Accounts receivable are normally reported at the:

a. Present value of future cash receipts.

b. Current value plus accrued interest.

c. Expected amount to be received.

d. Current value less expected collection costs.

When a deposit on returnable containers is forfeited, the firm holding the deposit will

experience:

a. A decrease in cost of goods sold.

b. An increase in current liabilities.

c. An increase in accounts receivable.

d. An increase in revenue.

Stanhope Associates accounts for the following investments under IFRS No. 9:

1> 10 shares of Blackstone equity, held for long-term investment, no election of

FVOCI.

2> 10 shares of Erickson equity, held for risk management, election to classify as

FVOCI.

3> 10 shares of AT&E equity, held for immediate resale.

4> 10 bonds (consisting of only interest and principal) issued by Filo Inc., held for

long-term collection of cash flows.

5> 10 bonds (consisting of only interest and principal) of SimSung, held for risk

management but also might be sold

6> 10 bonds (consisting of only interest and principal) issued by Attachi, held for

immediate resale. Required:

For each investment, indicate: (a) the accounting approach that will be used to account

for the investment, and briefly explain why that approach is appropriate, and (b) the

effect on earnings of an increase in the fair value of the investment in the period

following acquisition of the investment, assuming that Stanhope does not sell the

investment. You may group the specific investments if they have the same answers.

Identify the investments you are including in the group.

Assume that the scales, software and calibration service are all separate performance

obligations. How much revenue will Ortiz recognize in 2016 for this contract?

On July 15, 2016, Ortiz & Co. signed a contract to provide EverFresh Bakery with an

ingredient-weighing system for a price of $90,000. The system included finely tuned

scales that fit into EverFresh’s automated assembly line, Ortiz’s proprietary software

modified to allow the weighing sytem to function in EverFresh’s automated system, and

a one-year contract to calibrate the equipment and software on an as-needed basis.

(Ortiz competes with other vendors who offer ongoing calibration contracts for Ortiz’s

systems.) If Ortiz was to provide these goods and services separately, it would charge

$60,000 for the scales, $10,000 for the software, and $30,000 for the calibration

contract. Ortiz delivered and installed the equipment and software on August 1, 2016,

and the calibration service commenced on that date. a. $0

b. $63,000

c. $74,250

d. $90,000

Inventory records for Herb’s Chemicals revealed the following: March 1, 2016,

inventory: 1,000 gallons @ $7.20 = $7,200

Ending inventory assuming LIFO in a periodic inventory system would be:

a. $5,040.

b. $5,055.

c. $5,075.

d. $5,135.

