The debt to assets ratio measures the percentage of assets financed by creditors.

If a company has significant concentrations of credit risk, it must discuss this risk in the

notes to its financial statements.

At December 31, 2014 Mohling Company’s inventory records indicated a balance of

$602,000. Upon further investigation it was determined that this amount included the

following:

– $112,000 in inventory purchases made by Mohling shipped from the seller 12/27/14

terms FOB destination, but not due to be received until January 2nd

– $74,000 in goods sold by Mohling with terms FOB destination on December 27th. The

goods are not expected to reach their destination until January 6th.

– $6,000 of goods received on consignment from Dollywood Company

What is Mohling’s correct ending inventory balance at December 31, 2014?

a.$490,000

b.$596,000

c.$410,000

d.$484,000

The two fundamental qualities of useful information are

a.relevance and faithful representation.

b.verifiability and timeliness.

c.comparability and flexibility.

d.understandability and consistency.

If $1,200,000 of bonds are issued during the year but $2,500,000 of old bonds are

retired during the year, the statement of cash flows will show a(n)

a.net increase in cash of $1,300,000.

b.net decrease in cash of $1,200,000.

c.increase in cash of $1,200,000 and a decrease in cash of $2,500,000.

d.net loss on retirement of bonds of $1,300,000.

The following information is related to December 31, 2013 balances.

During 2014 sales on account were $580,000 and collections on account were

$344,000. Also during 2014 the company wrote off $32,000 in uncollectible accounts.

An analysis of outstanding receivable accounts at year end indicated that bad debts

should be estimated at $216,000. Bad debt expense for 2014 is

a.$ 68,000.

b.$ 36,000.

c.$216,000.

d.$ 4,000.

These are selected account balances on December 31, 2014.

What is the total amount of property, plant, and equipment that will appear on the

balance sheet?

a.$1,500,000

b.$1,300,000

c.$1,800,000

d.$1,150,000

Financial information is presented below:

The profit margin would be

a..32

b..16

c..03

d..04

On January 1, 2014, Michelin Company, a calendar-year company, is issued

9,000,000 of mortgage notes payable, of which 3,000,000 is due on January 1 for

each of the next three years. The proper statement of financial position presentation on

December 31, 2014, is

a.Current liabilities, 9,000,000.

b.Long-term Debt, 9,000,000.

c.Current liabilities, 4,500,000; Long-term Debt, 4,500,000.

d.Current liabilities, 3,000,000; Long-term Debt, 6,000,000.

The accounts receivable turnover is computed by dividing

a.total sales by average receivables.

b.total sales by ending receivables.

c.net credit sales by average receivables.

d.net credit sales by ending receivables.

Mason Transport has the following stock outstanding at December 31, 2014:

Mason paid no dividends during 2013. During 2014, it declares $13,000 of dividends.

How much of the $13,000 will preferred stockholders receive?

a.$1,980

b.$3,960

c.$1,083

d.None of the answer choices are correct.

The difference between the amount borrowed (or invested) and the amount repaid (or

collected) is commonly known as

a.simple interest.

b.an annuity.

c.interest

d.present value.

Newell Company purchased a machine with a list price of $96,000. They were given a

10% discount by the manufacturer. They paid $600 for shipping and sales tax of $4,500.

Newell estimates that the machine will have a useful life of 10 years and a residual

value of $30,000. If Newell uses straight-line depreciation, annual depreciation will be

a.$6,150.

b.$6,108.

c.$9,150.

d.$5,640.

Assume that the Quinn Corporation uses the indirect method to depict cash flows.

Indicate where, if at all, stock issued for equipment would be classified on the statement

of cash flows.

a.Operating activities section.

b.Investing activities section.

c.Financing activities section.

d.Does not represent a cash flow.

On June 1, Huntley Company borrows $50,000 from the bank by signing a 60-day, 6%,

interest-bearing note.

Instructions

Prepare the necessary entries below associated with the note payable on the books of

Huntley Company.

(a)Prepare the entry on June 1 when the note was issued.

(b)Prepare any adjusting entries necessary on June 30 in order to prepare the monthly

financial statements. Assume no other interest accrual entries have been made.

Prepare the entry to record payment of the note at maturity.

During the year, Sarah’s Pet Shop’s merchandise inventory decreased by $40,000. If the

company’s cost of goods sold for the year was $600,000, purchases would have been

a.$640,000.

b.$560,000.

c.$520,000.

d.Unable to determine.

Dalton Company was undergoing an end of year audit of its financial records. The

auditors were in the process of reviewing Dalton’s inventory for year end, December 31,

2014. They completed an end of year inventory. The value of the ending inventory prior

to any adjustments was $185,000, but before finishing up they had a few questions.

Discussion with Dalton’s accountant revealed the following:

(a)Dalton sold goods costing $60,000 to Summey Company FOB shipping point on

December 28. The goods are not expected to reach Summey until January 12. The

goods were not included in the physical inventory because they were not in the

warehouse.

(b)The physical count of the inventory did not include goods costing $95,000 that were

shipped to Dalton FOB destination on December 27 and were still in transit at year-end.

(c)Dalton received goods costing $25,000 on January 2. The goods were shipped FOB

shipping point on December 26 by Strong Company. The goods were not included in

the physical count.

