1) In the absorption approach to cost-plus pricing, the anticipated markup in dollars is

NOT equal to the anticipated profit.

2) Paying taxes to governmental bodies is considered a cash outflow in the operating

activities section on the statement of cash flows.

3) Depreciation on manufacturing equipment is a product cost.

4) Setting transfer prices at full cost can lead to good decisions because, among other

reasons, full cost takes into account opportunity costs.

5) In the cost reconciliation report under the FIFO method, the costs accounted for

equals the cost of beginning work in process inventory plus the cost of units transferred

out.

6) A vertically integrated company is more dependent on its suppliers than a company

that is not vertically integrated.

7) The equivalent units of production for a department using the FIFO process costing

method is equal to the number of units completed plus the equivalent units in the ending

inventory less the equivalent units in the beginning inventory.

8) Unless the organization is tax-exempt, income taxes should be considered when

using net present value analysis to make capital budgeting decisions.

9) In determining whether a company’s financial condition is improving or deteriorating

over time, horizontal analysis of financial statement data would be more useful than

vertical analysis.

10) The materials price variance is computed by multiplying the difference between the

actual price and the standard price by the actual quantity of materials purchased.

11) The overall contribution margin ratio for a company producing three products may

be obtained by adding the contribution margin ratios for the three products and dividing

the total by three.

12) A quantity standard indicates how much output should have been produced.

13) Cost behavior is considered linear whenever a straight line is a reasonable

approximation for the relation between cost and activity.

14) An unfavorable materials price variance is recorded as a debit in the Materials Price

Variance account.

15) The target cost per lawn blower is closest to:

A.$33.63

B.$30.30

C.$38.00

D.$42.18

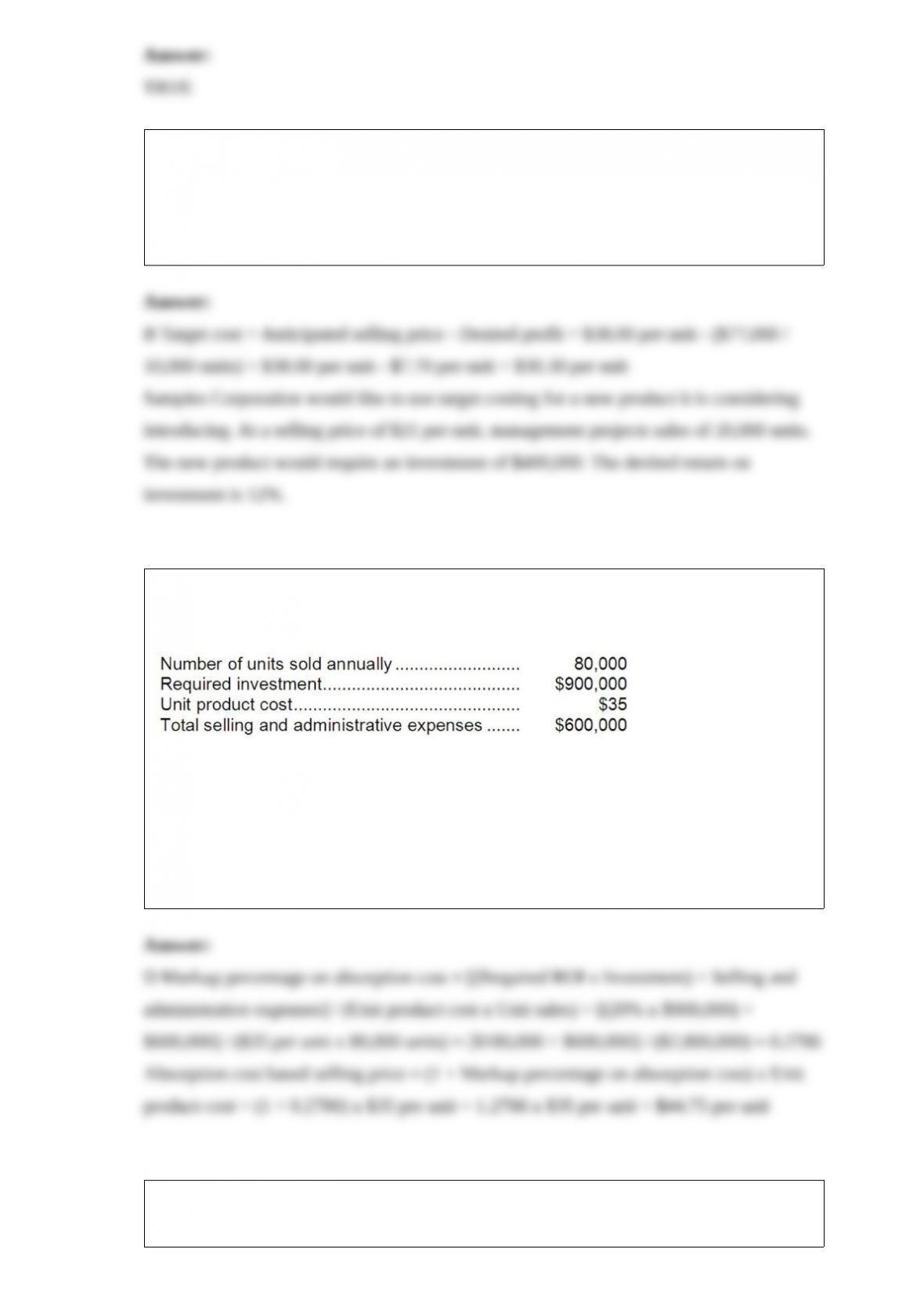

16) Simmons Corporation estimated that the following costs and activity would be

associated with Product T:

If the company uses the absorption costing approach to cost-plus pricing described in

the text and desires a 20% ROI, the selling price for Product T would be:

A.$37.25

B.$38.75

C.$42.00

D.$44.75

17) Selling used equipment at book value for cash will:

A.increase working capital.

B.decrease working capital.

C.decrease the debt-to-equity ratio.

D.increase net income.

18) Stench Foods Corporation uses a standard cost system to collect costs related to the

production of its garlic flavored yogurt. The garlic (materials) standards for each

container of yogurt produced are 0.8 ounces of crushed garlic at a standard cost of

$2.30 per ounce.

During the month of June, Stench purchased 75,000 ounces of crushed garlic at a total

cost of $171,000. Stench used 64,000 of these ounces to produce 71,500 containers of

yogurt.

The direct materials purchases variance is computed when the materials are purchased.

What is Stench’s materials price variance for June?

A.$1,500 Favorable

B.$15,640 Unfavorable

C.$17,250 Favorable

D.$23,800 Favorable

19) The product’s price elasticity of demand as defined in the text is closest to:

A.-2.13

B.-1.47

C.-1.57

D.-1.81

20) The company’s net cash provided by operating activities is:

A.$48,000

B.$18,000

C.$40,000

D.$52,000

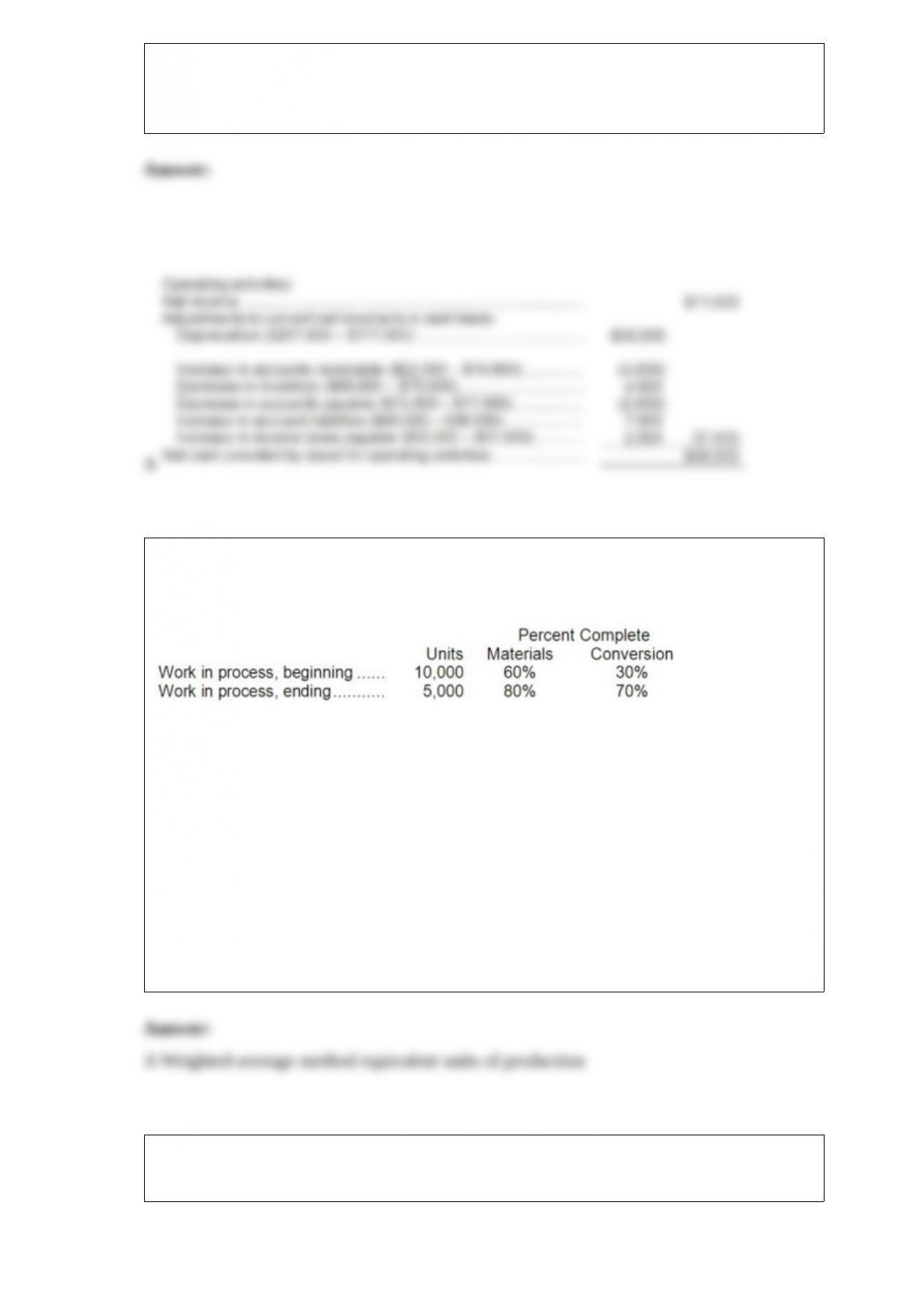

21) Higgins Labs, Inc. uses a process costing system. The following data are available

for one department for October:

The department started 45,000 units into production during the month and completed

and transferred 50,000 units to the next department.

Assuming the weighted-average method is used, the equivalent units for material for

October would be:

A.54,000 units

B.50,000 units

C.48,000 units

D.44,000 units

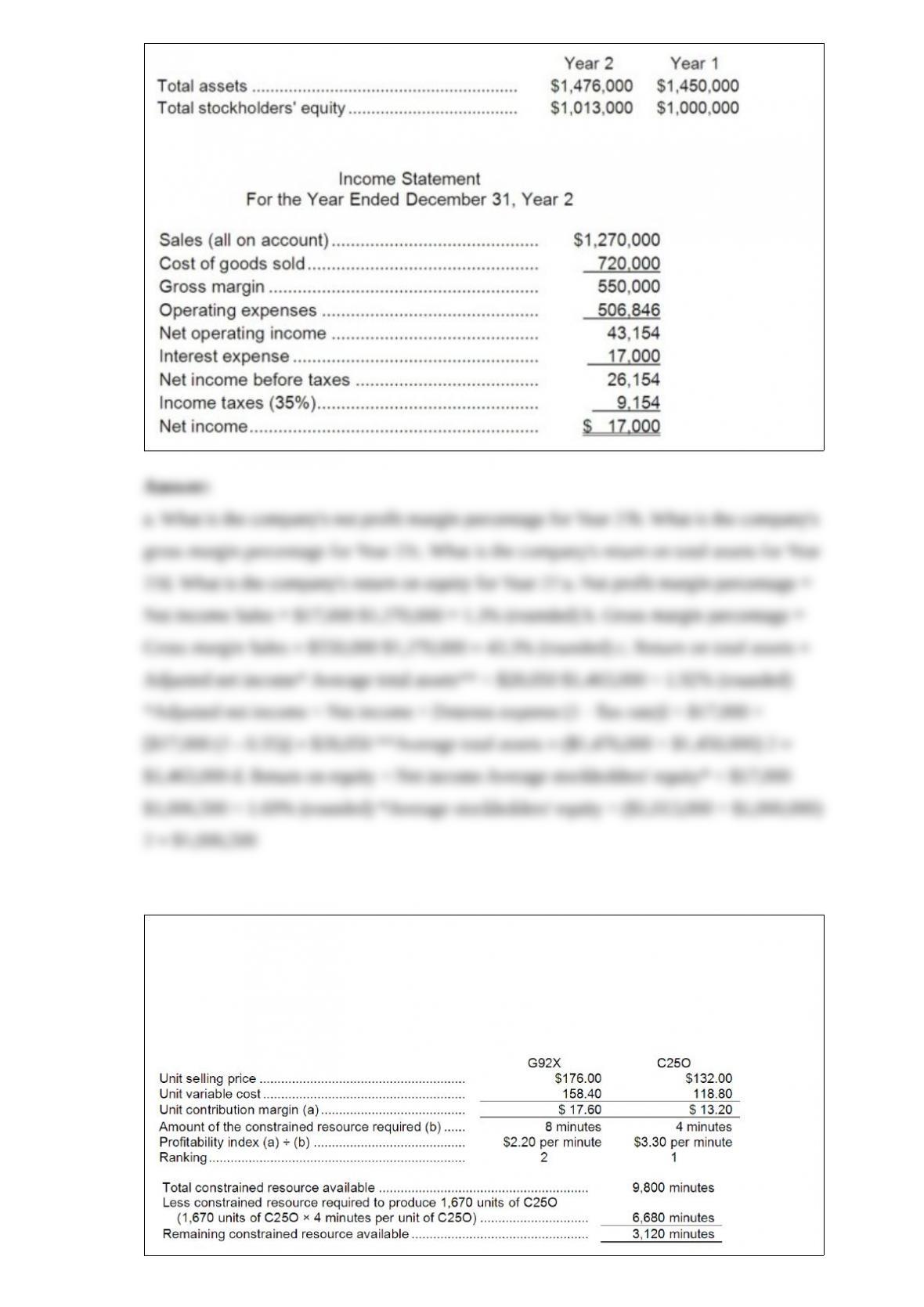

22) Pribyl Corporation has provided the following financial data:

23) How many units of product G92X should be produced each month?

A.0

B.1,655

C.820

D.390

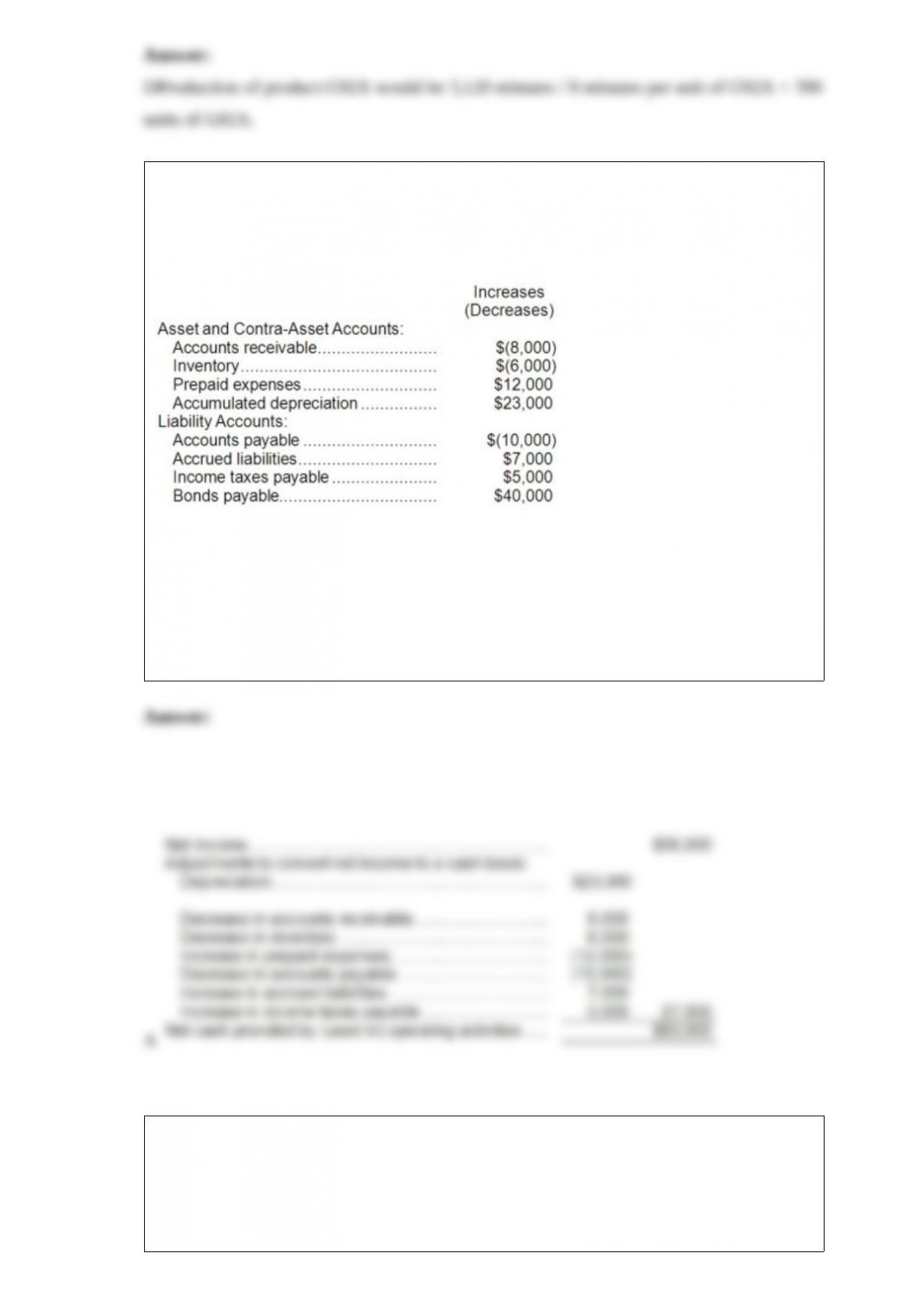

24) Morbeck Corporation’s net income last year was $56,000. The company paid a cash

dividend of $31,000 and did not sell or retire any property, plant, and equipment last

year. Changes in selected balance sheet accounts for the year appear below:

Based solely on this information, the net cash provided by operating activities under the

indirect method on the statement of cash flows would be:

A.$83,000

B.$102,000

C.$29,000

D.$79,000

25) The average sale period for Year 2 is closest to:

A.63.0 days

B.89.2 days

C.236.3 days

D.97.3 days

26) Solen Corporation’s break-even-point in sales is $900,000, and its variable expenses

are 75% of sales. If the company lost $32,000 last year, sales must have amounted to:

A.$868,000

B.$804,000

C.$772,000

D.$628,000

27) Which of the following is not a source of financial leverage?

A.Bonds payable.

B.Accounts payable.

C.Taxes payable.

D.Prepaid rent.

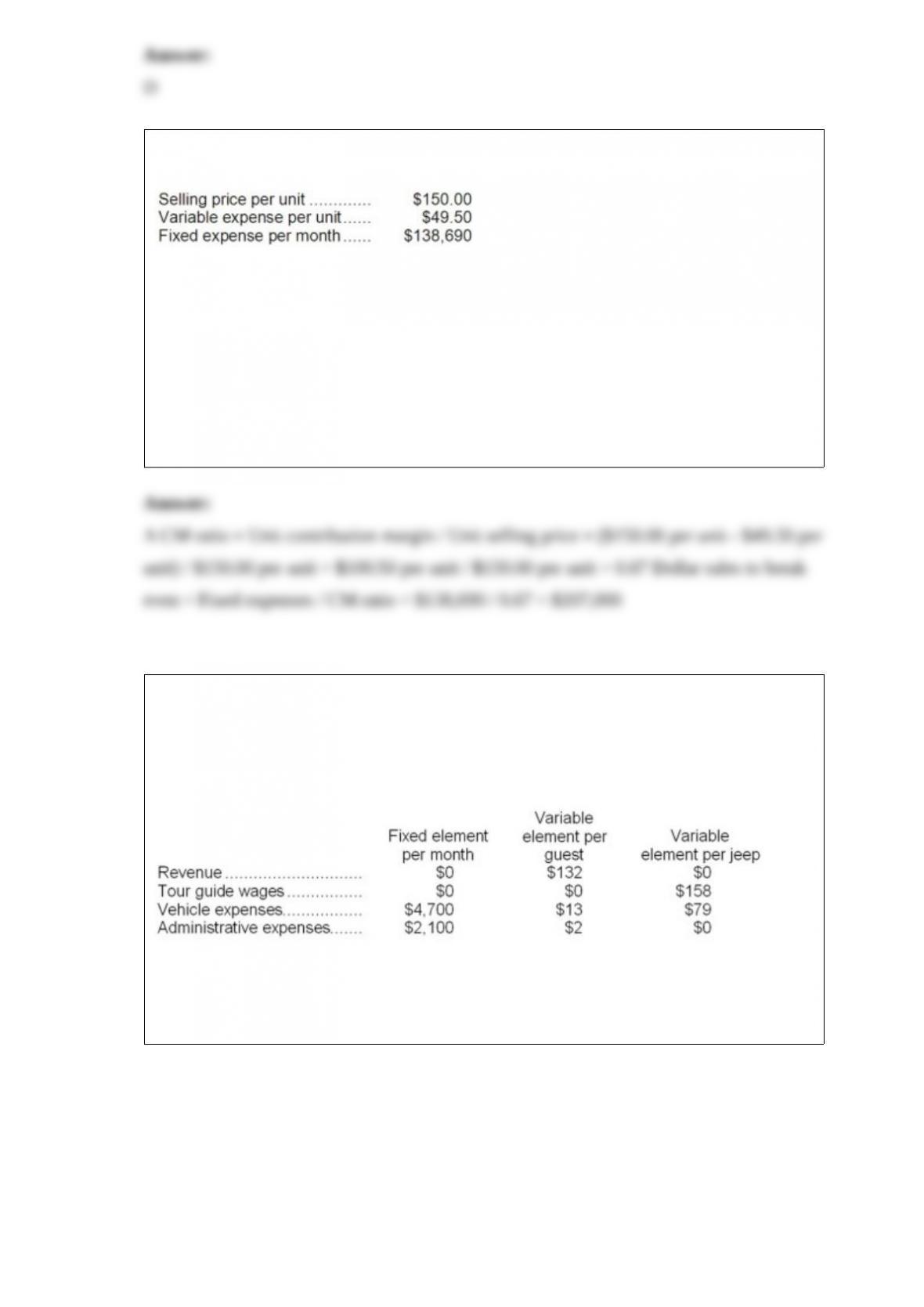

28) Data concerning Wang Corporation’s single product appear below:

The break-even in monthly dollar sales is closest to:

A.$207,000

B.$255,321

C.$138,690

D.$420,273

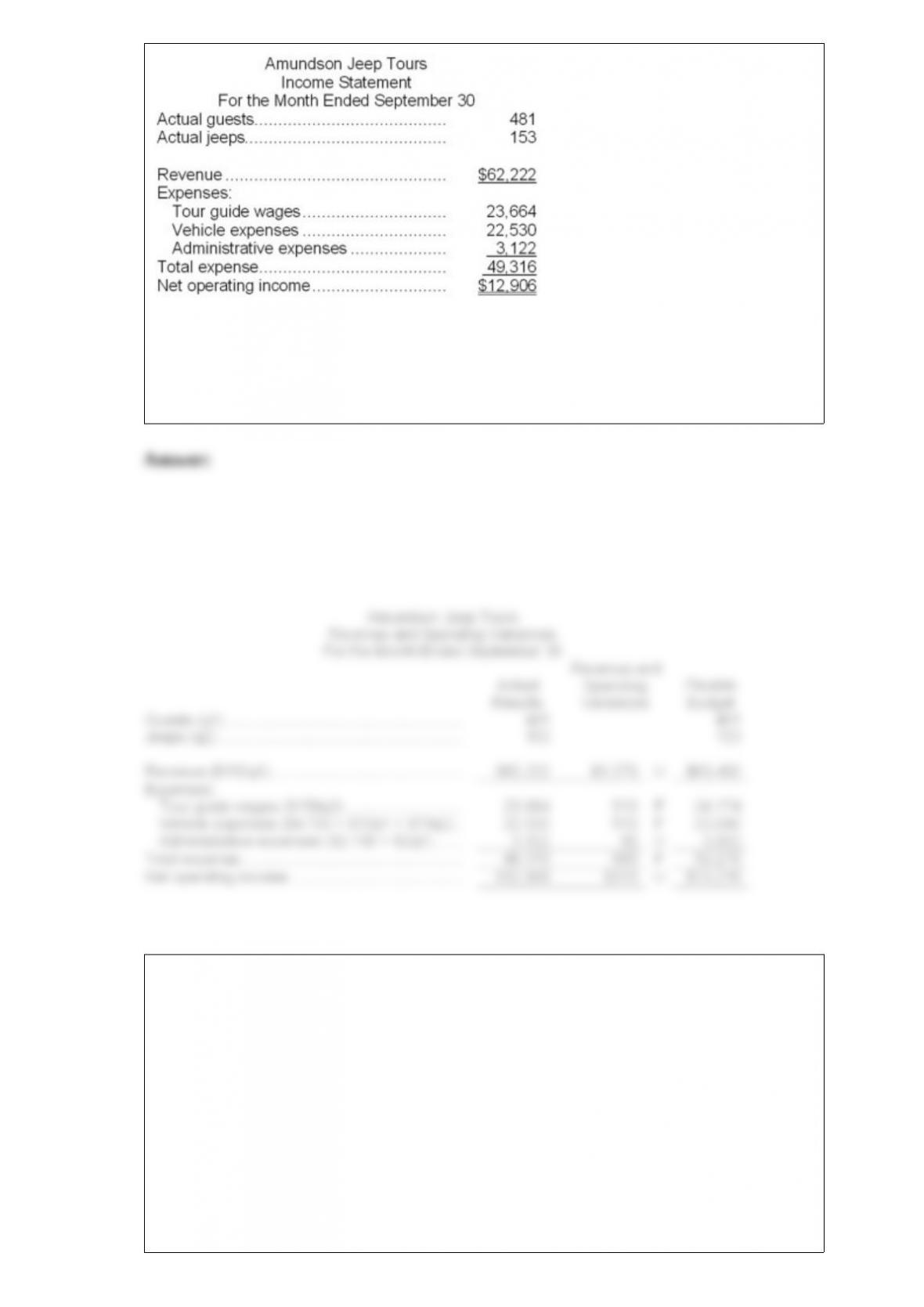

29) Amundson Jeep Tours operates jeep tours in the heart of the Colorado Rockies. The

company bases its budgets on two measures of activity (i.e., cost drivers), namely

guests and jeeps. One vehicle used in one tour on one day counts as a jeep. Each jeep

has one tour guide. The company uses the following data in its budgeting:

In September, the company budgeted for 456 guests and 155 jeeps. The company’s

income statement showing the actual results for the month appears below:

Required:

Prepare a report showing the company’s revenue and spending variances for September.

Label each variance as favorable (F) or unfavorable (U).

30) Some companies use process costing and some use job-order costing. Which

method a company uses depends on its industry. A number of companies in different

industries are listed below:

1) Contract printer that produces posters, books, and pamphlets to order

2) Corn meal mill

3) Cattle feedlot that fattens cattle prior to slaughter

4) Shirt manufacturer that makes clothing on contract for department stores

5) Commercial photographer

Required:

For each company, indicate whether the company is most likely to use job-order costing

or process costing.

31) Rossetto Corporation bases its budgets on the activity measure customers served.

During January, the company planned to serve 30,000 customers, but actually served

33,000 customers. Revenue is $4.10 per customer served. Wages and salaries are

$36,000 per month plus $1.50 per customer served. Supplies are $0.50 per customer

served. Insurance is $12,000 per month. Miscellaneous expenses are $4,800 per month

plus $0.10 per customer served.

Required:

Prepare a report showing the company’s activity variances for January. Indicate in each

case whether the variance is favorable (F) or unfavorable (U).

32) Sehrt Corporation has provided the following financial data:

The company’s net income for Year 2 was $44,000. Dividends on common stock during

Year 2 totaled $11,000. The market price of common stock at the end of Year 2 was

$6.29 per share.

33) Data concerning Kurek Corporation’s single product appear below:

Fixed expenses are $190,000 per month. The company is currently selling 4,000 units

per month.

Required:

The marketing manager would like to cut the selling price by $12 and increase the

advertising budget by $11,100 per month. The marketing manager predicts that these

two changes would increase monthly sales by 1,500 units. What should be the overall

effect on the company’s monthly net operating income of this change? Show your work!

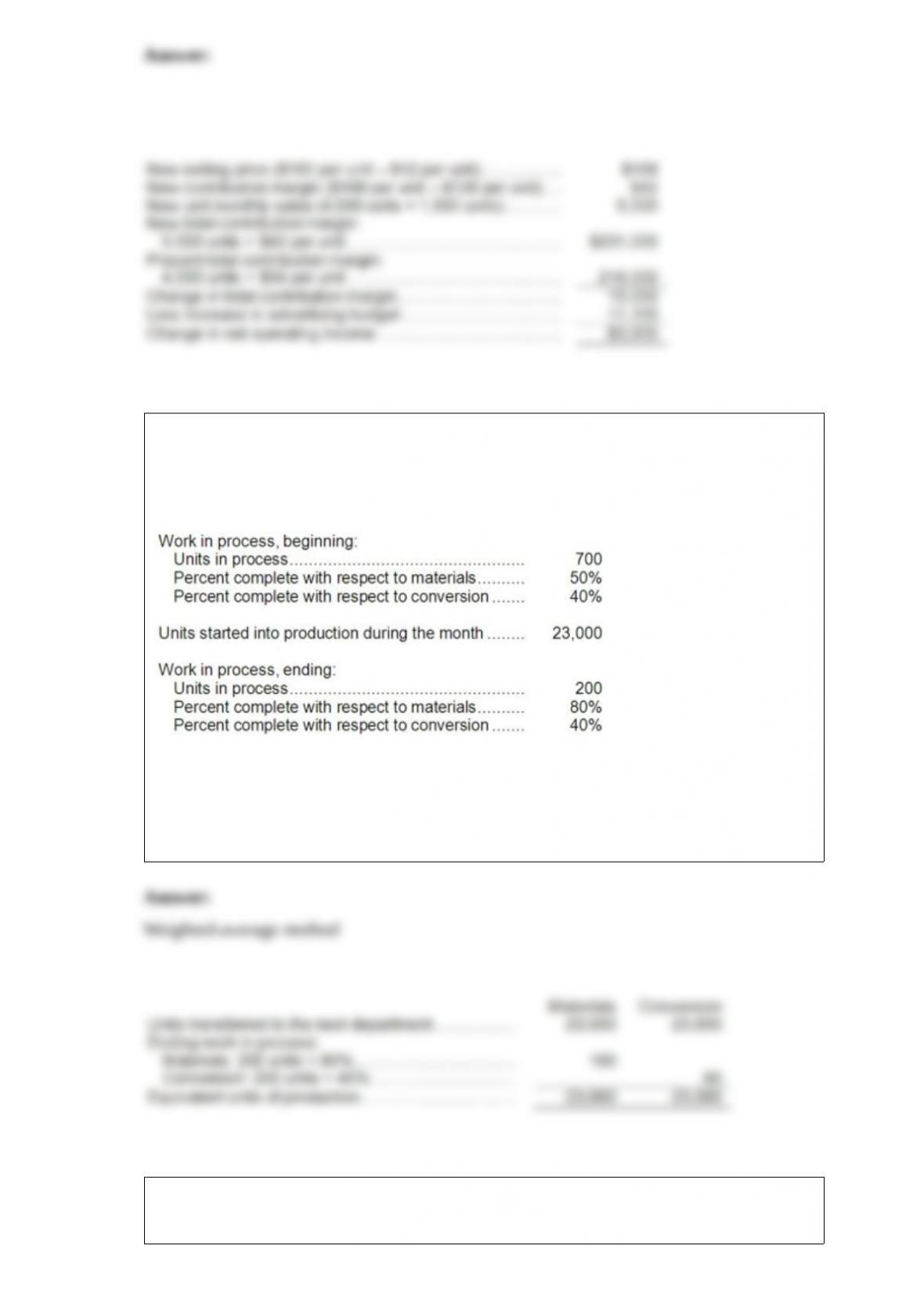

34) Carver Inc. uses the weighted-average method in its process costing system. The

following data concern the operations of the company’s first processing department for

a recent month.

Required:

Using the weighted-average method, determine the equivalent units of production for

materials and conversion costs.

35) ( Janes, Inc., is considering the purchase of a machine that would cost $400,000 and

would last for 5 years, at the end of which, the machine would have a salvage value of

$67,000. The machine would reduce labor and other costs by $109,000 per year.

Additional working capital of $4,000 would be needed immediately, all of which would

be recovered at the end of 5 years. The company requires a minimum pretax return of

12% on all investment projects.

Required:

Determine the net present value of the project. Show your work!

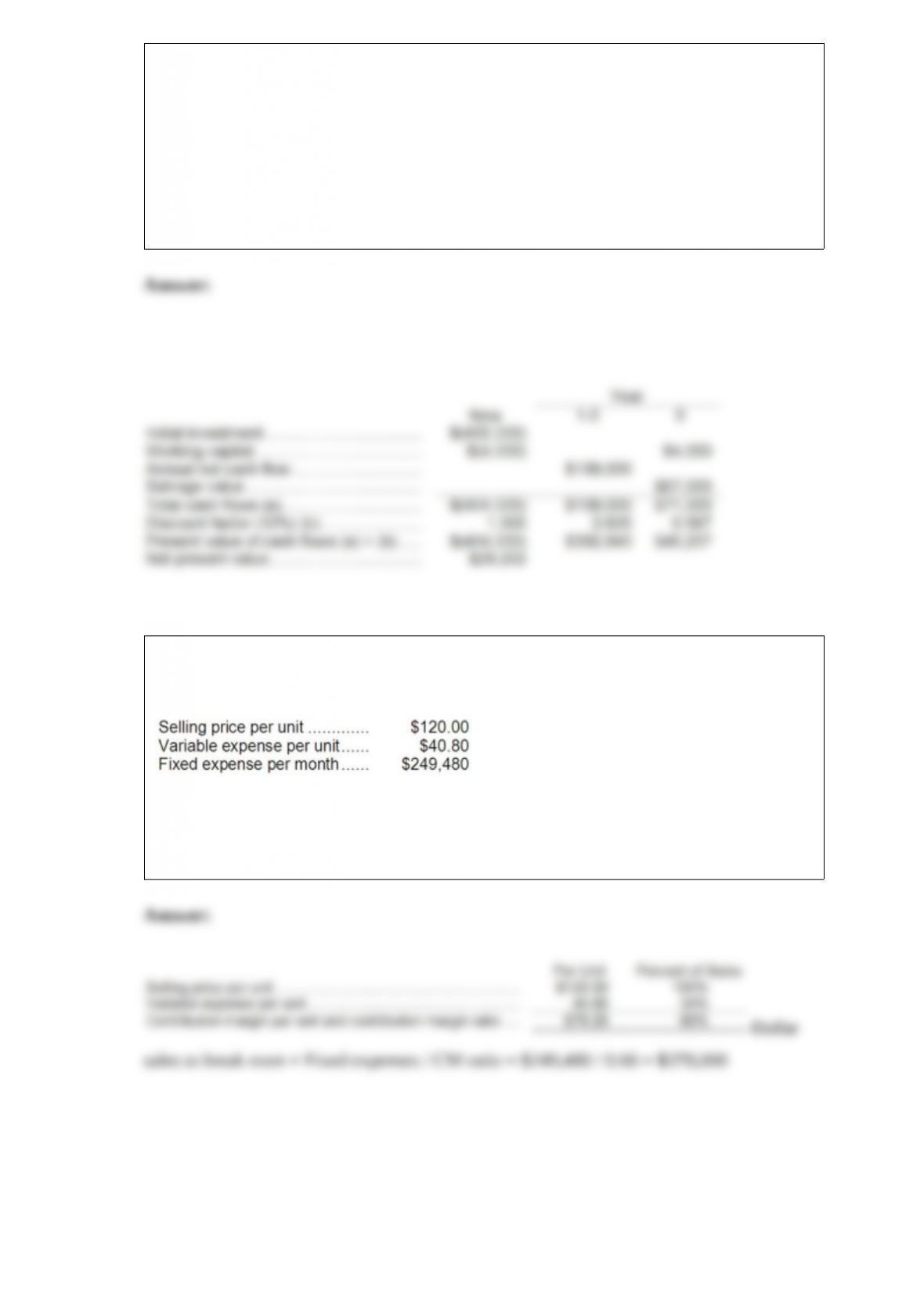

36) Pultz Corporation produces and sells a single product. Data concerning that product

appear below:

Required:

Determine the monthly break-even in total dollar sales. Show your work!