Direct material costs are generally variable costs.

Answer:

If the actual rate per direct labor-hour exceeds the standard rate per direct labor-hour,

then the journal entry to record the Direct Labor Rate Variance would be a credit.

Answer:

As the inventory turnover increases, the number of days required to sell the inventory

one time also increases.

Answer:

A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The company’s

choice of the denominator level of activity affects the Variable component of the

predetermined overhead rate.

Answer:

Flexible budgets cannot be used when there is more than one cost driver (i.e., measure

of activity).

Answer:

On a CVP graph for a profitable company, the total revenue line will be steeper than the

total expense line.

Answer:

When a company shifts from a traditional cost system in which manufacturing overhead

is applied based on direct labor-hours to an activity-based costing system in which there

are batch-level and product-level costs, the unit product costs of high volume products

typically decrease whereas the unit product costs of low volume products typically

increase.

Answer:

If the actual quantity of materials used is less than the standard quantity of materials

allowed for the actual output, then the journal entry to record the Direct Materials

Quantity Variance would be a credit.

Answer:

Contribution margin and segment margin mean the same thing.

Answer:

When the level of activity increases, total variable cost will increase.

Answer:

The total volume in sales dollars that would be required to attain a given target profit is

determined by dividing the sum of the fixed expenses and the target profit by the

contribution margin ratio.

Answer:

Sunk costs are considered to be avoidable costs.

Answer:

In a standard costing system, underapplied or overapplied fixed manufacturing

overhead is equal to the sum of the fixed manufacturing overhead budget variance and

the fixed manufacturing overhead volume variance.

Answer:

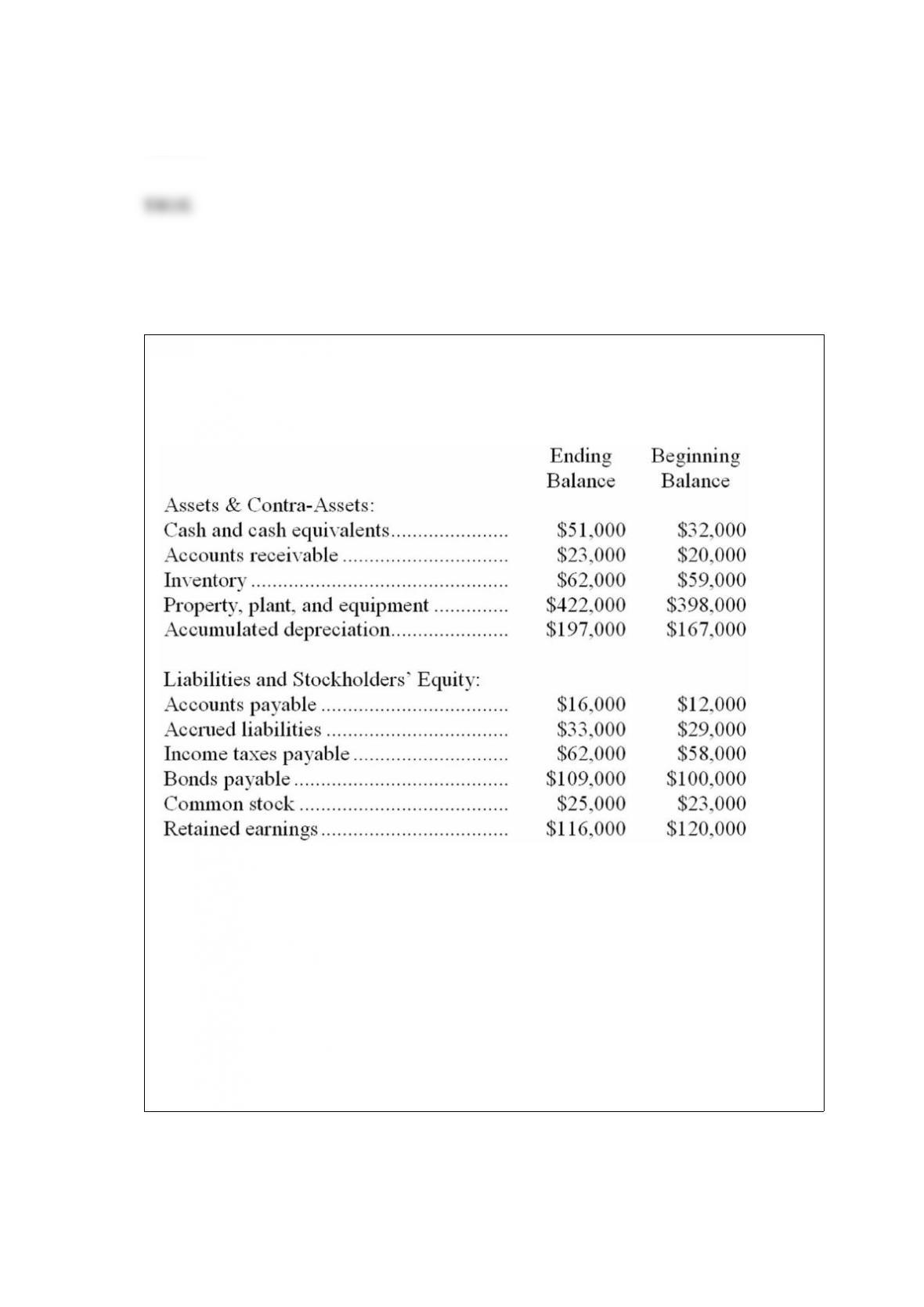

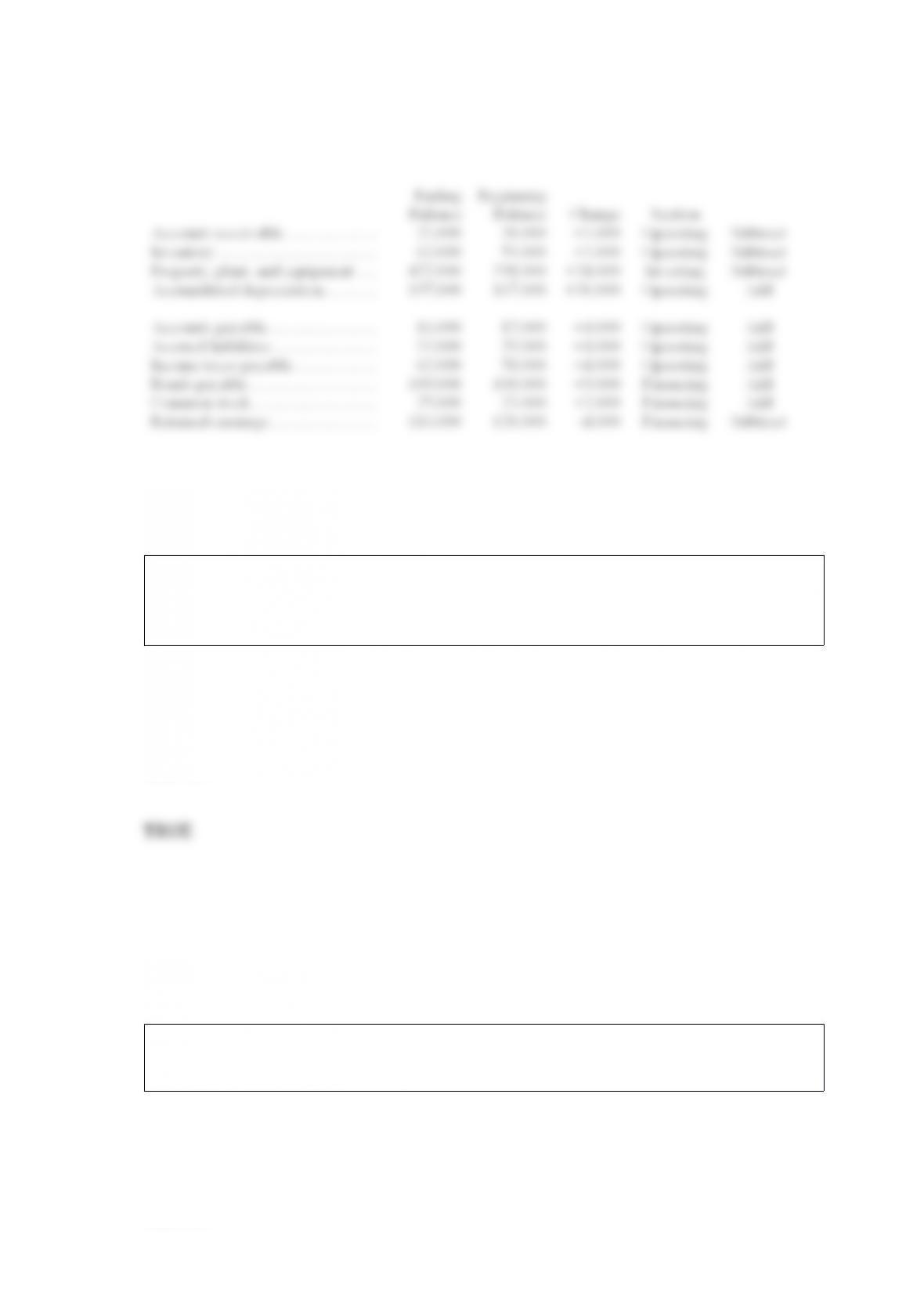

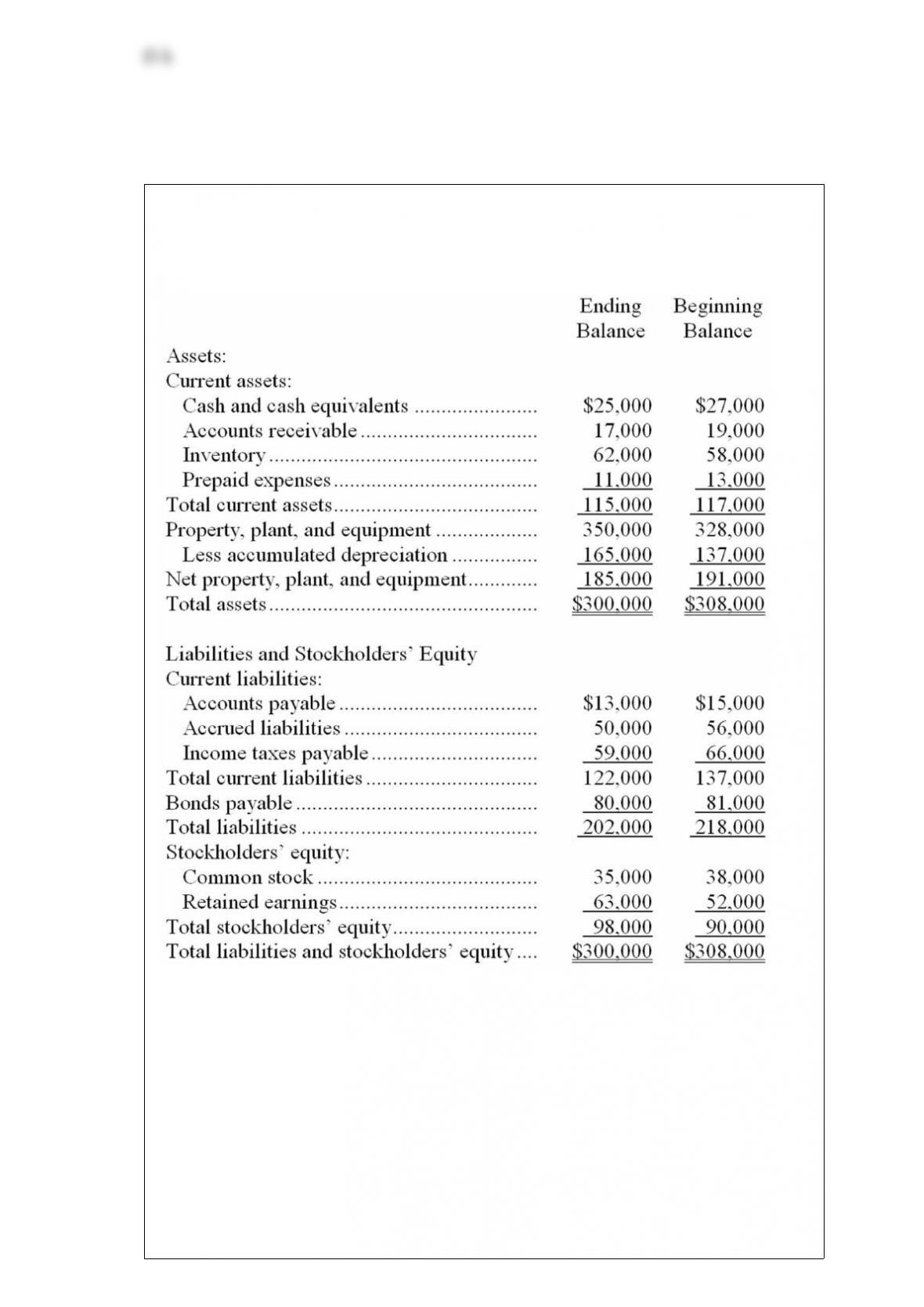

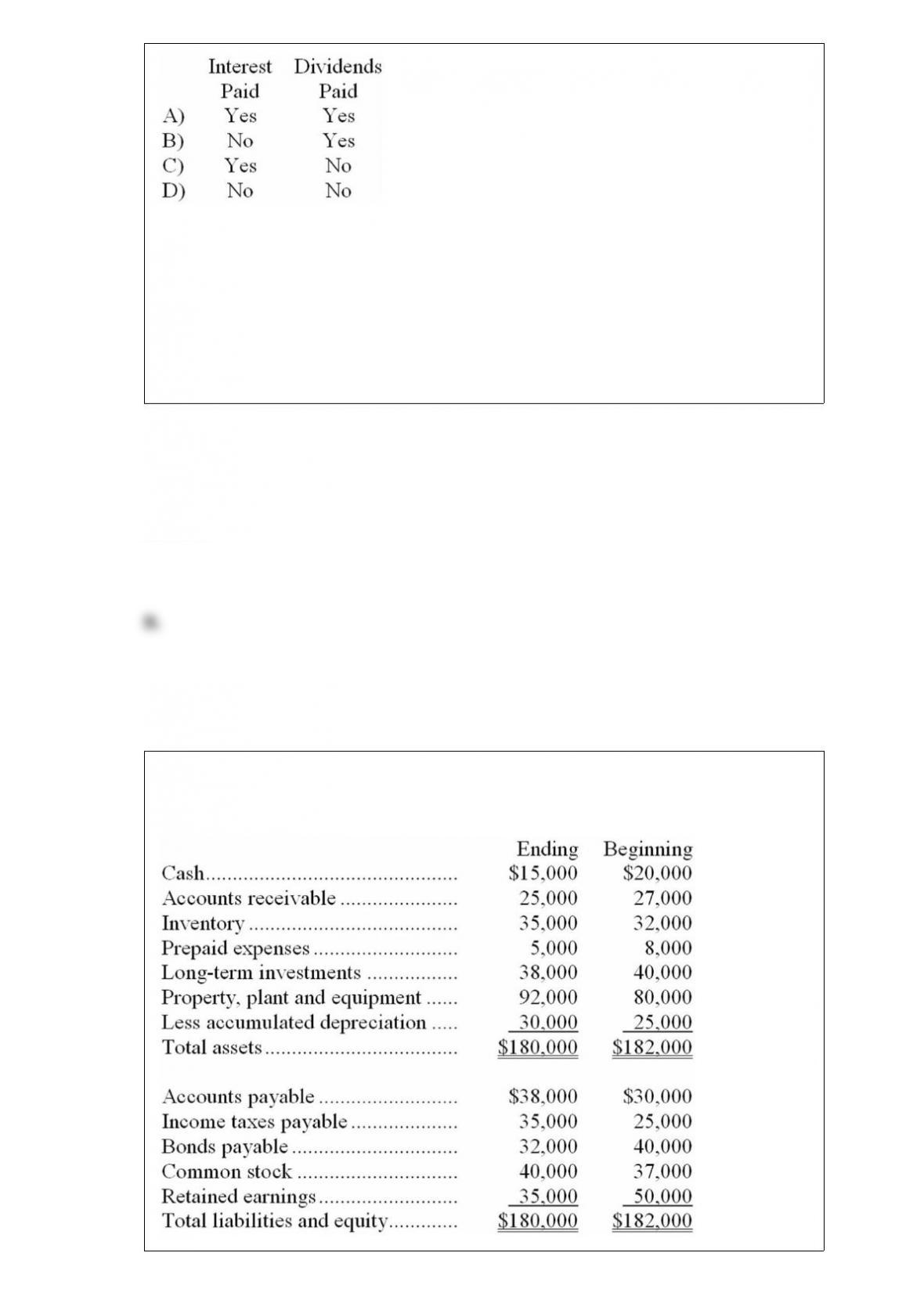

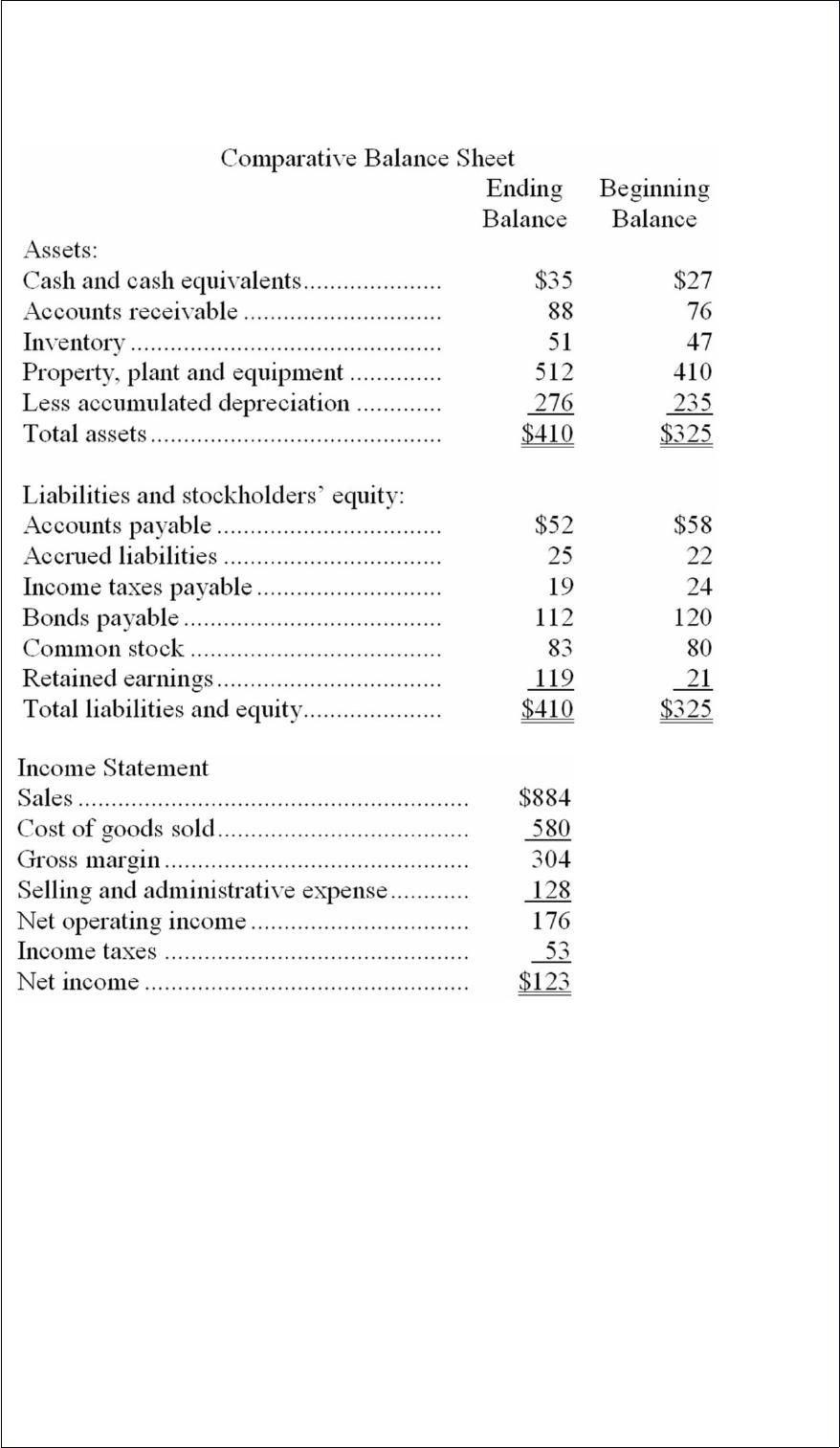

The ending and beginning balances of Parma Corporation’s balance sheet accounts for

the most recent year are listed below:

The company’s net income (loss) for the year was $0 and its cash dividends were

$4,000. It did not dispose of any property, plant, and equipment, retire any bonds

payable, or repurchase any of its own common stock during the year.

Compute the change in each noncash balance sheet account. Indicate whether the

change in each balance will be recorded in the operating, investing, or financing

activities section of the statement of cash flows. For items recorded in the operating

activities section, also indicate whether the change will be added to or subtracted from

net income. For all other items, indicate whether the change will be added as a cash

inflow or subtracted as a cash outflow.

Answer:

Under the direct method of determining the net cash provided by operating activities on

the statement of cash flows, an increase in income taxes payable would be subtracted

from income tax expense to convert income tax expense to a cash basis.

Answer:

Only those costs that would disappear over time if a segment were eliminated should be

considered traceable costs of the segment.

Answer:

The acid-test ratio is always smaller than the current ratio.

Answer:

When a company issues common stock in exchange for cash, the cash inflow is

recorded in the investing activities section of the statement of cash flows.

Answer:

In activity-based costing, there are a number of activity cost pools, each of which is

allocated to products using its own unique measure of activity.

Answer:

The weighted-average method and the FIFO method of process costing use the same

manufacturing accounts.

Answer:

Both variable and fixed manufacturing overhead costs are included in the

manufacturing overhead budget.

Answer:

Under the weighted-average method, the cost of materials in the beginning work in

process inventory is not used in the computation of the cost per equivalent unit for

materials.

Answer:

The fixed manufacturing overhead volume variance will be unfavorable if production

volume is less than sales volume.

Answer:

Free cash flow increases when a company issues common stock for cash.

Answer:

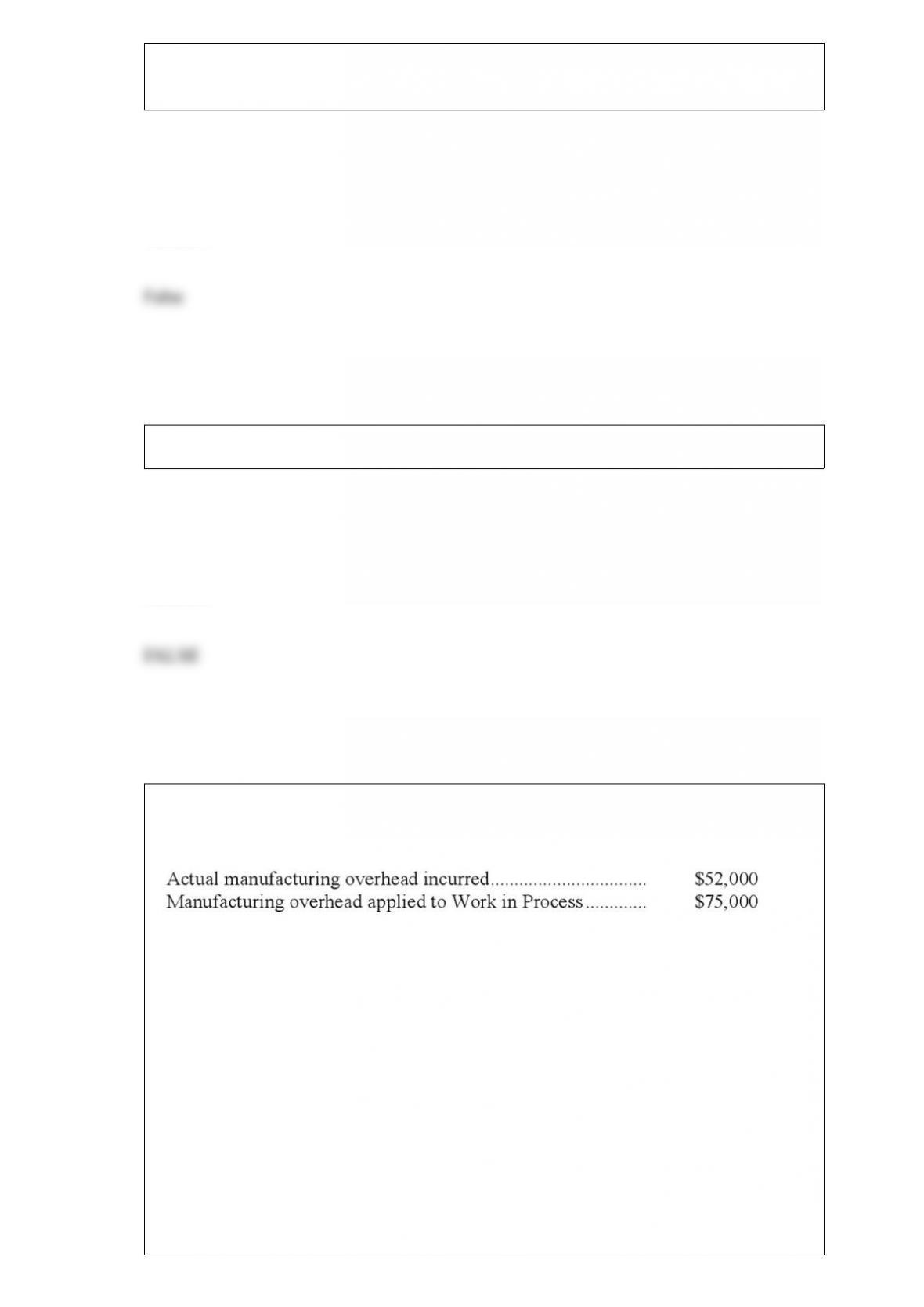

Lietz Corporation has provided the following data concerning manufacturing overhead

for January:

The company’s Cost of Goods Sold was $369,000 prior to closing out its Manufacturing

Overhead account. The company closes out its Manufacturing Overhead account to

Cost of Goods Sold. Which of the following statements is TRUE?

A. Manufacturing overhead was underapplied by $23,000; Cost of Goods Sold after

closing out the Manufacturing Overhead account is $392,000

B. Manufacturing overhead was underapplied by $23,000; Cost of Goods Sold after

closing out the Manufacturing Overhead account is $346,000

C. Manufacturing overhead was overapplied by $23,000; Cost of Goods Sold after

closing out the Manufacturing Overhead account is $346,000

D. Manufacturing overhead was overapplied by $23,000; Cost of Goods Sold after

closing out the Manufacturing Overhead account is $392,000

Answer:

For contra-asset accounts, debits are added to the beginning balance on the statement of

cash flows.

Answer:

A company has a standard cost system in which fixed and variable manufacturing

overhead costs are applied to products on the basis of direct labor-hours. The companys

choice of the denominator level of activity affects the Fixed component of the

predetermined overhead rate.

Answer:

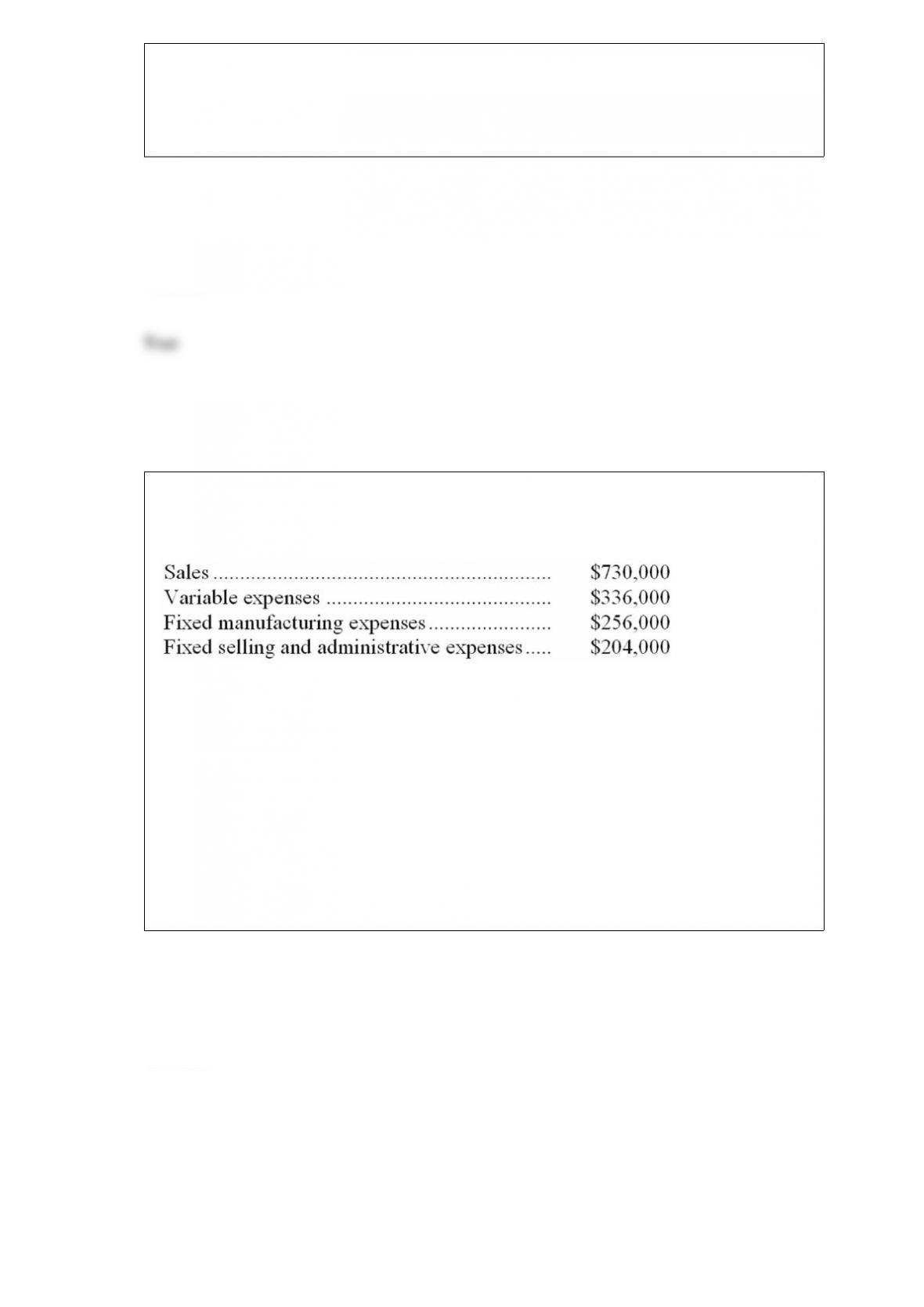

Nutall Corporation is considering dropping product N28X. Data from the company’s

accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company’s

accounting system. Further investigation has revealed that $199,000 of the fixed

manufacturing expenses and $114,000 of the fixed selling and administrative expenses

are avoidable if product N28X is discontinued.

a. According to the company’s accounting system, what is the net operating income

earned by product N28X? Show your work!

b. What would be the effect on the company’s overall net operating income of dropping

product N28X? Should the product be dropped? Show your work!

Answer:

Top management salaries should not go into the Manufacturing Overhead account.

Answer:

The first-stage allocation in activity-based costing is the process by which overhead

costs are assigned to activity cost pools.

Answer:

If manufacturing overhead applied exceeds the actual manufacturing overhead costs of

the period, then manufacturing overhead is overapplied.

Answer:

Sharp Company’s records show that overhead was overapplied by $10,000 last year.

This overapplied manufacturing overhead was closed out to the Cost of Goods Sold

account at the end of the year. In trying to determine why overhead was overapplied by

such a large amount, the company has discovered that $6,000 of depreciation on factory

equipment was charged to administrative expense in error. Given the above

information, which of the following statements is TRUE?

A. Manufacturing overhead was actually overapplied by $16,000 for the year.

B. The company’s net income is understated by $6,000 for the year.

C. Under the circumstances posed above, the error in recording depreciation would

have no effect on net operating income for the year.

D. The $6,000 in depreciation should have been charged to Work in Process rather than

to administrative expense.

Answer:

The cost of a resource that has no alternative use in a make or buy decision problem has

an opportunity cost of zero.

Answer:

Selling and administrative expenses are product costs under generally accepted

accounting principles.

Answer:

Reference: 8-25

Lotson Corporation bases its budgets on machine-hours. The companys static planning

budget for May appears below:

Actual results for the month were:

The spending variance for power costs for the month should be:

A) $1,550 F

B) $4,160 F

C) $1,550 U

D) $4,160 U

Answer:

The most recent comparative balance sheet of Broekemeier Corporation appears below:

The company uses the indirect method to construct the operating activities section of its

statements of cash flows.

Which of the following is correct regarding the operating activities section of the

statement of cash flows?