(d)Dalton sold goods costing $40,000 to Hampton Company FOB destination on

December 30. The goods were received by Hampton Company on January 8. Because

the goods had been shipped, they were excluded from the physical inventory count.

(e)Dalton received goods costing $42,000 on January 2 that were shipped FOB

destination on December 29. The shipment was a rush order that was suppose to arrive

December 31. This purchase was included in the ending inventory of $192,000.

(f)Dalton Company, as the consignee, had goods on consignment that cost $3,000.

Because these goods were on hand as of December 31, they were included in the

physical inventory count.

Instructions

Analyze the above information and calculate a corrected amount for the ending

inventory. Explain the basis for your treatment of each item.

North Company has other operating expenses of $330,000. There has been a decrease in

prepaid expenses of $16,000 during the year, and accrued liabilities are $24,000 larger

than in the prior period. Using the direct method of reporting cash flows from operating

activities, what were North’s cash payments for operating expenses?

a.$338,000.

b.$322,000.

c.$290,000.

d.$370,000.

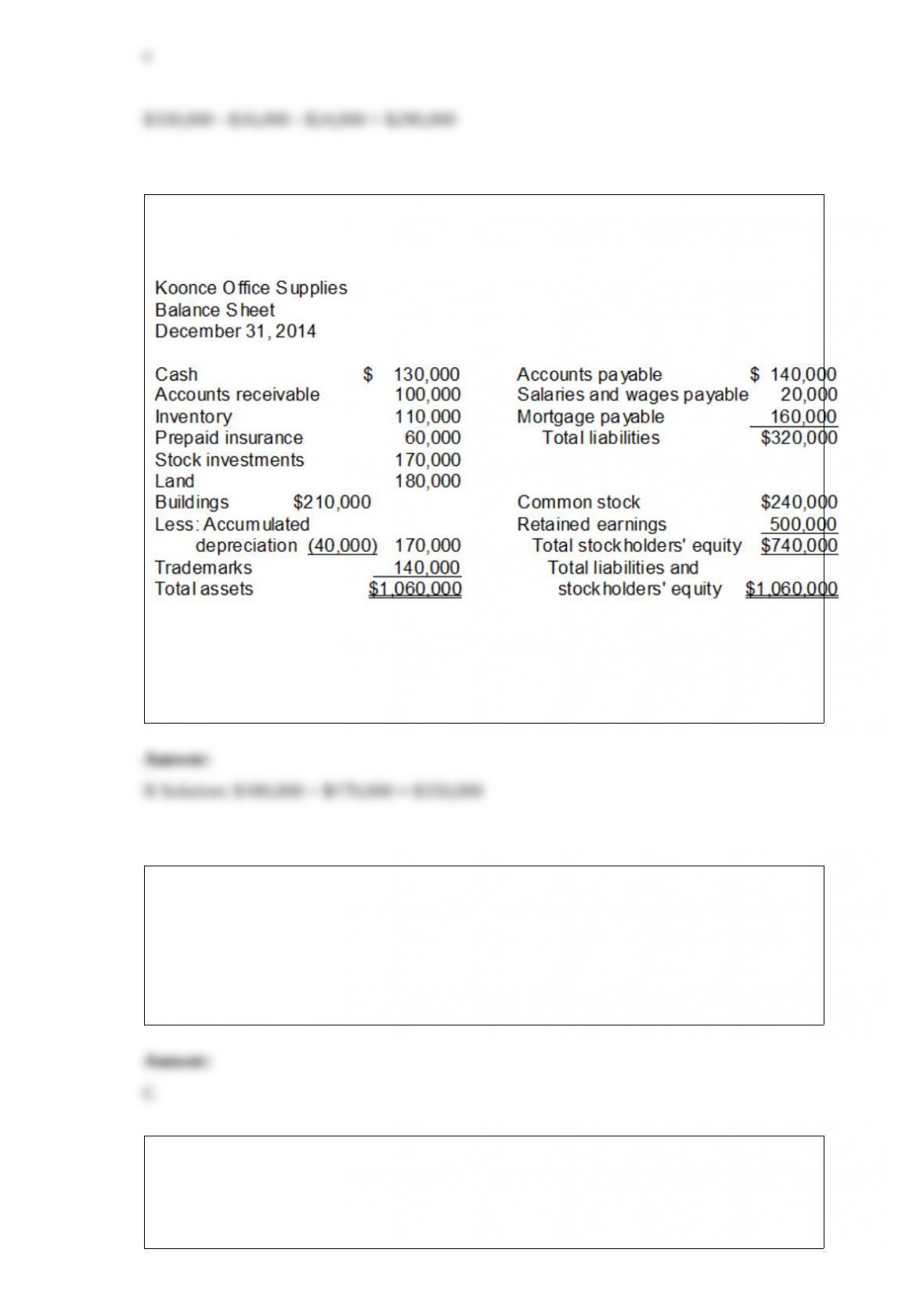

Use the following data to determine the total dollar amount of assets to be classified as

property, plant, and equipment.

a.$660,000

b.$350,000

c.$490,000

d.$390,000

The accounting concept that indicates assets should be reported at the price received to

sell an asset is the

a.economic entity assumption.

b.monetary unit assumption.

c.fair value principle.

d.historical cost principle.

