The principal issue to be resolved in cases involving alleged negligence is usually

A) the amount of the damages suffered by the plaintiff.

B) whether to impose punitive damages on the defendant.

C) the level of care required to be exercised.

D) whether the defendant was involved in fraud.

There are many elements of quality control at the firm level. Which element does

“adequate hiring policies (and documentation of their implementation) that ensure

competence and integrity of personnel should be in place” belong to?

A) leadership and responsibilities within the firm

B) independence

C) general human resource policies

D) extent of professional development

In the auditing environment, failure to meet generally accepted auditing standards is

often

A) an accepted practice.

B) a suggestion of negligence.

C) strong evidence of negligence.

D) tantamount to criminal behaviour.

Why is it important to separate systems development (or acquisition) and program

maintenance activities from accounting?

A) Accounting personnel have the expertise to evaluate program changes that have been

implemented.

B) Custody of media is important to help ensure ongoing operations.

C) This allows accounting to reconcile transaction totals to transaction details.

D) Lack of separation could result in unauthorized changes to programs and systems.

When setting the objectives for auditing notes, the auditor should consider inherent

risks associated with

A) recording errors.

B) uncollectible notes.

C) duplicated notes.

D) management bias.

Which of the following internal controls would help ensure that existing payroll

transactions are recorded?

A) Time records are approved by supervisors

B) Time clock is used to record time

C) Independent preparation of payroll bank reconciliation

D) Comparison of payroll master file totals with general ledger control account

An example of an audit procedure that relates to the auditor’s understanding of internal

control is

A) reperform the counting of physical inventory.

B) inspect documents and records.

C) recalculate the depreciation expenses.

D) trace all legal expenses to supporting invoices.

A risk of material misstatement in accounts receivable associated with the allocation

balance-related audit objective is that “long term service revenue is recorded as current

revenue or in the wrong period, overstating revenue and accounts receivable.” Which of

the following tests of detail of balances would respond to this risk?

A) read customer contracts and audit the criteria used to allocate revenue to components

of the sales contract

B) check cash received after the year end and trace to accounts receivable master file

C) read the notes to the financial statements and compare to audited financial

information

D) inquire of management about the process used to make sure that revenue is recorded

in the correct period

An important reason for auditors to obtain a good knowledge of a client’s industry is

that

A) payroll processing functions could differ from client to client.

B) control risks will vary from zero to 100% and can be better assessed in context.

C) detection risk must be set in accordance with the needs of the industry as well as of

the individual client.

D) organizations like city governments have unique accounting requirements that could

be complex.

“Independence” in auditing means

A) remaining aloof from the client.

B) not being financially dependent on the client.

C) impartiality in performing professional services.

D) being an advocate for the client.

A common way for a public accounting firm to demonstrate its defence of a lack of

duty to perform is by use of a(n)

A) engagement letter.

B) letter of representation.

C) confirmation letter.

D) expert witness.

Audit risk is assessed for

A) the financial statements as a whole and is not usually allocated to various accounts

or objectives.

B) the financial statements as a whole and then allocated to various accounts.

C) various accounts but not for the financial statements as a whole.

D) various accounts and objectives, and the sum is then assigned to the financial

statements as a whole.

Negative confirmations of accounts receivable is less effective than positive

confirmations of accounts receivable because

A) a majority of recipients usually lack the willingness to respond objectively.

B) some recipients may report incorrect balances that require extensive follow-up.

C) the auditor cannot infer that all nonrespondents have verified their account

information.

D) negative confirmations do not produce evidential matter that is statistically

quantifiable.

The following are two unrelated situations. For each situation outline possible

deviations (if any) from a standard auditor’s report that may be necessary, and give

reasons. State your assumptions.

A) Rosebud Ltd. is a construction company that builds and repairs greenhouses for

nurseries. An architect does the design, and three different small construction

companies are used to build the greenhouses. You are concerned that some of the

projects that span the April year end may result in material losses, even though income

has been reported in the coming year. Management has refused permission for you to

enter construction sites, as they feel that the construction sites will be dangerous and

they do not want to be exposed to such liability.

