1) the current market value of a bond is equal to the present value of all future cash

payments promised by the bond.

2) the current ratio takes into account the composition of current assets.

3) a debit balance in the retained earnings account is identified as a deficit.

4) using borrowed money to increase the rate of return on common stockholders’ equity

is called “trading on the equity.”

5) a change in the estimated salvage value of a plant asset requires a restatement of

prior years’ depreciation.

6) dividends received on stock investments of less than 20% should be credited to the

stock investments account.

7) debt investments are investments in government and corporation bonds.

8) a change in accounting principle occurs when the principle used in the current year is

different from the one used by competitors in the current year.

9) dividends in arrears are liabilities of the corporation.

10) restricted retained earnings are available for preferred stock dividends but

unavailable for common stock dividends.

11) both profit margin and asset turnover affect a companys return on assets.

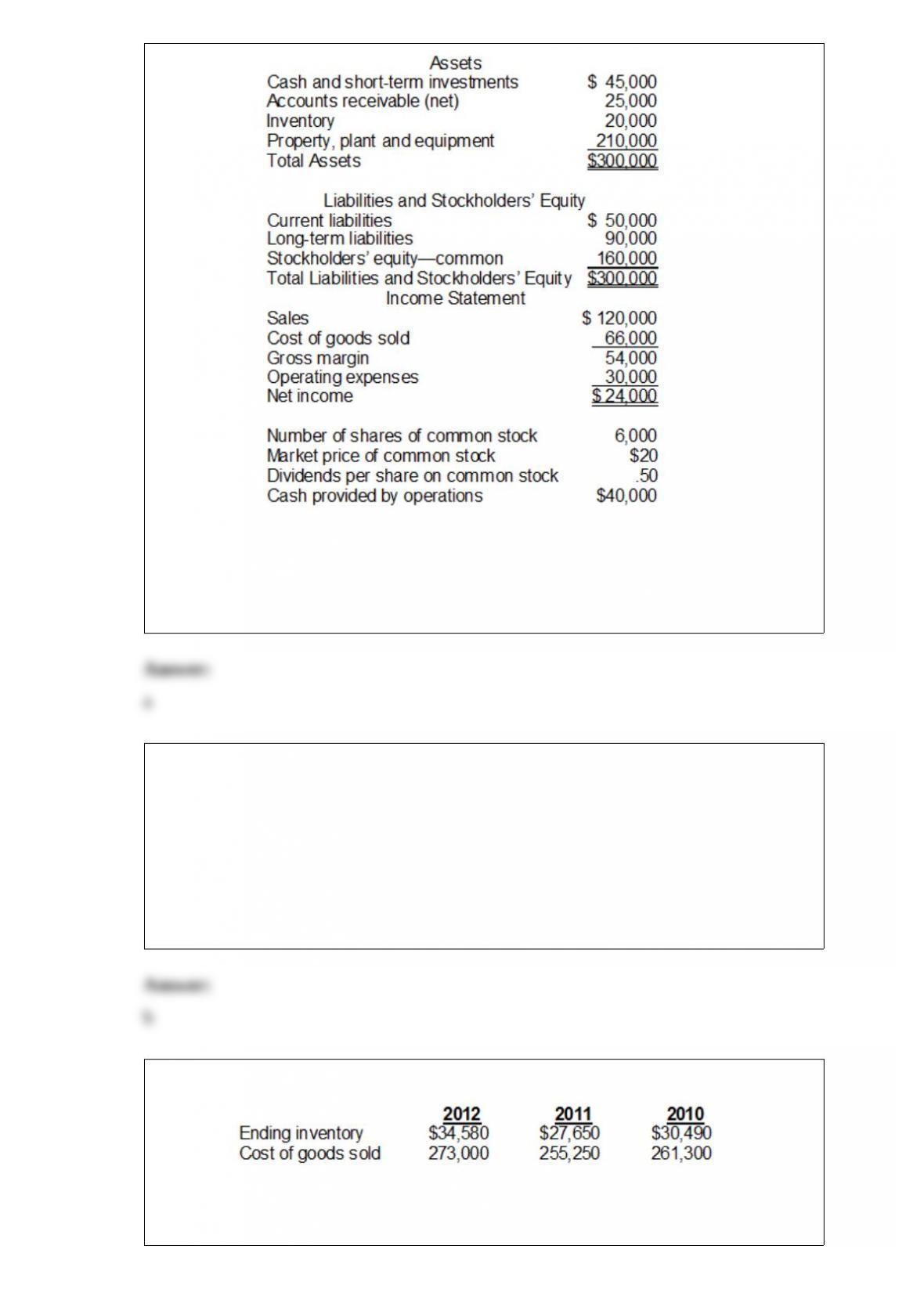

12) the following information is available for bradshaw corporation and newell

corporation:

based on this information, what is the amount of bradshaw’s earnings per share

(rounded to two decimals) for 2012?

