1) Earth Company, Fire Incorporated, and Wind Incorporated created a joint venture to

market their products on the internet. Earth owns 40% of the stock, Fire owns 45% of

the stock and Wind owns the remaining 15%. Which firms should report their joint

venture investments using the equity method?

A) Earth

B) Fire

C) Earth and Fire

D) Earth, Fire and Wind

2) Which one of the following operating segment information items is not directly

named by GAAP to be reconciled to consolidated totals?

A) Assets

B) Liabilities

C) Revenues

D) Profit or loss

3) The risk that interest payments will not be made, or that the face value of a bond is

not repaid when a bond matures is

A) interest rate risk

B) inflation risk

C) moral hazard

D) default risk

4) The following are transactions for the city of Clinton.

a.Borrowed $100,000 by issuing a one-year, 5% note, three months before year-end.

b.Accrued interest at year end, but did not pay the interest at year end.

c.Charges for services rendered of $2,500 were billed and collected immediately.

d.Incurred salary costs of $5,000, unpaid.

Required:

Analyze the above transactions by using the accounting equation for a governmental

fund.

5) In reference to estates, which of the following statements is correct?

A) An estate comes into existence at the death of an individual

B) If the deceased person had a valid will at the time of death, he or she is said to have

died intestate

C) The heir receiving the largest portion of the estate is typically appointed the executor

D) Claims may be made for up to seven years against an estate

6) Goldberg Corporation owned a 70% interest in Savannah Corporation on December

31, 2010, and Goldberg’s Investment in Savannah account had a balance of $3,900,000.

Savannah’s stockholders’ equity on this date was as follows:

Capital stock, $10 par value$3,000,000

Retained Earnings2,400,000

Total Stockholders’ Equity$5,400,000

On January 1, 2011, Savannah issues 80,000 new shares of common stock to Goldberg

for $16 each.

What is Goldberg’s percentage ownership in Savannah after Savannah issues its stock to

Goldberg?

A) 76.32%

B) 80.43%

C) 82.57%

D) 83.43%

7) Sadie Corporation’s stockholders’ equity at December 31, 2010 included the

following:

6% Preferred stock, $10 par value$1,000,000

Common stock, $1 par value10,000,000

Other paid-in capitalcommon4,000,000

Retained earnings 4,000,000

$19,000,000

Pilga Corporation purchased a 30% interest in Sadie’s common stock from other

shareholders on January 1, 2011 for $5,800,000. What was the book value of Pilga’s

investment in Sadie on January 1, 2011?

A) $5,400,000

B) $5,700,000

C) $7,120,000

D) $7,440,000

8) A(n) ________ in the riskiness of corporate bonds will ________ the price of

corporate bonds and ________ the yield on corporate bonds, all else equal

A) increase; increase; increase

B) increase; decrease; increase

C) decrease; increase; increase

D) decrease; decrease;decrease

9) Under the provisions of FASB Statement No. 141R, in a business combination, when

the fair value of identifiable net assets acquired exceeds the investment cost, which of

the following statements is correct?

A) A gain from a bargain purchase is recognized for the amount that the fair value of

the identifiable net assets acquired exceeds the acquisition price

B) The difference is allocated first to reduce proportionately (according to market

value) non-current assets, then to non-monetary current assets, and any negative

remainder is classified as a deferred credit

C) The difference is allocated first to reduce proportionately (according to market

value) non-current assets, and any negative remainder is classified as an extraordinary

gain

D) The difference is allocated first to reduce proportionately (according to market

value) non-current, depreciable assets to zero, and any negative remainder is classified

as a deferred credit

10) A decrease in the liquidity of corporate bonds, other things being equal, shifts the

demand curve for corporate bonds to the ________ and the demand curve for Treasury

bonds shifts to the ________

A) right; right

B) right; left

C) left; left

D) left; right

11) The additional incentive that the purchaser of a Treasury security requires to buy a