B) Save our Trees is a charitable organization devoted to maintaining national

woodland and green space. Fund raising is handled primarily by means of electronic

mail and door to door canvassing by volunteers. Volunteers conducting canvassing

provide receipts at the door using prenumbered receipts. Funds raised by email are sent

receipts by email.

When the auditor would like to improve the efficiency of the audit by focusing work on

transactions that may be more subject to material error in a particular area of the

population, the auditor will use

A) block testing.

B) haphazard sample selection.

C) random sample selection.

D) stratified sample selection.

Which of the following procedures would ordinarily be expected to best reveal

unrecorded sales at the balance sheet date?

A) Compare shipping documents with sales invoices.

B) Apply gross profit rates to inventory disposed of during the period.

C) Trace payments received subsequent to the balance sheet date.

D) Send accounts receivable confirmation requests.

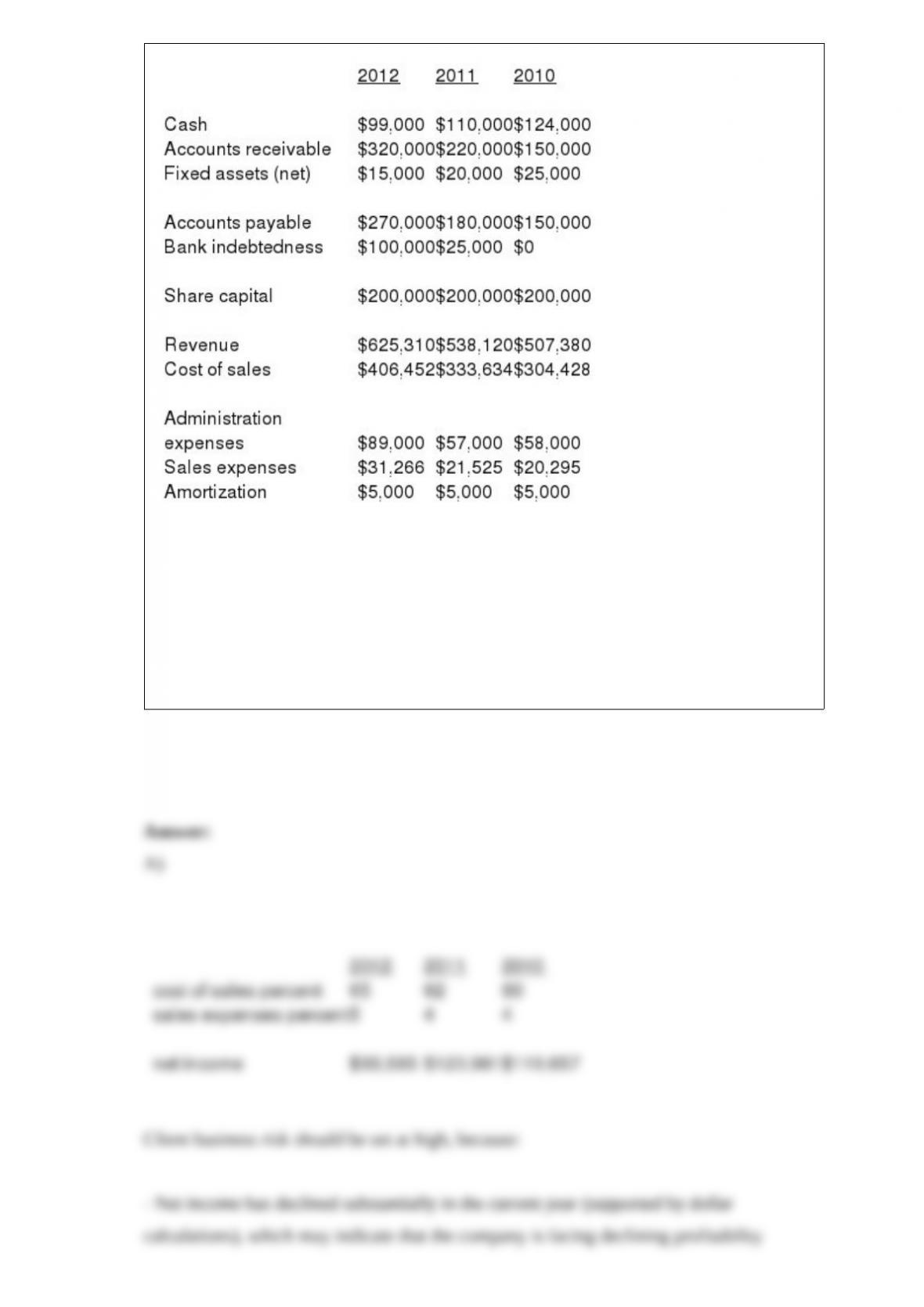

Mugsy Brights Limited (MBL) is a private company in Winnipeg that sells mugs, jars

and bottles in a variety of colours, sizes and materials. MBL is owned by four equal

owners since inception. The owners have different skills – creative design, marketing,

finance and information systems. The company attributes much of its success to the use

of materials that can be easily shipped without breaking, and unique designs that appeal

to a variety of buyers, particularly commercial buyers who purchase for restaurants, or

for businesses who choose to advertise their business by giving away or selling regular

or travel mugs.

The owners meet formally every month, and have informal meetings two or three times

per week to discuss particular clients or new approaches. About a quarter of the sales

are via the company’s secure web site, while the remainder are by telephone or purchase

order. MBL works with distributors of kitchenware, selling wholesale to hundreds of

outlets in Canada. Most of these sales are done via the telephone, although a

salesperson does spend some time in major cities across the country visiting some of

the large customers, helping with shelf layout and marketing to the ultimate consumers

for larger distributors. These efforts have resulted in gradually increasing market share

for the company.

All sales are recorded in the accounting software package used by the company. The

accounting manager reports directly to one of the owners, and there are two other

employees in the accounting department. Password controls are used to limit functions

that are accessible by employees. For example, only the controller can implement wage

rate increases or product price increases (which are reviewed and approved by the

owner responsible for marketing). Two owners are required to sign cheques, and do so