Which accounting assumption requires that only those things that can be expressed in

dollar values are included in the accounting records?

a.monetary unit assumption.

b.historical cost principle.

c.periodicity assumption.

d.full disclosure principle.

Assume Grammar Company uses the periodic inventory system and has a beginning

inventory balance of $5,000, purchases of $75,000, and sales of $125,000. Grammar

closes its records once a year on December 31. In the accounting records, the inventory

account would be expected to have a balance on December 31 prior to adjusting and

closing entries that was

a.equal to $5,000.

b.more than $5,000.

c.less than $5,000.

d.indeterminate.

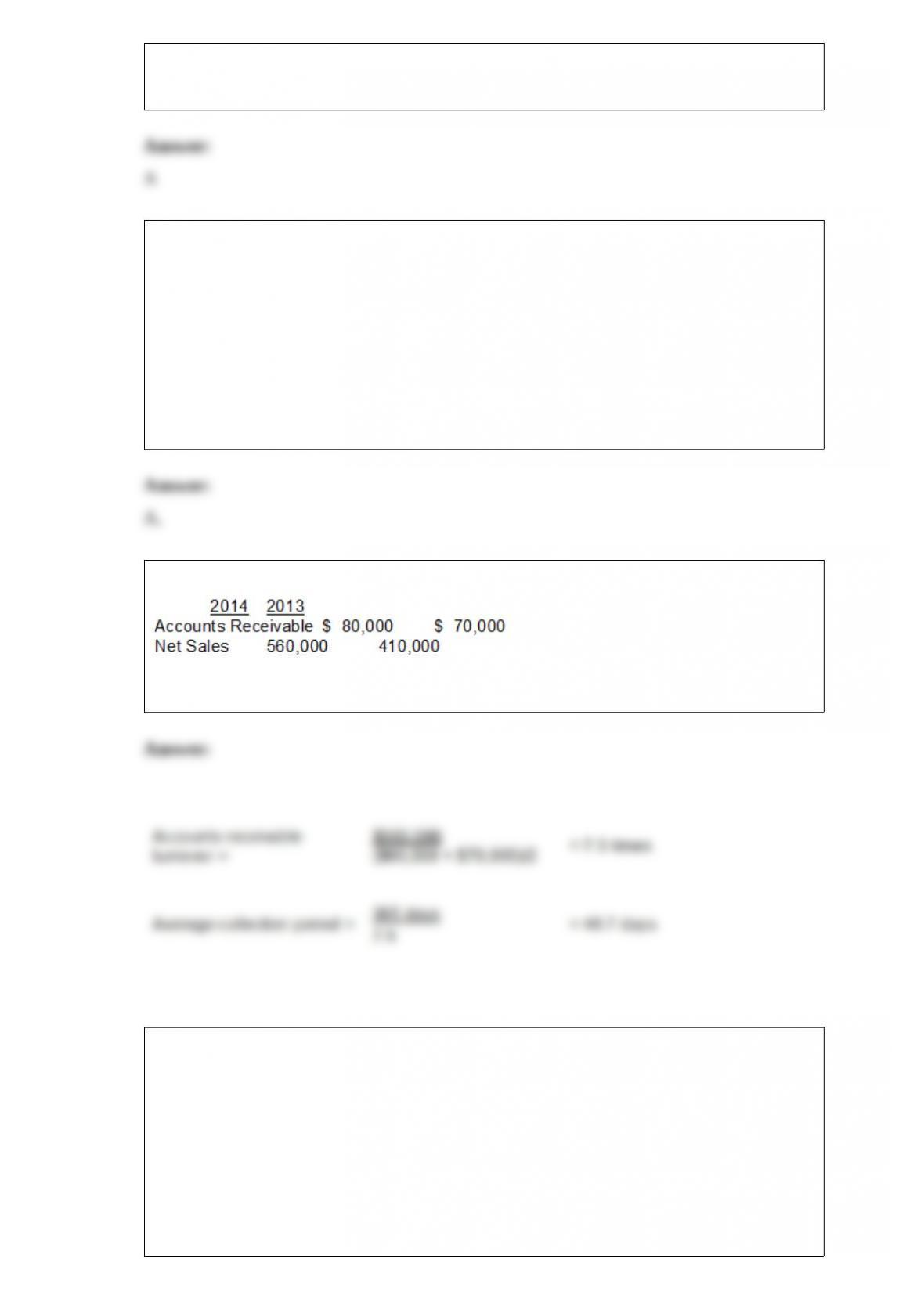

The following data exists for Mather Company.

Calculate the accounts receivable turnover and the average collection period for

accounts receivable in days for 2014.