a.$2.76

b.$2.50

c.$1.25

d.$1.32

13) the following information pertains to lance company. assume that all balance sheet

amounts represent both average and ending balance figures. assume that all sales were

on credit.

what is the inventory turnover for this company?

a.3.3 times

b.2 times

c.6 times

d.0.30 time

14) the board of directors of yancey company declared a cash dividend of $1.50 per

share on 42,000 shares of common stock on july 15, 2012. the dividend is to be paid on

august 15, 2012, to stockholders of record on july 31, 2012. the correct entry to be

recorded on july 15, 2012, will include a

a.debit to dividends payable

b.debit to cash dividends

c.credit to cash

d.credit to cash dividends

15) barnett company had the following records:

what is barnetts inventory turnover ratio for 2011? (rounded)

a.9.0 times

b.8.8 times

c.4.4 times

d.8.9 times

16) during january 2014, its first month of operation, osborn enterprises earned net

income of $1,700 and paid dividends to the owners of $500. at january 31, the balance

in retained earnings will be

a.$0.

b.$1,700 credit.

c.$1,200 credit.

d.$500 debit.

17) in developing the cash flows from operating activities, most companies in the

united states

a.use the direct method

b.use the indirect method

c.present both the indirect and direct methods in their financial reports

d.prepare the operating activities section on the accrual basis

18) when determining the proceeds received when issuing a bond, the factor applied to

the amount of the interest payments is determined from the table of the

a.present value of 1

b.present value of an annuity of 1

c.future value of 1

d.future value of an annuity of 1

19) (a)preferred stock may be cumulative. discuss this feature.

(b)how are dividends in arrears presented in the financial statements?

20) if total liabilities decreased by $4,000, then

a.stockholders equity must have decreased by $4,000.

b.assets must have decreased by $4,000, or stockholders equity must have increased by

$4,000.

c.assets and stockholders equity each increased by $2,000.

d.assets must have increased by $4,000.

21) comstock company provided consulting services and billed the client $2,500. as a

result of this event

a.assets remained unchanged.

b.assets increased by $2,500.

c.equity increased by $2,500

d.both assets and equity increased by $2,500.

22) belfry, inc. disposes of an unprofitable segment of its business. the operation of the

segment suffered a $160,000 loss in the year of disposal. the loss on disposal of the

segment was $80,000. if the tax rate is 30%, and income before income taxes was

$1,000,000,

a.the income tax expense on the income before discontinued operations is $228,000

b.the income from continuing operations is $700,000

c.net income is $760,000

d.the losses from discontinued operations are reported net of income taxes at $120,000

23) the harris company purchased a computer for $3,000 on december 1. it is estimated

that annual depreciation on the computer will be $600. if financial statements are to be

prepared on december 31, the company should make the following adjusting entry:

a.debit depreciation expense, $600; credit accumulated depreciation, $600

b.debit depreciation expense, $50; credit accumulated depreciation, $50

c.debit depreciation expense, $2,400; credit accumulated depreciation, $2,400

d.debit office equipment, $3,000; credit accumulated depreciation, $3,000

24) which of the following statements is true regarding the profit margin ratio?

a.the profit margin ratio can be improved by decreasing the gross profit rate and/or

controlling operating expenses and other costs

b.the profit margin ratio does not vary across industries

c.discount stores with high merchandise turnover generally have higher profit margins

d.if the profit margin ratio has a higher value, this suggests favorable return on each

dollar of sales

25) cost allocation of an intangible asset is referred to as

a.amortization

b.depreciation

c.accretion

d.capitalization

26) a.sales = $850,000; accounts receivable decreased by $40,000. calculate cash

receipts from sales.

b.cost of goods sold = $650,000; inventory increased by $22,000; accounts payable

increased by $28,000. calculate cash payments for purchases.

c.income statement shows $25,500 in income taxes. the balance sheet shows an increase

in taxes payable of $3,500. calculate the cash paid for income taxes.

d.operating expenses total $103,000; depreciation expense = $14,000; prepaid expenses

decreased by $13,000; accrued liabilities increased by $6,000. calculate cash payments

for operating expenses.

27) the managers of hong company receive performance bonuses based on the net

income of the firm. which inventory costing method are they likely to favor in periods

of declining prices?

a.lifo

b.average cost

c.fifo

d.physical inventory method

28) using the percentage of receivables method for recording bad debts expense,

estimated uncollectible accounts are $20,000. if the balance of the allowance for

doubtful accounts is $4,000 debit before adjustment what is the balance after

adjustment?

a.$20,000

b.$24,000

c.$16,000

d.$4,000

29) insert the qualitative characteristics listed below that are associated with relevance

and faithful representation.

