The D Company develops, manufactures, distributes, and markets branded health care

products as well as private-label vitamin products in the United States and more than 50

other countries. A disclosure note from D’s 2014 annual report is shown below:

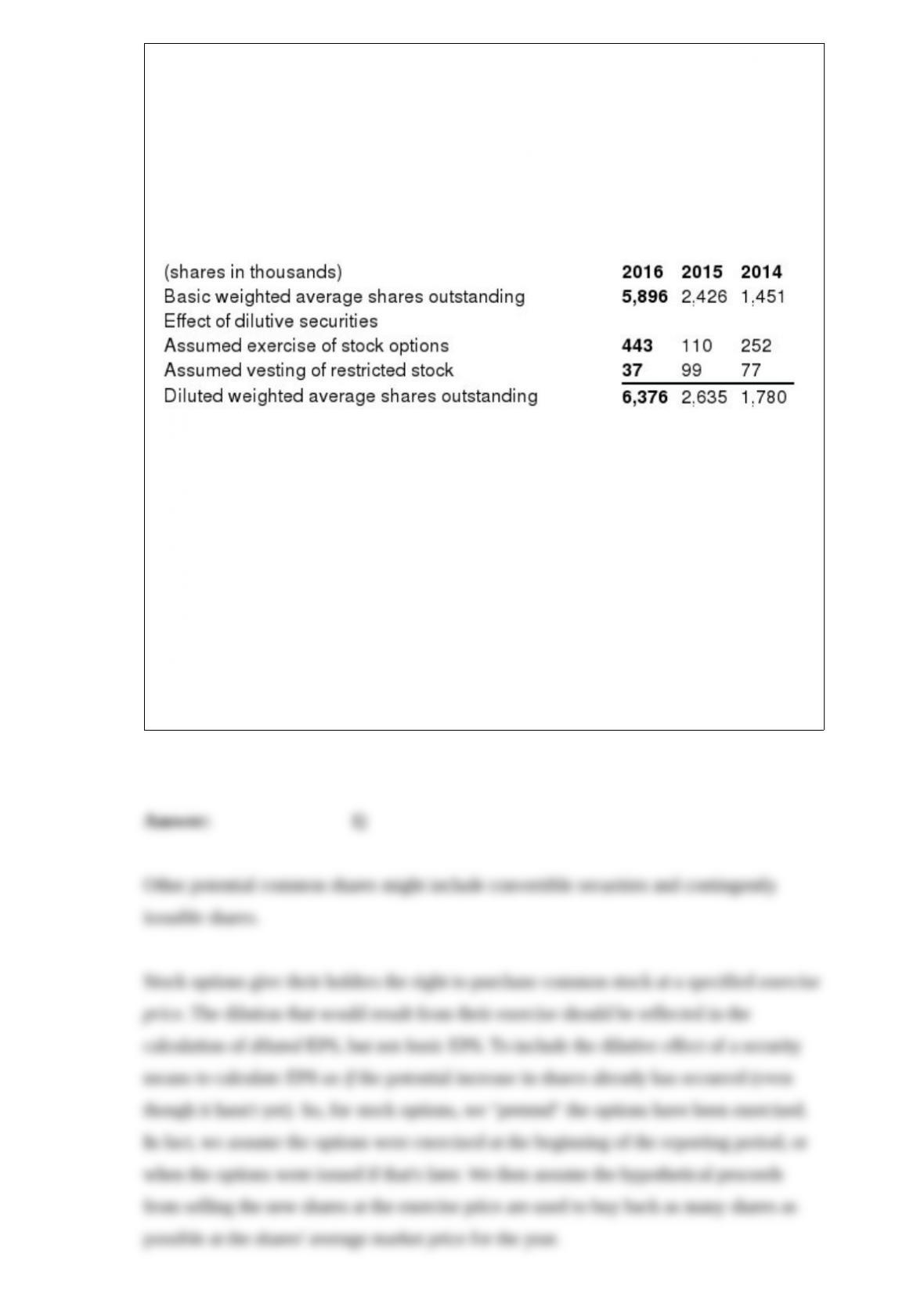

Weighted Average Shares Outstanding

The following table provides information about basic and diluted weighted average

shares outstanding:

The computations of diluted weighted average shares outstanding exclude 4 million

shares in fiscal year 2016, 2 million shares in fiscal year 2015 and 1 million shares in

fiscal year 2014 since the options were antidilutive.

Required:

1) The disclosure note shows adjustments for “assumed exercise of stock options and

assumed vesting of restricted stock.” What other adjustments might be needed? Explain

why and how these adjustments are made to the weighted-average shares outstanding.

