1) The least helpful common audit test to verify current period acquisitions of property,

plant, and equipment is examining vendors’ invoices and receiving reports.

A) True

B) False

2) Which of the following statements regarding the letter of representation is not

correct?

A) It is prepared on the client’s letterhead

B) It is addressed to the CPA firm

C) It is signed by high-level corporate officials, usually the president and chief financial

officer

D) It is optional, not required, that the auditor obtain such a letter from management

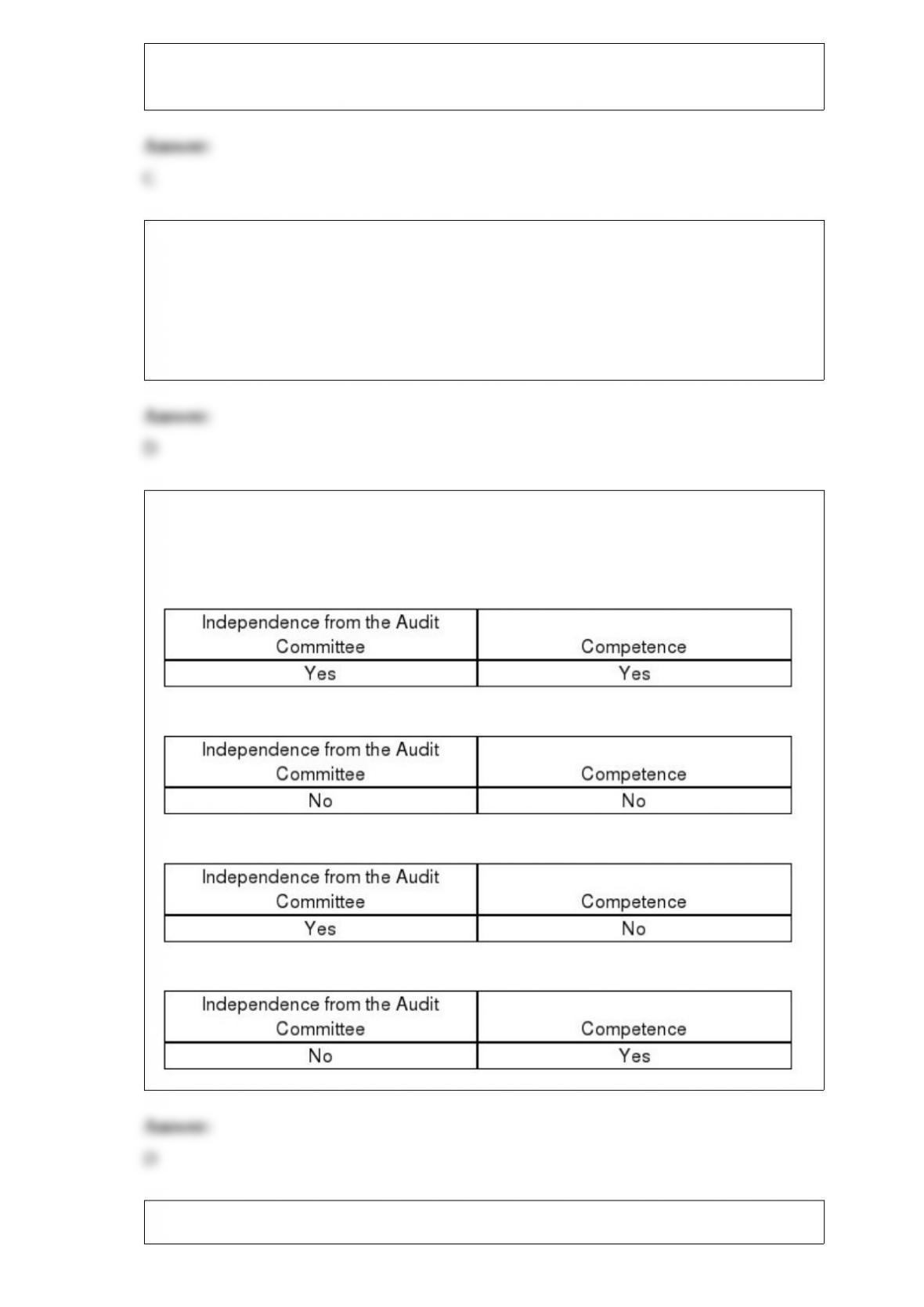

3) The most effective audit evidence gathered for accounts receivable is the:

