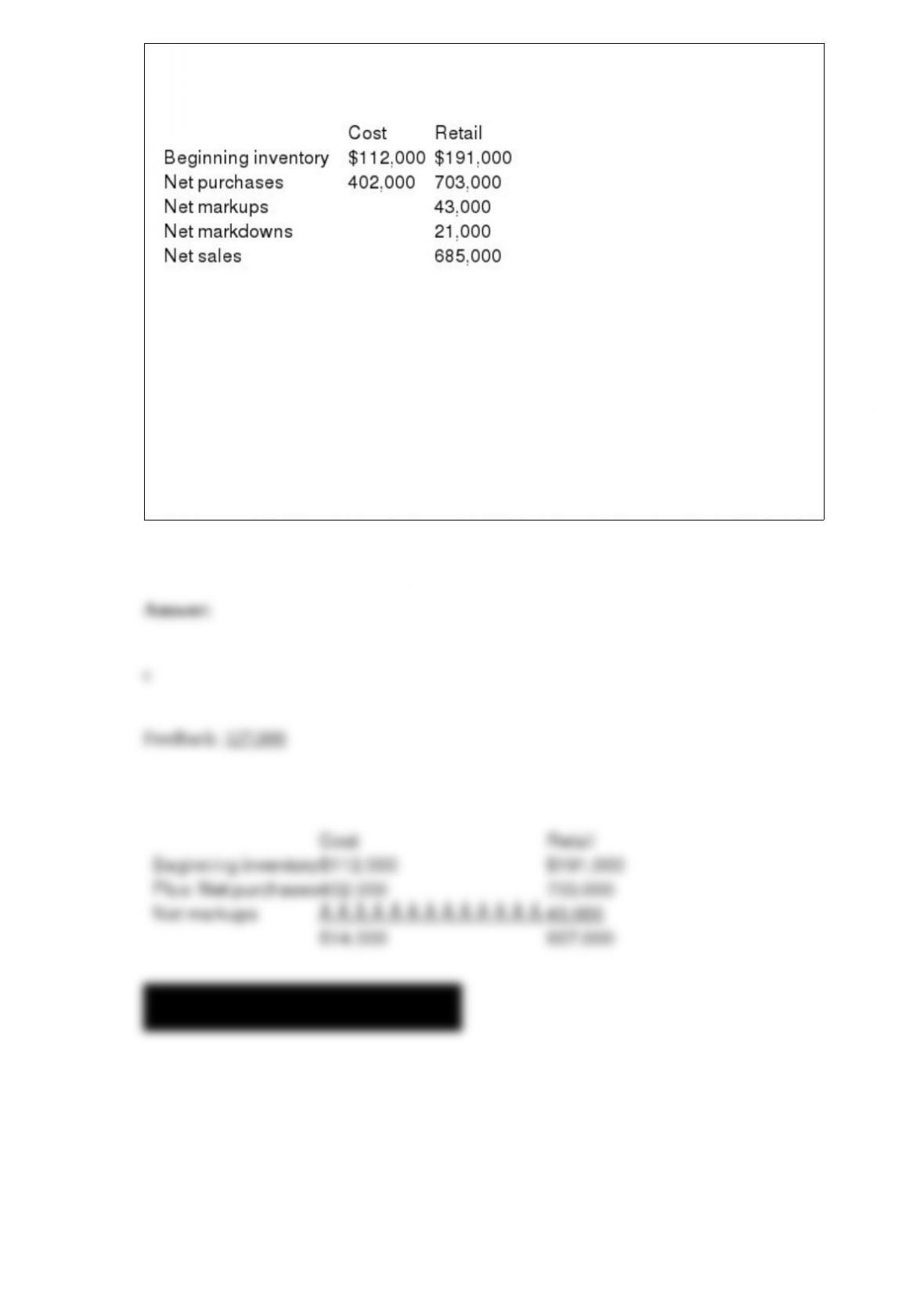

Clarabell Inc. uses the conventional retail method to estimate ending inventory. Cost

data for the most recent quarter is shown below:

To the nearest thousand, estimated ending inventory using the conventional retail

method is:

a. $163,000.

b. $124,000.

c. $127,000.

d. $136,000.

