Administrative functions are not included in the value chain because they are implicitly

included in every business function.

Answer:

The predetermined overhead rate is computed by dividing the estimated activity of the

allocation base into the estimated manufacturing overhead costs.

Answer:

The equivalent unit concept refers to the actual amount of work during the period

stated in terms of the work required to complete an equal number of whole units.

Answer:

At the end of the accounting period, manufacturing overhead costs are applied to

uncompleted jobs using the same predetermined overhead rate that is used to apply

manufacturing overhead costs to completed jobs.

Answer:

The degree of completion associated with prior department costs is always 100%.

Answer:

A problem with ratio-based measures is that managers can make decisions that improve

divisional income but lower total organizational income.

Answer:

Variances are the difference between actual results and budgeted results.

Answer:

Job costing requires more detailed recordkeeping than process costing.

Answer:

Two important characteristics to consider when deciding how many variances to

review are how large the variance is and the extent to which the variance can be

managed.

Answer:

In general, decreasing (or eliminating) the resources committed to nonvalue-added

activities will decrease customer response time.

Answer:

Target costs equal the difference between the target selling price and the desired profit

margin.

Answer:

A business model is a description of how different levels and employees in the

organization must perform for the organization to achieve its goals and objectives.

Answer:

The selection of an appropriate cost allocation base is more important for single-stage

cost allocation systems than for two-stage cost allocation systems.

Answer:

The engineering method of determining cost behavior is particularly useful for totally

new activities or products.

Answer:

Actual costing does not use a predetermined overhead rate to apply manufacturing

overhead costs to jobs completed during the period.

Answer:

A flexible budget adjusts the static budget to reflect the actual activity level achieved

during the period.

Answer:

With the reciprocal method, the total service department costs less the direct costs of

the service department equals the cost allocated to the service department.

Answer:

The JK Manufacturing Company sells two products, J and K. J has a higher

contribution margin ratio than K. If the product mix shifts towards K, the company’s

break-even point in total units (i.e., J plus K) will increase.

Answer:

In general, cost behavior results are likely to differ between the engineering method

and the account analysis method.

Answer:

The flexible and master budget amounts are the same for fixed marketing and

administrative costs.

Answer:

An organization’s operating leverage is high when it has a low proportion of variable

costs in its total costs.

Answer:

Individual managers’ beliefs and expectations are incorporated into the budgeting

process using grass roots budgeting procedures.

Answer:

The sales budget drives the rest of the budgeting process for both manufacturers and

merchandisers.

Answer:

It is possible for units in the beginning Work-in-Process Inventory to also be part of the

ending Work-in-Process Inventory.

Answer:

The sales price variance is the actual selling price per unit times the difference between

budgeted number of units and the actual number of units sold.

Answer:

Theoretical capacity is the long-run expected volume based on reasonably attainable

working conditions.

Answer:

Internal failure costs include materials wasted in the production process and correcting

products before they are sold.

Answer:

The primary objective of benchmarking is to evaluate performance of an activity,

operation, or organization relative to the performance by other companies.

Answer:

A balanced scorecard is basically a balance sheet prepared using nonfinancial

measures.

Answer:

The direct labor yield variance is unfavorable when the total hours worked during a

period are less than the total standard hours allowed for the actual number of units

produced.

Answer:

Using net book values instead of gross book values to compute return on investment

(ROI) might encourage an investment center manager to delay replacing inefficient

assets until they are fully depreciated.

Answer:

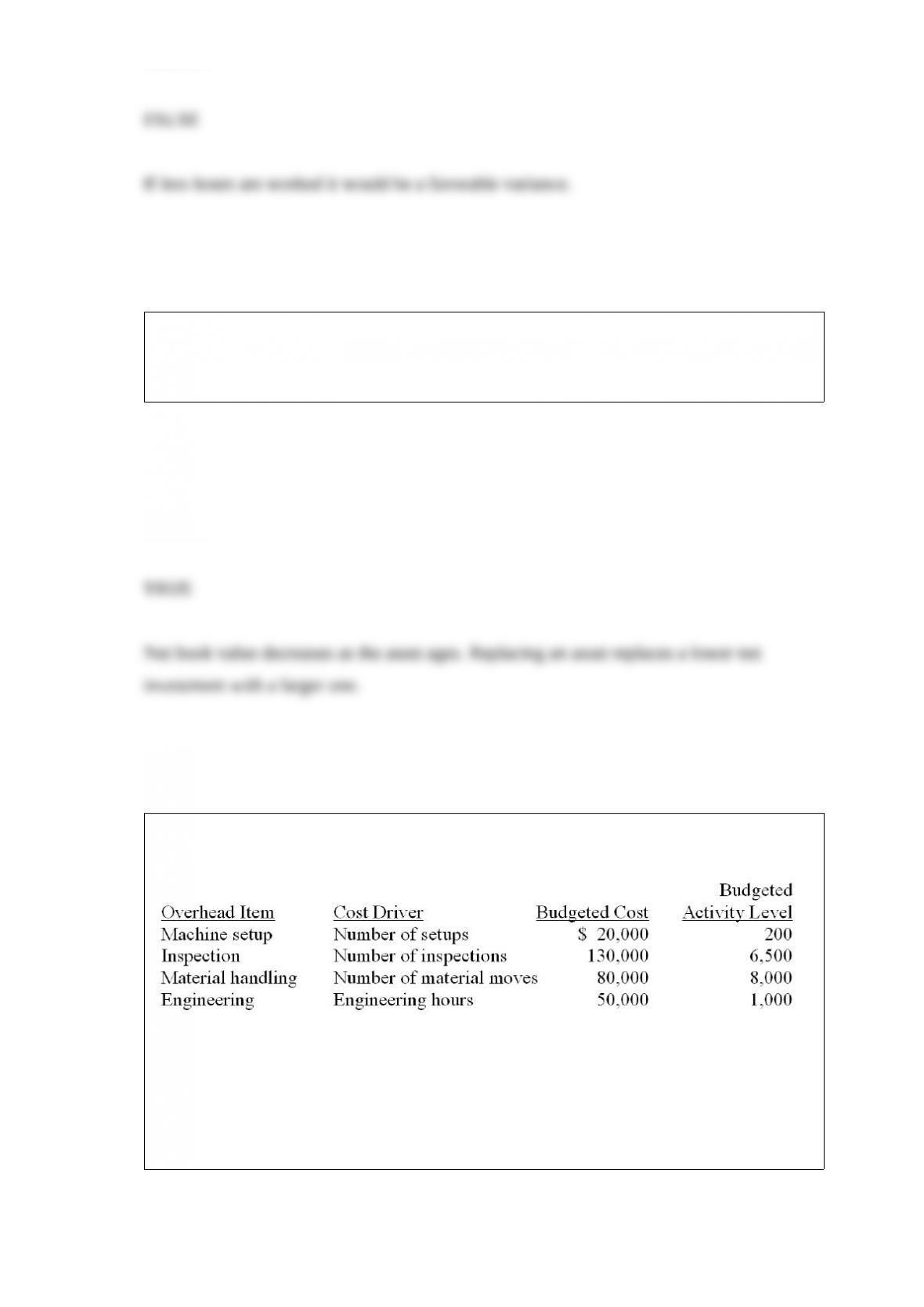

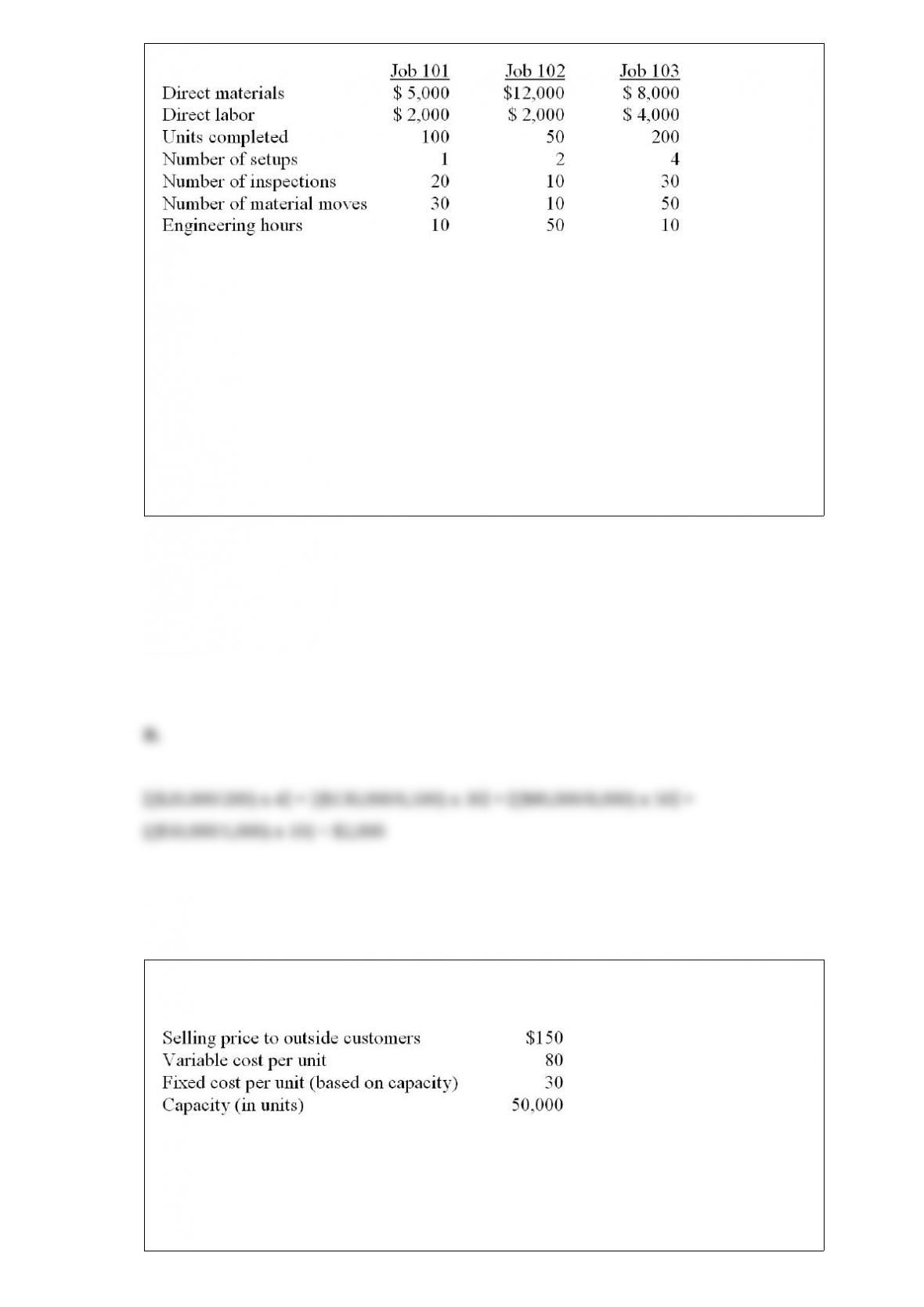

A company has identified the following overhead costs and cost drivers for the coming

year: (CIA adapted)

Budgeted direct labor cost was $100,000 and budgeted direct material cost was

$280,000. The following information was collected on three jobs that were completed

during the year:

If the company uses activity-based costing (ABC), how much overhead cost should be

assigned to Job 103?

