1) A direct cost is a cost that cannot be easily traced to the particular cost object under

consideration.

2) Opportunity costs are not usually recorded in the accounts of a business.

3) If the FIFO cost method is used in a process costing system, costs in the beginning

inventory are kept separate from current period costs.

4) When using segmented income statements, the dollar sales for a segment to break

even equals the common fixed expenses of the segment divided by the segment CM

ratio.

5) Only future costs that differ between alternatives are relevant in decision making.

6) Only variable manufacturing overhead costs are included in the manufacturing

overhead budget.

7) In a decision to drop a segment, the opportunity cost of the space occupied by the

segment is the cost of renting or building similar space nearby.

8) An avoidable cost is a cost that can be completely eliminated irrespective of whether

one chooses one alternative or another in a decision.

9) All profit centers are responsibility centers, but not all responsibility centers are

profit centers.

10) A common fixed cost is a fixed cost that is incurred because of the existence of a

particular business segment and that would be eliminated if the segment were

eliminated.

11) When materials are purchased in a process costing system, a materials account is

debited with the cost of the materials.

12) The formula for total asset turnover is: Total asset turnover = Total assets Total

stockholders’ equity.

13) The applied manufacturing overhead for the year was closest to:

A.$58,017

B.$59,590

C.$60,600

D.$58,597

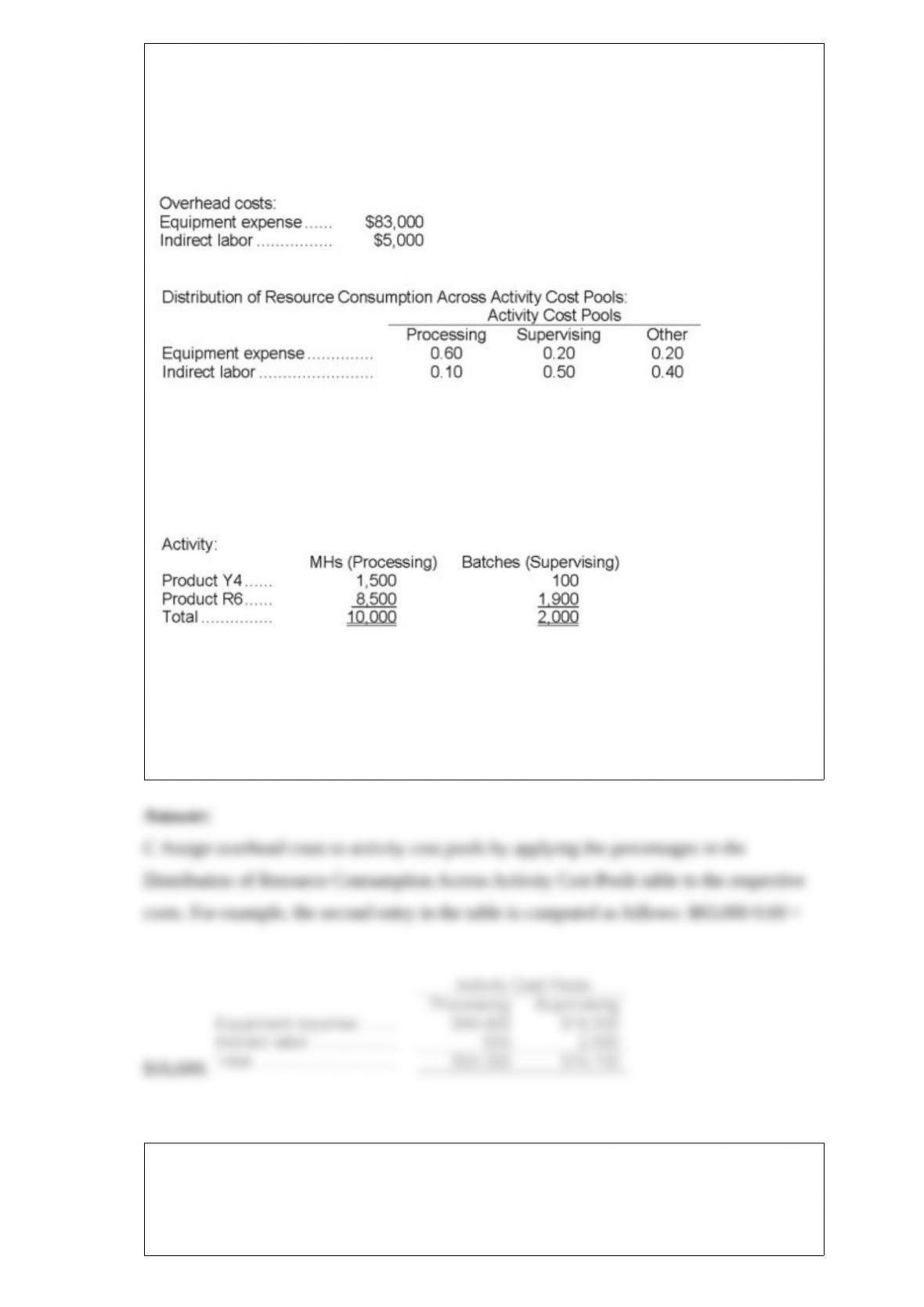

14) Studler Corporation has an activity-based costing system with three activity cost

pools-Processing, Supervising, and Other. In the first stage allocations, costs in the two

overhead accounts, equipment expense and indirect labor, are allocated to the three

activity cost pools based on resource consumption. Data used in the first stage

allocations follow:

Processing costs are assigned to products using machine-hours (MHs) and Supervising

costs are assigned to products using the number of batches. The costs in the Other

activity cost pool are not assigned to products. Activity data for the company’s two

products follow:

How much overhead cost is allocated to the Supervising activity cost pool under

activity-based costing?