long-term security rather than a short-term security is called the

A) risk premium

B) term premium

C) tax premium

D) market premium

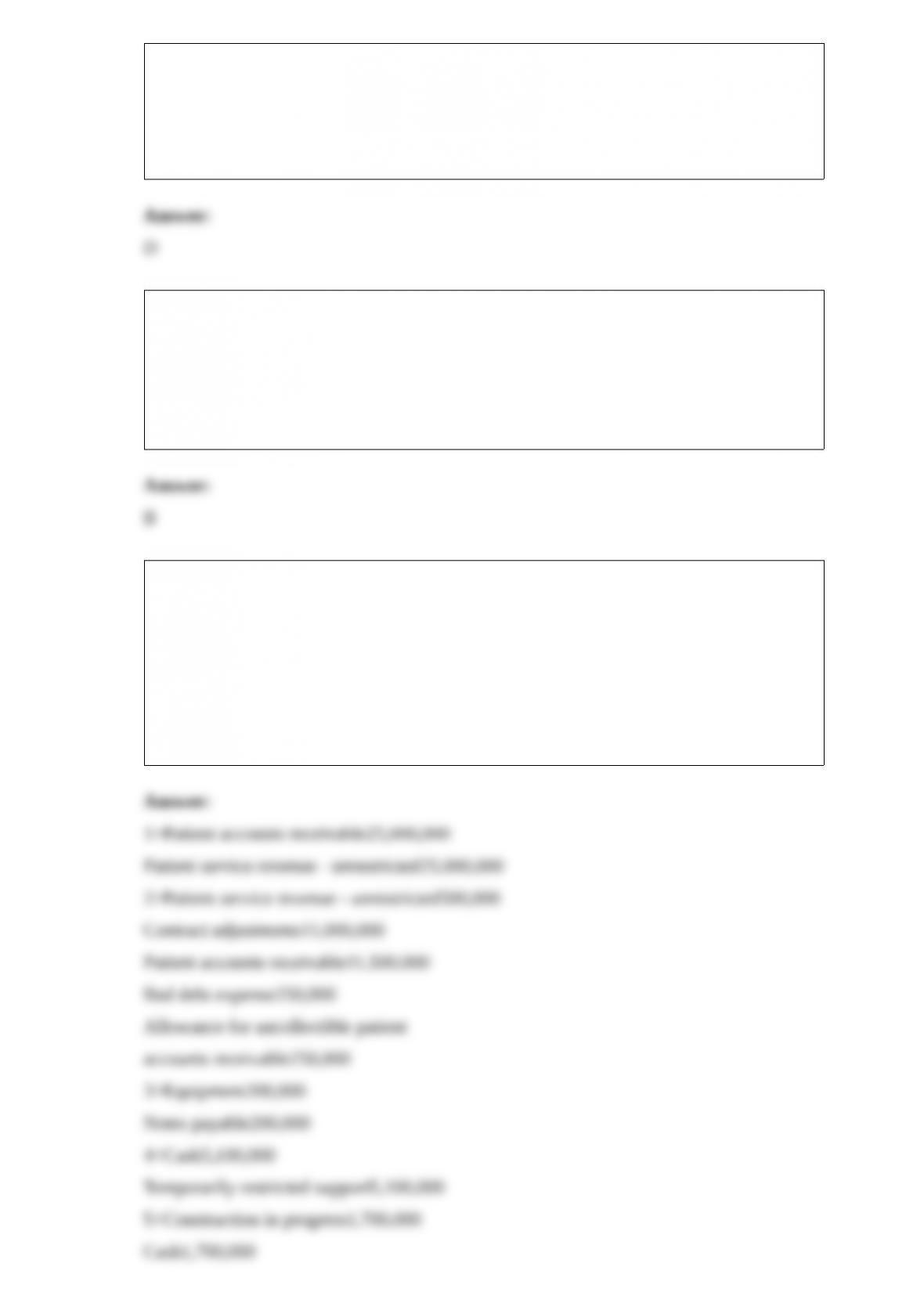

12) Record the following transactions for Porter Hospital, a private, nonprofit hospital:

1>Gross patient services revenues: $25,000,000. Billed to patients.