A. The change in Accounts Payable will be added to net income; The change in

Accrued Liabilities will be subtracted from net income

B. The change in Accounts Payable will be subtracted from net income; The change in

Accrued Liabilities will be added to net income

C. The change in Accounts Payable will be subtracted from net income; The change in

Accrued Liabilities will be subtracted from net income

D. The change in Accounts Payable will be added to net income; The change in

Accrued Liabilities will be added to net income

Answer:

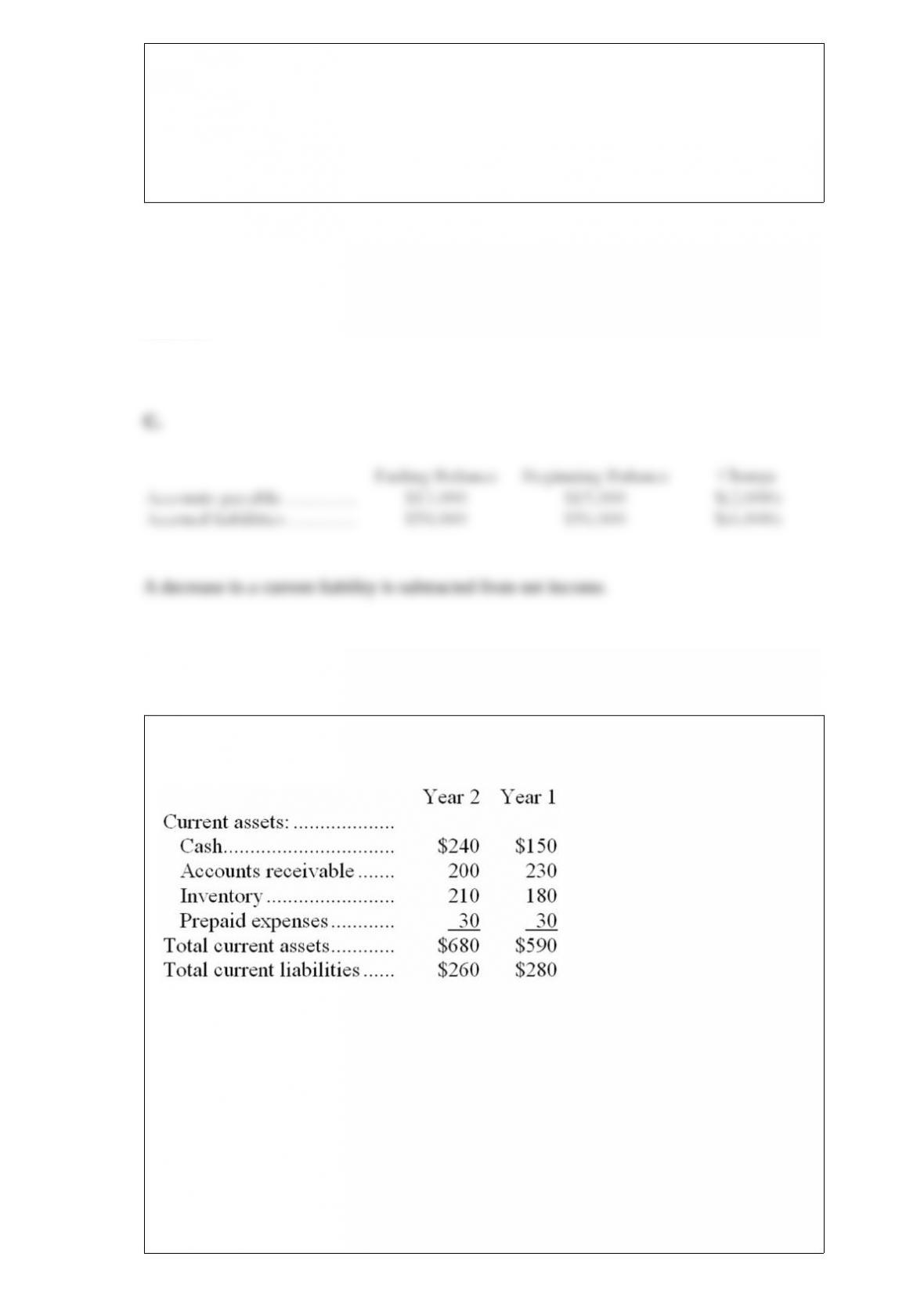

Excerpts from Zorra Corporation’s most recent balance sheet appear below:

Sales on account in Year 2 amounted to $1,370 and the cost of goods sold was $850.

The average collection period for Year 2 is closest to:

A. 57.3 days

B. 53.3 days

C. 0.9 days

D. 1.2 days

Answer:

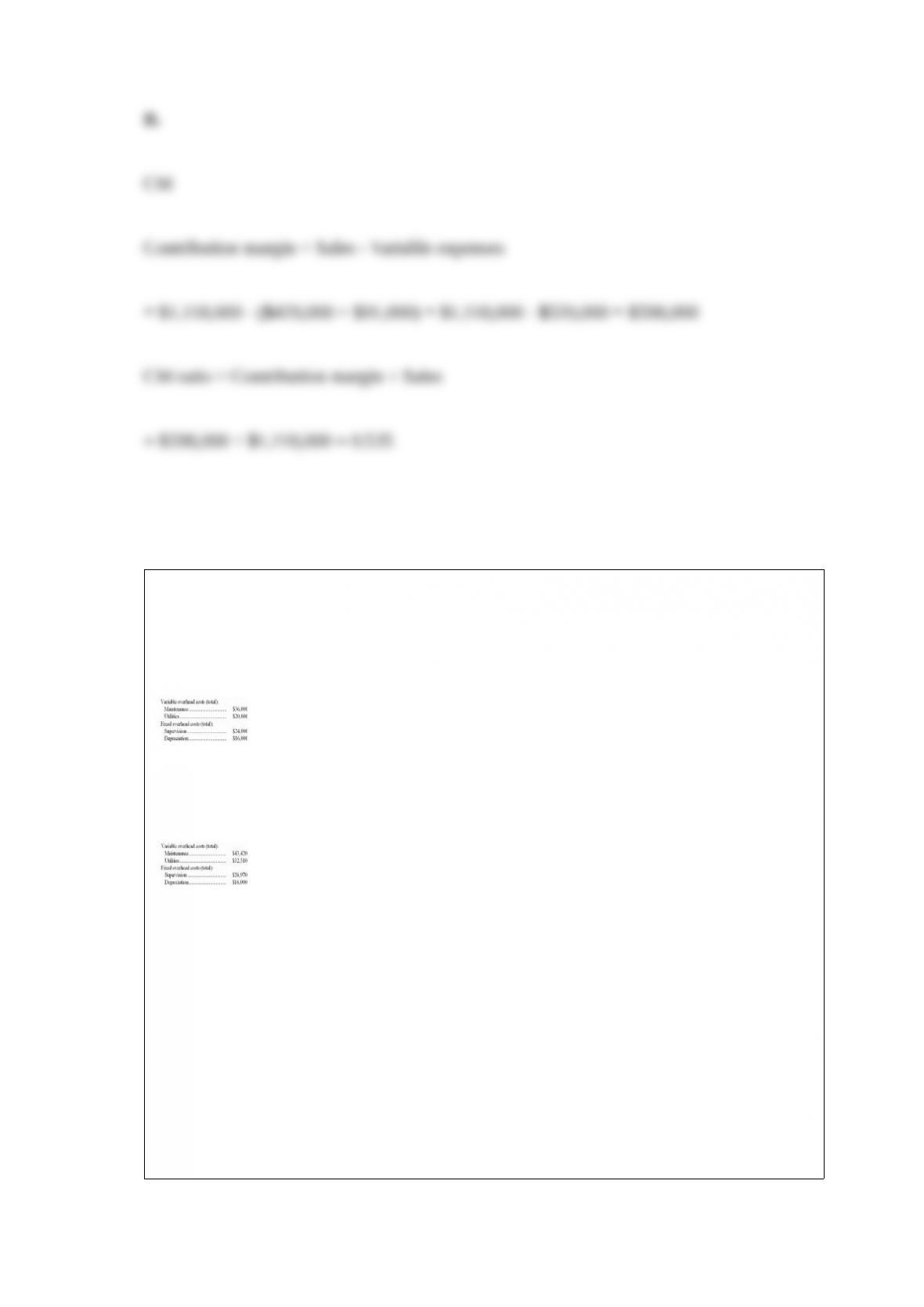

A cement manufacturer has supplied the following data:

The company’s contribution margin ratio is closest to:

A. 46.5%

B. 53.5%

C. 7.4%

D. 42.8%

Answer:

The Chase Company uses a standard cost system in which manufacturing overhead

costs are applied to products on the basis of standard machine-hours. For November, the

company’s flexible budget for manufacturing overhead showed the following total

budgeted costs at the denominator activity level of 40,000 machine-hours:

During November 42,000 machine-hours were used to complete 13,200 units of product

with the following actual overhead costs:

The standard time allowed to complete one unit of product is 3.6 machine-hours.

The variable overhead rate variance for maintenance cost for November was:

A. $7,420 unfavorable

B. $2,400 favorable

C. $9,820 unfavorable

D. $5,620 unfavorable

Answer:

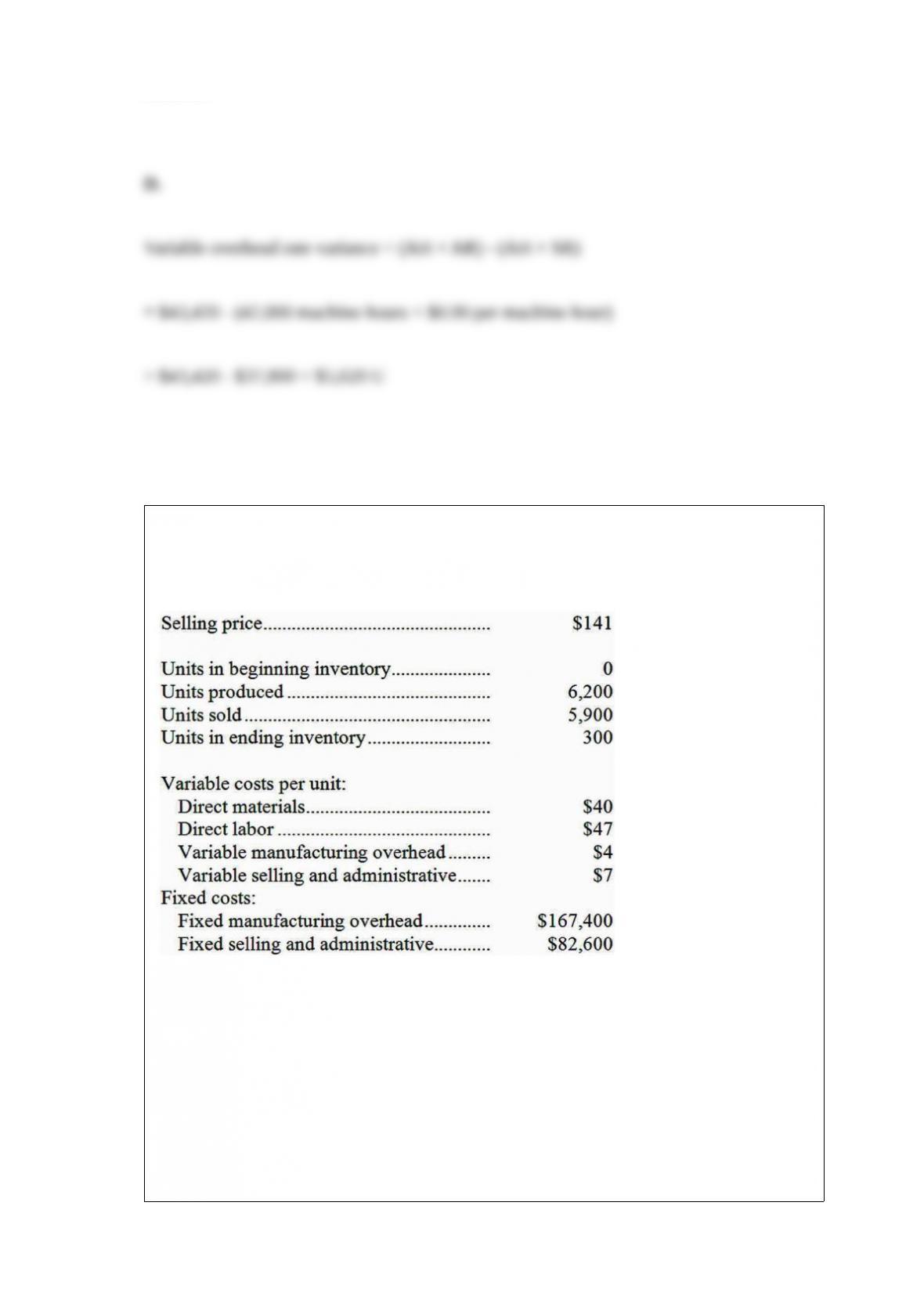

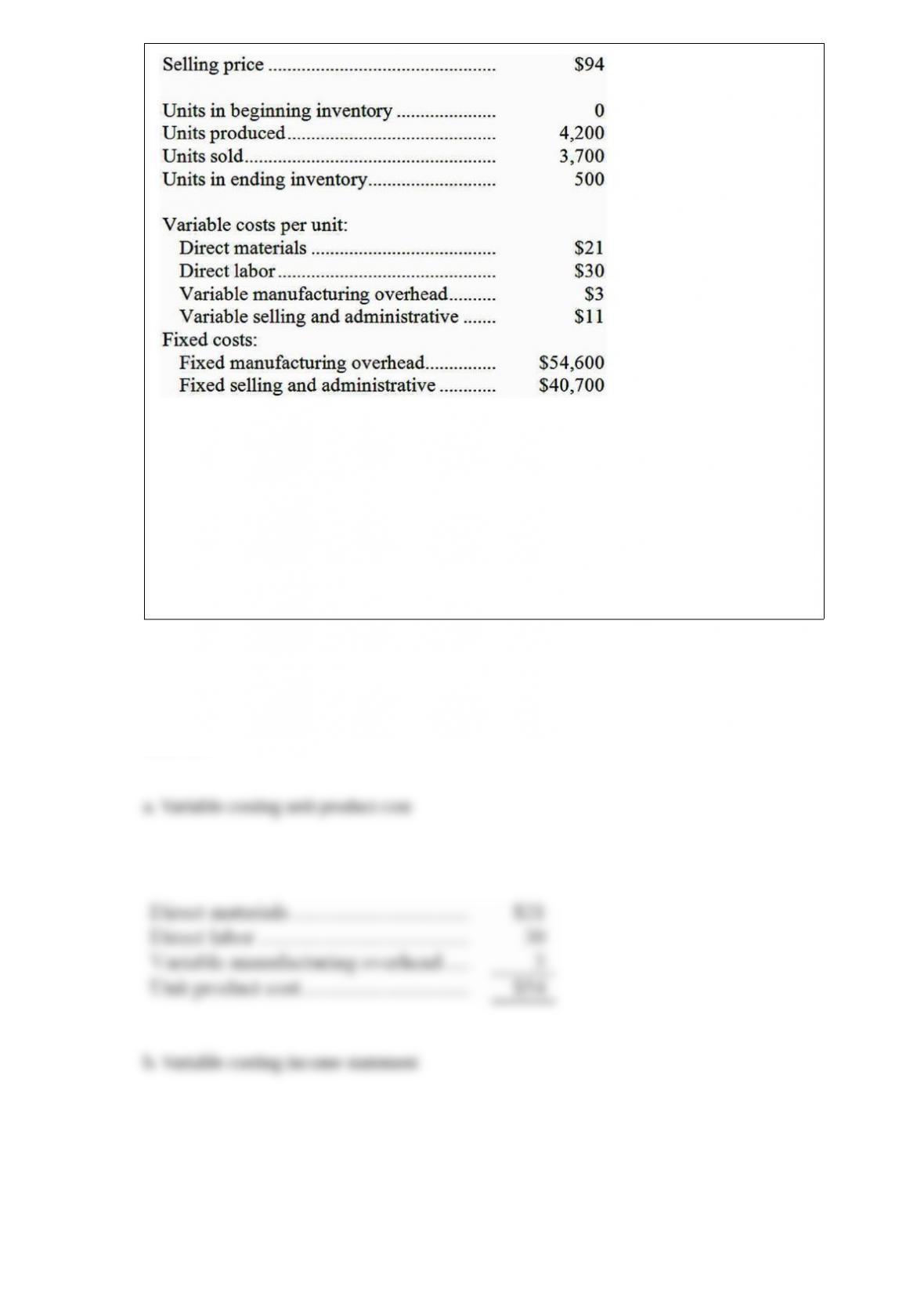

Favini Company, which has only one product, has provided the following data

concerning its most recent month of operations:

What is the unit product cost for the month under variable costing?

A. $98

B. $125

C. $118

D. $91

Answer:

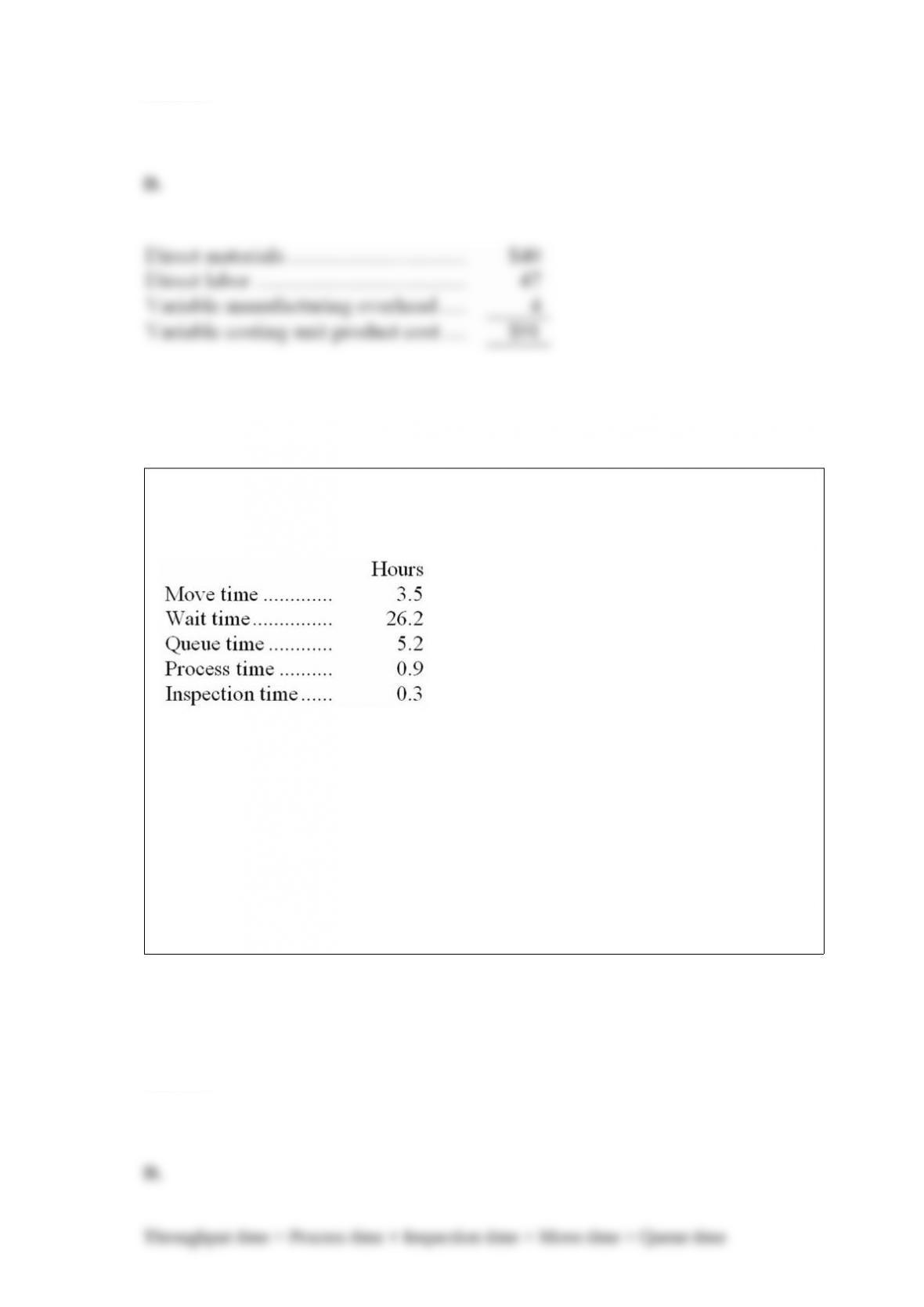

Garnick Corporation keeps careful track of the time required to fill orders. The times

recorded for a particular order appear below:

The delivery cycle time was:

A. 3.5 hours

B. 8.7 hours

C. 34.9 hours

D. 36.1 hours

Answer:

Dolittle Company purchased materials on account. The entry to record the purchase of

materials having a standard cost of $0.50 per pound from a supplier at $0.60 per pound

would include a:

A. credit to Raw Materials Inventory.

B. debit to Work in Process.

C. credit to Materials Price Variance.

D. debit to Materials Price Variance.

Answer:

Which of the following should be classified as a financing activity on a statement of

cash flows?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

Alkine Company’s comparative balance sheet appears below:

Alkine reported the following net income for the year:

Dividends were declared and paid during the year. A gain of $8,000 was recorded on the

sale of the long-term investments. The company did not purchase any long-term

investments or dispose of any property, plant, and equipment during the year. It also did

not issue any bonds payable or repurchase any of its own common stock.

