Under IFRS No. 9, equity investments are classified as either “fair value through other

comprehensive income (FVOCI)” or “fair value through profit and loss (FVPL).”

Accruals occur when the cash flow precedes either revenue or expense recognition.

The classification of deferred tax assets is sometimes dependent on when the benefit

will be realized.

In franchise arrangements, the franchisor’s performance obligations are not separately

identifiable, so revenue must be recognized over time.

Equity is a residual amount representing the owner’s interest in the assets of the

business.

Accounting for stock-based compensation is an area in which the FASB has received

little political interference.

Lower of cost and net realizable value can be applied to individual inventory items, to

logical categories of inventory, or to the entire inventory.

The depreciable base for an asset is:

a. Its service life.

b. The excess of its cost over residual value.

c. The difference between its replacement value and cost.

d. The amount allowable under MACRS

Bull’sEye sells gift cards redeemable for Bull’sEye products either in-store or online.

During 2016, Bull’sEye sold $2,000,000 of gift cards, and $1,800,000 of the gift cards

were redeemed for products. As of December 31, 2016, $150,000 of the remaining gift

cards had passed the date at which Bull’sEye concludes that the cards will never be

redeemed. How much gift card revenue should Bull’sEye recognize in 2016?

a. $2,000,000

b. $1,950,000

c. $1,850,000

d. $1,800,000

The balance sheet reports:

a. Net income at a point in time.

b. Cash flows for a period of time.

c. Assets and equities at a point in time.

d. Assets and liabilities for a period of time.

Corporations are formed in accordance with:

a. The Model Business Corporation Act.

b. Federal statutes.

c. The laws of individual states.

d. Federal trade commission regulations.

Adjusting entries are primarily needed for:

a. Cash basis accounting.

b. Accrual accounting.

c. Current value accounting.

d. Manual accounting systems.