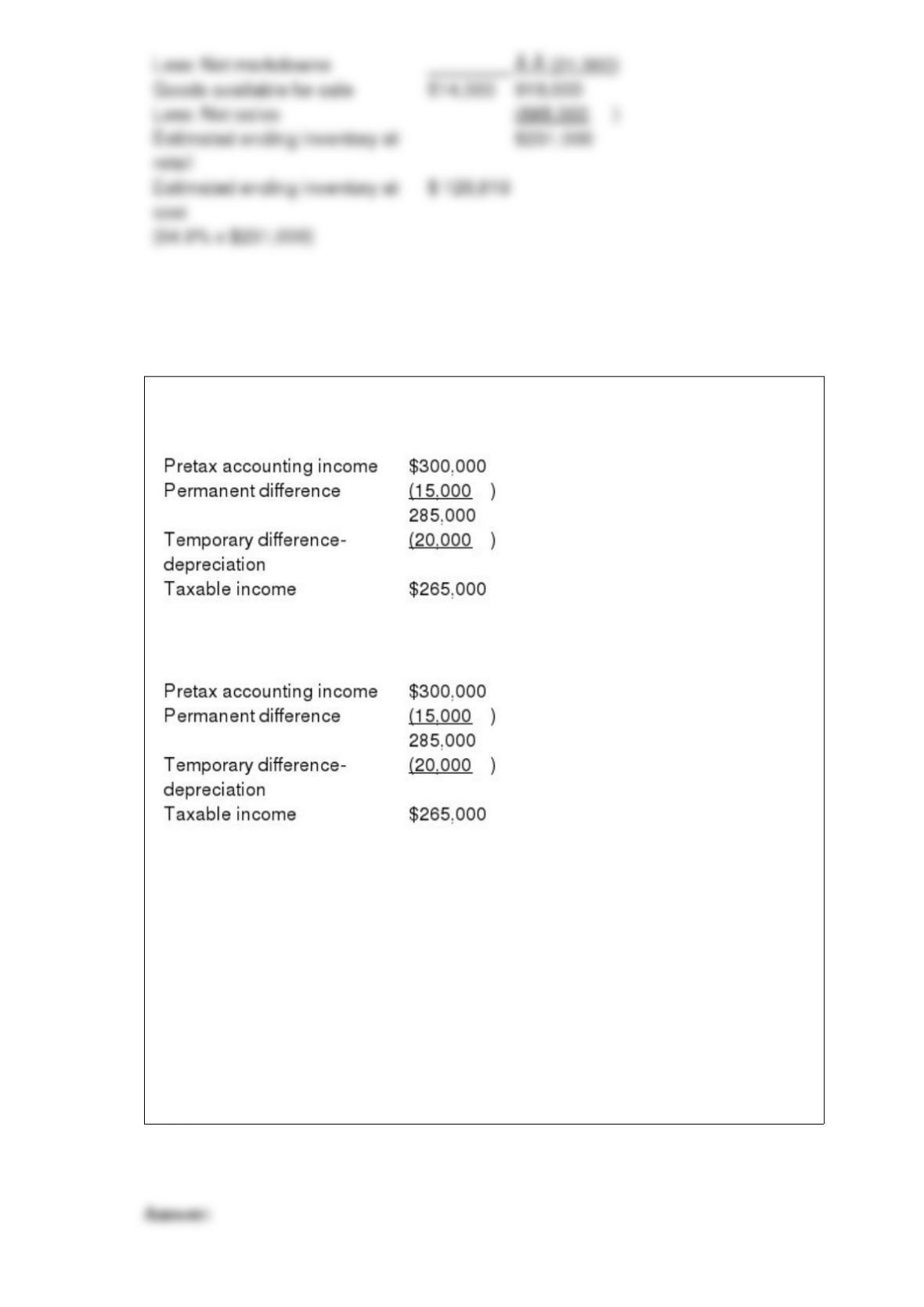

For its first year of operations, Tringali Corporation’s reconciliation of pretax

accounting income to taxable income is as follows:

Tringali’s tax rate is 40%. Assume that no estimated taxes have been paid.