Under the direct method, the cost of goods sold adjusted to a cash basis would be:

A. $152,000

B. $160,000

C. $163,000

D. $155,000

Answer:

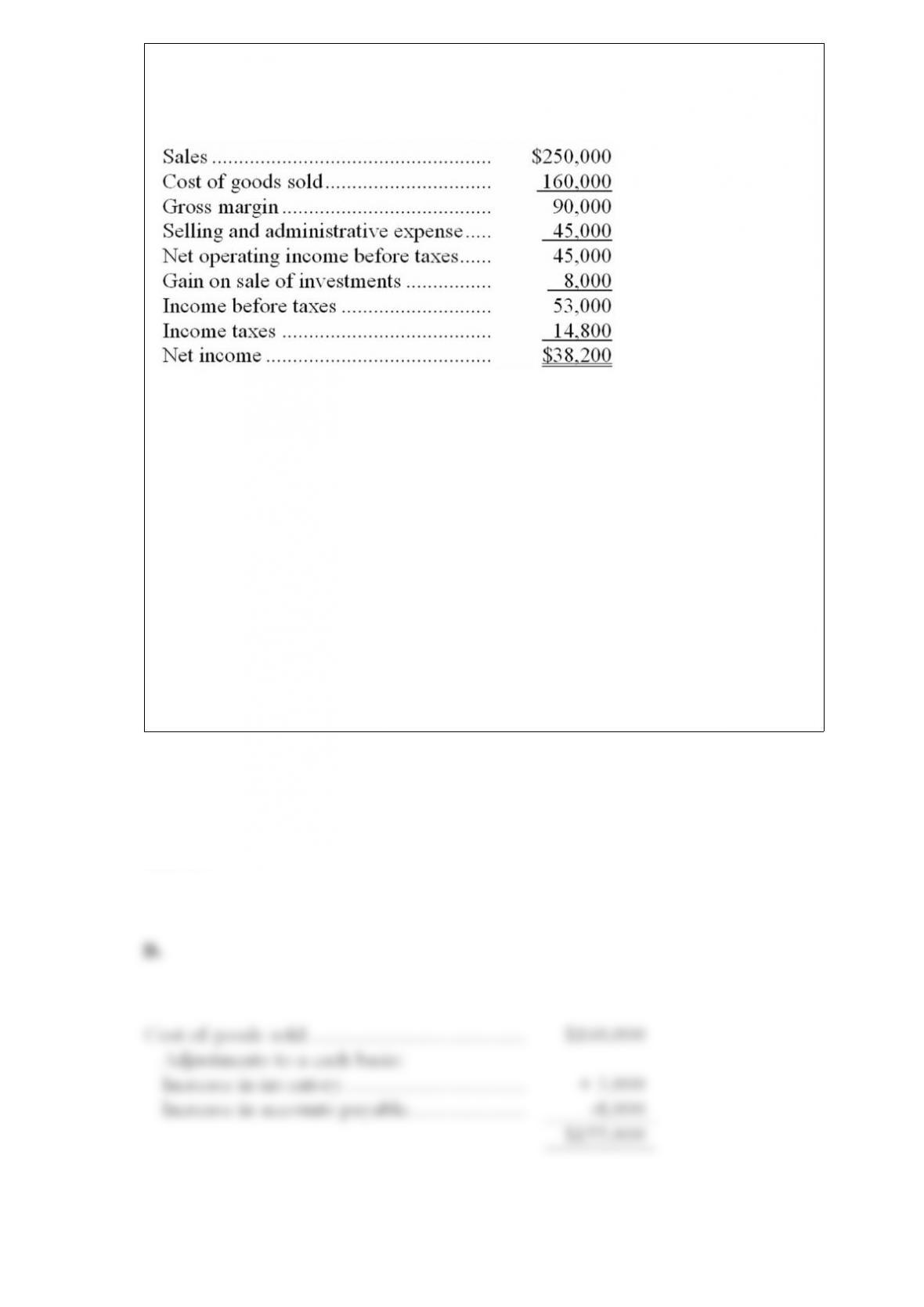

The Gasson Company sells three products, Product A, Product B and Product C, and

had sales of $1,000,000 during the month of June. The company’s overall contribution

margin ratio was 37% and fixed expenses totaled $350,000. Sales were: Product A,

$500,000; Product B, $300,000; and Product C, $200,000. Traceable fixed costs were:

Product A, $120,000; Product B, $100,000; and Product C, $60,000. The variable

expenses of Product A were $300,000 and the variable expenses of Product B were

$180,000.

The net operating income for the company as a whole for June was:

A. $20,000

B. $90,000

C. $170,000

D. $300,000

Answer:

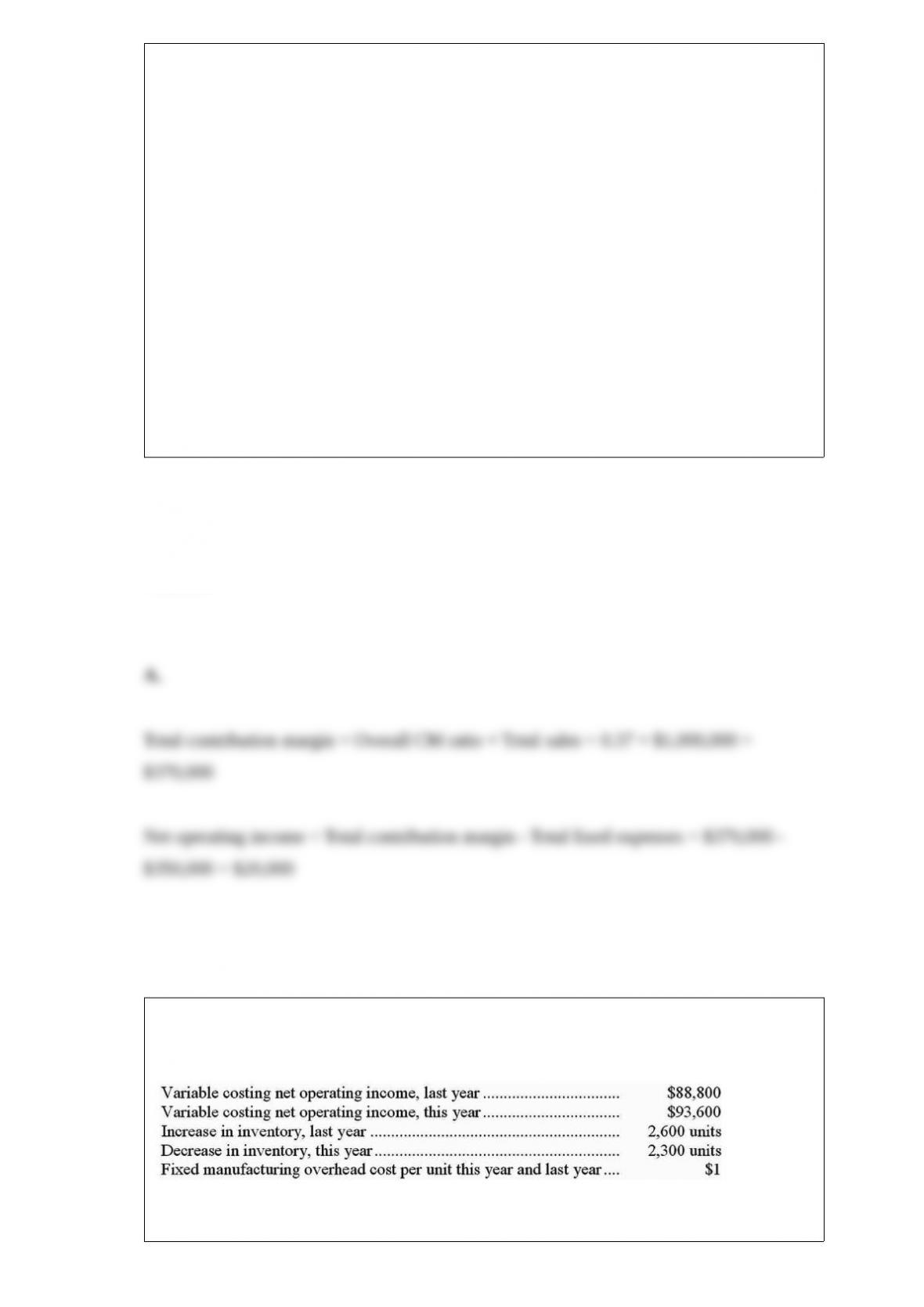

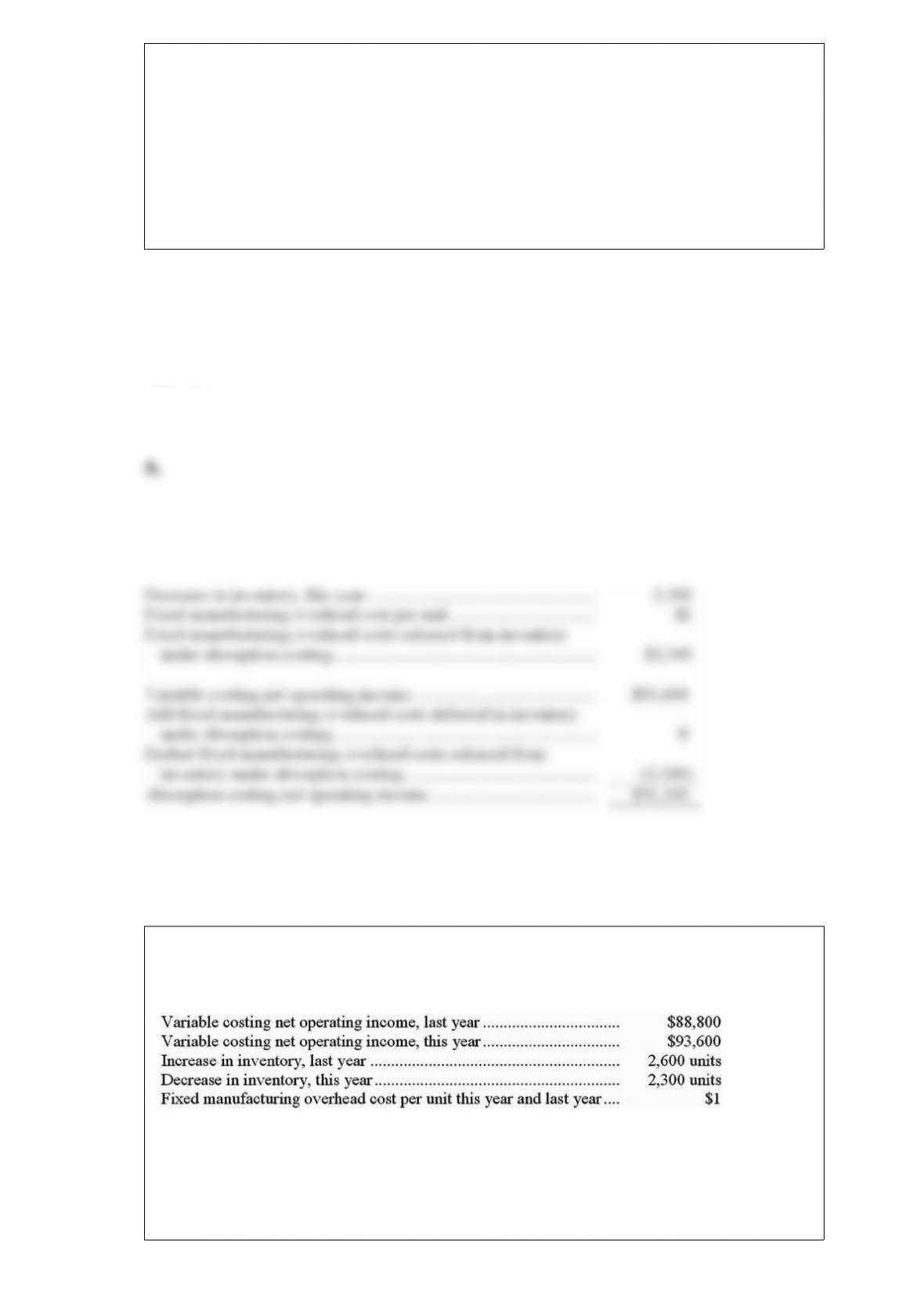

Krug Corporation manufactures a variety of products. The following data pertain to the

company’s operations over the last two years:

What was the absorption costing net operating income this year?

A. $91,300

B. $93,300

C. $95,900

D. $88,500

Answer:

Krug Corporation manufactures a variety of products. The following data pertain to the

company’s operations over the last two years:

What was the absorption costing net operating income last year?

A. $86,200

B. $89,100

C. $88,800

D. $91,400

Answer:

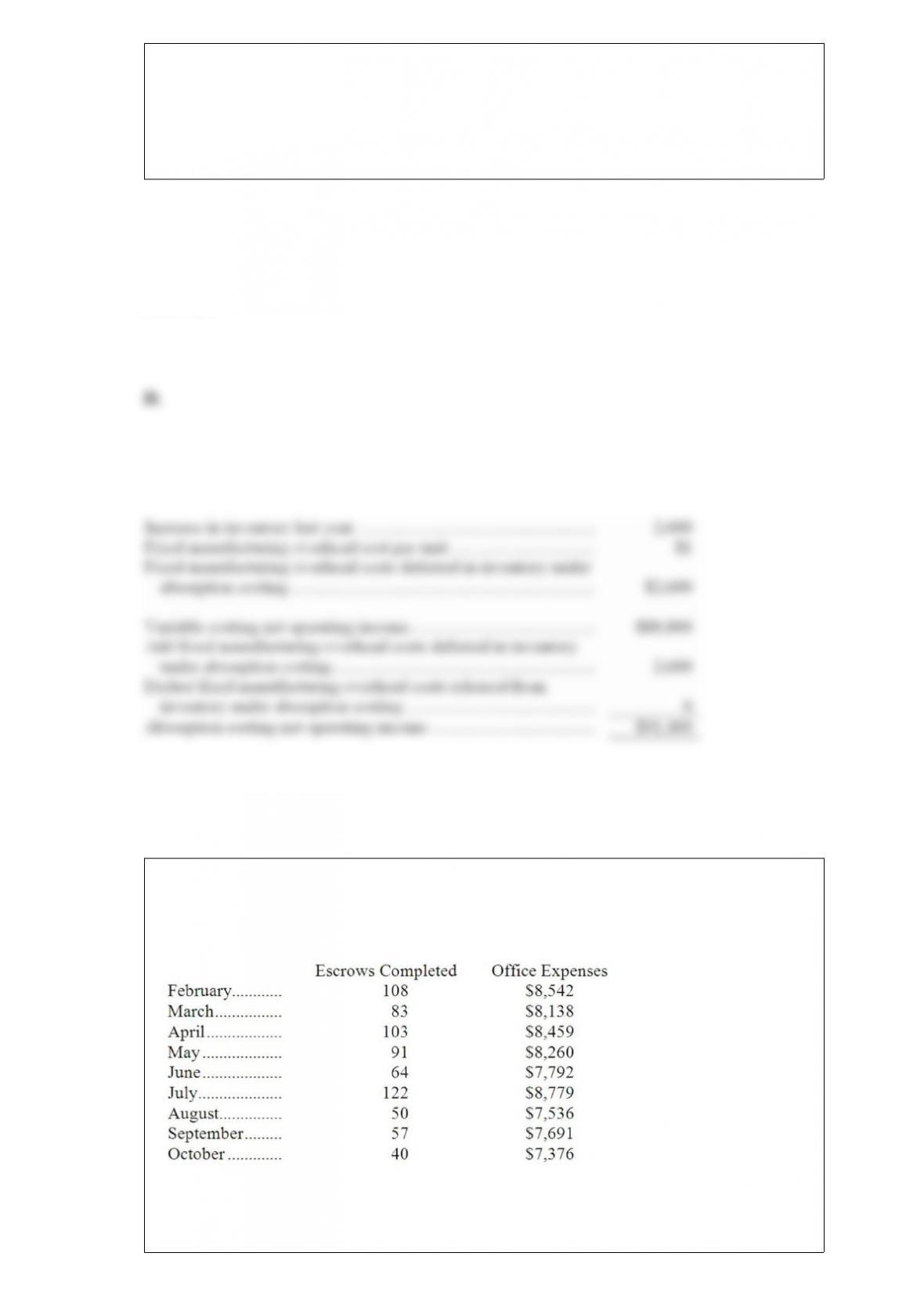

Glatt Inc., an escrow agent, has provided the following data concerning its office

expenses:

Management believes that office expense is a mixed cost that depends on the number of

escrows completed. Note: Real estate purchases usually involve the services of an

escrow agent that holds funds and prepares documents to complete the transaction.