A. $1,300

B. $2,000

C. $5,000

D. $5,600

Answer:

Given the following data for Division L:

Division N would like to purchase 10,000 units from Division L at a price of $125 per

unit. Division L has no excess capacity to handle Division N’s requirements. Division N

currently purchases from an outside supplier at a price of $140. If Division L accepts a

$125 price internally, the company, as a whole, will be better or worse off by

A. $600,000

B. ($100,000)

C. $115,000

D. $250,000

Answer:

In a decision analysis situation, which one of the following costs is not likely to contain

a variable cost component? (CMA adapted)

A. Labor

B. Overhead

C. Straight-line Depreciation

D. Selling

E. Material

Answer:

A master budget

A. drops the current month or quarter and adds a future month or quarter as the current

month or quarter is completed.

B. presents a statement of expectations for a period of time but does not present a firm

commitment.

C. presents the plan for only one level of activity and does not adjust to changes in the

level of activity.

D. presents the plan for a range of activity so that the plan can be adjusted for changes

in activity levels.

E. divides the activities of individual responsibility centers into a series of packages

which are ranked ordinally.

Answer:

The purpose of the flexible budget is to

A. allow management some latitude in meeting goals.

B. eliminate cyclical fluctuations in production reports by ignoring variable costs.

C. compare actual and budgeted results at virtually any level of production.

D. reduce the total time in preparing the annual budget.

Answer:

Cohasset Company currently manufactures all component parts used in the

manufacture of various hand tools. Hurley Division produces a steel handle used in

three different tools. The budget for these handles is 120,000 units with the following

unit cost.

Ironwood Division purchases 20,000 handles from Hurley Division and completes the

hand tools. An outside supplier, R & M Steel, has offered to supply 20,000 units of the

handle to Ironwood Division for $1.25 per unit. Hurley currently has idle capacity that

cannot be used.

If Cohasset would like to develop a range of transfer prices, what would be the

minimum transfer price that Hurley would be willing to accept?

A. $1.00

B. $1.10

C. $1.25

D. $1.30

Answer:

Excess direct labor wages resulting from overtime premium will be disclosed in which

type of variance? (CPA adapted)

A. Yield.

B. Quantity.

C. Labor efficiency.

D. Labor rate.

Answer:

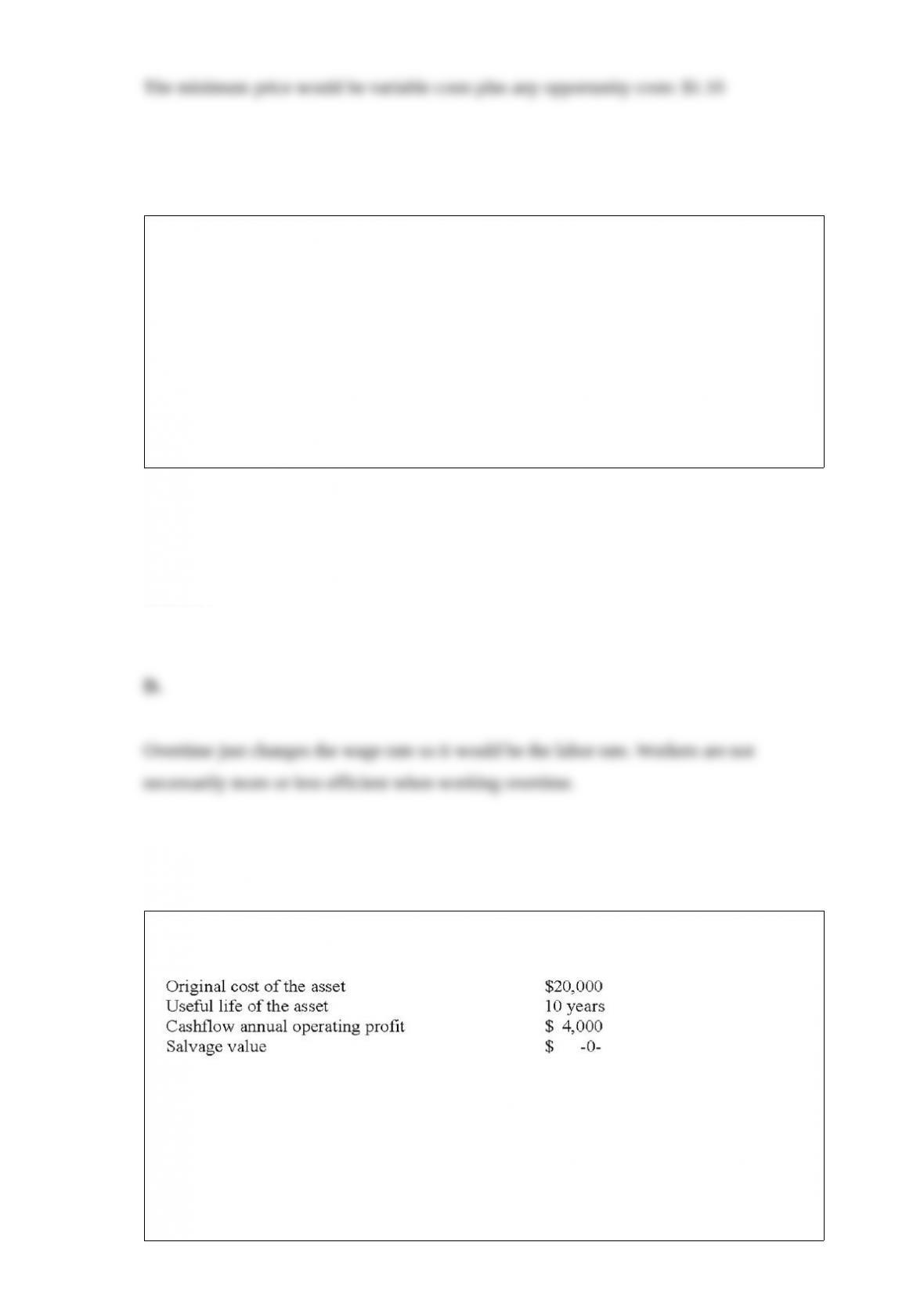

The following information was presented by Charlie Manufacturing Company for an

asset purchased at the beginning of the previous year.

What is the return on investment (ROI) assuming Charlie (a) uses the straight-line

method for depreciation and (b) average net book values to compute ROI?

A. 21.1%

B. 20.0%

C. 22.2%

D. 11.76%

Answer:

Cascade Cliffs, Inc., operates two divisions: (1) a management division that owns and

manages bulk carriers on the Great Lakes and (2) a repair division that operates a dry

dock in Cheboygan, Michigan. The repair division works on company ships, as well as

other large-hull ships.

The repair division has an estimated variable cost of $37 per labor-hour. The repair

division has a backlog of work for outside ships. They charge $70.00 per hour for labor,

which is standard for this type of work. The management division complained that it

could hire its own repair workers for $45.00 per hour, including leasing an adequate

work area.

If the repair division had idle capacity, what is the minimum transfer price that the

repair division should obtain?

A. $33.00

B. $37.00

C. $45.00

D. $70.00

E. $82.00

Answer:

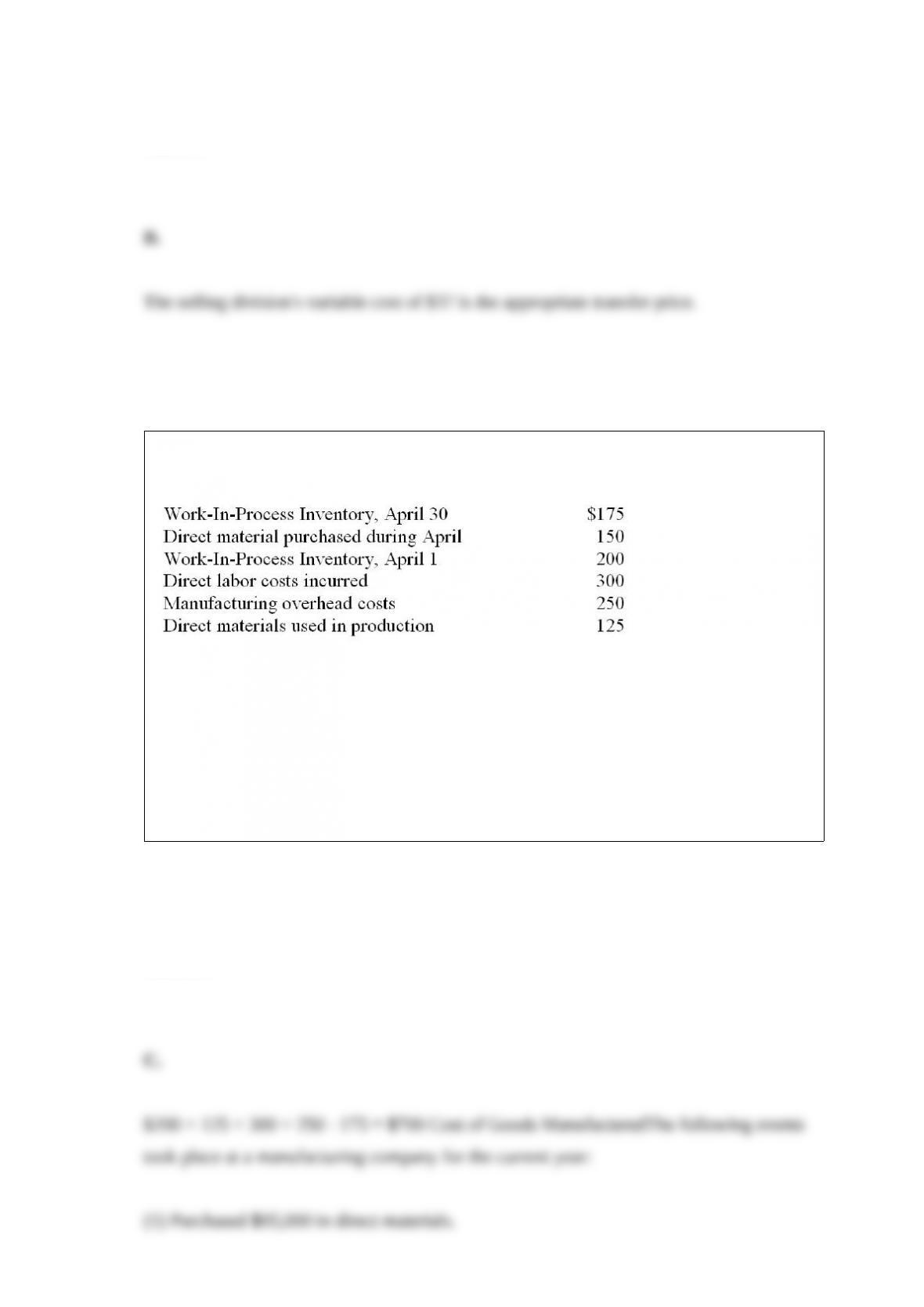

Compute the Work-in-Process transferred to the finished goods warehouse on April 30

using the following information:

A. $650

B. $675

C. $700

D. $750

Answer:

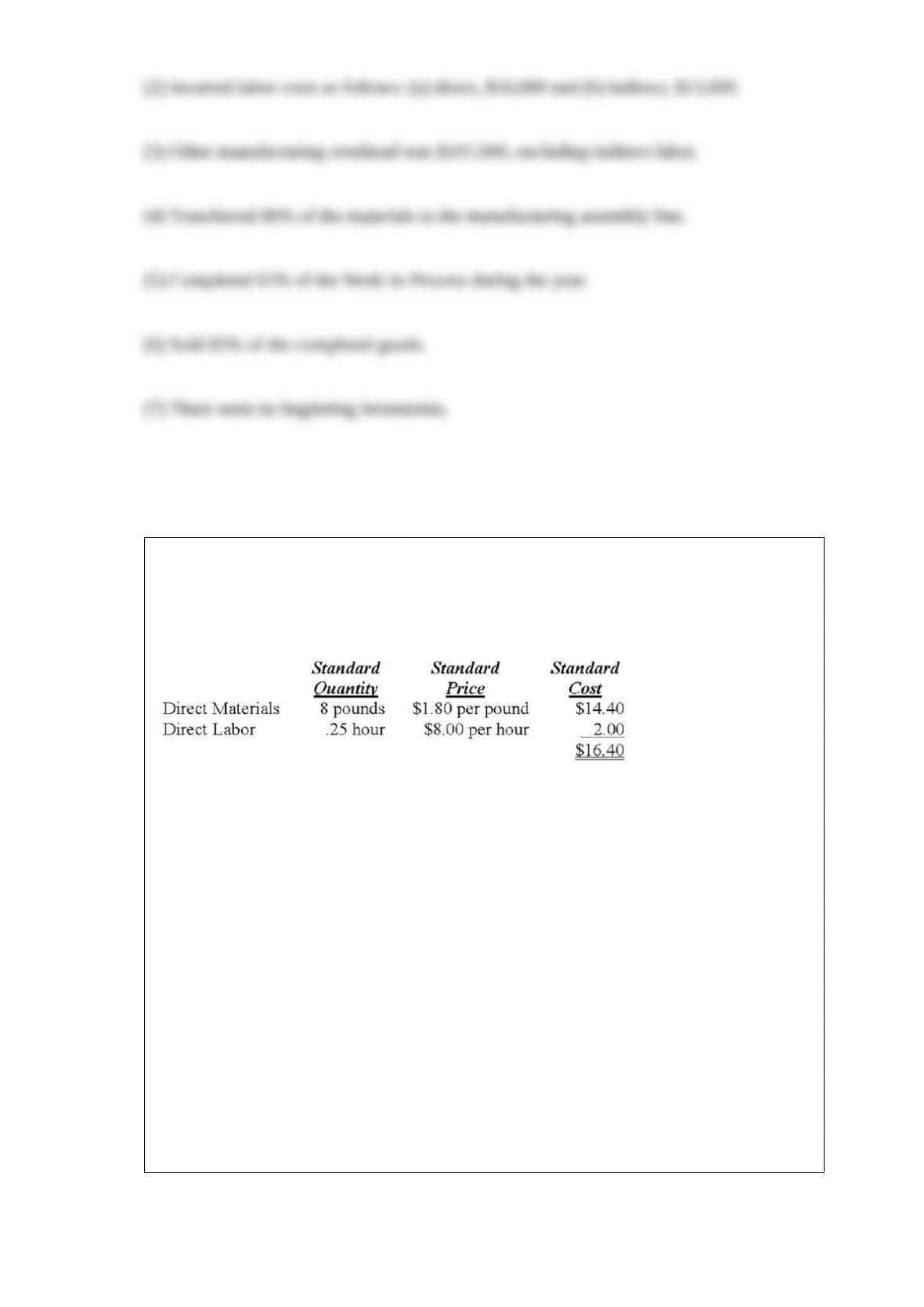

Arrow Industries employs a standard cost system in which direct materials inventory is

carried at standard cost. Arrow has established the following standards for the prime

costs of one unit of product.

During November, Arrow purchased 160,000 pounds of direct materials at a total cost

of $304,000. The total factory wages for November were $42,000, 90% of which were

for direct labor. Arrow manufactured 19,000 units of product during November using

142,500 pounds of direct materials and 5,000 direct labor hours.

What is the direct labor price (rate) variance for November?

A. $1,800

B. $1,900

C. $2,000

D. $2,090

E. $2,200

Answer:

Danner Corporation applies overhead based upon machine-hours. Budgeted factory

overhead was $375,000 and budgeted machine-hours were 12,500. Actual factory

overhead was $387,920 and actual machine-hours were 13,150.

Required:

a) Compute the overhead application rate.

b) Compute the amount of overhead applied to production.

c) Determine the amount of over- or underapplied overhead.

Answer:

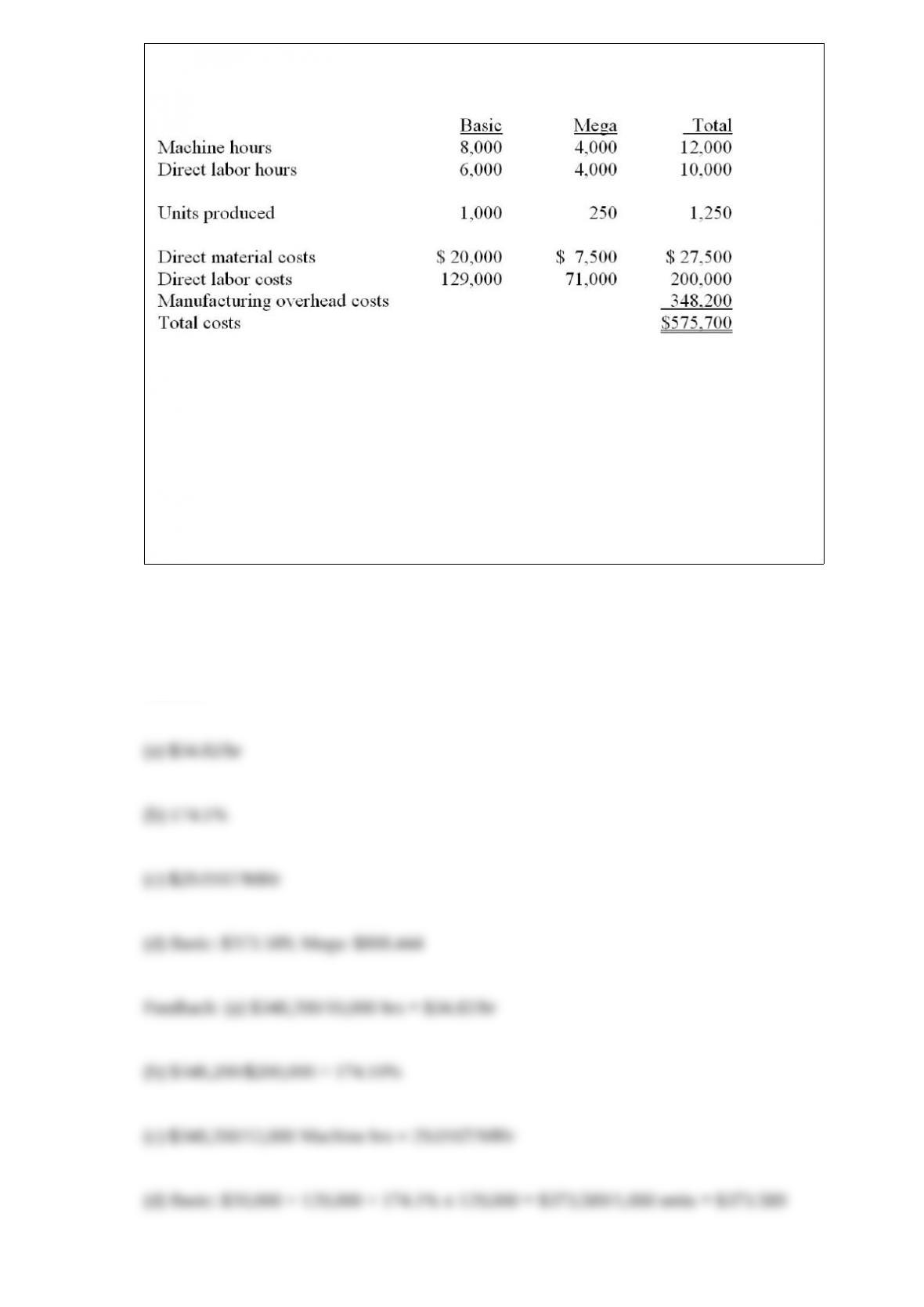

Loin Cabinetry produces two models of home shelving, the Basic and the Mega. Data

on operations and costs for November are:

Required: Compute the predetermined overhead rate, assuming Loin Cabinetry uses:

(a) Direct labor hours to allocate overhead costs.

