On a bank reconciliation, interest income would be added to the balance per bank.

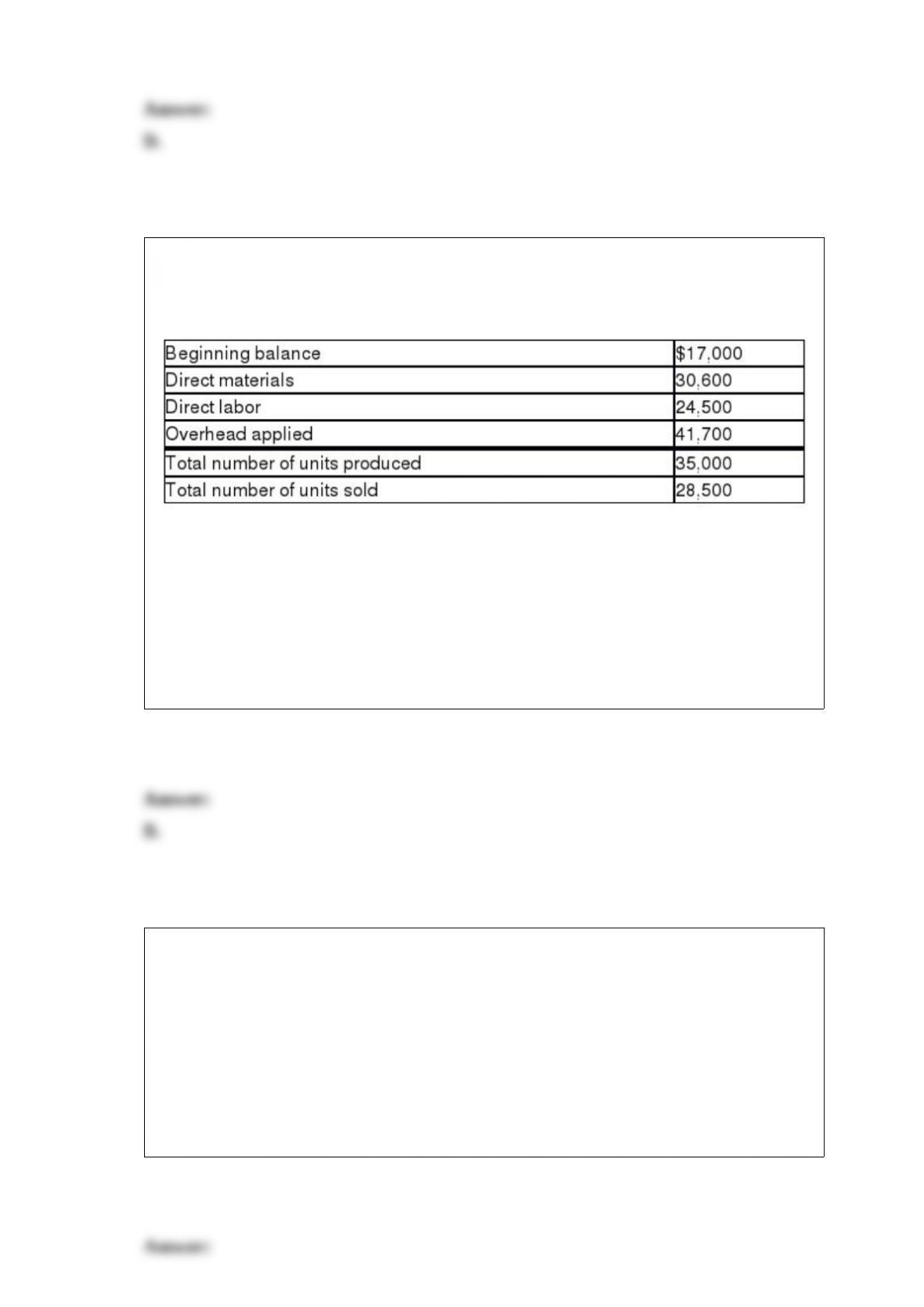

In a process costing system, the equivalent units of production must be computed after

determining the value of ending inventory.

The ending balance in the Work in Process Inventory account equals the ending

Overhead balance.

On a statement of cash flows prepared using the direct method, if accounts payable

have decreased, cash payments for purchases will be greater than net purchases.

The statement of owner’s equity relates the income statement to the balance sheet by

showing how the owner’s capital account changed during the accounting period.

One advantage of a corporation is the lack of mutual agency.

Book value per share of stock represents the amount the shareholder will receive per

share if the company is sold or liquidated.

The key to produce an accurate and useful report include identifying the why, who,

what, and when of the report.

When the terms are FOB shipping point, the title passes at the destinationand the seller

pays the transportation costs.

The call feature of bonds is useful if a company wants to retire a bond issue.

The direct method converts each item on the income statement to its cash equivalent.

The direct charge-off method of recognizing uncollectible accounts is not in accordance

with generally accepted accounting principles.