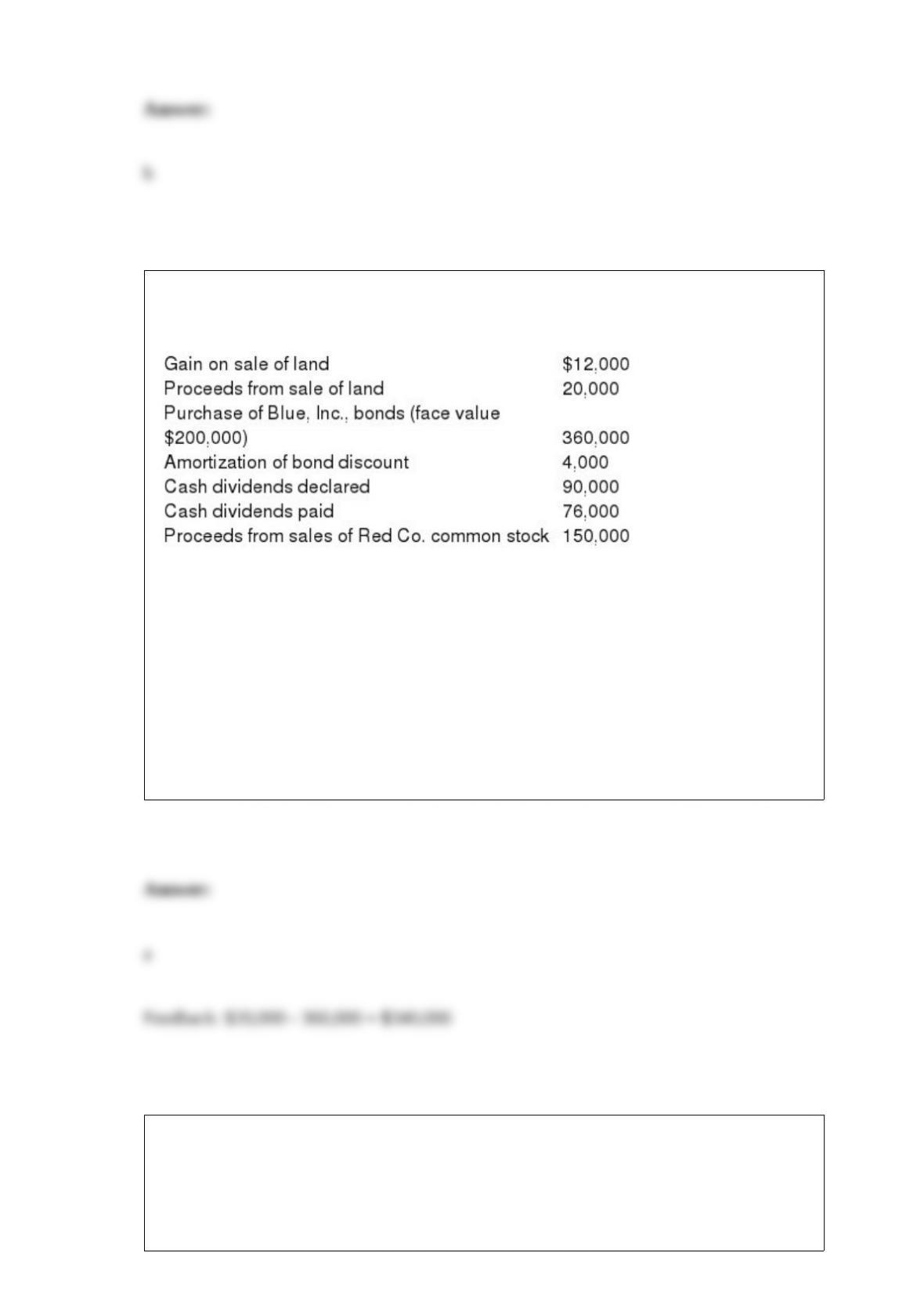

In preparing its cash flow statement for the year ended December 31, 2016, Red Co.

gathered the following data:

In its December 31, 2016, statement of cash flows, what amount should Red report as

net cash outflows from investing activities?

a. $340,000.

b. $352,000.

c. $376,000.

d. $388,000.

On January 2, 2015, Howdy Doody Corporation purchased 12% of Ranger

Corporation’s common stock for $50,000 and classified the investment as available for

sale. Ranger’s net income for the years ended December 31, 2015 and 2016, were

$10,000 and $50,000, respectively. During 2016, Ranger declared and paid a dividend

of $60,000. There were no dividends in 2015. On December 31, 2015, the fair value of

the Ranger stock owned by Howdy Doody had increased to $70,000. How much should

Howdy Doody show in the 2016 income statement as income from this investment?

a. $26,000.

b. $ 7,200.

c. $20,000.

d. $27,200.

The Ultimate Frisbee League (UFL) licenses its trademark to Tank-Skin Apparel. Under

the license arrangement, Tank-Skin pays the UFL a $1 million initial license fee plus a

bonus when annual sales of Tank-Skin merchandise reach a threshold. The license

agreement is for 4 years.

How much of the $1 million initial license fee should the UFL recognize as revenue in

the first year of the contract?

a. $0

b. $250,000

c. $1,000,000

d. Cannot tell from information given.

Which of the following is reported as an operating activity in the statement of cash

flows?

a. The payment of dividends.

b. The sale of office equipment.

c. The payment of interest on long-term notes.

d. The issuance of a stock dividend.

Dulce Corporation had 200,000 shares of common stock outstanding during the current

year. There were also fully vested options for 10,000 shares of common stock were

granted with an exercise price of $20. The market price of the common stock averaged

$25 for the year. Net income was $4 million. What is diluted EPS (rounded)?

a. $20.00.

b. $19.80.

c. $19.23.

d. $18.18.

