1) Qualified pension plans permit deductibility of the employers contributions to the

pension fund.

2) Companies record corrections of errors from prior periods as an adjustment to the

beginning balance of retained earnings in the current period.

3) Dividends declared on common and preferred stock are subtracted from net income

in the computation of earnings per share.

4) From the lessees viewpoint, an unguaranteed residual value is the same as no

residual value in terms of computing the minimum lease payments.

5) Improvements are often referred to as betterments and involve the substitution of a

better asset for the one currently used.

6) Under IFRS, there is a specific standard that mandates segregation of receivables

with different characteristics.

7) Amortization of a premium increases bond interest expense, while amortization of a

discount decreases bond interest expense.

8) If the market rate is greater than the coupon rate, bonds will be sold at a premium.

9) Gross profit and income from operations are reported on a multiple-step but not on a

single-step income statement.

10) Bishop Co. began operations on January 1, 2014 . Financial statements for 2014 and

2015 con- tained the following errors:

Dec. 31, 2014Dec. 31, 2015

Ending inventory$132,000 too high$146,000 too low

Depreciation expense84,000 too high

Insurance expense60,000 too low60,000 too high

Prepaid insurance60,000 too high

In addition, on December 31, 2015 fully depreciated equipment was sold for $28,800,

but the sale was not recorded until 2016 . No corrections have been made for any of the

errors. Ignore income tax considerations.

The total effect of the errors on the amount of Bishop’s working capital at December 31,

2015 is understated by

a.$390,800

b.$306,800

c.$174,800

d.$114,800

11) Which of the following does not demonstrate evidence regarding the ability to

consummate a refinancing of short-term debt?

a.Management indicated that they are going to refinance the obligation

b.Actually refinance the obligation

c.Have capacity under existing financing agreements that can be used to refinance the

obligation

d.Enter into a financing agreement that clearly permits the entity to refinance the

obligation

12) Norling Corporation reports the following information:

Net income$750,000

Dividends on common stock$210,000

Dividends on preferred stock$ 90,000

Weighted average common shares outstanding250,000

Norling should report earnings per share of

a.$1.80

b.$2.16

c.$2.64

d.$3.00

13) Jenks Corporation acquired Linebrink Products on January 1, 2015 for $8,000,000,

and recorded goodwill of $1,500,000 as a result of that purchase. At December 31,

2015, Linebrink Products had a fair value of $6,800,000. The net identifiable assets of

the Linebrink (excluding goodwill) had a fair value of $5,800,000 at that time. What

amount of loss on impairment of goodwill should Jenks record in 2015?

a.$ -0-

b.$500,000

c.$700,000

d.$1,200,000

14) Financial statements in the early 2000s provide information related to

a.nonfinancial measurements

b.forward-looking data

c.hard assets (inventory and plant assets)

d.None of these answer choices are correct

15) According to the FASB, recognition of a liability is required when the projected

benefit obligation exceeds the fair value of plan assets. Conversely, when the fair value

of plan assets exceeds the projected benefit obligation, the Board

a.requires recognition of an asset

b.requires recognition of an asset if the excess fair value of plan assets exceeds the