A.$18,600

B.$16,600

C.$19,100

D.$2,500

15) Norton Inc. could improve its current ratio of 2 by:

A.paying a previously declared stock dividend.

B.writing off an uncollectible receivable.

C.selling merchandise on credit at a profit.

D.purchasing inventory on credit.

16) The income tax expense in year 2 is:

A.$17,500

B.$52,500

C.$28,000

D.$10,500

17) Beakins Corporation produces a single product. The standard cost card for the

product follows:

During a recent period the company produced 1,200 units of product. Various costs

associated with the production of these units are given below:

The company records all variances at the earliest possible point in time. Variable

manufacturing overhead costs are applied to products on the basis of standard direct

labor-hours.

The variable overhead efficiency variance for the period is:

A.$1,200 U

B.$1,440 U

C.$1,200 F

D.$1,440 F

18) The company’s average sale period (turnover in days) for Year 2 is closest to:

A.65.6 days

B.226.6 days

C.43.8 days

D.70.6 days

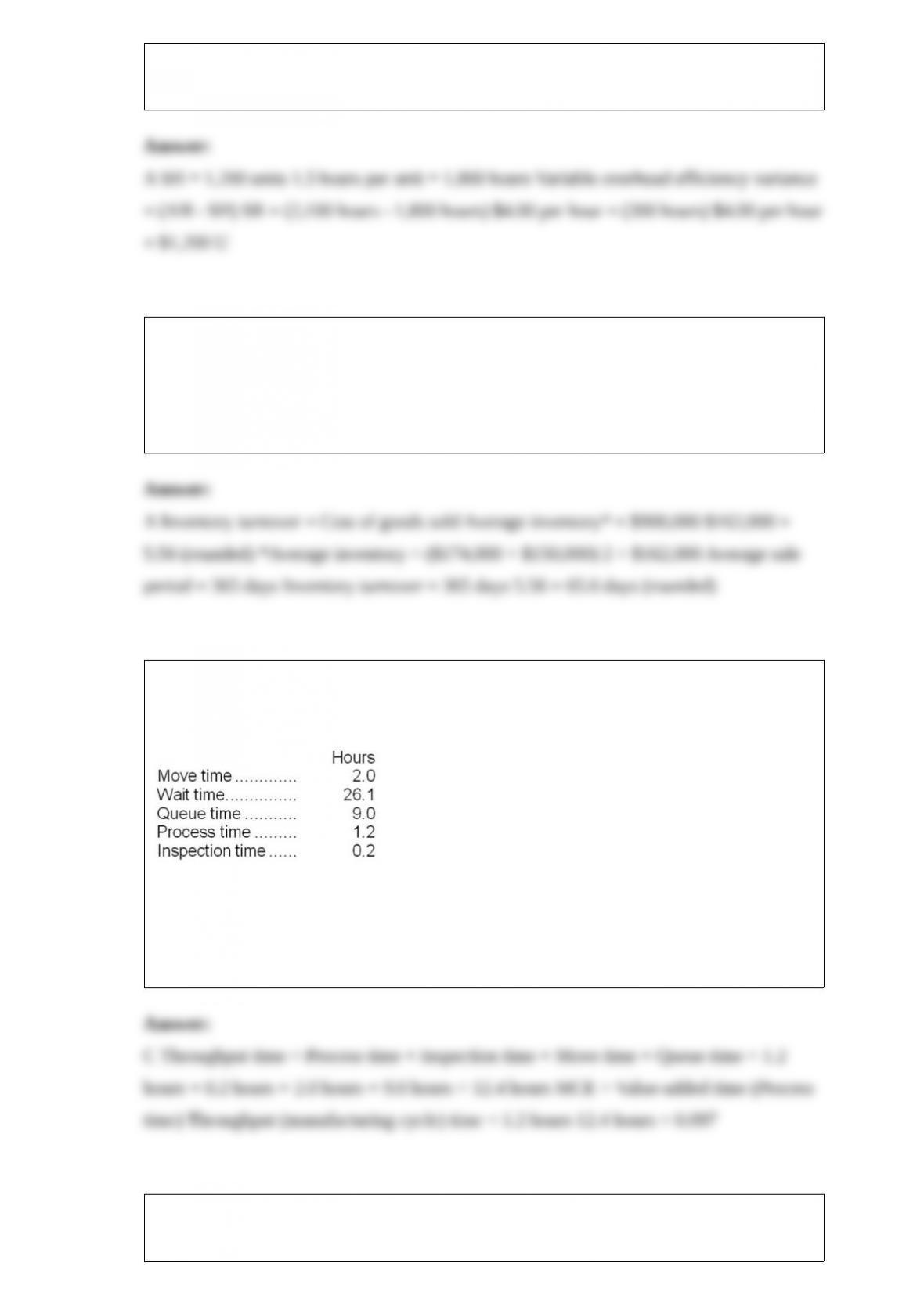

19) Jolin Corporation keeps careful track of the time required to fill orders. The times

recorded for a particular order appear below:

The manufacturing cycle efficiency (MCE) was closest to:

A.0.03

B.0.16

C.0.10

D.0.48

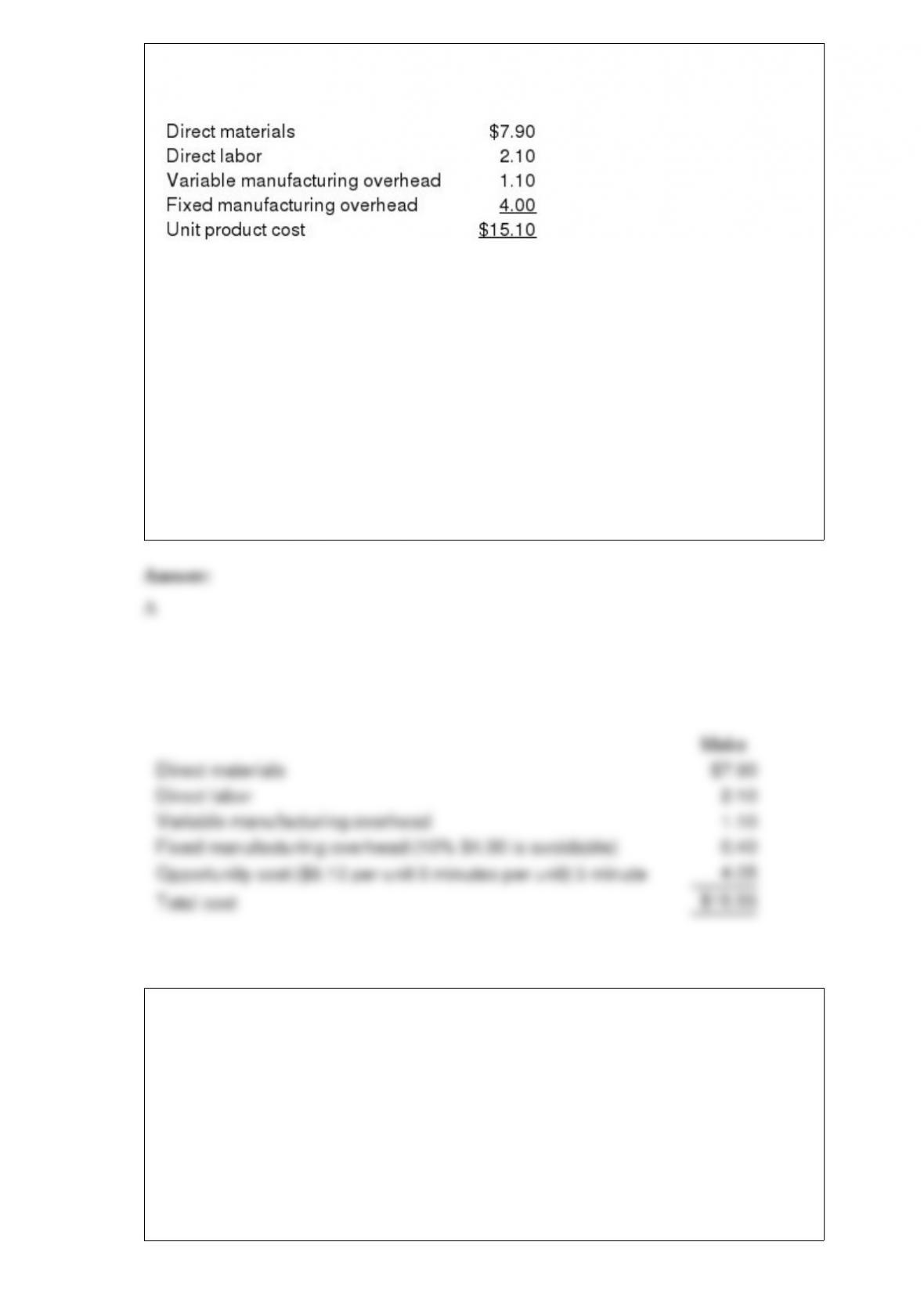

20) Teich Inc. is considering whether to continue to make a component or to buy it from

an outside supplier. The company uses 15,000 of the components each year. The unit

product cost of the component according to the company’s absorption cost accounting

system is given as follows:

Assume that direct labor is a variable cost. Of the fixed manufacturing overhead, 10%

is avoidable if the component were bought from the outside supplier; the remainder is

not avoidable. In addition, making the component uses 3 minutes on the machine that is

the company’s current constraint. If the component were bought, time would be freed up

for use on another product that requires 6 minutes on this machine and that has a

contribution margin of $8.10 per unit.

When deciding whether to make or buy the component, what cost of making the

component should be compared to the price of buying the component?

A) $15.55 per unit

B) $11.50 per unit

C) $19.15 per unit

D) $15.10 per unit

21) Kellog Corporation is considering a capital budgeting project that would have a

useful life of 4 years and would involve investing $160,000 in equipment that would

have zero salvage value at the end of the project. Annual incremental sales would be

$390,000 and annual cash operating expenses would be $260,000. The company uses

straight-line depreciation on all equipment. Its income tax rate is 35%.