Prior service cost is included among OCI items in the statement of comprehensive

income and thus subsequently becomes part of AOCI where it is amortized over the

average remaining service period using

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

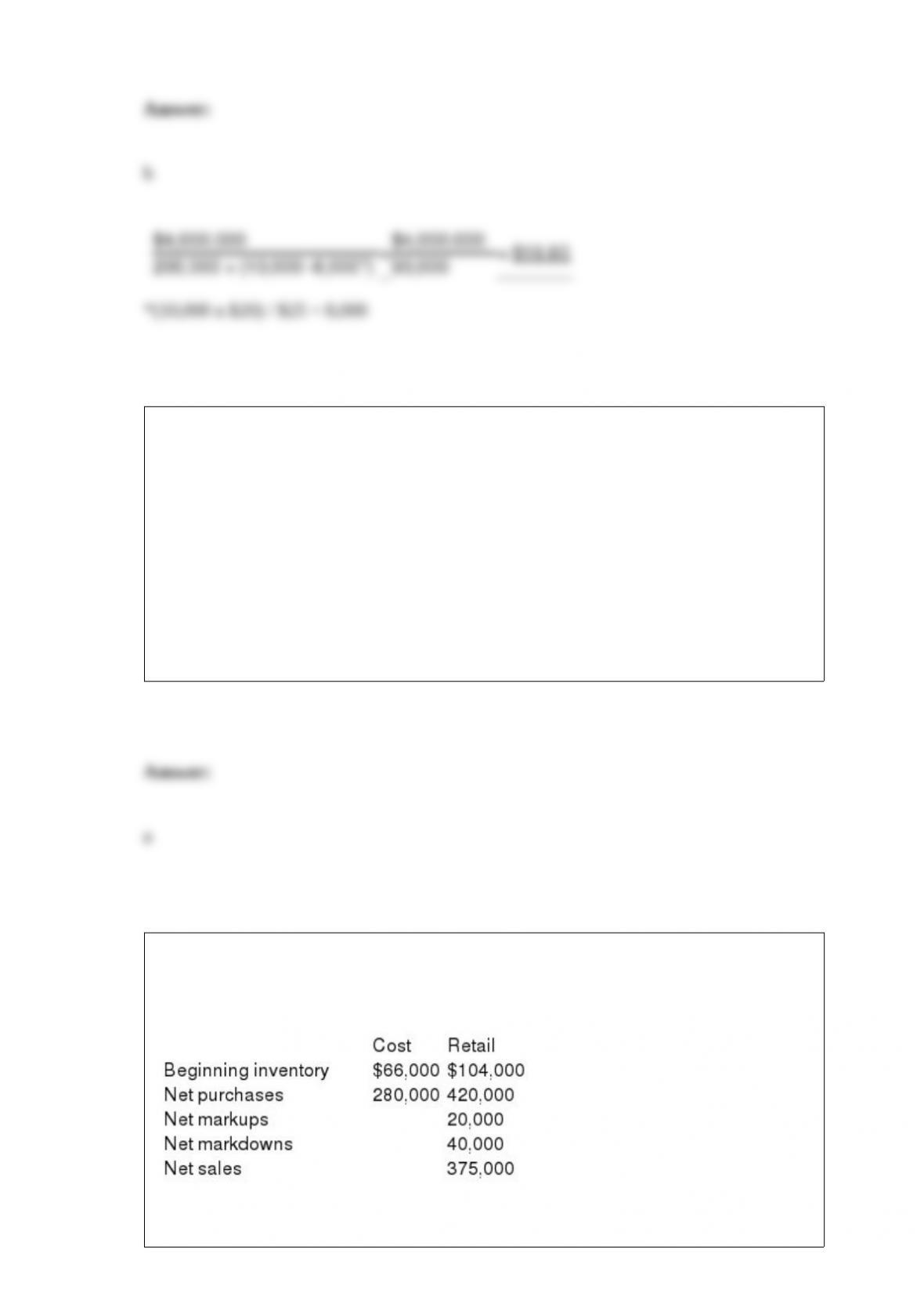

Data below for the year ended December 31, 2016, relates to Houdini Inc. Houdini

started business January 1, 2016, and uses the LIFO retail method to estimate ending

inventory.

Estimated ending inventory at retail is:

a. $ 65,000.

b. $169,600.

c. $ 25,000.

d. $129,000.

In computing diluted earnings per share, the treasury stock method is used for:

a. Stock warrants.

b. Stock splits.

c. Reverse stock splits.

d. Convertible preferred stock.

If the fair value of a held-to-maturity investment declines for a reason that is viewed as

“other than temporary” because the company has incurred a credit loss on the

investment:

a. The investment is written down to fair value, and only the noncredit-loss component

of the impairment loss is recognized in net income.

b. The investment is written down to fair value, and the entire impairment loss is

recognized in net income.

c. The investment is written down to fair value, and only the credit-loss component of

the impairment loss is recognized in net income.

d. The investment is written down to fair value, but none of the impairment loss is

recognized in net income.