Tringali’s tax rate is 40%.

What should Tringali report as its income tax expense for its first year of operations?

a. $120,000.

b. $114,000.

c. $106,000.

d. $8,000.

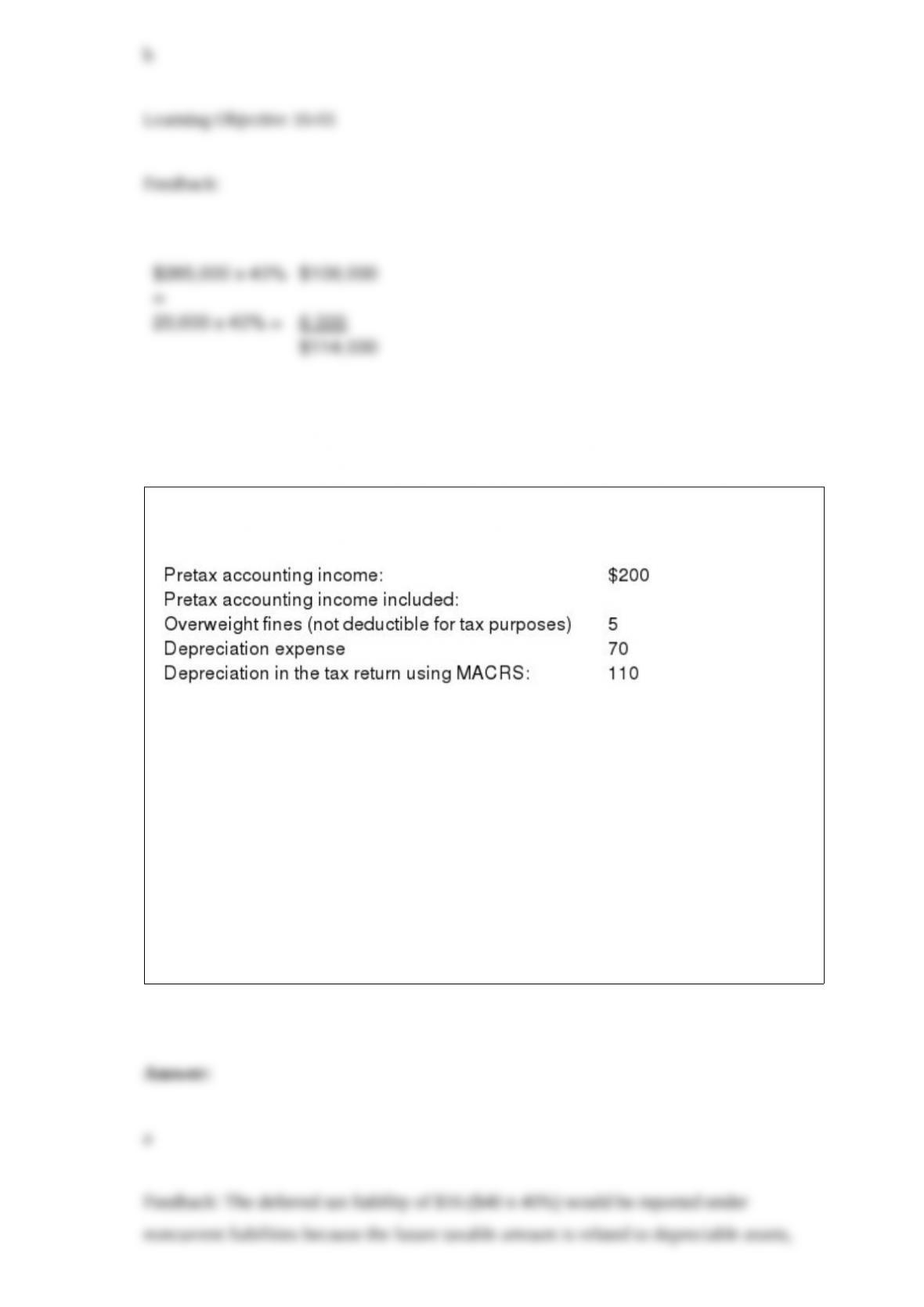

The following information relates to Franklin Freightways for its first year of

operations (data in millions of dollars):

The applicable tax rate is 40%. There are no other temporary or permanent differences.

Franklin’s balance sheet at the end of its first year would report:

a. A deferred tax liability of $16 among noncurrent liabilities.

b. A deferred tax liability of $16 among current liabilities.

c. A deferred tax asset of $16 among noncurrent assets.

d. A deferred tax asset of $16 among current assets.

On December 31, 2015, the Frisbee Company had 250,000 shares of common stock

issued and outstanding. On March 31, 2016, the company sold 50,000 additional shares

for cash. Frisbee’s net income for the year ended December 31, 2016, was $700,000.

During 2016, Frisbee declared and paid $80,000 in cash dividends on its nonconvertible

preferred stock. What is the 2016 basic earnings per share (rounded)?

a. $2.16.

b. $3.50.

c. $3.10.

d. $2.80.

When preferred stock is purchased by the issuing corporation at a price below the

original issue price and the stock is retired, the transaction:

a. Increases net income for the year.

b. Increases retained earnings.

c. Increases revenue for the year.

d. Increases paid-in capital share repurchase.