A) detail tie-in of the records

B) analysis of the allowance for doubtful accounts

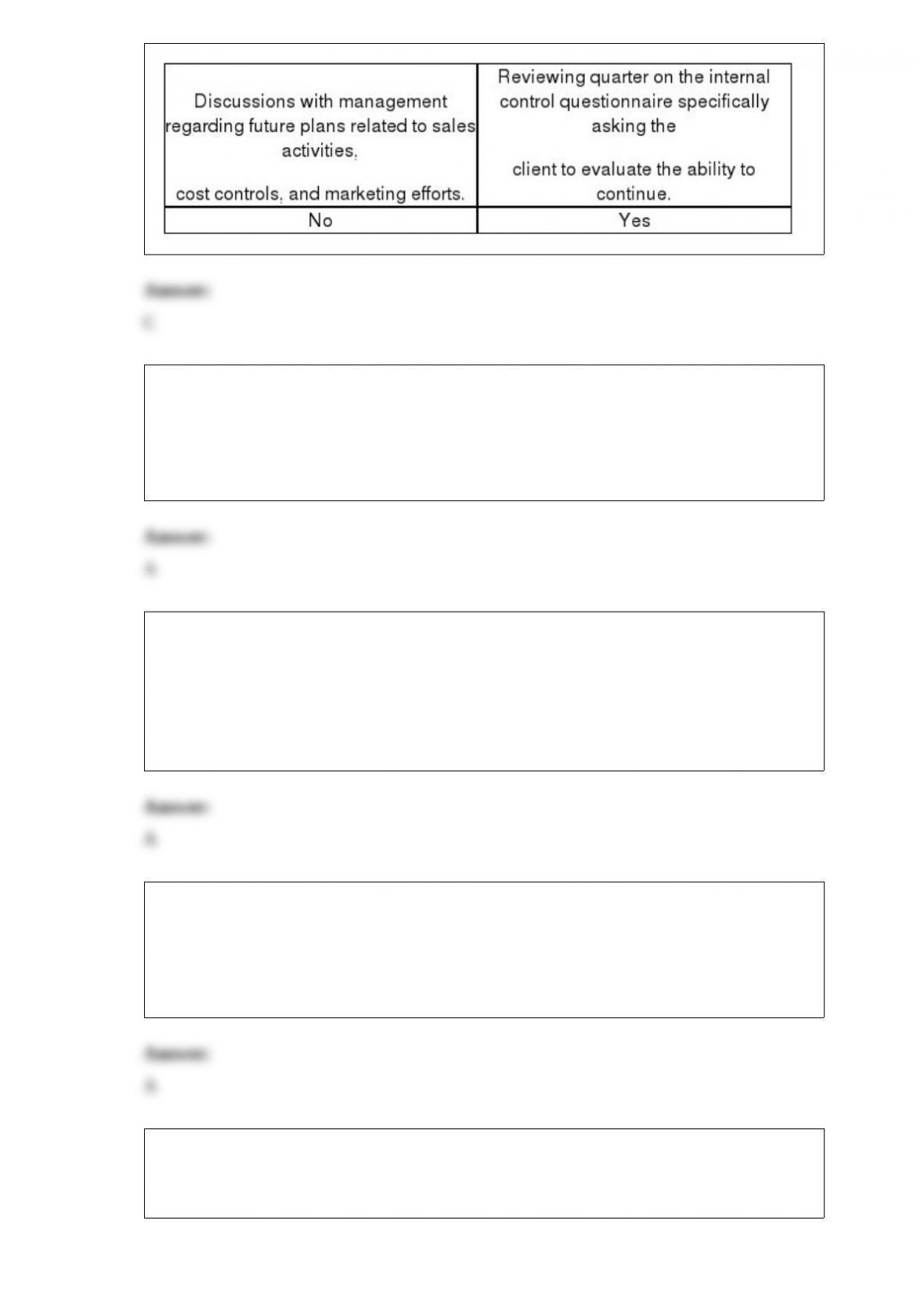

C) confirmation of accounts receivable

D) examination of sales invoices

4) The most important output control is:

A) distribution control, which assures that only authorized personnel receive the reports

generated by the system

B) review of data for reasonableness by someone who knows what the output should

look like

C) control totals, which are used to verify that the computer’s results are correct

D) logic tests, which verify that no mistakes were made in processing

5) An increased extent of tests of controls is most likely to occur when:

A) it is a first-year audit

B) the auditor is doing a “fraud audit”

C) controls are effective and the preliminary control risk assessment is low

D) controls are ineffective and the preliminary control risk assessment is high

6) When auditors allocate the preliminary judgment about materiality to account

balances, the materiality allocated to any given account balance is referred to as:

A) the materiality range

B) the error range

C) tolerable materiality

D) tolerable misstatement

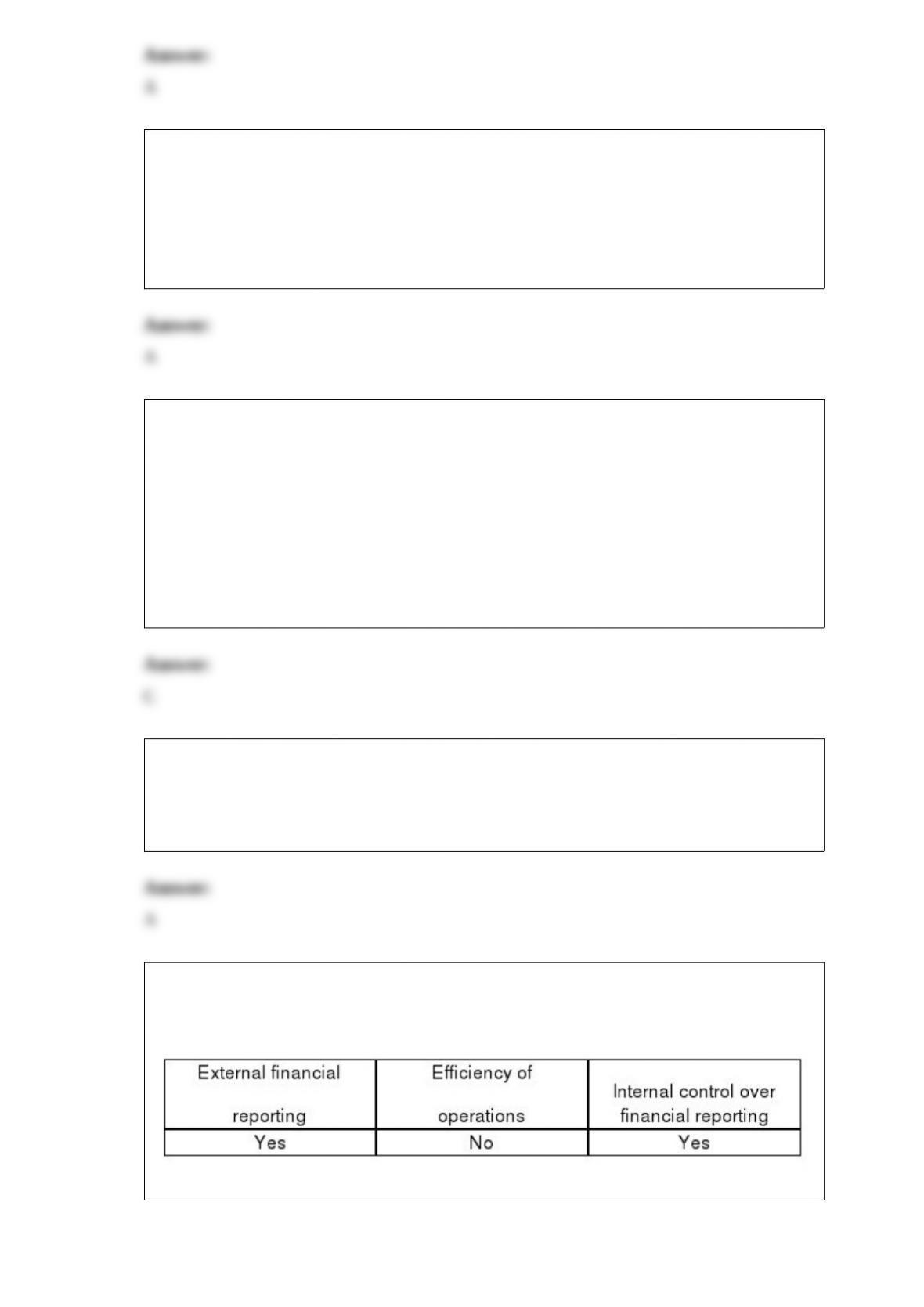

7) External financial statement auditors must obtain evidence regarding what attributes

of an internal audit department if the external auditors intend to rely on the internal

auditor’s work?

A)

B)

C)

D)

8) A document review of which of the following is most likely to yield evidence of any

unrecorded liabilities?

A) Receiving reports

B) Vendor Memorandums

C) Unpaid accounts payable

D) Sales invoices out of sequence

9) Which of the following types of owners’ equity transactions would not require

authorization by the board of directors?