The income tax expense in year 2 is:

A.$7,000

B.$45,500

C.$31,500

D.$24,500

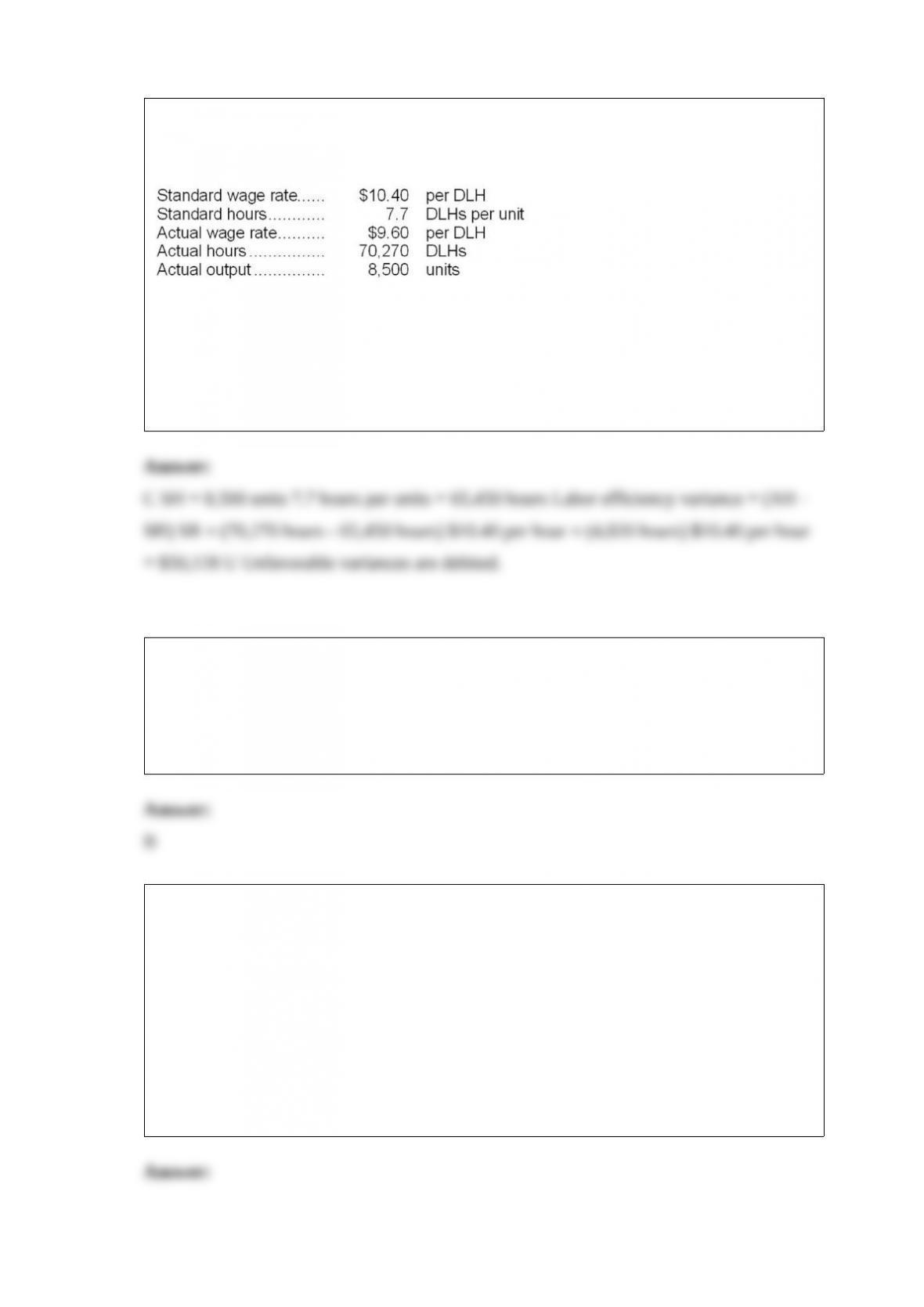

22) Enwall Corporation’s standard wage rate is $11.20 per direct labor-hour (DLH) and

according to the standards, each unit of output requires 2.9 DLHs. In December, 5,900

units were produced, the actual wage rate was $10.20 per DLH, and the actual hours

were 14,150 DLHs.

In the journal entry to record the incurrence of direct labor costs in December, the Work

in Process entry would consist of a:

A.credit of $144,330.

B.debit of $191,632.

C.debit of $144,330.

D.credit of $191,632.

23) The total of the period costs listed above for September is:

A) $303,000

B) $59,000

C) $366,000

D) $362,000

24) Miolen Corporation has provided the following data concerning its direct labor

costs for June:

The Labor Efficiency Variance for June would be recorded as a:

A.credit of $50,128.

B.debit of $46,272.

C.debit of $50,128.

D.credit of $46,272.

25) In a make-or-buy decision, relevant costs include:

A) unavoidable fixed costs

B) avoidable fixed costs

C) fixed factory overhead costs applied to products

D) fixed sellling and administrative expenses

26) Reven Corporation prepares its statement of cash flows using the direct method.

Last year, Reven reported Income Tax Expense of $25,000. At the beginning of last

year, Reven had a $5,000 balance in the Income Taxes Payable account. At the end of

last year, Reven had a $9,000 balance in the account. On its statement of cash flows for

last year, what amount should Reven have shown for its Income Tax Expense adjusted

to a cash basis (i.e., income taxes paid)?