30) on january 10 donna stark uses her baver co. credit card to purchase merchandise

from baver co. for $2,100. on february 10, she is billed for the amount due of $2,100.

on february 12 stark pays $1,600 on the balance due. on march 10 stark is billed for the

amount due, including interest at 1% per month on the unpaid balance as of february

12.

instructions

prepare the entries on baver co.’s books related to the transactions that occurred on

january 10, february 12, and march 10.

31) the adjusting entry for accrued salaries requires a debit to salaries payable.

32) west county bank agrees to lend drake builders company $100,000 on january 1.

drake builders company signs a $100,000, 6%, 6-month note. what is the adjusting

entry required if drake builders company prepares financial statements on march 30?

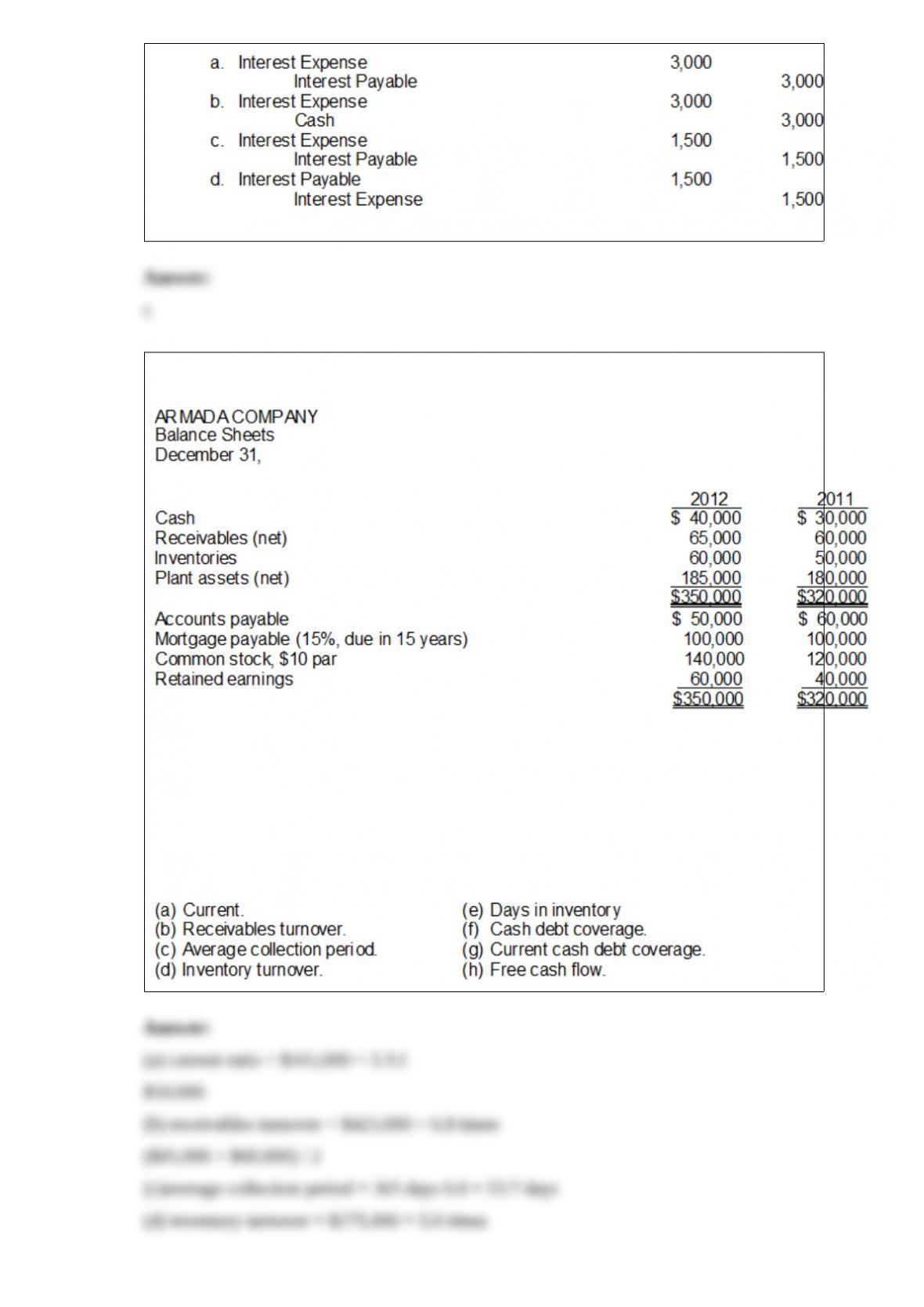

33) armada company has these comparative balance sheet data:

additional information for 2012:

1>net income was $25,000.

2>sales on account were $450,000. sales returns and allowances amounted to $25,000.

3>cost of goods sold was $275,000.

4>net cash provided by operating activities was $49,000.

5>capital expenditures were $23,000, and cash dividends were $18,000.

instructions

compute the following ratios at december 31, 2012.

34) when vacant land is acquired, expenditures for clearing, draining, filling, and

grading should be charged to the ______________ account.