2>Included in the above revenues are: charity services, $500,000; contractual

adjustments, $11,000,000; and estimated uncollectible amounts, $250,000.

3>Purchased equipment by issuing a 5-year note for $200,000.

4>Received cash donations restricted for a capital building addition program,

$5,100,000.

5>Incurred and paid $1,700,000 of contractor billings for the capital building program.

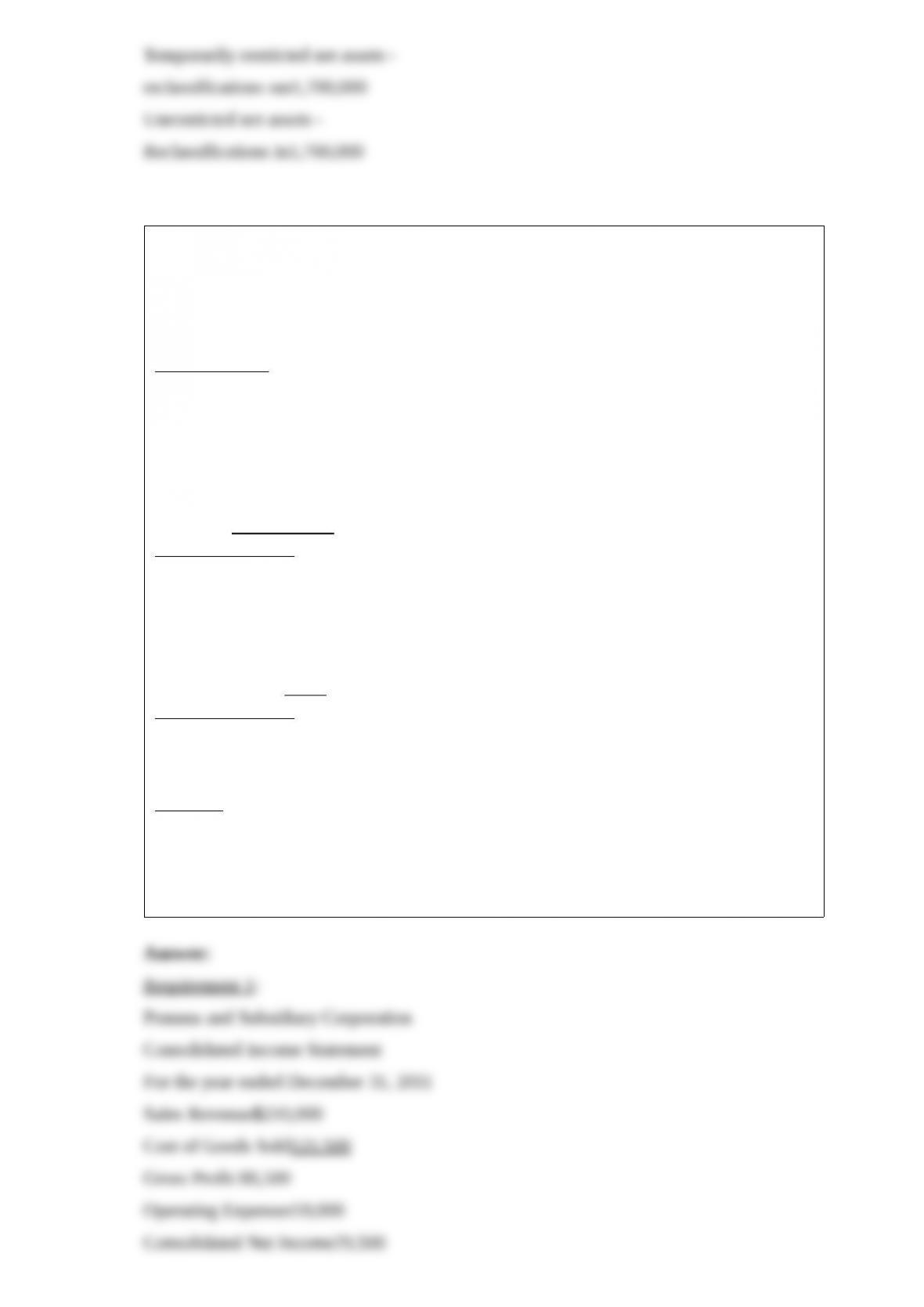

13) Pommu Corporation paid $78,000 for a 60% interest in Schtick Inc. on January 1,

2011, when Schtick’s Capital Stock was $80,000 and its Retained Earnings $20,000.

The fair values of Schtick’s identifiable assets and liabilities were the same as the

recorded book values on the acquisition date. Trial balances at the end of the year on

December 31, 2011 are given below:

PommuSchtick

Cash$4,500$20,000

Accounts Receivable24,00030,000

Inventory100,00070,000

Investment in Schtick78,000

Cost of Goods Sold71,50050,000

Operating Expenses22,00037,000

Dividends15,00010,000

$315,000$217,000

Liabilities$47,000$27,000

Capital stock, $10 par value100,00080,000

Additional Paid-in Capital11,000

Retained Earnings31,00020,000

Sales Revenue120,00090,000

Dividend Income6,000

$315,000$217,000

During 2011, Pommu made only two journal entries with respect to its investment in

Schtick. On January 1, 2011, it debited the Investment in Schtick account for $78,000

and on November 1, 2011, it credited Dividend Income for $6,000.

Required:

1>Prepare a consolidated income statement and a statement of retained earnings for

Pommu and Subsidiary for the year ended December 31, 2011 .

2>Prepare a consolidated balance sheet for Pommu and Subsidiary as of December 31,

2011 .

14) A cash distribution plan for the Sammi, Tammy, and Udd partnership was as

follows:

Priority

CreditorsSammiTammyUdd

First $250,000100%

Next $100,00070%30%

Next $150,00011/154/15

Remainder20%35%45%

Required:

If $850,000 of cash was distributed by the partnership, how much was received

respectively by the priority creditors, Sammi, Tammy, and Udd?

15) Adam, Bella, and Chris operate a partnership with a complex profit and loss sharing

agreement. The average capital balance for Adam, Bella and Chris on December 31,

2011 is $120,000, $270,000, and $340,000, respectively. A 6% interest allocation is

provided to each partner based on the average capital balance on December 31, 2011 .

Adam and Bella receive salary allocations of $40,000 and $50,000, respectively. If

partnership net income is above $160,000, after the salary allocations are considered

(but before the interest allocations are considered), Chris will receive a bonus of 10% of

the income (pre-salary and interest, but net of the bonus). All residual income is

allocated in the ratios of 2:2:6 to Adam, Bella, and Chris, respectively.

Required:

1>Prepare a schedule to allocate income or loss to the partners assuming that the

partnership incurs a net loss of $26,200 for 2011 .

2>Prepare a journal entry to distribute the partnership’s loss to the partners (assume that

an Income Summary account is used by the partnership).

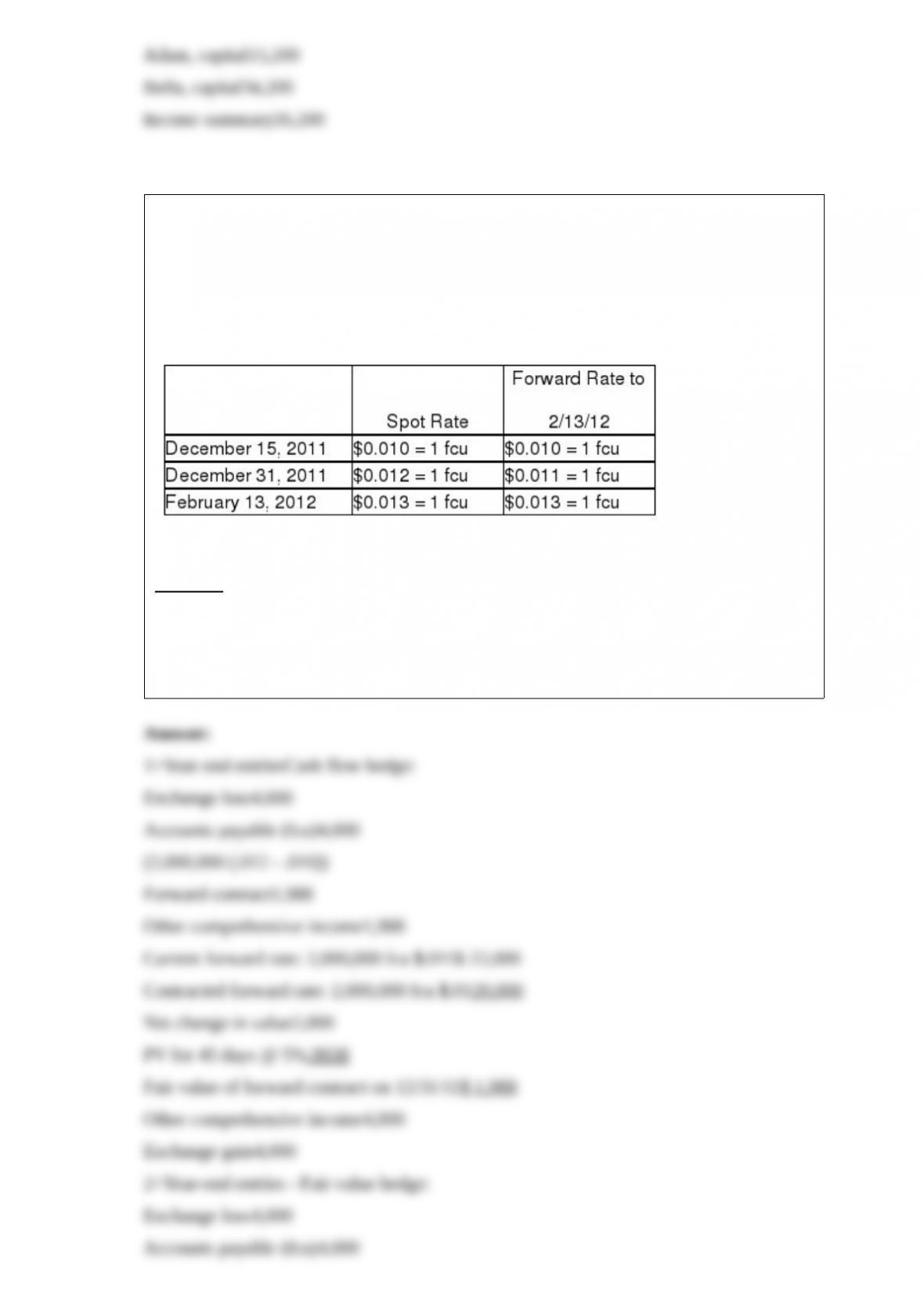

16) On December 15, 2011, Electronix Company purchased inventory from a foreign

supplier for 2,000,000 foreign currency units (fcu’s). Payment will be made on February

13, 2012 . On December 15, 2011, to hedge the transaction, Electronix signed a forward

contract to buy 2,000,000 fcu’s in 60 days. Electronix uses a discount rate of 5%

resulting in a 45-day present value factor of .9938. The forward contract will be settled

net. The related exchange rates are shown below:

On December 15, 2011, Electronix recorded a debit to Inventory and a credit to

Accounts Payable (fcu) for $20,000, using the current spot rate.

Required:

1> Show the required entries on December 31, 2011 if the hedge is a cash flow hedge.

Round to the nearest whole dollar.

2> Show the required entries on December 31, 2011 if the hedge is a fair value hedge.

Round to the nearest whole dollar.

17) Samantha’s Sporting Goods had net assets consisting of the following:

Book ValueFair Value

Cash150,000 150,000

Inventory820,000 960,000

Building and Fixtures330,000 310,000

Liabilities(90,000)(88,000)

Pedic Incorporated purchased Samantha’s Sporting Goods, and immediately dissolved

Samantha’s as a separate legal entity.

Requirement 1: If Samantha’s was purchased for $1,000,000 cash, prepare the entry

recorded by Pedic.

Requirement 2: If Samantha’s was purchased for $1,500,000 cash, prepare the entry

recorded by Pedic.