A company’s five-day weekly payroll of $890 is paid on Fridays. Assume that the last

day of the month falls on Tuesday. Which of the following is the required adjusting

entry for the month end?

A.Debit Salaries Payable $534 and credit Salaries Expense $534.

B.Debit Salaries Expense $534 and credit Salaries Payable $534.

C.Debit Unpaid Salaries $356 and credit Salaries Payable $356.

D.Debit Salaries Expense $356 and credit Salaries Payable $356.

Which of the following transactions does not involve an exchange of value?

A.Payment of a debt

B.Purchase of a building on credit

C.Borrowing money

D.Loss from theft

Which of the following is not considered an operating expense?

A.General office expenses.

B.Cost of goods sold.

C.Freight-out expense.

D.Advertising expense.

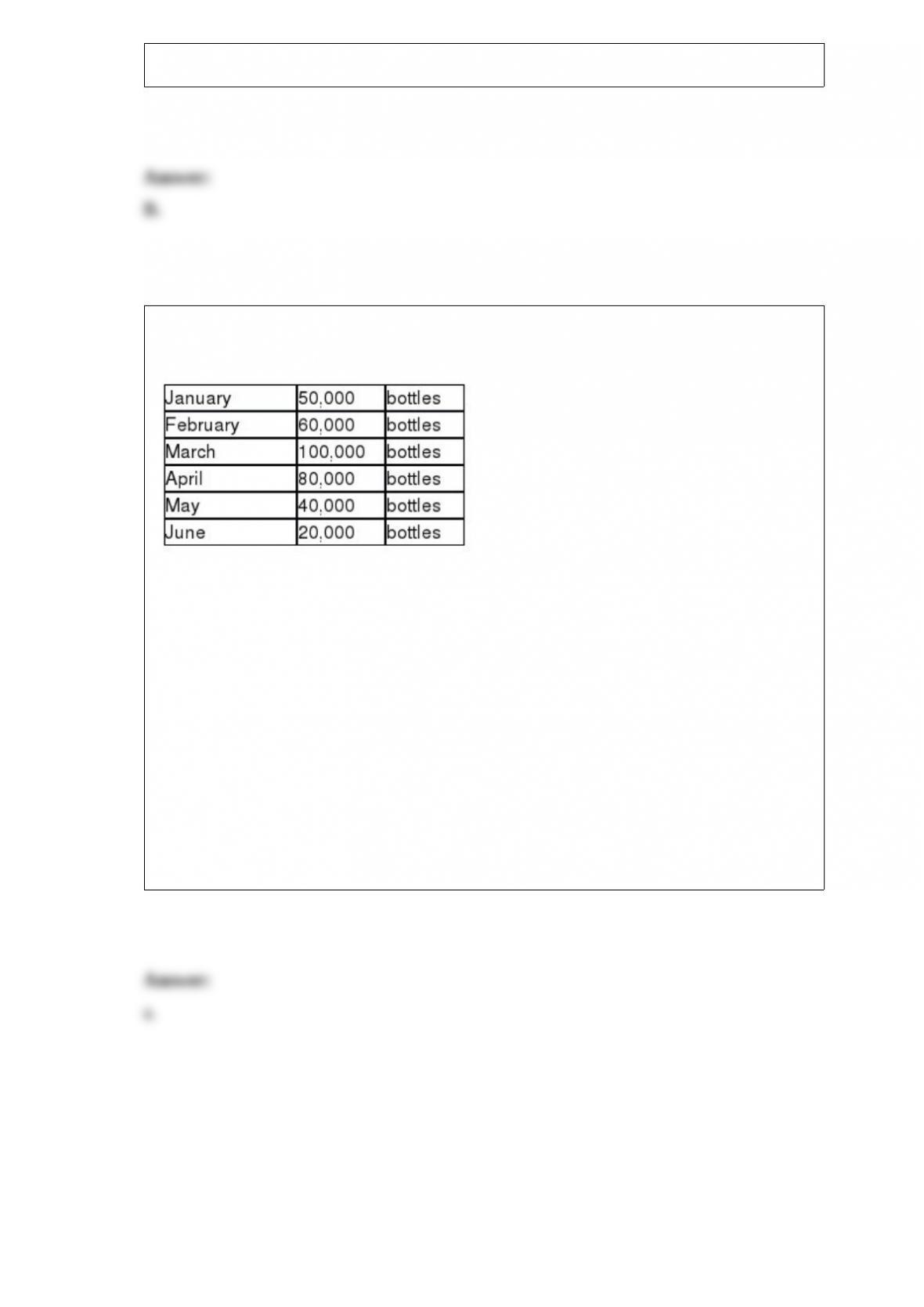

Crosson Wineries & Bottling is preparing its budget for 2014 and has completed the

sales budget for the first six months of the year. The projected volume is as follows:

The desired ending inventory for each month must be equal to 30 percent of the next

month’s sales. The December 31, 2013, inventory was 15,000 bottles.

a. Prepare the production budget for the first four months of 2014.

b. Explain why Crosson Wineries & Bottling must produce more bottles than it sells in

January and February, and why it must produce fewer bottles than it sells in March and

April.

c. Assume each finished bottle requires 25 ounces of wine and that the ending inventory

each month must be equal to 20 percent of the next month’s production needs. The

December 31, 2013, inventory of wine was 265,000 ounces. Prepare the direct materials

purchases budget for the first three months of 2014.