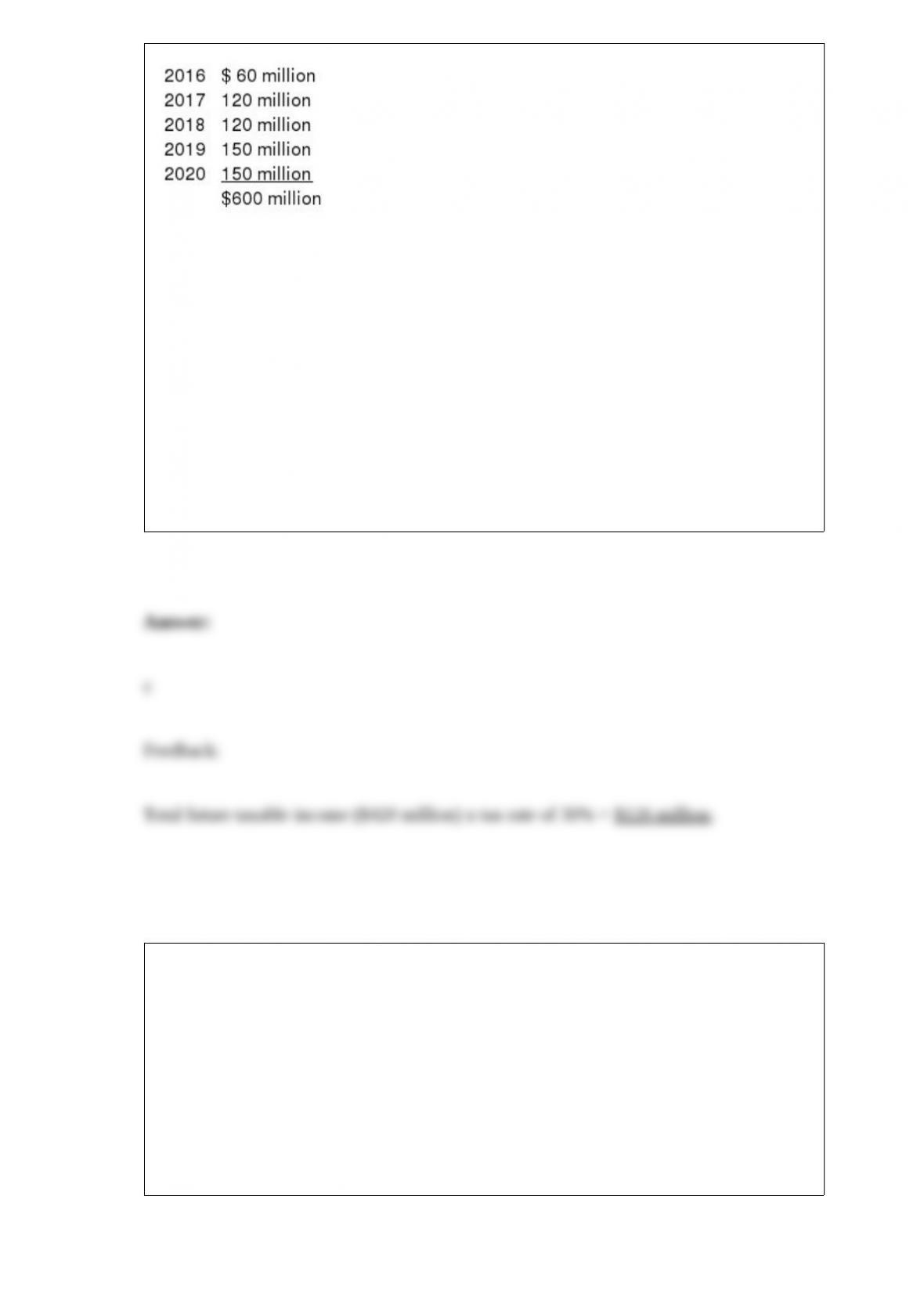

Isaac Inc. began operations in January 2016. For certain of its property sales, Isaac

recognizes income in the period of sale for financial reporting purposes. However, for

income tax purposes, Isaac recognizes income when it collects cash from the buyer’s

installment payments.

In 2016, Isaac had $600 million in sales of this type. Scheduled collections for these

sales are as follows:

Assume that Isaac has a 30% income tax rate and that there were no other differences in

income for financial statement and tax purposes.

Ignoring operating expenses and additional sales in 2017, what deferred tax liability

would Isaac report in its year-end 2017 balance sheet?

a. $ 54 million

b. $144 million

c. $126 million

d. $180 million.

What is the effective interest rate (rounded) on a 3-month, noninterest-bearing note with

a stated rate of 12% and a maturity value of $200,000?

a. 12.4%.

b. 13.6 %.

c. 11.5%.

d. 3.1%.

Woody Corp. had taxable income of $8,000 in the current year. The amount of MACRS

depreciation was $3,000, while the amount of depreciation reported in the income

statement was $1,000. Assuming no other differences between tax and accounting

income, Woody’s pretax accounting income was:

a. $ 5,000.

b. $ 6,000.

c. $10,000.

d. $11,000.

Under the LIFO retail method, which of the following are not included in the

denominator of the cost-to-retail conversion percentage?

a. Freight-in.

b. Purchase returns.

c. Purchases.

d. Net markdowns.

The use of LIFO in accounting for a firm’s inventory:

a. Usually matches the physical flow of goods through the business.

b. Is usually used for internal management purposes.

c. Usually provides a better match of expenses with revenues.

d. None of these answer choices is correct.

According to GAAP for accounting for income taxes, when a company has a net

operating loss carryforward:

a. A deferred tax liability is recognized.

b. A receivable is created.

c. A deferred tax equity account is created.

d. A deferred tax asset is recorded along with any applicable valuation allowance.

A change from the straight-line method to the sum-of-years’-digits method of

depreciation is handled as:

a. A retrospective change back to the date of acquisition as though the current estimated

life had been used all along.

b. A cumulative adjustment to income in the current year for the difference in

depreciation under the new versus old useful life estimate.

c. A prospective change from the current year through the remainder of its useful life.

d. None of these answer choices are correct.

Describe the way we account for a change in estimate. What is the appropriate

accounting if we are unable to determine whether a change is a change in estimate or a

change in principle?