(b) Direct labor costs to allocate overhead costs.

(c) Machine hours to allocate overhead costs.

(d) Compute the unit cost for each model using direct labor costs to allocate overhead.

Answer:

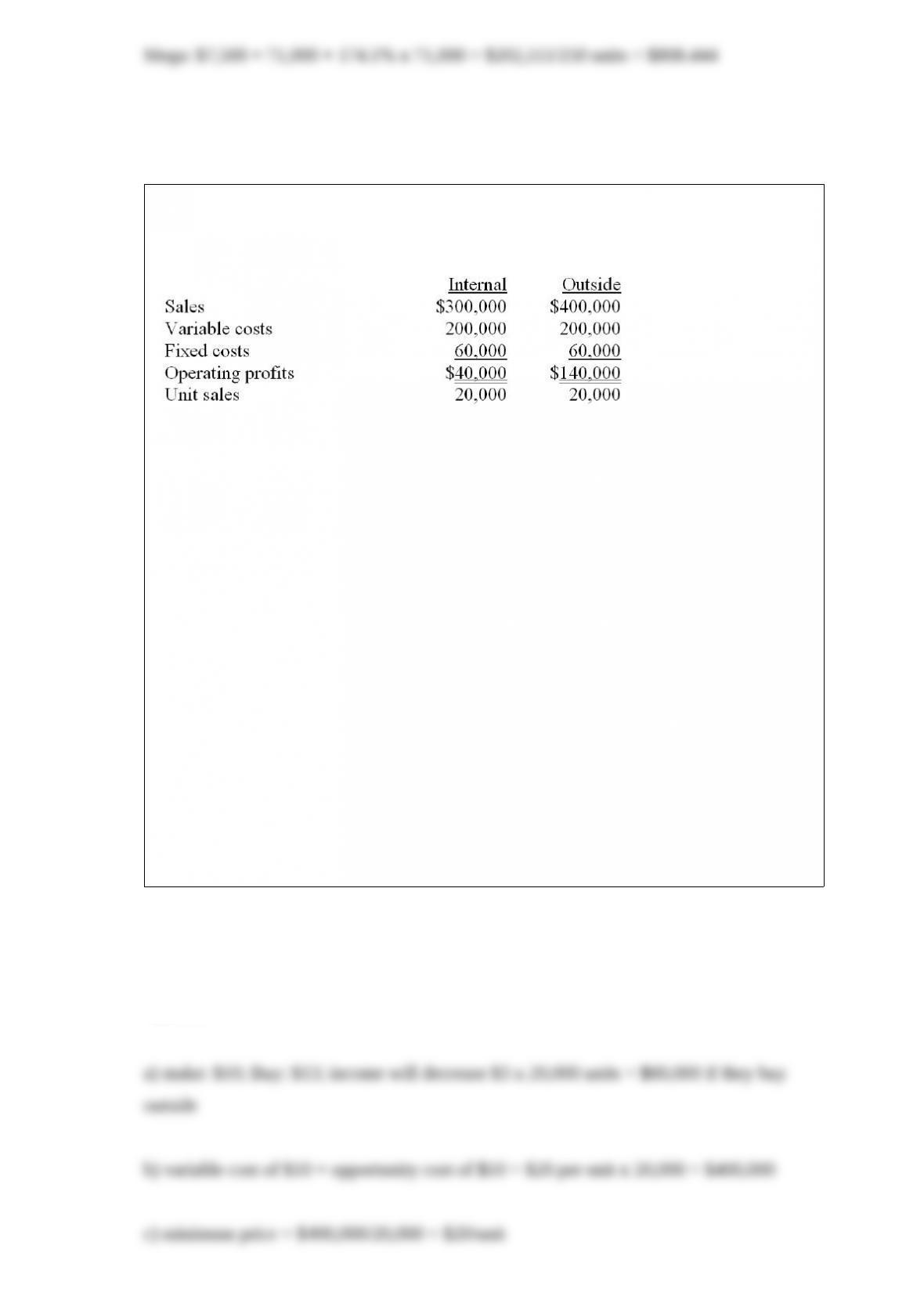

The Sutton Division of Haugen Company produces wheels for off-road sport vehicles.

One-half of Sutton’s output is sold to the Wilson Division of Haugen; the remainder is

sold to outside customers. Sutton’s estimated operating profit for the year is:

Wilson Division has an opportunity to purchase 20,000 wheels of the same quality from

an outside supplier on a continuing basis.

Required:

a) The Sutton Division cannot sell any additional products to outside customers. Should

the Haugen Company allow Wilson Division to purchase the wheels from the outside

supplier at $13.00 per unit?

b) If the Sutton Division is now operating at full capacity and can sell all its units to

outside customers at the present selling price, what is the differential cost to Haugen of

requiring that the wheels be made internally and sold to Wilson Division?

c) If the Sutton Division is now operating at full capacity and can sell all its units to

outside customers at the present selling price, what is the minimum selling price that

Sutton should accept from Wilson Division?

d) The Sutton Division cannot sell any additional products to outside customers. What

is the minimum selling price that Sutton should accept from the Wilson Division?

Answer:

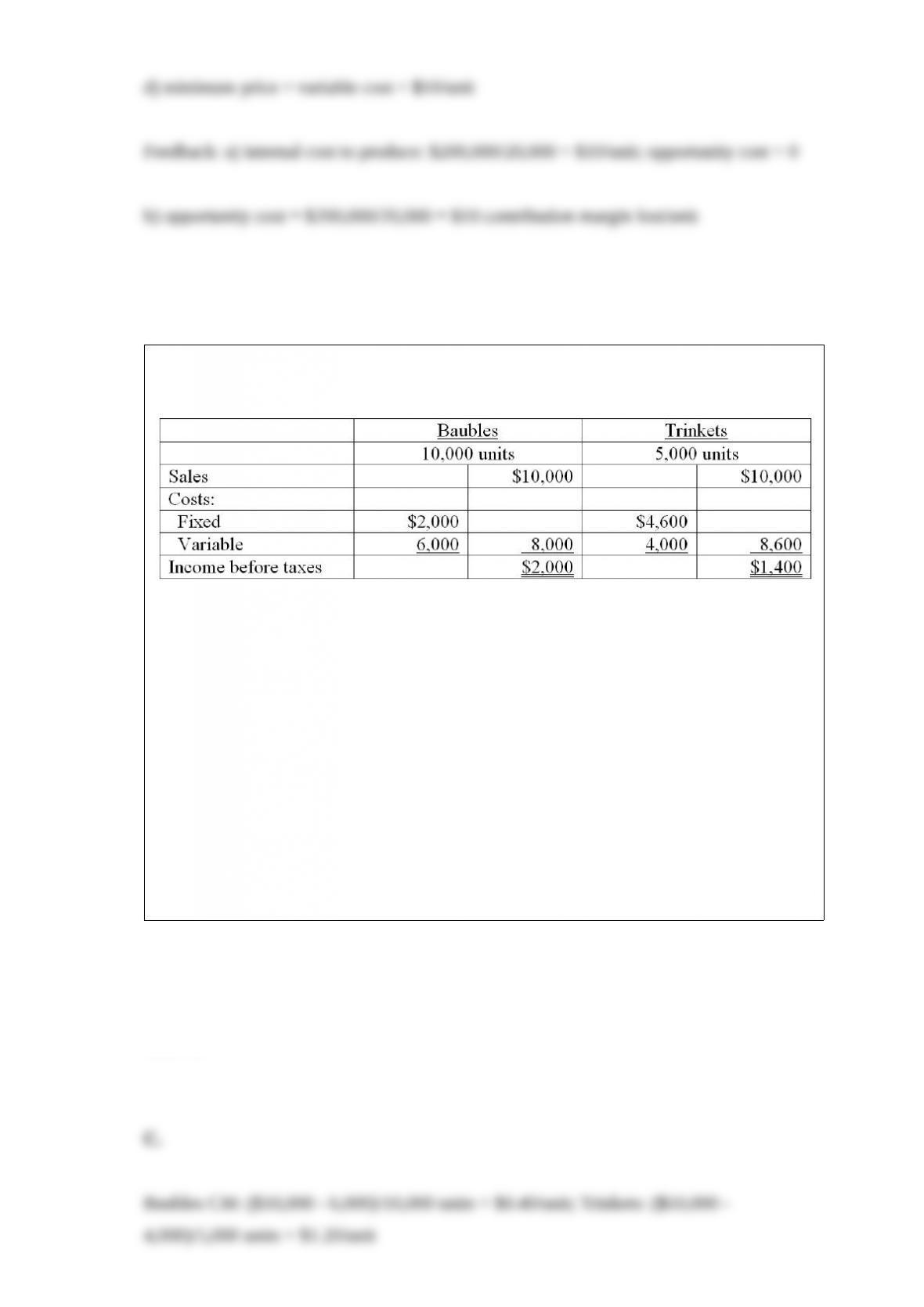

The Dooley Co. manufactures two products, Baubles and Trinkets. The following are

projections for the coming year:

How many Baubles will be sold at the break-even point, assuming that the facilities are

jointly used and the sales mix will remain constant?

A. 9,900

B. 8,800

C. 6,600

D. 5,000

E. 3,300

Answer:

The beginning Finished Goods Inventory plus the cost of goods manufactured equals

A. ending finished goods inventory.

B. cost of goods sold for the period.

C. total work-in-process during the period.

D. total cost of goods manufactured for the period.

E. cost of goods available for sale for the period.

Answer:

Which of the following statements concerning a process cost accounting system is

false?

A. The units in beginning inventory plus the units transferred out during the month

should equal the units in the ending inventory plus the units transferred in during the

month.