A) Issuance of capital stock

B) Repurchase of capital stock

C) Declaration of dividends

D) None of the above

10) The advantage of systematic sample selection is that:

A) it is easy to use

B) there is limited possibility of it being biased

C) it is unnecessary to determine if the population is arranged randomly

D) it automatically selects items material to the financial statements

11) The two most important qualities for an operational auditor are:

A) personality and appearance

B) independence and competence

C) competence and technical training

D) academic background and sufficient experience

12) Rodgers CPA believes that the rate of client billing errors is 4% and has established

a tolerable deviation rate of 6%. In auditing client invoices Rodgers should use:

A) stratified sampling

B) classical sampling

C) proportional sampling

D) attributes sampling

13) Companies with securities traded on national and over-the-counter exchanges are

required to submit audited financial statements once every three years to the Securities

and Exchange Commission.

A) True

B) False

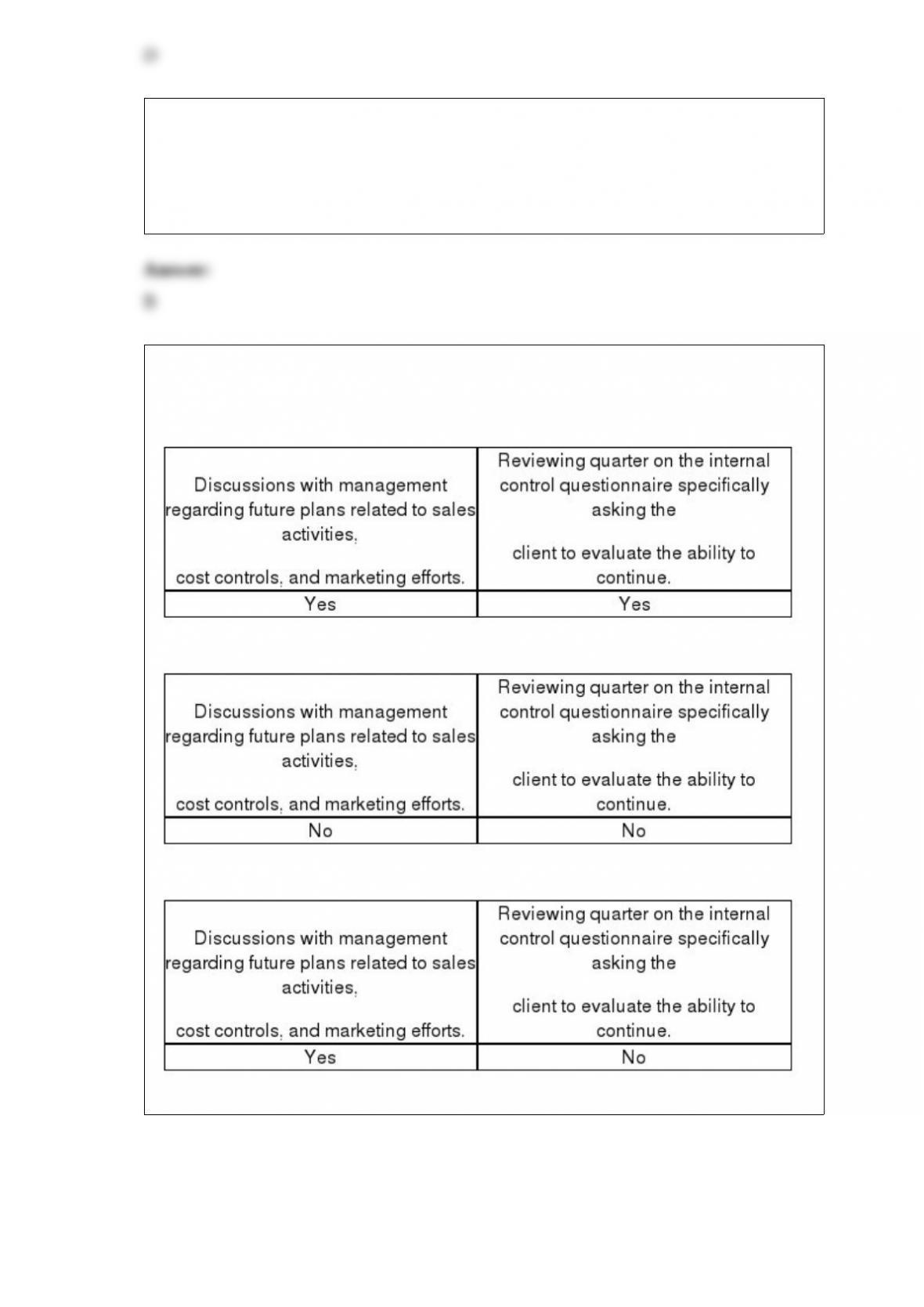

14) Which of the following procedures and methods are important in assessing a

company’s ability to continue as a going concern?