Using the high-low method, the estimate of the fixed component of office expense per

month is closest to:

A. $6,692

B. $8,064

C. $7,376

D. $7,720

Answer:

The most recent balance sheet and income statement of Heldt Corporation appear

below:

The company paid a cash dividend and it did not dispose of any property, plant, and

equipment. The company did not purchase any bonds payable or repurchase any of its

own common stock. The following question pertain to the company’s statement of cash

flows.

The net cash provided by (used in) investing activities for the year was:

A. $102

B. $61

C. $(102)

D. $(61)

Answer:

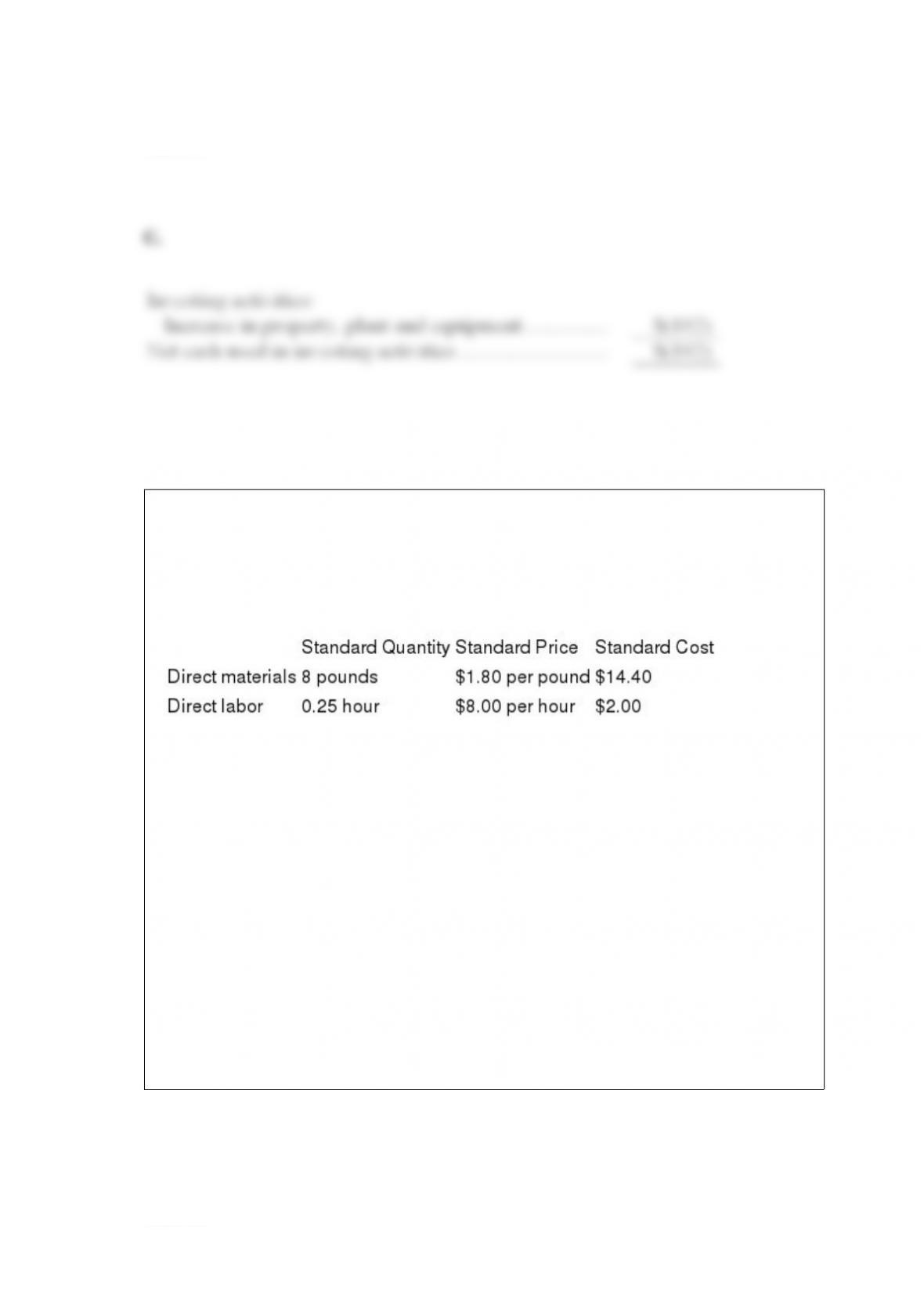

Reference: 8-37

Arrow Industries uses a standard cost system in which direct materials inventory is

carried at standard cost. Arrow has established the following standards for the prime

costs of one unit of product.

During May, Arrow purchased 160,000 pounds of direct material at a total cost of

$304,000. The total direct labor wages for May were $37,800. Arrow manufactured

19,000 units of product during May using 142,500 pounds of direct material and 5,000

direct labor-hours.

The direct materials price variance for May is:

A) $16,000 favorable

B) $16,000 unfavorable

C) $14,250 favorable

D) $14,250 unfavorable

Answer:

Vanstee Corporation manufactures a variety of products. Variable costing net operating

income last year was $60,000 and this year was $67,000. Last year, $37,000 in fixed

manufacturing overhead costs were deferred in inventory under absorption costing. This

year, $8,000 in fixed manufacturing overhead costs were released from inventory under

absorption costing.

What was the absorption costing net operating income last year?

A. $60,000

B. $23,000

C. $97,000

D. $89,000

Answer:

Sohr Corporation processes sugar beets that it purchases from farmers. Sugar beets are

processed in batches. A batch of sugar beets costs $50 to buy from farmers and $15 to

crush in the company’s plant. Two intermediate products, beet fiber and beet juice,

emerge from the crushing process. The beet fiber can be sold as is for $20 or processed

further for $19 to make the end product industrial fiber that is sold for $58. The beet

juice can be sold as is for $41 or processed further for $23 to make the end product

refined sugar that is sold for $58.

How much profit (loss) does the company make by processing the intermediate product

beet juice into refined sugar rather than selling it as is?

A. $(71)

B. $(6)

C. $(39)

D. $(21)

Answer:

The Phelps Company applies overhead costs to products on the basis of standard direct

labor-hours. The standard cost card shows that 5 direct labor-hours are required per unit

of product. Phelps Company had the following budgeted and actual data for March:

The budgeted direct labor-hours is used as the denominator activity for the month.

The variable overhead rate variance for March is:

A. $7,000 unfavorable

B. $9,000 unfavorable

C. $13,000 unfavorable

D. $11,000 unfavorable

Answer:

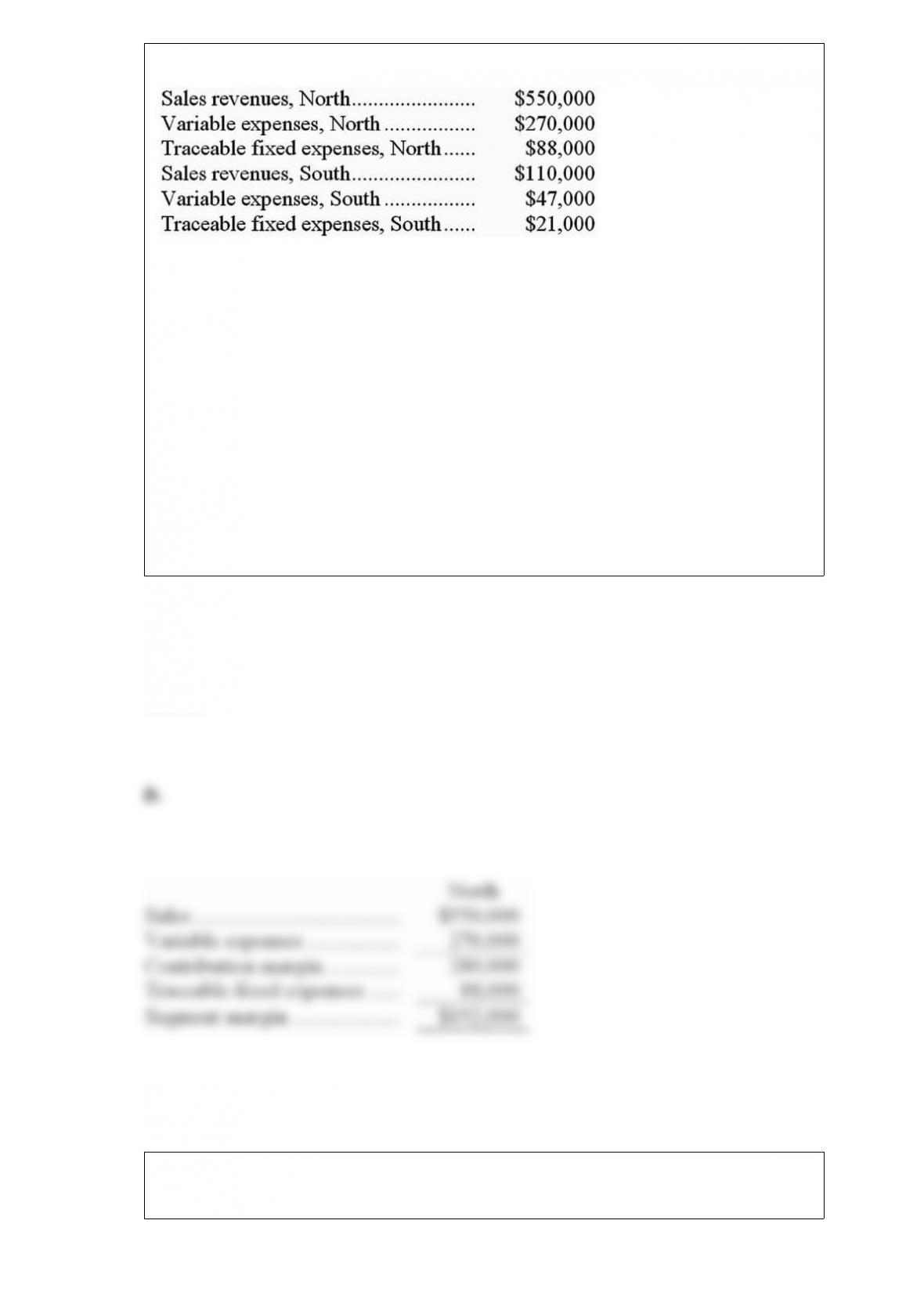

Data for June for Ozaki Corporation and its two major business segments, North and

South, appear below:

In addition, common fixed expenses totaled $145,000 and were allocated as follows:

$73,000 to the North business segment and $72,000 to the South business segment.

A properly constructed segmented income statement in a contribution format would

show that the segment margin of the North business segment is:

A. $270,000

B. $119,000

C. $207,000

D. $192,000

Answer:

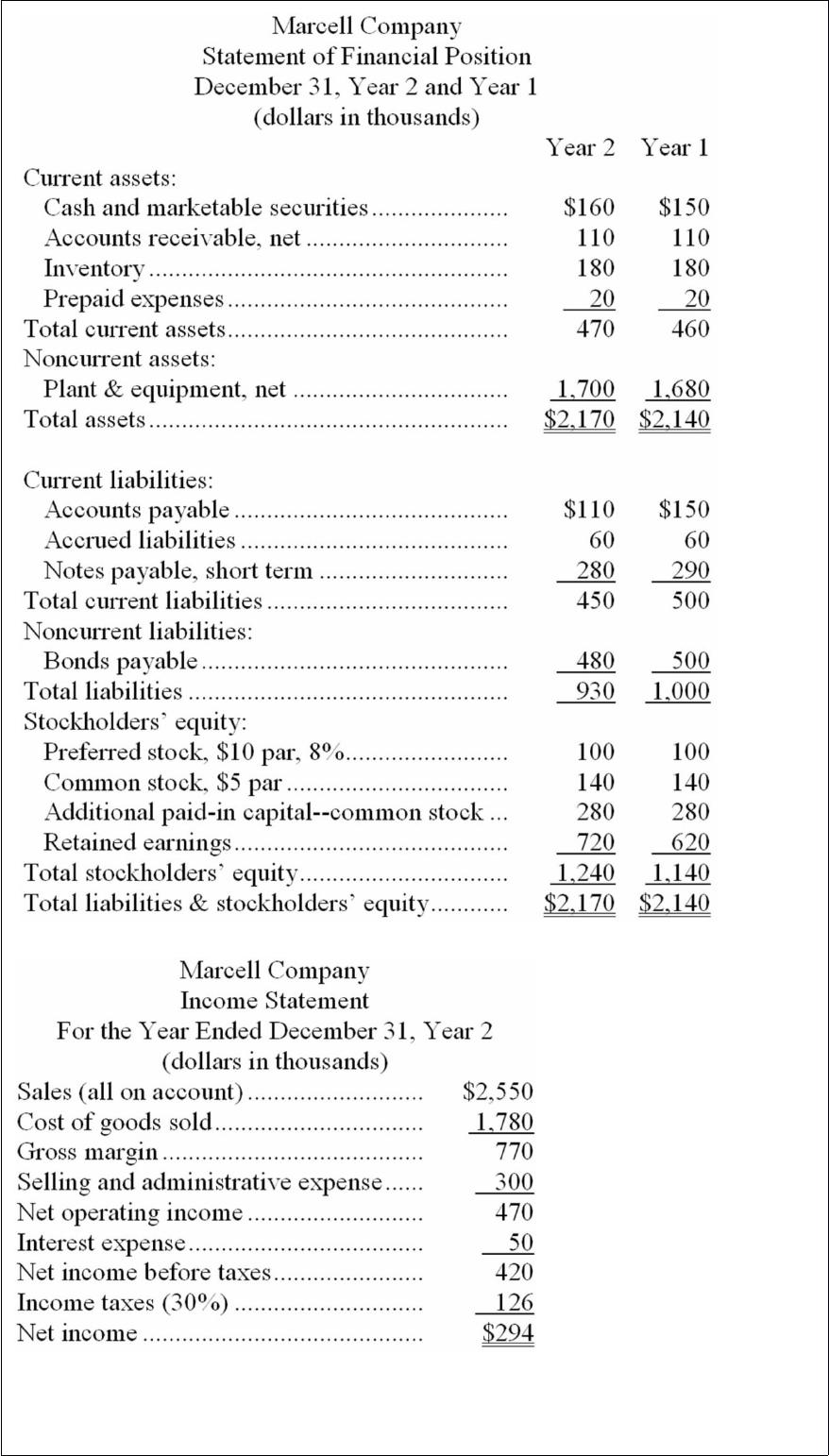

Financial statements for Marcell Company appear below:

Marcell Company’s accounts receivable turnover for Year 2 was closest to:

A. 16.2

B. 9.9

C. 23.2

D. 14.2

Answer:

Which of the following represents the correct order in which the indicated budget

documents for a manufacturing company would be prepared?

A. Sales budget, cash budget, direct materials budget, direct labor budget

B. Production budget, sales budget, direct materials budget, direct labor budget

C. Sales budget, cash budget, production budget, direct materials budget

D. Selling and administrative expense budget, cash budget, budgeted income

statement, budgeted balance sheet

Answer:

In January, one of the processing departments at Seidl Corporation had ending work in

process inventory of $35,000. During the month, $111,000 of costs were added to

production and the cost of units transferred out from the department was $86,000.

In the department’s cost reconciliation report for January, the total cost accounted for

would be:

A. $242,000

B. $232,000

C. $121,000

D. $45,000

Answer:

The Gasson Company sells three products, Product A, Product B and Product C, and

had sales of $1,000,000 during the month of June. The company’s overall contribution

margin ratio was 37% and fixed expenses totaled $350,000. Sales were: Product A,

$500,000; Product B, $300,000; and Product C, $200,000. Traceable fixed costs were:

Product A, $120,000; Product B, $100,000; and Product C, $60,000. The variable

expenses of Product A were $300,000 and the variable expenses of Product B were

$180,000.

