The initial cost of property, plant, and equipment includes all the identifiable

expenditures necessary to bring the asset to its desired condition and location for use.

LIFO usually provides a better match of revenue and expense than does FIFO.

A contract exists for purposes of revenue recognition if either the seller or customer has

performed an obligation specified by the contract.

If a license is acquired to use intellectual property for a 5-year period, revenue always is

recognized at the point in time the customer begins to benefit from the license.

Income from continuing operations sometimes includes gains from nonoperating

activities.

The exclusive right to display a symbol of product identification is a:

a. Patent.

b. Copyright.

c. Trademark.

d. Franchise.

Which of the following is not a provision of the Public Company Accounting Reform

and Investor Protection Act of 2002?

a. Corporate executive accountability.

b. Auditor rotation.

c. Retention of work papers.

d. All of the above are provisions of the Act.

Which of the following statements is true with regard to preferred stock (preference

shares)?

a. Most preferred stock (preference shares) is reported under U.S. GAAP as debt.

b. Most preferred stock (preference shares) is reported under IFRS as equity.

c. Under U.S. GAAP, mandatorily redeemable preferred stock is reported as equity.

d. Under IFRS, preferred stock dividends are reported in the income statement as

interest expense.

Tammy wants to buy a car that costs $10,000 and wishes to know the amount of the

monthly payments, which will be made at the first of the month, with interest of 12%

on the unpaid balance. She should use a table for the:

a. Present value of 1.

b. Present value of an ordinary annuity of 1.

c. Present value of an annuity due of 1.

d. Future value of an annuity due of 1.

A sale on account would be recorded by:

a. Debiting revenue.

b. Crediting assets.

c. Crediting liabilities.

d. Debiting assets.

On July 1, 2016, Cromartie Furniture established a $150 petty cash fund. A check for

$150 was made out to the petty cash custodian. During July, the petty cash custodian

paid the following bills from the petty cash fund:

At the end of July the petty cash fund was replenished. The journal entry to establish

the petty cash fund includes:

a. A credit to petty cash and a debit to cash for $150.

b. A debit to petty cash and a credit to cash for $150.

c. A credit to cash and a debit to various expenses for $126.

d. A credit to petty cash and a debit to various expenses for $126.

The following disclosure note appeared in a recent annual report to stockholders of Dell

Inc., the computer manufacturer: “Net revenue includes sales of hardware, software and

peripherals, and services (including extended service contracts and professional

services). These products and services are sold either separately or as part of a

multiple-element arrangement. Dell allocates fees from multiple-element arrangements

to the elements based on the relative fair value of each element, which is generally

based on the relative list price of each element. For sales of extended warranties with a

separate contract price, Dell defers revenue equal to the separately stated price.

Revenue associated with undelivered elements is deferred and recorded when delivery

occurs. Product revenue is recognized, net of an allowance for estimated returns, when

both title and risk of loss transfer to the customer, provided that no significant

obligations remain. Revenue from extended warranty and service contracts, for which

Dell is obligated to perform, is recorded as deferred revenue and subsequently

recognized over the term of the contract or when the service is completed. Revenue

from sales of third-party extended warranty and service contracts, for which Dell is not

obligated to perform, is recognized on a net basis at the time of sale.” Briefly explain

why Dell Computer recognizes revenue at different times for (a) product sales, (b)

extended warranty and service contracts for which Dell is obligated to perform, and (c)

extended warranty and service contracts for which a third party is obligated to perform.

Prior years’ financial statements are restated under the:

a. Current approach.

b. Prospective approach.

c. Retrospective approach.

d. None of these answer choices is correct.

In determining cash flows from operating activities (indirect method), adjustments to

net income should not include:

a. An addition for depreciation expense.

b. An addition for bond discount amortization.

c. An addition for a gain on sale of equipment.

d. An addition for patent amortization.

One of the four criteria for a capital lease specifies that the present value of the

minimum lease payments be equal to or greater than:

a. 90% of the cost of the asset.

b. 75% of the fair value of the asset.

c. 90% of the fair value of the asset.

d. 75% of the cost of the asset.

