Which of the following is a value-added activity by a manufacturer of chocolate

candies?

A. The addition of chocolate syrup into the candy mix.

B. Hiring production workers.

C. Storing the candy bars until they are distributed to stores.

D. Managing the cost of electricity by the production department.

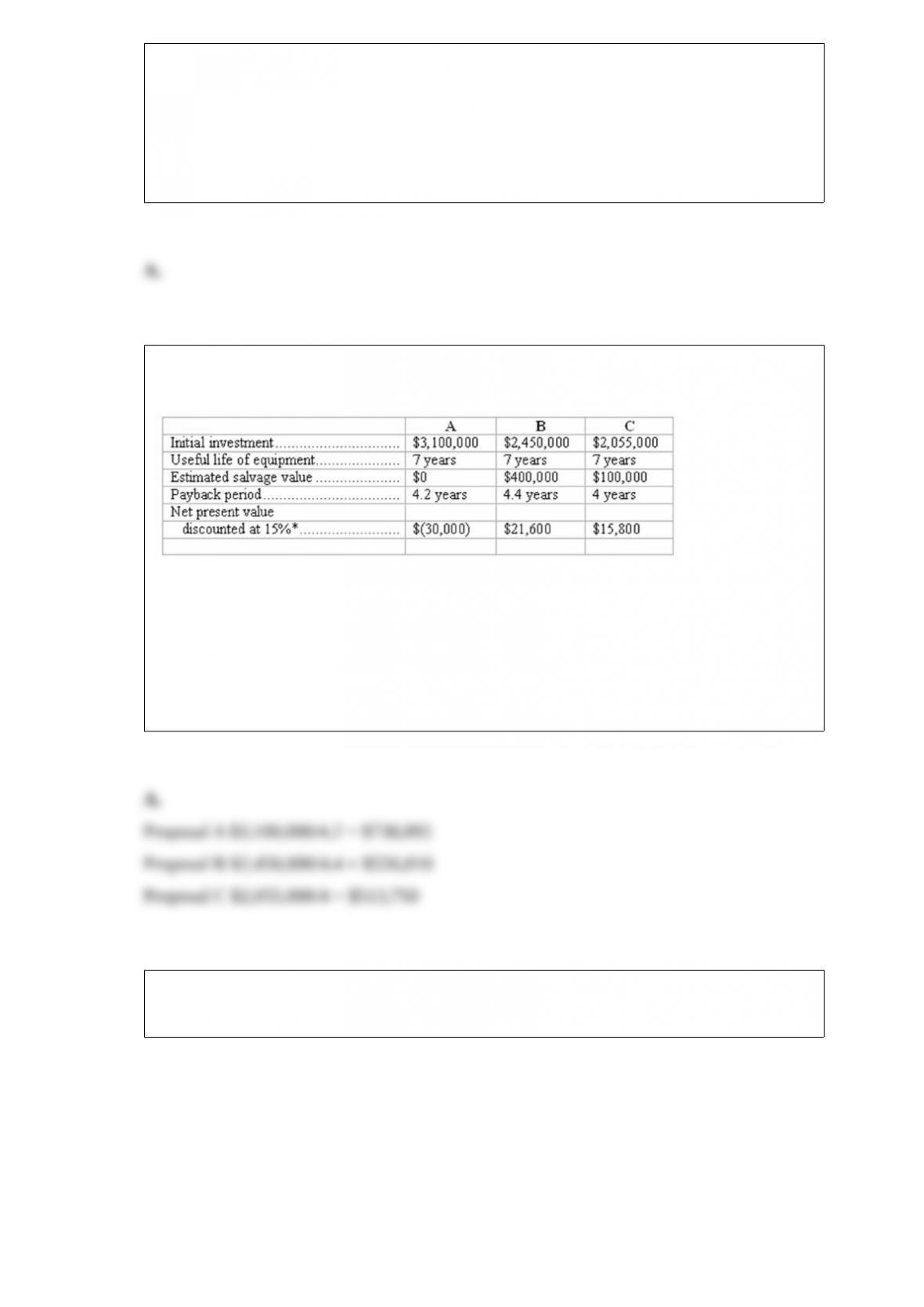

The management of Ortega Manufacturing has three different proposals under

consideration. The Accounting Department has prepared the following information:

*Management’s required rate of return is 15%.

Refer to the information above. Which of the above proposals generates the greatest

annual cash flow?