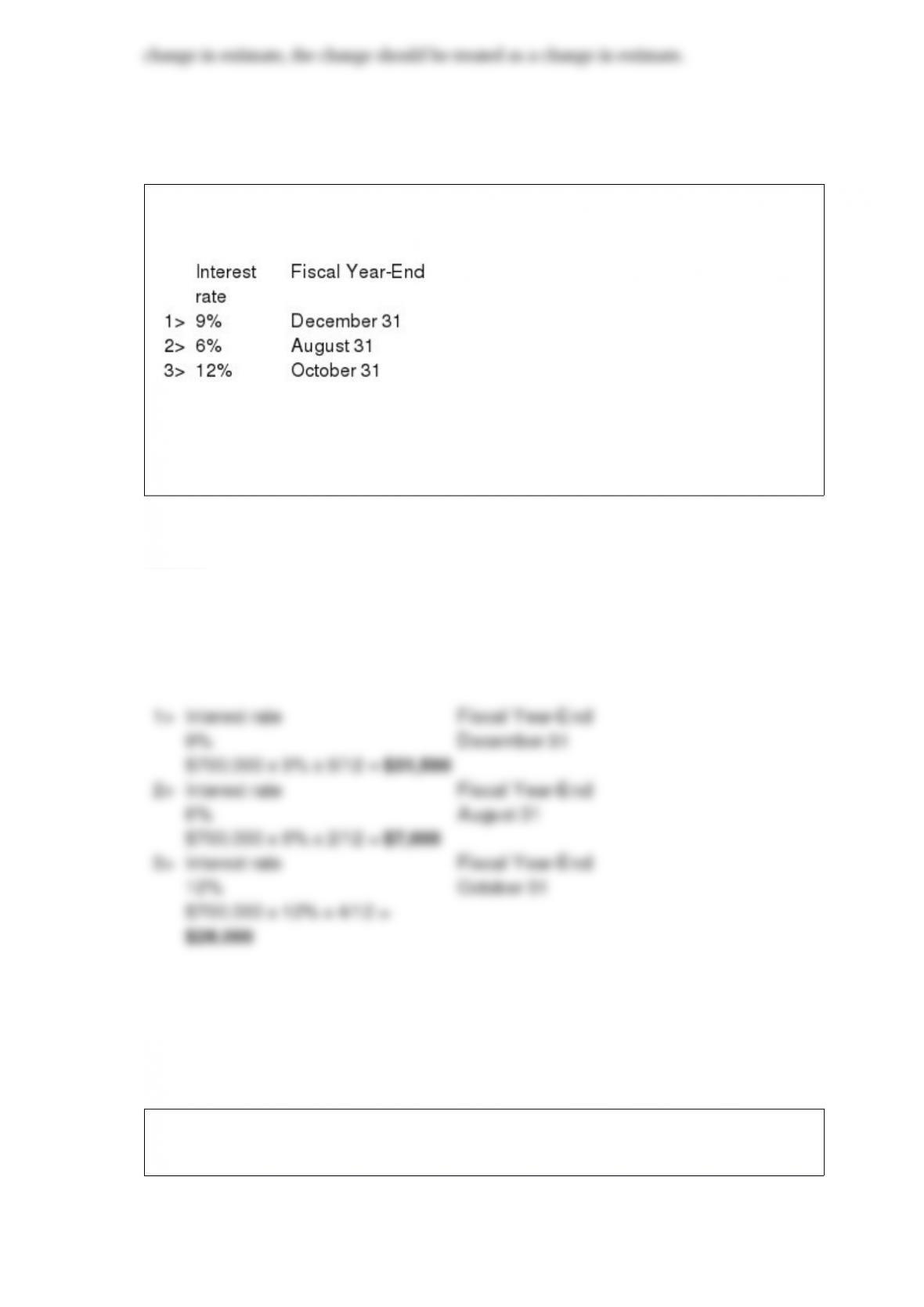

On June 30, 2016, Chu Industries issued 9-month notes in the amount of $700,000.