B. If material is used evenly throughout a process, the number of equivalent material

units will equal the number of equivalent units for the conversion (processing) costs.

C. Actual costing may be used in a process costing system to assign indirect overhead

costs to departments.

D. The units in beginning inventory plus the units transferred in during the month

should equal the units in the ending inventory plus the units transferred out during the

month.

Answer:

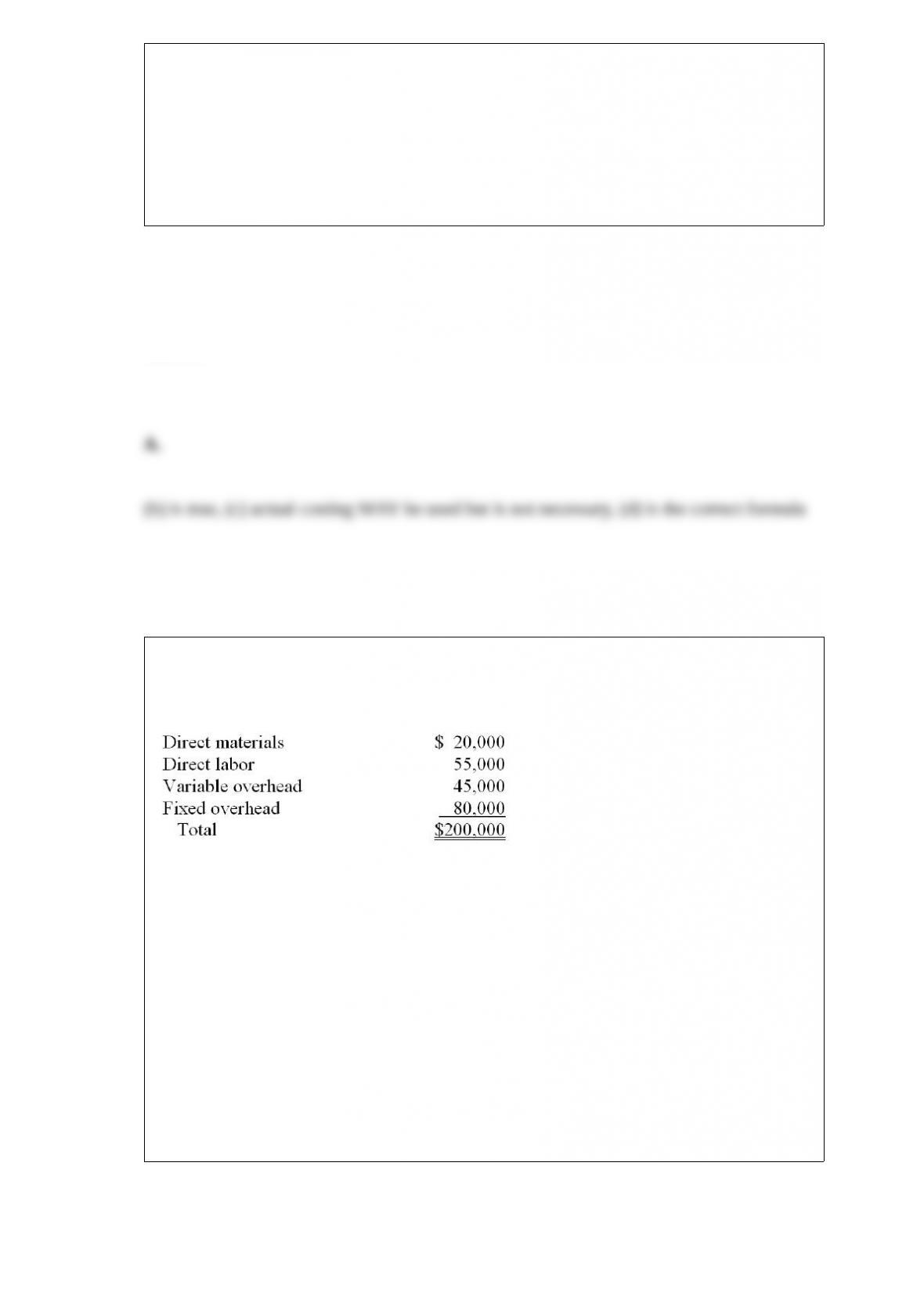

The Bremmer Company produces 5,000 units of item ZQ98 annually at a total cost of

$200,000.

The Daisy Company has offered to supply all 5,000 units of ZQ98 per year for $35 per

unit. If Bremmer accepts the offer, $8 per unit of the fixed overhead would be saved. In

addition, some of Bremmer’s leased facilities could be vacated, reducing lease payments

by $30,000 per year. What are the relevant costs for the “make” alternative?

A. $120,000

B. $175,000

C. $190,000

D. $200,000

Answer:

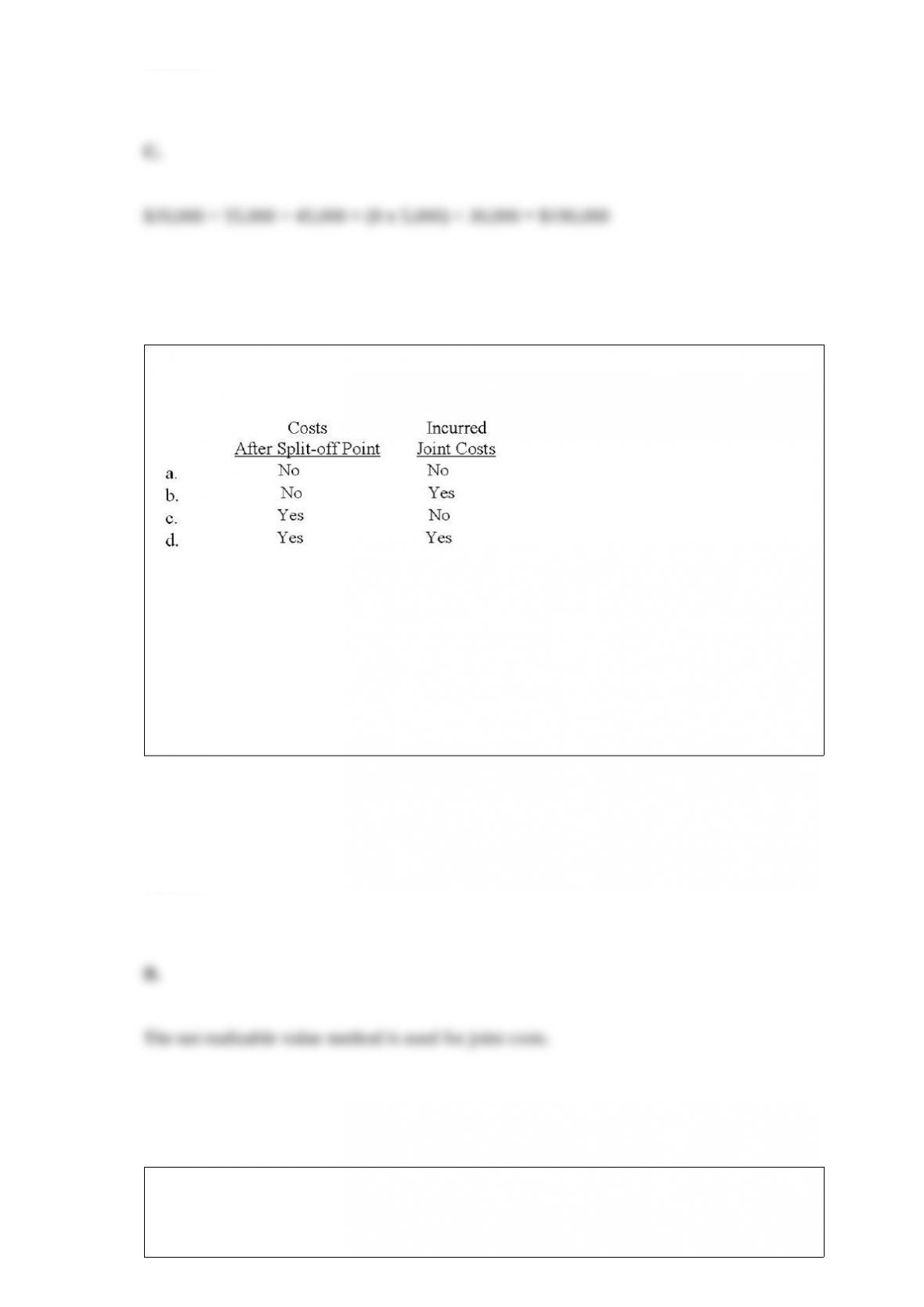

Net realizable value at the split-off point is used to allocate

A. a

B. b

C. c

D. d

Answer:

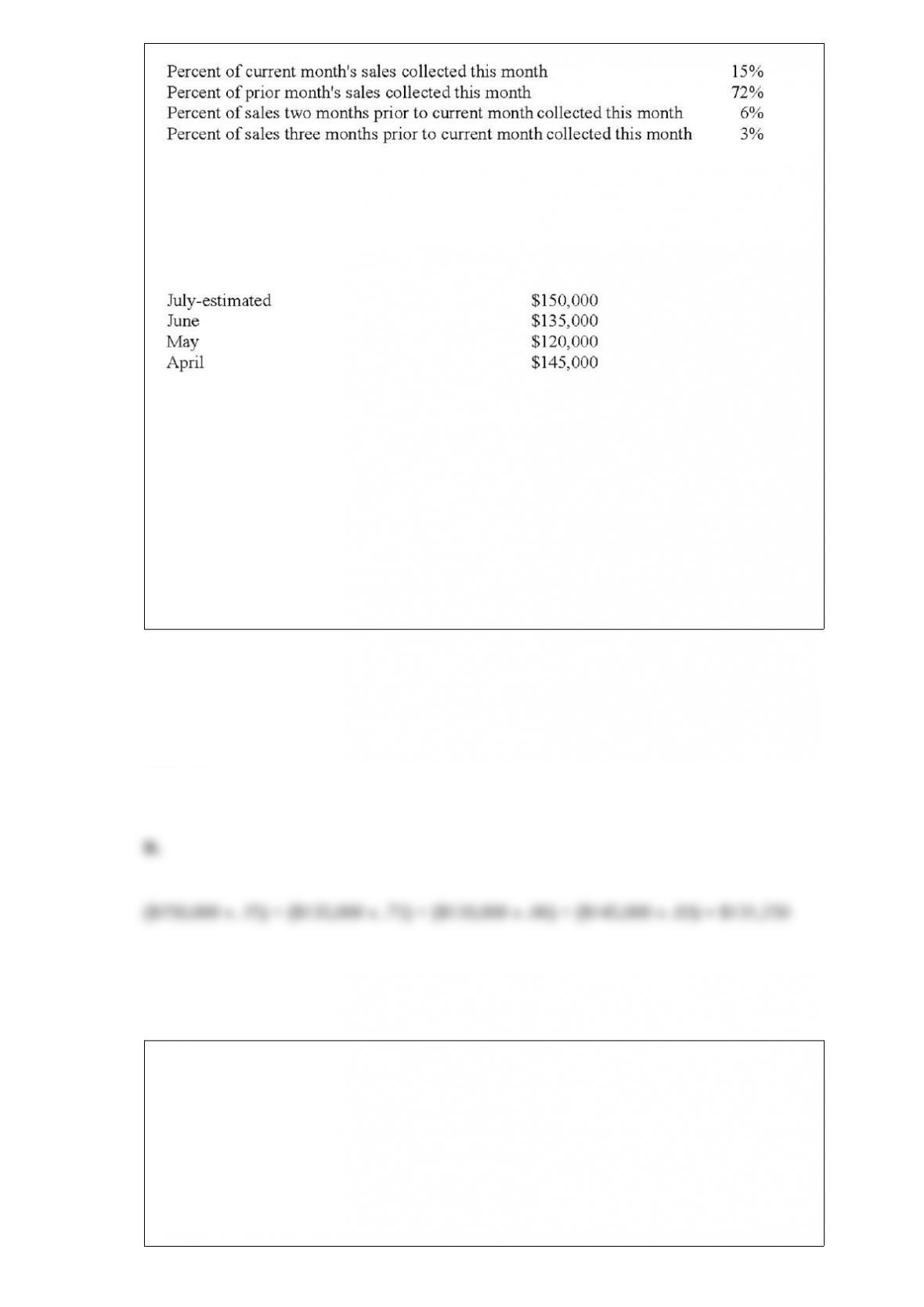

The Sport Company is preparing a cash budget for the month of July. The following

information on accounts receivable collections is available from Sport’s past collection

experience:

The remaining 4% are not collected and are written off as bad debts.

Credit sales to date are as follows:

What are the estimated collections in July?

A. $125,250.

B. $131,250.

C. $133,250.

D. $137,250.

Answer:

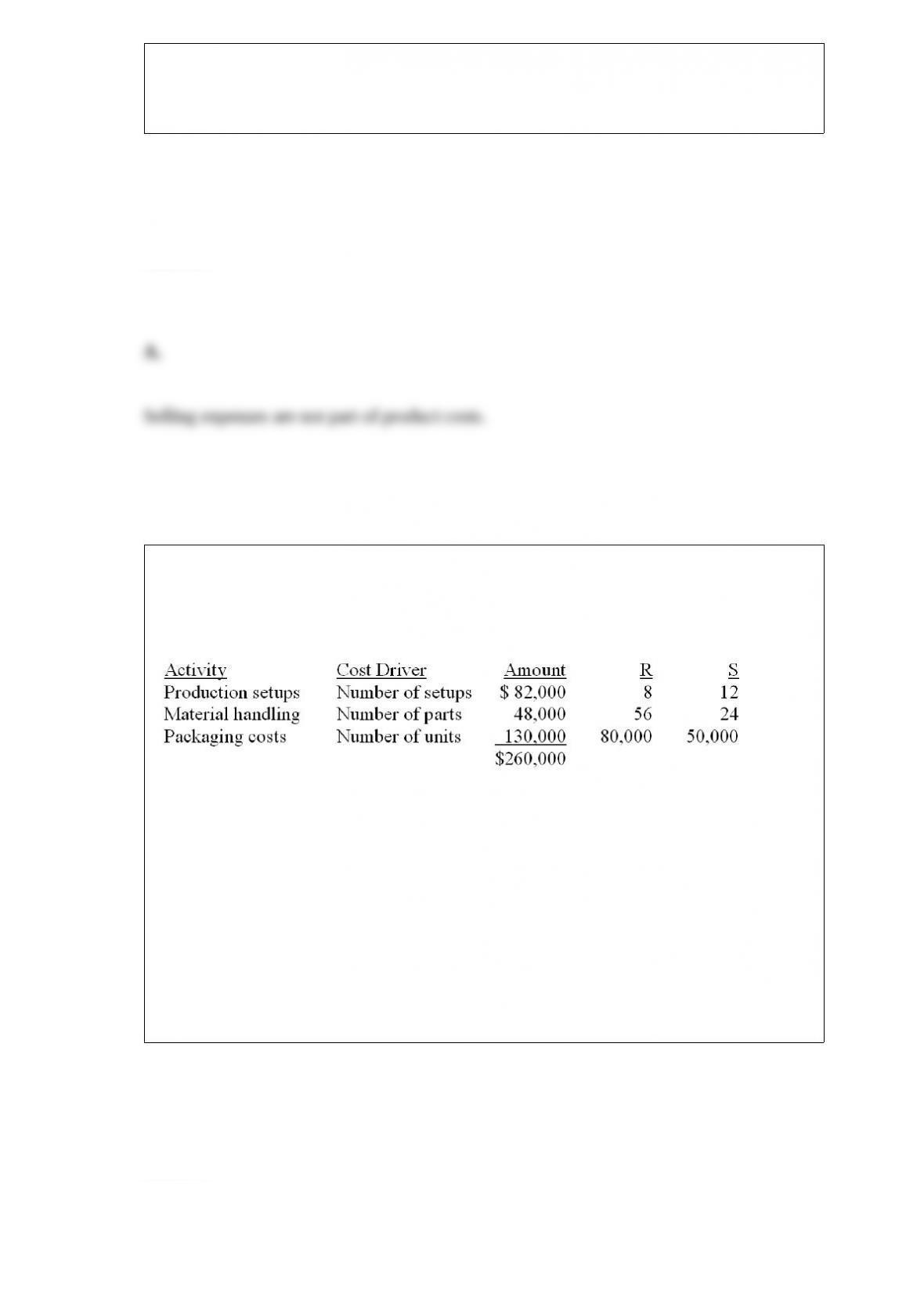

The Cost Flow Diagram for product costing includes all of the following costs except:

A. Selling expenses

B. Direct materials

C. Direct labor

D. Fixed manufacturing overhead

E. Variable manufacturing overhead

Answer:

RS Company manufactures and distributes two products, R and S. Overhead costs are

currently allocated using the number of units produced as the allocation base. The

controller has recommended changing to an activity-based costing (ABC) system. She

has collected the following information:

What is the total overhead per unit allocated to Product S using activity-based costing

(ABC)?

A. $2.60

B. $2.27

C. $2.00

D. $1.83

Answer:

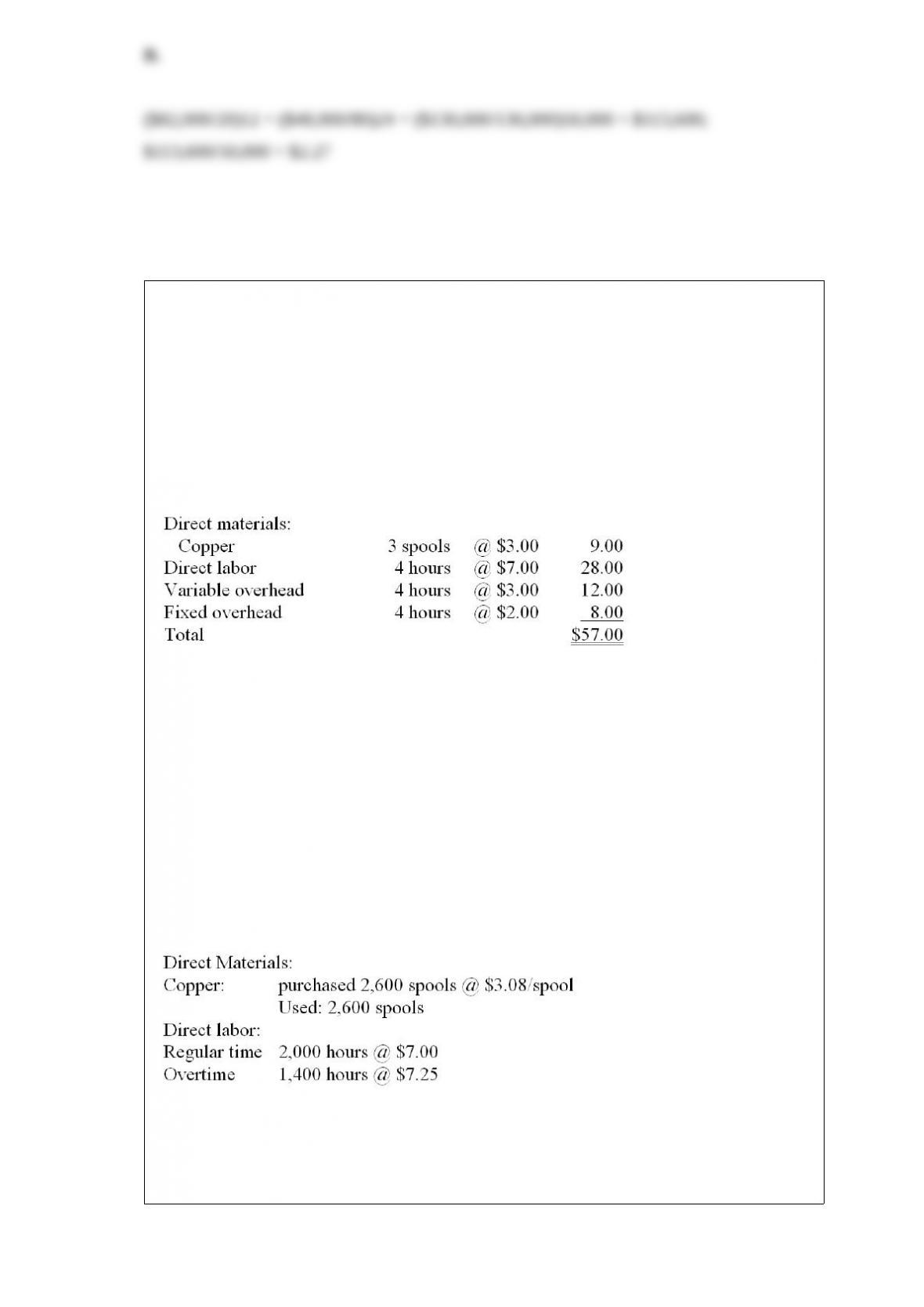

Western Company manufactures special electrical equipment and parts. Western

employs a standard cost accounting system with separate standards established for each

product.