A. Proposal A.

B. Proposal B.

C. Proposal C.

D. Cannot be determined with the given information.

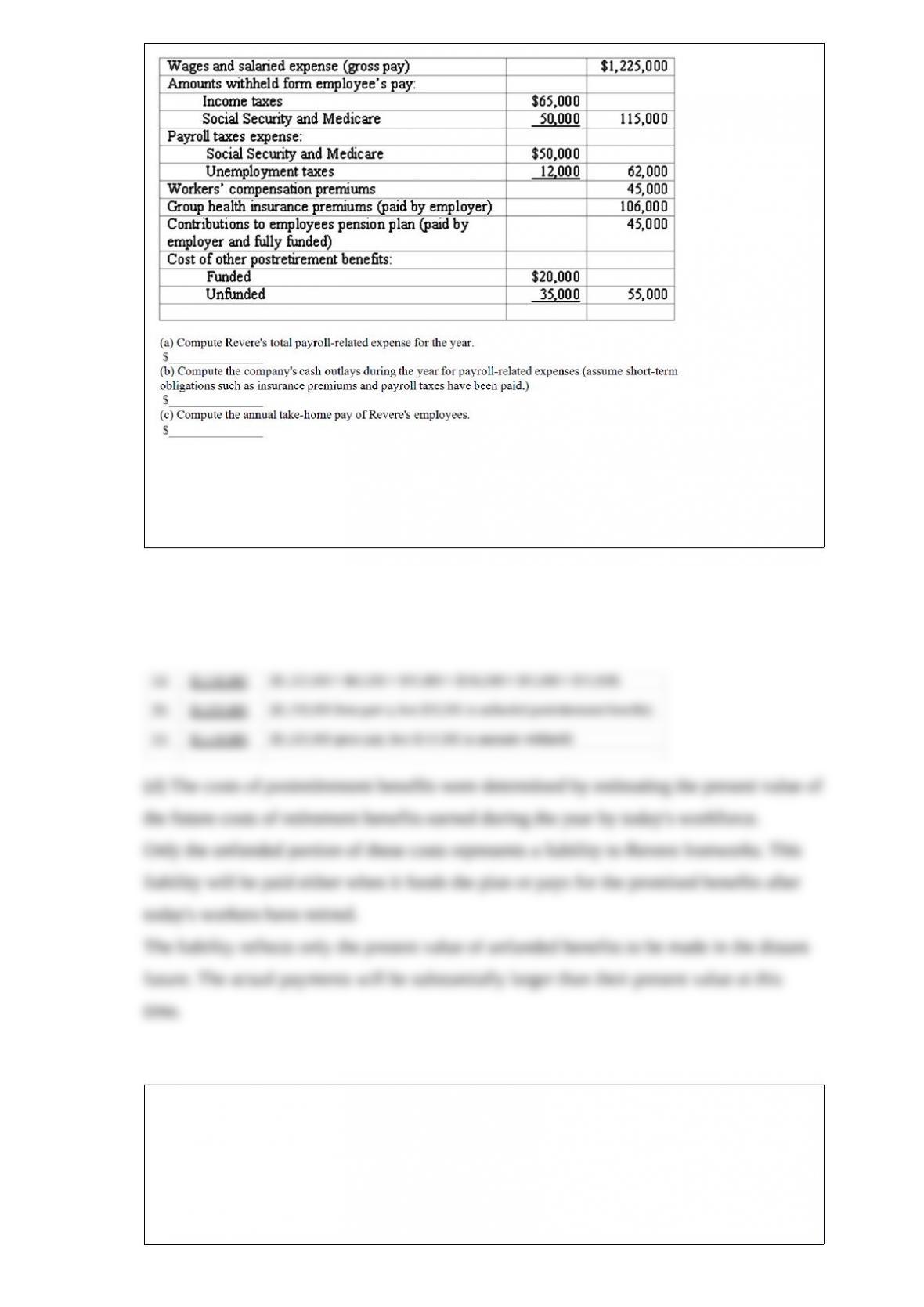

Payroll-related expenses

Shown below is a summary of the annual payroll data of Revere Ironworks:

(d) How were the costs of postretirement benefits determined? Which of these amounts

results in a liability to Revere Ironworks, and when will this liability be paid? Will the

amount of the payments be more or less than the amount now shown as a liability?

Explain.

At year-end, the perpetual inventory records of Anderson Co. indicate 60 units of a

particular product in inventory, acquired at the following dates and unit costs:

Purchased in August: 30 units at $750 per unit.

Purchased in November: 30 units at $700 per unit.

A complete physical inventory taken at year-end indicates only 50 units of this product

actually are on hand.

Refer to the information above. Assuming that Anderson uses the LIFO cost flow

assumption, it should record this inventory shrinkage by:

A. Debiting Cost of Goods Sold $7,000.

B. Crediting Cost of Goods Sold $7,500.

C. Debiting Cost of Goods Sold $7,500.

D. Crediting Cost of Goods Sold $7,000.

Which of the following is an example of a contingent liability?

A. A lawsuit pending against a restaurant chain for improper storage of perishable food

items.

B. The liability for future warranty repairs on computers sold during the current period.

C. A corporation’s long-term employment contract with its chief executive officer.

D. A liability for notes payable with interest included in the face amount.

The adjusting entries to record depreciation or amortization expense or to write down

assets that have become impaired:

A. Reduce both net income and cash balances.

B. Reduce net income, but have no direct effect on cash balances.

C. Decrease cash balances, but have no direct effect upon net income.

D. Affect neither net income nor cash balances.

When no-par stock is issued:

A. The entire amount received is credited to the Additional Paid-in Capital account.

B. The issue price is credited to the Capital Stock account.

C. There is no legal capital created because there is no par or stated value.

D. The transaction usually involves only an exchange for non-cash assets or services,

since the stock has no value on the stock exchanges.

A balance sheet:

A. Provides owners, investors, and other interested parties with all the financial

information they need to evaluate the financial strength, profitability, and future

prospects of a given business entity.

B. Shows the current market value of the owners’ equity in the business at the balance

sheet date.

C. Assists creditors in evaluating the debt-paying ability of a business by showing the

assets and liabilities of the business combined with those of its owner (or owners).

D. Shows the assets, liabilities, and owners’ equity of a business entity, valued in

conformity with generally accepted accounting principles.

On January 31, 2015, Village Bank had 500,000 shares of $2 par value common stock

outstanding. On that date, the company declared a 14% stock dividend when the market

price of the stock was $37 per share. The immediate effect of this dividend upon Village

Bank was:

A. A reduction in cash of $2,590,000.

B. A reduction in retained earnings of $2,590,000.

C. A reduction in retained earnings of $140,000.

D. A liability to the stockholders of $140,000.

Refer to the information above. If total assets of Hercules Manufacturing, Inc. are

$556,000, Retained Earnings at December 31, 2014, must be:

A. $811,000.

B. $180,000.

C. $221,000.

D. $335,000.

A/P ($12,000) + N/P ($135,000) + Capital Stock ($188,000) + R.E.(?) = $556,000

When evaluating the liquidity of a partnership, creditors will likely base their decision

on:

A. the business ability to generate a profit.

B. previous debts of the business.

C. the total assets owned by the business.

D. the financial strength of the owners.

Refer to the information above. The journal entry to record the cost of direct materials

used in June includes:

A. A debit to Work in Process Inventory of $12,220.

B. A credit to Materials Price Variance of $520.

C. A debit to Materials Price Variance of $520.

D. A credit to Direct Materials Inventory of $12,250.

Which of the following is a period cost?

A. Direct materials used.

B. Direct labor costs applicable to production.

C. Manufacturing overhead.

D. Advertising expense.

A future amount is the dollar amount to which a present value will ______________

over time.

A. vanish

B. accumulate

C. disappear

D. remain

Short-term creditors are most likely to use the quick ratio instead of the current ratio in

evaluating the solvency of a company with large, slow-moving:

A. Plant and equipment.

B. Receivables.

C. Inventories.

D. Employees.

If a company purchases equipment for $65,000 by issuing a note payable:

A. Total assets will increase by $65,000.

B. Total assets will decrease by $65,000.

C. Total assets will remain the same.

D. The company’s total owners’ equity will decrease.

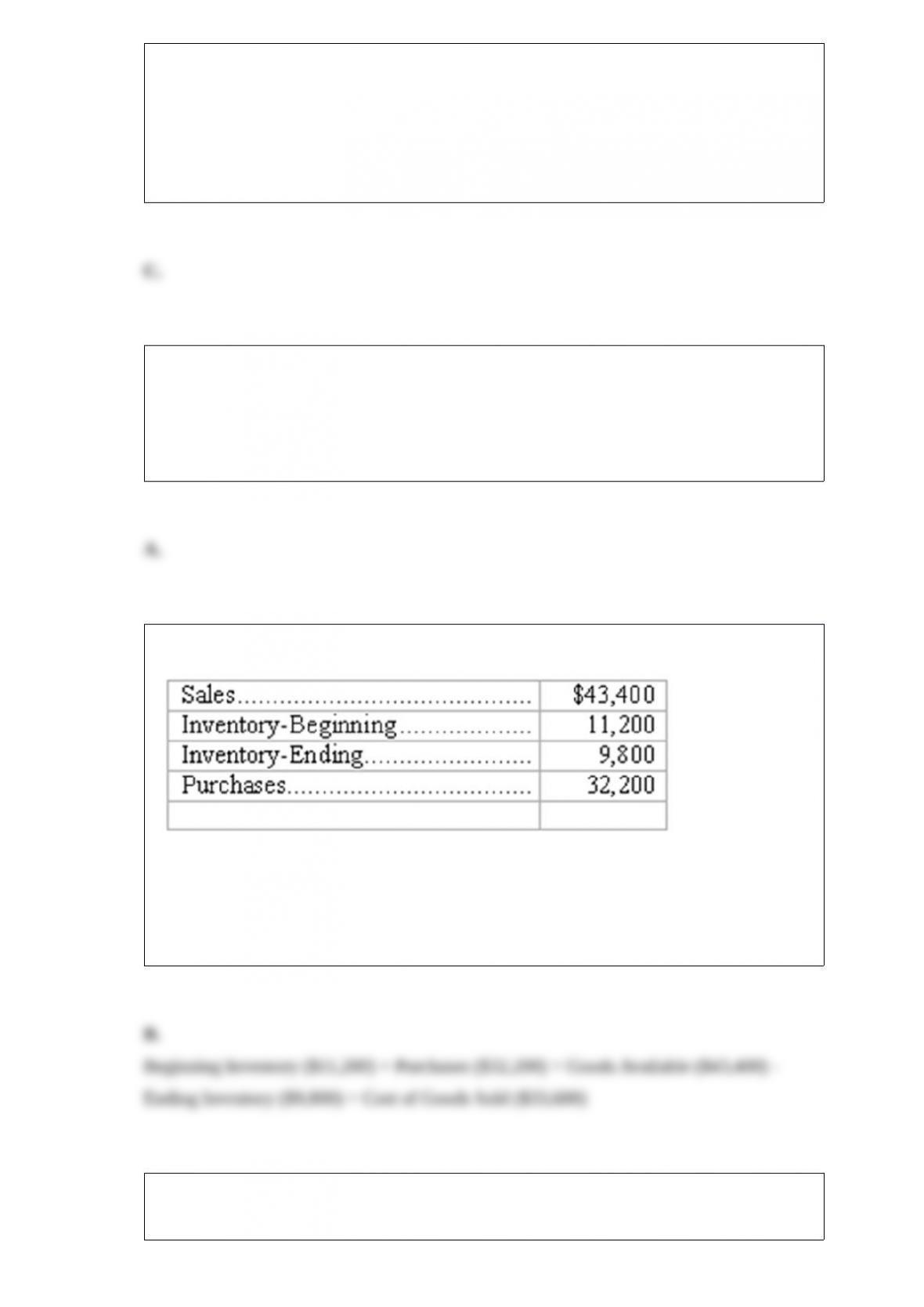

Michael uses its periodic inventory system and the following information is available:

Refer to the information above. What is the cost of goods sold?

A. $9,800.

B. $33,600.

C. $32,200.

D. $43,400.

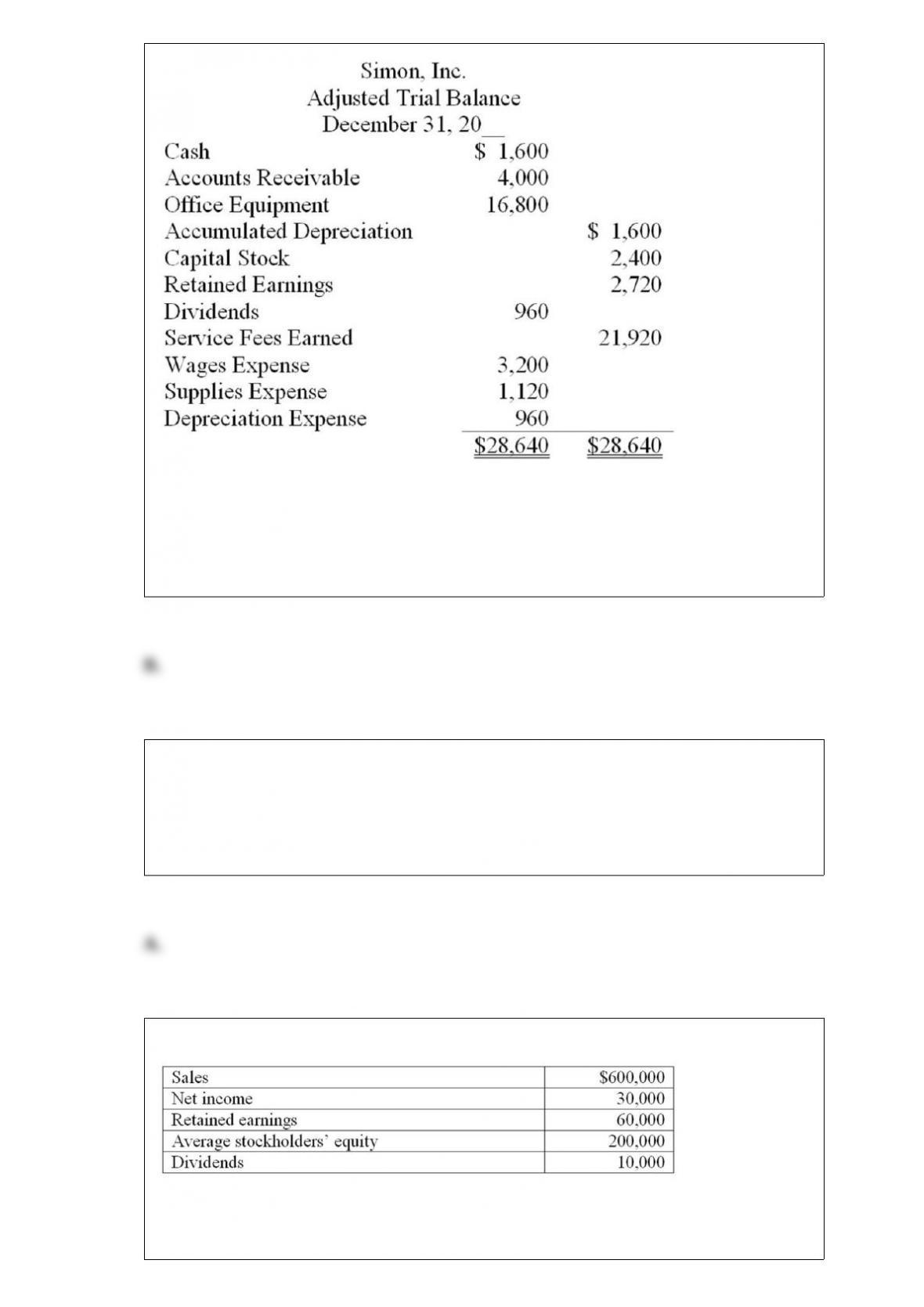

Shown below is the adjusted Trial Balance for Simon Inc., on December 31, after the

first year of operations, after adjusting entries:

Refer to the information above. The entry to close Depreciation Expense account will:

A. Transfer the balance of Depreciation Expense directly to Retained Earnings.

B. Include a debit to Income Summary.

C. Include a debit to Depreciation Expense.

D. Include a credit to Capital Stock.

Gross profit is the difference between:

A. Net sales and the cost of goods sold.

B. The cost of merchandise purchased and the cost of merchandise sold.

C. Net sales and net income.

D. Net sales and all expenses.

The following information is available:

What is the return on equity? (round to the nearest number)

A. 5%.

B. 15%.

C. 20%.

D. 25%.

Which of the following indicates cash receipts?

A. Debit entries in the Notes Receivable account.

B. Credit entries in the Marketable Securities account.

C. Debit entries in the Notes Payable account.

D. Credit entries in the Accumulated Depreciation account.

Benefits of activity-based costing include all of the following except:

A. More accurate measures of product costs.

B. More accurate evaluations of product profitability.

C. A better understanding of what “drives” manufacturing overhead costs.

D. More subjective product pricing decisions.

Before any month-end adjustments are made, the net income of Russell Company is

$38,000. However, the following adjustments are necessary: office supplies used,

$3,160; services performed for clients but not yet recorded or collected, $3,040; interest

accrued on a note payable to bank, $3,640. After adjusting entries are made for the

items listed above, Russell Company’s net income would be:

A. $38,000.

B. $34,240.

C. $41,160.

D. $44,200.

Kent Company has used the same inventory method for many years. This is an example

of which principle?

A. Matching.

B. Realization.

C. Cost.

D. Consistency.

If I invest $20,000 at 2.5% today, how long will it take to reach a minimum of $50,000

compounded semi-annually?

A. 5 years.

B. 19 years.

C. 9 and years.

D. 17 years.

Refer to the information above. If Summit Products requires a 25% return on sales to

undertake production, what is the target cost for the new widget?

A. $65.00.

B. $67.50.

C. $80.00.

D. Some other amount.

The adjustment of available for sale marketable securities to their current market value

affects:

A. The balance sheet.

B. The income statement.

C. The cash flow statement.

D. All of the answers are correct.

Gamma Company adjusts its accounts at the end of each month. The following

information has been assembled in order to prepare the required adjusting entries at

December 31:

(1) A one-year bank loan of $720,000 at an annual interest rate of 6% had been obtained

on December 1.

(2) The company’s pays all employees up-to-date each Friday. Since December 31 fell

on Tuesday, there was a liability to employees at December 31 for two day’s pay.

Employees earn a total of $12,800 per week.

(3) On December 1, rent on the office building had been paid for three months. The

monthly rent is $7,000.

(4) Depreciation of office equipment is based on an estimated useful life of five years.

The balance in the Office Equipment account is $12,360; no change has occurred in the

account during the year.

(5) All fees totaling $19,800 were earned during the month for clients who had paid in

advance.

Refer to the information above. What should be the balance of the Prepaid Rent?

A. $0.

B. $7,000.

C. $14,000.

D. $21,000.

At December 31, before adjusting and closing the accounts had occurred, the

Allowance for Doubtful Accounts of Seaboard Corporation showed a debit balance of

$3,200. An aging of the accounts receivable indicated the amount probably

uncollectible to be $2,100. Under these circumstances, a year-end adjusting entry for

uncollectible accounts expense would include a:

A. Debit to the Allowance for Doubtful Accounts for $1,100.

B. Credit to the Allowance for Doubtful Accounts for $1,100.

C. Debit to Uncollectible Accounts Expense of $2,100.

D. Debit to Uncollectible Accounts Expense of $5,300.

Relationship of cash flows to accrual accounting

(a) The 2015 statement of cash flows of Citation Corporation shows the amount of cash

received from customers as $800,000. Comparative balance sheets report accounts

receivable to be $70,000 at January 1 and $100,000 at December 31, 2015. Compute

the amount of net sales reported in Citation Corporation’s income statement for 2015:

$_______________

(b) The supplementary schedule for noncash investing and financing activities

accompanying Citation Corporation’s 2015 statement of cash flows disclosed the

following:

Citation Corporation’s 2015 income statement reports a $61,000 loss on the disposal of

land. Prepare the journal entry made by Citation in 2015 to record this sale of land.

The dollar amount by which sales can decline before an operating loss is incurred is

called the:

A. Contribution margin.

B. Contribution margin ratio.

C. Margin of safety.

D. Relevant range.

Washington Warehouse is a small retail business that specializes in the sale of

top-of-the-line televisions. This year, the store has begun to carry the Flat TV

manufactured by Bass Co. Thus far, Washington has recorded the following transactions

involving the Flat TV:

Jan. 5 Purchased 8 Flat TVs at a unit cost of $1,400

Jan. 18 Purchased 5 additional Flat TVs at $1,400 each

Feb. 12 Sold 9 Flat TVs to the Duke Hotel for $15,300

Refer to the information above. If Washington uses a perpetual inventory system, the

journal entry to record the purchase on January 18th would include which of the

following?

A. A debit to the Purchases account for $7,000.

B. A debit to the Cost of Goods Sold for $7,000.

C. A credit to Inventory for $7,000.

D. A debit to Inventory for $7,000.