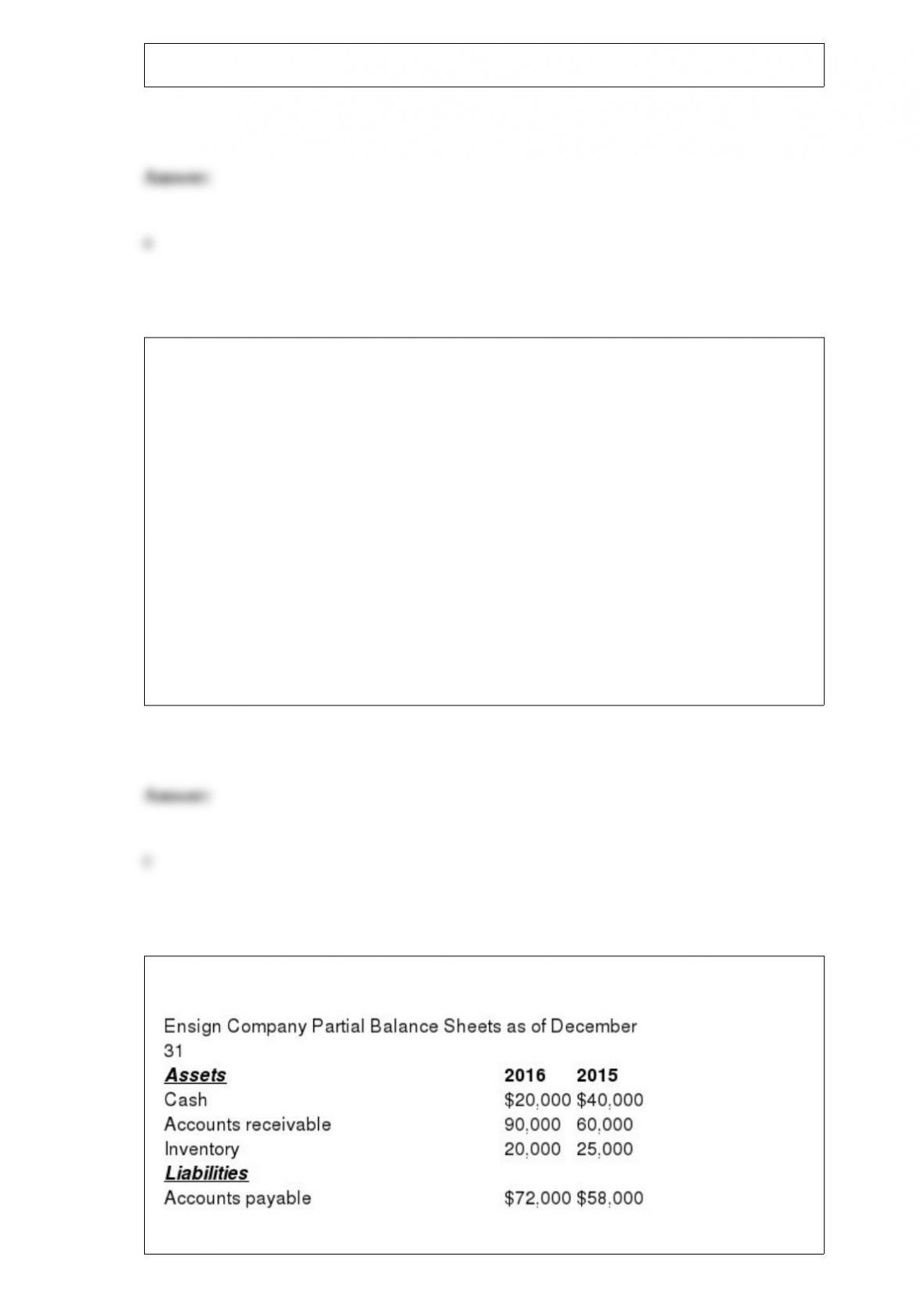

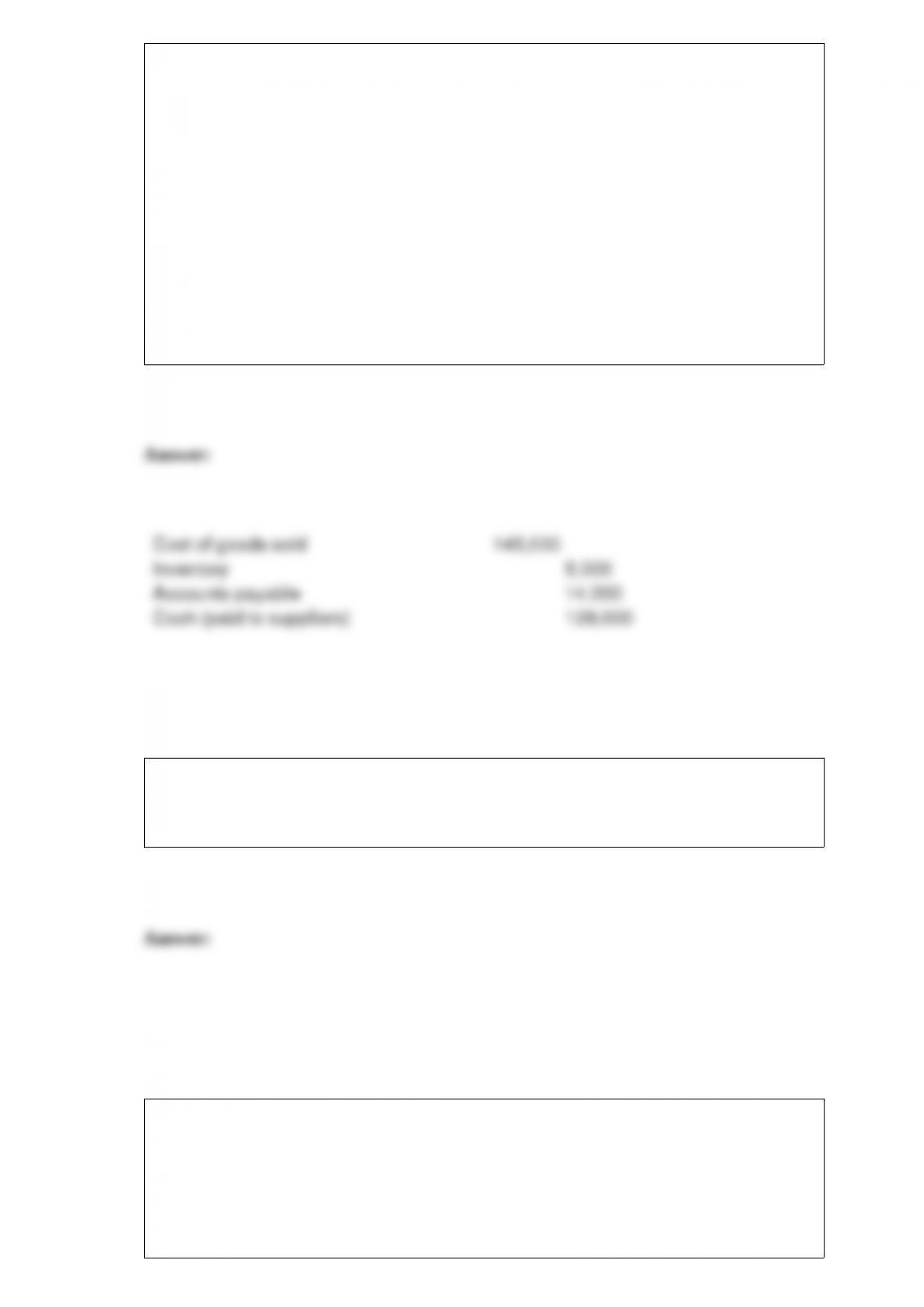

Partial balance sheets and additional information are listed below for Ensign Company.

Additional information for 2016:

Net income was $170,000.

Depreciation expense was $30,000.

Sales totaled $400,000.

Cost of goods sold totaled $145,000.

Required:

Prepare the summary entry for the amount of cash paid to merchandise suppliers during

2016.

Open Arms Industries has a noncontributory, defined benefit pension plan. During

2016, changing economic conditions caused the actuary to increase the assumed rate of

salary progression.