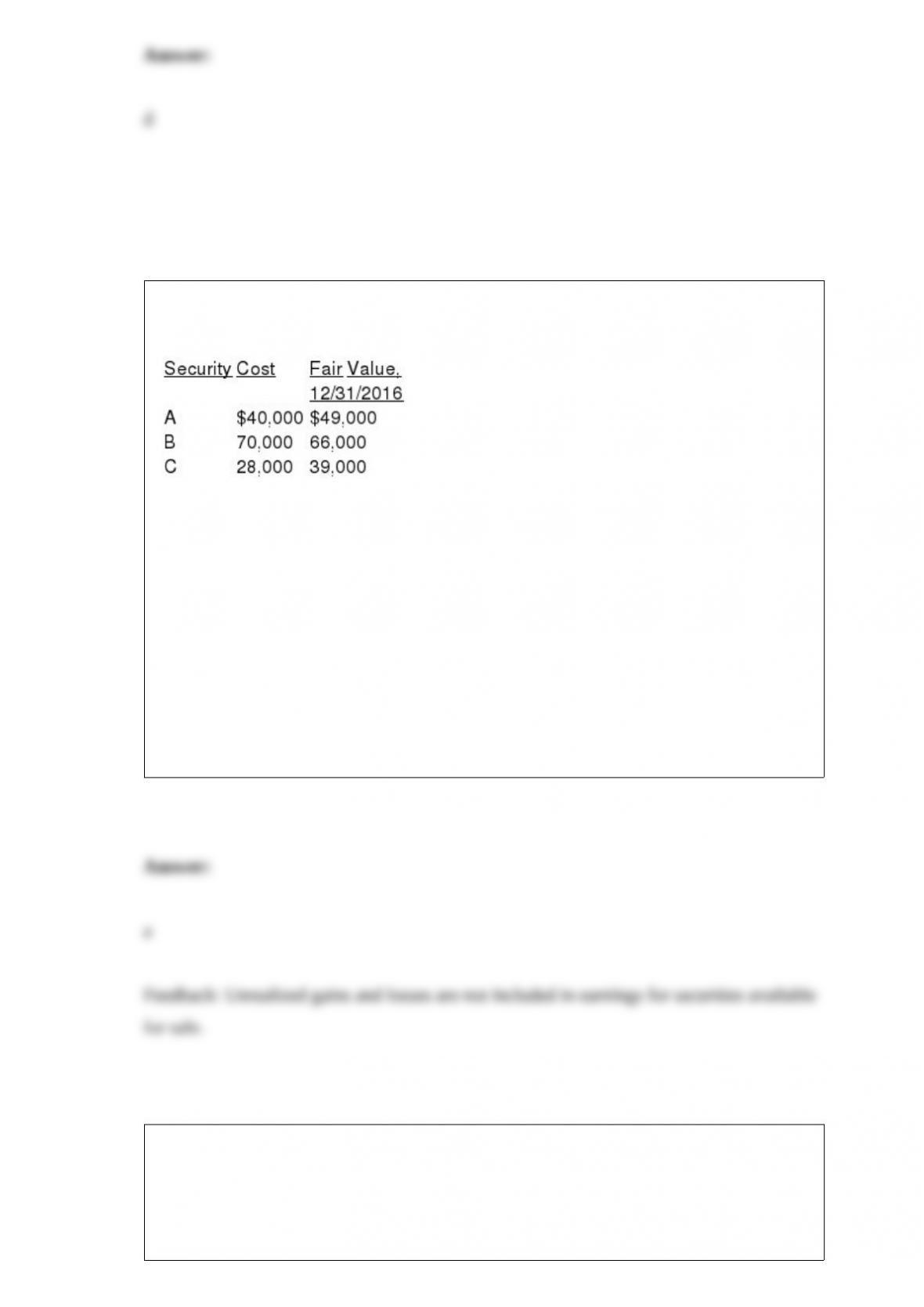

Jeremiah Corporation purchased securities during 2016 and classified them as securities

available for sale:

All declines are considered to be temporary. How much gain will be reported by

Jeremiah Corporation in the December 31, 2016, income statement relative to the

portfolio?

a. $0.

b. $16,000.

c. $20,000.

d. None of these answer choices is correct.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

sum-of-the-years’-digits method, depreciation for 2017 and book value at December 31,

2017, would be:

a. $19,200 and $30,800.

b. $17,600 and $26,400.

c. $19,200 and $28,800.

d. $17,600 and $32,400.

Which of the following is least likely to be a reason why a long-term construction

contract would qualify for revenue recognition over time?

a. The customer consumes the benefit of the seller’s work as it is performed.

b. The customer controls the asset as it is created.

c. The seller is creating an asset that has no alternative use to the seller, and the seller

has the legal right to receive payment for progress to date.

d. The seller is constructing an addition to property that is owned by the customer.

The core revenue principle states that

a. Companies recognize revenue when the earnings process is virtually complete and it

is probable that payments will be received.

b. Companies recognize revenue when goods or services are transferred to customers

for the amount the company expects to be entitled to receive in exchange for those

goods or services.

c. Companies recognize revenue when goods or services are transferred to the customer

and payments are received.

d. Companies recognize revenue when the goods or services are transferred to the

customer in an arm’s length transaction.

Cutter Enterprises purchased equipment for $72,000 on January 1, 2016. The equipment

is expected to have a five-year life and a residual value of $6,000. Using the

straight-line method, depreciation for 2017 and the equipment’s book value at

December 31, 2017, would be:

a. $14,400 and $43,200.

b. $28,800 and $37,200.

c. $13,200 and $39,600.

d. $13,200 and $45,600.

In its 2016 income statement, WME reported $440,000 for the cost of goods sold.

WME paid inventory suppliers $380,000 in 2016, and its inventory balance decreased

by $41,000 during the year. In its reconciliation schedule, WME should:

Each year, White Mountain Enterprises (WME) prepares a reconciliation schedule that

compares its income statement with its statement of cash flows on both the direct and

indirect method bases.

a. Show a $19,000 positive adjustment to net income under the indirect method for the

increase in accounts payable.

b. Show a $19,000 positive adjustment to net income under the indirect method for the

decrease in accounts payable.

c. Show a $19,000 negative adjustment to net income under the indirect method for the

increase in accounts payable.

d. Show a $19,000 negative adjustment to net income under the indirect method for the

decrease in accounts payable.

Preferred dividends are subtracted from earnings when computing basic earnings per

share whether or not the dividends are declared or paid if the preferred stock is:

a. Callable.

b. Convertible.

c. Participating.

d. Cumulative.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the most correct term.

On May 1, 2016, Bo Smith, proud father of newborn son Bobo, purchased $200,000 in

zero-coupon bonds that mature on May 1, 2036. The bonds pay no interest during the

period of time they are outstanding. The interest rate for such borrowings is at 9%.

Interest compounds annually.

Required: Calculate the price Bo paid for the bonds.

Give an example of a noncash financing and investing activity and explain when and

how it would be reported in the financial statements.

In 2014, Osgood Corporation purchased $4 million of 10-year municipal bonds at face

value. On December 31, 2016, the bonds had a market value of $3,600,000 and Osgood

reclassified the bonds from held to maturity to trading securities. Osgood’s December

31, 2016, balance sheet and the 2016 income statement would show the following:

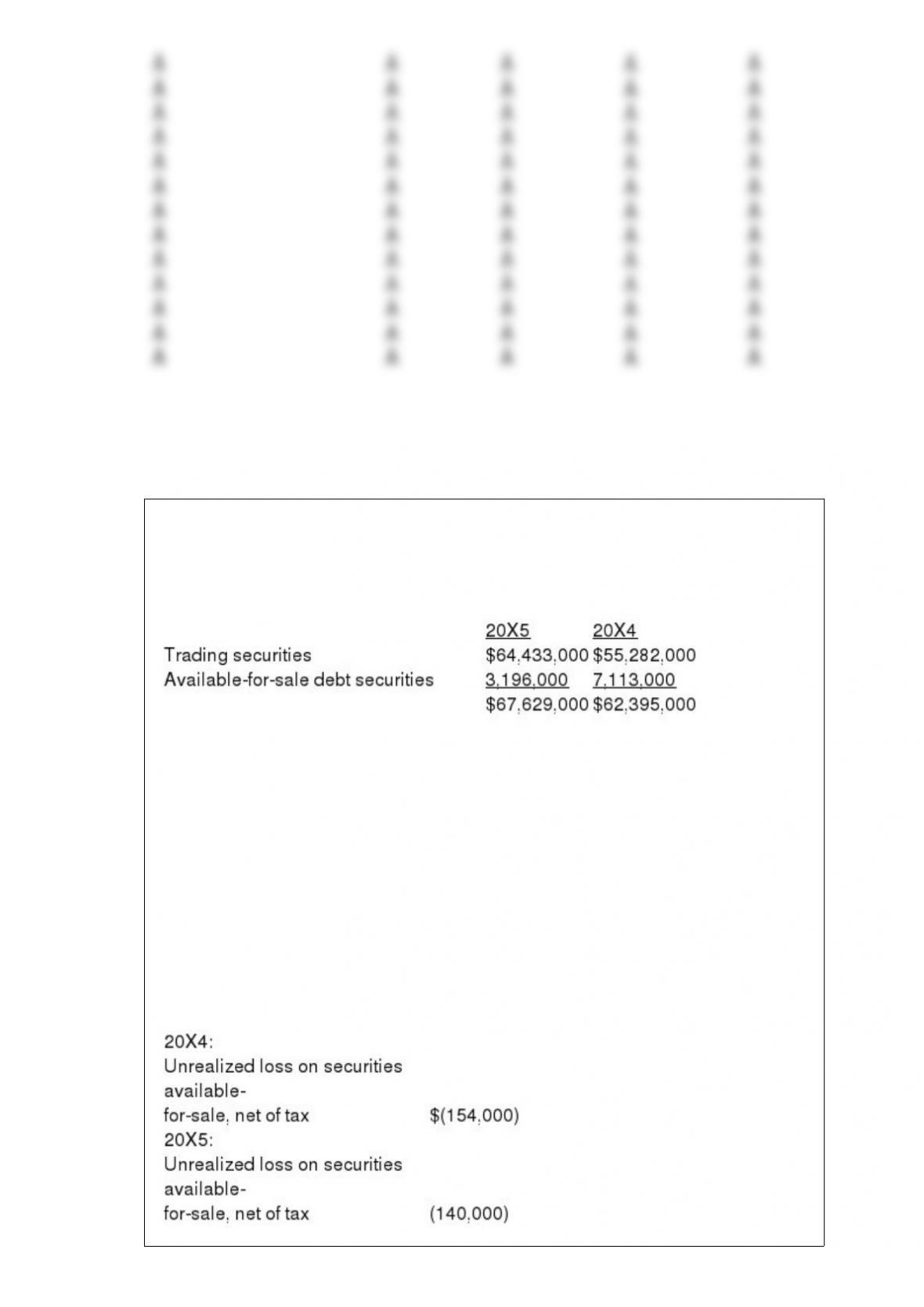

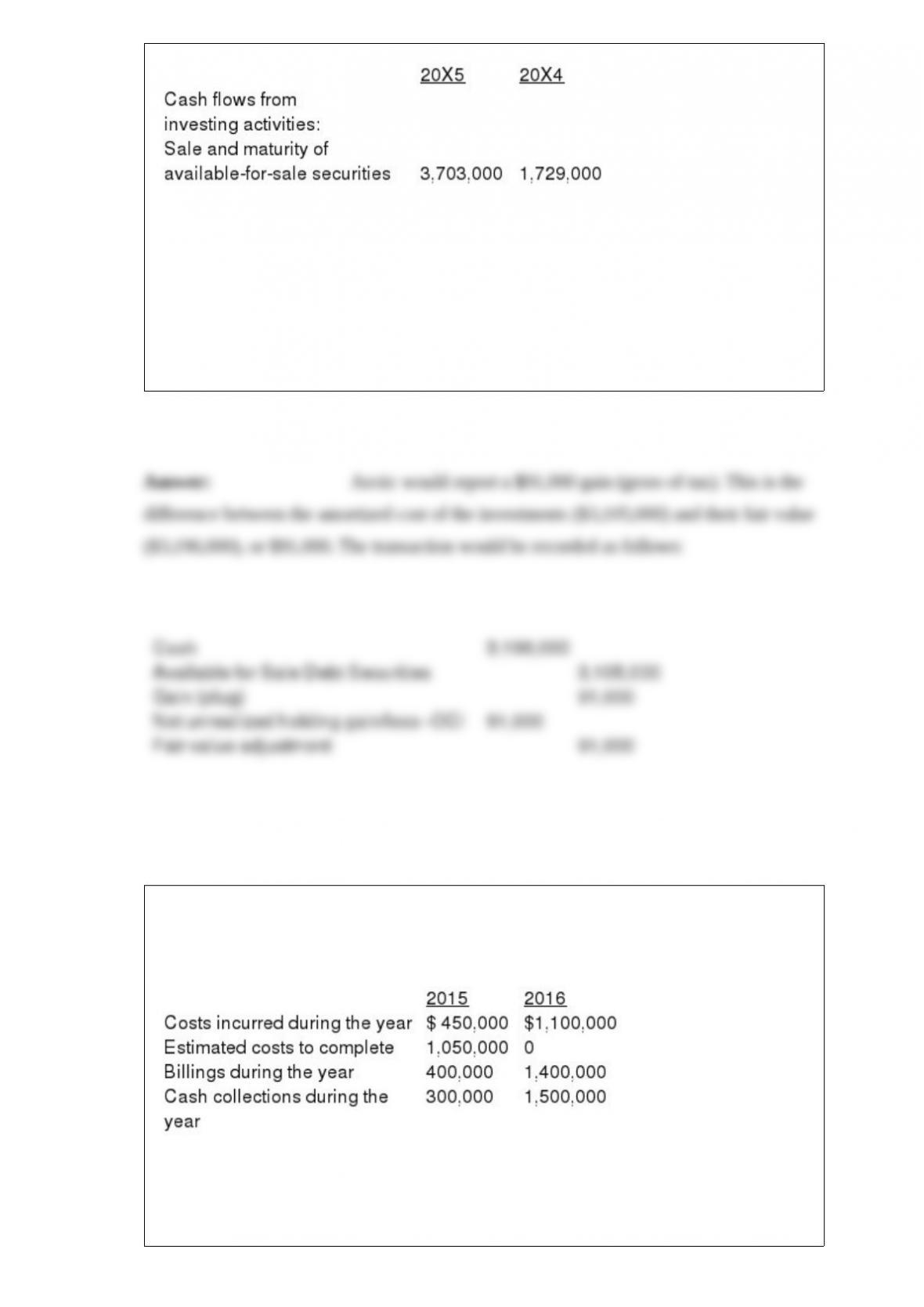

Arctic Cat Inc., the snowmobile manufacturer, reported the following in its 20X5

annual report to shareholders: NOTE B – SHORT-TERM INVESTMENTS

Short-term investments consist primarily of a diversified portfolio of municipal bonds

and money market funds and are classified as follows at March 31:

Trading securities consist of $54,608,000 and $41,707,000 invested in various money

market funds at March 31, 20X5 and 20X4, respectively, while the remainder of trading

securities and available-for-sale securities consist primarily of A-rated or higher

municipal bond investments. The amortized cost and fair value of debt securities

classified as available-for-sale was $3,105,000 and $3,196,000, at March 31, 20X5. The

unrealized gain on available-for-sale debt securities is reported, net of tax, as a separate

component of shareholders’ equity. Arctic Cat Inc.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

Years Ended March 31, Accumulated Other Comprehensive Income changed by the

following amounts:

In its 20X4 annual report, Arctic Cat disclosed, “The contractual maturities of

available-for-sale debt securities at March 31, 20X4, are $3,573,000 within one year

and $3,340,000 from one year through five years.”

What gain or loss would be realized if the available for sale securities on Arctic Cat’s

3/31/X5 balance sheet were sold immediately for their fair value? Show the journal

entry that would record the sale, and show a journal entry to record the effects of the

sale on their fair value adjustment at the end of the period (ignore taxes).

Beavis Construction Company was the low bidder on a construction project to build an

earthen dam for $1,800,000. The project was begun in 2015 and completed in 2016.

Cost and other data are presented below:

Assume that Beavis recognizes revenue on this contract over time according to

percentage of completion.

Required: Prepare all journal entries to record costs, billings, collections, and profit

recognition.

The following selected transactions relate to liabilities of Chicago Glass Corporation for

2016. Chicago’s fiscal year ends on December 31.

1> On January 15, Chicago received $7,000 from Henry Construction toward the

purchase of $66,000 of plate glass to be delivered on February 6.

2> On February 3, Chicago received $6,700 of refundable deposits relating to

containers used to transport glass components.

3> On February 6, Chicago delivered the plate glass to Henry Construction and

received the balance of the purchase price.

4> First quarter credit sales totaled $700,000. The state sales tax rate is 4% and the

local sales tax rate is 2%.

Required:

Prepare journal entries for the above transactions.