corridor amount

c.recommends recognition of an asset but does not require such recognition

d.does not permit recognition of an asset

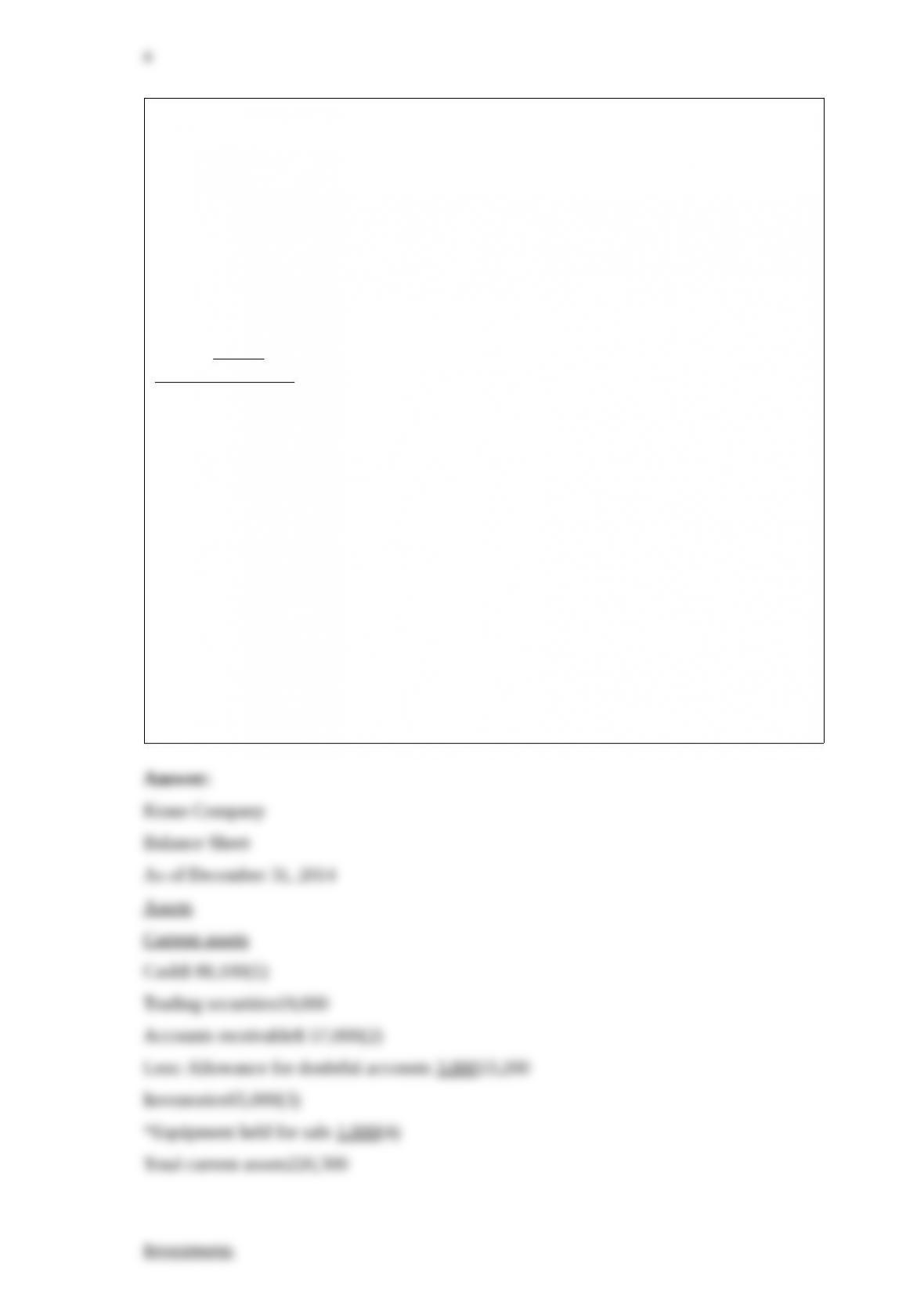

16) The following balance sheet was prepared by the bookkeeper for Kraus Company

as of December 31, 2014 .

Kraus Company

Balance Sheet

as of December 31, 2014

Cash$ 95,000Accounts payable$ 85,000

Accounts receivable (net)52,200Bonds payable100,000

Inventory62,000Stockholders’ equity238,500

Investments76,300

Equipment (net)106,000

Patents 32,000

$423,500$423,500

The following additional information is provided:

1>Cash includes the cash surrender value of a life insurance policy $9,400, and a bank

overdraft of $2,500 has been deducted.

2>The net accounts receivable balance includes:

(a)accounts receivabledebit balances $60,000;

(b)accounts receivablecredit balances $4,000;

(c)allowance for doubtful accounts $3,800.

3>Inventory does not include goods costing $3,000 shipped out on consignment.

Receivables of $3,000 were recorded on these goods.

4>Investments include investments in common stock, trading $19,000 and

available-for-sale $48,300, and franchises $9,000.

5>Equipment costing $5,000 with accumulated depreciation $4,000 is no longer used

and is held for sale. Accumulated depreciation on the other equipment is $40,000.

Instructions

Prepare a balance sheet in good form (stockholders’ equity details can be omitted.)