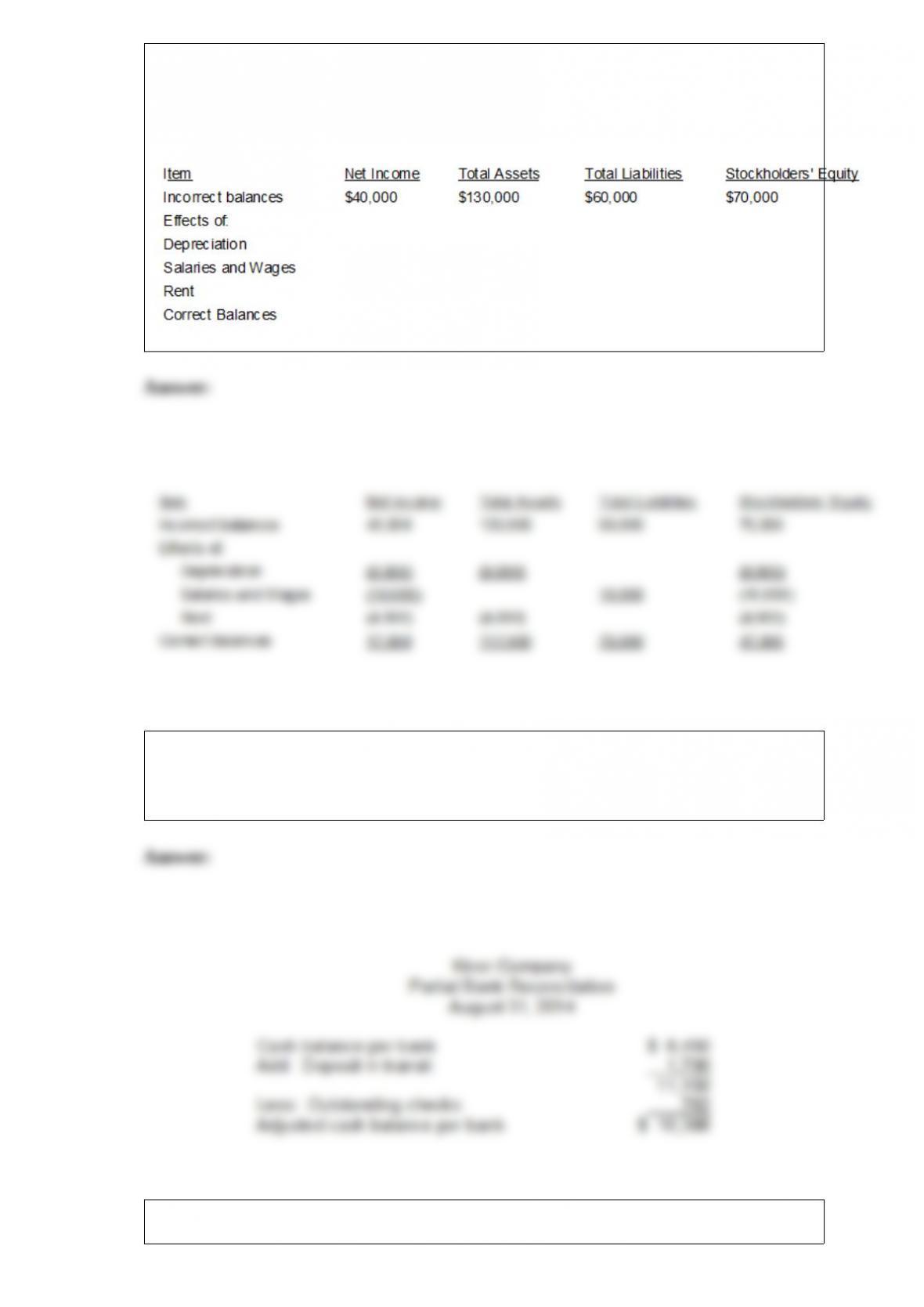

On December 31, 2014, olski Company prepared an income statement and balance

sheet and failed to take into account three adjusting entries. The incorrect income

statement showed net income of $40,000. The balance sheet showed total assets,

$130,000; total liabilities, $60,000; and stockholders’ equity, $70,000.

The data for the three adjusting entries were:

(1)Depreciation of $9,000 was not recorded on equipment.

(2)Salaries and Wages amounting to $10,000 for the last two days in December were

not paid and not recorded. The next payroll will be in January.

(3)Rent of $8,000 was paid for two months in advance on December 1. The entire

amount was debited to Prepaid Rent when paid.

Instructions:

Complete the following tabulation to correct the financial statement amounts shown

(indicate deductions with parentheses):

At August 31 Kiner Company has this bank information: cash balance per bank $9,450;

outstanding checks $762; deposits in transit $1,700; and a bank service charge $20.

Determine the adjusted cash balance per bank at August 31, 2014.