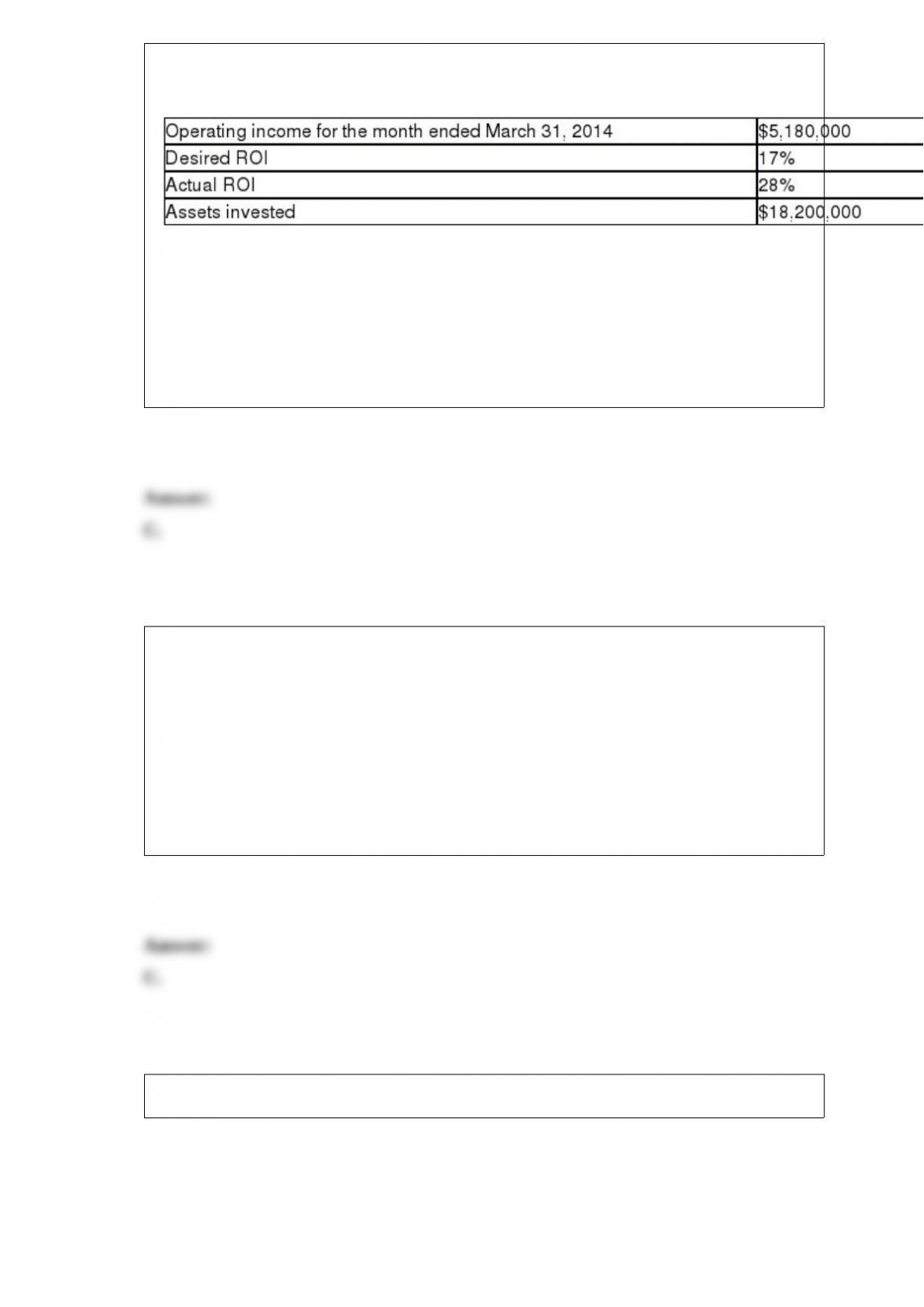

Determine the March 2014 residual income for an investment center with the following

information:

A.$5,180,000

B.$3,094,000

C.$2,086,000

D.$8,806,000

In which of the following situations should a company use process costing rather than

job order costing?

A.If the product cost is accumulated in a single Work in Process Inventory account

B.If the product is produced based on individual customer specifications

C.If the product is composed of mass-produced homogeneous units

D.If the product goes through a single stage of production

Use this information to answer the following question.