A.$29,000

B.$21,000

C.$25,000

D.$4,000

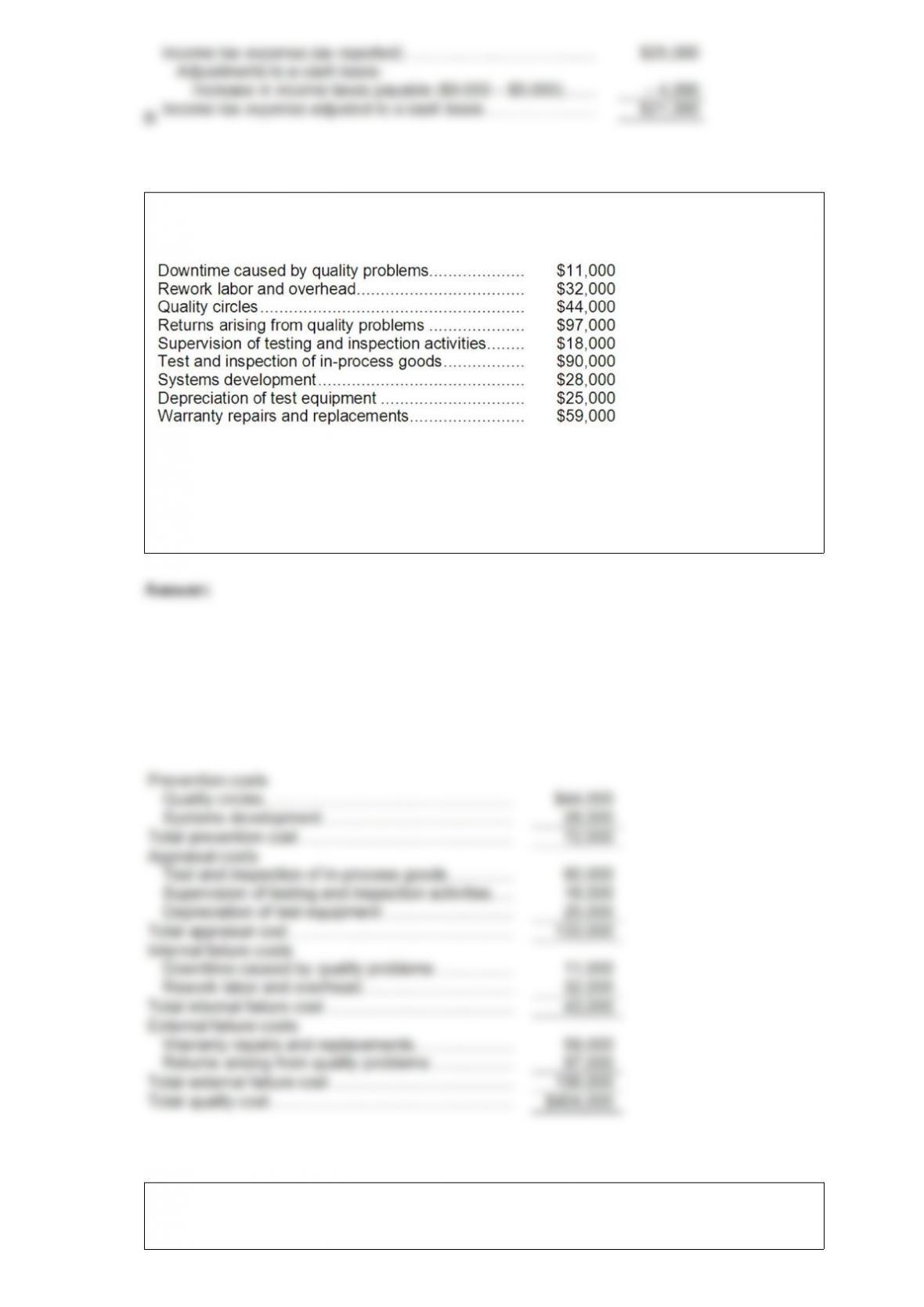

27) Galant Company’s quality cost report is to be based on the following data:

Required:

Prepare a Quality Cost Report in good form with separate sections for prevention costs,

appraisal costs, internal failure costs, and external failure costs.

28) ( The management of Kountz Corporation is considering the purchase of a machine

that would cost $74,520 and would have a useful life of 8 years. The machine would

have no salvage value. The machine would reduce labor and other operating costs by

$20,000 per year.

Required:

Determine the internal rate of return on the investment in the new machine. Show your

work!

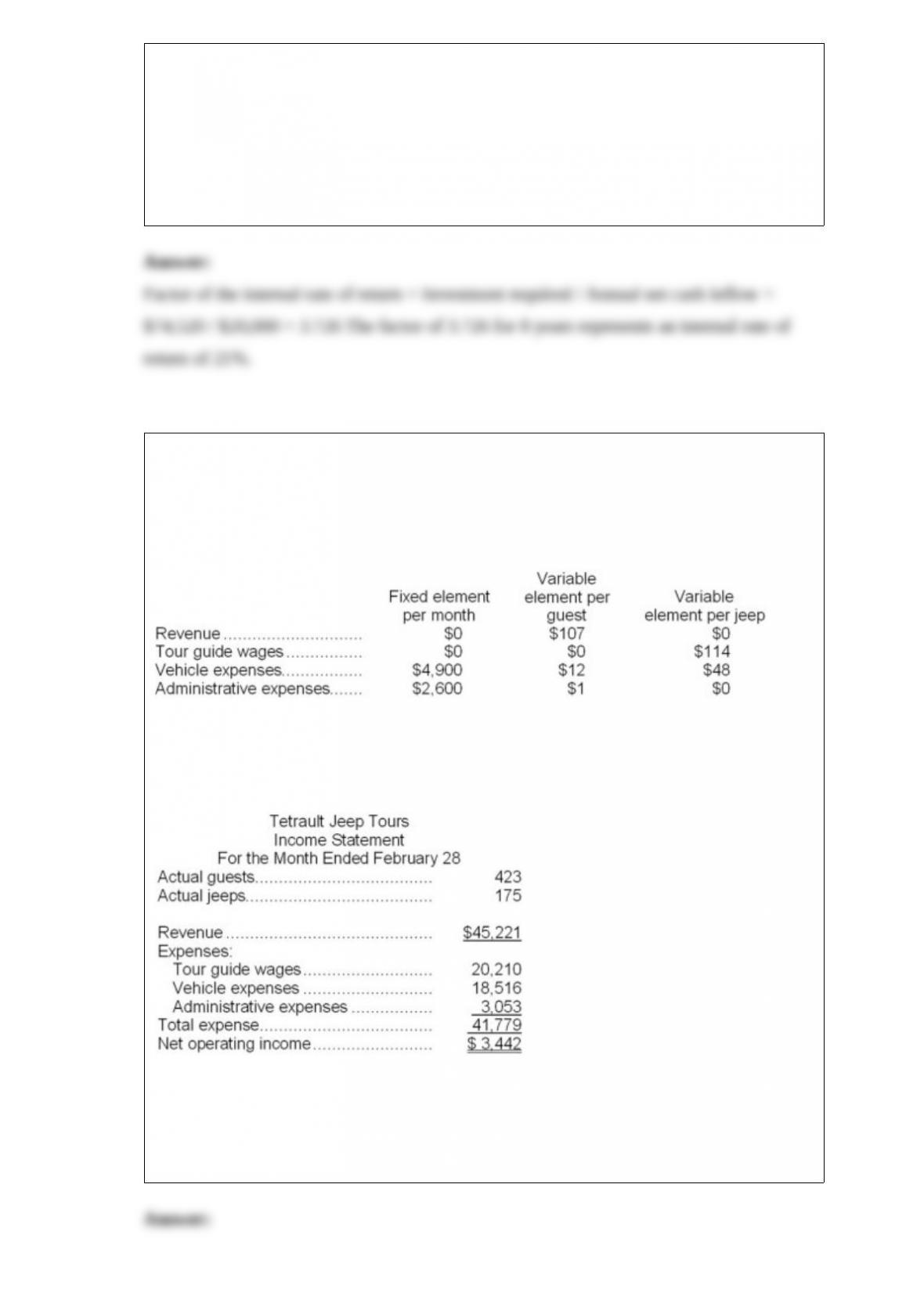

29) Tetrault Jeep Tours operates jeep tours in the heart of the Colorado Rockies. The

company bases its budgets on two measures of activity (i.e., cost drivers), namely

guests and jeeps. One vehicle used in one tour on one day counts as a jeep. Each jeep

has one tour guide. The company uses the following data in its budgeting:

In February, the company budgeted for 448 guests and 173 jeeps. The company’s

income statement showing the actual results for the month appears below:

Required:

Prepare a report showing the company’s activity variances for February. Label each

variance as favorable (F) or unfavorable (U).

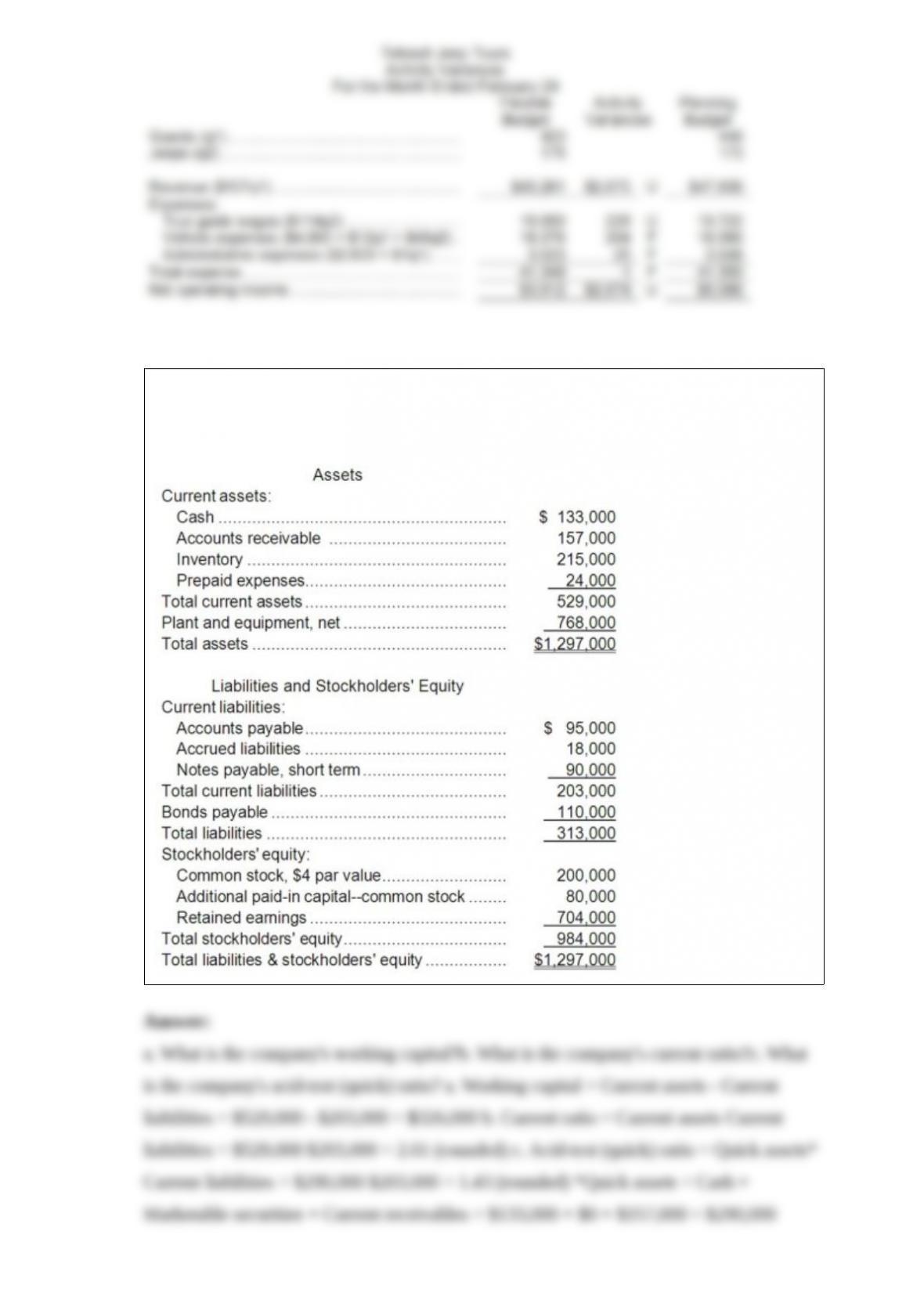

30) Wowk Corporation has provided the following financial data:

31) ( Dunay Corporation is considering investing $510,000 in a project. The life of the

project would be 4 years. The project would require additional working capital of

$24,000, which would be released for use elsewhere at the end of the project. The

annual net cash inflows would be $162,000. The salvage value of the assets used in the

project would be $41,000. The company uses a discount rate of 10%.

Required:

Compute the net present value of the project.

32) Free cash flow decreases when a company issues common stock for cash.

TRUE

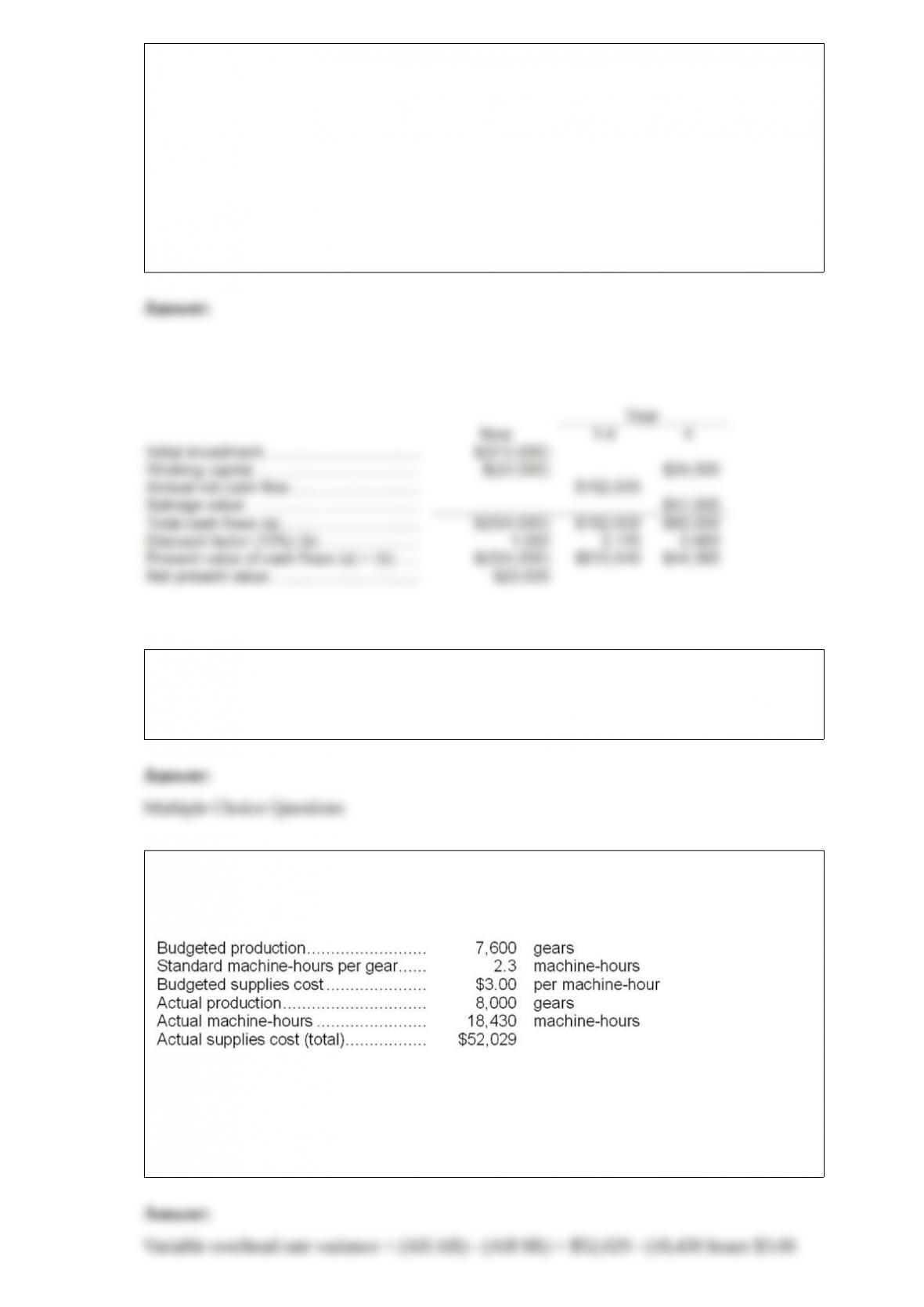

33) Vath Corporation, which makes landing gears, has provided the following data for a

recent month:

Required:

Determine the rate and efficiency variances for the variable overhead item supplies and

indicate whether those variables are favorable or unfavorable. Show your work!