A)

B)

C)

D)

15) The final step in the evaluation of the audit results is the decision to:

A) accept the population as fairly stated or to require further action

B) determine sampling error and calculate the estimated total population error

C) project the point estimate

D) determine the error in each sample

16) Which of the following components of the control environment define the existing

lines of responsibility and authority?

A) Organizational Structure

B) Management philosophy and operating style

C) Human resource policies and practices

D) Management integrity and ethical values

17) When performing analytical procedures for notes payable, if actual interest expense

is materially larger than the auditor’s expectation, one possible cause would be interest

payments on unrecorded notes payable.

A) True

B) False

18) Government auditing standards are included in the Yellow Book.

A) True

B) False

19) The employee in charge of authorizing credit to the company’s customers does not

fully understand the concept of credit risk. This lack of knowledge would constitute:

A) a deficiency in operation of internal controls

B) a deficiency in design of internal controls

C) a deficiency of management

D) not constitute a deficiency

20) Because the failure to record disposals of property, plant, and equipment can

significantly affect the financial statements, the search for unrecorded disposals is

essential. Which of the following is not a procedure used to verify disposals?

A) Make inquiries of management and production personnel about the possibility of the

disposal of assets

B) Review whether newly acquired assets replace existing assets

C) Test the valuation of fixed assets recorded in prior periods

D) Review plant modifications and changes in product line, taxes, or insurance

coverage

21) One common substantive test of payroll transactions for the existence objective is to

compare canceled payroll checks with personnel records.

A) True

B) False

22) Section 404 requires auditors to evaluate the effectiveness of the audit committee’s

oversight of the company’s:

A)

B)

C)

D)

