1) An advantage of common-size statements is that they reflect the dollar magnitude

(size) of the different companies under analysis.

2) A company that finances a relatively large portion of its assets with liabilities is said

to have a high degree of financial leverage.

3) If the predetermined overhead allocation rate is 350% of direct labor cost and the

Painting Department’s direct labor cost for the reporting period is $20,000, the

following entry would record the allocation of overhead to the products processed in

this department:

4) Risk is the uncertainty about the return we expect to earn.

5) Retained earnings generally consist of a company’s cumulative net income less any

net losses and dividends declared since its inception.

6) Dividend yield is defined as the market price per share of a company’s stock divided

by its earnings per share.

7) An adjusting entry often includes an entry to Cash.

8) The income statement reports on operating activities at a point in time.

9) A contingent liability is a potential obligation that depends on a future event arising

from a future transaction or event.

10) Dividend yield shows the annual amount of cash dividends distributed to common

shares relative to the stock’s market price.

11) Land is not subject to depreciation because it has an unlimited life. This means that

items which increase the usefulness of the land such as parking lots are not depreciated.

12) Consulting the persons affected by a budget when it is prepared can provide an

effective means of motivation and cooperation.

13) Continuous budgeting is the practice of preparing a new budget for a selected

number of future periods and replacing budgets for periods that have lapsed.

14) The general journal is used for transactions not covered by special journals and for

adjusting, closing, and correcting entries.

15) Gross profit is also called gross margin.

16) The file of job cost sheets for completed but undelivered jobs equals the balance in

the Goods in Process Inventory account.

17) Adjustments must be entered in the journal and posted to the ledger after the work

sheet is prepared.

18) Although direct labor and raw materials costs are treated as manufacturing costs and

therefore make up part of the finished goods inventory cost, factory overhead is charged

to expense as it is incurred because it is a period cost.

19) The purchases journal is used to record cash purchases of merchandise.

20) To compute trend percents the analyst should:

A.Select a base period, assign each item in the base period statement a weight of 100%,

and then express financial numbers from other periods as a percent of their base period

number

B.Subtract the analysis period number from the base period number

C.Subtract the base period amount from the analysis period amount, divide the result by

the analysis period amount, then multiply that amount by 100

D.Compare amounts across industries using Dun and Bradstreet

E.All of these

21) A flexible budget performance report compares the differences between:

