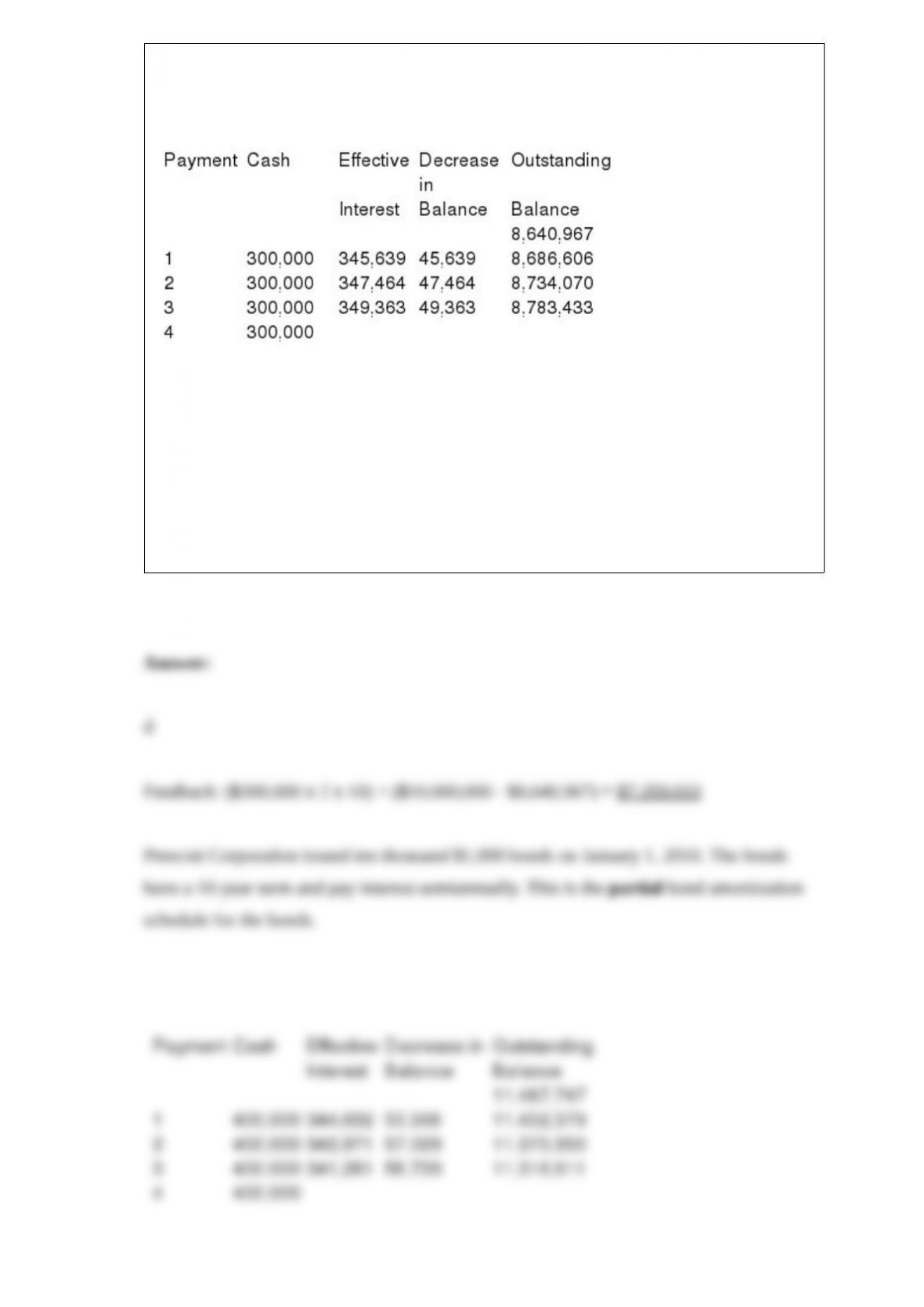

Discount-Mart issued ten thousand $1,000 bonds on January 1, 2016. The bonds have a

10-year term and pay interest semiannually. This is the partial bond amortization

schedule for the bonds.

What would be the total interest cost of the bonds over their full term?

a. $1,359,033.

b. $4,640,967.

c. $6,000,000.

d. $7,359,033.