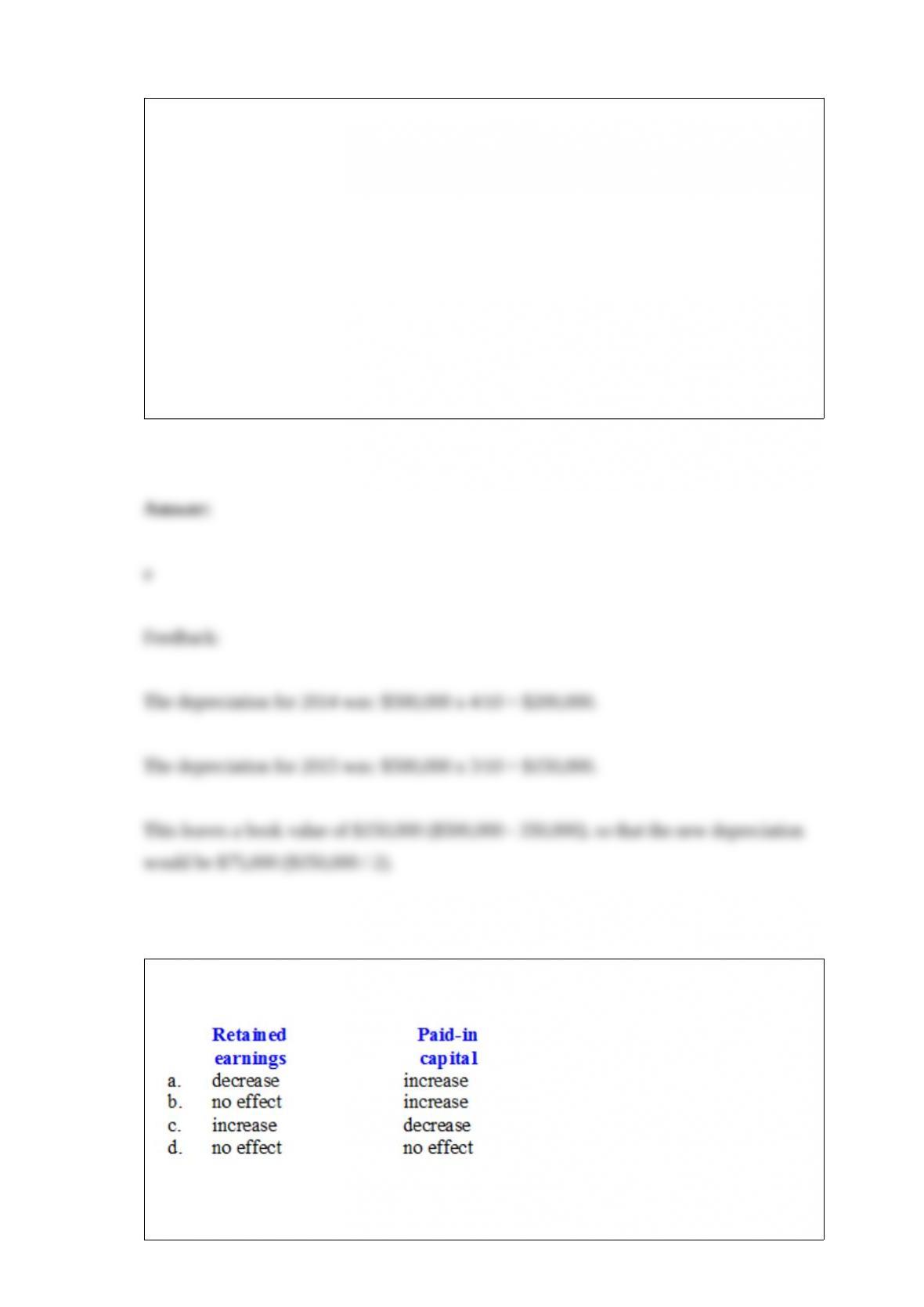

Murgatroyd Co. purchased equipment on January 1, 2014, for $500,000, estimating a

four-year useful life and no residual value. In 2014 and 2015, Murgatroyd depreciated

the asset using the sum-of-years’-digits method. In 2016, Murgatroyd changed to

straight-line depreciation for this equipment. What depreciation would Murgatroyd

record for the year 2016 on this equipment?

a. $ 75,000.

b. $125,000.

c. $150,000.

d. None of these answer choices are correct.

