1) IFRS permits some capitalization of internally generated intangible assets, if it is

probable there will be a future benefit and the amount can be readily measured.

2) The payout ratio is determined by dividing cash dividends paid to common

stockholders by net income available to common stockholders.

3) Under U.S. GAAP, impairment loss is measured as the excess of the carrying amount

over the assets discounted cash flow.

4) Revenues, gains, and distributions to owners all increase equity.

5) Periodic alterations to existing products are an example of research and development

costs.

6) The fair value of an asset retirement obligation is recorded as both an increase to the

related asset and a liability.

7) The MD&A section must provide information about the effects of inflation and

changing prices, if they are material to financial statement trends.

8) The inventory turnover ratio is computed by dividing the cost of goods sold by the

ending inventory on hand.

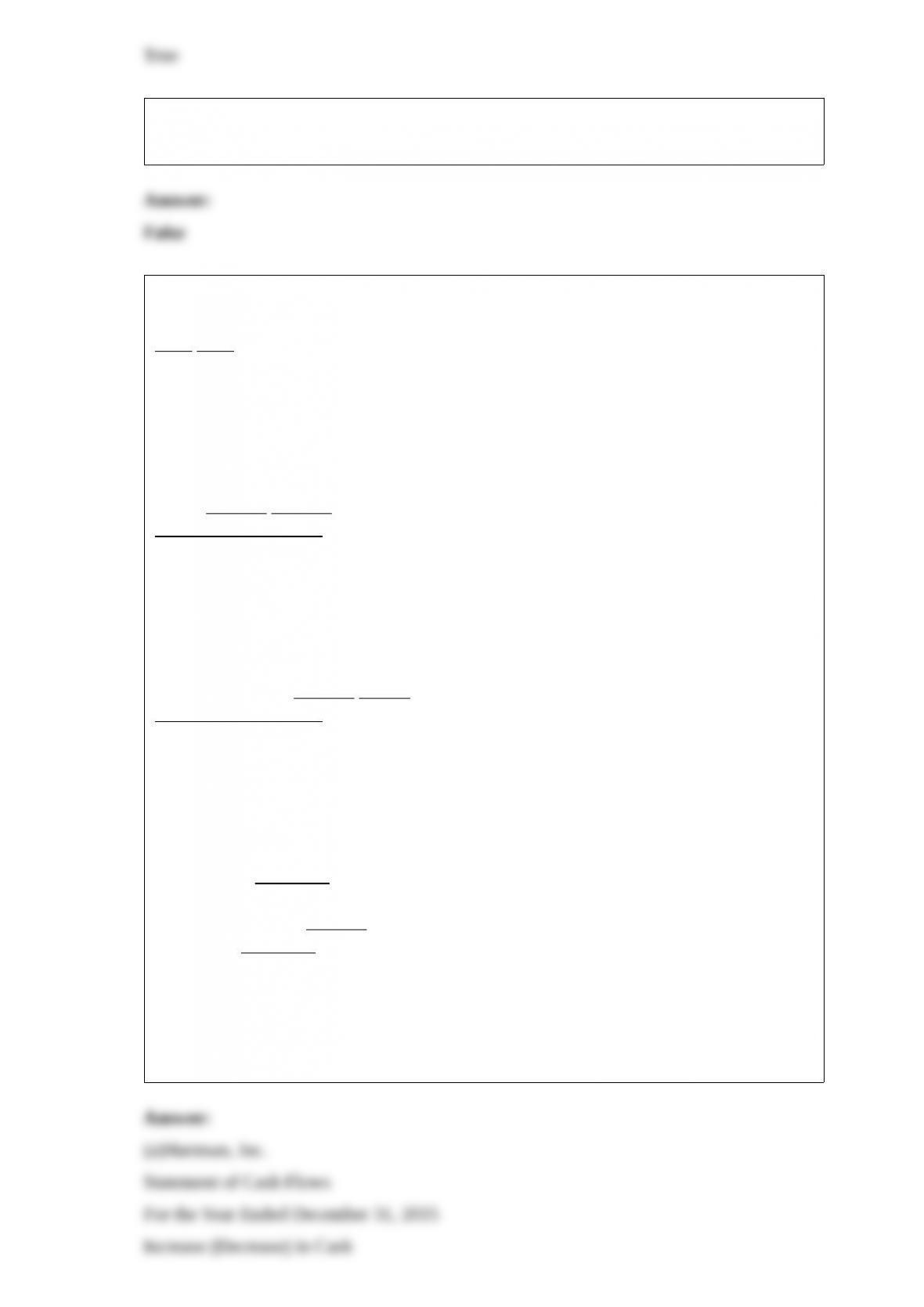

9) Hartman, Inc. has prepared the following comparative balance sheets for 2014 and

2015:

2015 2014

Cash$ 292,000$ 153,000

Accounts receivable149,000117,000

Inventory150,000180,000

Prepaid expenses18,00027,000

Plant assets1,275,0001,050,000

Accumulated depreciation(450,000)(375,000)

Patent 153,000 174,000

$1,587,000$1,326,000

Accounts payable$ 153,000$ 168,000

Accrued liabilities60,00042,000

Mortgage payable450,000

Preferred stock525,000

Additional paid-in capitalpreferred120,000

Common stock600,000600,000

Retained earnings 129,000 66,000

$1,587,000$1,326,000

1>The Accumulated Depreciation account has been credited only for the depreciation

expense for the period.

2>The Retained Earnings account has been charged for dividends of $148,000 and

credited for the net income for the year.

The income statement for 2015 is as follows:

Sales revenue$1,980,000

Cost of sales 1,089,000

Gross profit891,000

Operating expenses 680,000

Net income$ 211,000

Instructions

(a)From the information above, prepare a statement of cash flows (indirect method) for

Hartman, Inc. for the year ended December 31, 2015 .

(b)From the information above, prepare a schedule of cash provided by operating

activities using the direct method.

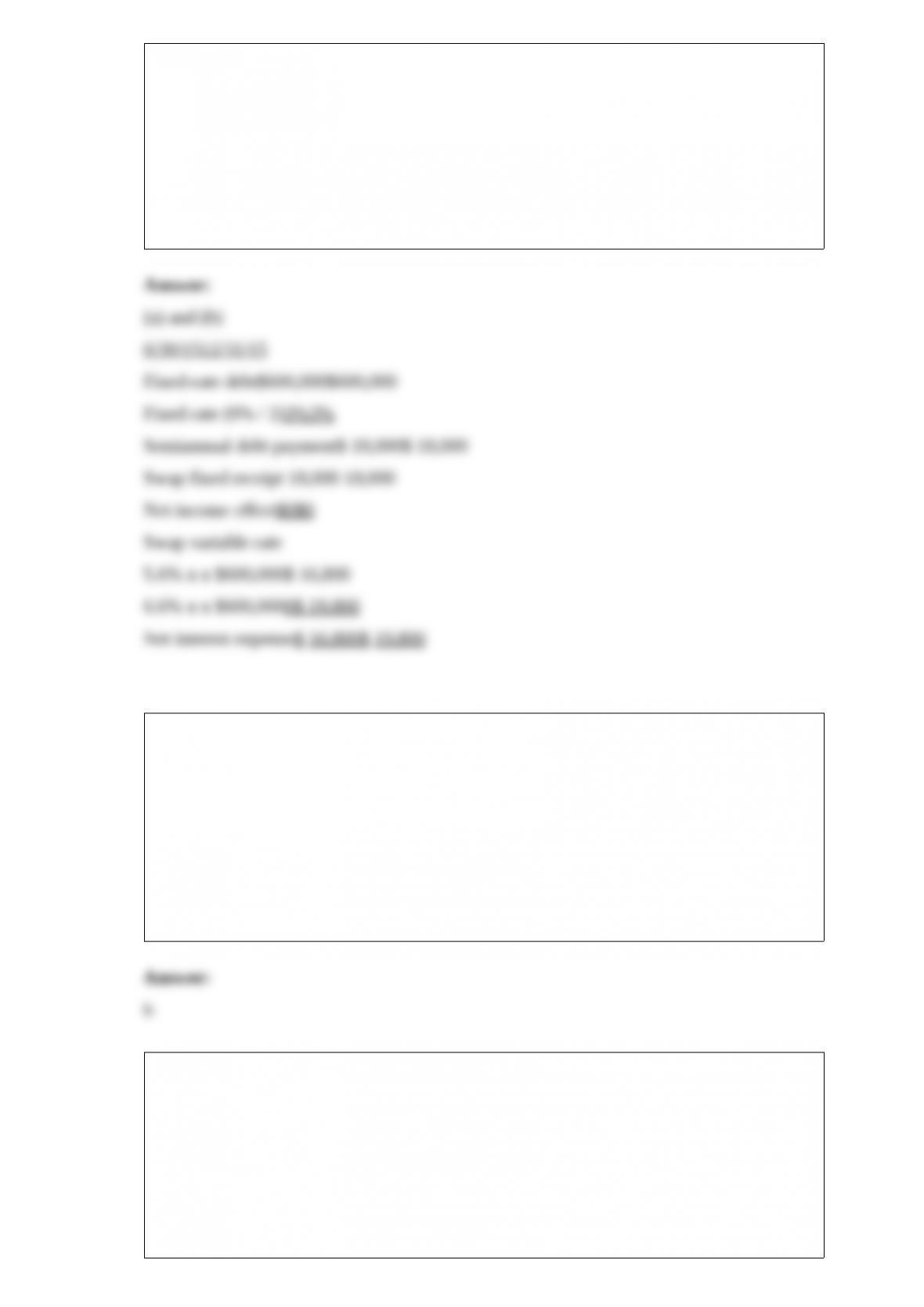

10) On January 2, 2015, Tylor Company issued a 4-year, $600,000 note at 6% fixed

interest, interest payable semiannually. Tylor now wants to change the note to a variable

rate note. As a result, on January 2, 2015, Tylor Company enters into an interest rate

swap where it agrees to receive 6% fixed and pay LIBOR of 5.6% for the first 6 months

on $600,000. At each 6-month period, the variable interest rate will be reset. The

variable rate is reset to 6.6% on June 30, 2015 .

Instructions

(a)Compute the net interest expense to be reported for this note and related swap

transaction as of June 30, 2015 .

(b)Compute the net interest expense to be reported for this note and related swap

transaction as of December 31, 2015 .

11) On January 2, 2015, Mize Co. issued at par $300,000 of 9% convertible bonds.

Each $1,000 bond is convertible into 60 shares. No bonds were converted during 2015 .

Mize had 100,000 shares of common stock outstanding during 2015 . Mize ‘s 2015 net

income was $240,000 and the income tax rate was 30%. Mize’s diluted earnings per

share for 2015 would be (rounded to the nearest penny)

a.$2.03

b.$2.19

c.$2.26

d.$2.40

12) Melton Company sold some machinery to Addison Company on January 1, 2014 .

The cash selling price would have been $947,700. Addison entered into an installment

sales contract which required annual payments of $250,000, including interest at 10%,

over five years. The first payment was due on December 31, 2014 . What amount of

interest income should be included in Melton’s 2015 income statement (the second year

of the contract)?

a.$25,000

b.$79,247

c.$50,000

d.$69,770

13) Younger Company has outstanding both common stock and nonparticipating,

non-cumulative preferred stock. The liquidation value of the preferred is equal to its par

value. The book value per share of the common stock is unaffected by

a.the declaration of a stock dividend on preferred payable in preferred stock when the

market price of the preferred is equal to its par value

b.the declaration of a stock dividend on common stock payable in common stock when

the market price of the common is equal to its par value

c.the payment of a previously declared cash dividend on the common stock

d.a 2-for-1 split of the common stock

14) The following data concerning the retail inventory method are taken from the

financial records of Welch Company.

Cost Retail

Beginning inventory$ 147,000$ 210,000

Purchases672,000960,000

Freight-in18,000

Net markups60,000

Net markdowns42,000

Sales1,008,000

Assuming no change in the price level if the LIFO inventory method were used in

conjunction with the data, the ending inventory at cost would be

a.$127,800

b.$126,000

c.$122,400

d.$129,600

15) An accountant wishes to find the present value of an annuity of $1 payable at the

beginning of each period at 10% for eight periods. The accountant has only one present

value table which shows the present value of an annuity of $1 payable at the end of

each period. To compute the present value, the accountant would use the present value

factor in the 10% column for

a.seven periods

b.eight periods and multiply by (1 + .10)

c.eight periods.

d.nine periods and multiply by (1 .10)

16) Dicer uses the conventional retail method to determine its ending inventory at cost.

Assume the beginning inventory at cost (retail) were $260,000 ($396,000), purchases

during the current year at cost (retail) were $1,370,000 ($2,200,000), freight-in on these

purchases totaled $86,000, sales during the current year totaled $2,000,000, and net

markups (markdowns) were $48,000 ($72,000). What is the ending inventory value at

cost?

a.$371,228

b.$378,092

c.$386,804

d.$572,000

17) On December 31, 2014, Gonzalez Company granted some of its executives options

to purchase 150,000 shares of the companys $10 par common stock at an option price

of $50 per share. The Black-Scholes option pricing model determines total

compensation expense to be $1,125,000. The options become exercisable on January 1,

2015, and represent compensation for executives services over a three-year period

beginning January 1, 2015 . At December 31, 2015 none of the executives had

exercised their options. What is the impact on Gonzalezs net income for the year ended

December 31, 2015 as a result of this transaction under the fair value method?

a.$ 375,000 increase

b.$1,125,000 decrease

c.$ 375,000 decrease

d.$0

18) Which of the following principles best describes the current method of accounting

for research and development costs?

a.Associating cause and effect

b.Systematic and rational allocation

c.Income tax minimization

d.Immediate recognition as an expense

19) Which of the following publications does not qualify as a statement of generally

accepted accounting principles?

a.Statements of financial standards issued by the FASB

b.Accounting interpretations issued by the FASB

c.APB Opinions

d.Accounting research studies issued by the AICPA

20) How should an unusual event not meeting the criteria for an extraordinary item be

disclosed in the financial statements?

a.Shown as a separate item in operating revenues or expenses if material and combined

with other items if not material in amount

b.Shown in operating revenues or expenses if material but not shown as a separate item

c.Shown net of income tax after ordinary net earnings but before extraordinary items

d.Shown net of income tax after extraordinary items but before net earnings