17) In consignment sales, the consignee

a.records the merchandise as an asset on its books

b.records a liability for the merchandise held on consignment

c.recognizes revenue when it ships merchandise to the consignor

d.prepares an account report for the consignor which shows sales, expenses, and cash

receipts

18) The acquisition cost of a certain raw material changes frequently. The book value of

the inventory of this material at year end will be the same if perpetual records are kept

as it would be under a periodic inventory method only if the book value is computed

under the

a.weighted-average method

b.moving average method

c.LIFO method

d.FIFO method

19) Tongas Company applies revaluation accounting to plant assets with a carrying

value of $1,600,000, a useful life of 4 years, and no salvage value. Depreciation is

calculated on the straight-line basis. At the end of year 1, independent appraisers

determine that the asset has a fair value of $1,500,000.

The entry to record depreciation for this same asset in year two will include a

a.debit to Accumulated Depreciation for $400,000

b.debit to Depreciation Expense for $500,000

c.credit to Accumulated Depreciation for $300,000

d.debit to Depreciation Expense for $400,000

20) When preparing a statement of cash flows, the following are used for which method

in determining cash flows from operating activities?

Gross Accounts ReceivableNet Accounts Receivable

a.IndirectDirect

b.DirectIndirect

c.DirectDirect

d.NeitherIndirect

21) Icon Industries, a company who uses IFRS reporting standards, is installing a new

plant. The company has incurred the following costs

1>Consultants used for advice on the acquisition of the plant$245,000

2>Interest charges paid to the supplier of plant for deferred credit$275,000

3>Estimated dismantling cost to be incurred after 8 years$400,000

4>Cost of the plant$2,300,000

Which of these costs can Tram capitalize in accordance with IFRS?

a.1, 2, 3, & 4

b.4 only

c.1 & 4

d.1, 3, & 4

22) For interim financial reporting, an extraordinary gain occurring in the second

quarter should be

a.recognized ratably over the last three quarters

b.recognized ratably over all four quarters with the first quarter being restated

c.recognized in the second quarter

d.disclosed by note only in the second quarter

23) Which of the following is not required when using the retail inventory method?

a.All inventory items must be categorized according to the retail markup percentage

which reflects the item’s selling price

b.A record of the total cost and retail value of the goods purchased

c.A record of the total cost and retail value of the goods available for sale

d.Total sales amount for the period

24) If bonds are initially sold at a discount and the straight-line method of amortization

is used, interest expense in the earlier years will

a.exceed what it would have been had the effective-interest method of amortization

been used

b.be less than what it would have been had the effective-interest method of amortization

been used

c.be the same as what it would have been had the effective-interest method of

amortiza-tion been used

d.be less than the stated (nominal) rate of interest

25) Jones, Inc. has net income (30% tax rate) of $1,400,000 for 2015, and an average

number of shares outstanding during the year of 500,000 shares. The corporation issued

$2,000,000 par value of 10-year, 9% convertible bonds on January 1, 2013 at a

$180,000 discount. The convertible bonds are convertible into 70,000 shares of

common stock. Assume the company uses the straight-line method for amortizing bond

discount.

Instructions

Compute the earnings per share data, excluding any notes if required.

26) Milner Co. sold a machine that cost $74,000 and had a book value of $44,000 for

$48,000. Data from Milner’s comparative balance sheets are:

12/31/1512/31/14

Machinery$800,000$670,000

Accumulated depreciation190,000136,000

Instructions

What four items should be shown on a statement of cash flows (indirect method) from

this information? Show your calculations.

27) Determine the unit value that should be used for inventory costing following “lower

of cost or market value” as described in ARB No. 43 .

A B C D E F

Cost$2.35$2.47$2.25$2.54$2.34$2.42

Replacement cost2.262.552.202.522.322.46

Net realizable value2.502.502.502.452.502.50

Net realizable value less normal profit2.302.302.302.302.302.30

28) Kroft is involved in a pending court case. Krofts lawyers believe it is probable that

Kroft will be awarded damages of $1,000,000.

Instructions

Discuss the proper accounting treatment, including any required disclosures, for each

situation. Give the rationale for your answers.

29) The following balance sheet has been submitted to you by an inexperienced

bookkeeper. List your suggestions for improvements in the format of the balance sheet.