The debt to equity ratio is

A.0.48.

B.0.34.

C.0.52.

D.1.92.

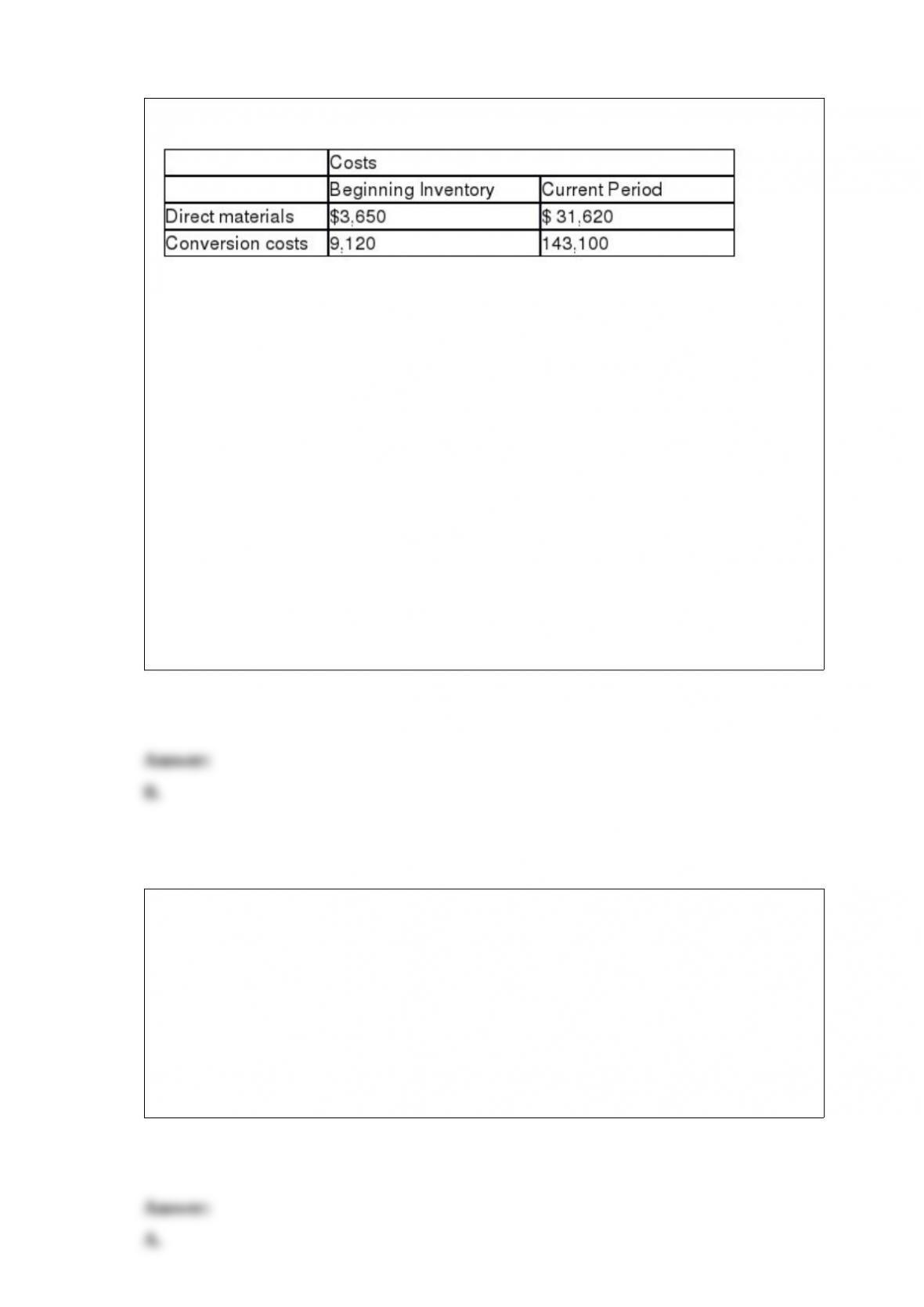

The Bakersfield Company has the following information available:

At the beginning of the period, there were 800 units in process that were 60 percent

complete as to conversion costs and 100 percent complete as to direct materials costs.

During the current period, 5,800 units were started and completed. Ending inventory

contained 400 units that were 60 percent complete as to conversion costs and 100

percent complete as to direct materials costs. (Assume that the company uses the FIFO

process costing method.)

The cost of completing a unit of Bakersfield during the current period was

A.$30.12.

B.$27.60.

C.$28.18.

D.$24.96.

When special journals are used, the general journal is used to record

A.purchase returns.

B.sales of merchandise on credit.

C.receipts of cash.

D.purchases on credit.

In a process costing system, some of the increases to Department C’s Work in Process

Inventory account would come from Department B’s

A.Finished Goods Inventory account.