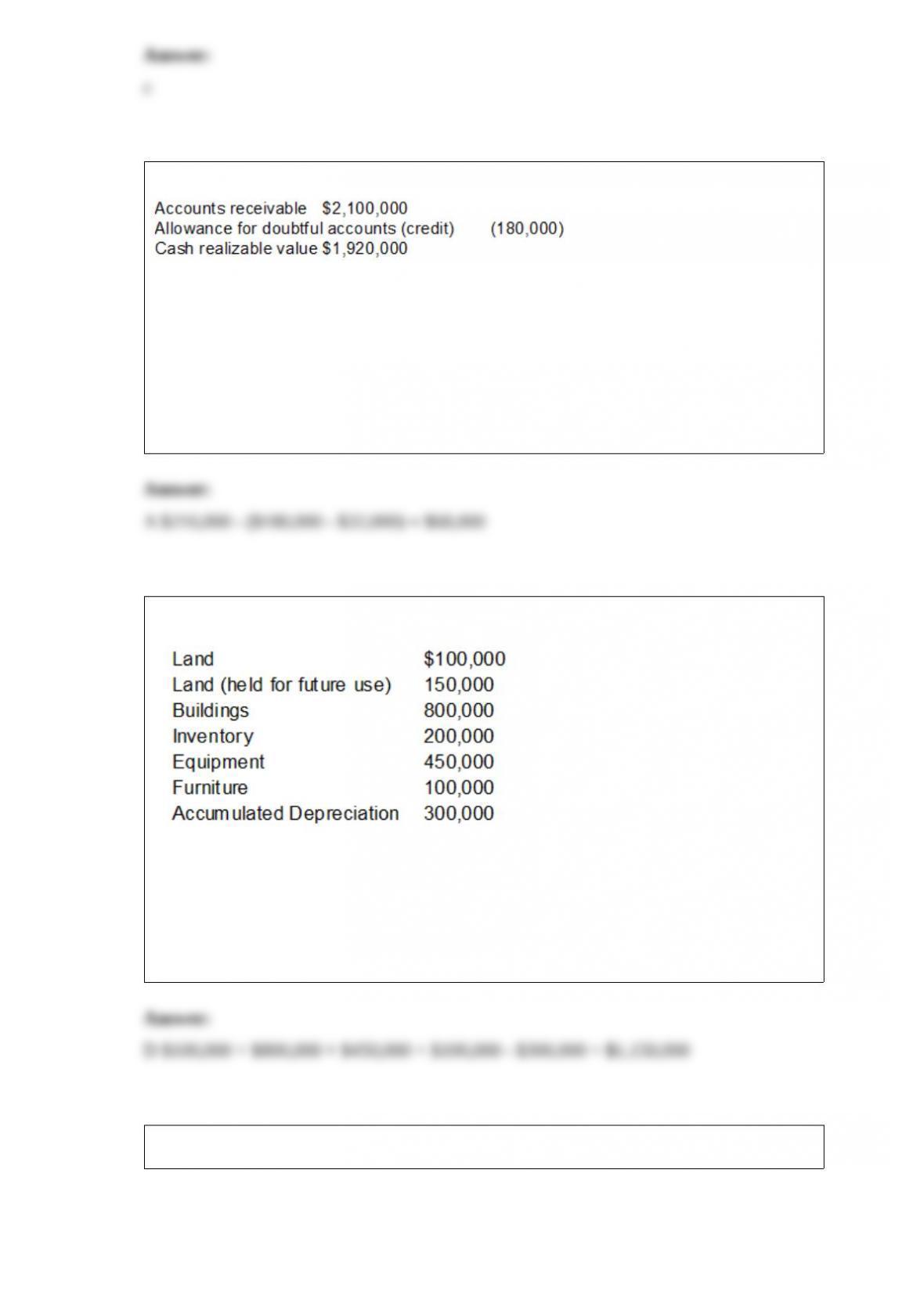

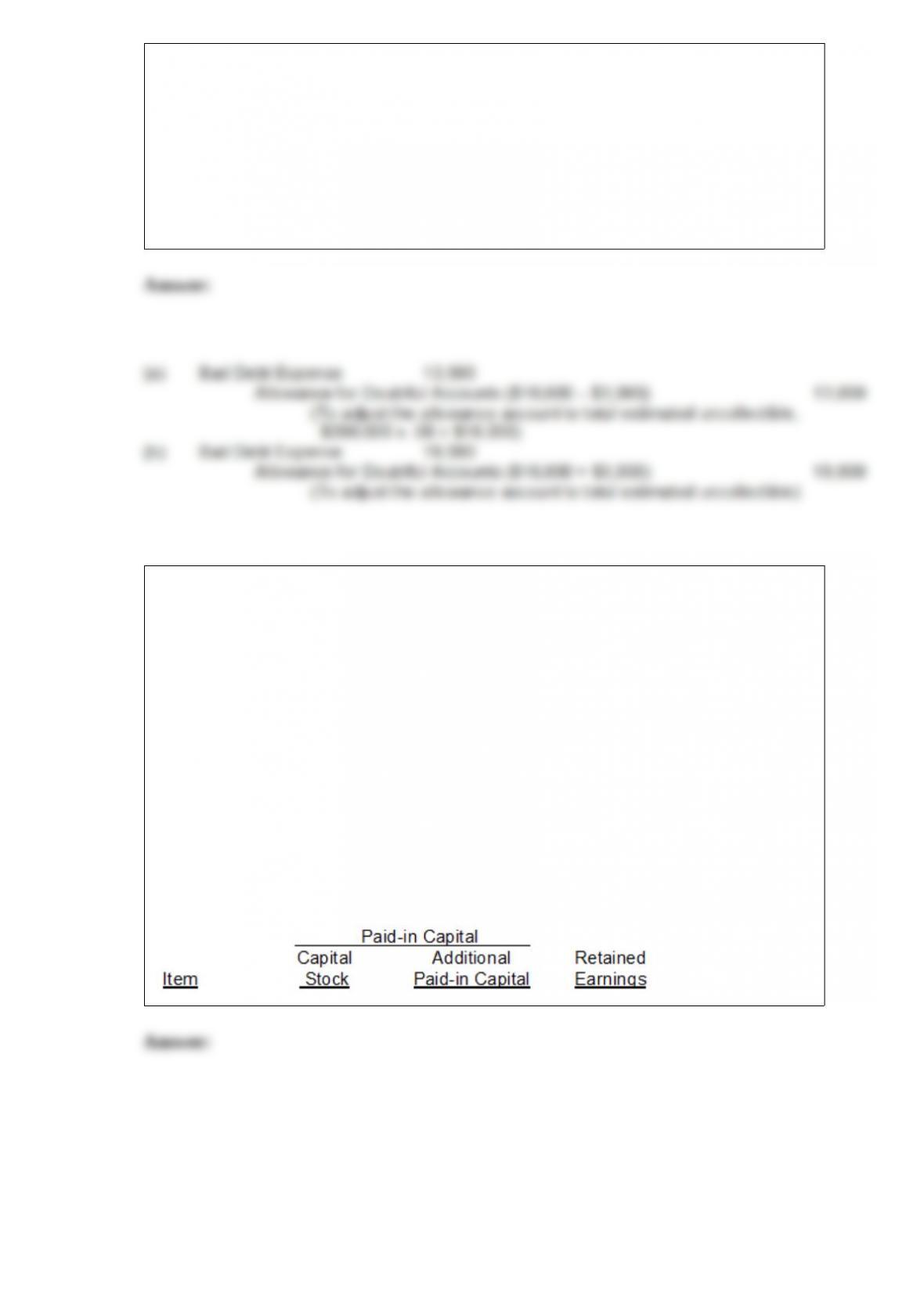

The ledger of the Ramirez Company at the end of the current year shows Accounts

Receivable of $200,000.

Instructions

If Allowance for Doubtful Accounts has a credit balance of $3,000 in the trial balance

and bad debts are expected to be 8% of accounts receivable, journalize the adjusting

entry for end of the period. (Show all calculations.)

If Allowance for Doubtful Accounts has a debit balance of $3,000 in the trial balance

and bad debts are expected to be 8% of accounts receivable, journalize the adjusting

entry for end of the period. (Show all calculations.)

During 2014 Kenton Corporation had the following transactions and events:

1)Issued par value preferred stock for cash at par value

2)Issued par value common stock for cash at an amount greater than par value

3)Completed a 2 for 1 stock split in which the $10 par value common stock was

changed to $5 par value stock

4)Declared a small stock dividend when the market value was higher than the par value

5)Declared a cash dividend

6)Issued the shares of common stock required by the stock dividend declaration in 4.

above

7)Issued par value common stock for cash at par value

8)Paid the cash dividend

Instructions

Indicate the effect(s) of each of the foregoing items on the subdivisions of stockholders’

equity. Present your answers in tabular form with the following columns. Use (I) for

increase, (D) for decrease, and (NE) for no effect.