What is the effect of the declaration and subsequent issuance of a 10% stock dividend

on each of the following?

Retained Paid-in

earnings capital

a. decrease increase

b. no effect increase

c. increase decrease

d. no effect no effect

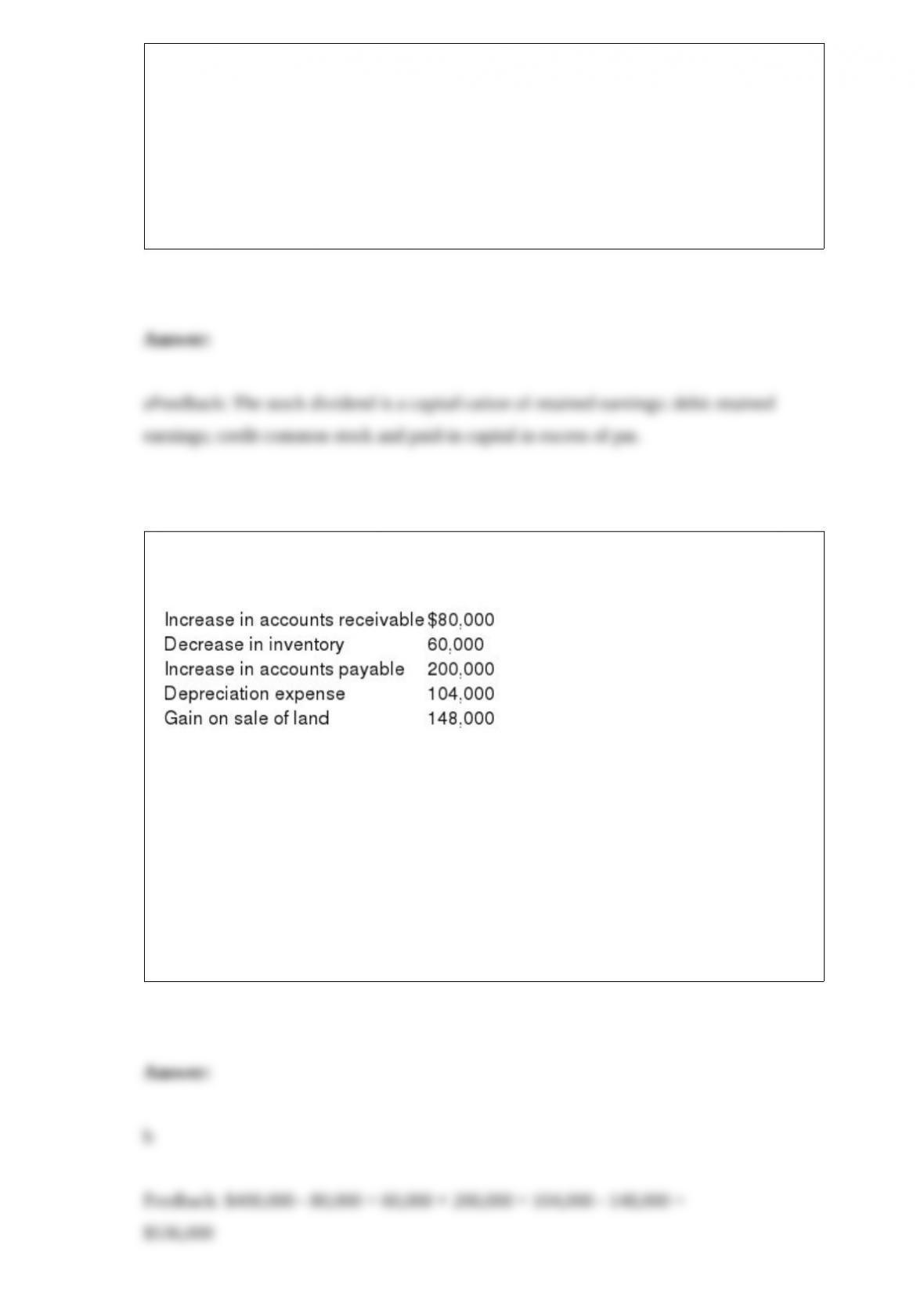

S Company reported net income for 2016 in the amount of $400,000. The company’s

financial statements also included the following:

What is net cash provided by operating activities under the indirect method?

a. $432,000.

b. $536,000.

c. $580,000.

d. $832,000.