B.Materials Inventory account.

C.Cost of Goods Sold account.

D.Work in Process Inventory account.

Return on assets is most closely related to

A.interest coverage and the debt to equity ratios.

B.profit margin and the debt to equity ratio.

C.profit margin and asset turnover.

D.inventory turnover and profit margin.

Closing entries are important to managing a business because

A.the owners expect periodic reports of the progress of the business.

B.management needs to prepare budgets for future time periods.

C.to assess progress toward goals, managers need to divide the life of the business into

relatively short time periods.

D.All of these choices.

The following information is available at the end of the period for the completed Job

73:

What is the unit cost for Job 73?

A.$2.55

B.$3.19

C.$1.50

D.$3.92

Which of the following would not be debited to the Machinery account?

A.Installation costs

B.Electricity used by the machine

C.Freight charges

D.Cost of trial runs

Use this information to answer the following question.

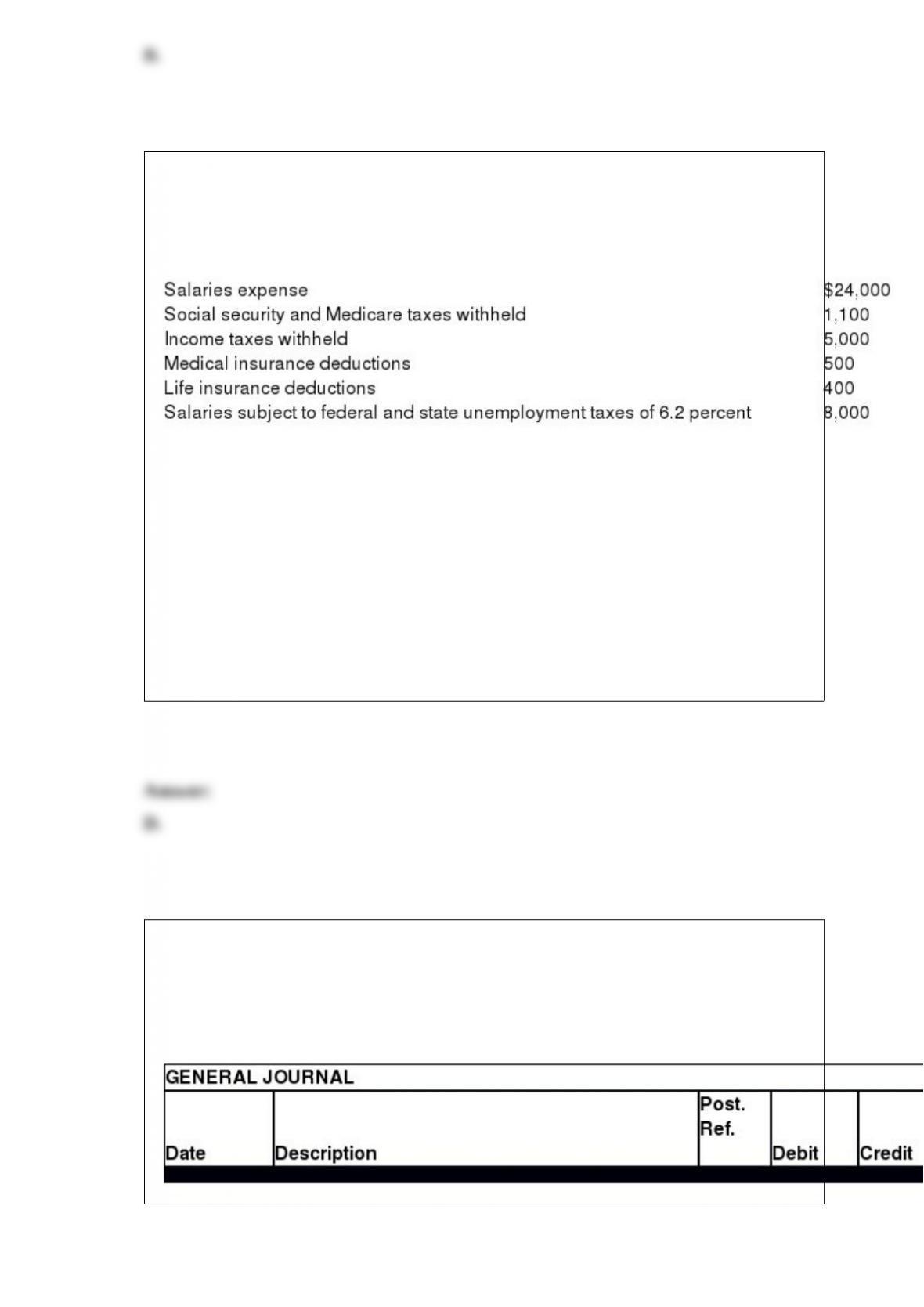

The following totals for the month of September were taken from the payroll register of

Meadors Company:

The amount of liabilities relating to payroll, other than Salaries Payable, is

A.$8,356.

B.$7,496.

C.$7,256.

D.$8,596.

Valdez Corporation has outstanding $1,500,000 of 10 percent bonds callable at 103. On

July 1, a semiannual interest payment date, the unamortized bond premium equaled

$60,000. On that date, $900,000 of the bonds were called and retired. Prepare an entry

in journal form without explanation to record the retirement of the bonds on July 1.

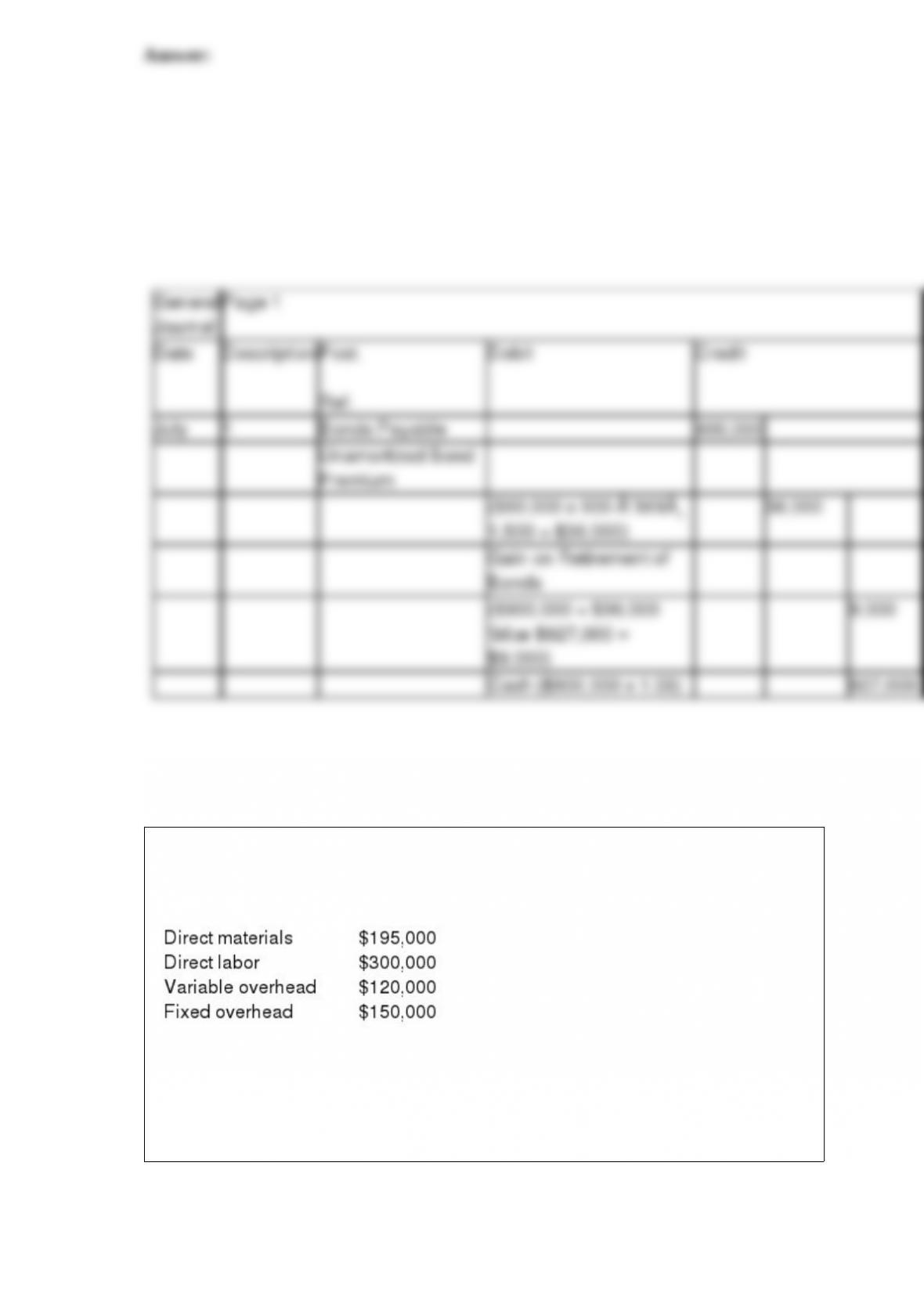