34) ( Consider the following three investment opportunities:

Project I would require an immediate cash outlay of $10,000 and would result in cash

savings of $3,000 each year for 5 years.

Project II would require cash outlays of $3,000 per year and would provide a cash

inflow of $30,000 at the end of 5 years.

Project III would require a cash outlay of $10,000 now and would provide a cash inflow

of $30,000 at the end of 5 years.

Required:

The discount rate is 14%. Use the net present value method to determine which, if any,

of the three projects is acceptable.

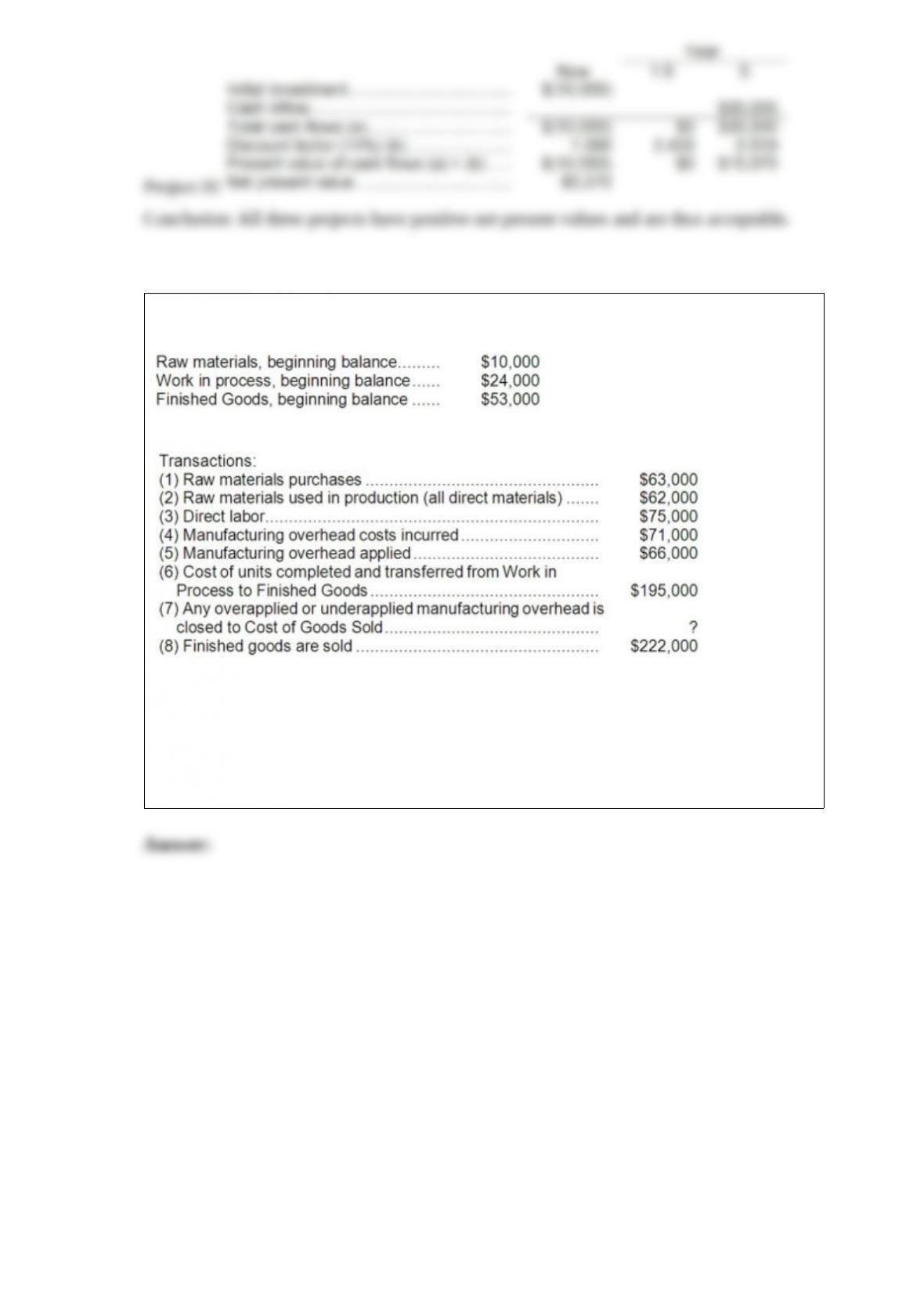

35) During January, Shanker Corporation recorded the following:

Required:

Prepare T-accounts for Raw Materials, Work in Process, Finished Goods, and

Manufacturing Overhead, and Cost of Goods Sold. Record the beginning balances and

each of the transactions listed above. Finally, determine the ending balances.

36) Febbo Clinic bases its budgets on the activity measure patient-visits. During

February, the clinic planned for 3,200 patient-visits, but its actual level of activity was

3,000 patient-visits. Revenue should be $54.00 per patient-visit. Personnel expenses

should be $39,400 per month plus $16.70 per patient-visit. Medical supplies should be

$1,300 per month plus $10.90 per patient-visit. Occupancy expenses should be $11,600

per month plus $2.00 per patient-visit. Administrative expenses should be $5,400 per

month plus $0.30 per patient-visit.

Required:

Prepare a report showing the clinic’s activity variances for February. Indicate in each

case whether the variance is favorable (F) or unfavorable (U).