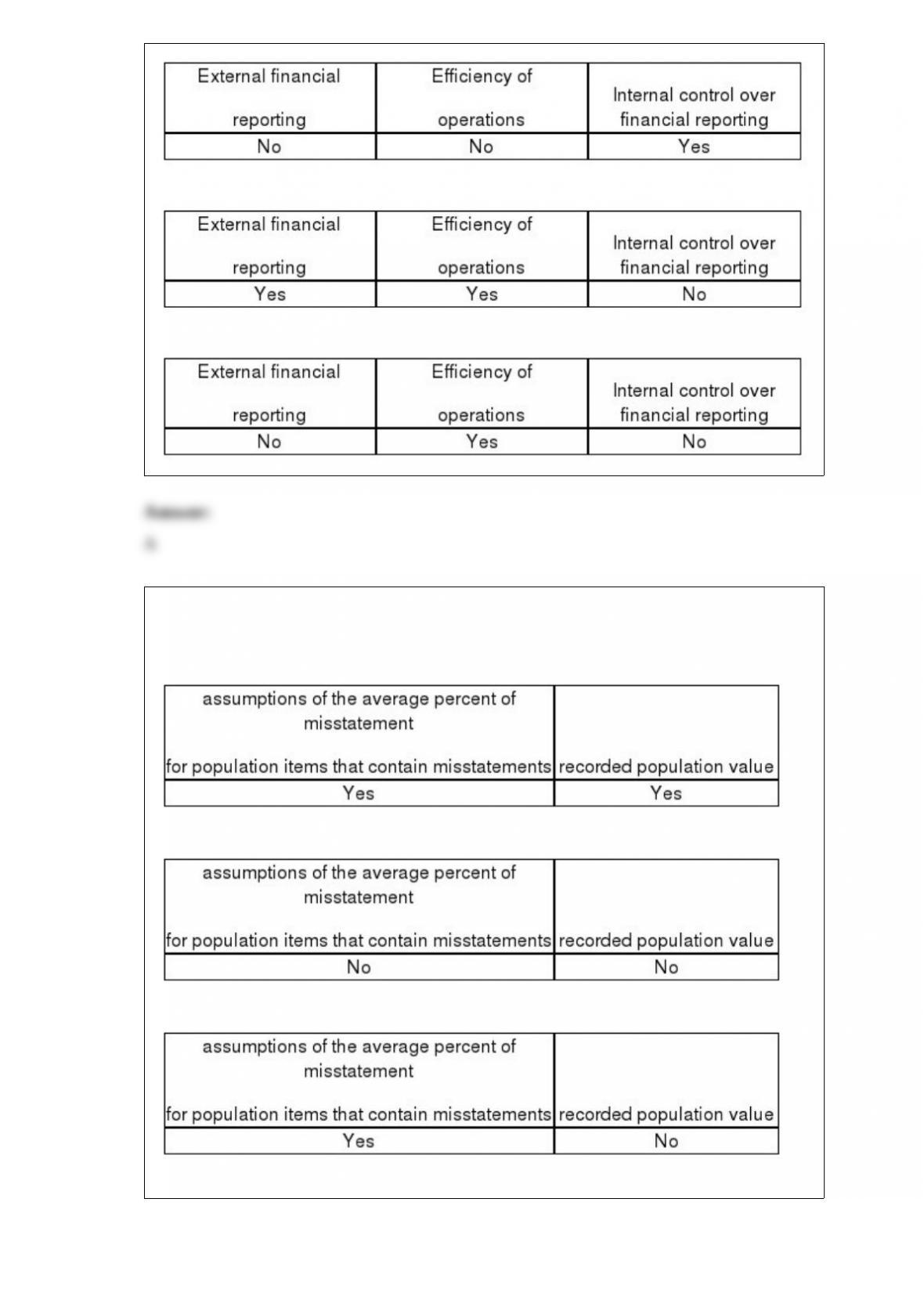

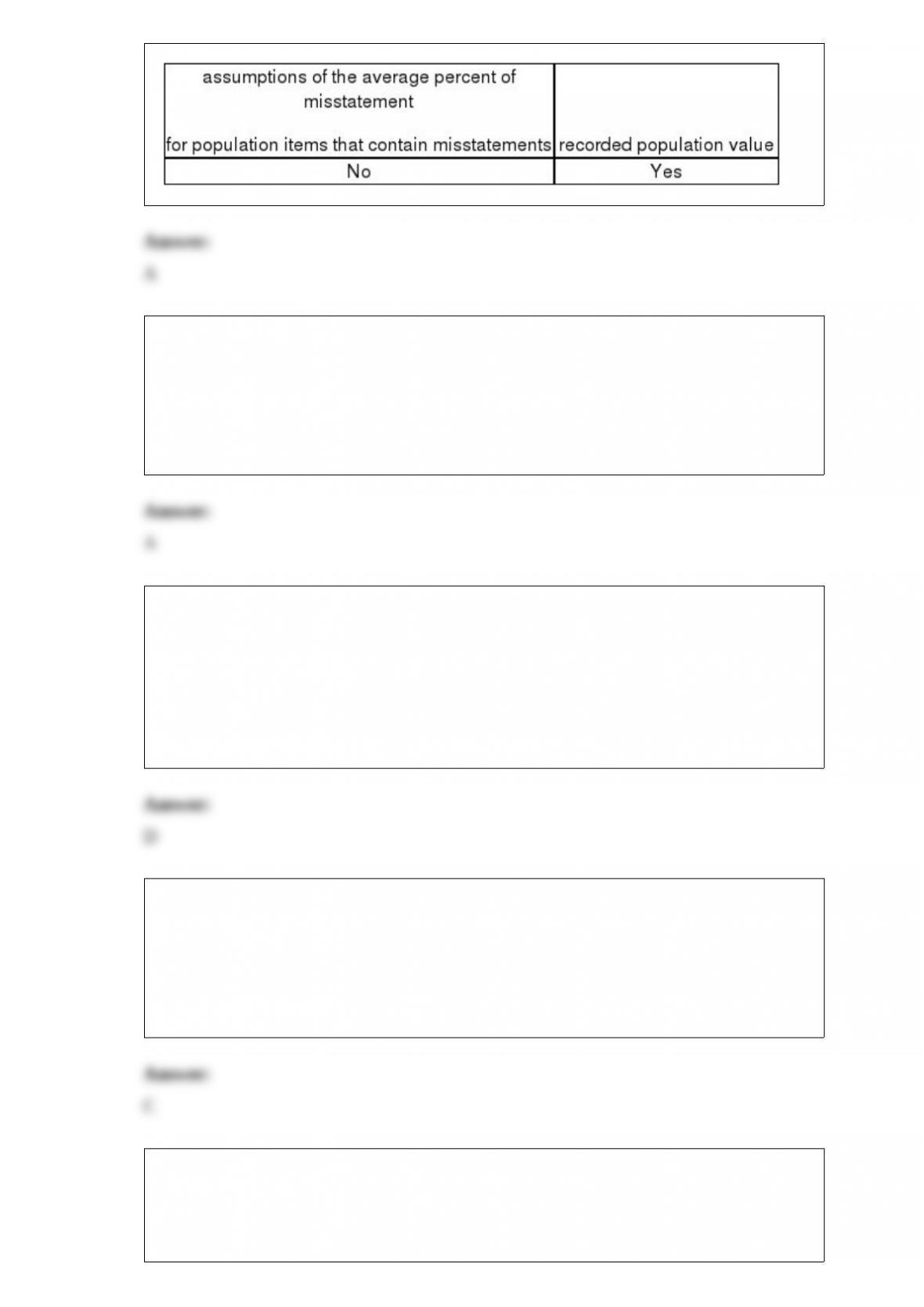

23) Calculating the sample size using monetary-unit-sampling depends on which of the

following factors?

A)

B)

C)

D)

24) Almost all companies need physical controls over their assets to prevent loss.

Which of the following is not an example of such a control?

A) perpetual inventory master files

B) segregated, limited-access storage areas

C) custody of assets assigned to specific responsible individuals

D) approved prenumbered documents for authorizing movement of inventory

25) Which of the following is not a procedure that can be performed on canceled

checks in an effort to detect defalcations?

A) Compare the endorsements on checks with authorized signatures

B) Scan endorsements for unusual or recurring second endorsements

C) Examine voided checks to be sure they haven’t been used

D) Examine the payroll records in subsequent periods to determine that terminated

employees are no longer being paid

26) Which of the following audit procedures would not likely detect a client’s decision

to pledge or factor accounts receivable?

A) A review of the minutes of the board of directors’ meetings

B) Discussions with the client

C) Confirmation of receivables

D) Examination of correspondence files

27) One disadvantage of functional auditing is the failure to evaluate interrelated

functions.

A) True

B) False

28) The primary source of authoritative literature for doing government audits is the:

A) Purple Book

B) Yellow Book

C) Green Book

D) Red Book

29) From which of the following evidence-gathering audit procedures would an auditor

obtain most assurance concerning the existence of inventories?

A) observation of physical inventory counts

B) written inventory representations from management

C) confirmation of inventories in a public warehouse

D) auditor’s recomputation of inventory extensions

30) Match the engagement described to the (A) type of audit and (B) auditor that would

perform the engagement. Each engagement will have an answer from List-A and

List-B. An answer can be used once, more than once, or not at all.

List A – Type of Audit: List B – Type of Auditor:

a. Financial Statement b. Compliance c. Operational d. Internal e. External f.

Government g. IRS

Engagement:

1> Evaluate a company’s payroll processing for economy.

2> Evaluate/determine if bank covenants are being met.

3> Evaluate financial statements that are to be submitted to a bank.

4> Evaluate the promptness of materials inspection in a manufacturer’s receiving

department.

5> Determine if Medicare reimbursements are in accordance with the Healthcare

Financing Administration (HCFA).

6> Determine if the tax return of a multinational corporation is in accordance with the

tax code.

7> Determine if a public school is properly applying their reimbursement for the

payment-in-kind program.

8> Determine the effectiveness of the department of defense starwars project.

31) Inherent risk and control risk are directly related.

A) True

B) False

32) The auditor’s objective during an observation of a client’s physical inventory count

is to:

A) discover whether a client has counted a particular inventory item or group of items

B) obtain direct knowledge that the inventory exists and has been properly counted

C) provide an appraisal of the quality of the merchandise on hand on the day of the

physical count

D) allow the auditor to supervise the conduct of the count so as to obtain assurance that

inventory quantities are reasonably accurate

33) Which of the following audit tests both have the effect of simultaneously verifying

balance sheet and income statement accounts?

A) Analytical procedures and substantive tests of transactions

B) Tests of controls and substantive tests of transactions

C) Tests of details of balances and substantive tests of transactions

D) Tests of controls and analytical procedures

34) In nonstatistical sampling, the calculated sampling error is the difference between

the tolerable exception rate and the sample exception rate.

A) True

B) False

35) Auditors often use analytical procedures in gathering audit evidence. For example,

an unexplained decrease in the amount of accounts receivable may indicate:

A) Sales were overstated

B) Inventory purchases were curtailed

C) Cost of Goods sold was overstated

D) Accounts Receivables were sold

36) Within the context of quality control, the primary purpose of continuing

professional education and training activities is to enable a CPA firm to provide its

personnel with:

A) technical training that assures proficiency as a valuation expert

B) professional education that is required in order to perform with due professional care

C) knowledge required to fulfill assigned responsibilities

D) knowledge required to perform a peer review

37) Adequate separation of duties is an important control activity. Discuss the four

general guidelines for separation of duties to prevent both intentional and unintentional

misstatements that are of significance to auditors.

38) Explain the decision rule used with difference estimation sampling to determine

whether the population is acceptable.

39) There are four major sources of an auditor’s legal liability. One source is liability to

the audit client. List the other three sources.