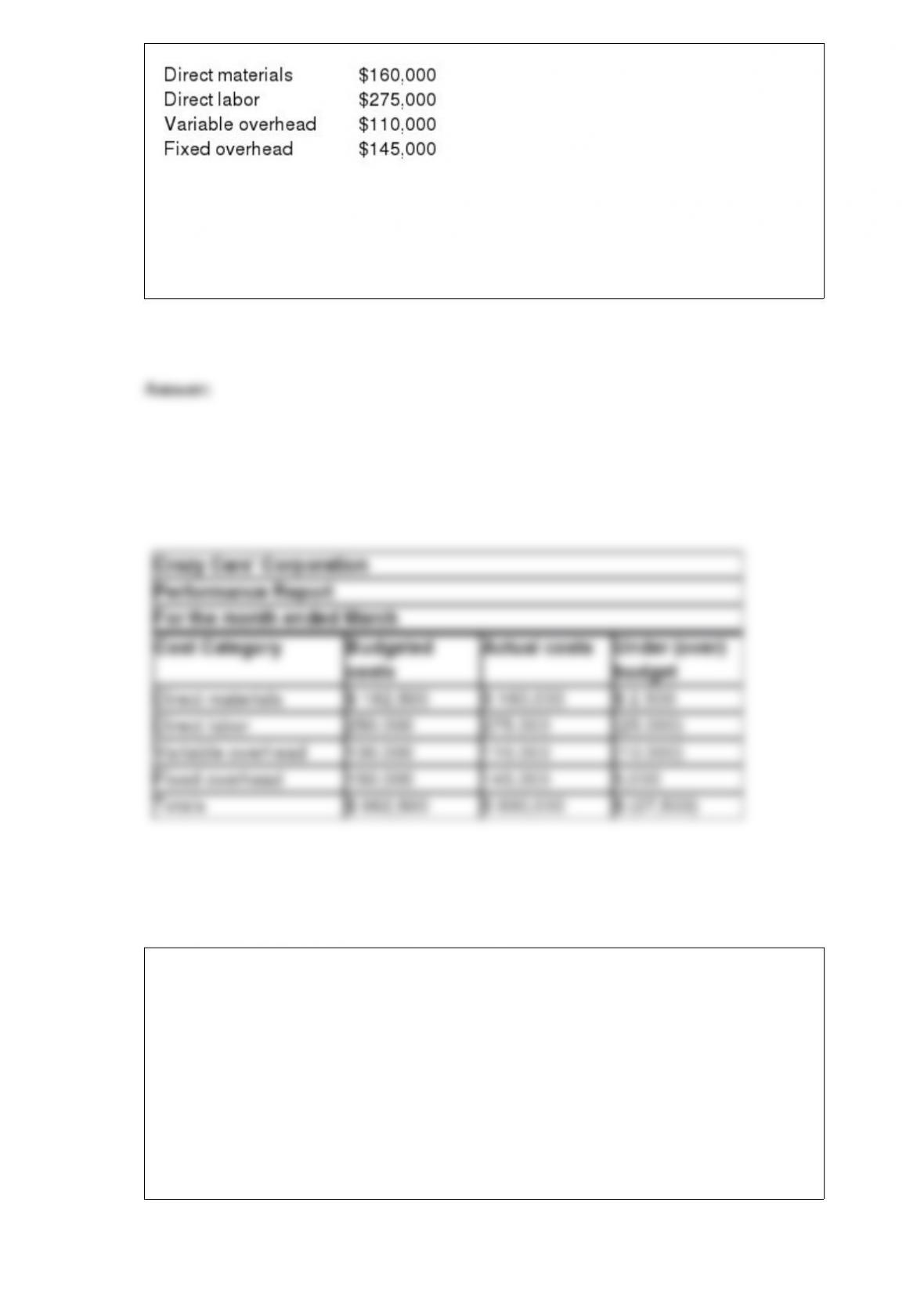

Crazy Cars Corporation’s flexible budget for 30,000 units, for March, gives you the

following information:

The company produced 25,000 units in March with the following actual costs:

Prepare a performance report for March, to compare the data from Crazy Cars’ flexible

budget with the actual costs incurred. Also, find if the costs are under or over budgeted.