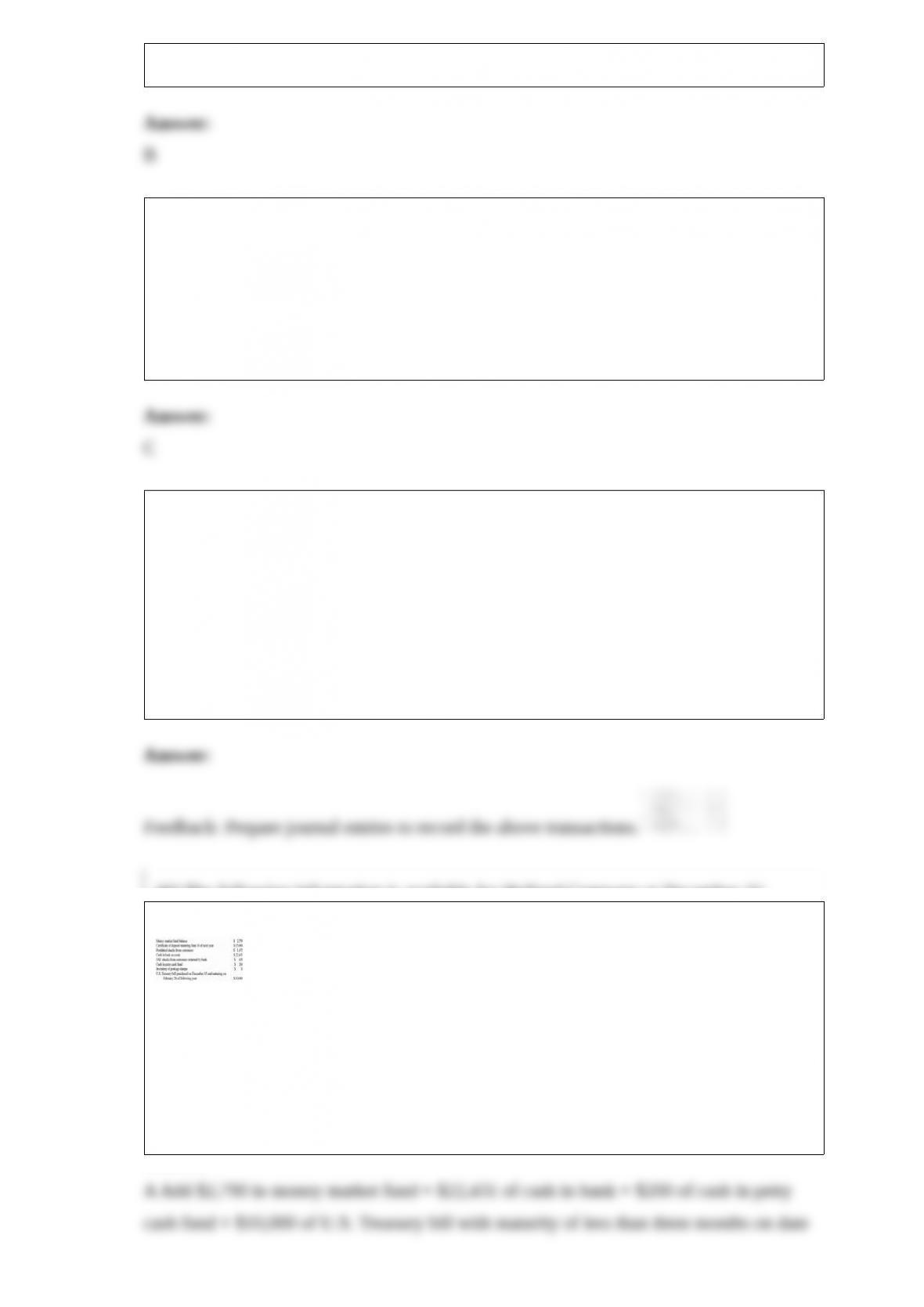

A.Actual performance and budgeted performance based on actual sales volume

B.Actual performance over several periods

C.Budgeted performance over several periods

D.Actual performance and budgeted performance based on budgeted sales volume

E.Actual performance and standard costs at the budgeted sales volume

22) Choosing to outsource a component of a product or manufacture it internally is an

example of a(n):

A.Opportunity cost

B.Sunk cost

C.Out-of-pocket cost

D.Period cost

E.Fixed cost

23) You are reviewing the accounting records of Cathy’s Antiques, owned by Cathy

Miller. You have uncovered the following situations. Compose a memo to Ms. Miller.

Cite the appropriate accounting principle and suggest an action for each separate item.

1> In August, a check for $500 was written to Wee Day Care Center. This amount

represents child care for her son Brandon.

2> Cathy plans a Going Out of Business Sale for May, since she will be closing her

business for a month-long vacation in June. She plans to reopen July 1 and will

continue operating Cathy’s Antiques indefinitely.

3> Cathy received a shipment of pine furniture from Quebec, Canada. The invoice was

stated in Canadian dollars.

4> Joseph Clark paid $1,500 for a dining table. The amount was recorded as revenue.

The table will be delivered to Mr. Clark in six weeks.

24) Management decisions in accounting for inventory cost include all of the following

except:

A.Costing method

B.Inventory system (perpetual or periodic)

C.Customer demand for inventory

D.Use of market values or other estimates

E.Items included in inventory and their costs

25) The buyer who purchases and takes ownership of another company’s accounts

receivable is called a:

A.Payer

B.Pledgor

C.Factor

D.Payee

E.Pledgee

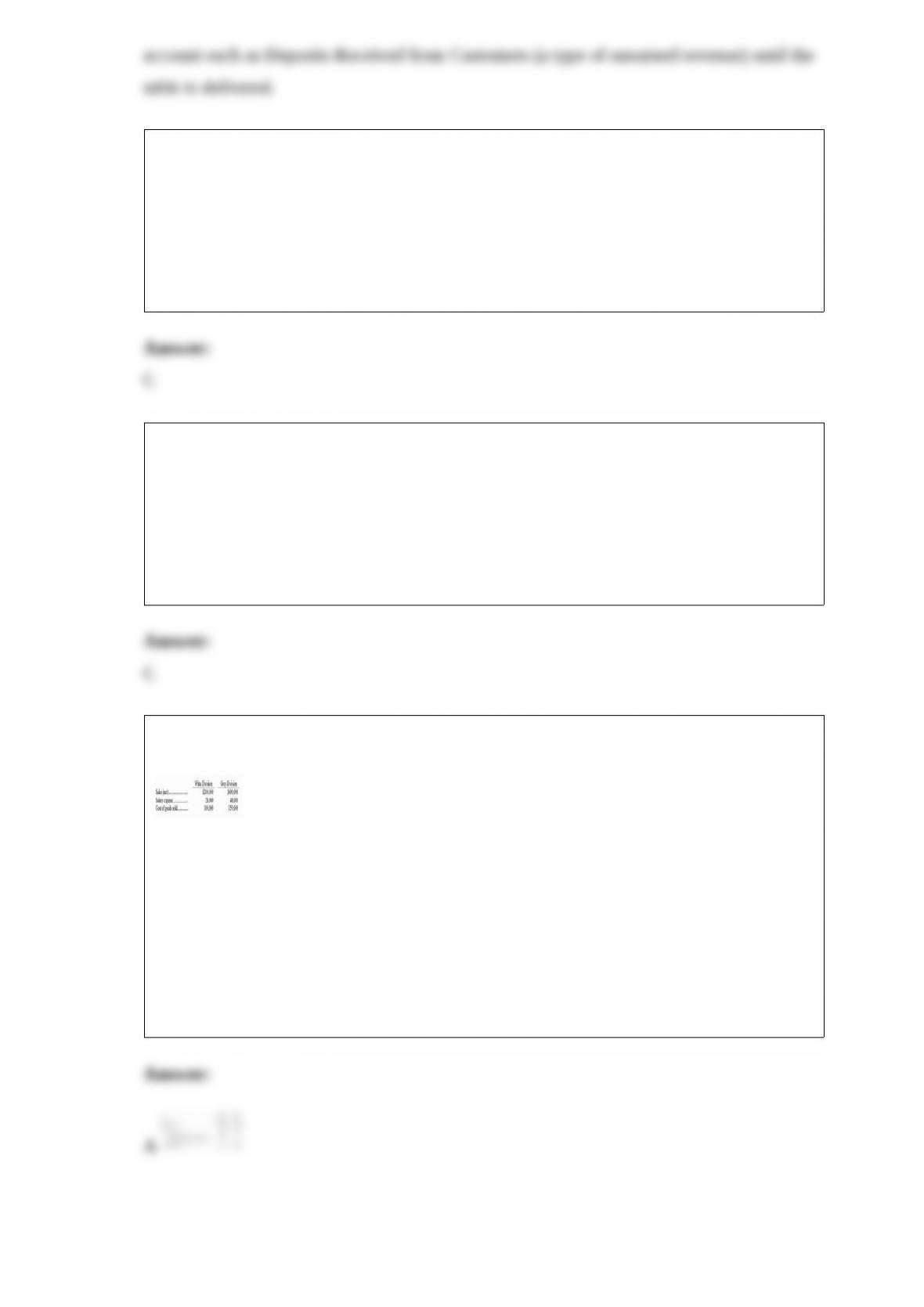

26) Jamesway Corporation has two separate divisions that operate as profit centers. The

following information is available for the most recent year:

The White Division occupies 20,000 square feet in the plant. The Grey Division

occupies 30,000 square feet. Rent is an indirect expense and is allocated based on

square footage. Rent expense for the year was $50,000. Compute departmental income

for the White and Grey Divisions, respectively.

A.$52,000; $163,000

B.$172,000; $352,000

C.$72,000; $163,000

D.$72,000; $193,000

E.$100,000; $241,000

27) Prior to recording adjusting entries, the Office Supplies account had a $359 debit

balance. A physical count of the supplies showed $105 of unused supplies available.

The required adjusting entry is:

A.Debit Office Supplies $105 and credit Office Supplies Expense $105

B.Debit Office Supplies Expense $105 and credit Office Supplies $105

C.Debit Office Supplies Expense $254 and credit Office Supplies $254

D.Debit Office Supplies $254 and credit Office Supplies Expense $254

E.Debit Office Supplies $105 and credit Supplies Expense $254

28) A company has 1,000 shares of $100 par preferred stock. It also has 25,000 shares

of common stock outstanding, and its total stockholders’ equity equals $500,000. The

book value per common share is:

A.$15.38

B.$16.00

C.$19.96

D.$20.00

E.$100.00

29) MixRecording Studios purchased $7,800 in electronic components from TechCom.

MixRecording Studios signed a 60-day, 10% promissory note for $7,800. TechCom’s

journal entry to record the sales portion of the transaction is:

A.Debit Accounts Receivable $7,800; credit Sales $7,800

B.Debit Accounts Receivable $7,930; credit Sales $7,930

C.Debit Notes Receivable $7,800; credit Sales $7,800

D.Debit Notes Receivable $7,930; credit Sales $7,930

E.Debit Notes Receivable $7,800; debit Interest Receivable $130; credit Sales $7,930

30) A company purchased a heating system on January 2 for $225,000. The system had

an estimated useful life of 15 years. On January 3 of the thirteenth year, the company

completed a renovation of the system at a cost of $33,000 and now expects the system

to be more efficient and last 8 years beyond the original estimate. The company uses the

straight-line method of depreciation.

(a) Prepare the journal entry at January 3, to record the renovation of the heating

system.

(b) Prepare the journal entry at December 31, to record the revised depreciation for the

thirteenth year.

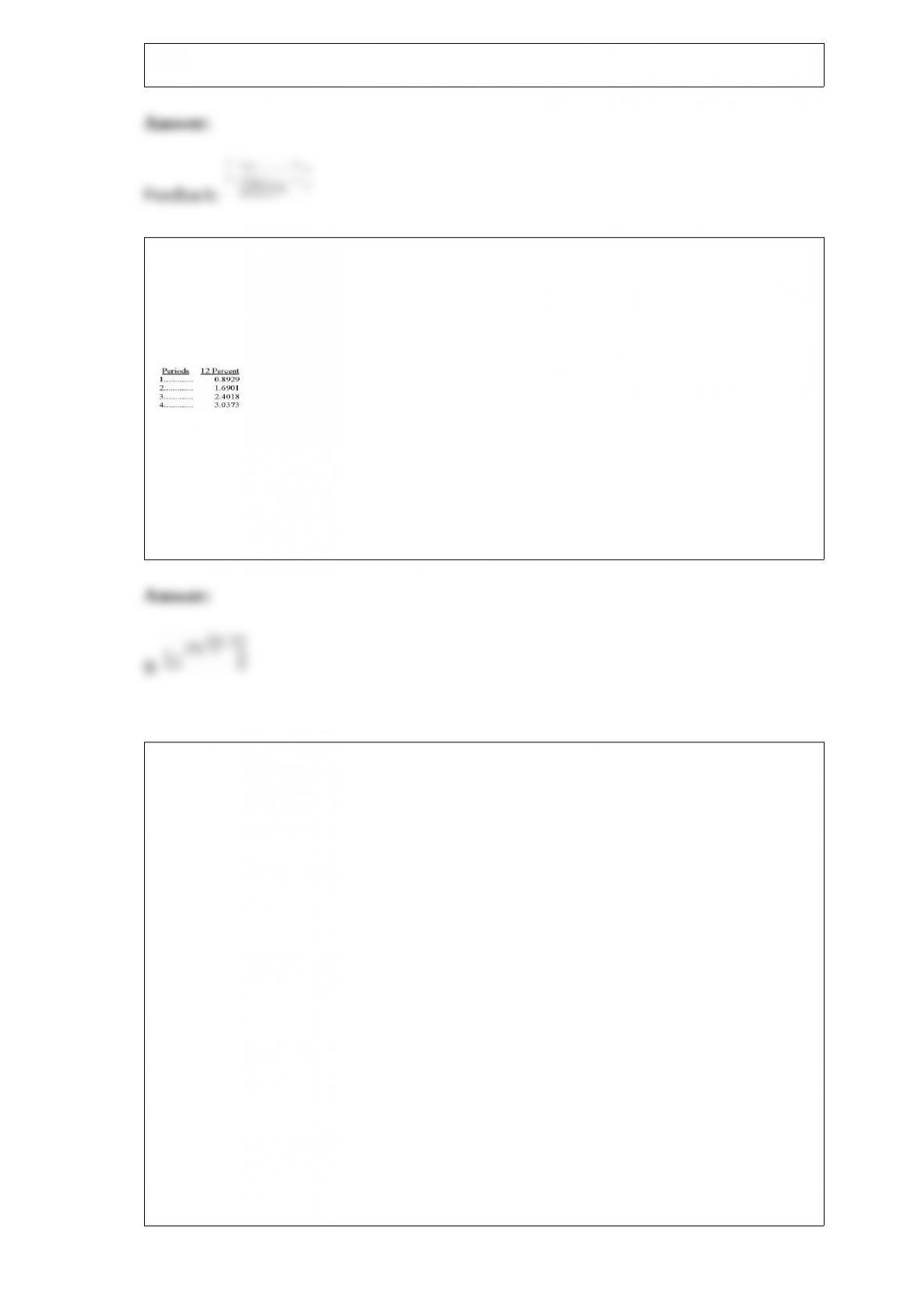

31) Daniels Corporation is considering the purchase of new equipment costing $30,000.

The projected annual after-tax net income from the equipment is $1,200, after deducting

$10,000 for depreciation. The revenue is to be received at the end of each year. The

machine has a useful life of 3 years and no salvage value. Daniels requires a 12% return

on its investments. The present value of an annuity of 1 for different periods follows:

What is the net present value of the machine?

A.$24,018

B.$(3,100)

C.$30,000

D.$26,900

E.$(29,520)

32) Match the following definitions and terms by placing the letter that identifies the

best definition in the blank space next to the term.

1>A list of accounts and their balances at a point in time; the total debit balances should

equal the total credit balances. A. General journal

2>A column in journals where individual account numbers are entered when entries are

posted to ledger accounts B. Chart of accounts

3>The most flexible type of journal, it can be used to record any kind of transaction. C.

Note receivable

4>A record of the increases and decreases in a specific asset, liability, equity, revenue,

or expense item. D. T-account

5>A journal entry that affects at least three accounts E. Unearned revenues

6>A list of all accounts used by a company and the identification number assigned to

each account F. Compound journal entry

7>A simple form used as a helpful tool in understanding the effect of transactions and

events on specific accounts G. Posting reference column

8>A written promise from a customer to pay a definite sum of money on a specified

future date H. Posting

9>The process of transferring journal entry information to the ledger. I. Account

10>Liabilities created when customers pay in advance for products or services; satisfied

by delivering the products or services in the future J. Trial Balance

33) Timmons Company had a January 1, balance in its Allowance for Doubtful

Accounts of $7,000 for the current year. The following transactions and events affected

the Allowance for Doubtful Accounts during the current year:

What amount should appear in the allowance for doubtful accounts in the December 31,

balance sheet for the current year?

34) At the beginning of the year, a company’s balance sheet reported the following

balances: Total Assets = $125,000; Total Liabilities = $75,000; and Owner’s Capital =

$50,000. During the year, the company reported revenues of $46,000 and expenses of

$30,000. In addition, owner’s withdrawals for the year totaled $20,000. Assuming no

other changes to owner’s capital, the balance in the owner’s capital account at the end of

the year would be:

A.$66,000

B.$86,000

C.$(4,000)

D.$46,000

E.$54,000

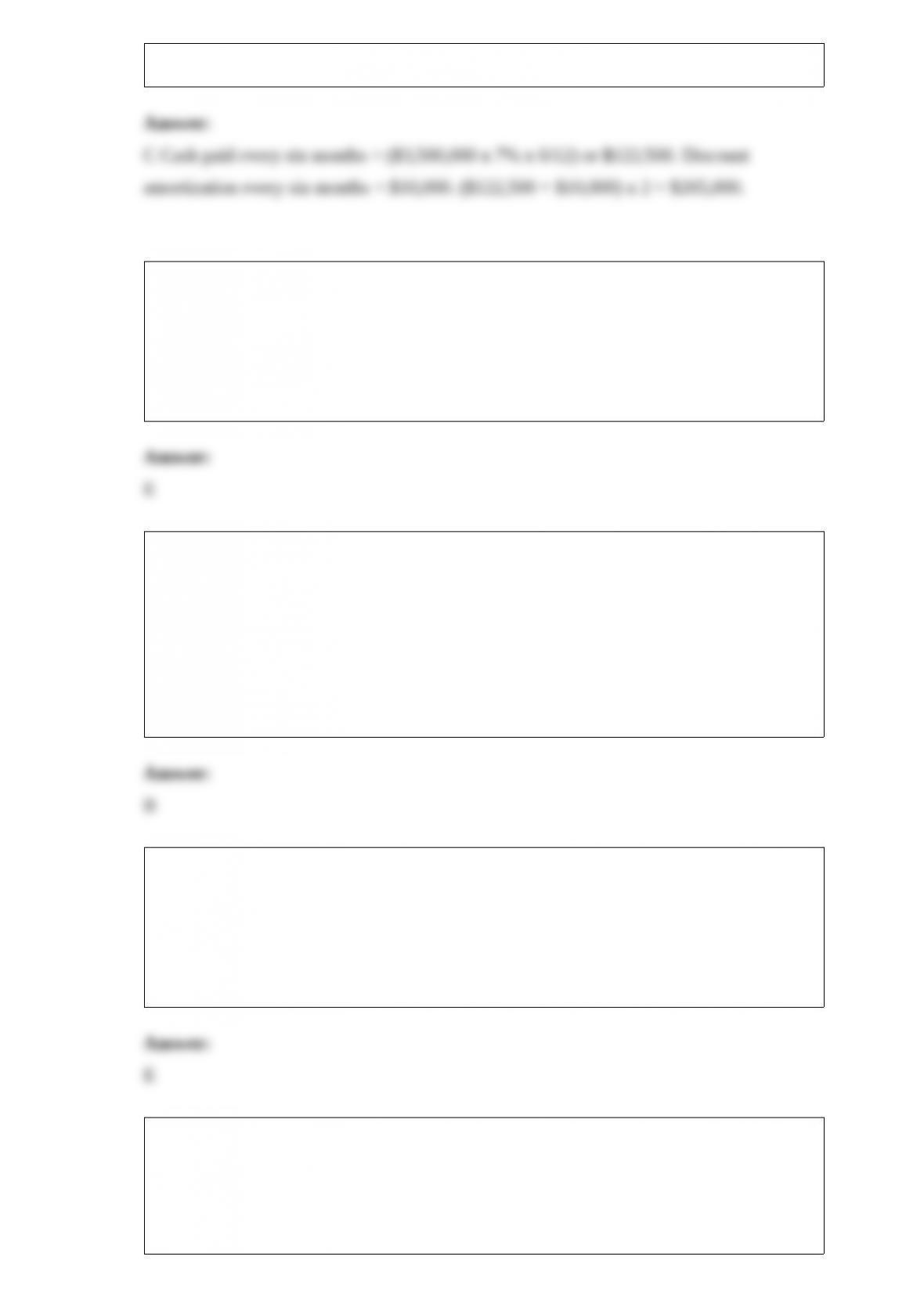

35) On January 1 of Year 1, Drum Line Airways issued $3,500,000 of par value bonds

for $3,200,000. The bonds pay interest semiannually on January 1 and July 1. The

contract rate of interest is 7% while the market rate of interest for similar bonds is 8%.

The bond premium or discount is being amortized at a rate of $10,000 every six

months.

The amount of interest expense recognized by Drum Line Airways on the bond issue in

Year 1 would be:

A.$132,500

B.$225,000

C.$265,000

D.$245,000

E.$280,000

36) Pledging receivables:

A.Allows firms to raise cash

B.Allows a firm to retain ownership of its receivables

C.Does not transfer risk of bad debts to the lender

D.Should be disclosed in the financial statements

E.All of these

37) A company had revenues of $75,000 and expenses of $62,000 for the accounting

period. The owner withdrew $8,000 in cash during the same period. Which of the

following entries could not be a closing entry?

A.Debit Income Summary $13,000; credit Owner’s, Capital $13,000

B.Debit Income Summary $75,000; credit Revenues $75,000

C.Debit Revenues $75,000; credit Income Summary $75,000

D.Debit Income Summary $62,000, credit Expenses $62,000

E.Debit Owner’s, Capital $8,000, credit Owner’s, Withdrawals $8,000

38) Which of the following statements about budgeting is false?

A.Budgeting is an aid to planning and control

B.Budgets create standards for performance evaluation

C.Budgets help coordinate the activities of the entire organization

D.Budgeting forces managers to think ahead and formalize long-range objectives

E.The master budget should only be prepared by top management

39) Total asset turnover is calculated by dividing:

A.Gross profit by average total assets

B.Average total assets by gross profit

C.Net sales by average total assets

D.Average total assets by net sales

E.Net assets by total assets

40) A company issues at par 9% bonds with a par value of $100,000 on April 1, which

is 4 months after the most recent interest date. The cash received for accrued interest on

April 1 by the bond issuer is:

A.$750

B.$5,250

C.$1,500

D.$3,000

E.$6,000

41) A record of the increases and decreases in a specific asset, liability, equity, revenue,

or expense is a(n):

A.Journal

B.Posting

C.Trial balance

D.Account

E.Chart of accounts

42) Liabilities:

A.Must be certain

B.Must sometimes be estimated

C.Must be for a specific amount

D.Must always have a definite date for payment

E.Must involve an outflow of cash

43) When the maker of a note honors a note this indicates that the note is:

A.Signed

B.Paid in full

C.Guaranteed

D.Notarized

E.Cosigned

44) A subsidiary ledger that contains a separate account for each supplier (creditor) to

the company is a(n):

A.Controlling account

B.Accounts receivable ledger

C.Accounts payable ledger

D.General ledger

E.Special journal

45) PRO, Inc. had the following activities during its most recent period of operations:

(a) Purchased raw materials on account for $140,000 (both direct and indirect materials

are recorded in the Raw Materials Inventory account).

(b) Issued raw materials to production of $130,000 (80% direct and 20% indirect).

(c) Incurred and paid factory labor costs of $250,000 cash; allocated the factory labor

costs to production (70% direct and 30% indirect).

(d) Incurred factory utilities costs of $20,000; this amount is still payable.

(e) Applied overhead at 80% of direct labor costs.

(f) Recorded factory depreciation, $22,000.

46) The following information is available for Holland Company at December 31:

Based on this information, Holland Company should report Cash and Cash Equivalents

on December 31 of:

A.$35,421

B.$50,421

C.$37,546

D.$36,246

E.$40,439

47) The sales level at which a company neither earns a profit nor incurs a loss is the:

A.Relevant range

B.Margin of safety

C.Step-wise variable level

D.Break-even point

E.Contribution margin

48) Bonds that have interest coupons attached to their certificates, which the

bondholders detach during each interest period and present to a bank for collection, are

called:

A.Coupon bonds

B.Callable bonds

C.Serial bonds

D.Convertible bonds

E.Registered bonds

49) What is the proper adjusting entry at December 31, the end of the accounting

period, if the balance in the prepaid insurance account is $7,750 before adjustment, and

the unexpired amount per analysis of policies is, $3,250?

A.Debit Insurance Expense, $3,250; credit Prepaid Insurance, $3,250

B.Debit Insurance Expense, $4,500; credit Prepaid Insurance, $4,500

C.Debit Prepaid Insurance, $4,500; credit Insurance Expense, $4,500

D.Debit Insurance Expense, $7,750; credit Prepaid Insurance, $7,750

E.Debit Cash, $7,750; Credit Prepaid Insurance, $7,750

50) Brown Company’s contribution margin ratio is 24%. Total fixed costs are $84,000.

What is Brown’s break-even point in sales dollars?

A.$20,160

B.$110,526

C.$350,000

D.$240,000

E.$84,000

51) Teller purchased merchandise from TechCom on October 17 of the current year and

TechCom accepted Teller’s $4,800, 90-day, 10% note. What entry should TechCom

make on December 31, to record the accrued interest on the note?

A.Debit Cash $20; credit Notes Receivable $20

B.Debit Cash $100; credit Notes Receivable $100

C.Debit Interest Receivable $20; credit Interest Revenue $20

D.Debit Interest Receivable $100; credit Interest Revenue $100

E.Debit Cash $120; credit Interest Revenue $100; credit Interest Receivable $20

52) Griggs Company uses the direct write-off method of accounting for uncollectible

accounts receivable. On December 6, Year 1, Griggs sold $6,300 of merchandise to the

Hillman Company. On August 8, Year 2, after numerous attempts to collect the account,

Griggs determined that the $6,300 account of the Hillman Company was uncollectible.

a. Prepare the journal entry required to record the transactions on August 8.

b. Assuming that the $6,300 is material, explain how the direct write-off method

violates the matching principle in this case.

53) The following information relating to a company’s overhead costs is available.

Based on this information, the total overhead variance is:

Based on this information, the total overhead variance is:

A.$7,000 favorable

B.$6,000 favorable

C.$1,000 unfavorable

D.$6,000 unfavorable

E.$1,000 favorable

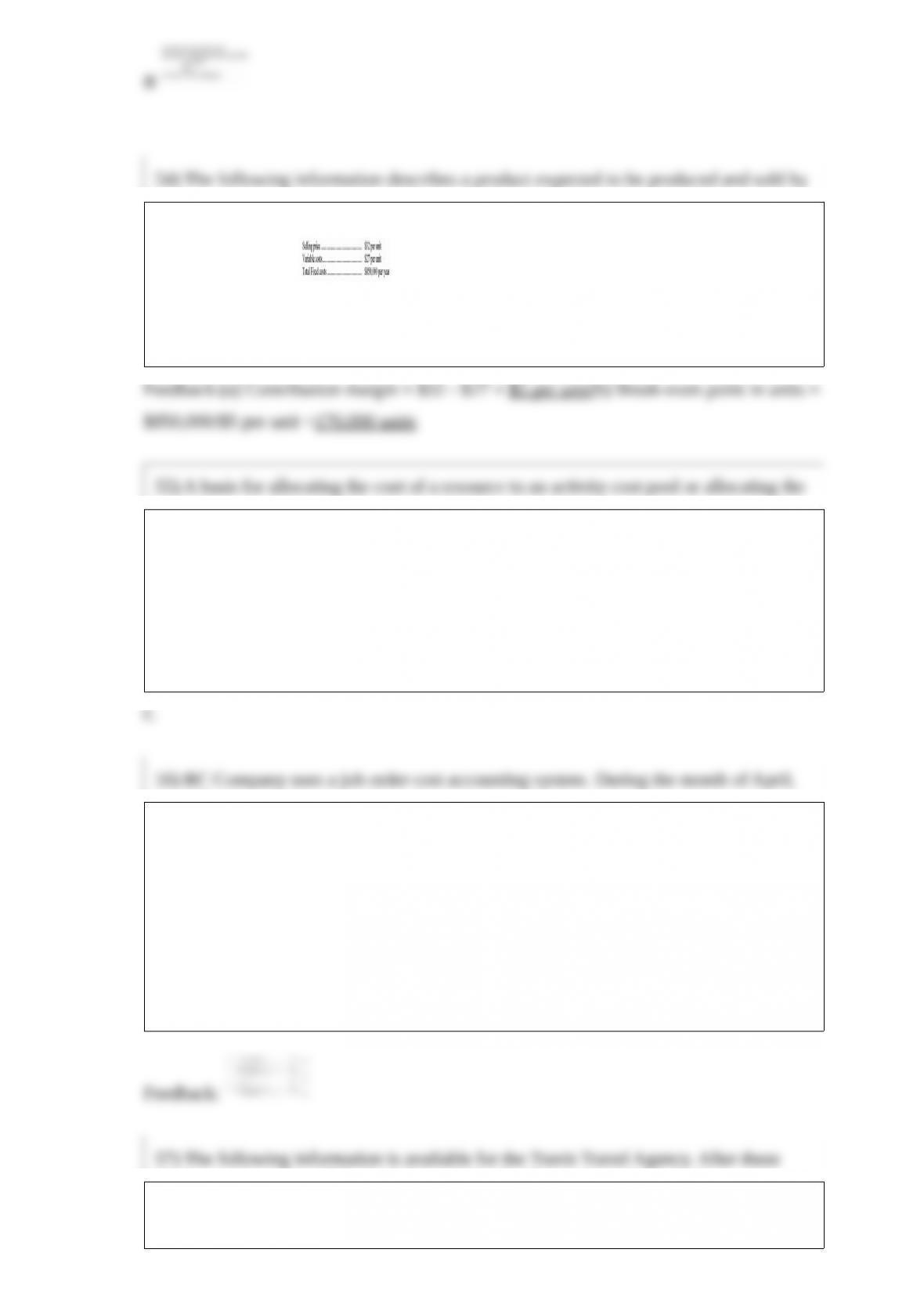

54) The following information describes a product expected to be produced and sold by

Pepin Corporation:

Required:

(a) Calculate the contribution margin per unit.

(b) Calculate the break-even point in units.

55) A basis for allocating the cost of a resource to an activity cost pool or allocating the

cost of an activity cost pool to a cost object is a(n):

A.Direct factor

B.Indirect factor

C.Cost driver

D.Joint cost

E.Opportunity cost

56) BC Company uses a job order cost accounting system. During the month of April,

the following events occurred:

(a) Purchased raw materials on credit, $32,000.

(b) Raw materials requisitioned: $25,800 as direct materials and $10,500 indirect

materials.

(c) Paid factory payroll for the month totaling $37,700 which includes $8,200 indirect

labor.

(d) Assigned the factory payroll to jobs and overhead.

Make the necessary journal entries to record the above transactions and events.

57) The following information is available for the Travis Travel Agency. After these

closing entries what will be the balance in the Jay Travis, Capital account?

A.$65,000

B.$80,000

C.$130,000

D.$145,000

E.$280,000

58) Josephine’s Bakery had the following assets and liabilities at the beginning and end

of the current year:

If Josephine invested an additional $12,000 in the business during the year, but

withdrew no assets during the year, what was the amount of net income earned by

Josephine’s Bakery?

59) What are the accounting basics for debt securities, including recording their

acquisition, interest earned, and their disposal?

60) The following information refers to Annie’s Attic and its competitors in the antiques

business.

61) Define liabilities and explain the difference between current and long-term

liabilities.

62) The amounts and timing of payment from a buyer to a seller are the

___________________.