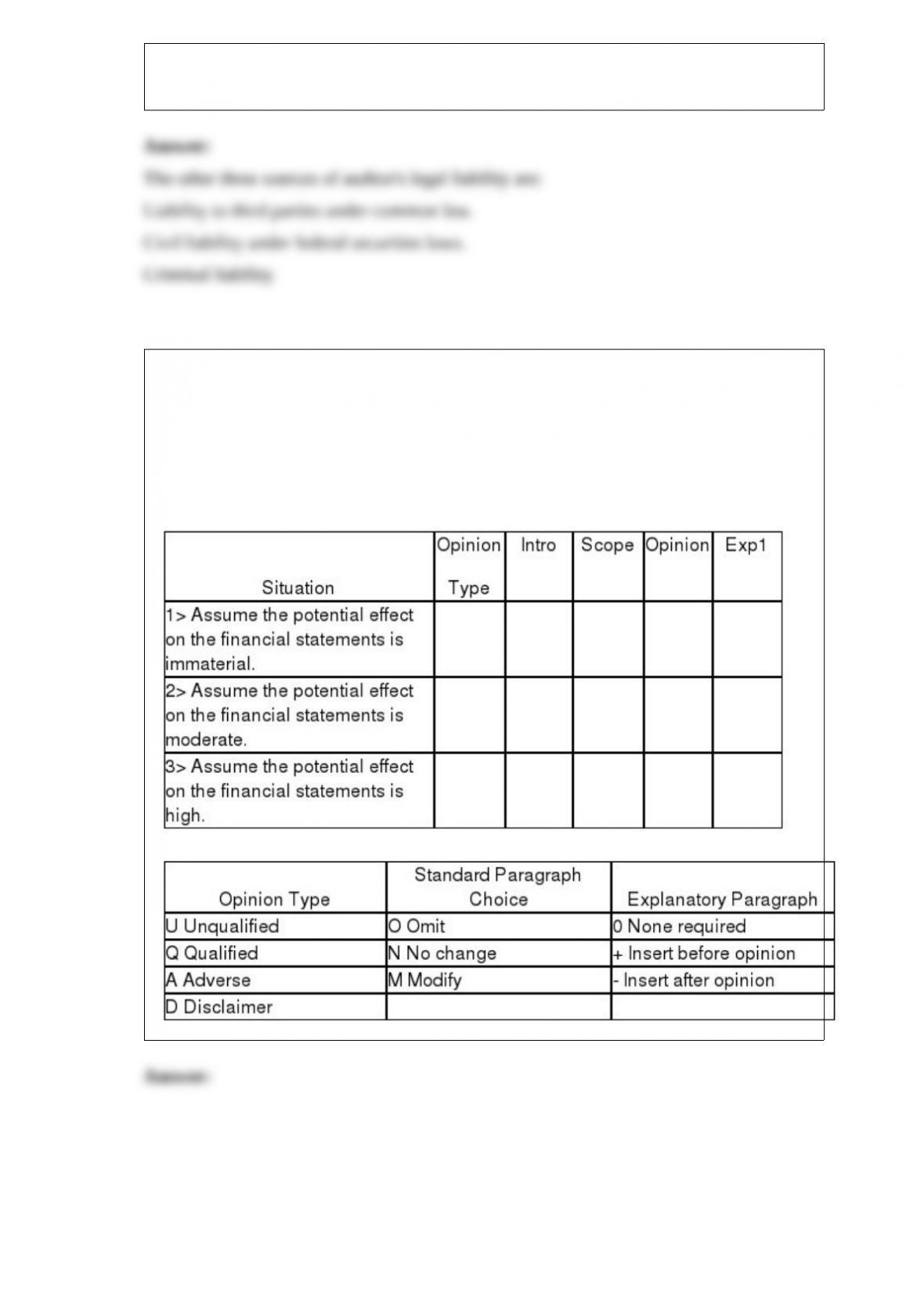

40) In auditing the long-term investments account, Arens, CPA, is unable to obtain

audited financial statements for an investee located in a foreign country. Levine

concludes sufficient appropriate audit evidence regarding this investment cannot be

obtained.

For each of the following situations below, identify the appropriate opinion type and

report modification by selecting a choice from the appropriate tables below.

41) Discuss the key internal controls that should be present in the “recognizing the

liability” function in the acquisitions and payment cycle.

42) Define the term contingent liability and discuss the criteria accountants and auditors

use to classify these accounting events.

43) What key separation of duties should the auditor expect to find within the payroll

and personnel cycle?

44) What are several analytical procedures used in the audit of prepaid insurance and

insurance expense?