with source documents attached. Similarly, two owners are required to approve new

employees.

All manufacturing is outsourced to local producers who work with different materials.

For example, a different supplier handles steel mugs versus plastics or glass. Ceramics

is rarely used as it is quite breakable, whereas some forms of glass are very durable.

MBL does not hold any inventory, as manufacturing is all done to order. However, as

there have been some collection problems from customers, the company has had to go

to the maximum of its line of credit, and has no additional borrowing capacity

available. It is waiting for the results of the audited financial statements to approach the

bank for an increase in its line of credit.

Internet sales are prepared (via credit card), while sales to distributors are net thirty. The

company has an April year end.

Following are extracts from the annual financial statements:

Required:

A) What audit risk would you assign to the company? Why? [Tip: Do some calculations

and consider client business risk.]

B) Calculate preliminary materiality. Justify your decision of materiality base and

choice of materiality.

Which of the following situations would indicate increased inherent risk in the accounts

payable and acquisition cycle?

A) good quality internal controls for cash handling

B) the use of packaged software for accounting (including accounts payable)

C) the use of clear, standard terms when negotiating supplier discounts

D) significant related party transactions

CAS 320 (Materiality in planning and performing an audit) defines materiality in terms

of three key concepts. The first and second concepts are that a material misstatement

should be considered in the context of knowledgeable users and the effect on decision

making and that material is relative to circumstances surrounding the decision and

nature of the information. The third concept is

A) that the auditor should consider users of financial statements as a group.

B) that the auditor should consider users of financial statements individually.

C) that the users should be informed and approve of the materiality used by the auditor.

D) that the auditor should be conservative in setting the materiality level.

Management safeguards assets by

A) having the internal auditors conduct periodic counts of physical assets.

B) controlling access and by comparison of physical items to records.

C) requiring the external auditors to do surprise audits.

D) having management sign a management representation letter.

A) Many auditors prove the subsequent period bank statement if a cutoff statement is

not received directly from the bank. Discuss the purpose of proving the subsequent

period statement, and explain the audit procedures performed during the proof of cash.

B) Discuss the circumstances in which an auditor would prepare a proof of cash.

The auditor has a responsibility to review transactions and activities occurring after the

year-end to determine whether anything occurred that might affect the valuation or

disclosure of the statements being audited. The auditing procedures required to verify

these transactions are commonly referred to as the review for

A) contingent liabilities.

B) subsequent year’s transactions.

C) late unusual occurrences.

D) subsequent events.

The controls over purchase requisitions and the related purchase orders are evaluated

and tested as part of the

A) inventory and distribution cycle.

B) acquisitions and payments cycle.

C) human resources and payroll cycle.

D) capital acquisitions cycle.

To ensure that employees remain independent, an audit firm should

A) ask employees to sign a form confirming that they do not have an investment in a

company that they are auditing.

B) prohibit an employee from the Toronto office to have an investment in a company

audited by the Hong Kong branch of the PA firm.

C) include a section in the code of conduct indicating that the employees should not

invite their client to dinner.

D) refuse an audit mandate where the cousin of a staff member works in the marketing

department.

The primary objective of analytical procedures used in the final review stage of an audit

is to

A) obtain evidence from details tested to corroborate particular assertions.

B) identify areas that represent specific risks relevant to the audit.

C) assist the auditor in looking for potential material misstatements.

D) satisfy doubts when questions arise about a client’s ability to continue in existence.

Which of the following audits can be regarded as being solely “compliance” audits?

A) Canada Revenue Agency’s examinations of the returns of taxpayers

B) the Auditor General’s evaluation of the computer operations of governmental units

C) an internal auditor’s review of his employer’s payroll authorization procedures

D) a public accounting firm’s audit of the local school district

The working papers prepared during the engagement are the property of the

A) auditor, but do not include the working papers prepared by the client for the auditor.

B) auditor, even including those prepared by the client for the auditor.

C) client, who will provide copies to the auditor.

D) auditor and client jointly.

A four-column proof of cash can be performed for

A) one or more interim months.

B) the entire year.

C) the last month of the year.

D) any specified time period for which bank statements are available and which the

auditor chooses to designate.

What is the first step that the auditor takes when auditing the valuation of inventory?

A) conduct analytical review, comparing gross margin for the current year to the prior

year

B) do an industry analysis to determine whether there is a potential for

technology-induced obsolescence

C) ask the client about the level of obsolete inventory that was on hand and counted

during the inventory count

D) establish clearly the valuation method used and how the calculations are being

performed

The auditor has decided that there is a risk of material misstatement with respect to

sales revenue. Which of the following audit tests should the auditor use to quantify the

potential error?

A) discuss the process used to assign credit limits with the sales manager and the

controller

B) send external confirmations to customers with accounts receivable balances

C) determine whether all sales tested have a supporting customer purchase order

D) determine whether all sales tested have a matching bill of lading

A) There are several internal controls in the human resources and personnel function

that are important from an audit perspective. For example, there should be an adequate

investigation of the competence and trustworthiness of new employees. Discuss other

internal controls in the personnel and employment function that are important from an

audit perspective.

B) There are several key internal controls over the timekeeping and payroll preparation

function that should be present. For example, adequate control over the time on

employees’ time records includes the use of a time clock or other method of making

certain that employees are paid for the number of hours they worked. Discuss other key

internal controls over the timekeeping and payroll preparation function.

C) There are several key internal controls over the payment of payroll function that

should be present. For example, the payroll should be distributed by someone who is

not involved in the other payroll functions. Discuss other key internal controls over the

payment of payroll function.

What is an important benefit of independent preparation of bank reconciliations?

A) An opportunity to independently check that cheques have two signatures

B) The client being able to check that the bank is processing transactions correctly

C) The ability to internally verify cash receipts and disbursements transactions

D) The best time to carefully serially account for cheques issued

Comparing bad debt expense as a percentage of gross sales with previous years will

detect what kind of possible misstatement?

A) cut-off errors in recording cash receipts

B) overstatement of sales and accounts receivable

C) understatement of sales and accounts receivable

D) understatement of allowance for uncollectible accounts

When conducting a review engagement, how is materiality calculated?

A) materiality is not calculated as a lower level of assurance is being provided

B) the concept of significance is used, rather than the concept of materiality

C) always as a percentage of net income before income taxes

D) in the same manner as an audit engagement

Identify and describe each of the three parts to the Code of Professional Conduct. Also

discuss which parts are officially enforceable and which are not.

You are having lunch with a former employee of your firm, a friend of yours. Gino had

been laid off last year when he had failed to pass his professional examinations for the

third year in a row. Gino told you that he managed to obtain a CMA designation in the

past year, and has started his public practice.

He has been circulating flyers and electronic email announcements with fixed rates:

$400 for a compilation engagement, $1,000 for a review, and $5,000 for an audit where

revenues are less than $1 million, $15,000 for an audit for a client with revenues up to

$5 million. He already has clients to keep him busy for the next three months. He even

has some feelers for clients that he personally handled while he was working for your

firm – there were a lot of contacts developed during the five years that he was working

there! To help attract some of the larger clients, he is considering not charging any fee

for the first ten hours spent on tax-related services.

Gino ended the conversation by asking you if you would like to join him in his new

firm, because at this rate he’ll need a second person real soon!

Required:

Identify the violations in the professional rules of conduct and explain why they are

violations.

Define “direct reporting engagements.”

Discuss three factors that affect client business risk, and therefore audit risk.

State three types of information that should be included in a standard letter of inquiry of

client’s law firms.

Explain four different variations that could occur in unqualified audit reports. For each

variation, state how the auditor’s report is affected and provide an example.

State the four audit concerns for capital stock and describe how the auditor typically

verifies each of these areas.

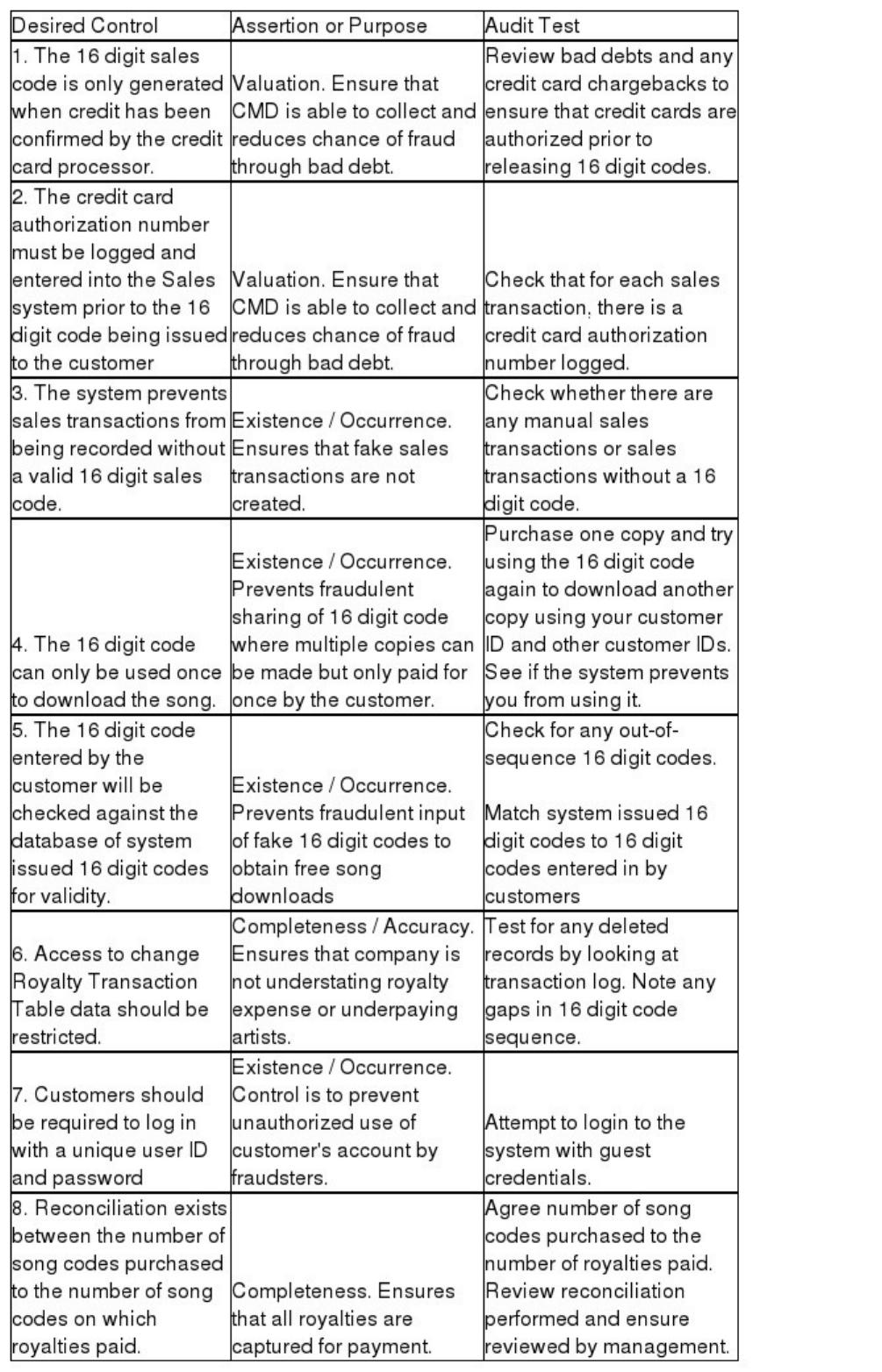

You have just been assigned to manage the audit for a new large client of your firm,

Cheap Music Downloads Inc. (CMD). CMD is a subsidiary of a client of your firm that

manufactures audio and video equipment for international distribution. CMD has been

in operation for two years, when its custom information systems were established.

CMD runs a web site that allows customers to order songs using their credit card only.

There are tens of thousands of small transactions daily. Once the credit card has been

authorized by the credit card processing intermediary, CMD’s web sales system

generates a 16 digit sequential code that the customer uses to access the song via the

web site. CMD will then record both the sale and the royalty for the song.

Quarterly, CMD remits royalties to artists based upon the number of copies of the song

that has sold, if the accumulated royalty exceeds $25.00 for that artist. Artist royalties

that do not exceed $25.00 will be paid every two years if there has not been a payment

during that time.

All contracted royalty rates, artist names and song titles are recorded in CMD’s database

tables.

Required:

Describe three internal controls that should exist over sales or royalty transactions or

over the database tables. For each control:

(i) State the control

(ii) Describe (not just state) the audit assertion associated with the control

(or state the purpose of the control)

(iii) Provide an audit test that you could use to test the control

Define “attest engagements.”

State the three main reasons why it is essential that working papers be thoroughly

reviewed by another member of the audit firm at the completion of the audit.

You are the auditor of Brody Grass Inc. The CEO expressed a concern that the audit

fees for the year were very high. You then explained that this is largely due to poor

internal controls in the cash and transaction cycle and that the audit fees could decrease

if better controls were in place.

Provide 5 examples of general cash account controls that Brody Grass Inc. could

implement.

Discuss the methodology for designing tests of details of balances for inventory.

Identify and explain the three determinants of the persuasiveness of evidence.

First Global is a public company. You are currently performing the audit of the owner’s

equity section and you have been asked to write a short memo about the control

weaknesses you have identified and the potential risk attached to each weakness.

First Global is a public company since March of the current year as it underwent an IPO

during the year. The corporation has been implementing various controls with regards

to keeping records of the company, but it is still a growing company, and Sasha, the

equity accountant, has been having a tough time learning all the new regulations,

keeping the records up to date and ensuring that the dividend payments are made on

time.

First Global issued 2 classes of shares in the IPO. Class A shares with 10 votes were

issued to the Truman family so they could retain control and Class B shares with 1 vote

each were issued to the general public. When you reviewed the accounting records, you

noticed that they contained only one account for capital stocks.

Kimora is a senior manager at a public accounting firm. Kimora was assigned to the

audit of Toble Corp. Upon arriving at the client, Kimora met with the controller, Brad,

who was a classmate in college, 20 years ago. She had not been in contact with Brad

since college, but they realized that they still had many friends in common. Brad invited

Kimora to go to the company box to watch a hockey game and catch up.

Discuss the issue of independence between Kimora and Toble Corp.