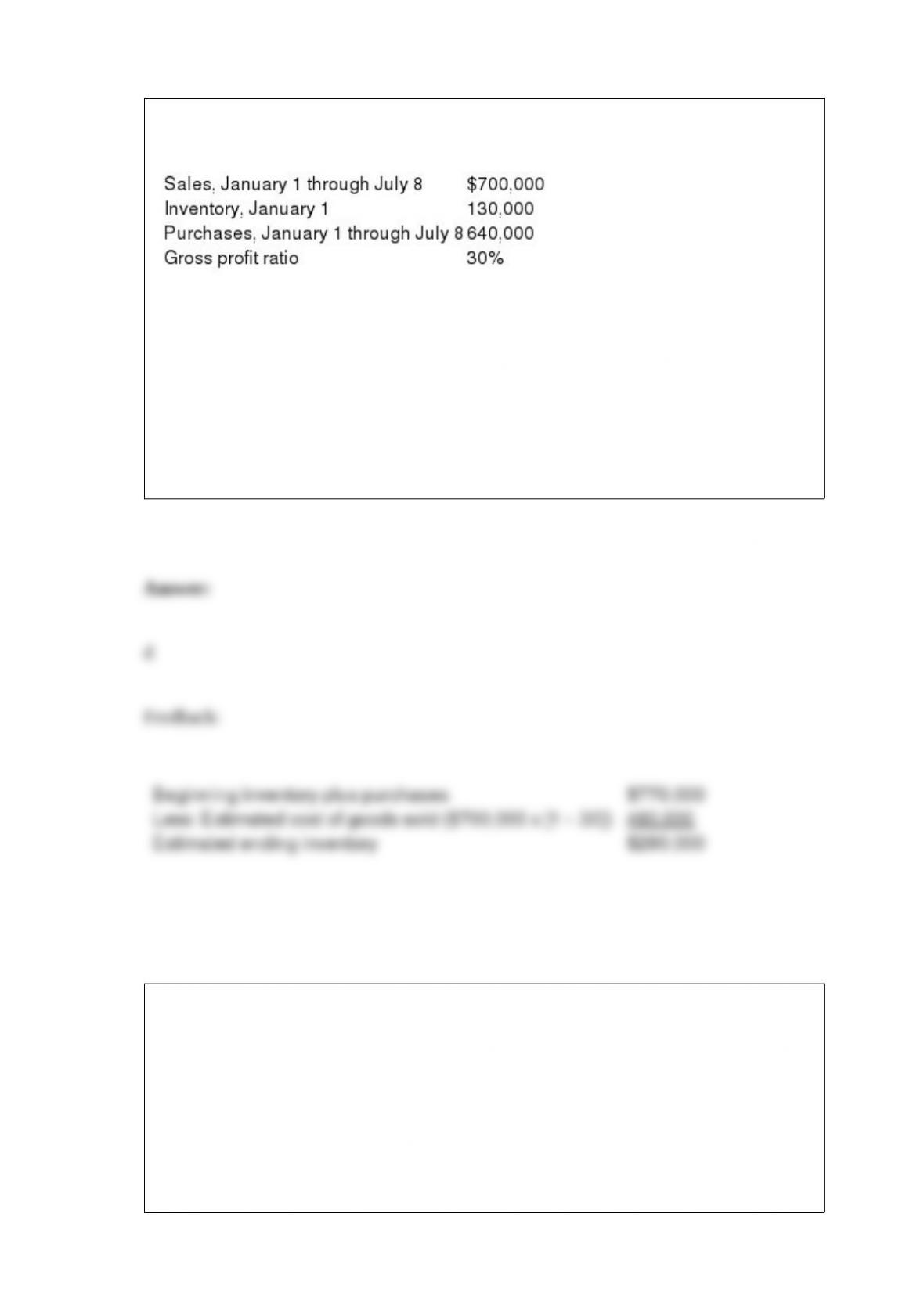

On July 8, a fire destroyed the entire merchandise inventory on hand of Larrenaga