The contribution margin in dollars for Product B for June was:

A. $20,000

B. $111,000

C. $120,000

D. $200,000

Answer:

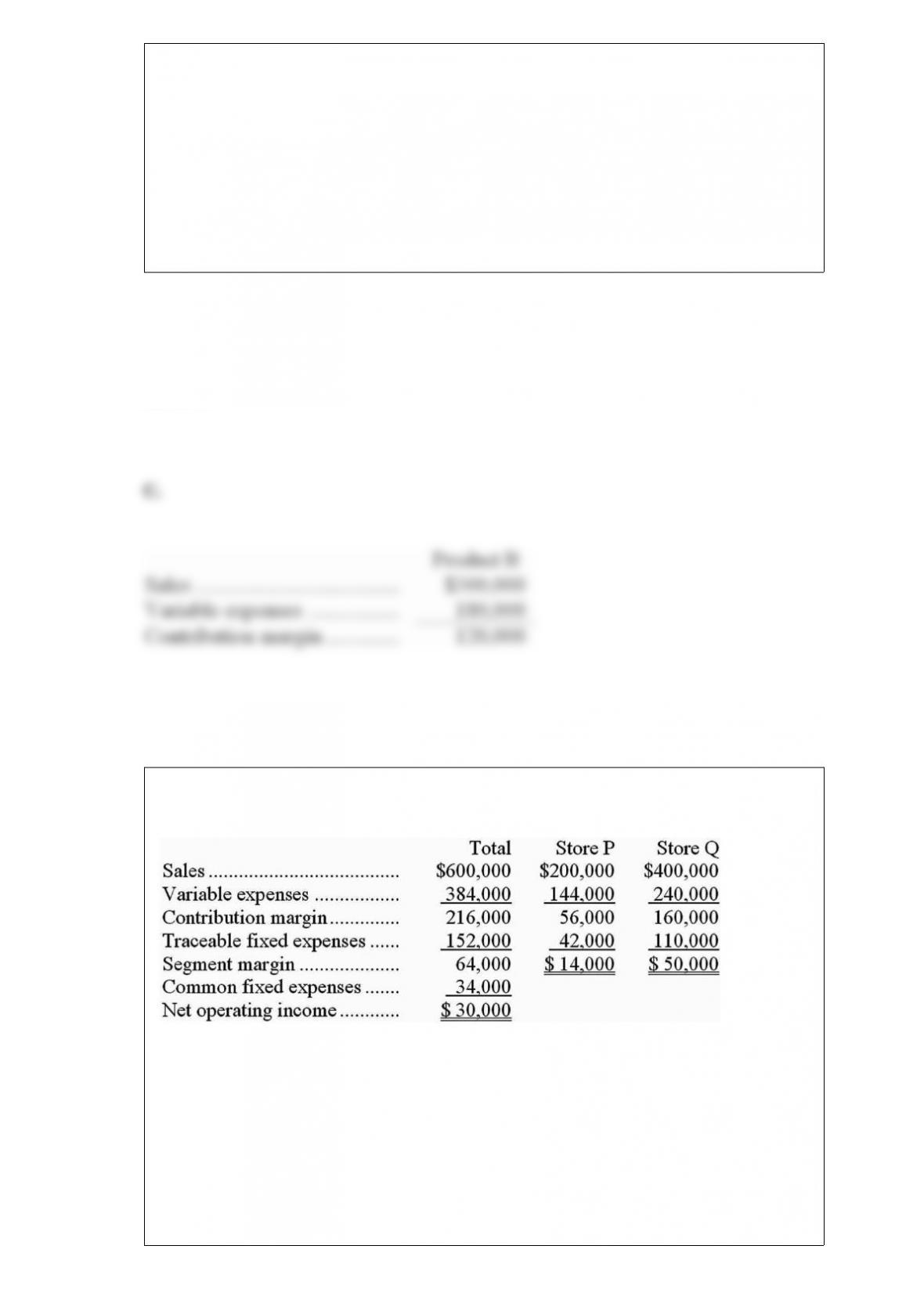

Ring, Incorporated’s income statement for the most recent month is given below.

Refer to the original data.

If sales in Store Q increase by $30,000 as a result of a $7,000 increase in traceable fixed

costs:

A. Store Q’s contribution margin should increase by $18,000

B. Store Q’s segment margin should increase by $12,000

C. Store Q’s contribution margin should increase by $11,000

D. Store Q’s segment margin should increase by $5,000

Answer:

In a job-order costing system, indirect materials that have been previously purchased

and that are used in production are recorded as a debit to:

A. Work in Process inventory.

B. Manufacturing Overhead.

C. Finished Goods inventory.

D. Raw Materials inventory.

Answer:

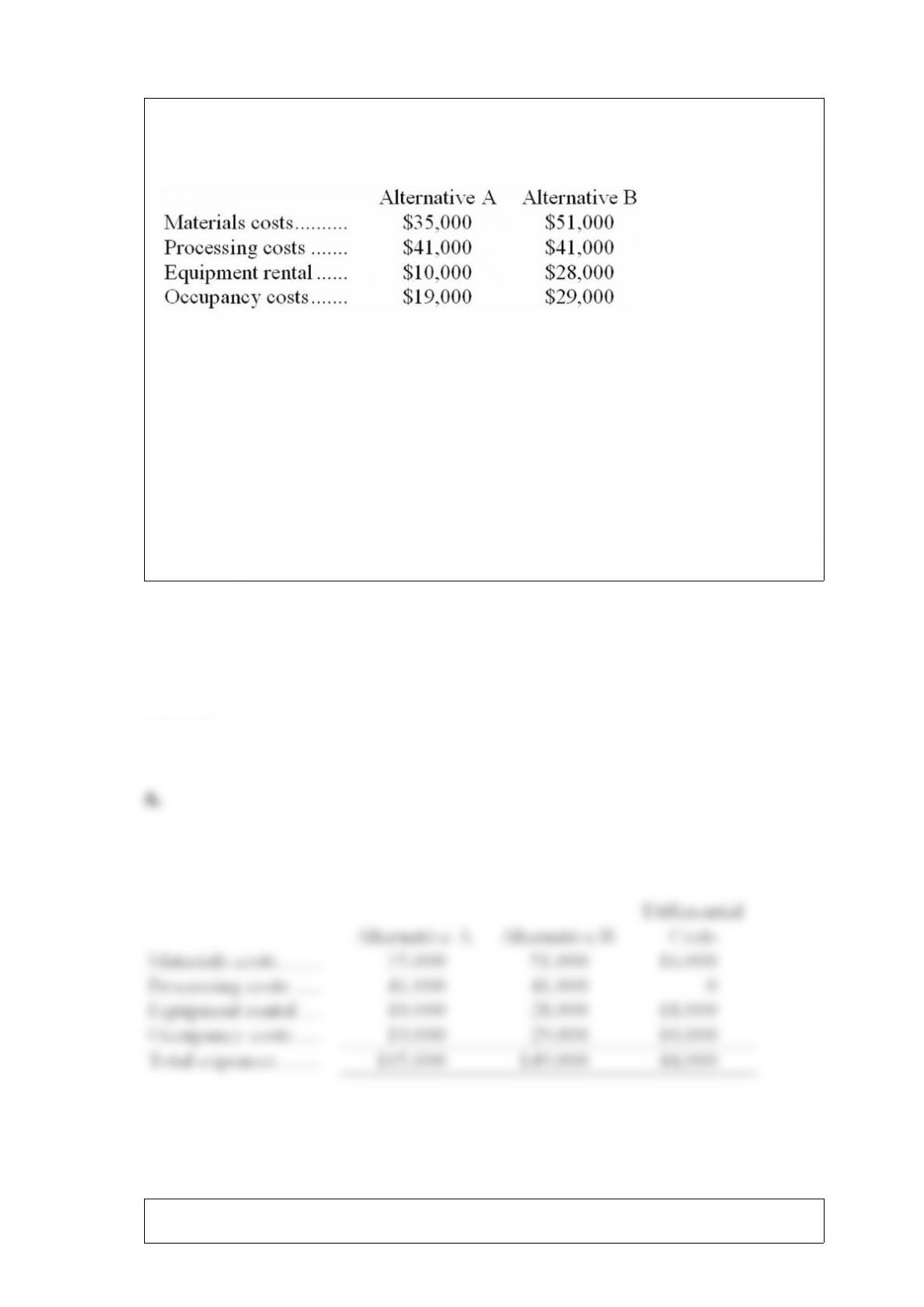

Zurasky Corporation is considering two alternatives: A and B. Costs associated with the

alternatives are listed below:

What is the differential cost of Alternative B over Alternative A, including all of the

relevant costs?

A. $44,000

B. $149,000

C. $105,000

D. $127,000

Answer:

Lagasca Corporation’s contribution format income statement for December appears

below:

The degree of operating leverage is closest to:

A. 10.56

B. 0.21

C. 4.69

D. 0.09

Answer:

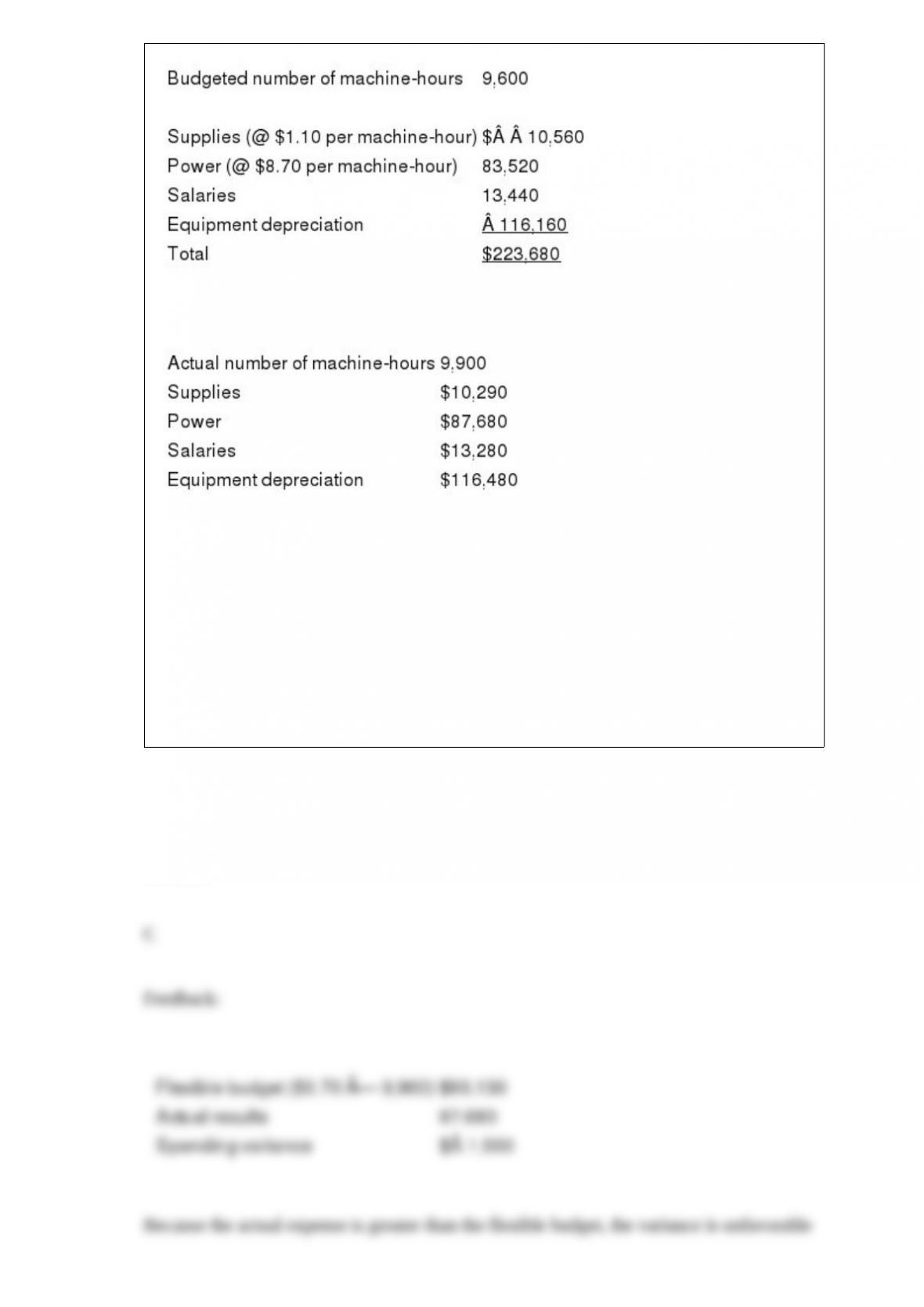

Reference: 8-28

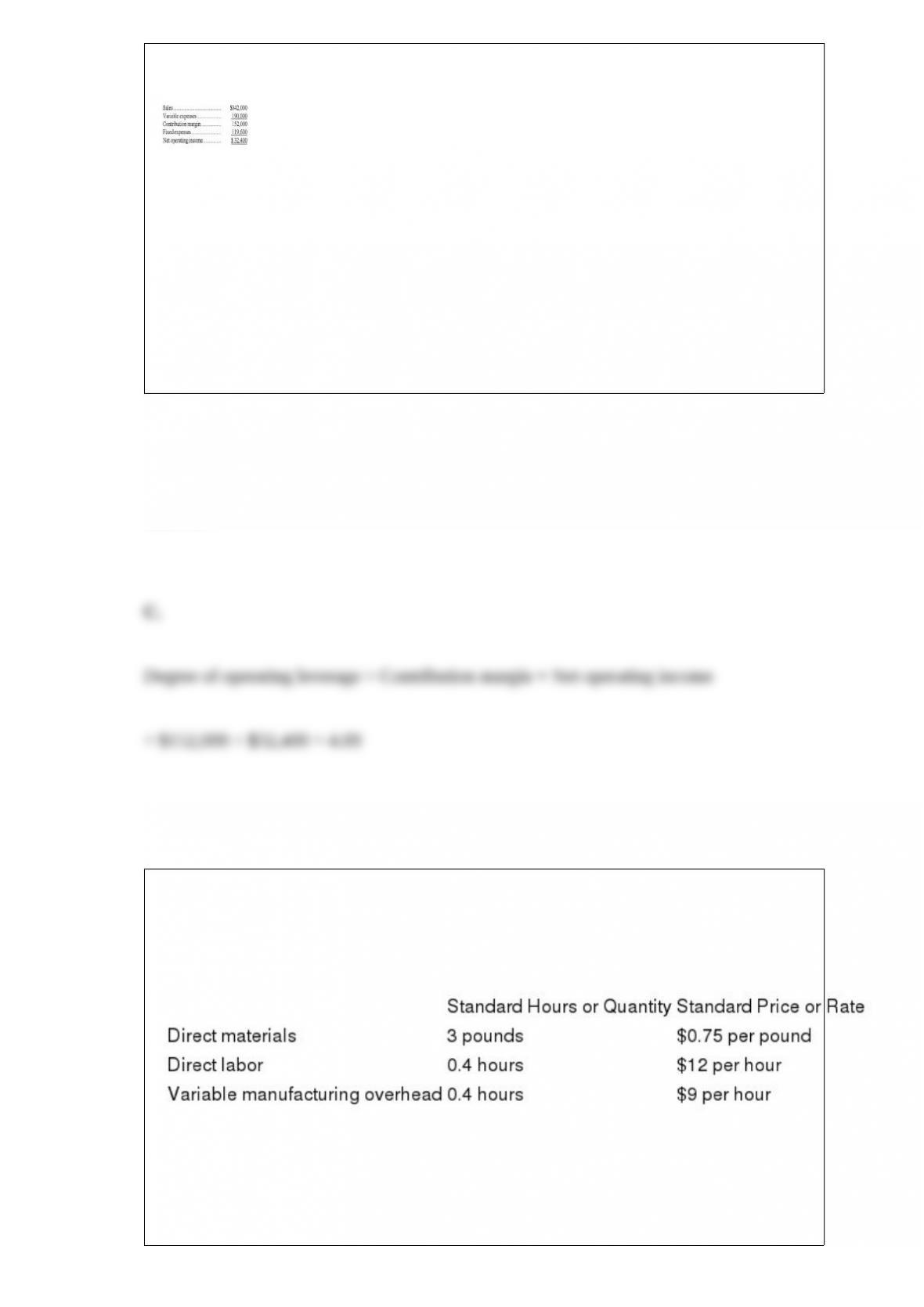

Cox Engineering performs cement core tests in its laboratory. The following standards

have been set for each core test performed:

During March, the laboratory performed 2,000 core tests. On March 1 no direct

materials (sand) were on hand. Variable manufacturing overhead is assigned to core

tests on the basis of standard direct labor-hours. The following events occurred during

March:

– 8,600 pounds of sand were purchased at a cost of $7,310.

– 7,200 pounds of sand were used for core tests.

– 840 actual direct labor-hours were worked at a cost of $8,610.

– Actual variable manufacturing overhead incurred was $3,200.