A special transformer is manufactured in the Transformer Department. Production

volume is measured by direct labor hours in this department and a flexible budget

system is used to plan and control department overhead. Standard costs for the special

transformer are determined annually in September for the coming year. The standard

cost of a transformer was computed at $57.00 as shown below.

Overhead rates were based upon normal and expected monthly capacity, both of which

were 4,000 direct labor hours. Practical capacity for this department is 5,000 direct

labor hours per month. Variable overhead costs are expected to vary with the number of

direct labor hours actually used.

During October, 900 transformers were produced. This was below expectations because

a work stoppage occurred during contract negotiations with the labor force. Once the

contract was settled, the wage rate was increased to $7.25/hour and overtime was

scheduled in an attempt to catch up to expected production levels.

The following costs were incurred in October:

600 of the 1,400 hours were subject to overtime premium. The total overtime premium

is included in variable overhead in accordance with company accounting practices

Required: Compute each of the following variances, showing all your work. Be sure to

indicate whether the variances are favorable or unfavorable.

a) Direct materials price variance

b) Direct material efficiency (quantity) variance

c) Direct labor rate variance

d) Direct labor efficiency variance

e) Variable overhead spending variance

f) Variable overhead efficiency variance

g) Fixed overhead spending (budget) variance

h) Production volume variance

Answer:

The WISCO Company uses a weighted-average process costing system. The following

data are available:

Equivalent units of production for material are

A. 16,000.

B. 17,000.

C. 19,000.

D. 20,000.

Answer:

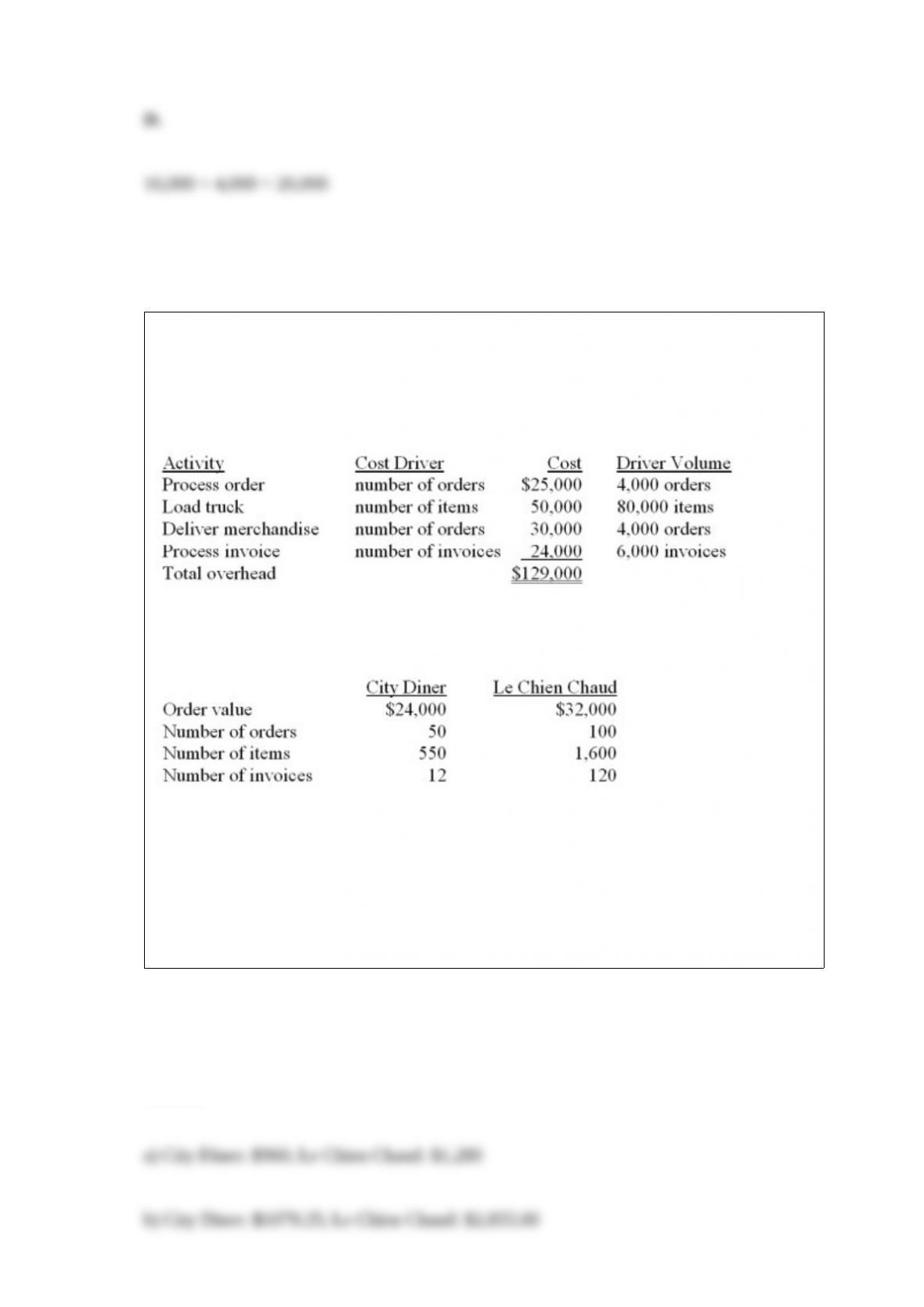

Marvin’s Kitchen Supply delivers restaurant supplies throughout the city. Marvin’s adds

4% to the order cost to cover the delivery cost. The delivery fee is meant to just cover

the cost of delivery. A consultant has analyzed the delivery service using activity-based

costing methods and identified four activities. Data on these activities are:

Two of Marvin’s customers are City Diner and Le Chien Chaud. Below are data on

orders and deliveries to these two customers:

Required:

(a) What would be the delivery charge for each customer under the current policy of 4%

of order value?

(b) What would the activity-based costing system estimate as the cost of delivering to

each customer?

Answer:

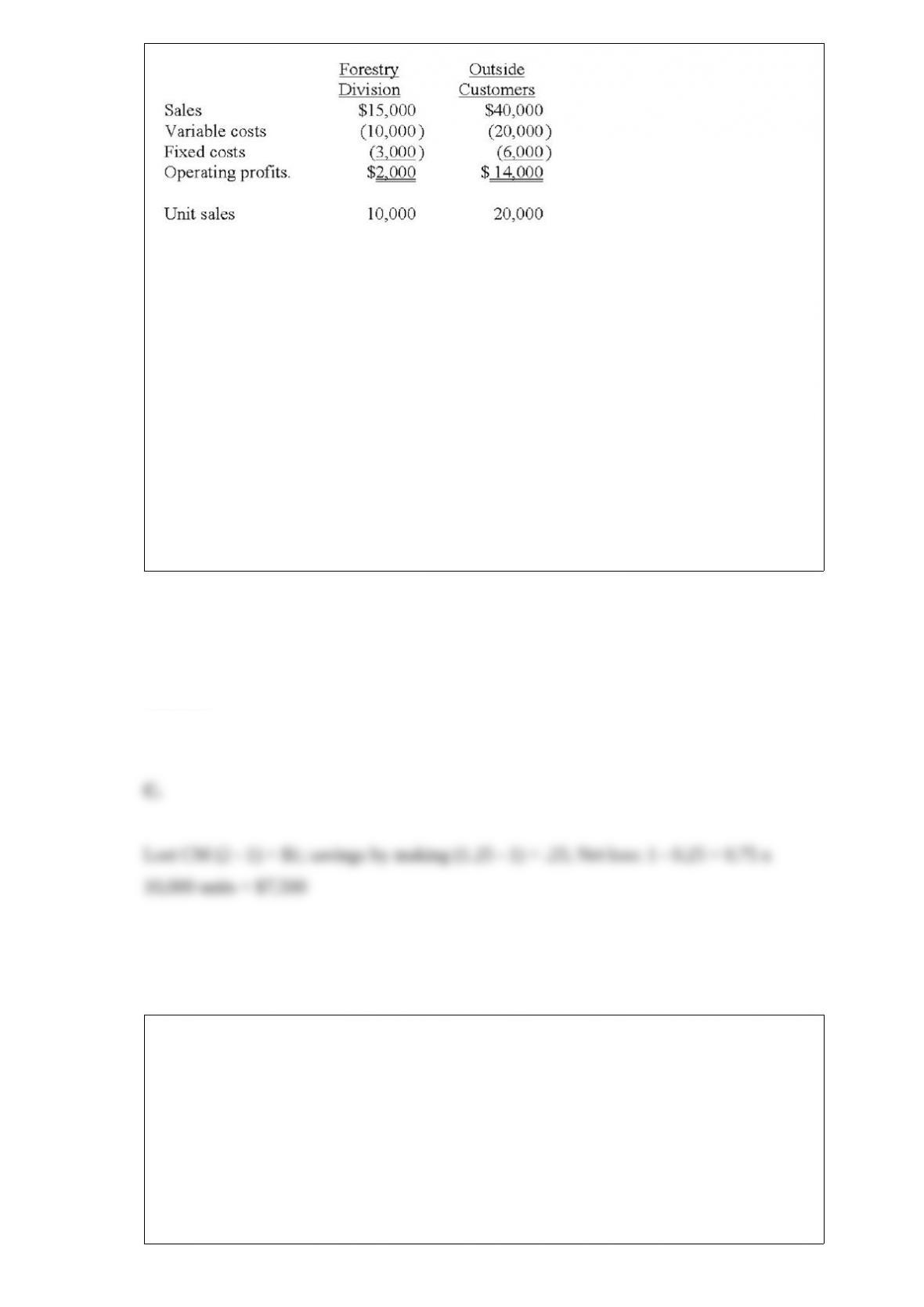

The Blade Division of Axe Company produces hardened steel blades. One-third of

Blade’s 30,000 unit output is sold to the Forestry Products Division of Axe; the

remainder is sold to outside customers. Blades’ estimated operating profit for the year

is:

The Forestry Division has an opportunity to purchase 10,000 blades of the same quality

from an outside supplier on a continuing basis. The purchase price would be $1.25. If

the Blade Division is now operating at full capacity and can sell all its units to outside

customers at the present selling price, what is the differential cost to Axe of requiring

that the blades be made internally and sold to the Forestry Division?

