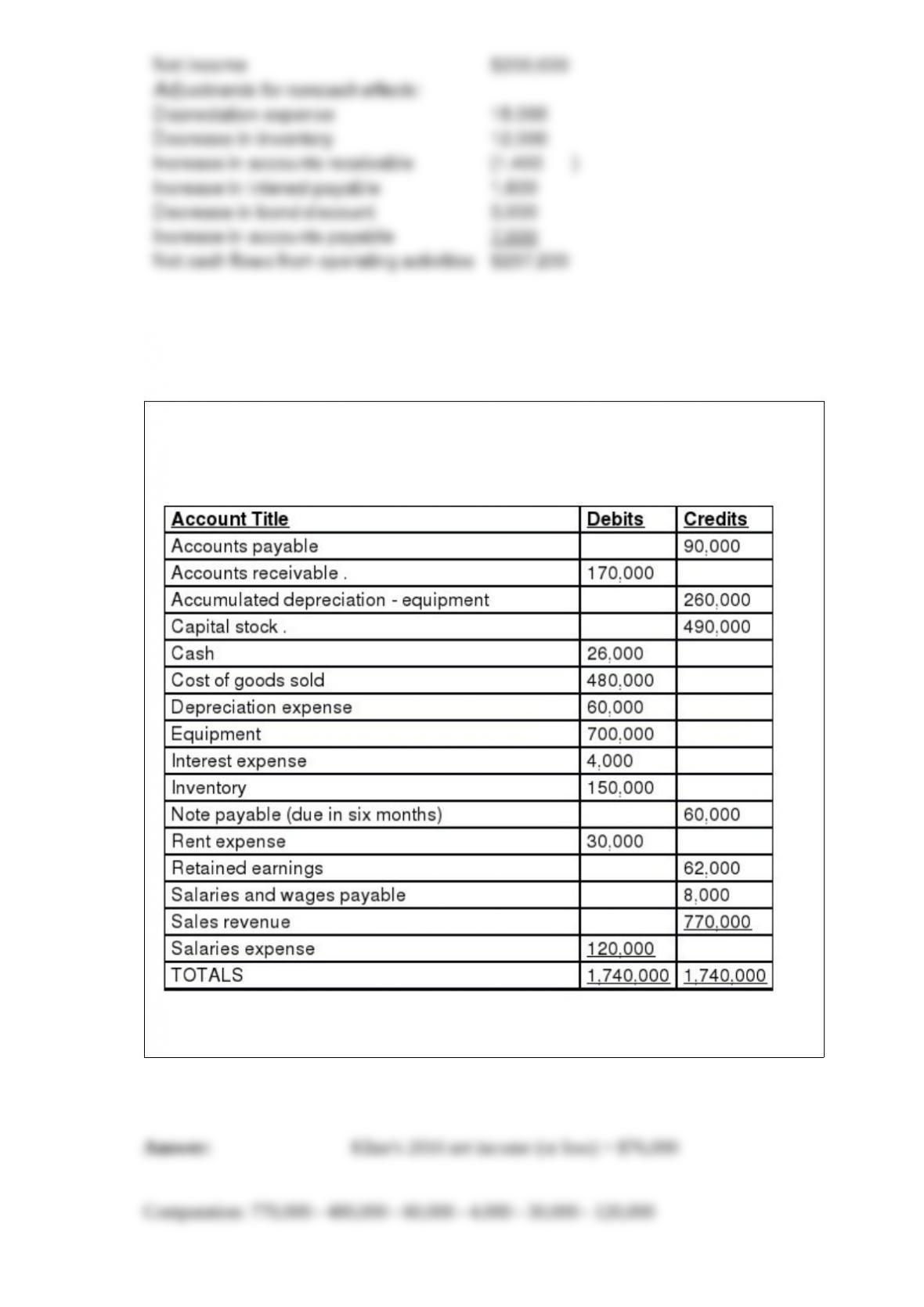

The December 31, 2016 (pre-closing) adjusted trial balance for Kline Enterprises was

as follows:

Required: Assuming no income taxes, compute the following, and place your answer

in the space provided: Kline’s 2016 net income (or loss):

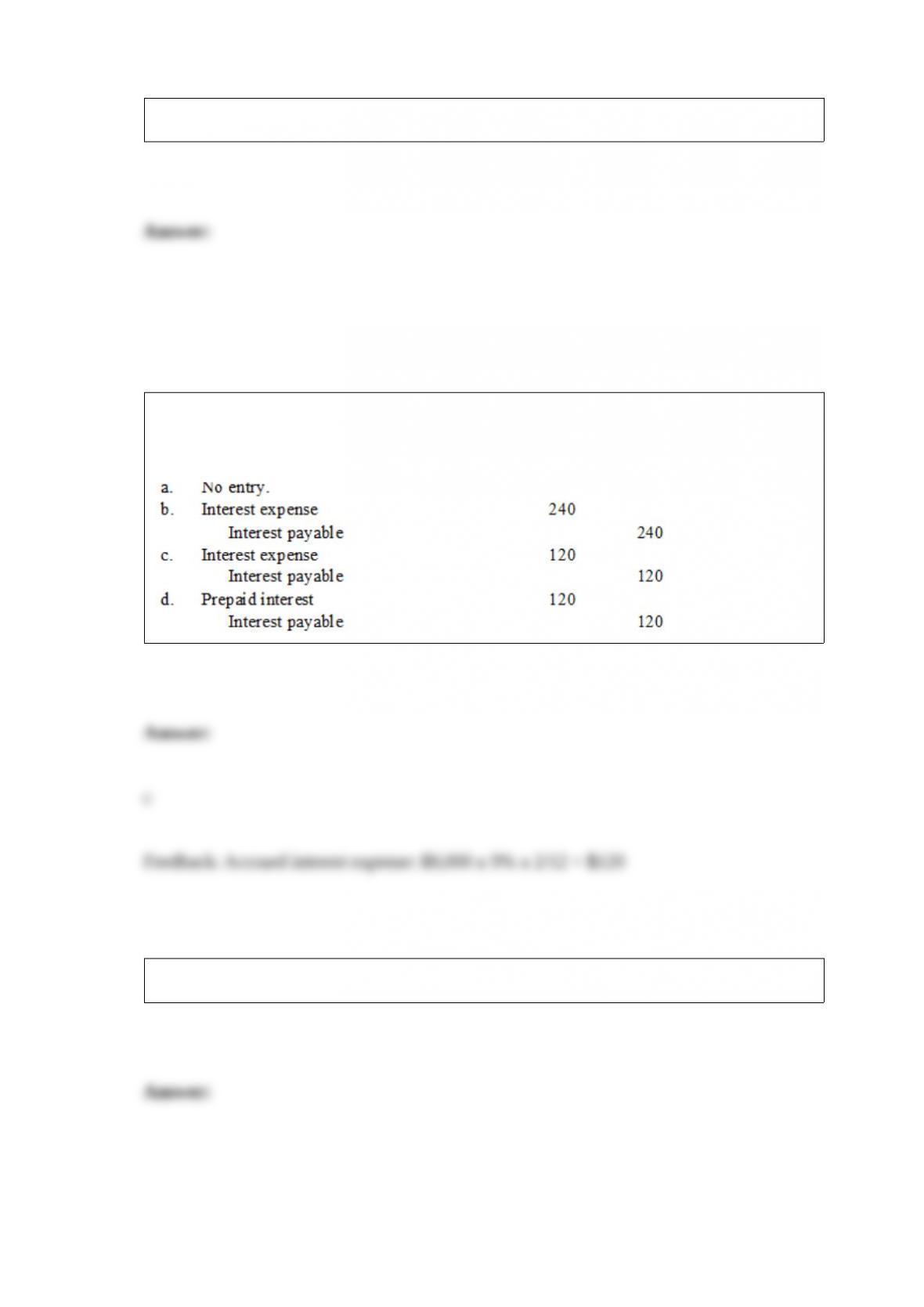

Mama’s Pizza Shoppe borrowed $8,000 at 9% interest on May 1, 2016, with principal

and interest due on October 31, 2017. The company’s fiscal year ends June 30, 2016.

What adjusting entry is necessary on June 30, 2016?

Briefly explain how a company that recognized revenue over time by estimating

percentage of completion using a cost-to-cost ratio could manage earnings upward to

meet a profit projection. What sort of ethical problems could result from that earnings

management?