Assume that interest is payable at maturity in the following three independent cases:

Required:

Determine the amount of interest expense that should be accrued in a year-end adjusting

entry under each assumption:

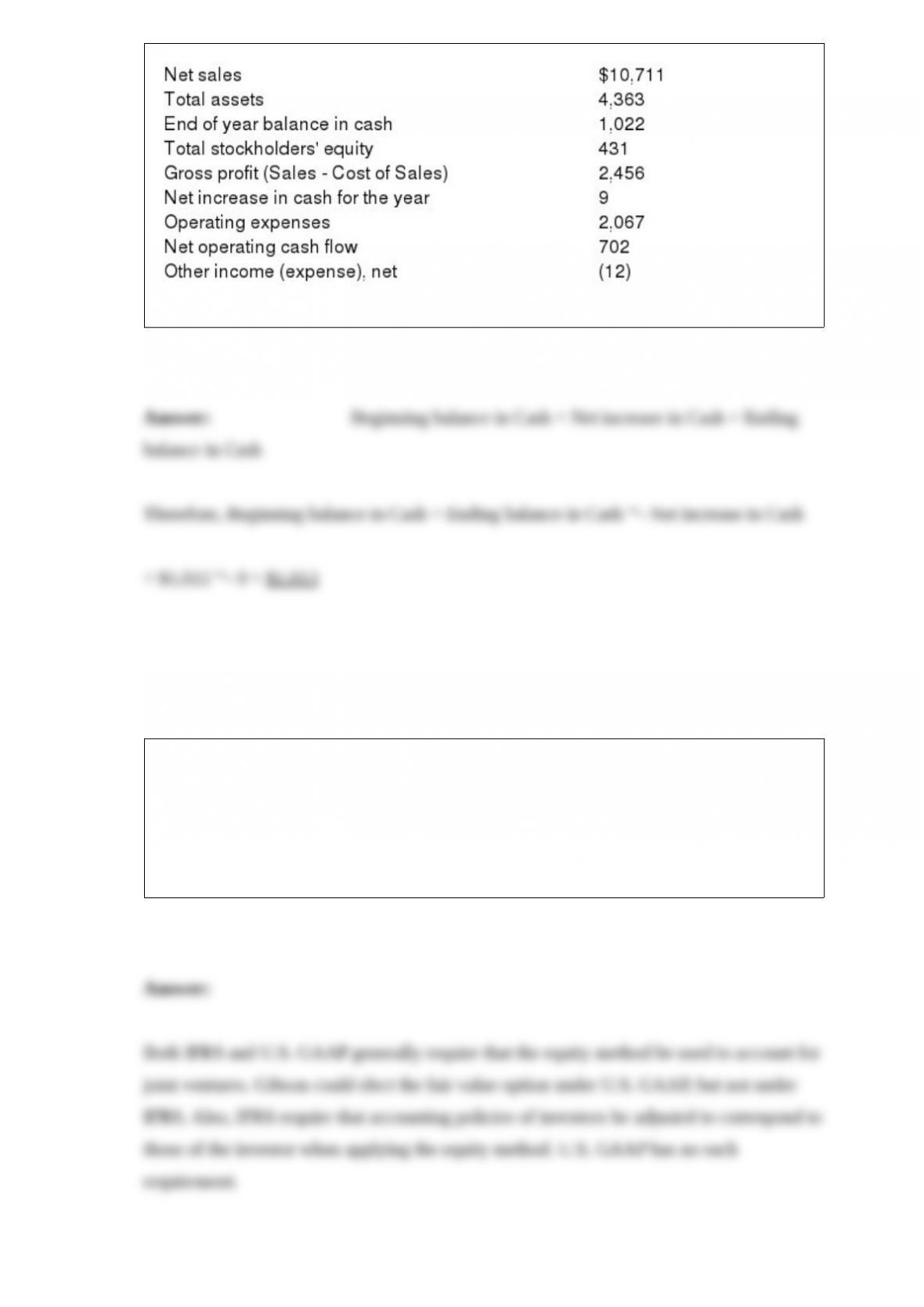

The following information ($ in millions) comes from a recent annual report of

Amazon.com, Inc.:

Compute Amazon’s balance in cash at the beginning of the year.

Assume Gibson Company is an equal partner in a joint venture with Glover Company.

Each company owns 50% of Pesci Company, and equally shares decision-making

authority. Required:

Describe how U.S. GAAP and IFRS differ in how they would have Gibson account for

this investment.