In February 2016, Omnibus Interior Corporation enters into a contract with Pike Realty

to remodel a 6-unit luxury condominium in New York City. Under the contract, the

company is entitled to receive a fixed fee of $1 million, and an additional performance

bonus of $500,000 if the property is sold during the same year. Required: Given a

strong demand for housing, Omnibus estimates that the property would most likely be

sold within the same year, and bases estimates of variable consideration on the most

likely estimate. On what transaction price should Omnibus base revenue recognition?

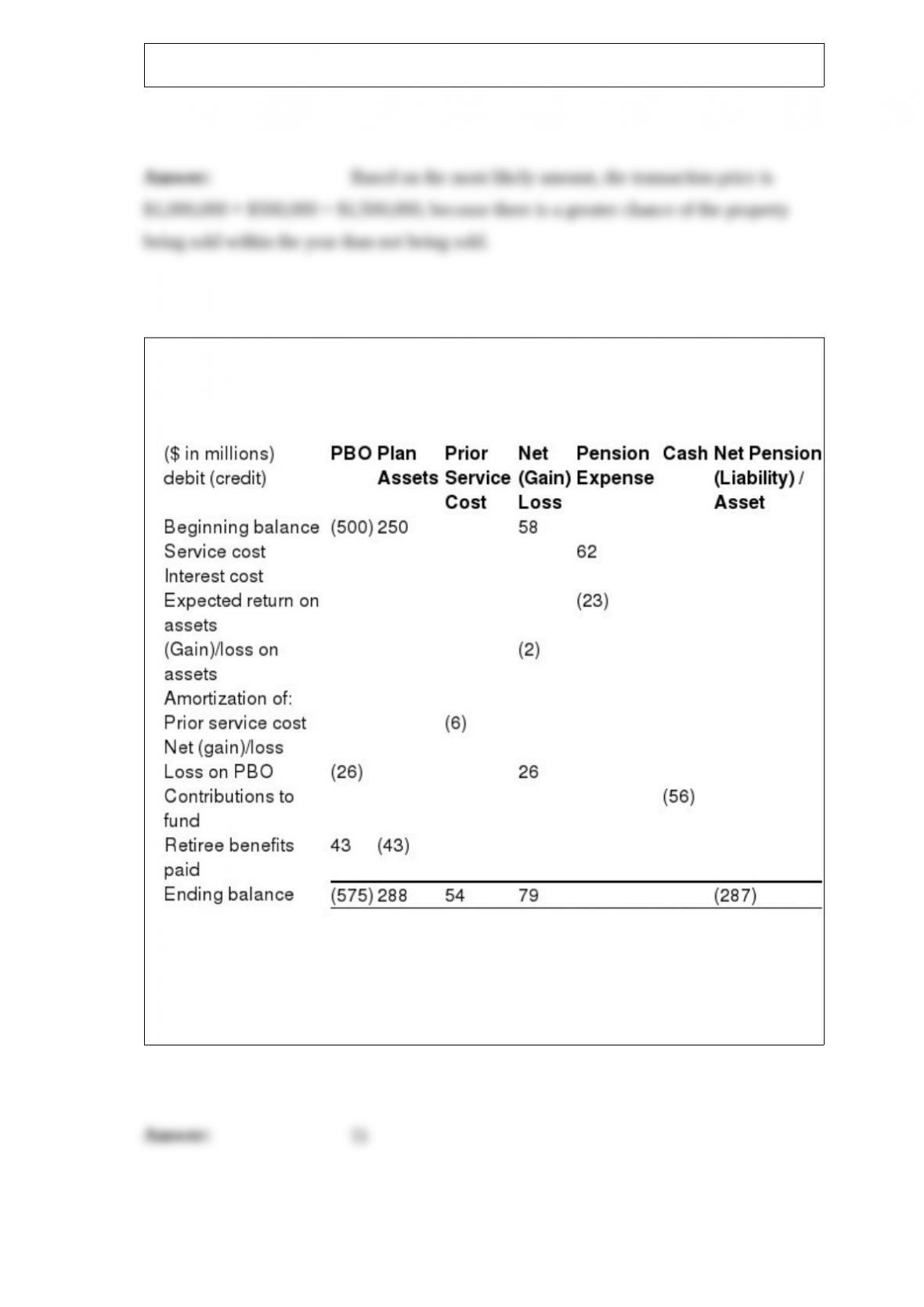

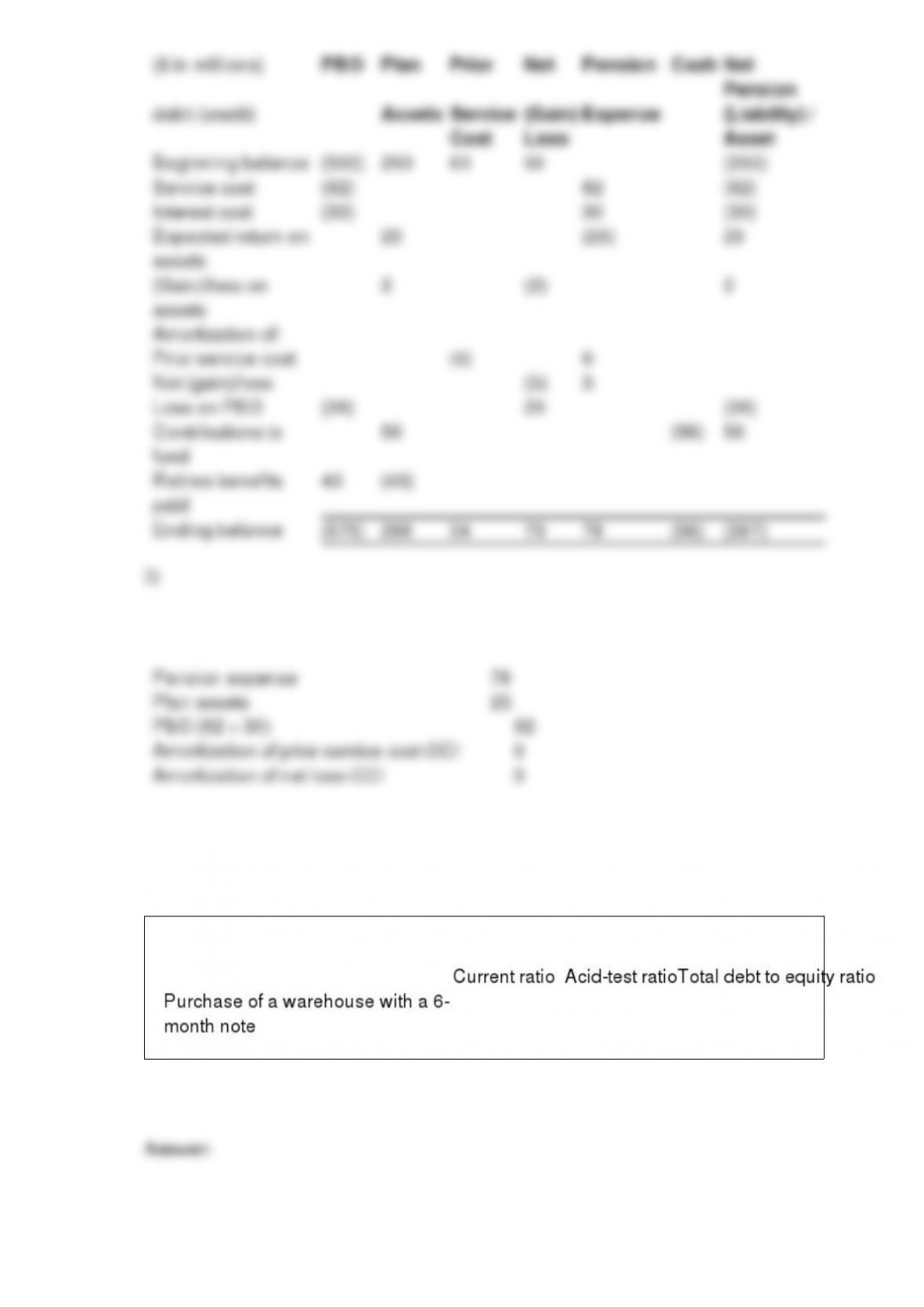

The following is an incomplete pension spreadsheet for the current year for Desperado

Corporation.