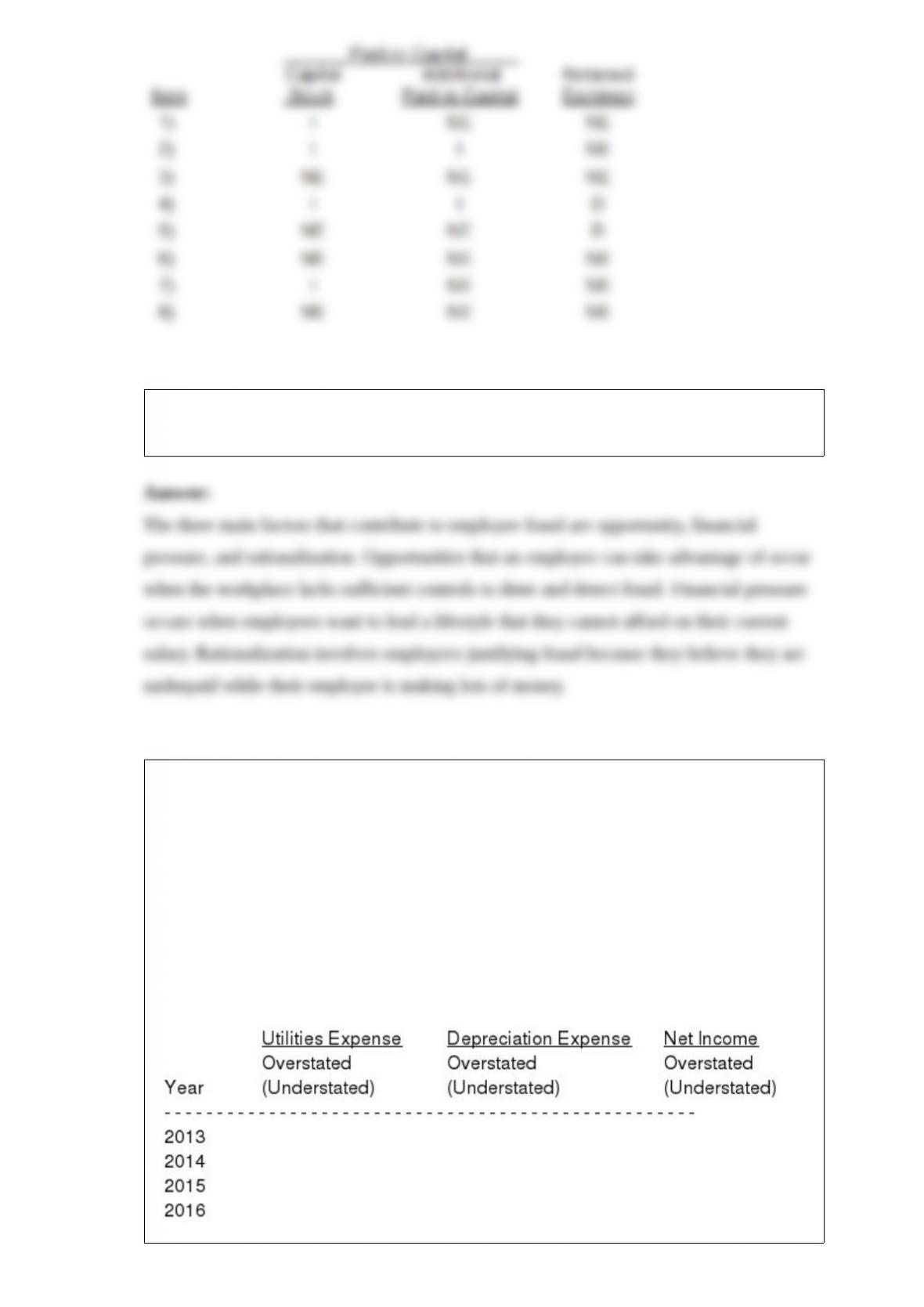

Fraud experts often say that there are three primary factors that contribute to employee

fraud. Identify the three factors and explain what is meant by each.

On January 1, 2012, Keller Company purchased and installed a telephone system at a

cost of $20,000. The equipment was expected to last five years with a salvage value of

$3,000. On January 1, 2013, more telephone equipment was purchased to tie-in with the

current system for $10,000. The new equipment is expected to have a useful life of four

years. Through an error, the new equipment was debited to Utilities Expense. Keller

Company uses the straight-line method of depreciation.

Instructions

Prepare a schedule showing the effects of the error on Utilities Expense, Depreciation

Expense, and Net Income for each year and in total beginning in 2013 through the

useful life of the new equipment.

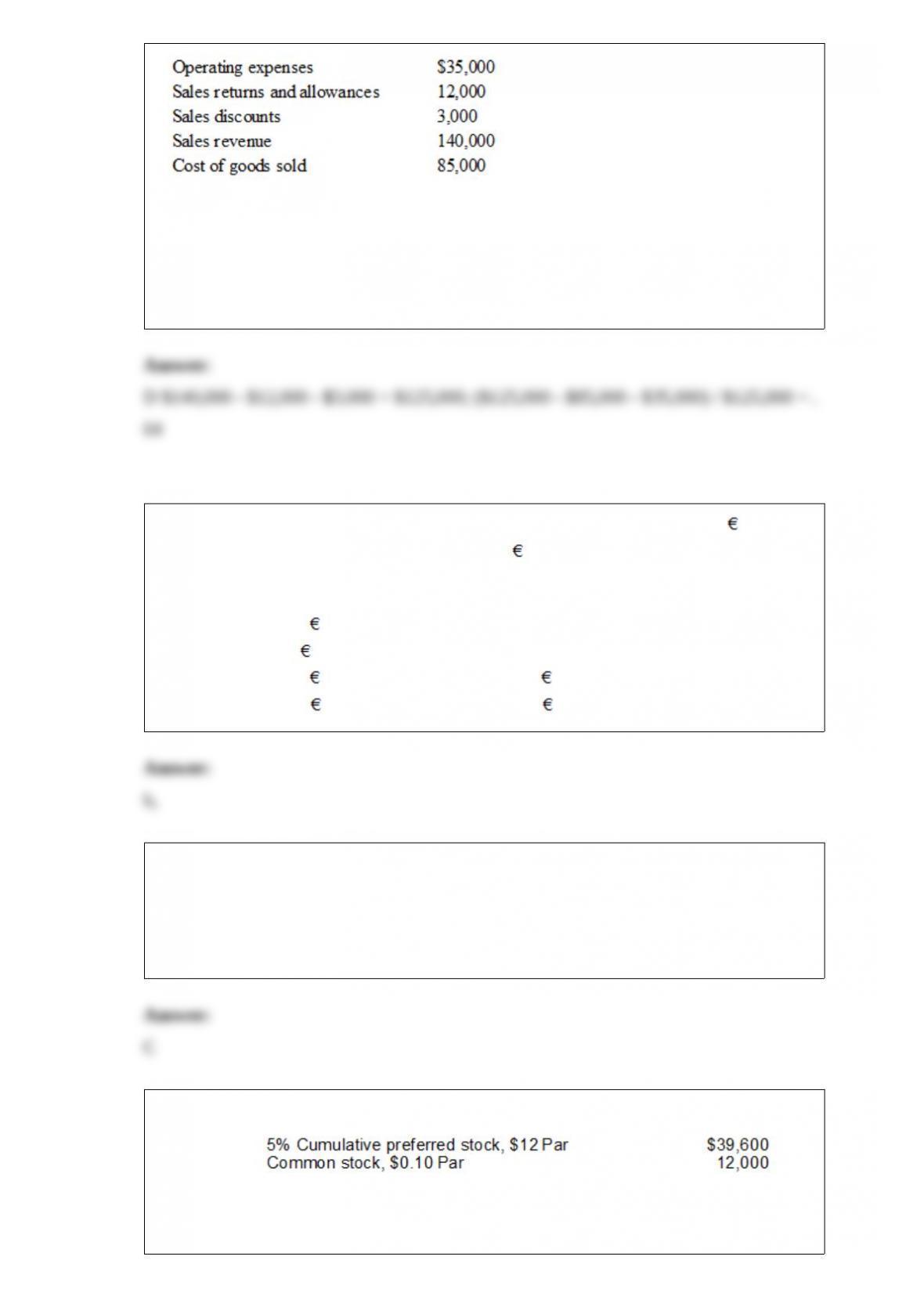

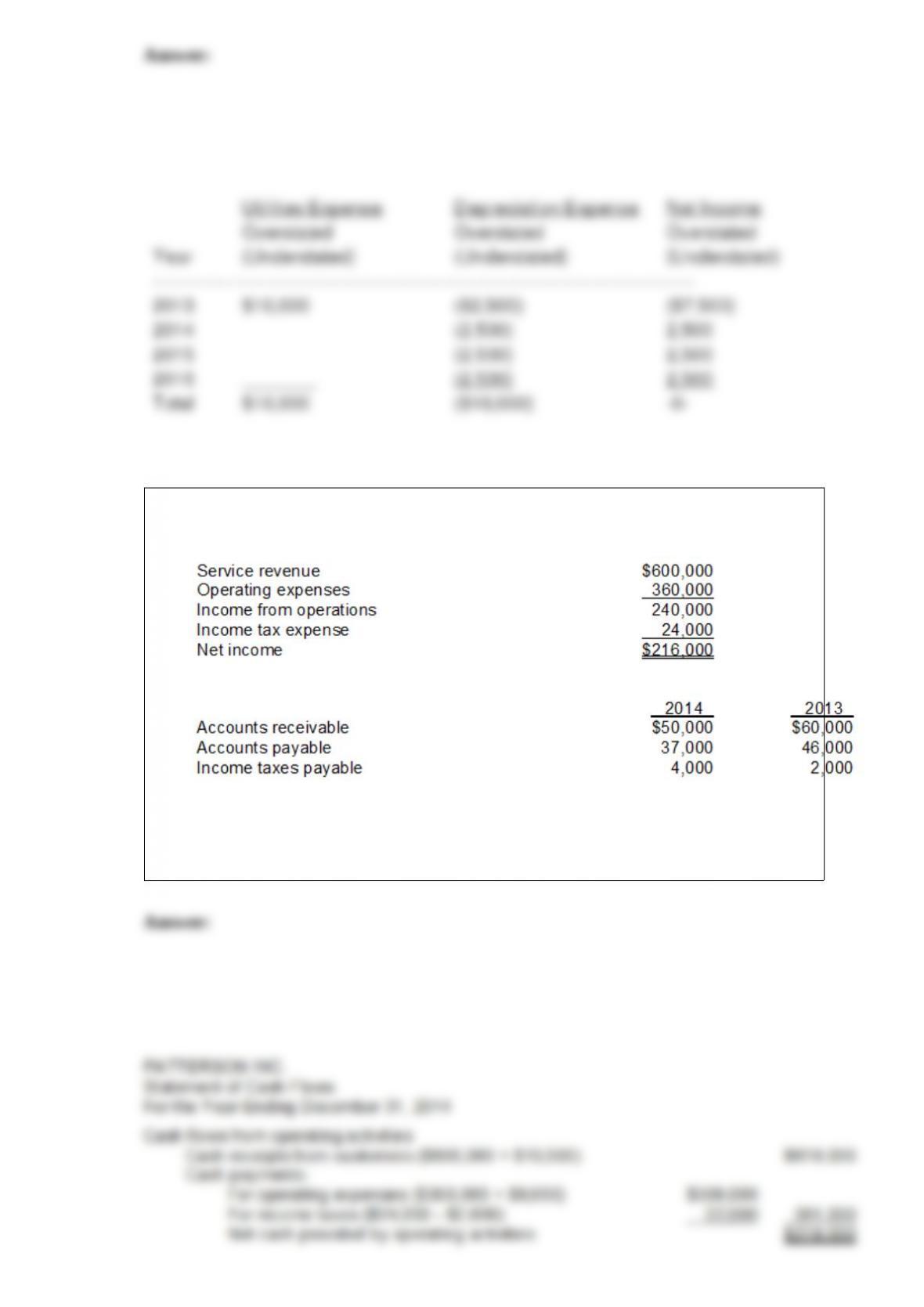

The income statement of Patterson Inc. for the year ended December 31, 2014, reported

the following condensed information:

Patterson’s balance sheet contained the following comparative data at December 31:

Patterson has no depreciable assets. Accounts payable pertains to operating expenses.

Instructions

Prepare the operating activities section of the statement of cash flows using the direct

method.