Estimated losses on long-term contracts are recognized as ratable over the contract term

regardless of whether revenue is recognized over time or upon contract completion.

A temporary difference originates in one period and reverses, or turns around, in one or

more later periods.

Securitization of receivables is a type of secured borrowing.

Dollar-value LIFO eliminates the risk of LIFO liquidations.

When accounting for a capital lease, the lessee records the leased asset at the present

value of the minimum lease payments or the asset’s fair value, whichever is lower.

Examples of external transactions include all of the following except:

a. Paying employee salaries.

b. Purchasing equipment.

c. Depreciating equipment.

d. Collecting a receivable.

Linguini Inc. adopted dollar-value LIFO (DVL) as of January 1, 2016, when it had an

inventory of $800,000. Its inventory as of December 31, 2016, was $811,200 at

year-end costs and the cost index was 1.04. What was DVL inventory on December 31,

2016?

a. $780,000.

b. $800,000.

c. $811,200.

d. $832,000.

Volt Electronics sells equipment that includes a three-year warranty. Repairs under the

warranty are performed by an independent service company under contract with Volt.

Based on prior experience, warranty costs are estimated to be $25 per item sold. Volt

should recognize these warranty costs:

a. When the equipment is sold.

b. When the repairs are performed.

c. When payments are made to the service firm.

d. Evenly over the life of the warranty.

Making insurance payments in advance is an example of:

a. An accrued receivable transaction.

b. An accrued liability transaction.

c. A deferred revenue transaction.

d. A prepaid expense transaction.

During 2016, M Co. had the following two classes of stock issued and outstanding for

the entire year:

– 400,000 shares of common stock, $1 par.

-2,000 shares of 4% preferred stock, $100 par, convertible share-for-share into common

stock.

M’s 2016 net income was $1,800,000, and its income tax rate for the year was 30%. In

the computation of diluted earnings per share for 2016, the amount to be used in the

numerator is:

a. $1,792,000.

b. $1,796,000.

c. $1,800,000.

d. $1,802,400.

Depreciation, depletion, and amortization:

a. All refer to the process of allocating the cost of long-term assets used in the business

over future periods.

b. All generally use the same methods of cost allocation.

c. Are all handled the same in arriving at taxable income.

d. All of these answer choices are correct.

A statement of cash flows and its related disclosure note typically do not report:

a. An acquisition of the use of a building with a lease agreement.

b. The purchase of treasury stock.

c. Stock dividends.

d. Notes payable issued for a tract of land.

Which of the following results in increasing basic earnings per share?

a. Paying more than book (carrying) value to retire outstanding bonds.

b. Issuing cumulative preferred stock.

c. Purchasing treasury stock.

d. All of these answer choices increase basic earnings per share.

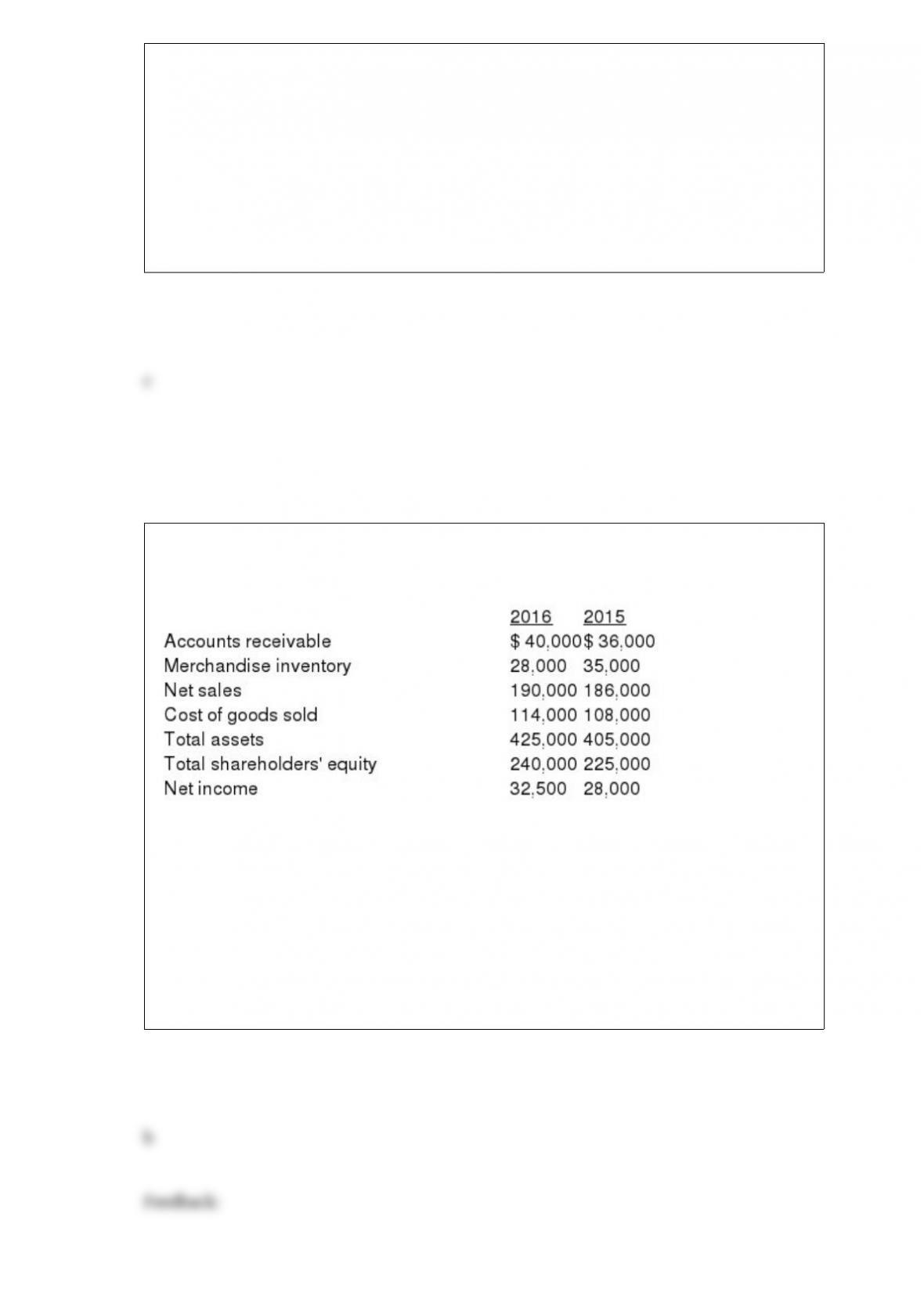

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Hulkster’s 2016 return on assets is (rounded):

a. 7.1%.

b. 7.8%.

c. 13.5%.

d. 44.7%.

A company’s total obligation for postretirement benefits is measured by the:

a. APBO.

b. HMOP.

c. HOBO.

d. EPBO.

In the year 2016, the internal auditors of Goofy Co. discovered that goods costing $25

million that were purchased in December of 2015 were recorded for $20 million. The

goods were properly measured in the December 31, 2015, ending physical inventory.

Required:

Prepare the journal entry needed in 2016 to correct the error. Also, briefly describe any

other measures Goofy would take in connection with correcting the error. (Ignore

income taxes.)

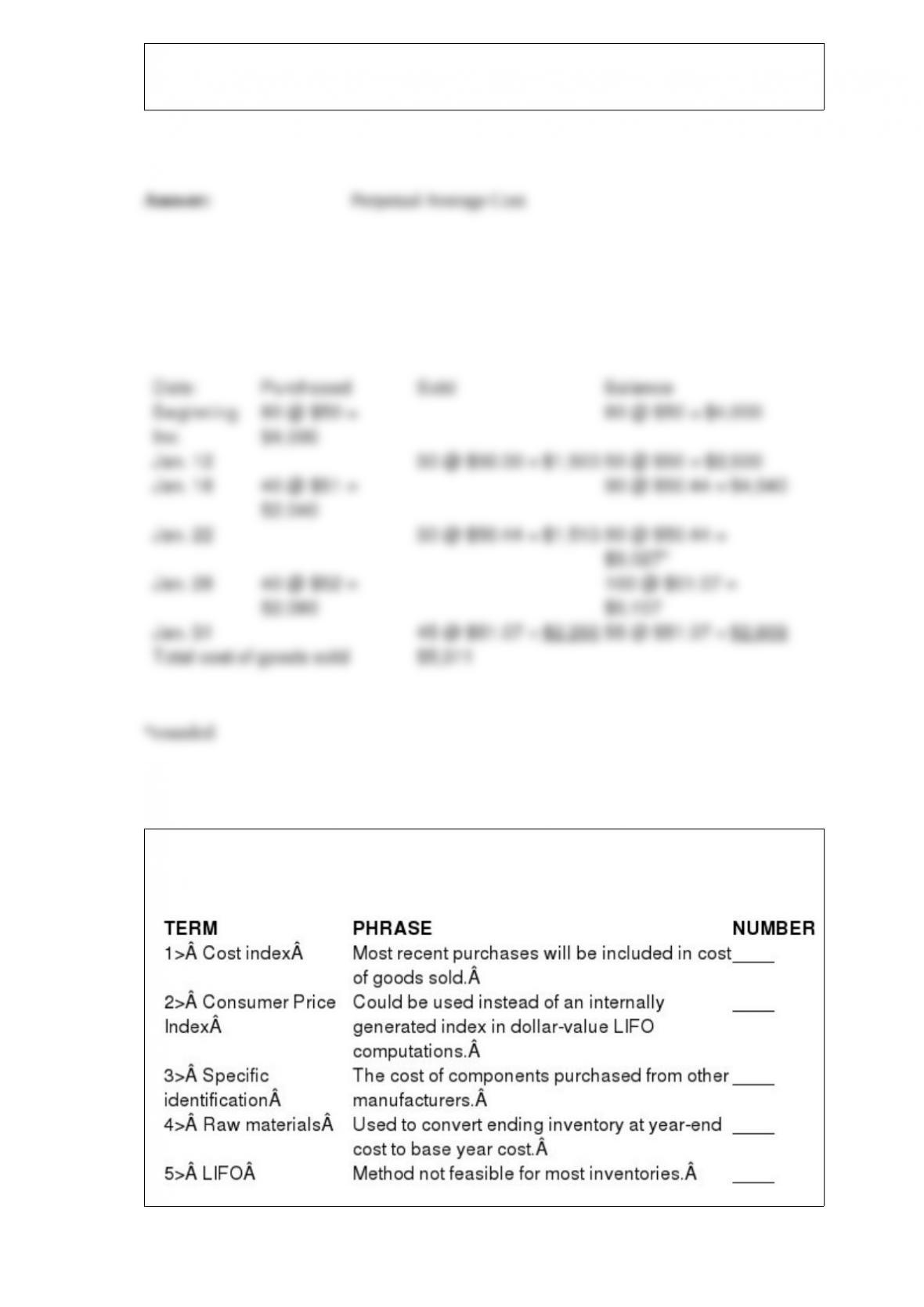

Shown below is the activity for one of the products of Random Creations: January 1

balance, 80 units @ $50 $4,000

Purchases:

January 18: 40 units @ $51

January 28: 40 units @ $52

Sales:

January 12: 30 units

January 22: 30 units

January 31: 45 units Required: Compute the January 31 ending inventory and cost of

goods sold for January, assuming Random Creations uses average cost and a perpetual

inventory system.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the correct term.

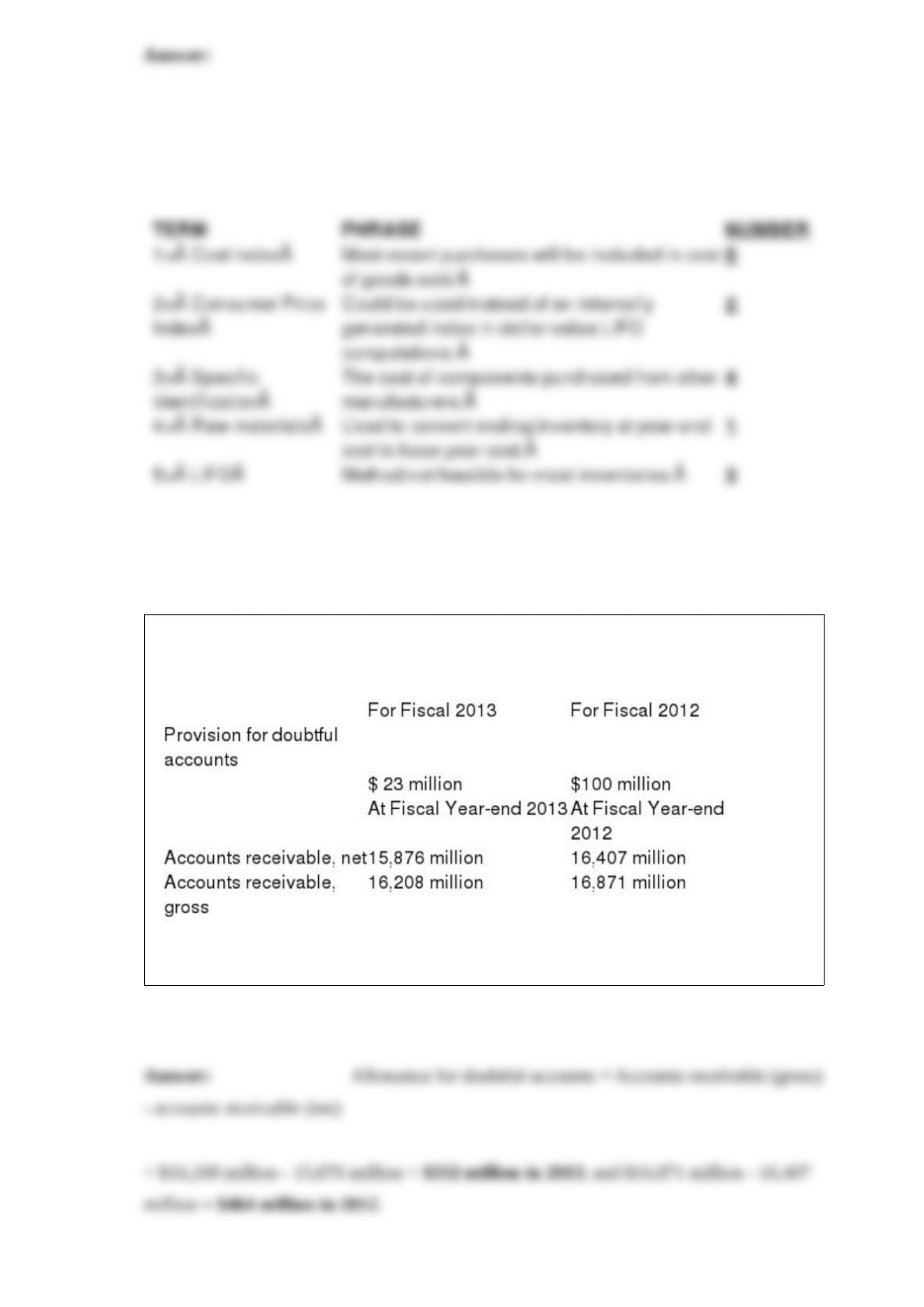

The following information is taken from the 2013 annual report to shareholders of

Hewlett-Packard (HP) Co.

What is the balance in HP’s allowance for doubtful accounts at the end of the fiscal

years 2013 and 2012, respectively?

On July 1, 2016, Silverwood Company purchased for cash 35% of the voting common

stock of Yellowstone Corporation. Both companies have a December 31 fiscal year-end.

Yellowstone Corporation, which is publicly traded on an organized stock exchange,

reported its net income for the year to Silverwood and paid a dividend to Silverwood

during the year.

Required:

How should Silverwood report the above information in its year-end income statement

and balance sheet? Discuss the rationale for your answer.