Which of the following is true about accounting for long-term construction contracts?

a. Contract assets are likely to be larger if revenue is recognized over time than if

revenue is recognized at a point in time.

b. Contract assets are likely to be smaller if revenue is recognized over time than if

revenue is recognized at a point in time.

c. Contract assets are likely to be the same size regardless of whether revenue is

recognized over time or at a point in time.

d. There is no way to tell how revenue recognition timing will affect the size of contract

assets without more information.

Ordinarily, the proceeds from the sale of a bond issue will be equal to:

a. The face amount of the bond.

b. The total of the face amount plus all interest payments.

c. The present value of the face amount plus the present value of the stream of interest

payments.

d. The face amount of the bond plus the present value of the stream of interest

payments.

Quaker State Inc. offers a new employee a lump-sum signing bonus at the date of

employment. Alternatively, the employee can take $8,000 at the date of employment

plus $20,000 at the end of each of his first three years of service. Assuming the

employee’s time value of money is 10% annually, what lump sum at employment date

would make him indifferent between the two options?

a. $23,026.

b. $57,737.

c. $62,711.

d. None of these answer choices is correct.

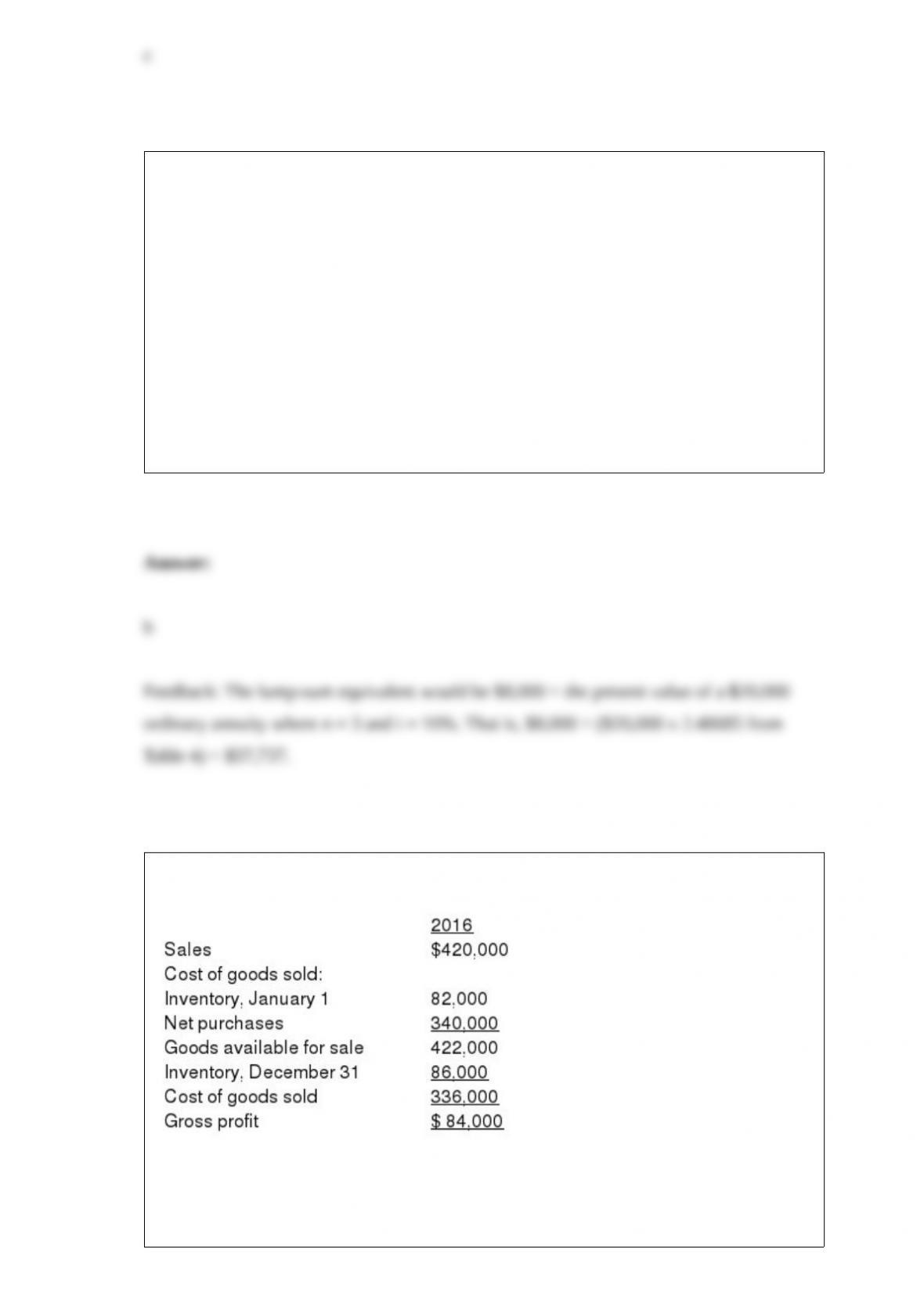

Thompson TV and Appliance reported the following in its 2016 financial statements:

Thompson’s 2016 gross profit ratio is:

a. 25%.

b. 19%.

c. 20%.

d. None of the above is correct.

What amount of interest revenue would Frankenstein earn on these notes during 2017?

a. Above $12,000.

b. Between $7,000 and 10,000.

c. Less than $5000.

d. None of these answer choices are correct.

Calstone, Inc., prepares a single, continuous statement of comprehensive income. The

following situations occurred during the company’s 2016 fiscal year: 1> Land that had

been held as an investment was sold and a gain was recognized.

2> Losses from foreign currency translation were recognized.

3> Interest revenue was recognized.

4> A division was sold that qualifies as a separate component according to GAAP

regarding discontinued operations.

5> Unrealized losses on investments.

6> Restructuring costs were incurred due to downsizing and reorganization of a

manufacturing facility. Required:

For each situation, identify the appropriate reporting treatment from the list below

(consider each event to be material).

a. As a component of operating income.

b. As a nonoperating income item (other income or expense).

c. As a discontinued operation.

d. As an item of other comprehensive income.

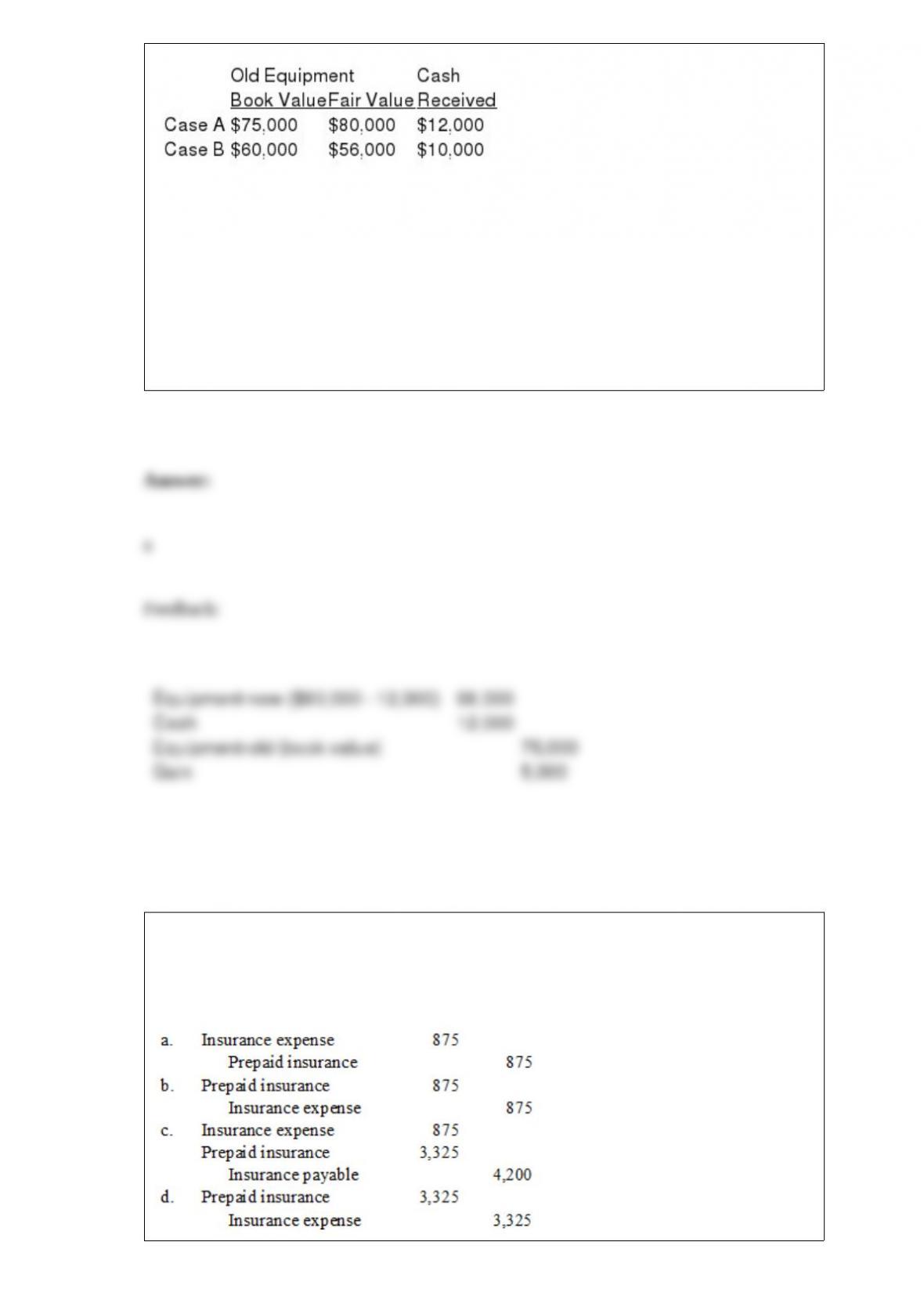

Below is information relative to an exchange of equipment by Pensacola Inc. Assume

the exchange has commercial substance.

In Case A, Pensacola would record the new equipment at:

a. $68,000.

b. $63,750.

c. $67,250.

d. $80,000.

Yummy Foods purchased a two-year fire and extended coverage insurance policy on

August 1, 2016, and charged the $4,200 premium to Insurance expense. At its

December 31, 2016, year-end, Yummy Foods would record which of the following

adjusting entries?

In the DuPont formula, return on assets equals:

a. Gross margin on sales x Inventory turnover.

b. Profit margin on sales x Inventory turnover.

c. Gross margin on sales x Asset turnover.

d. Profit margin on sales x Asset turnover.

Costs incurred by the lessor that are associated directly with originating a lease and are

essential to acquire that lease are called initial direct costs. Initial direct costs are

expensed at the inception of the lease in:

a. An operating lease.

b. A capital lease.

c. A direct financing lease.

d. A sales-type lease.

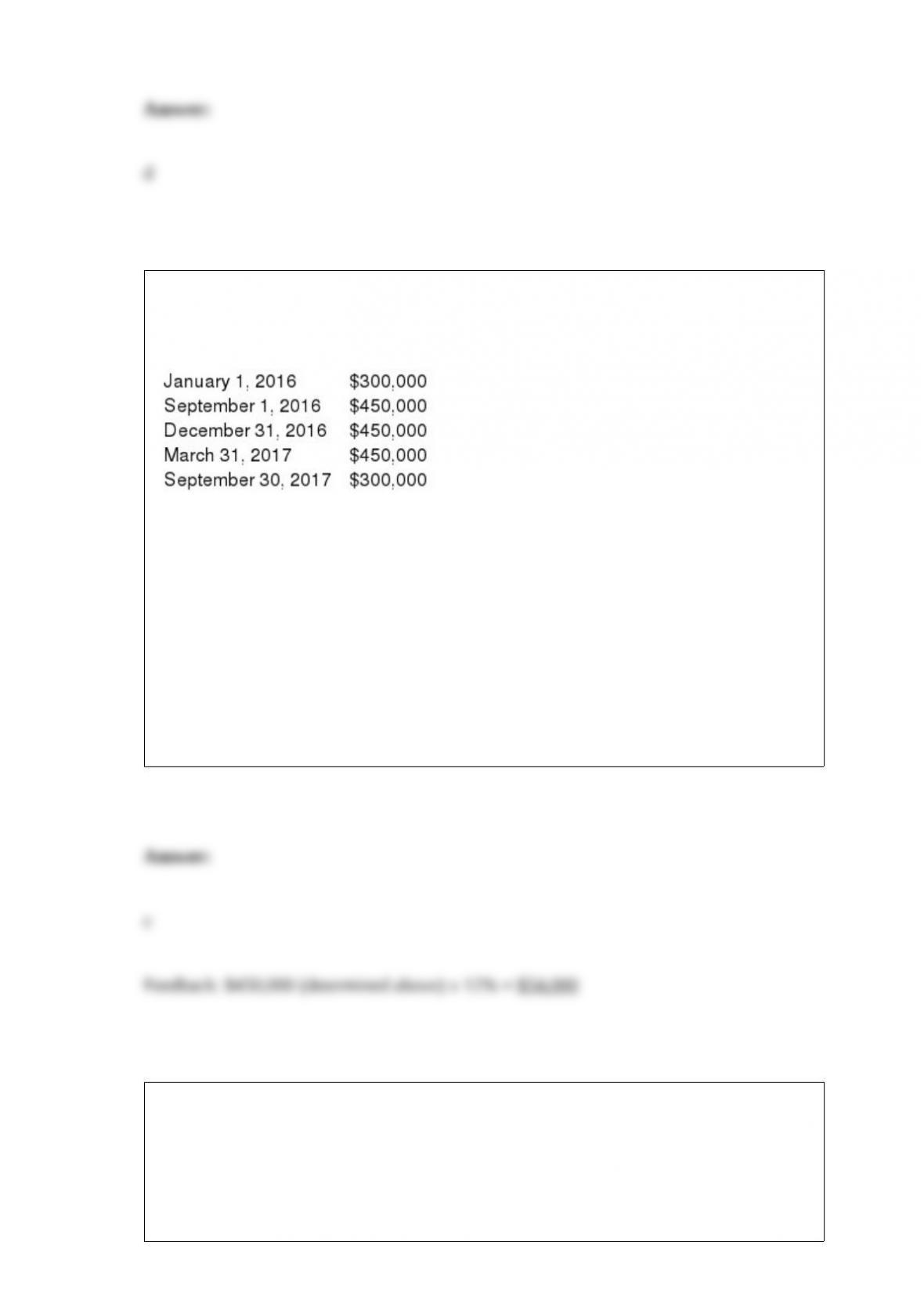

On January 1, 2016, Dreamworld Co. began construction of a new warehouse. The

building was finished and ready for use on September 30, 2017. Expenditures on the

project were as follows:

Dreamworld had $5,000,000 in 12% bonds outstanding through both years.

Dreamworld’s capitalized interest in 2016 was:

a. $72,000.

b. $63,000.

c. $54,000.

d. $36,000.

Lexikon Pianos sells customized concert pianos throughout the U.S. Its grand concert

piano sells for $200,000, which includes delivery and installation. The product comes

with a two-year warranty that covers any product defects, and customers can choose to

add an extended three-year warranty for maintenance and repair at a price of $2,000.

Customers also get an option to upgrade traditional plastic keys to bone ones for an

additional $20,000. The extended warranty would normally sell for $3,500, and the

installation of bone keys carries a standalone price of $30,000. Required:

(a) Given the information above, how many performance obligations exist in the

contract to purchase a grand concert piano?

(b) Now, assume that the standalone price of the extended warranty is $2,000, and that

of the bone key upgrade is $20,000. How many performance obligations exist in the

contract to purchase a grand concert piano?

Flapper Jack’s Pancake Restaurants Inc. sells franchises for an initial fee of $36,000

plus operating fees of $500 per month. The initial fee covers site selection, training,

computer and accounting software, and on-site consulting and troubleshooting, as

needed, over the first five years. On March 15, 2015, Tim Cruise signed a franchise

contract, paying the standard $6,000 down with the balance due over five years with

interest.

Assume that at the time of signing the contract, collection of the receivable was assured

and that service obligations were substantial. However, by October 20, 2015,

substantially all continuing obligations had been met. The journal entry required at

October 20, 2015 would include a:

a. Credit to franchise fee receivable for $27,000.

b. Debit to unearned franchise fee revenue for $36,000.

c. Credit to franchise fee revenue for $9,000.

d. Debit to unearned franchise fee revenue for $27,000.

Which of the following is not a required disclosure for related-party transactions?

a. The nature of the relationship.

b. A description of the transactions.

c. The amounts due from or to related parties.

d. The impact of the transactions on current year’s income.

Calistoga Produce estimates bad debt expense at ½% of credit sales. The company

reported accounts receivable and allowance for uncollectible accounts of $471,000 and

$1,650, respectively, at December 31, 2015. During 2016, Calistoga’s credit sales and

collections were $315,000 and $319,000, respectively, and $1,720 in accounts

receivable were written off. Calistoga’s 2016 bad debt expense is:

a. $1,720.

b. $1,650.

c. $1,505.

d. $1,575.

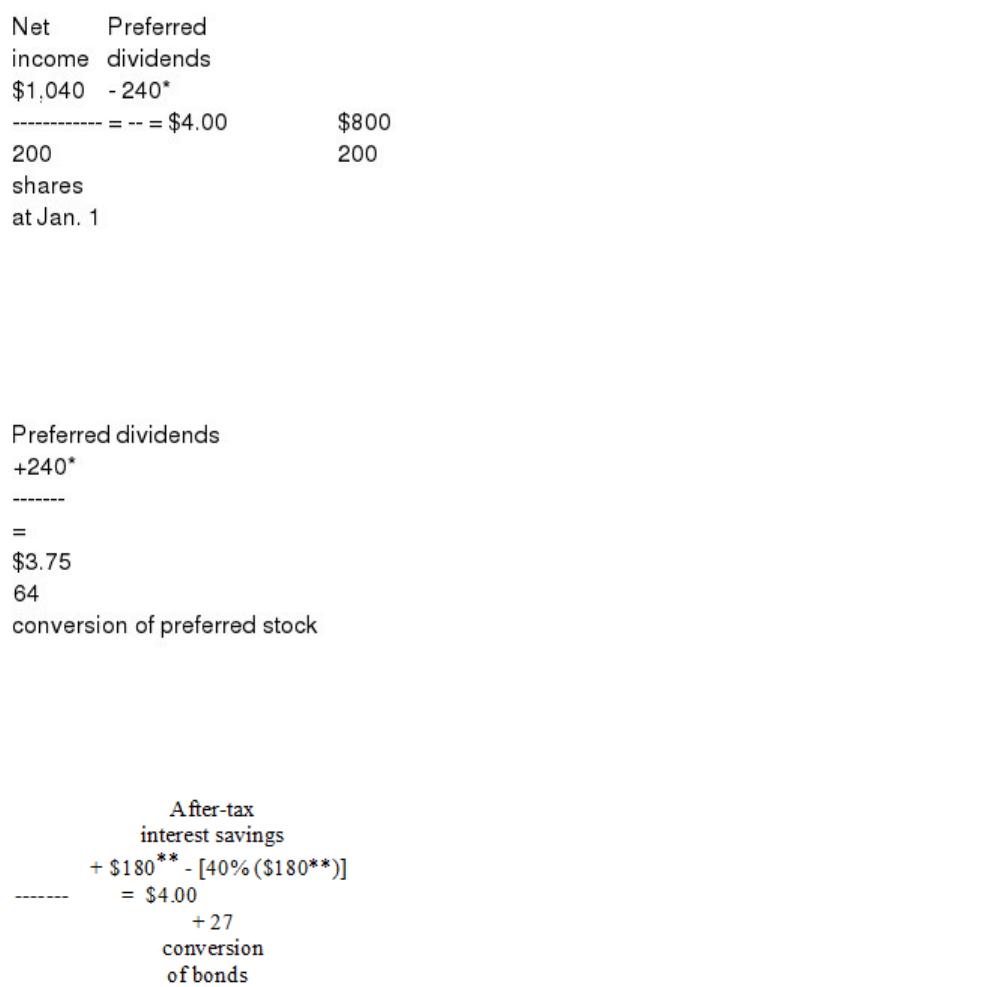

At December 31, 2016, MedX Corporation had outstanding 200,000 shares of common

stock. Also outstanding were 120,000 shares of preferred stock convertible into 64,000

common shares and $1,800,000 of 10% bonds convertible into 27,000 common shares

MedX’s net income for the year ended December 31, 2016, is $1,040,000. The income

tax rate is 40%. MedX paid dividends of $2 per share on its preferred stock during

2016.

Required:

Compute basic and diluted earnings per share for the year ended December 31, 2016,

considering possible antidilutive effects.

Briefly explain when there would be a tax benefit from electing LIFO rather than FIFO.

Champion Industries exchanged a dust-scrubbing piece of equipment for another

version of the same type of equipment and received $12,000 cash. The old dust

scrubber cost $76,200 and had a book value of $54,500. The new dust scrubber had a

fair value of $58,500.

Required:

Prepare the journal entry to record the exchange. Assume the exchange has commercial

substance.

Explain and show an example of how the FASB’s conceptual framework is needed in

formulating standards on controversial topics.

Give an example of a major investing activity cash outflow that would be reported in

the statement of cash flows for a manufacturing company.