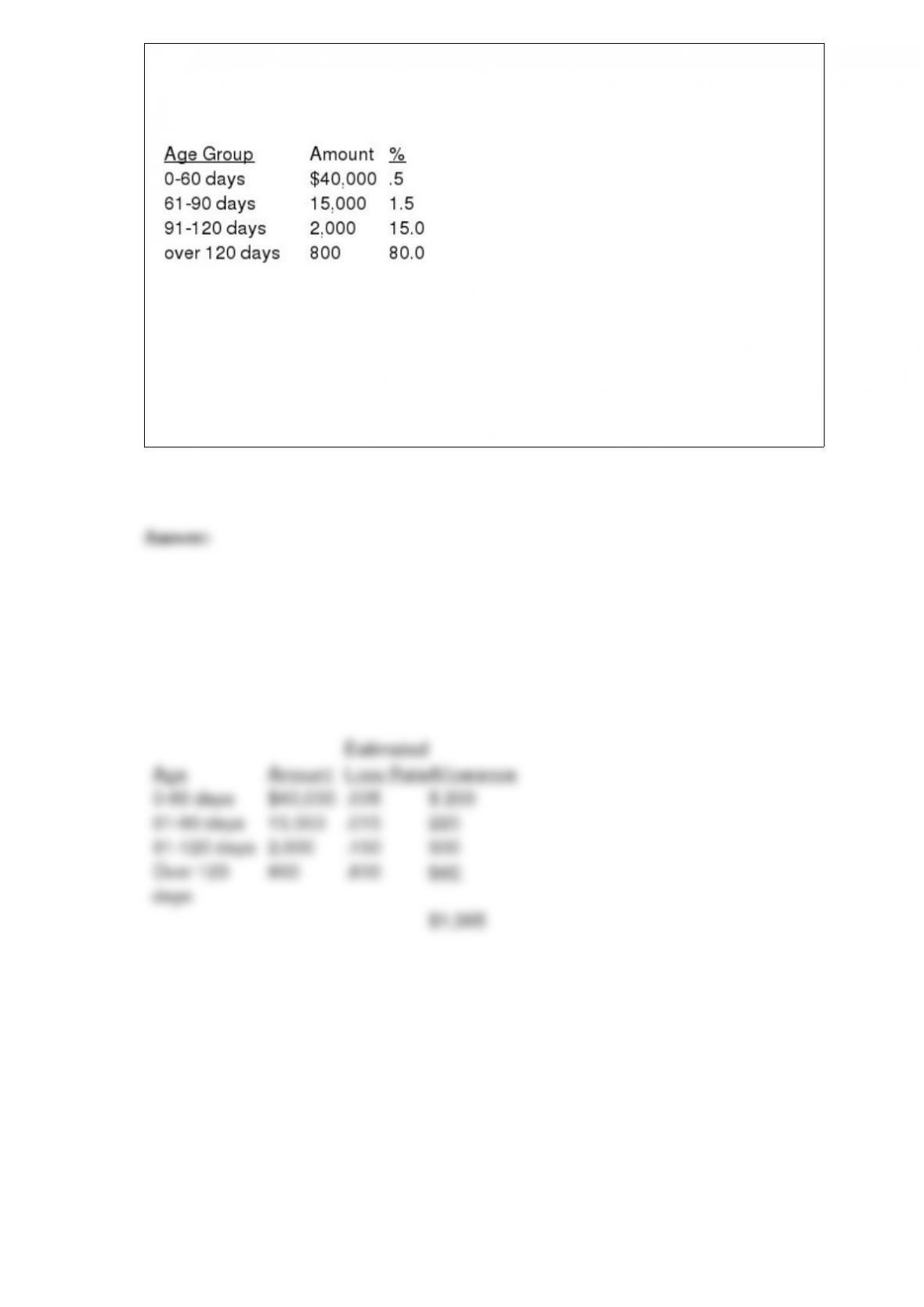

A summary of London Fashion’s December 31, 2016, accounts receivable aging

schedule is presented below along with the estimated percent uncollectible for each age

group:

The allowance for uncollectible accounts had a balance of $1,600 at January 1, 2016.

During the year bad debts of $1,150 were written off.

Required:

Prepare all 2016 journal entries with respect to bad debts and the allowance for

uncollectible accounts.

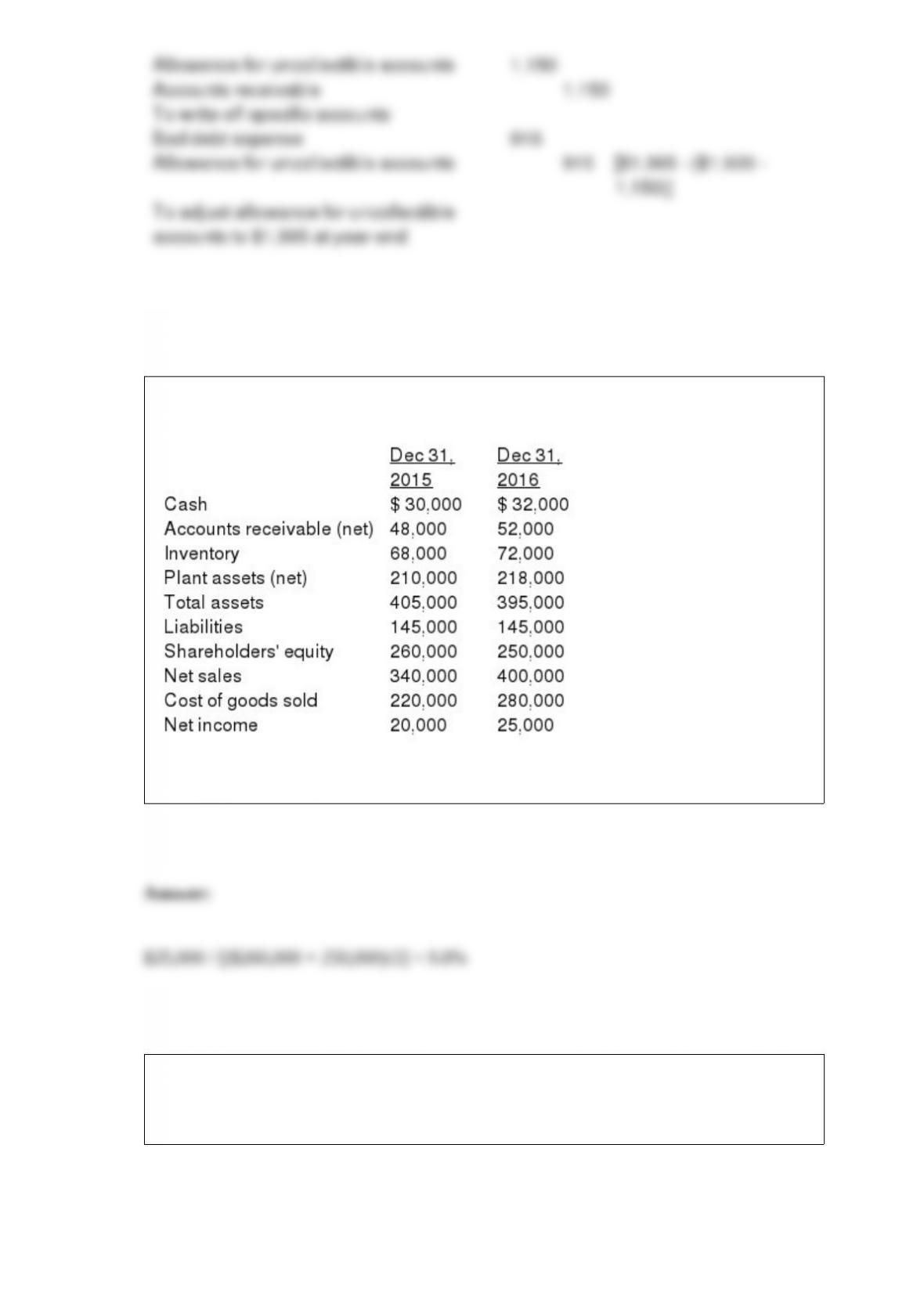

Missoula Inc. reported the following selected financial statement data:

Required: Compute the return on shareholders’ equity for 2016. Round your answer to

one decimal place, e.g., .1234 as 12.3%.

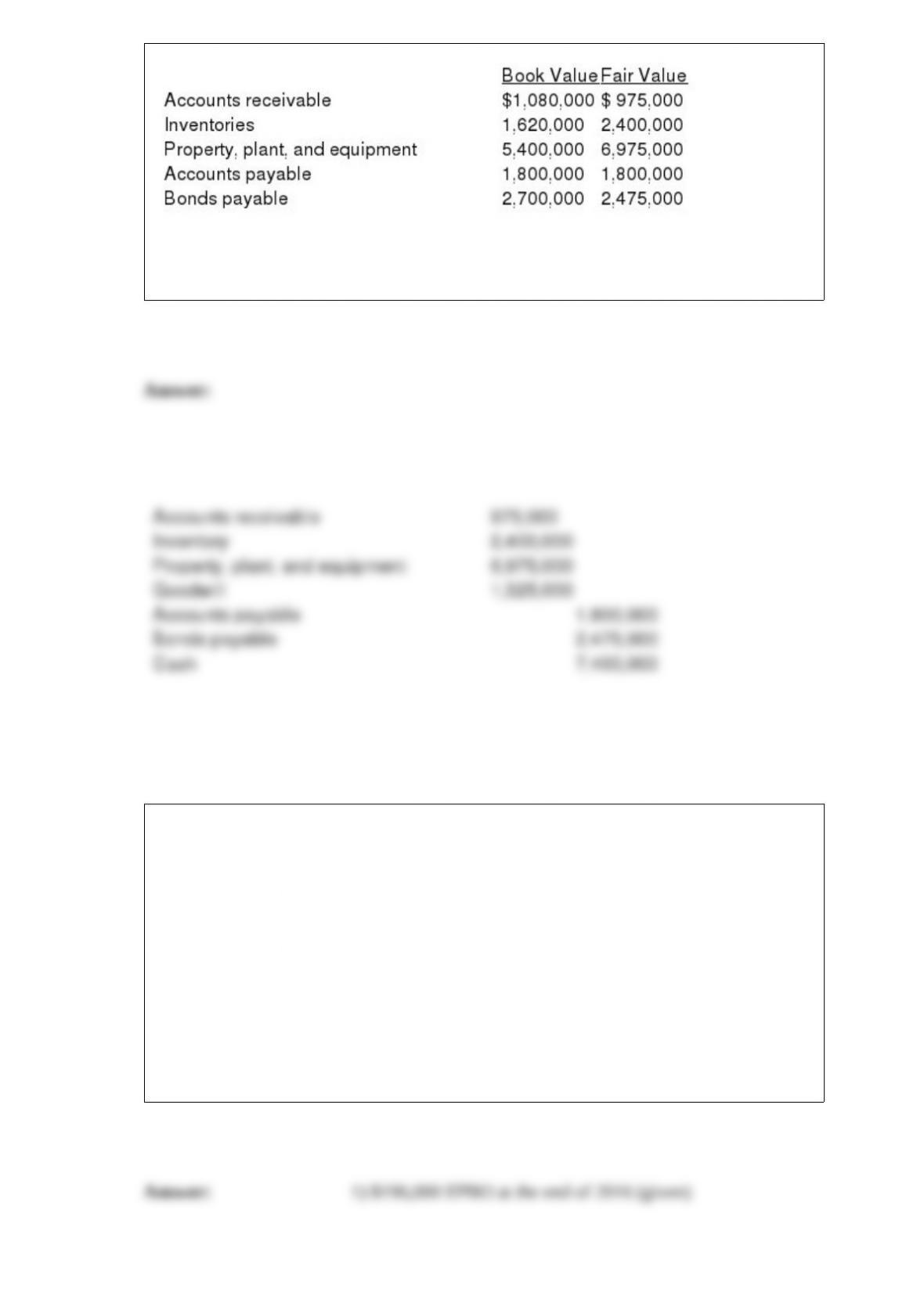

On August 15, 2016, Willis Inc. acquired all of the outstanding common stock of Bork

Inc. paying $7,400,000 cash. The book values and fair values of Willis’ assets and

liabilities are listed below:

Required:

Prepare the journal entry to record the acquisition by Willis Inc.

Silver Springs Company has an unfunded retiree health care plan. Each of the

company’s four employees has been with the organization since its inception at the

beginning of 2015. As of the end of 2016, the actuary estimates the total net cost of

providing benefits to employees during their retirement years to have a present value of

$196,000. Each of the employees will become fully eligible for benefits after 28 more

years of service, but aren’t expected to retire for 30 more years. The interest rate is 8%.

Required:

1) What is the expected postretirement benefit obligation at the end of 2016?

2) What is the accumulated postretirement benefit obligation at the end of 2016?

LaBelle Corporation owns a $6 million whole life insurance policy on the life of its

CEO, naming LaBelle as beneficiary. The annual premiums are $95,000 and are

payable at the beginning of each year. The cash surrender value of the policy was

$56,000 at the beginning of 2016.

Required:

1) Prepare the appropriate 2016 journal entry to record insurance expense and the

increase in the investment, assuming the cash surrender value of the policy increased

according to the contract to $70,000

2) The CEO died at the end of 2016. Prepare the appropriate journal entry.

•