Consider both terminology deficiencies as well as classification inaccuracies.

Jasper Industries, Inc.

Balance Sheet

For the Period Ended 12/31/14

Assets

Fixed AssetsTangible

Equipment$110,000

Less: reserve for depreciation (40,000)$ 70,000

Factory supplies22,000

Land and buildings400,000

Less: reserve for depreciation(150,000)250,000

Plant site held for future use 90,000$ 432,000

Current Assets

Accounts receivable175,000

Cash80,000

Inventory220,000

Treasury stock (at cost) 20,000495,000

Fixed Assets–Intangible

Goodwill80,000

Notes receivable 40,000

Patents 26,000 146,000

Deferred Charges

Advances to salespersons60,000

Prepaid rent27,000

Returnable containers 75,000 162,000

TOTAL ASSETS$1,235,000

Liabilities

Current Liabilities

Accounts payable$140,000

Allowance for doubtful accounts8,000

Common stock dividend distributable35,000

Income tax payable 42,000

Sales tax payable 17,000$ 242,000

Long-Term Liabilities, 5% debenture bonds, due 2017500,000

Reserve for contingencies 150,000 650,000

TOTAL LIABILITIES 892,000

Equity

Capital stock, $10 par value, issued 12,000 shares with

60 shares held as treasury stock$150,000

Capital surplus90,000

Dividends paid (20,000)

Earned surplus 123,000

TOTAL EQUITY 343,000

TOTAL LIABILITIES AND EQUITY$1,235,000

Note 1 .The reserve for contingencies has been created by charges to earned surplus and

has been established to provide a cushion for future uncertainties.

Note 2 .The inventory account includes only items physically present at the main plant and

warehouse. Items located at the company’s branch sales office amounting to $40,000 are

excluded since the company has consistently followed this procedure for many years.

30) What two assumptions are part of both the IFRS and GAAP conceptual framework?

31) Koch Co. sold convertible bonds at a premium. Interest is paid on May 31 and

November 30 . On May 31, after interest was paid, 100, $1,000 bonds are tendered for

conversion into 3,000 shares of $10 par value common stock that had a market price of

$40 per share. How should Koch Co. account for the conversion of the bonds into

common stock under the book value method? Discuss the rationale for this method.

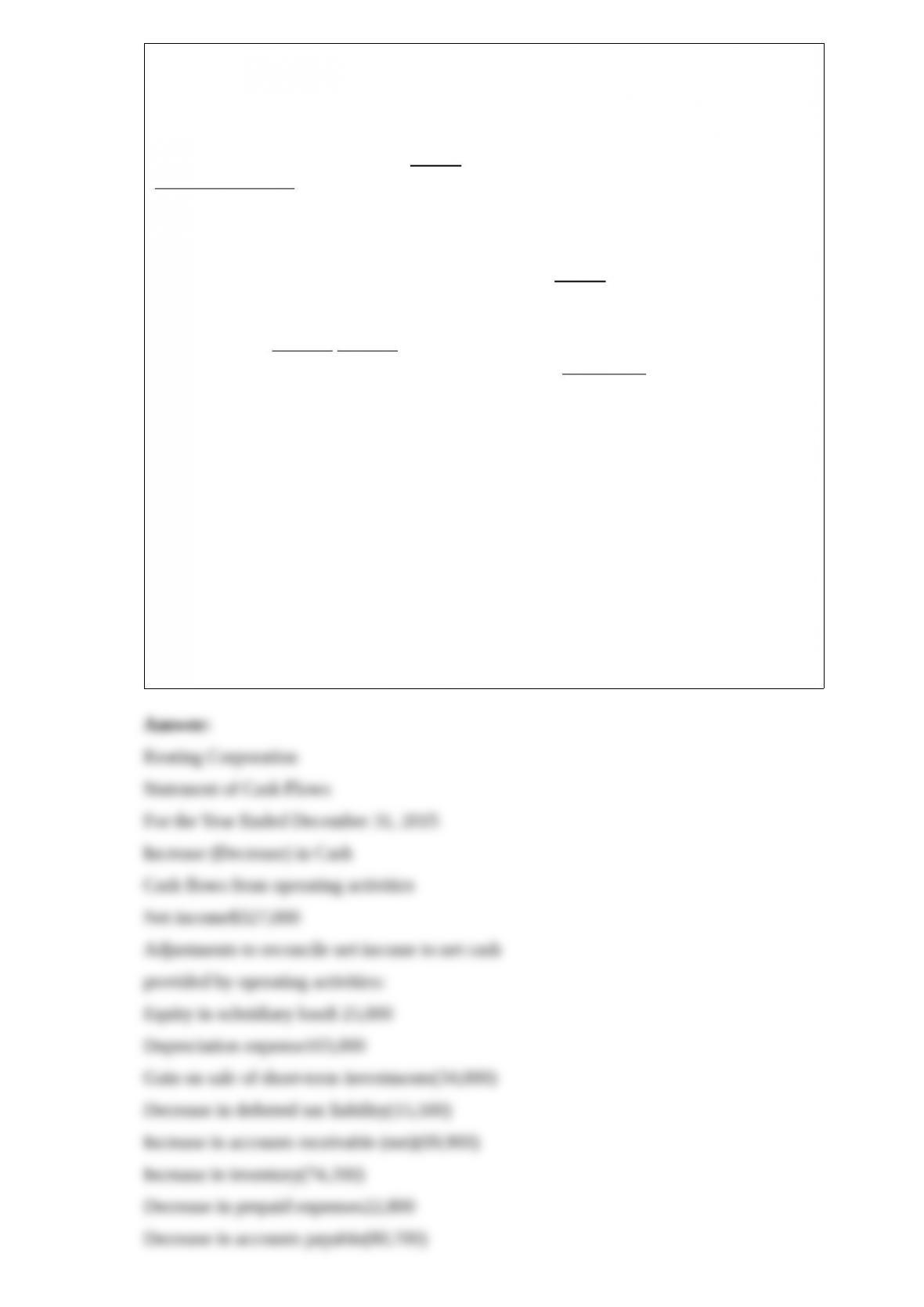

32) The net changes in the balance sheet accounts of Keating Corporation for the year

2015 are shown below.

Account Debit Credit

Cash$ 72,000

Short-term investments$121,000

Accounts receivable83,200

Allowance for doubtful accounts13,300

Inventory74,200

Prepaid expenses22,800

Investment in subsidiary (equity method)25,000

Plant and equipment220,000

Accumulated depreciation130,000

Accounts payable80,700

Accrued liabilities21,500

Deferred tax liability15,500

8% serial bonds70,000

Common stock, $10 par90,000

Additional paid-in capital150,000

Retained earningsAppropriation for bonded indebtedness60,000

Retained earningsUnappropriated 38,000

$643,600$643,600

An analysis of the Retained EarningsUnappropriated account follows:

Retained earnings unappropriated, December 31, 2014$1,300,000

Add:Net income327,000

Transfer from appropriation for bonded indebtedness 60,000

Total$1,687,000

Deduct:Cash dividends$185,000

Stock dividend 240,000 425,000

Retained earnings unappropriated, December 31, 2015$1,262,000

1>On January 2, 2015 short-term investments (classified as available-for-sale) costing

$121,000 were sold for $155,000.

2>The company paid a cash dividend on February 1, 2015 .

3>Accounts receivable of $16,200 and $19,400 were considered uncollectible and

written off in 2015 and 2014, respectively.

4>Major repairs of $33,000 to the equipment were debited to the Accumulated

Depreciation account during the year. No assets were retired during 2015 .

5>The wholly owned subsidiary reported a net loss for the year of $20,000. The loss

was recorded by the parent.

6>At January 1, 2015, the cash balance was $166,000.

Instructions

Prepare a statement of cash flows (indirect method) for the year ended December 31,

2015 . Keating Corporation has no securities which are classified as cash equivalents.

33) Briefly describe some of the similarities and differences between U.S. GAAP and

IFRS with respect to the accounting for investments.