A. $2,500

B. $5,000

C. $7,500

D. $10,000

Answer:

Which of the following is the least practical reason for allocating service department

costs to user departments?

A. To ascertain profitability of user departments.

B. To evaluate performance of managers and divisions.

C. To make user departments aware that services are costly.

D. To provide the best possible service to users.

Answer:

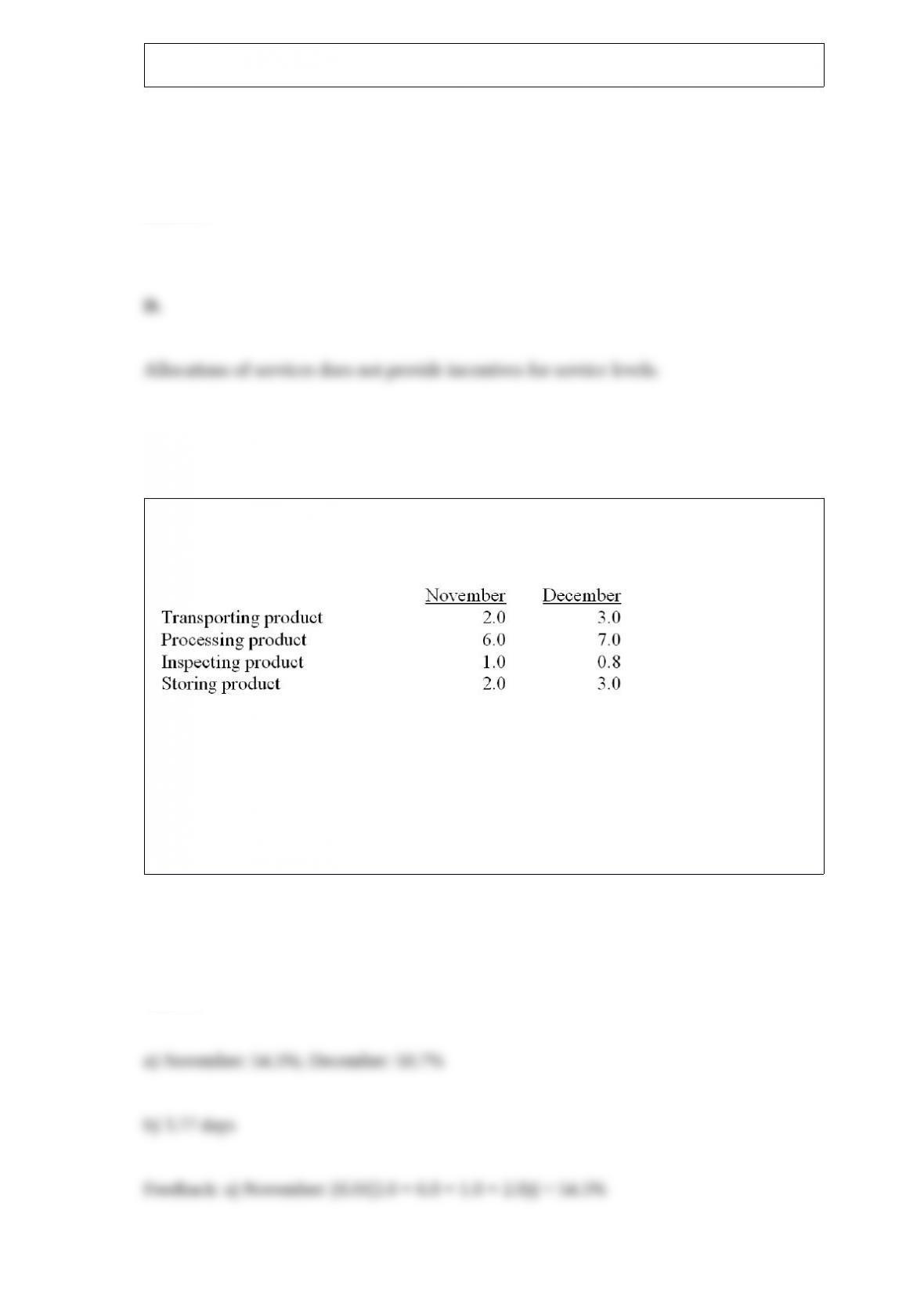

The Acme Company collected the following information (in days) for November and

December.

Required:

a) Calculate the manufacturing cycle efficiency for November and December.

b) Assume January’s processing time will be the same as December’s. If Acme’s target

for manufacturing cycle efficiency is 65%, what will January’s target for non-processing

times be?

Answer:

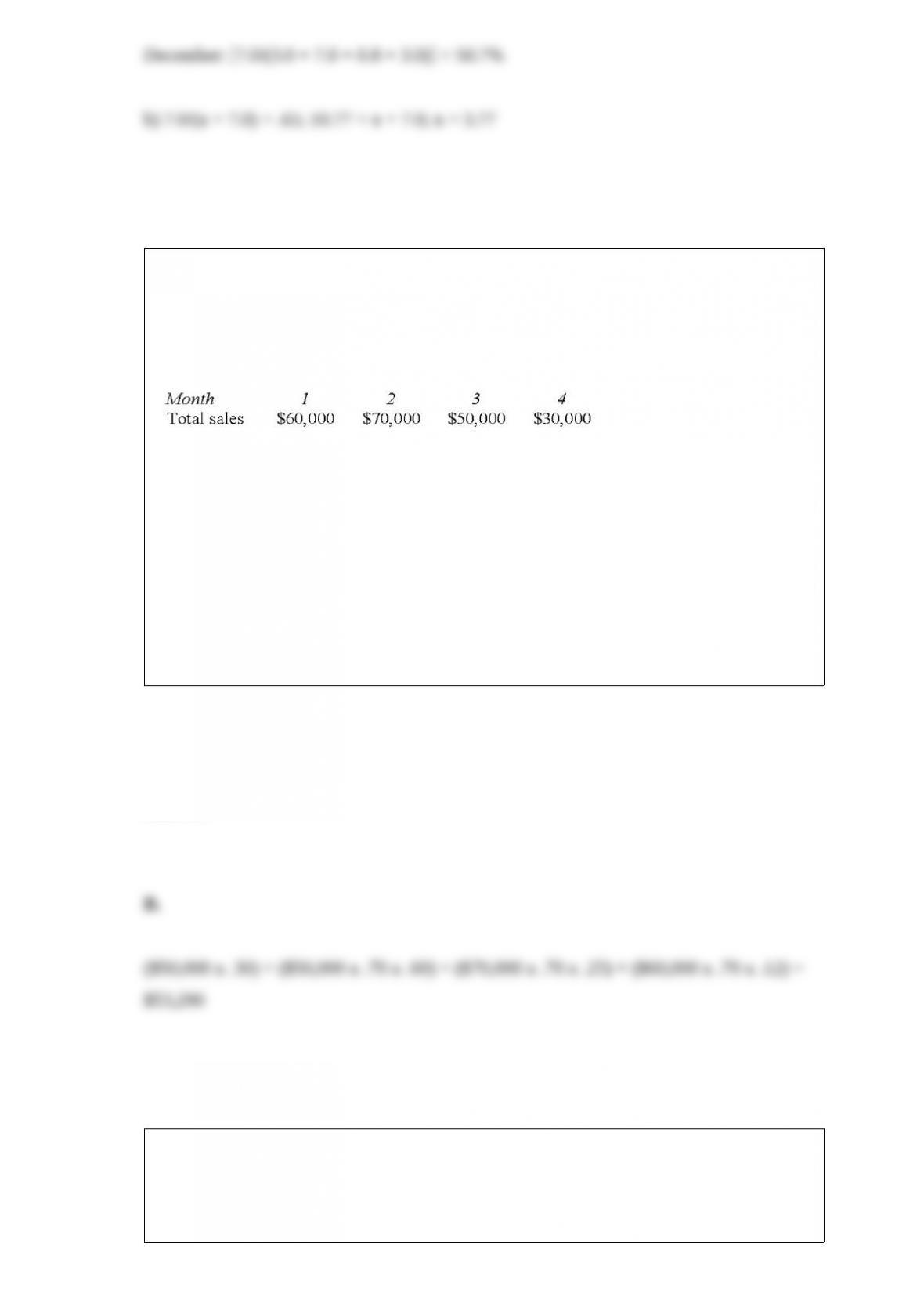

Pardee Company makes 30% of its sales for cash and 70% on account. 60% of the

account sales are collected in the month of sale, 25% in the month following sale, and

12% in the second month following sale. The remainder is uncollectible. The following

information has been gathered for Pardee’s first year of operations:

Total cash receipts in Month 3 will be

A. $52,200.

B. $53,290.

C. $50,000.

D. $51,510.

Answer:

Cost-based transfer prices that include a normal markup to the costs act as a surrogate

for

A. negotiated market prices.

B. opportunity costs.

C. differential costs.

D. market prices.

Answer:

A company purchased assets costing $200,000 which will be depreciated over 5-years

using straight-line depreciation and no salvage value. The company also purchased land

and other assets, which are not depreciable at a cost of $200,000. It is estimated that in

5-years, the value of these assets will be unchanged. Assume that annual cash profits

are $80,000 and, for return on investment (ROI) calculations, the company uses

end-of-year asset values.

If sales each year average $840,000, what will be the asset turnover using gross book

value?

A. 3.0

B. 2.6

C. 2.1

D. 1.9

Answer: