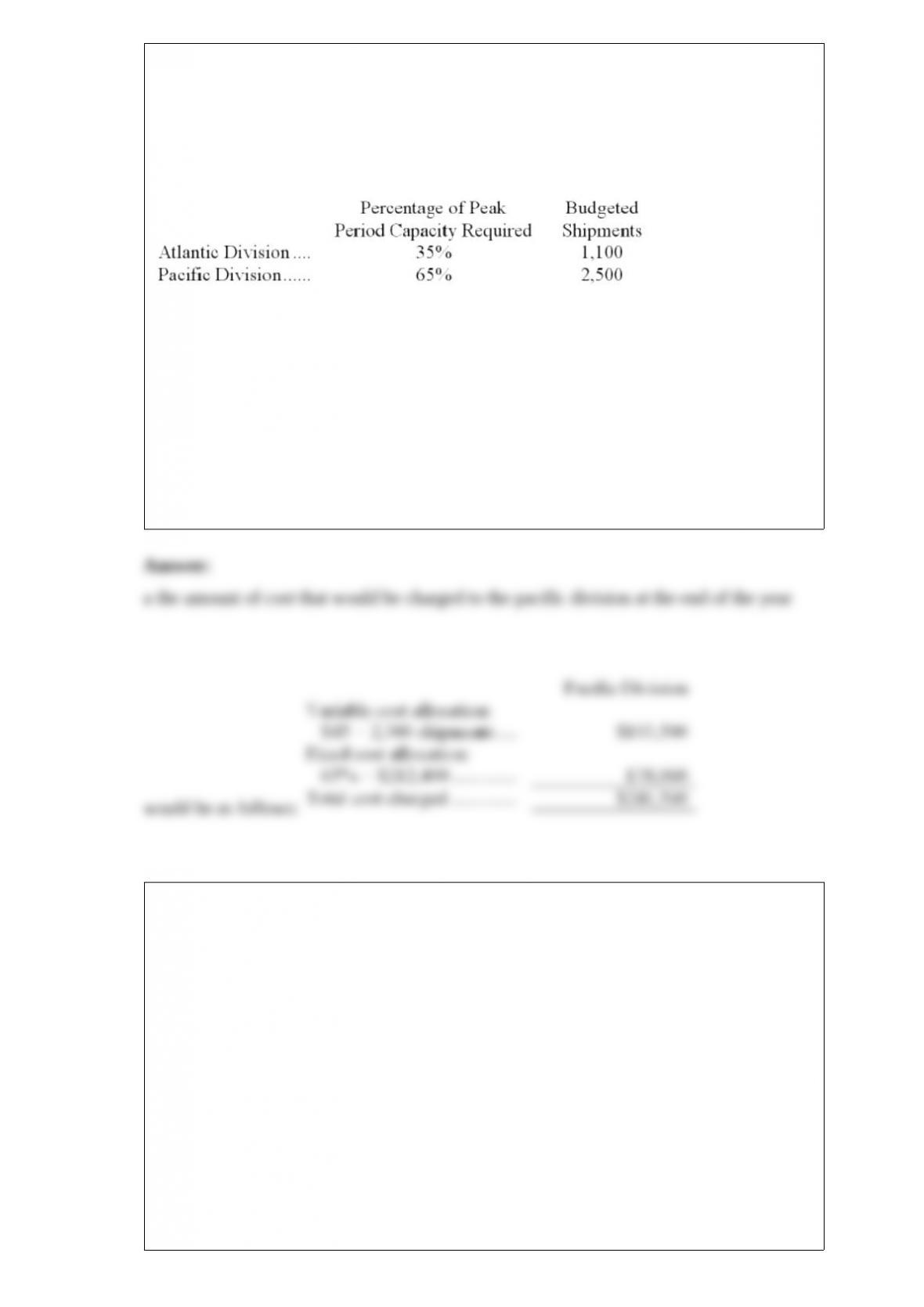

1) bunyard corporation has two operating divisions-an atlantic division and a pacific

division. the company’s logistics department services both divisions. the variable costs

of the logistics department are budgeted at $45 per shipment. the logistics department’s

fixed costs are budgeted at $212,400 for the year. the fixed costs of the logistics

department are determined based on peak-period demand.

at the end of the year, actual logistics department variable costs totaled $202,400 and

fixed costs totaled $223,900. the atlantic division had a total of 2,100 shipments and the

pacific division had a total of 2,300 shipments for the year. how much logistics

department cost should be charged to the pacific division at the end of the year for

performance evaluation purposes?

a.$241,560

b.$222,839

c.$251,335

d.$214,527

2) the management of haigler corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. the company’s controller

has provided an example to illustrate how this new system would work. in this example,

the allocation base is machine-hours and the estimated amount of the allocation base for

the upcoming year is 64,000 machine-hours. in addition, capacity is 80,000

machine-hours and the actual level of activity for the year is 66,300 machine-hours. all

of the manufacturing overhead is fixed and is $3,788,800 per year. for simplicity, it is

assumed that this is the estimated manufacturing overhead for the year as well as the

manufacturing overhead at capacity. it is further assumed that this is also the actual

amount of manufacturing overhead for the year.

if the company bases its predetermined overhead rate on the estimated amount of the

allocation base for the upcoming year, the predetermined overhead rate is closest to:

a.$59.20

b.$47.36

c.$57.15

d.$53.82

3) kaaihue detailing’s cost formula for its materials and supplies is $2,750 per month

plus $17 per vehicle. for the month of april, the company planned for activity of 95

vehicles, but the actual level of activity was 135 vehicles. the actual materials and

supplies for the month was $4,850.

the materials and supplies in the planning budget for april would be closest to:

a.$4,850

b.$5,045

c.$3,413

d.$4,365

4) assuming that the unit sales are unchanged, the total contribution margin will

decrease if:

a.fixed expenses increase

b.fixed expenses decrease

c.variable expense per unit increases

d.variable expense per unit decreases

5) process costing would be appropriate for each of the following except:

a.custom furniture manufacturing

b.oil refining

c.grain milling

d.newsprint production

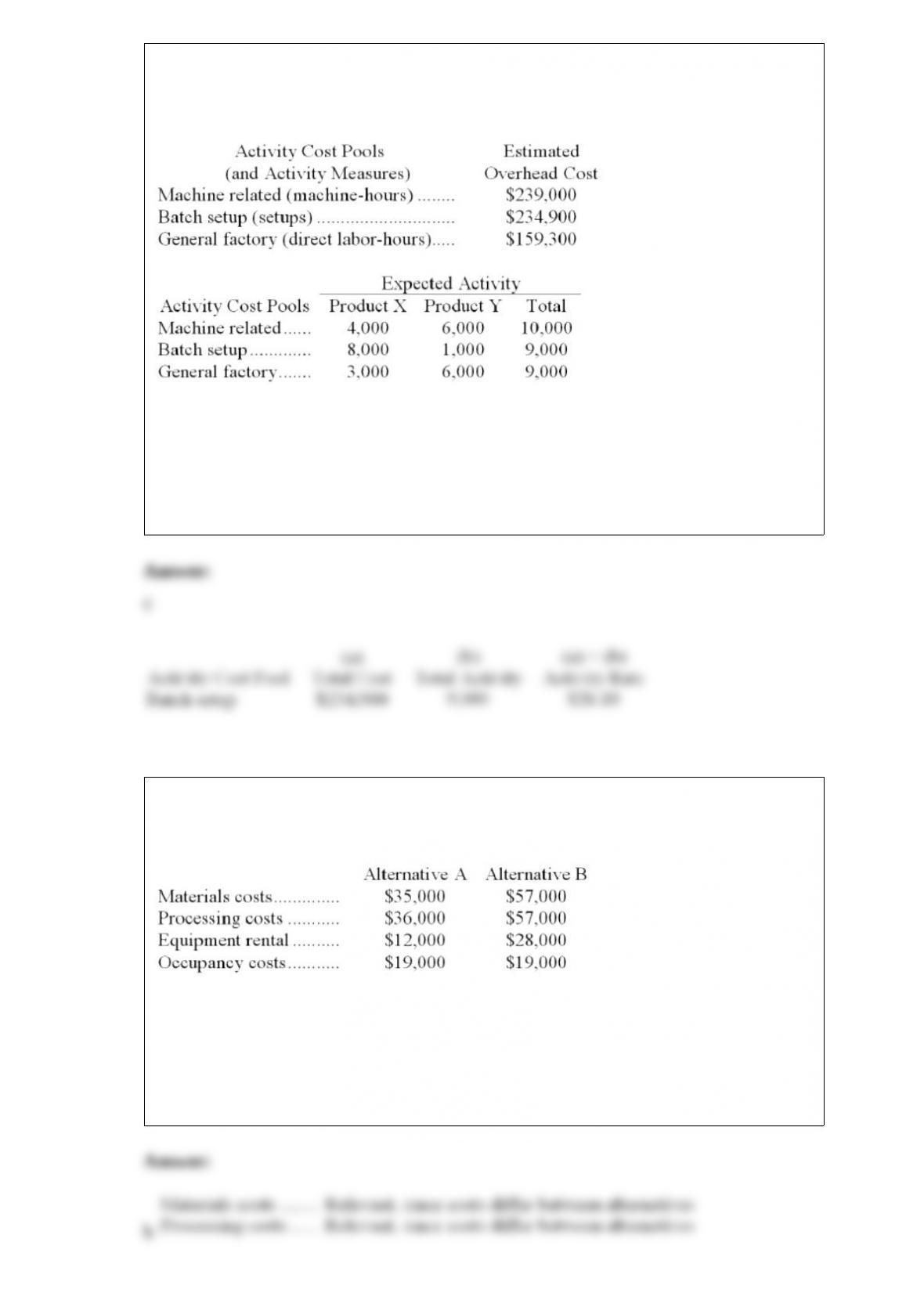

6) aujla corporation uses activity-based costing to determine product costs for external

financial reports. the company has provided the following data concerning its

activity-based costing system:

the activity rate for the batch setup activity cost pool is closest to:

a.$70.40

b.$29.40

c.$26.10

d.$234.90

7) mccubbin corporation is considering two alternatives: a and b. costs associated with

the alternatives are listed below:

are the materials costs and processing costs relevant in the choice between alternatives a

and b? (ignore the equipment rental and occupancy costs in this question.)

a.neither materials costs nor processing costs are relevant

b.both materials costs and processing costs are relevant

c.only processing costs are relevant

d.only materials costs are relevant

8) in a job-order costing system, the amount of overhead cost that has been applied to a

job that remains incomplete at the end of a period:

a.is deducted on the income statement as overapplied overhead

b.is closed to cost of goods sold

c.is transferred to finished goods at the end of the period

d.is part of the ending balance of the work in process inventory account

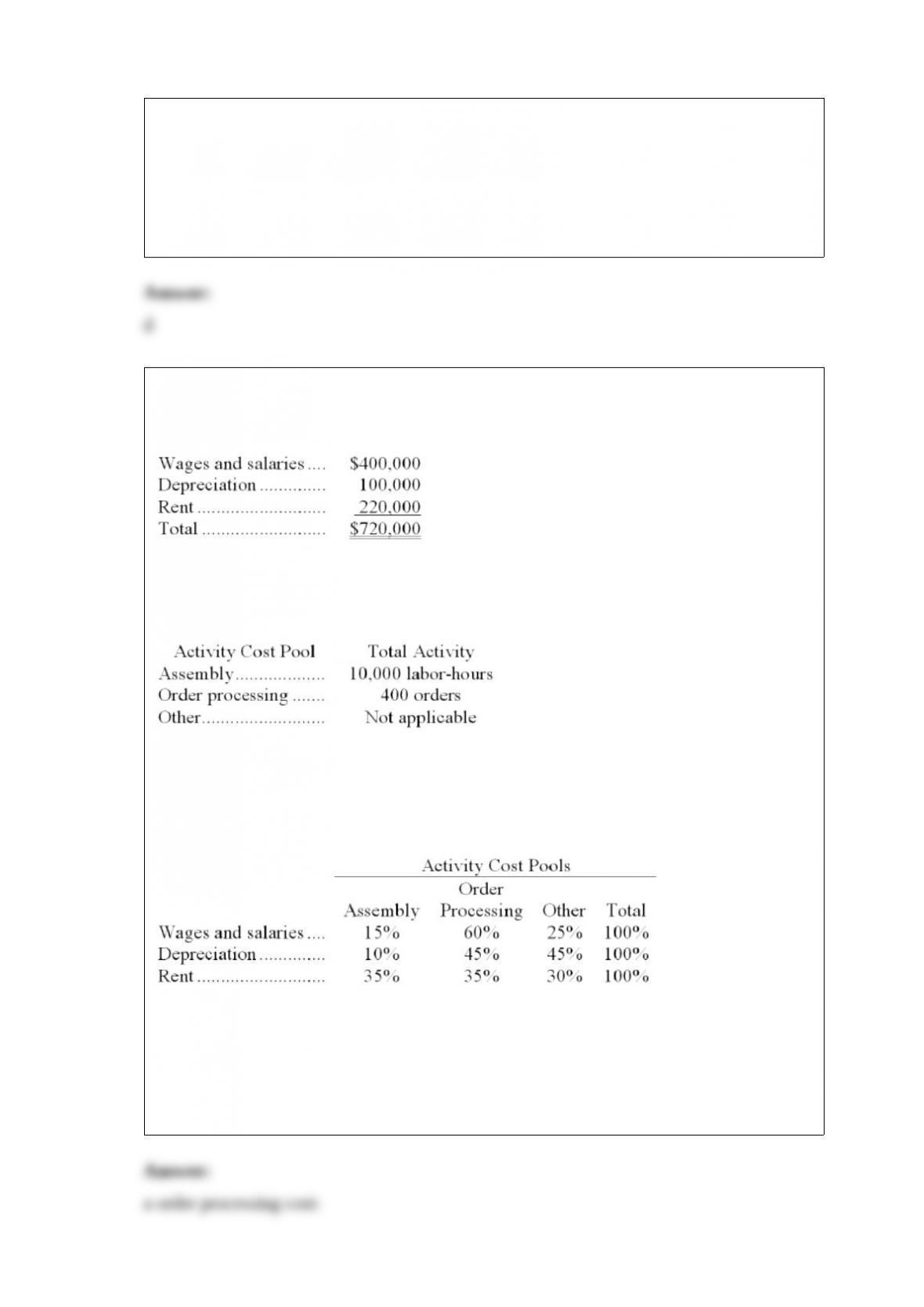

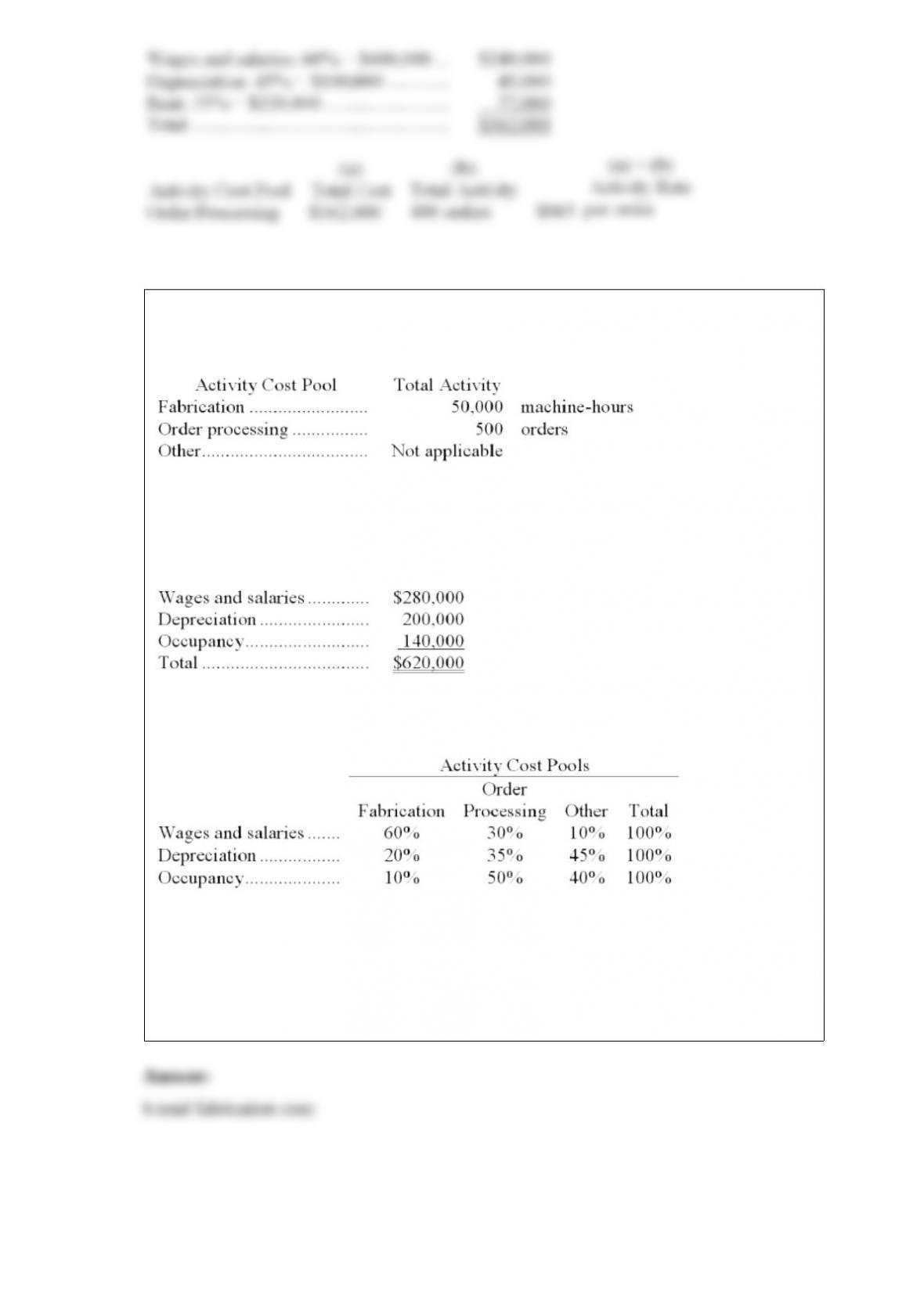

9) cuna corporation has provided the following data concerning its overhead costs for

the coming year:

the company has an activity-based costing system with the following three activity cost

pools and estimated activity for the coming year:

the other activity cost pool does not have a measure of activity; it is used to accumulate

costs of idle capacity and organization-sustaining costs.

the distribution of resource consumption across activity cost pools is given below:

the activity rate for the order processing activity cost pool is closest to:

a.$905 per order

b.$630 per order

c.$1,080 per order

d.$840 per order

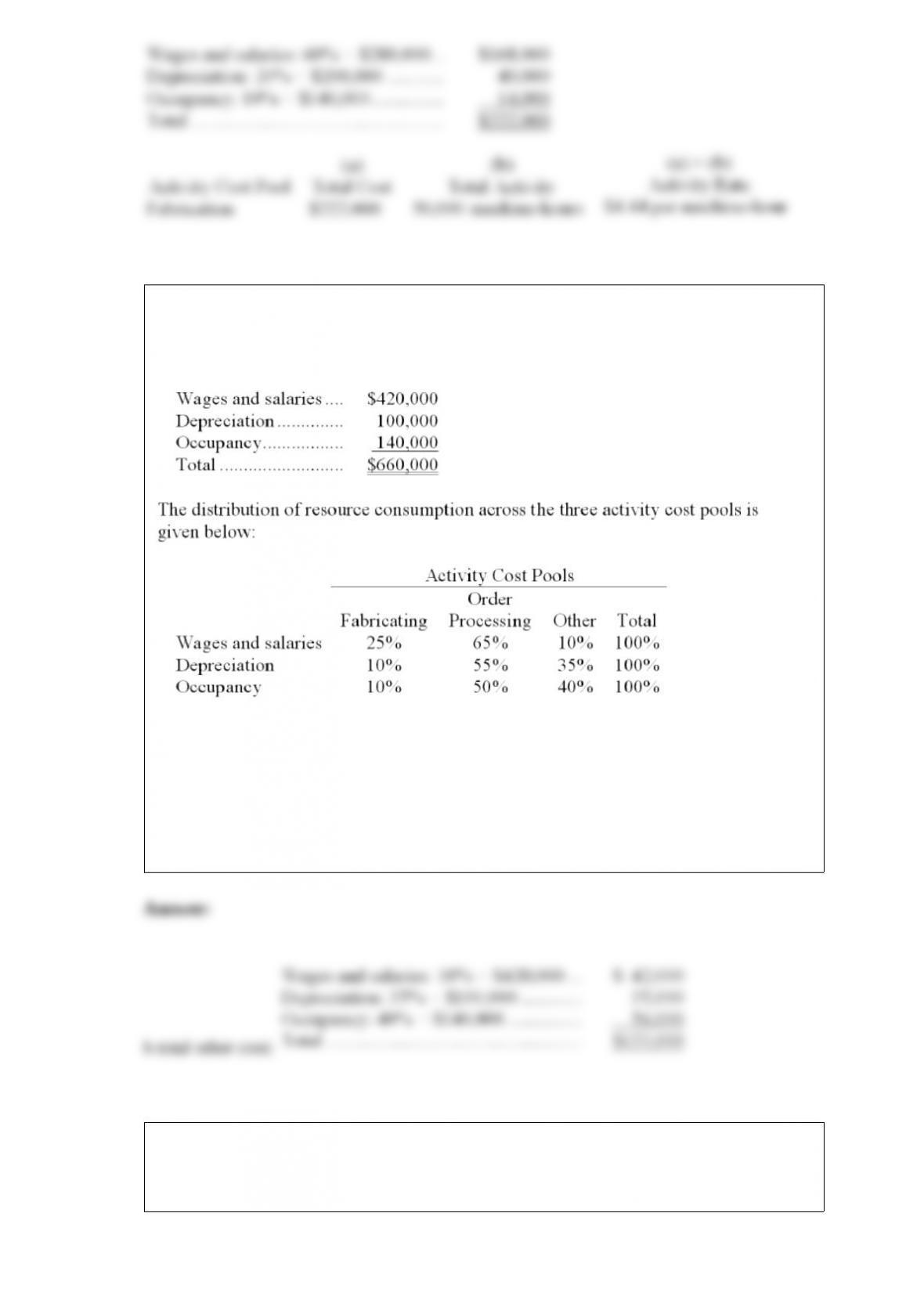

10) daniele corporation uses an activity-based costing system with the following three

activity cost pools:

the other activity cost pool is used to accumulate costs of idle capacity and

organization-sustaining costs.

the company has provided the following data concerning its costs:

the distribution of resource consumption across activity cost pools is given below:

the activity rate for the fabrication activity cost pool is closest to:

a.$3.72 per machine-hour

b.$4.44 per machine-hour

c.$7.44 per machine-hour

d.$1.24 per machine-hour

11) laib corporation uses an activity-based costing system with three activity cost pools.

the company has provided the following data concerning its costs:

how much cost, in total, would be allocated in the first-stage allocation to the other

activity cost pool?

a.$187,000

b.$133,000

c.$264,000

d.$66,000

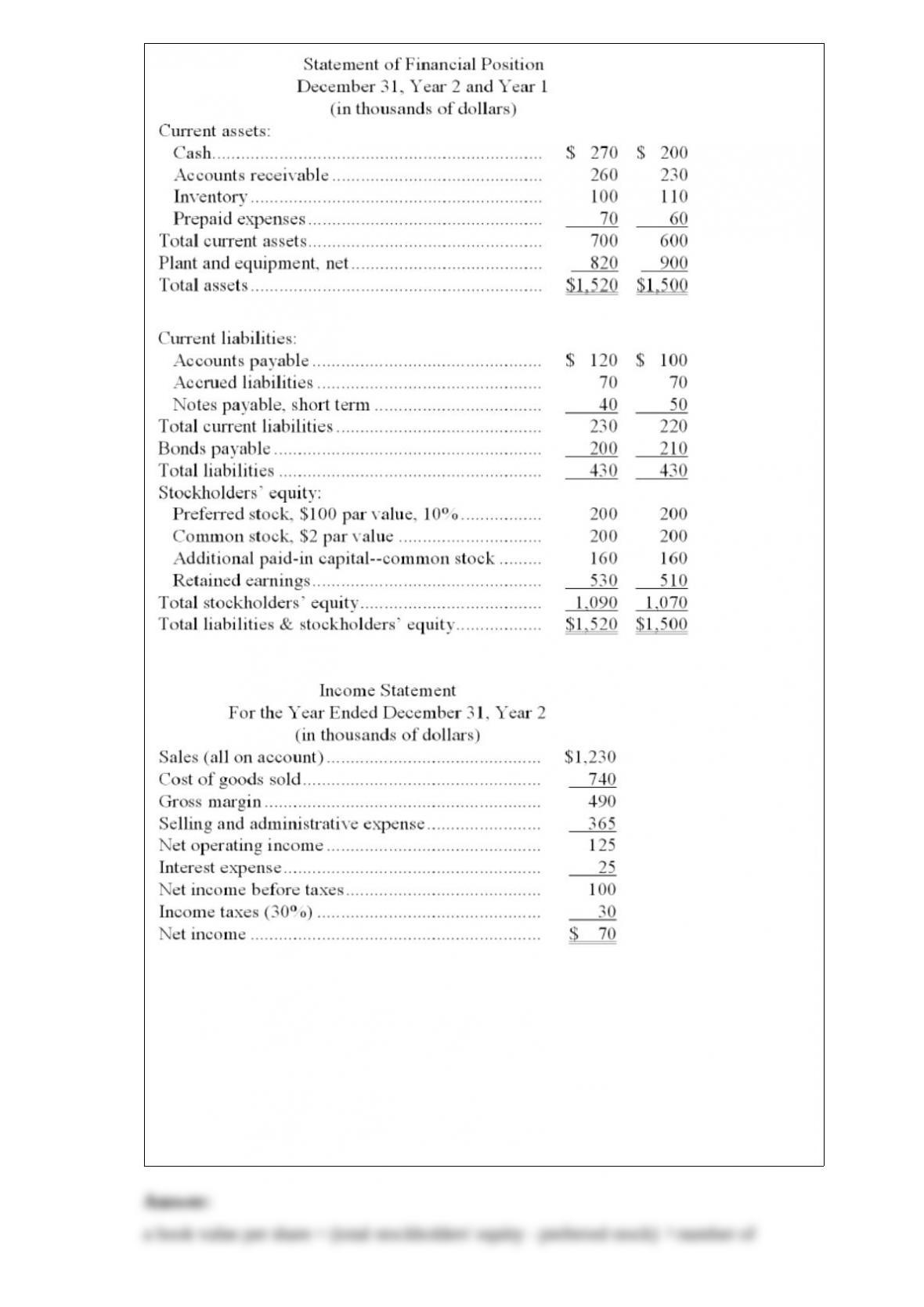

12) dadisman corporation’s most recent balance sheet and income statement appear

below:

dividends on common stock during year 2 totaled $30 thousand. dividends on preferred

stock totaled $20 thousand. the market price of common stock at the end of year 2 was

$6.75 per share.

the book value per share at the end of year 2 is closest to:

a.$8.90

b.$0.50

c.$15.20

d.$10.90

13) last year the house of orange had sales of $826,650, net operating income of

$81,000, and operating assets of $84,000 at the beginning of the year and $90,000 at the

end of the year. what was the company’s turnover rounded to the nearest tenth?

a.9.5

b.10.2

c.9.8

d.9.2

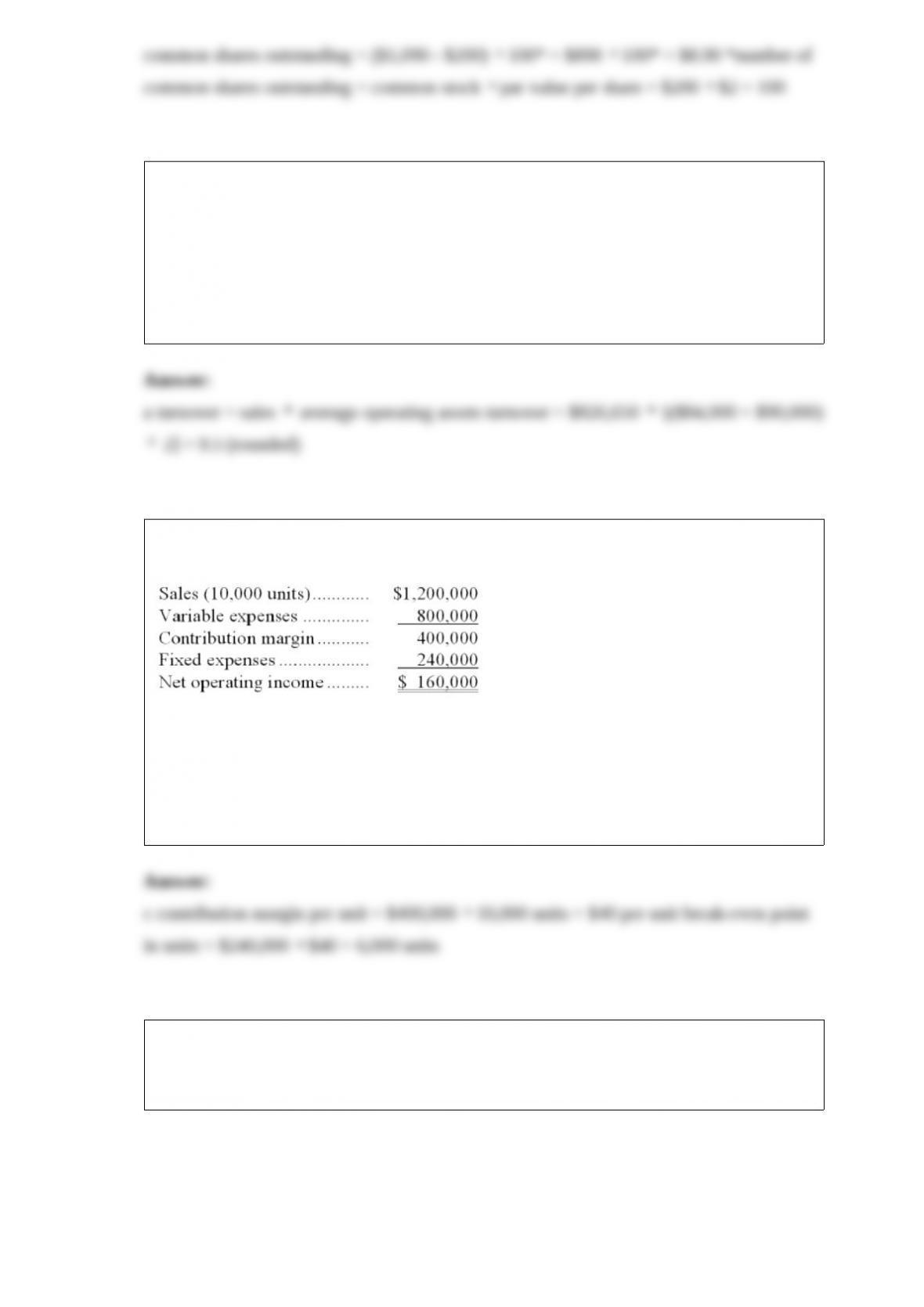

14) the following is last month’s contribution format income statement:

what is the company’s break-even in unit sales?

a.0 units

b.12,000 units

c.6,000 units

d.8,000 units

15) pfalzgraf corporation, a manufacturing company, has provided the following

financial data for january:

the company had no beginning or ending inventories.

the contribution margin for january was:

a.$14,000

b.$151,000

c.$91,000

d.$163,000

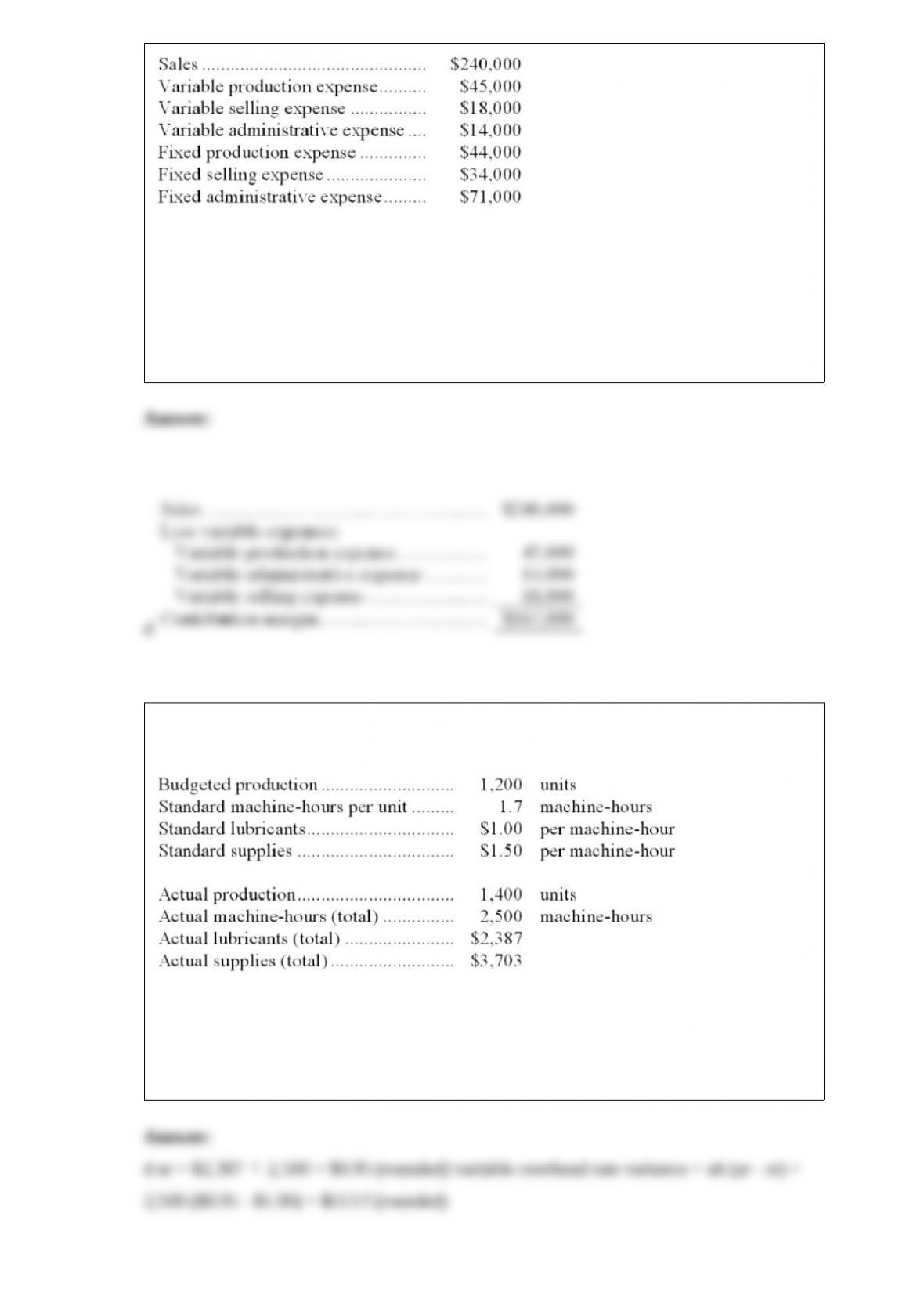

16) the following data have been provided by dicus corporation:

the variable overhead rate variance for lubricants is closest to:

a.$113 u

b.$120 u

c.$7 u

d.$113 f

17) vaccaro corporation produces and sells a single product. data concerning that

product appear below:

fixed expenses are $293,000 per month. the company is currently selling 3,000 units per

month. management is considering using a new component that would increase the unit

variable cost by $13. since the new component would increase the features of the

company’s product, the marketing manager predicts that monthly sales would increase

by 400 units. what should be the overall effect on the company’s monthly net operating

income of this change?

a.increase of $600

b.increase of $39,600

c.decrease of $600

d.decrease of $39,600