The variable overhead efficiency variance for March is:

A) $320 unfavorable

B) $320 favorable

C) $360 unfavorable

D) $360 favorable

Answer:

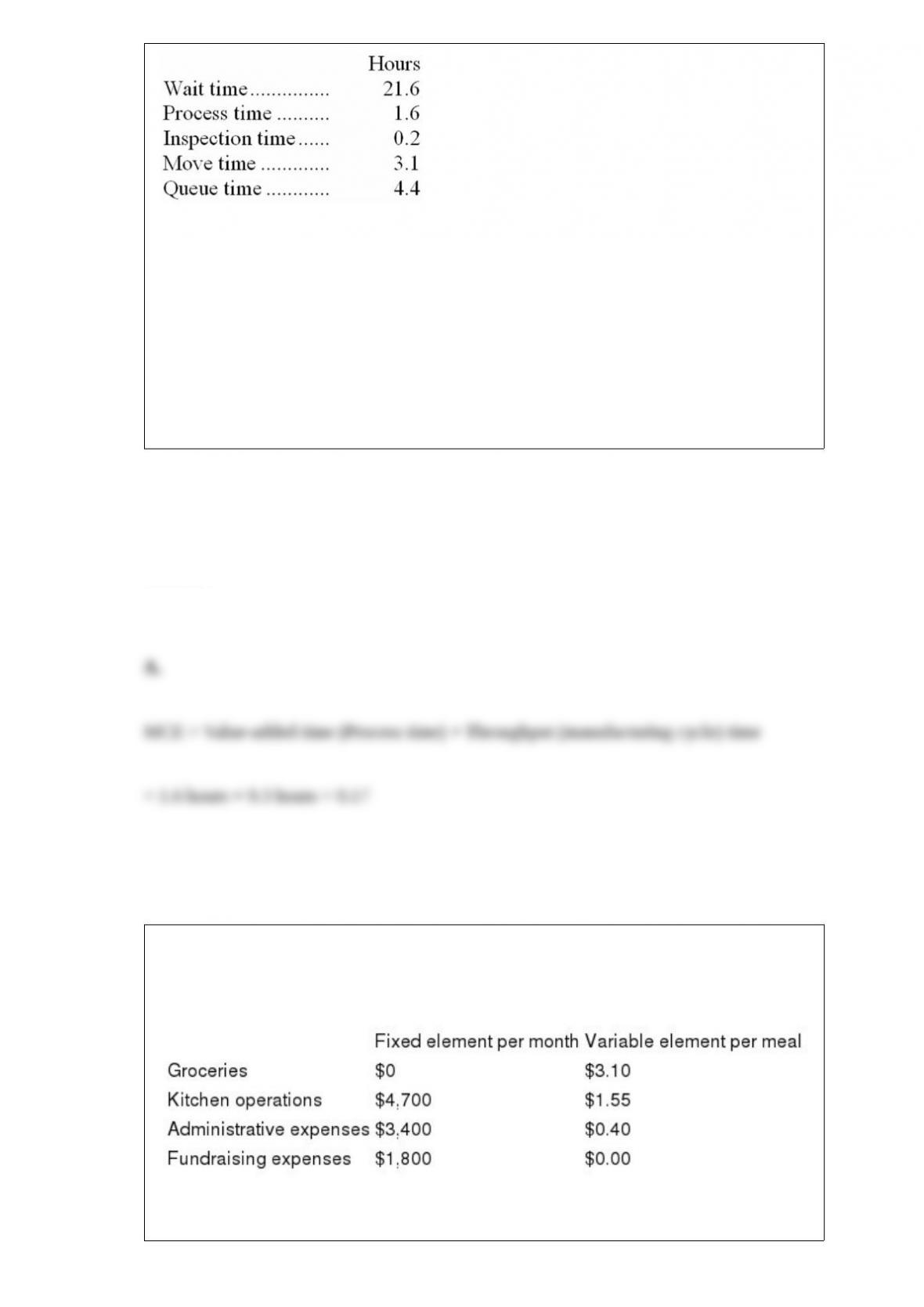

Saffer Corporation keeps careful track of the time required to fill orders. Data

concerning a particular order appear below:

The manufacturing cycle efficiency (MCE) was closest to:

A. 0.17

B. 0.05

C. 0.43

D. 0.19

Answer:

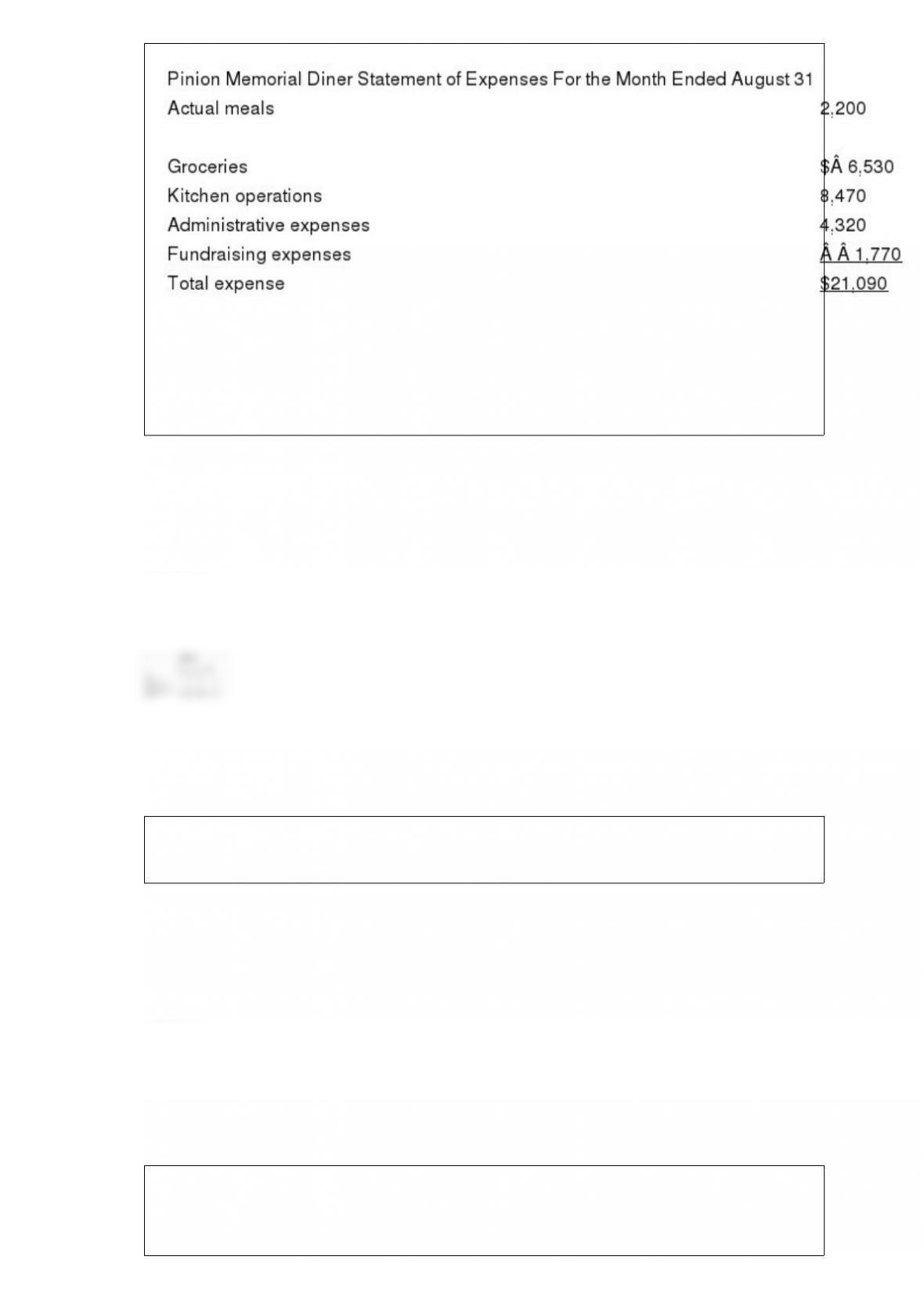

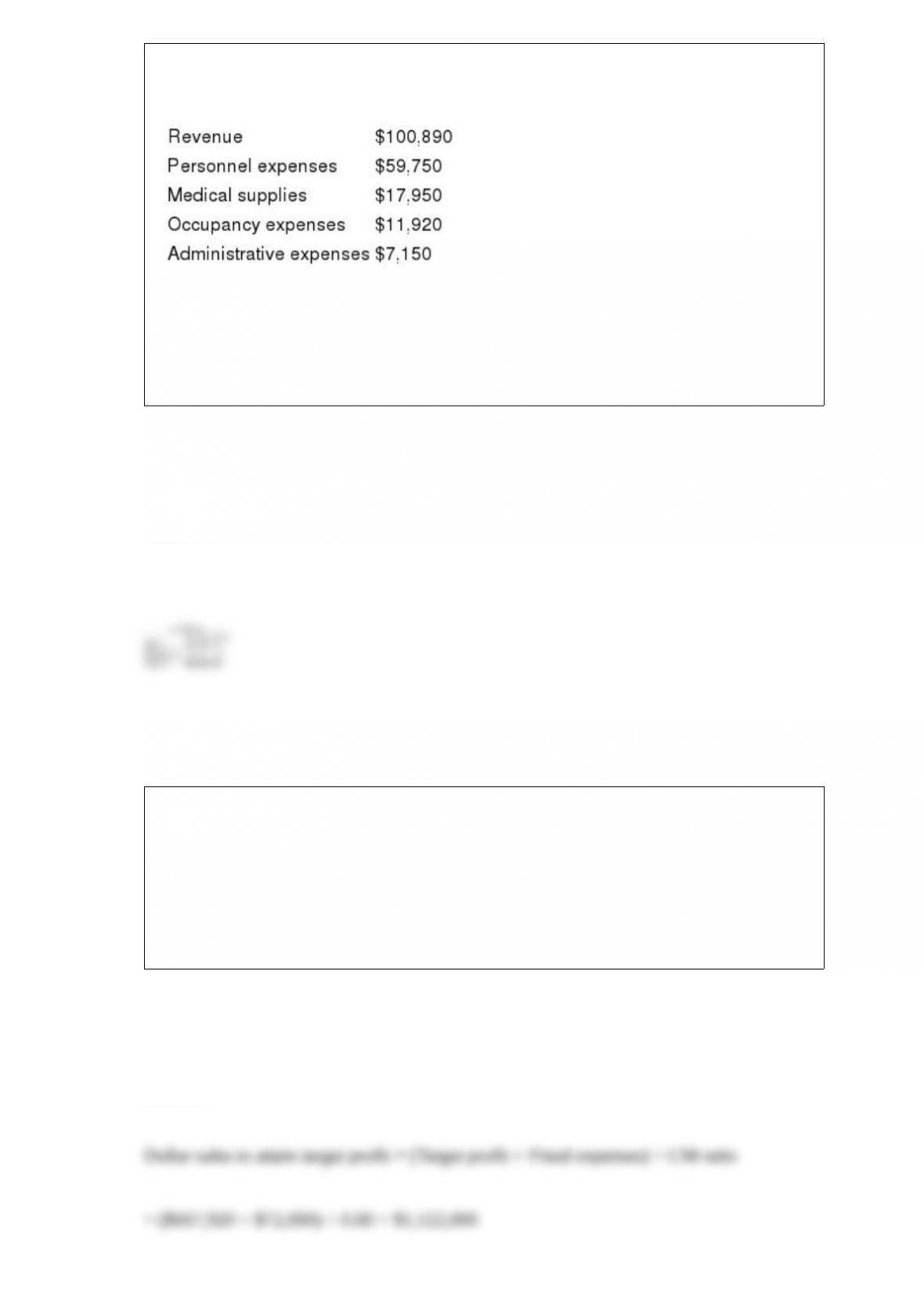

Pinion Memorial Diner is a charity supported by donations that provides free meals to

the homeless. The diners budget for August was based on 2,700 meals. The diners

director has provided the following cost formulas to use in budgets:

The director has also provided the diners statement of actual expenses for the month:

Required:

Prepare a report showing the spending variances for each of the expenses and for total

expenses for August. Label each variance as favorable (F) or unfavorable (U).

Answer:

Answer:

The Casket Division of Rosencranz Corporation had average operating assets of

$150,000 and net operating income of $27,800 in March. The company uses residual

income to evaluate the performance of its divisions, with a minimum required rate of

return of 17%.

What was the Casket Division’s residual income in March?

Answer:

Data from Paynter Corporation’s most recent balance sheet appear below:

A total of 100,000 shares of common stock and 20,000 shares of preferred stock were

outstanding at the end of the year.

Compute the book value per share. Show your work!

Answer:

Ermoin Inc. uses the FIFO method in its process costing system. The following data

concern the operations of the company’s first processing department for a recent month.

Using the FIFO method:

a. Determine the equivalent units of production for materials and conversion costs.

b. Determine the cost per equivalent unit for materials and conversion costs.

c. Determine the cost of ending work in process inventory.

d. Determine the cost of units transferred out of the department during the month.

Answer:

Parkins Company produces and sells a single product. The company’s income statement

for the most recent month is given below:

There are no beginning or ending inventories.

a. Compute the company’s monthly break-even point in units of product.

b. What would the company’s monthly net operating income be if sales increased by

25% and there is no change in total fixed expenses?

c. What dollar sales must the company achieve in order to earn a net operating income

of $50,000 per month?

d. The company has decided to automate a portion of its operations. The change will

reduce direct labor costs per unit by 40 percent, but it will double the costs for fixed

factory overhead. Compute the new break-even point in units.

Answer:

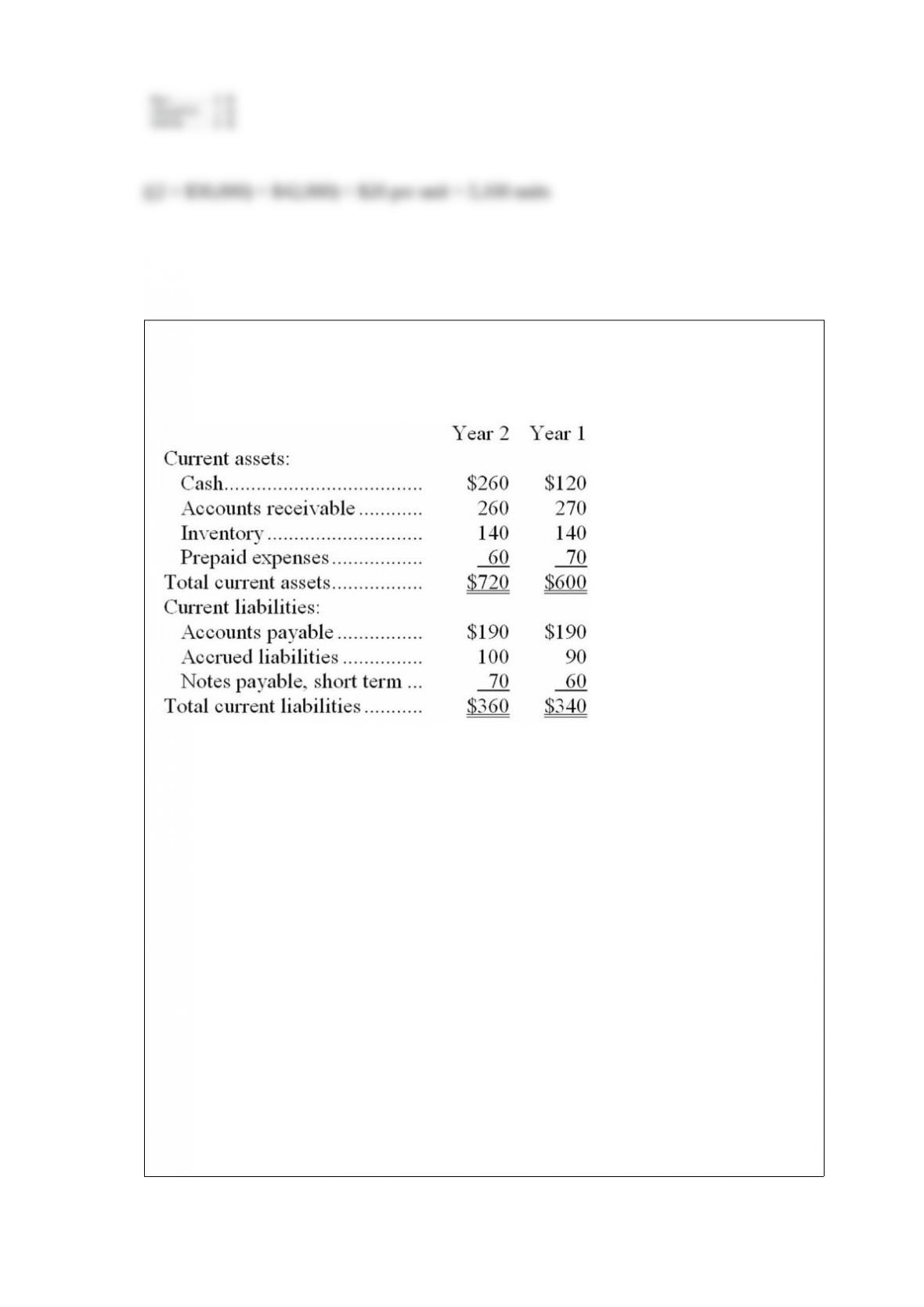

Excerpts from Stepney Corporation’s most recent balance sheet (in thousands of dollars)

appear below:

Sales on account during the year totaled $1,440 thousand. Cost of goods sold was $890

thousand.

Compute the following for Year 2:

a. Working capital.

b. Current ratio.

c. Acid-test ratio.

d. Accounts receivable turnover.

e. Average collection period.

f. Inventory turnover.

g. Average sale period.

Answer:

Part E43 is used in one of Ran Corporation’s products. The company’s Accounting

Department reports the following costs of producing the 12,000 units of the part that are

needed every year.

An outside supplier has offered to make the part and sell it to the company for $14.70

each. If this offer is accepted, the supervisor’s salary and all of the variable costs,

including direct labor, can be avoided. The special equipment used to make the part was

purchased many years ago and has no salvage value or other use. The allocated general

overhead represents fixed costs of the entire company. If the outside supplier’s offer

were accepted, only $5,000 of these allocated general overhead costs would be avoided.

a. Prepare a report that shows the effect on the company’s total net operating income of

buying part E43 from the supplier rather than continuing to make it inside the company.

b. Which alternative should the company choose?

Answer:

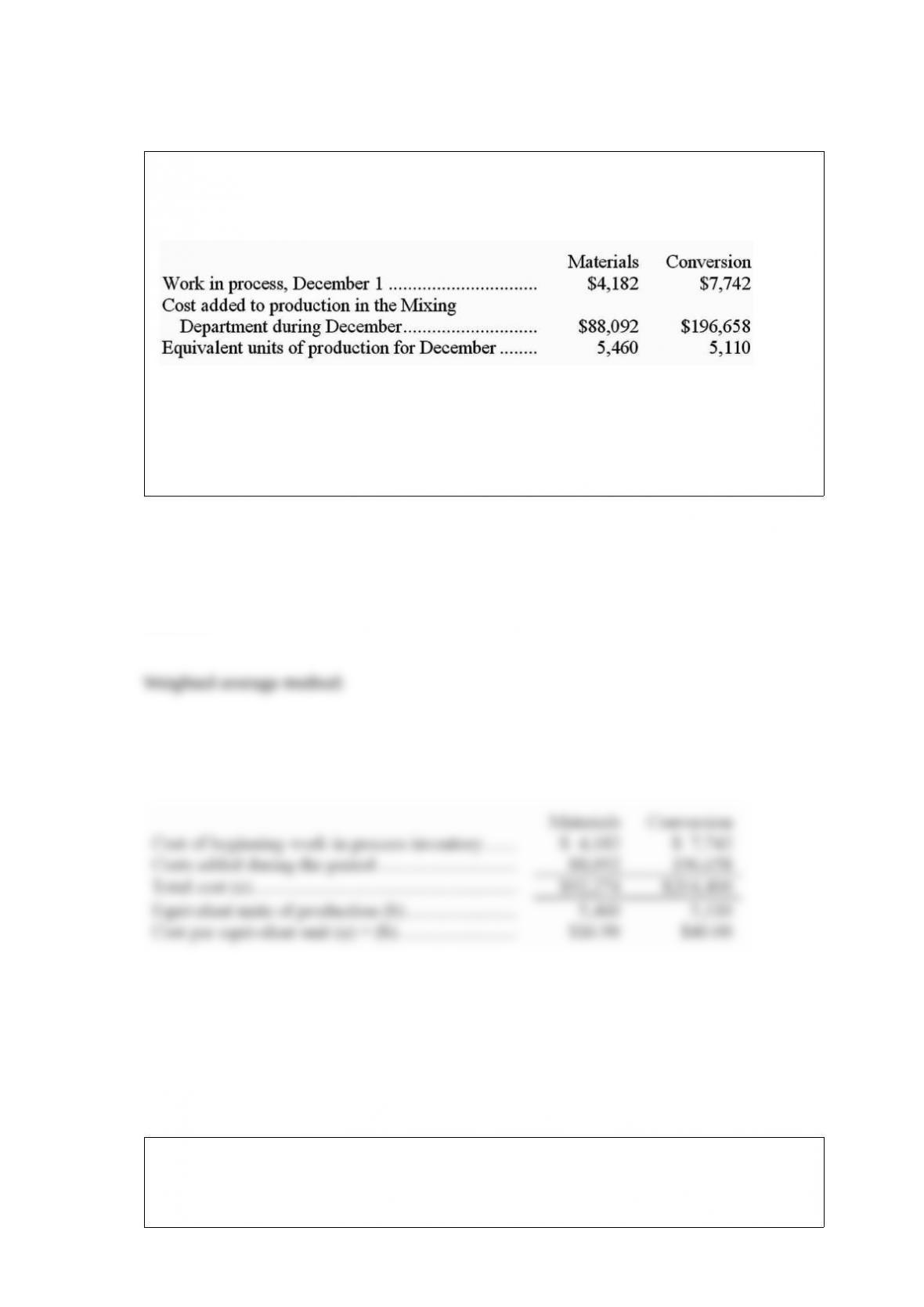

Dominick Inc. uses the weighted-average method in its process costing. The following

data concern the company’s Mixing Department for the month of December.

Compute the cost per equivalent unit for materials and conversion for the Mixing

Department in December.

Answer:

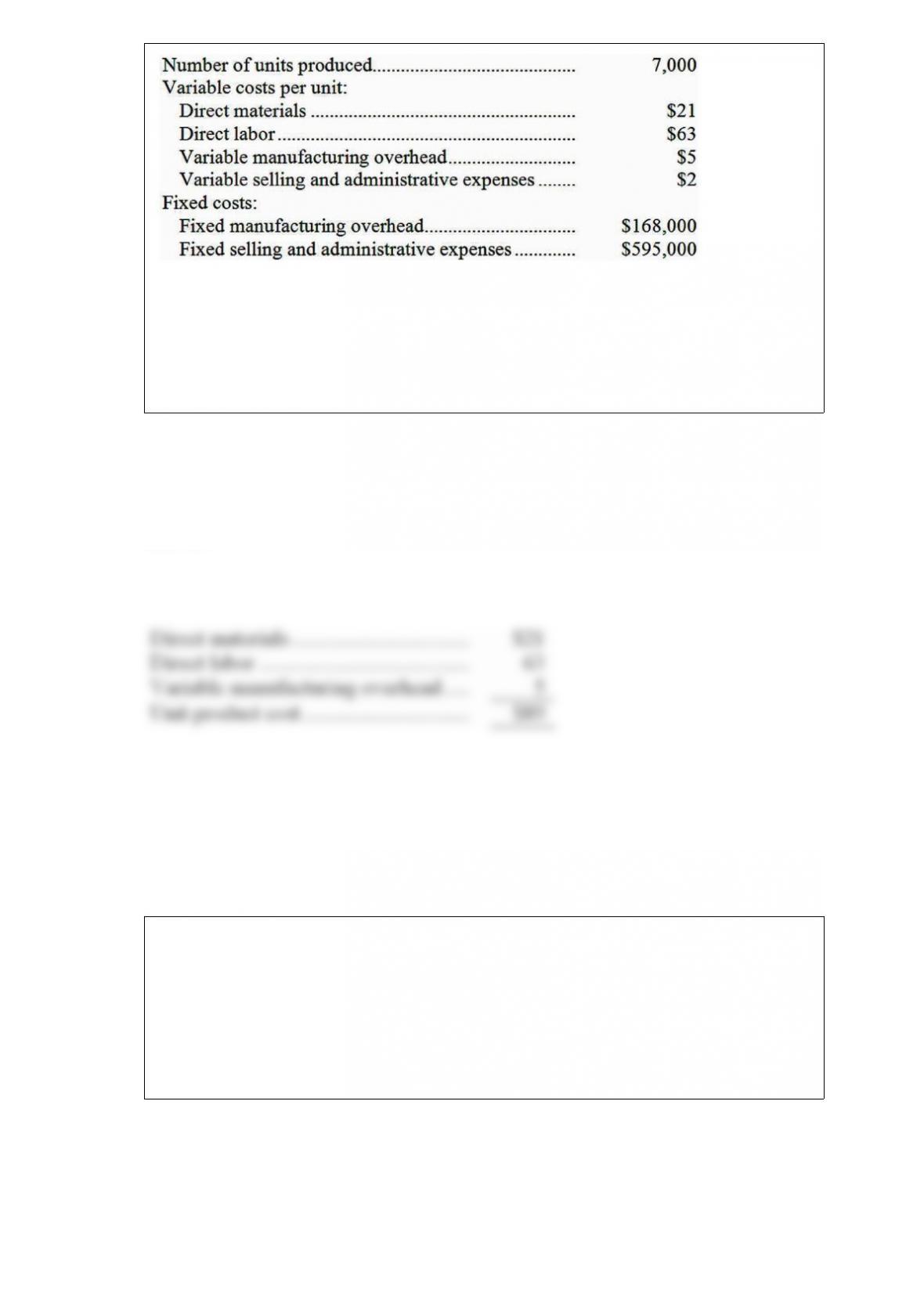

Bertone Inc., which produces a single product, has provided the following data for its

most recent month of operation:

The company had no beginning or ending inventories.

Compute the unit product cost under variable costing. Show your work!

Answer:

Titlow, Inc., produces and sells a single product. The product sells for $220.00 per unit

and its variable expense is $57.20 per unit. The company’s monthly fixed expense is

$713,064.

Determine the monthly break-even in unit sales. Show your work!

Answer:

Walkenhorst Corporations manufacturing overhead includes $7.80 per machine-hour

for supplies; $7.30 per machine-hour for indirect labor; $21,210 per period for salaries;

and $19,950 per period for depreciation.

Required:

Determine the predetermined overhead rate if the denominator level of activity is 1,500

machine-hours. Show your work!

Answer:

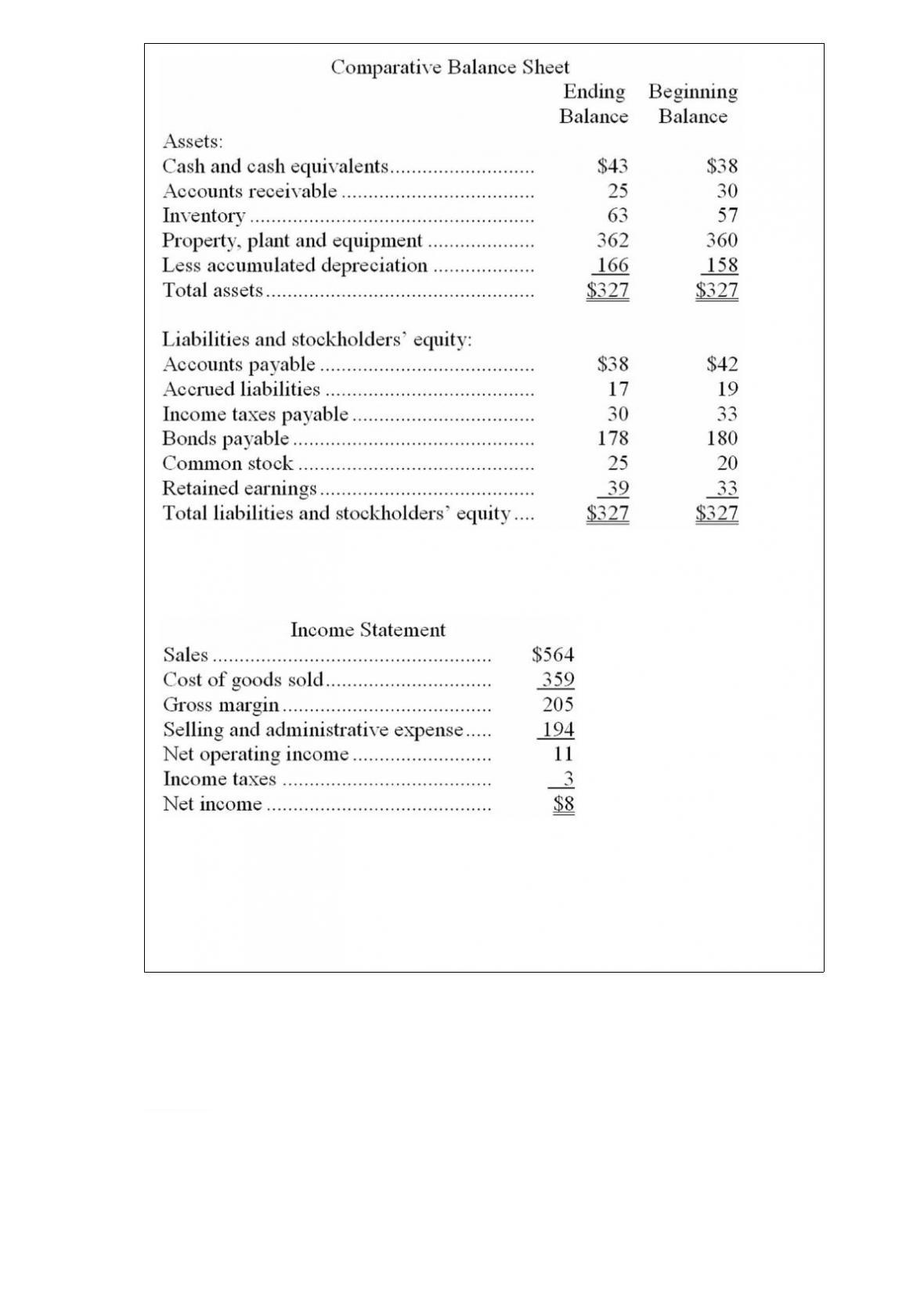

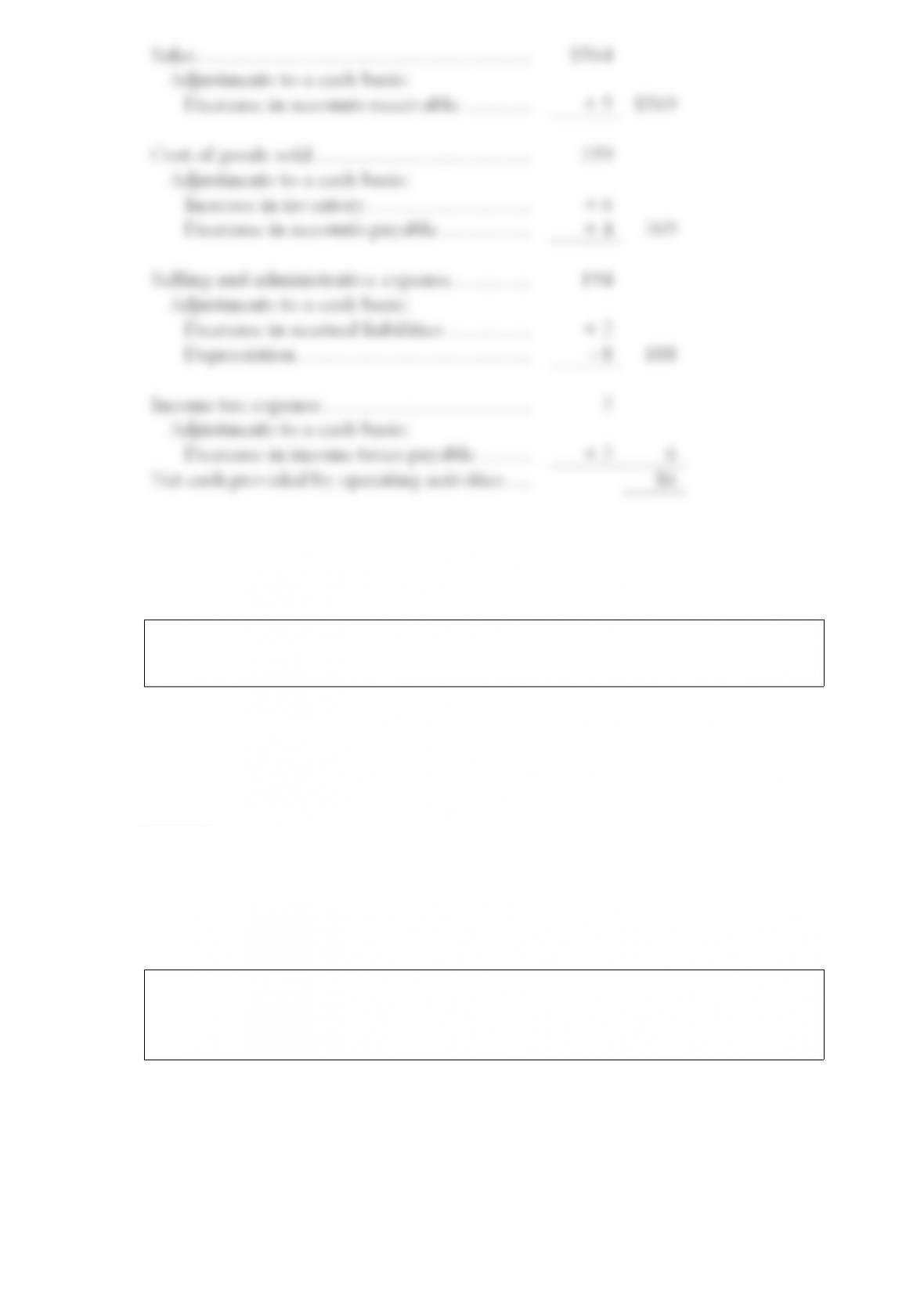

Milton Corporation’s balance sheet and income statement appear below:

Cash dividends were $2. The company did not dispose of any property, plant, and

equipment during the year.

Prepare the operating activities section of the statement of cash flows using the direct

method.

Answer:

Answer:

Qu Company, which has only one product, has provided the following data concerning

its most recent month of operations:

a. What is the unit product cost for the month under variable costing?

b. Prepare a contribution format income statement for the month using variable costing.

c. Without preparing an income statement, determine the absorption costing net

operating income for the month. (Hint: Use the reconciliation method.)

Answer:

Carlisle Clinic uses patient-visits as its measure of activity. During December, the clinic

budgeted for 2,500 patient-visits, but its actual level of activity was 2,100 patient-visits.

The clinic has provided the following data concerning the formulas used in its

budgeting and its actual results for December:

Data used in budgeting:

Actual results for December:

Required:

Prepare a report showing the clinics revenue and spending variances for December.

Label each variance as favorable (F) or unfavorable (U).

Answer:

Dagnan Corporation produces and sells a single product whose contribution margin

ratio is 66%. The company’s monthly fixed expense is $667,920 and the company’s

monthly target profit is $72,600.

Determine the dollar sales to attain the company’s target profit. Show your work!

Answer:

The following monthly data in contribution format are available for the MN Company

and its only product, Product SD:

The company produced and sold 300 units during the month and had no beginning or

ending inventories.

a. Without resorting to calculations, what is the total contribution margin at the

break-even point?

b. Management is contemplating the use of plastic gearing rather than metal gearing in

Product SD. This change would reduce variable expenses by $18 per unit. The

company’s sales manager predicts that this would reduce the overall quality of the

product and thus would result in a decline in sales to a level of 250 units per month.

Should this change be made?

c. Assume that MN Company is currently selling 300 units of Product SD per month.

Management wants to increase sales and feels this can be done by cutting the selling

price by $22 per unit and increasing the advertising budget by $20,000 per month.

Management believes that these actions will increase unit sales by 50 percent. Should

these changes be made?

d. Assume that MN Company is currently selling 300 units of Product SD. Management

wants to automate a portion of the production process for Product SD. The new

equipment would reduce direct labor costs by $20 per unit but would result in a

monthly rental cost for the new robotic equipment of $10,000. Management believes

that the new equipment will increase the reliability of Product SD thus resulting in an

increase in monthly sales of 12%. Should these changes be made?

Answer:

Answer:

Answer: