1) Minor Company installs a machine in its factory at the beginning of the year at a cost

of $135,000. The machine’s useful life is estimated to be 5 years, or 300,000 units of

product, with a $15,000 salvage value. During its first year, the machine produces

64,500 units of product. What journal entry would be needed to record the machines’

first year depreciation under the units-of-production method?

A.Debit Depletion Expense $25,800; credit Accumulated Depletion $25,800.

B.Debit Depletion Expense $29,025; credit Accumulated Depletion $29,025.

C.Debit Depreciation Expense $29,025; credit Accumulated Depreciation $29,025.

D.Debit Depreciation Expense $25,800; credit Accumulated Depreciation $25,800.

E.Debit Amortization Expense $24,000; credit Accumulated Amortization $24,000.

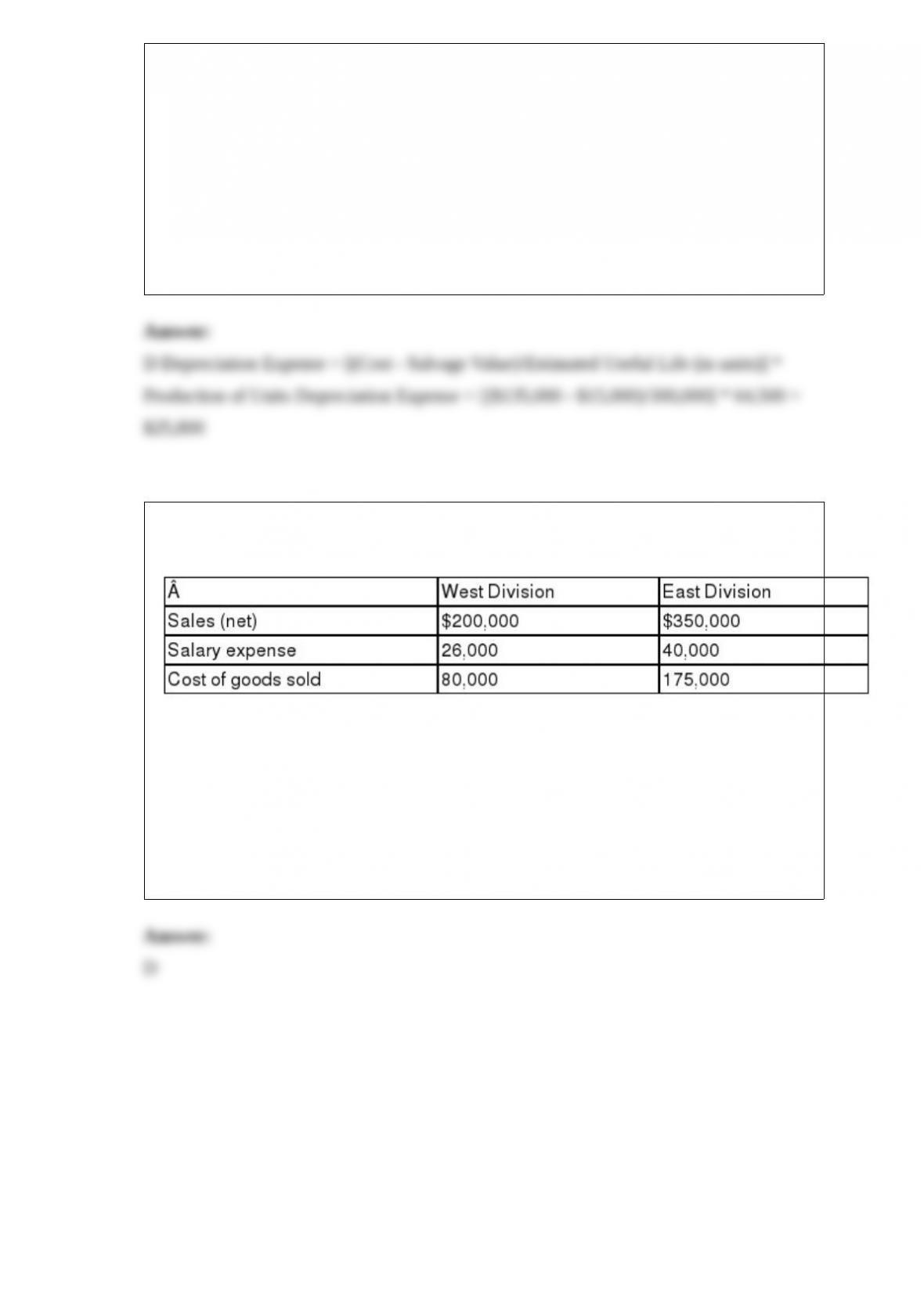

2) Fallow Corporation has two separate profit centers. The following information is

available for the most recent year:

The West Division occupies 5,000 square feet in the plant. The East Division occupies

3,000 square feet. Rent, which was $40,000 for the year, is an indirect expense and is

allocated based on square footage. Compute operating income for the West Division.

A.$120,000.

B.$95,000.

C.$94,000.

D.$69,000.

E.$54,000.

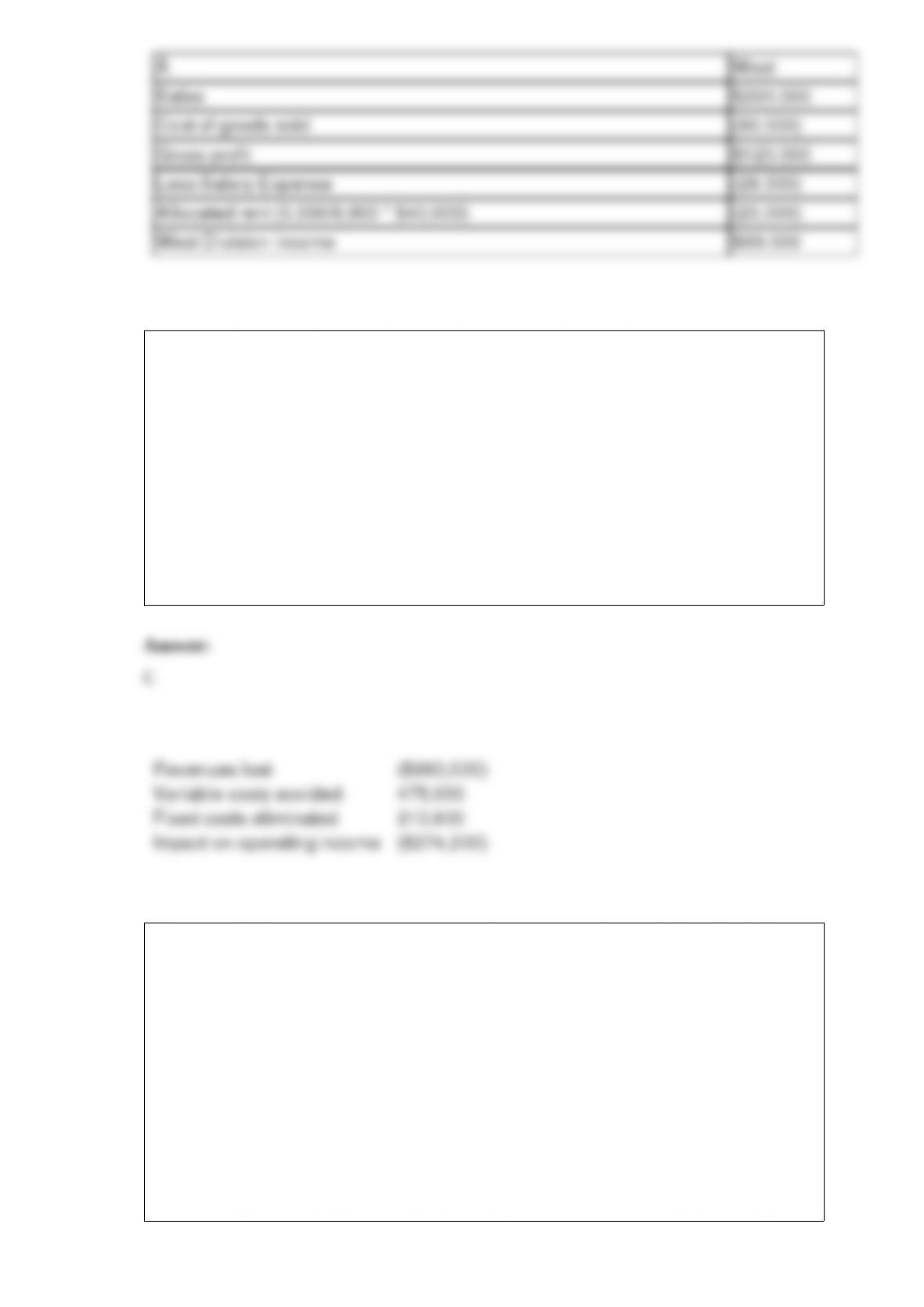

3) Granfield Company is considering eliminating its backpack division, which reported

an operating loss for the recent year of $42,000. The division sales for the year were

$960,000 and the variable costs were $475,000. The fixed costs of the division were

$527,000. If the backpack division is dropped, 40% of the fixed costs allocated to that

division could be eliminated. The impact on Granfield’s operating income for

eliminating this business segment would be:

A.$485,000 decrease

B.$210,800 increase

C.$274,200 decrease

D.$485,000 increase

E.$274,200 increase

4) A company uses the FIFO method for inventory costing. At the start of the period the

production department had 20,000 units in beginning Work in Process inventory which

were 40% complete; the department completed and transferred 165,000 units. At the

end of the period, 22,000 units were in the ending Work in Process inventory and are

75% complete. The production department had labor costs in the beginning goods is

process inventory of $99,000 and total labor costs added during the period are

$726,825. Compute the equivalent cost per unit for labor.

A.$4.40.

B.$4.76.

C.$4.19.

D.$4.55.

E.$4.61.

5) Materials that are used in manufacturing but are not clearly identified with specific

product units are called:

A.Secondary materials.

B.General materials.

C.Direct materials.

D.Indirect materials.

E.Materials inventory.

6) A bank does not issue a debit memorandum to notify the depositor of which of the

following?

A.All withdrawals through an ATM.

B.A fee assessed to the depositor’s account.

C.An uncollectible check.

D.Periodic payments arranged in advance, by a depositor.

E.A deposit to their account.

7) The process of adding the Debit column totals, then the credit column totals of a

journal and comparing the two sums for equality is an example of:

A.Crossfooting.

B.Footing.

C.Journalizing.

D.Posting.

E.Reconciling.

8) A company’s fixed interest expense is $8,000, its income before interest expense and

income taxes is $32,000. Its net income is $9,600. The company’s times interest earned

ratio equals:

A.0.25.

B.0.30.

C.0.83.

D.3.33.

E.4.0.

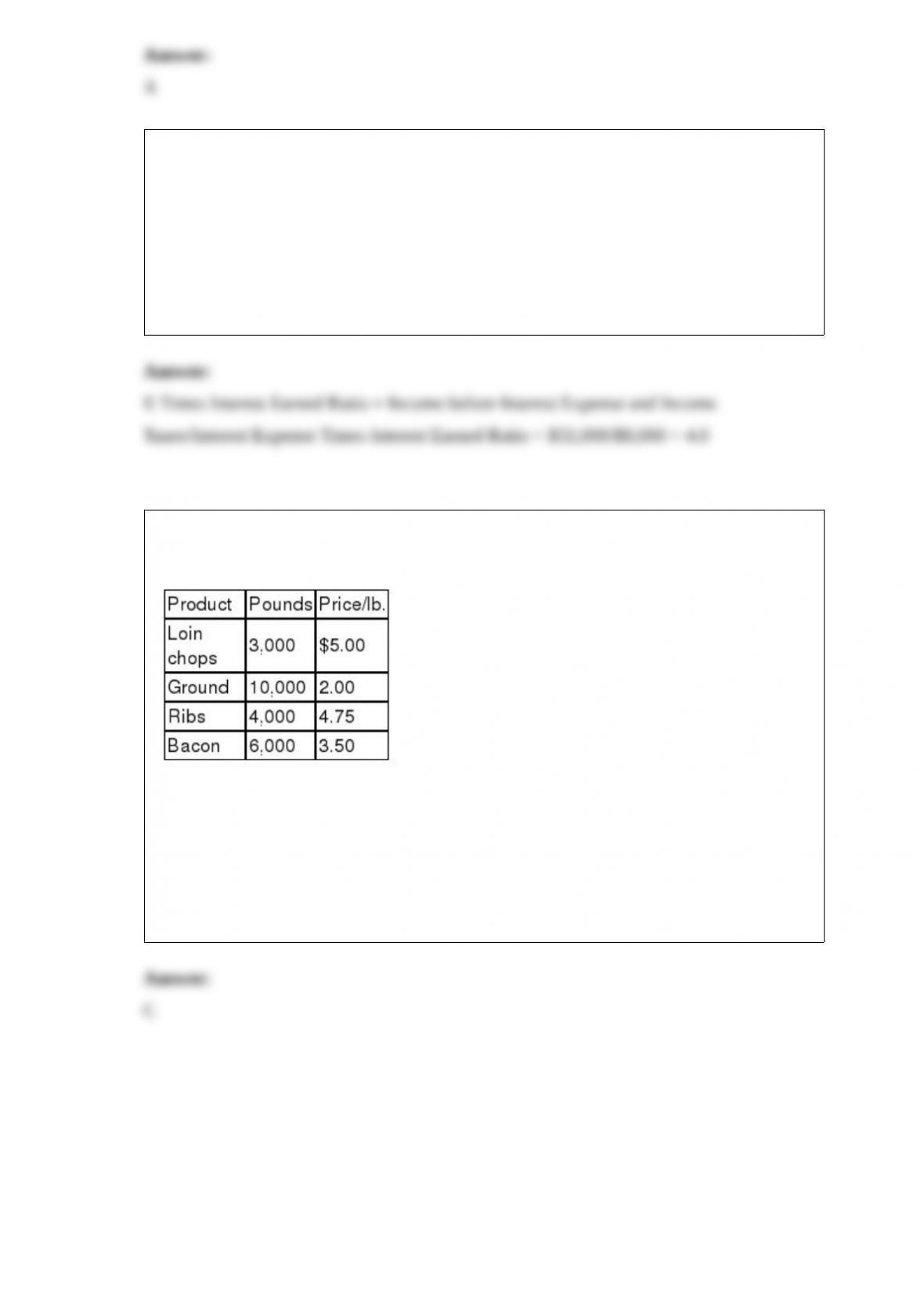

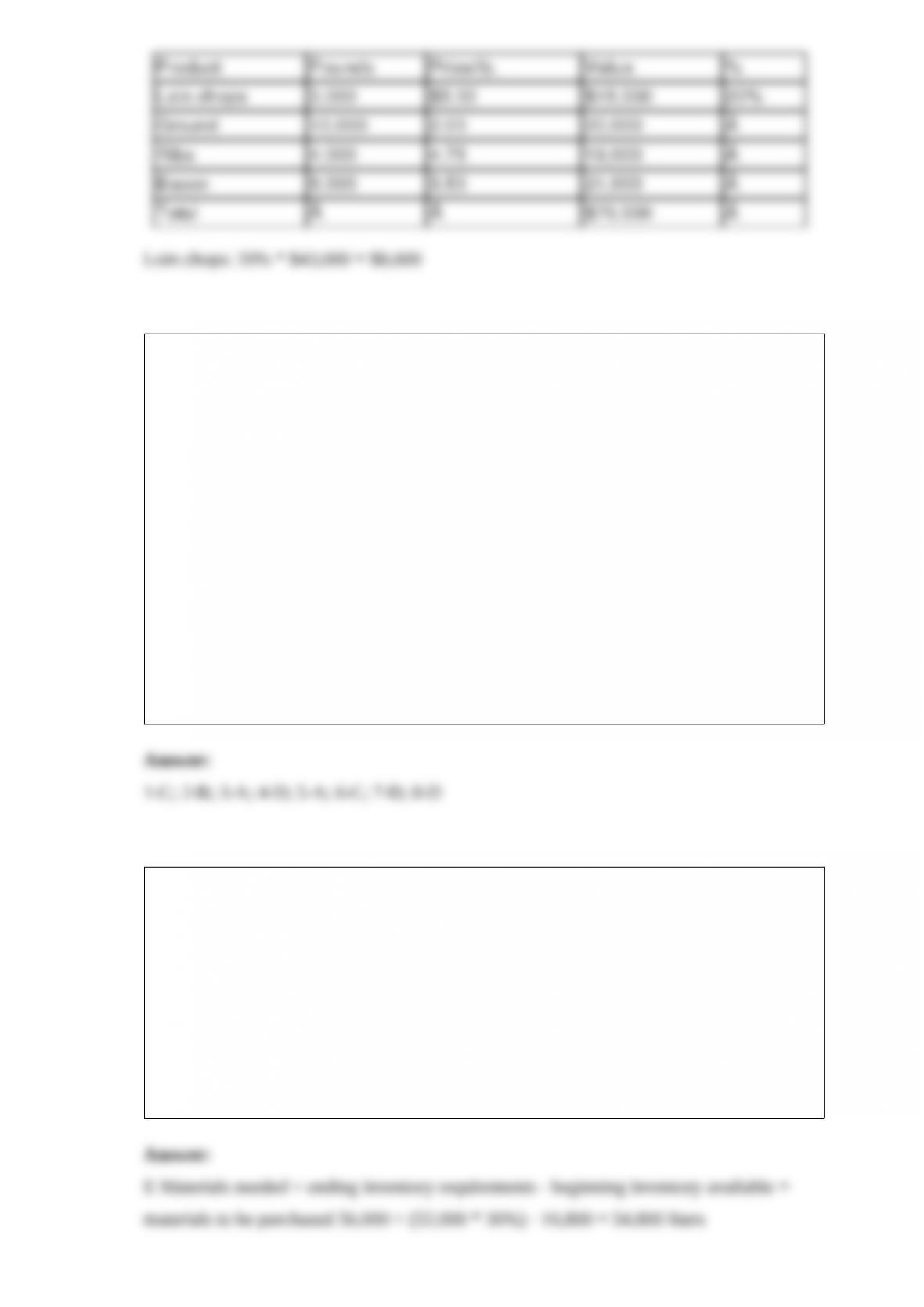

9) Wren Pork Company uses the relative market value method of allocating joint costs

in its production of pork products. Relevant information for the current period follows:

The total joint cost for the current period was $43,000. How much of this cost should

Wren Pork allocate to Loin chops?

A.$0.

B.$5,909.

C.$8,600.

D.$10,750.

E.$43,000.

10) Match each of the following items 1 through 8 with the financial statement a

through d in which each item would most likely appear. An item may appear on more

than one statement.

a. Income statement

b. Statement of owner’s equity

c. Balance sheet

d. Statement of cash flows

_____1> Assets.

_____2> Withdrawals.

_____3> Revenues.

_____4> Cash from investing activities.

_____5> Expenses.

_____6> Liabilities.

_____7> Cash from operating activities.

_____8> Cash from financing activities.

11) Masterson Company’s budgeted production calls for 56,000 liters in April and

52,000 liters in May of a key raw material that costs $1.85 per liter. Each month’s

ending raw materials inventory should equal 30% of the following month’s budgeted

materials. The January 1 inventory for this material is 16,800 liters. What is the

budgeted materials need in liters for April?

A.71,600 liters.

B.39,200 liters.

C.57,600 liters.

D.56,000 liters.

E.54,800 liters.

12) All of the following statements regarding accounting treatments for liabilities under

U.S. GAAP and IFRS are true except:

A.Accounting for bonds and notes under U.S. GAAP and IFRS is similar.

B.Both U.S. GAAP and IFRS require companies to distinguish between operating

leases and capital leases.

C.The criteria for identifying a lease as a capital lease are more general under IFRS.

D.Both U.S. GAAP and IFRS require companies to record costs of retirement benefits

as employees work and earn them.

E.Use of the fair value option to account for bonds and notes is not acceptable under

U.S. GAAP or IFRS.

13) The B&T Company’s production costs for May are: direct labor, $13,000; indirect

labor, $6,500; direct materials, $15,000; property taxes on production equipment, $800;

heat, lights and power, $1,000; and insurance on plant and equipment, $200. B&T

Company’s factory overhead incurred for May is:

A.$2,000.

B.$6,500.

C.$8,500.

D.$21,500.

E.$36,500.

14) Land improvements are:

A.Assets that increase the usefulness of land, and like land, are not depreciated.

B.Assets that increase the usefulness of land, but that have a limited useful life and are

subject to depreciation.

C.Included in the cost of the land account.

D.Expensed in the period incurred.

E.Also called basket purchases.

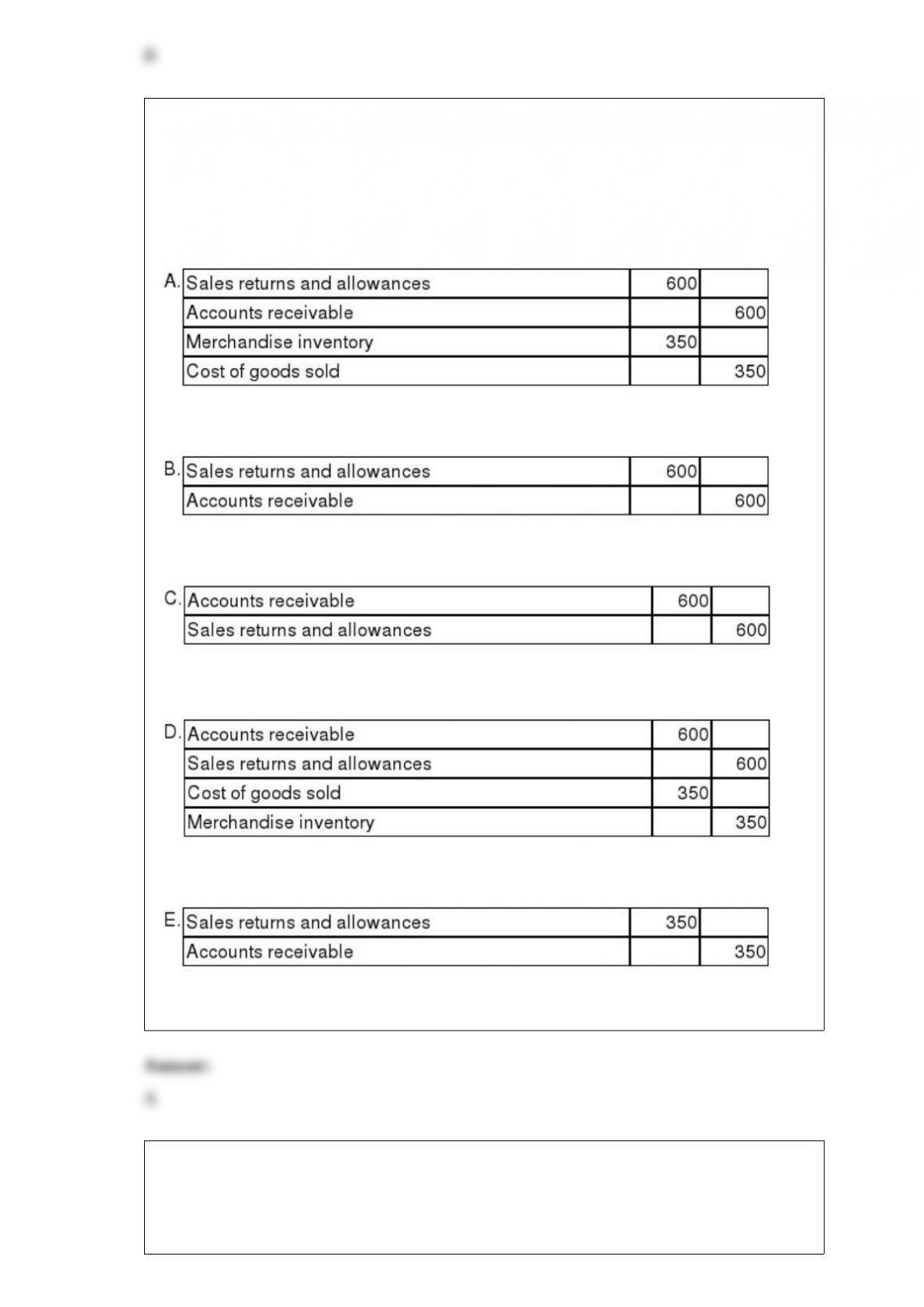

15) On March 12, Klein Company sold merchandise in the amount of $7,800 to Babson

Company, with credit terms of 2/10, n/30. The cost of the items sold is $4,500. Klein

uses the perpetual inventory system. On March 15, Babson returns some of the

merchandise. The selling price of the returned merchandise is $600 and the cost of the

merchandise returned is $350. The entry or entries that Klein must make on March 15

is:

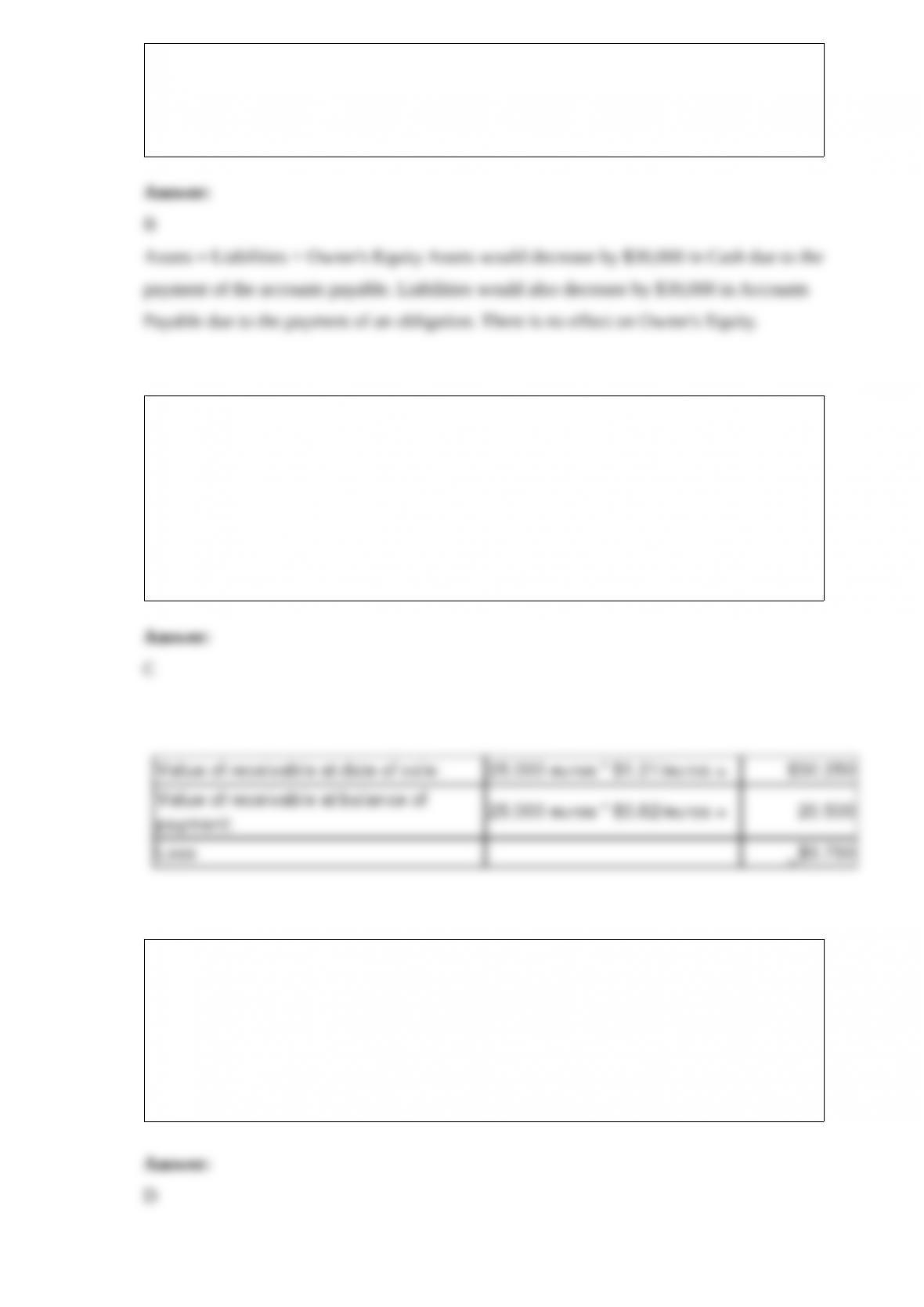

16) Saddleback Company paid off $30,000 of its accounts payable in cash. What would

be the effects of this transaction on the accounting equation?

A.Assets, $30,000 increase; equity, $30,000 increase.

B.Assets, $30,000 decrease; liabilities, $30,000 decrease.

C.Assets, $30,000 decrease; liabilities, $30,000 increase.

D.Liabilities, $30,000 decrease; equity, $30,000 increase.

E.Assets, $30,000 decrease; equity $30,000 decrease.

17) Marshall Company sold supplies in the amount of ¬25,000 (euros) to a French

company when the exchange rate was $1.21 per euro. At the time of payment, the

exchange rate decreased to $0.82. Marshall must record a:

A.gain of $9,750.

B.gain of $20,500.

C.loss of $9,750.

D.loss of $20,500.

E.neither a gain nor loss.

18) Which of the following is not one of the perspectives used to analyze performance

using the balanced scorecard?

A.Customer

B.Financial/owners

C.Internal process

D.Number of employees

E.Innovation and learning

19) Claymore Corp. has the following information about its standards and production

activity for September. The controllable variance is:

A.$1,295U.

B.$1,295F.

C.$2,400U.

D.$2,400F.

E.$3,695U.

20) Jasper makes a $25,000, 90-day, 7% cash loan to Clayborn Co. Jasper’s entry to

record the transaction should be:

A.Debit Notes Receivable for $25,000; credit Cash $25,000.

B.Debit Accounts Receivable $25,000; credit Notes Receivable $25,000.

C.Debit Cash $25,000; credit Notes Receivable for $25,000.

D.Debit Notes Payable $25,000; credit Accounts Payable $25,000.

E.Debit Notes Receivable $25,000; credit Sales $25,000.

21) MacArthur, Strong, and Viet form a partnership. MacArthur contributes $190,000

cash and Strong contributes $200,000 in cash. Viet contributes equipment worth

$215,000. Prepare the single journal entry to record the formation of this partnership.

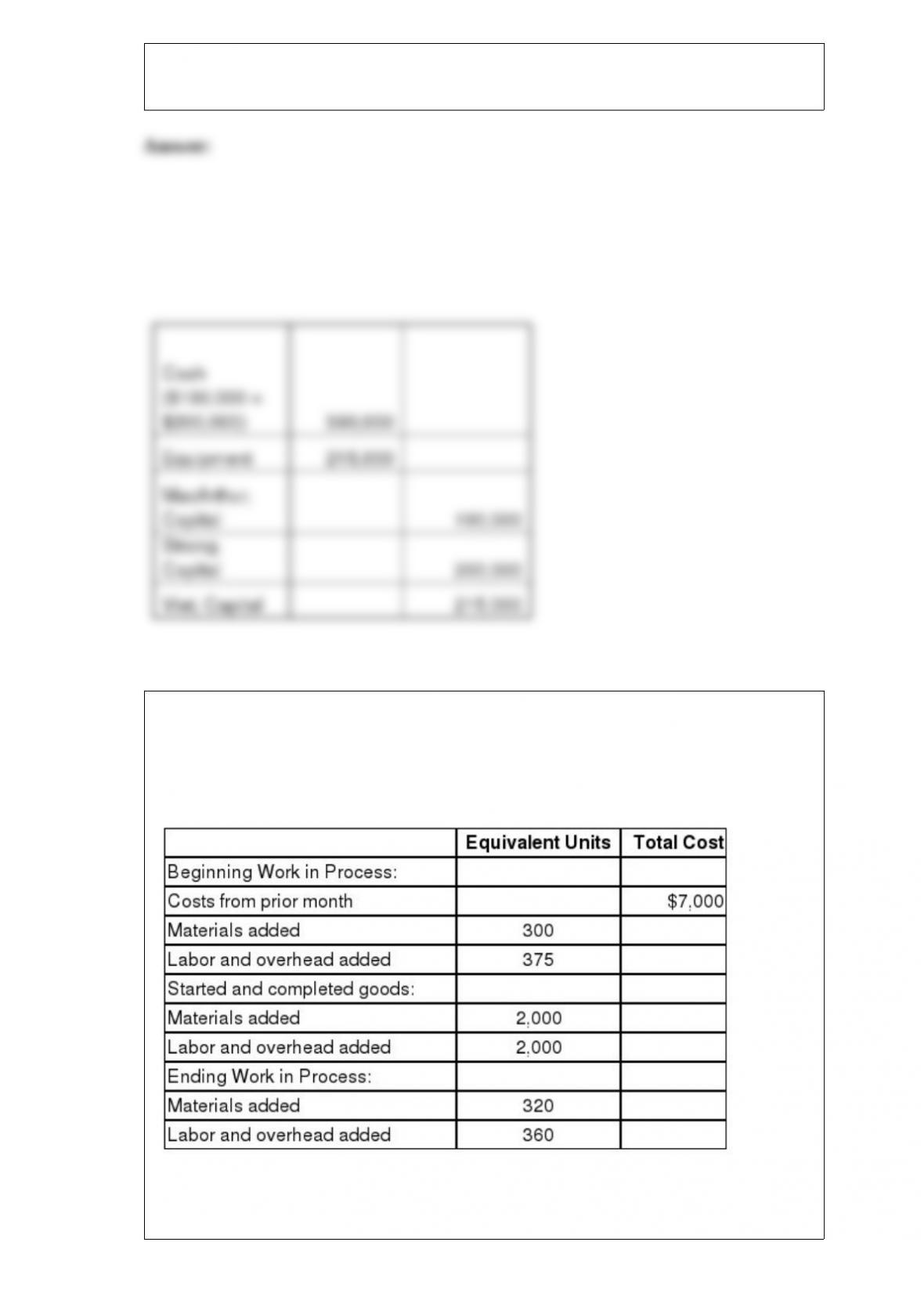

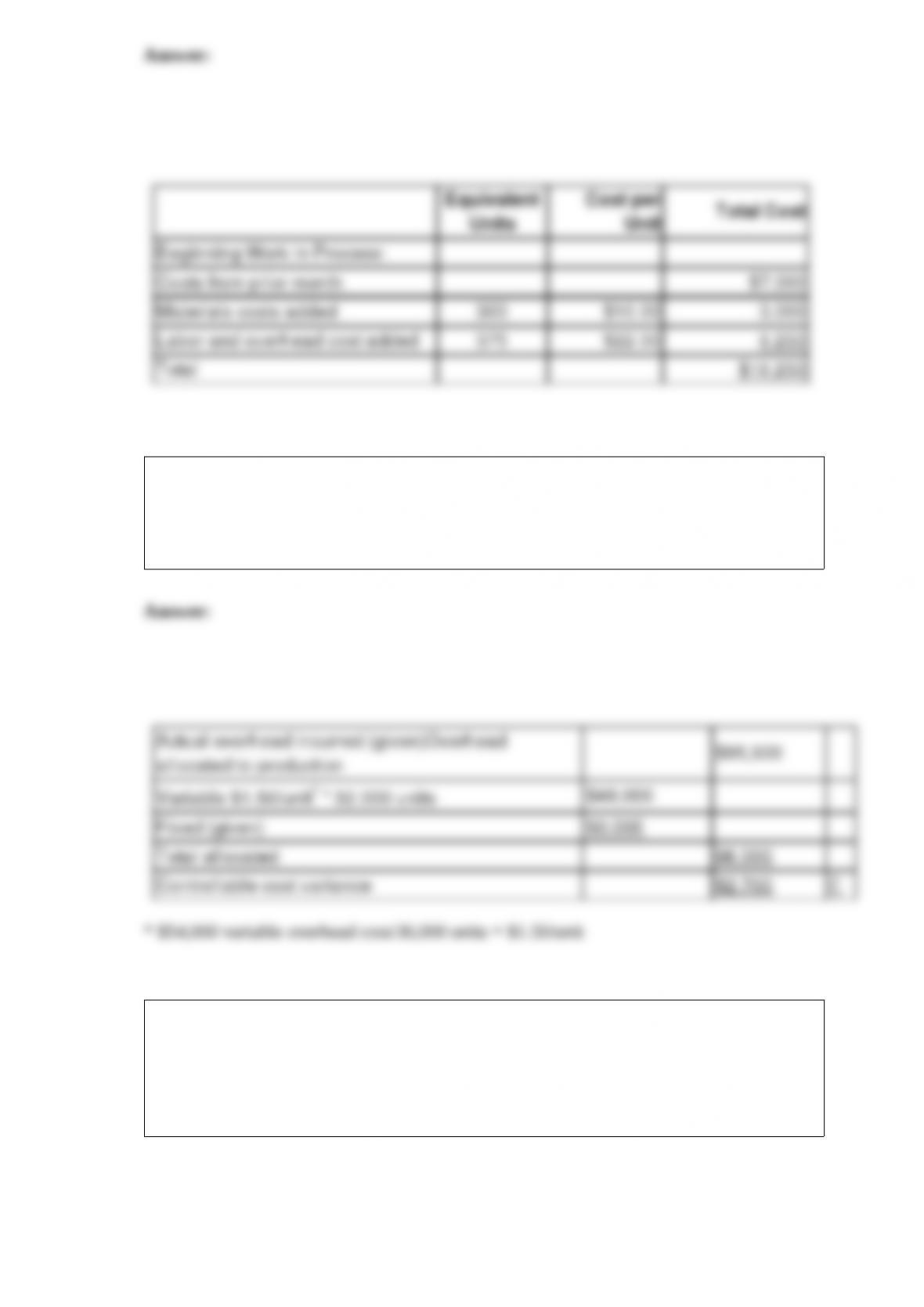

22) Refer to the following information about the Shaping Department of the Minnesota

Factory for the month of August. Minnesota Factory uses the FIFO method of inventory

costing.

The cost per equivalent unit of materials is $10.00, and the cost per equivalent unit of

labor and overhead is $22.00. Compute the cost that should be assigned to the

beginning units that were completed and transferred during August.

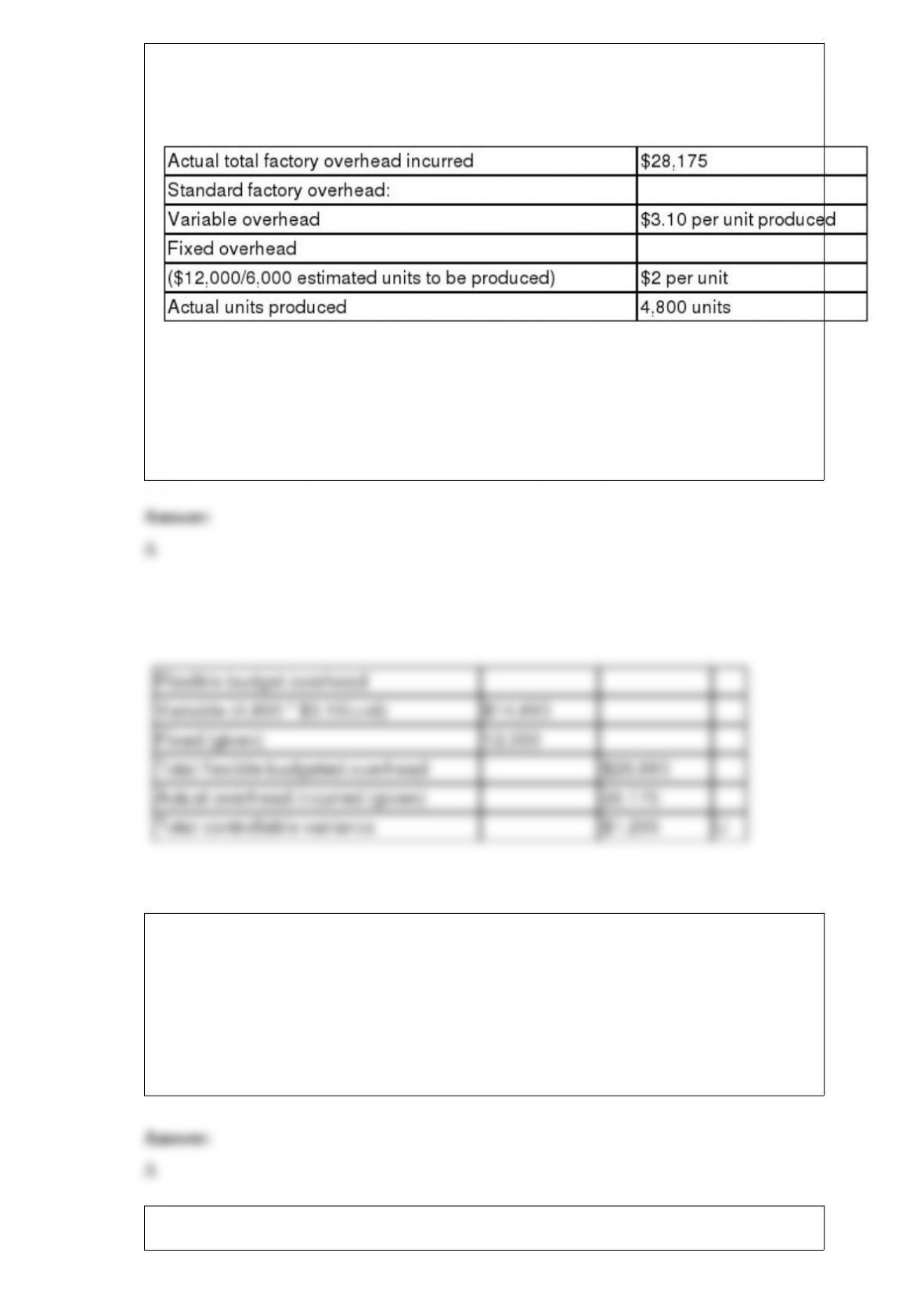

23) A company’s flexible budget for 36,000 units of production showed variable

overhead costs of $54,000 and fixed overhead costs of $50,000. The company actually

incurred total overhead costs of $95,300 while operating at a volume of 32,000 units.

What is the controllable variance?

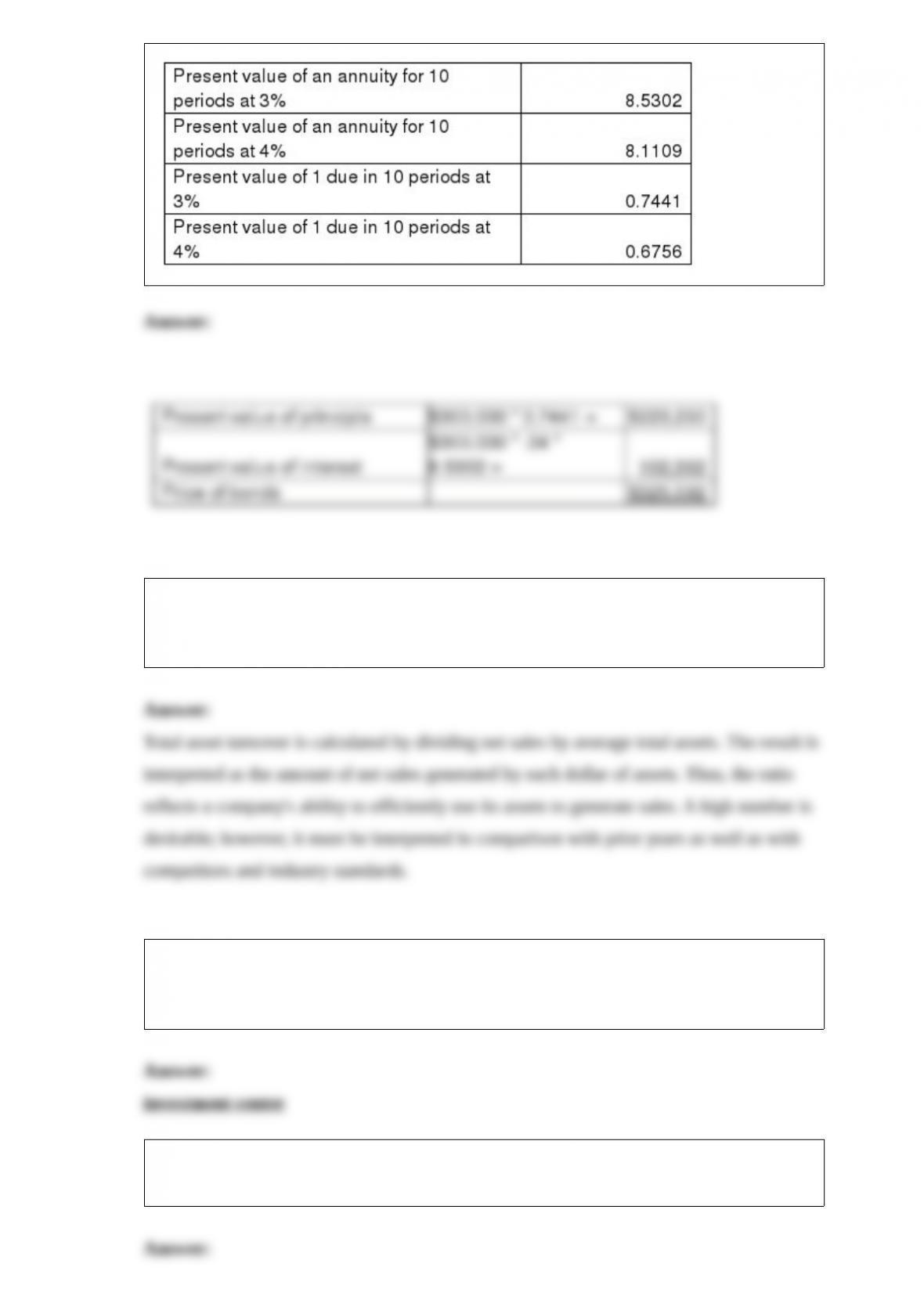

24) On January 1, a company issues 8%, 5 year, $300,000 bonds that pay interest

semiannually each June 30 and December 31. On the issue date, the annual market rate

of interest is 6%. Compute the price of the bonds on their issue date. The following

information is taken from present value tables:

25) Explain how to calculate total asset turnover. Describe what it reveals about a

company’s financial condition, whether a higher or lower ratio is desirable, and how it

is best applied for comparative purposes.

26) A(n) _______________________ is a department that generates revenues and

incurs costs and whose manager is also responsible for using the center’s assets to

generate income for the center.

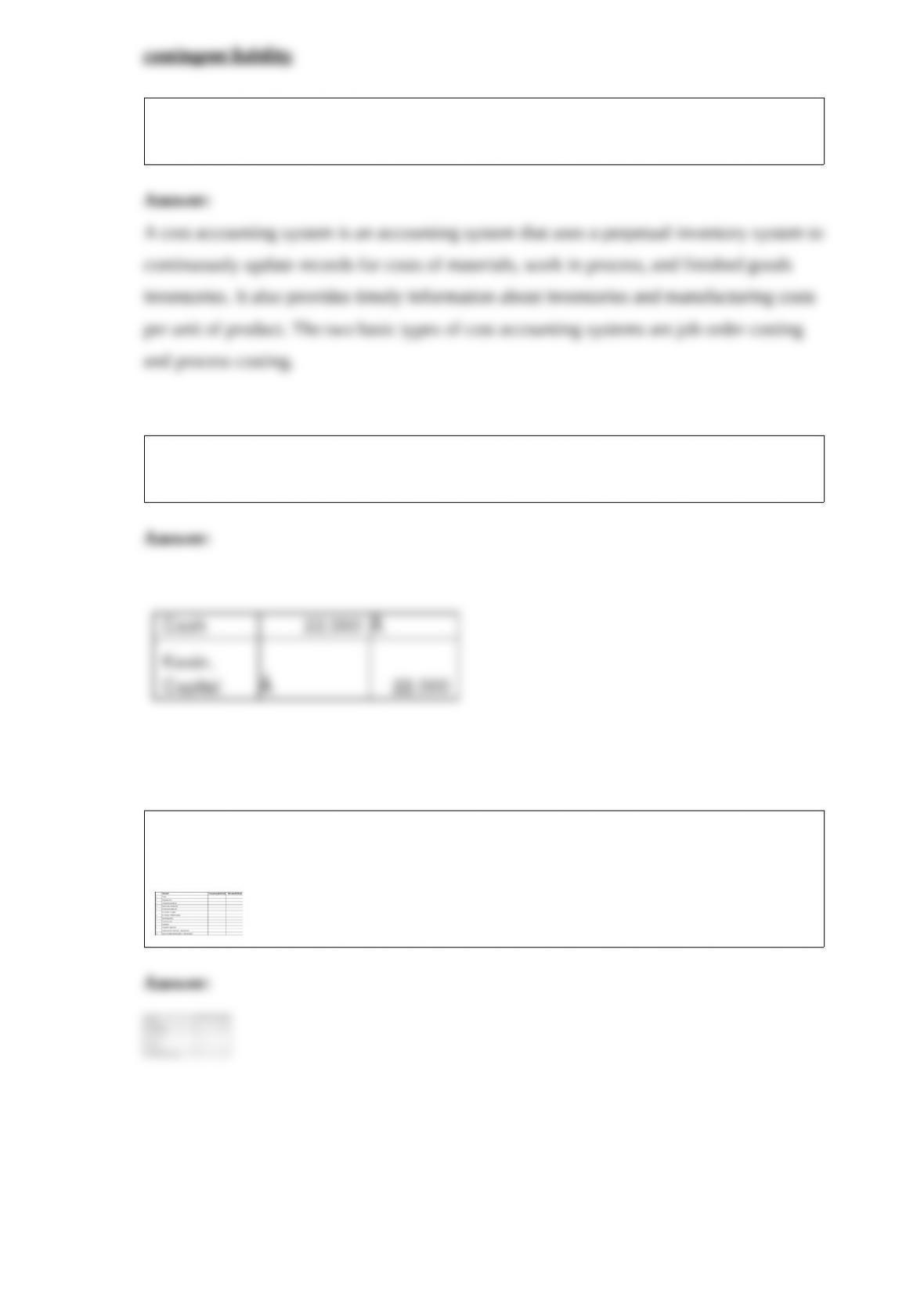

27) A ___________________ is a potential obligation that depends on a future event

arising from a past transaction or event.

28) What is a cost accounting system? What are the two basic types of cost accounting

systems?

29) Darien and Hayden agree to accept Kevin into their partnership. Kevin will

contribute $22,000 in cash. Prepare the journal entry to record this transaction.

30) In the table below, indicate with an “X” in the proper column whether the account is

a temporary (nominal) account or a permanent (real) account.