2) The disclosure note indicates that the effect of some of the stock options were not

included because they would be antidilutive. What does that mean? Why not include

antidilutive securities?

Briefly explain what is meant by a subsequent event. Give two examples of subsequent

events.

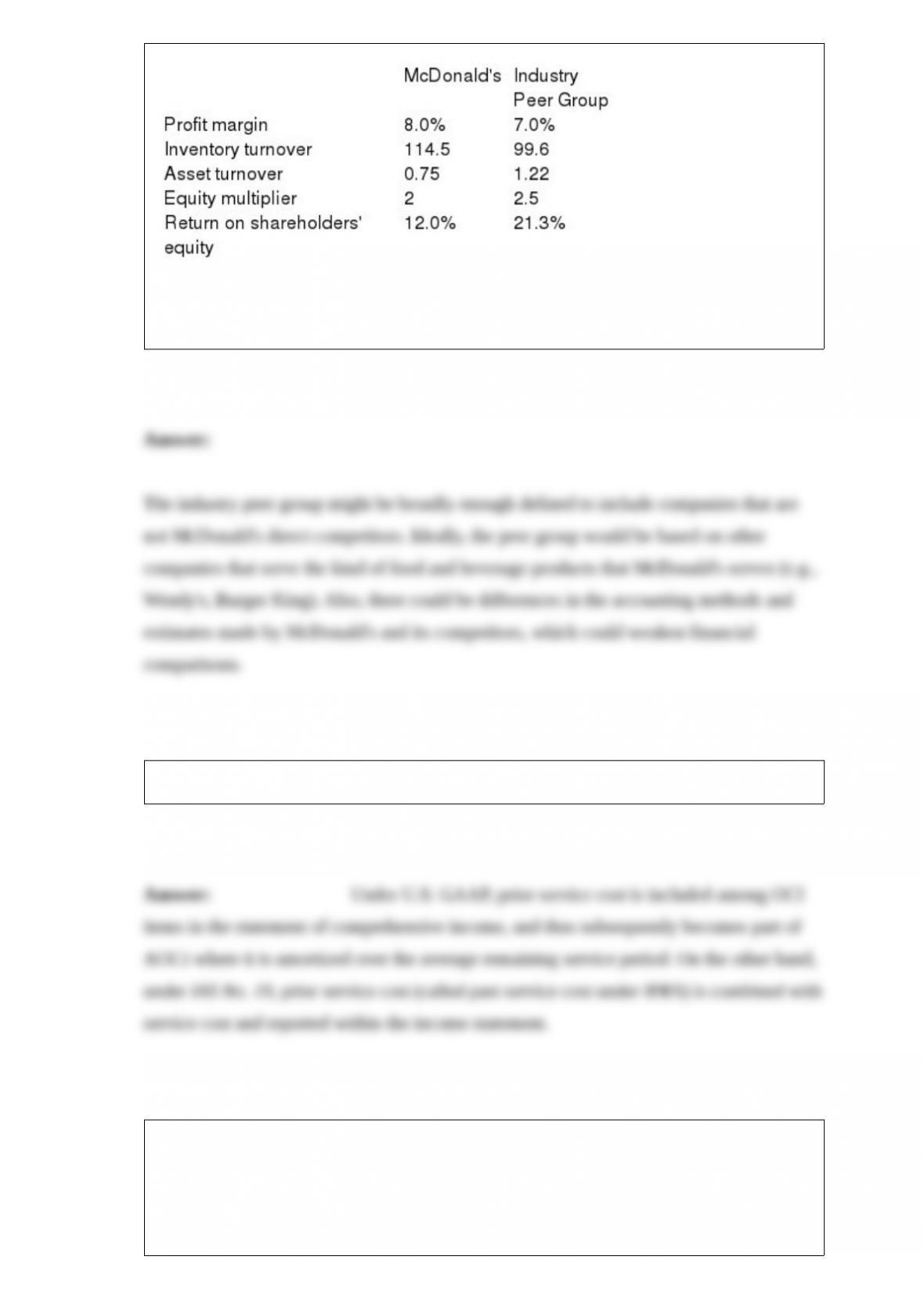

The following table presents a summary of ratio analysis for McDonald’s and averages

for their peer group:

Besides size differences, what other differences between McDonald’s and its industry

peer group could limit your ability to make meaningful comparisons about the

performance of McDonald’s from the data above?

How do U.S. GAAP and IFRS differ with regard to reporting prior service costs.

Companies can have accounts receivable from ordinary trade customers and from

related parties (e.g., directors, employees or large shareholders). How does U.S. GAAP

differ from IFRS in its requirements regarding separate disclosure of trade receivables

and related-party receivables? Why might separate disclosure of related party

receivables be useful?