Wholesale Corporation. The following information is available:

What is the estimated inventory on July 8 immediately prior to the fire?

a. $192,000.

b. $490,000.

c. $510,000.

d. $280,000.

Notes payable that are due in two years are:

a. Current liabilities.

b. Long-term intangible assets.

c. Long-term liabilities.

d. Long-term investments.

The adjusting entry required to record accrued expenses includes:

a. A credit to cash.

b. A debit to an asset.

c. A credit to an asset.

d. A credit to liability.

Brewer Inc. is owed $200,000 by Carol Co. under a 10% note with two years remaining

to maturity. Due to financial difficulties Carol Co. did not pay the prior year’s interest.

Brewer agrees to settle the receivable (and accrued interest) in exchange for a cash

payment of $150,000. The journal entry that Brewer would make to record this

transaction would include a loss on troubled debt restructuring of:

a. $0.

b. $20,000.

c. $50,000.

d. $70,000.

Assets acquired in a lump-sum purchase are valued based on:

a. Their assessed valuation.

b. Their relative fair values.

c. The present value of their future cash flows.

d. Their cost plus the difference between their cost and fair values.

The usual difference between accounts payable and notes payable is:

a. Legally enforceable debt.

b. Current-noncurrent classification.

c. Known payment terms.

d. Explicitly stated interest.

Explain how you would compute the imputed interest on cash borrowed at 0% interest

when the market rate of interest is 8%.

Fusion, Inc. introduced a new line of circuits in 2016 that carry a four-year warranty

against manufacturer’s defects. Based on experience with previous product

introductions, warranty costs are expected to approximate 3% of sales. Sales and actual

warranty expenditures for the first year of selling the product were:

Required:

1> Does this situation represent a loss contingency? Why or why not? How should it be

accounted for?

2> Prepare journal entries that summarize sales of the circuits (assume all credit sales)

and any aspects of the warranty that should be recorded during 2016.

3> What amount should Fusion report as a liability at December 31, 2016?

What is the entry to record the expiration of 10% of the options on December 31,

2020?

Wall Drugs offered an incentive stock option plan to its employees. On January 1, 2016,

options were granted for 60,000 $1 par common shares. The exercise price equals the

$5 market price of the common stock on the grant date. The options cannot be exercised

before January 1, 2019, and expire December 31, 2020. Each option has a fair value of

$1 based on an option pricing model.

On December 31, 2015, Belair Corporation had 100,000 shares of common stock

outstanding and 30,000 shares of 7%, $50 par, cumulative preferred stock outstanding.

On February 28, 2016, Belair purchased 24,000 shares of common stock on the open

market as treasury stock paying $20 per share. On June 30, 2016, Belair declared and

issued a 2-for-1 stock split on outstanding common stock. Belair sold 6,000 treasury

shares on September 30, 2016, for $15 per share. Net income for 2016 was $180,905.

Required:

Compute Belair’s basic earnings per share for 2016.

DJ Co. is a calendar-year firm with 120 million common shares outstanding

throughout 2016. As part of its executive compensation plan, at January 1, 2015, the

company had issued 12 million executive stock options permitting executives to buy 12

million shares of stock for $10 each within the next eight years, but not prior to January

1, 2018. The fair value of the options was estimated on the grant date to be $3 per

option. The stock options qualify for tax purposes as an incentive plan. The company’s

net income was $480 million in 2016. Its income tax rate is 40%. The average market

price of the stock during 2016 was $12 per share.

Required:

Determine basic and diluted earnings per share (rounded to two decimal places) for DJ

in 2016.