Required:

1) Complete the pension spreadsheet.

2) Prepare the journal entry to record pension expense for the year.

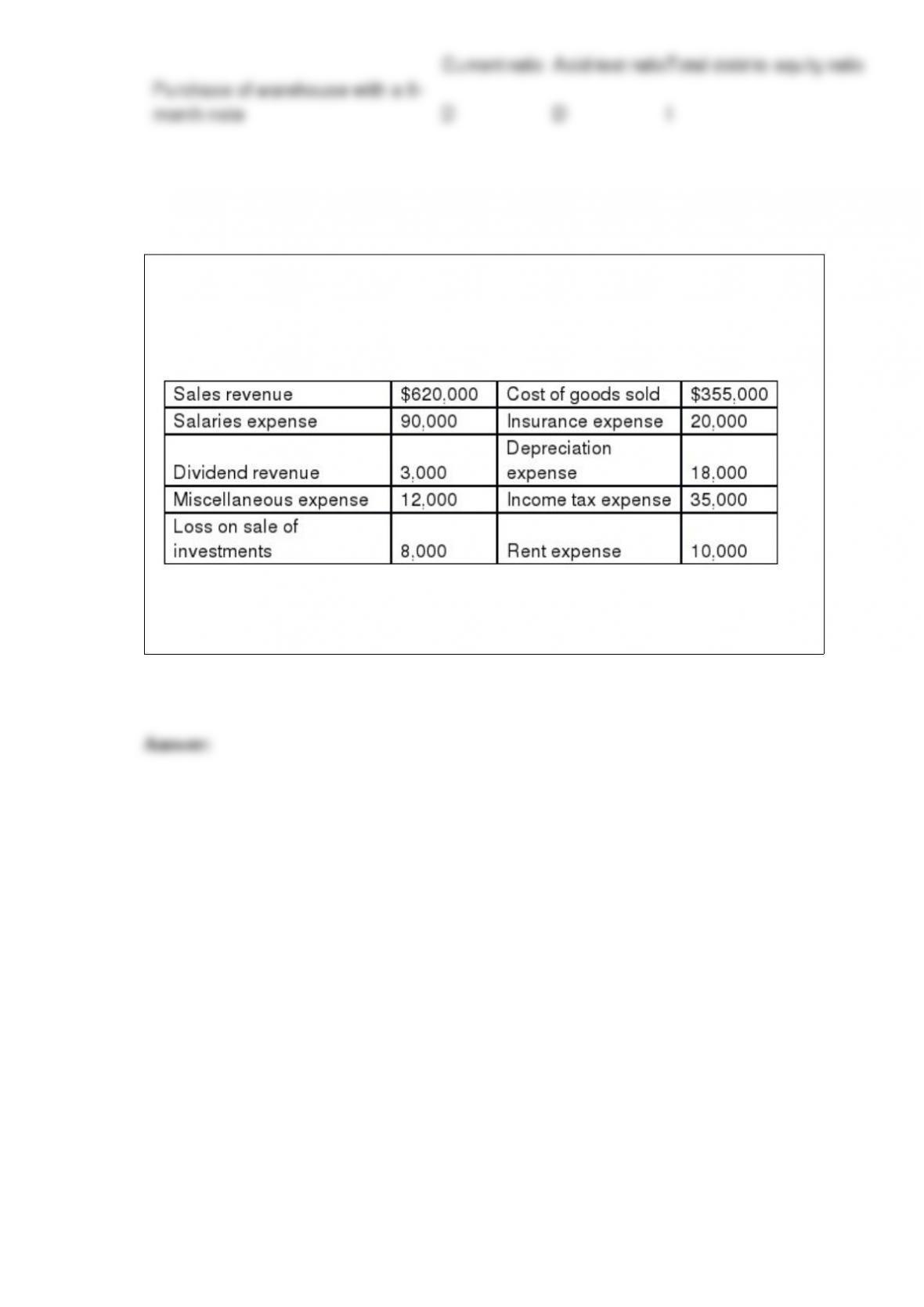

Presented below is income statement information of the Nebraska Corporation for the

year

ended December 31, 2016.

Required:

Prepare the necessary closing entries at December 31, 2016.