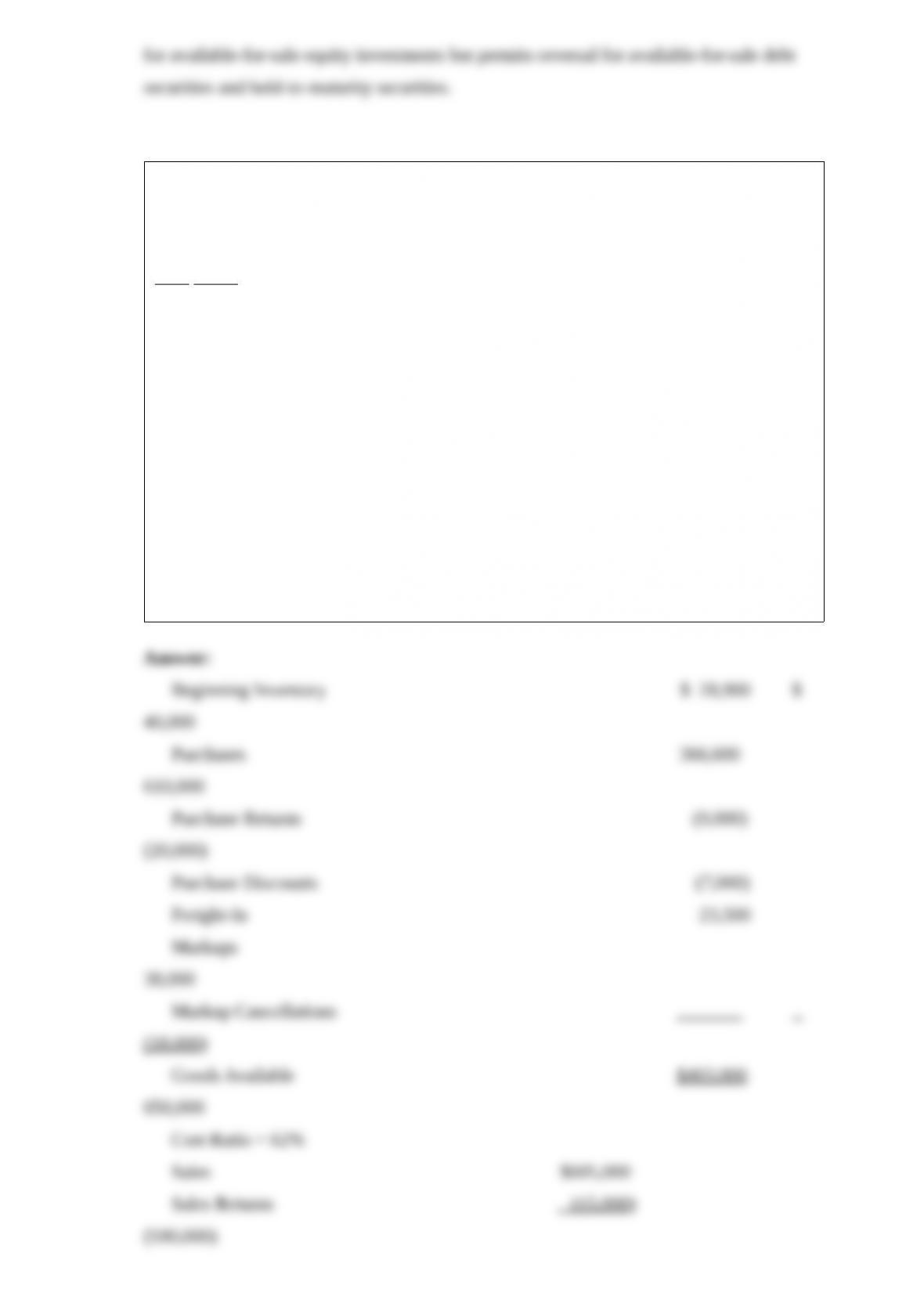

34) Landmark Book Store uses the conventional retail method.

Instructions

Given the following data, prepare a neat, labeled schedule showing the computation of

the cost of inventory on hand at 12/31/14.

Cost Retail

Inventory 1/1/14$ 28,900$ 40,000

Purchases366,600610,000

Purchases Returns9,00020,000

Purchase Discounts7,000

Sales (Gross)605,000

Sales Returns15,000

Employee Discounts5,000

Freight-in23,500

Freight-out50,000

Loss from Breakage2,500

Markups38,000

Markup Cancellations18,000

Markdowns13,500

Markdown Cancellations8,500