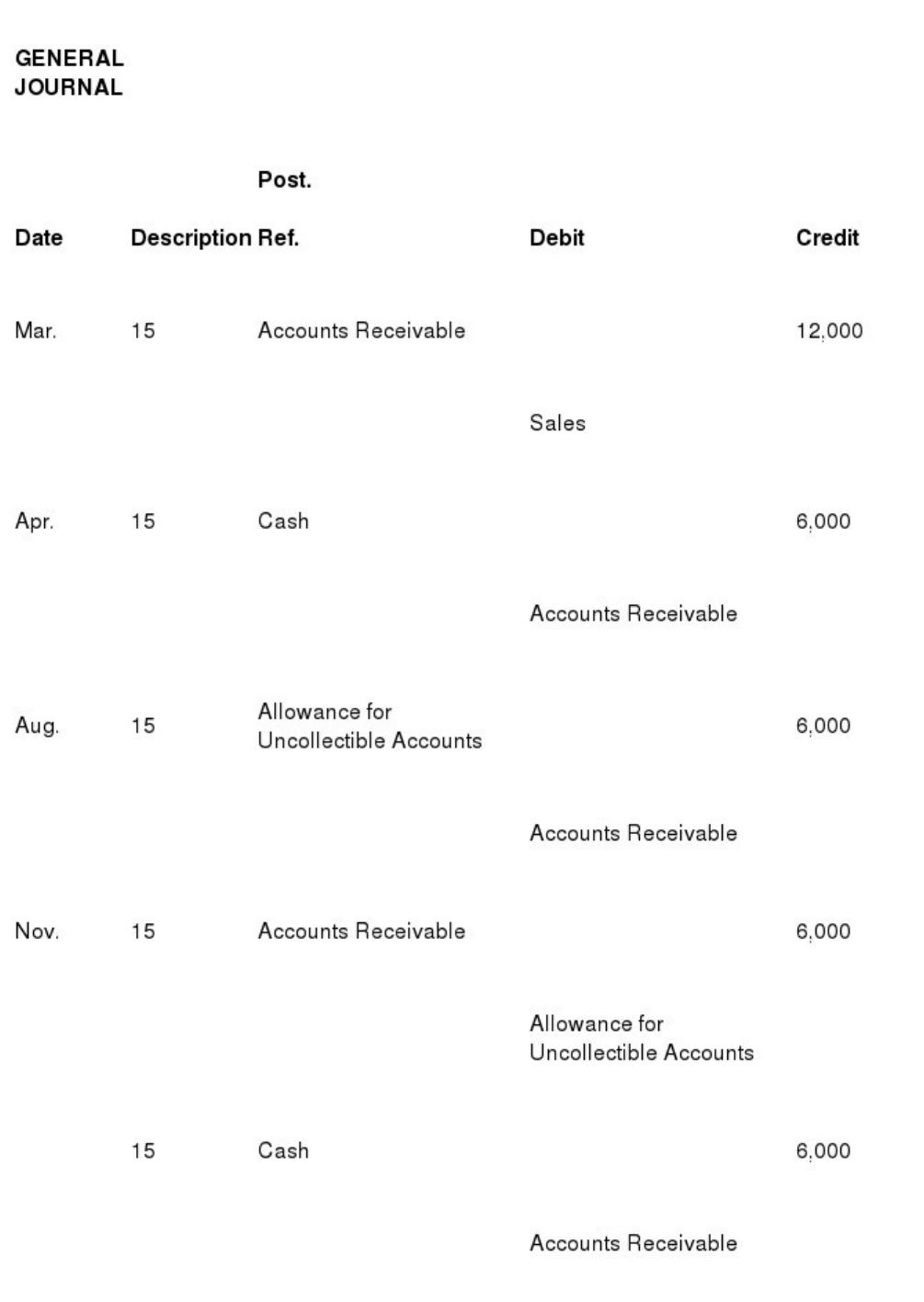

Assuming that the allowance method is being used, prepare journal entries to record the

following transactions. Omit explanations.

Mar. 15 Sold merchandise to Foster for $12,000 on account.

Apr. 15 Received $6,000 from Foster.

Aug. 15 Wrote off Foster’s account as uncollectible.

Nov. 15 Unexpectedly received payment in full from Foster.

On December 31, 20×5, the balance sheet of the Nowicki Company reported 2,000

bonds outstanding with a face value of $1,000,000 and a related unamortized discount

of $70,000. The bonds are convertible at the rate of 25 shares of common stock for each

$1,000 bond. On January 1, 20×6 , the bondholders presented $800,000 of the bonds for

conversion. The entry to record this conversion contained a credit to Additional Paid-in

Capital for $344,000. Calculate the par value per share of the common stock.

$20.00 [800,000 ‘“ ($70,000 x 0.8) = $744,000 ‘“ $344,000 = $400,000 ‚ (25 x 800)]

An accountant is responsible for the following activities: (1) receiving all cash; (2)

maintaining the general ledger; (3) maintaining the accounts receivable subsidiary

ledger that includes the individual records of each customer; (4) maintaining the

journals for recording sales, purchases, and cash receipts; and (5) preparing monthly

statements to be sent to customers. As a service to customers and employees, the

company allows the accountant to cash checks of up to $75 with money from the cash

receipts. When deposits are made, the checks are included in place of the cash receipts.

What weaknesses in internal control exist in this system?

Chao Corporation uses the accounts receivable aging method to account for

Uncollectible Accounts Expense. As of December 31, Chao’s accountant prepared the

following data about ending receivables: $40,000 was not yet due (1 percent expected

not to be collected), $20,000 was 1-60 days past due (4 percent expected not to be

collected), and $4,000 was over 60 days past due (8 percent expected not to be

collected). At December 31, Allowance for Uncollectible Accounts had a credit balance

prior to adjustment of $400. In the journal provided, prepare Chao’s end-of-period

adjustment for estimated uncollectible accounts. Also prepare the entry that would have

been made had the credit balance instead been a debit balance. Omit explanations