1) Process costing is applied to operations with repetitive production and customized

products.

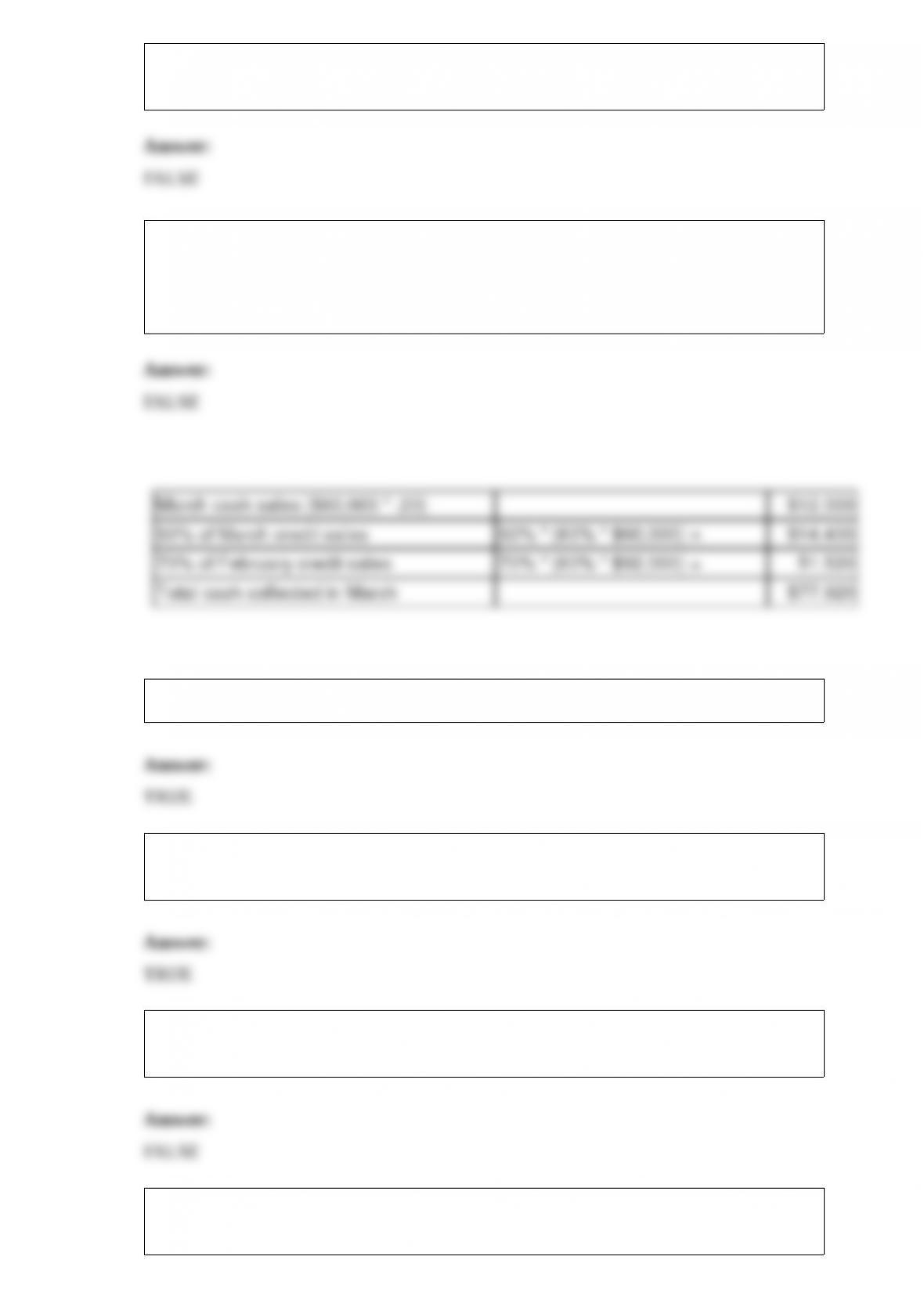

2) A company’s history indicates that 20% of its sales are for cash and the remaining

80% are on credit. Collections on credit sales are 30% in the month of the sale and 70%

the following month. Projected sales for January, February, and March are $75,000,

$92,000 and $60,000, respectively. The March expected cash receipts are $80,500.

3) Profit margin reflects the percent of net income in each dollar of net sales.

4) A potential lawsuit claim is disclosed when the claim can be reasonably estimated

and it is reasonably possible.

5) The date of record is the date that directors vote to pay a cash dividend to

shareholders.

6) The main difference between the cost of goods sold of a manufacturer and a

merchandiser is that the merchandiser includes cost of goods manufactured rather than

cost of goods purchased.

7) A stock dividend is a distribution of corporate assets that returns part of the original

investment to shareholders.

8) Paid-in capital is the total amount of cash and other assets the corporation receives

from its stockholders in exchange for its stock.

9) On January 1, a company issued a $500,000, 10%, 8-year bond payable, and received

proceeds of $473,845. Interest is payable each June 30 and December 31. The company

uses the straight-line method to amortize the discount. The amount of interest expense

to be recorded on June 30 is $25,000.

10) Ratios must refer to economically important relationships, such as a sale price

compared to its cost.

11) Hybrid costing systems can only be applied to auto manufacturing.

12) The primary purpose of the statement of cash flows is to report all major cash

receipts (inflows) and cash payments (outflows) during a period.

13) A company borrowed $16,000 by signing a 4-month promissory note at 12%. The

total interest on the note is $640.

14) A liability is a probable future payment of assets or services that a company is

presently obligated to make as a result of past transactions or events.

15) In process costing, the classification of materials as direct or indirect depends on

whether or not they are clearly linked with a specific process or department.

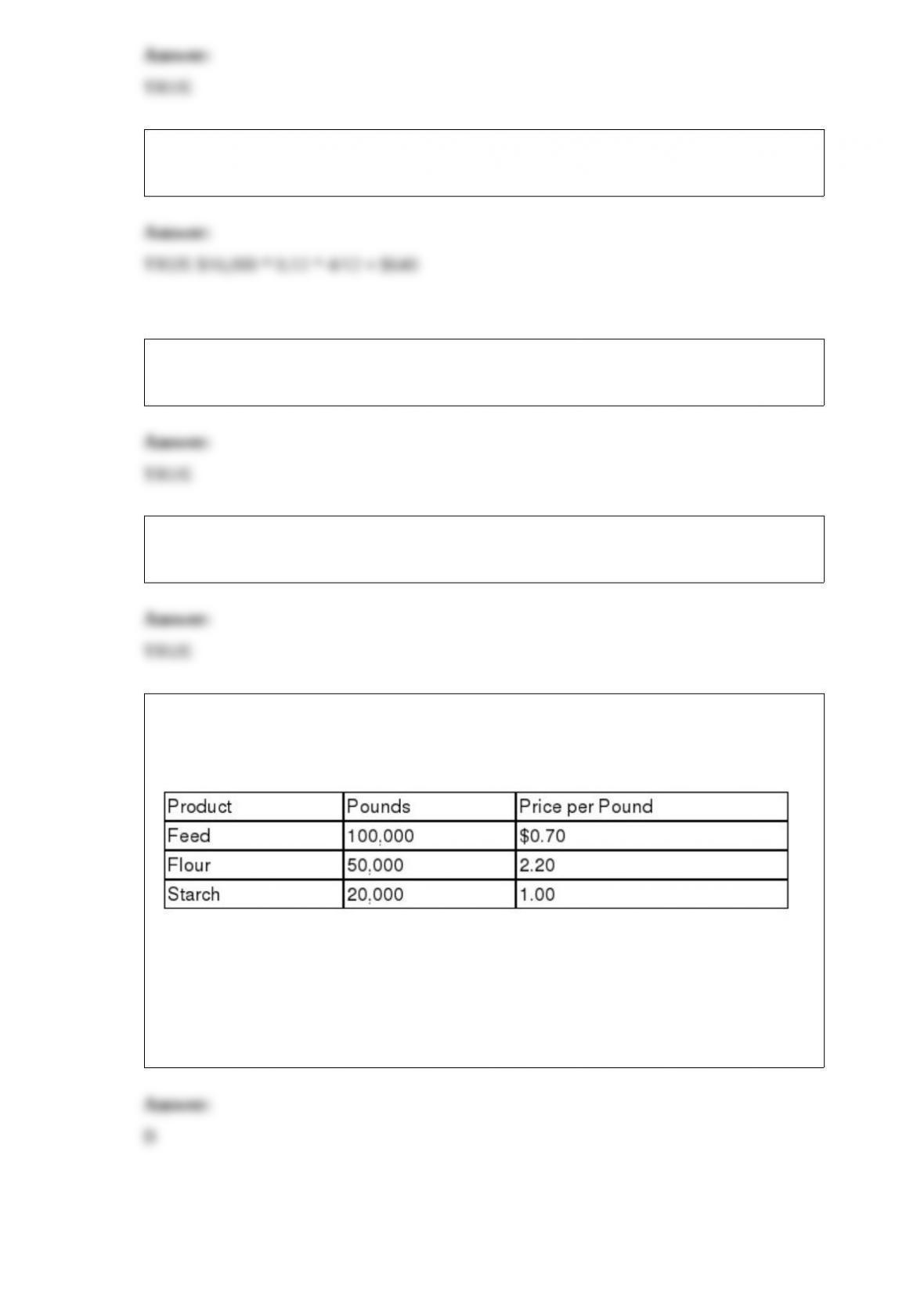

16) A granary allocates the cost of unprocessed wheat to the production of feed, flour,

and starch. For the current period, unprocessed wheat was purchased for $240,000, and

the following quantities of product and sales revenues were produced.

How much of the $240,000 cost should be allocated to feed?

A.$24,500.

B.$84,000.

C.$90,000.

D.$70,000.

E.$200,000.

17) An asset’s book value is $36,000 on January 1, Year 6. The asset is being

depreciated $500 per month using the straight-line method. Assuming the asset is sold

on July 1, Year 7 for $25,000, the company should record:

A.Neither a gain or loss is recognized on this type of transaction.

B.A gain on sale of $2,000.

C.A loss on sale of $1,000.

D.A gain on sale of $1,000.

E.A loss on sale of $2,000.

18) On January 1 of 2015, Parson Freight Company issues 7%, 10-year bonds with a

par value of $2,000,000. The bonds pay interest semi-annually. The market rate of

interest is 8% and the bond selling price was $1,864,097. The bond issuance should be

recorded as:

A.Debit Cash $2,000,000; credit Bonds Payable $2,000,000.

B.Debit Cash $1,864,097; credit Bonds Payable $1,864,097.

C.Debit Cash $2,000,000; credit Bonds Payable $1,864,097; credit Discount on Bonds

Payable $135,903.

D.Debit Cash $1,864,097; debit Discount on Bonds Payable $135,903; credit Bonds

Payable $2,000,000.

E.Debit Cash $1,864,097; debit Interest Expense $135,903; credit Bonds Payable

$2,000,000.

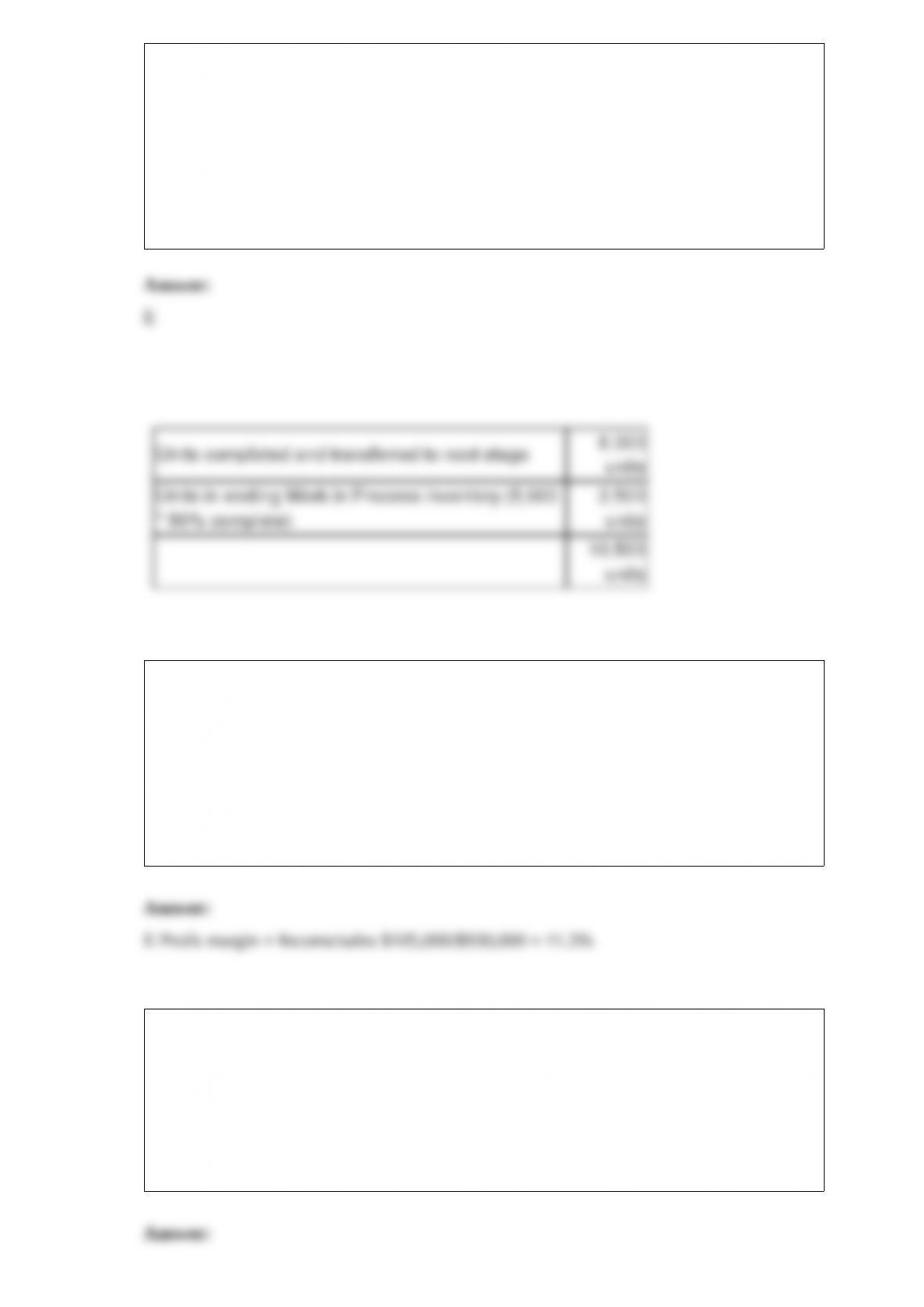

19) A production department’s output for the most recent month consisted of 8,000 units

completed and transferred to the next stage of production and 5,000 units in ending

Work in Process inventory. The units in ending Work in Process inventory were 50%

complete with respect to both direct materials and conversion costs. Calculate the

equivalent units of production for the month, assuming the company uses the weighted

average method.

A.6,500 units.

B.9,000 units.

C.13,000 units.

D.5,500 units.

E.10,500 units.

20) Kragle Corporation reported the following financial data for one of its divisions for

the year; average invested assets of $470,000; sales of $930,000; and income of

$105,000. The investment center profit margin is:

A.22.3%.

B.50.5%.

C.197.9%.

D.447.6%.

E.11.3%.

21) A company borrowed $80,000 from a bank by signing a long-term note payable.

The journal the transaction would be recorded in is the.

A.Cash disbursements journal.

B.Sales journal.

C.Cash receipts journal.

D.Purchases journal.

E.General journal.

22) On December 1, Watson Enterprises signed a $24,000, 60-day, 4% note payable as

replacement of an account payable with Erikson Company. What amount of interest

expense is accrued at December 31 on the note?

A.$0

B.$80

C.$320

D.$960

E.$160

23) The following information is available on a depreciable asset owned by Mutual

Savings Bank:

The asset’s book value is $70,000 on June 1, Year 3. On that date, management

determines that the asset’s salvage value should be $5,000 rather than the original

estimate of $10,000. Based on this information, the amount of depreciation expense the

company should recognize during the last six months of Year 3 would be:

A.$8,125.00

B.$7,375.00

C.$4,062.50

D.$3,750.00

E.$7,812.50

24) Cavern Company’s output for the current period results in a $5,250 unfavorable

direct material price variance. The actual price per pound is $56.50 and the standard

price per pound is $55.00. How many pounds of material are used in the current period?

A.5,393.

B.5,110.

C.3,500.

D.3,750.

E.4,000.

25) On April 1, Griffith Publishing Company received $1,548 from Santa Fe, Inc. for

36-month subscriptions to several different magazines. The company credited Unearned

Fees for the amount received and the subscriptions started immediately. What is the

adjusting entry that should be recorded by Griffith Publishing Company on December

31 of the first year?

A.debit Unearned Fees, $1,548; credit Fees Earned, $1,548.

B.debit Unearned Fees, $516; credit Fees Earned, $516.

C.debit Unearned Fees, $1,161; credit Fees Earned, $1,161.

D.debit Unearned Fees, $129; credit Fees Earned, $129.

E.debit Unearned Fees, $387; credit Fees Earned, $387.

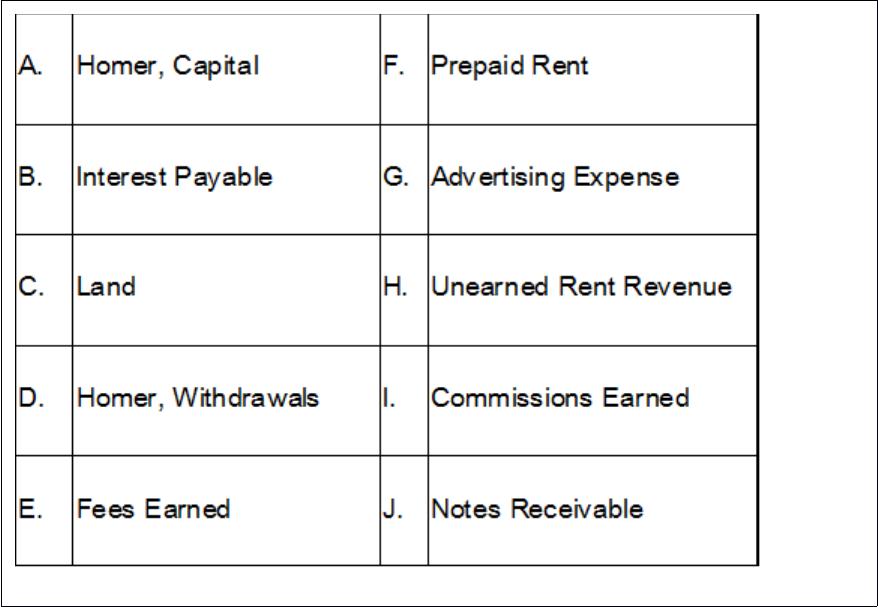

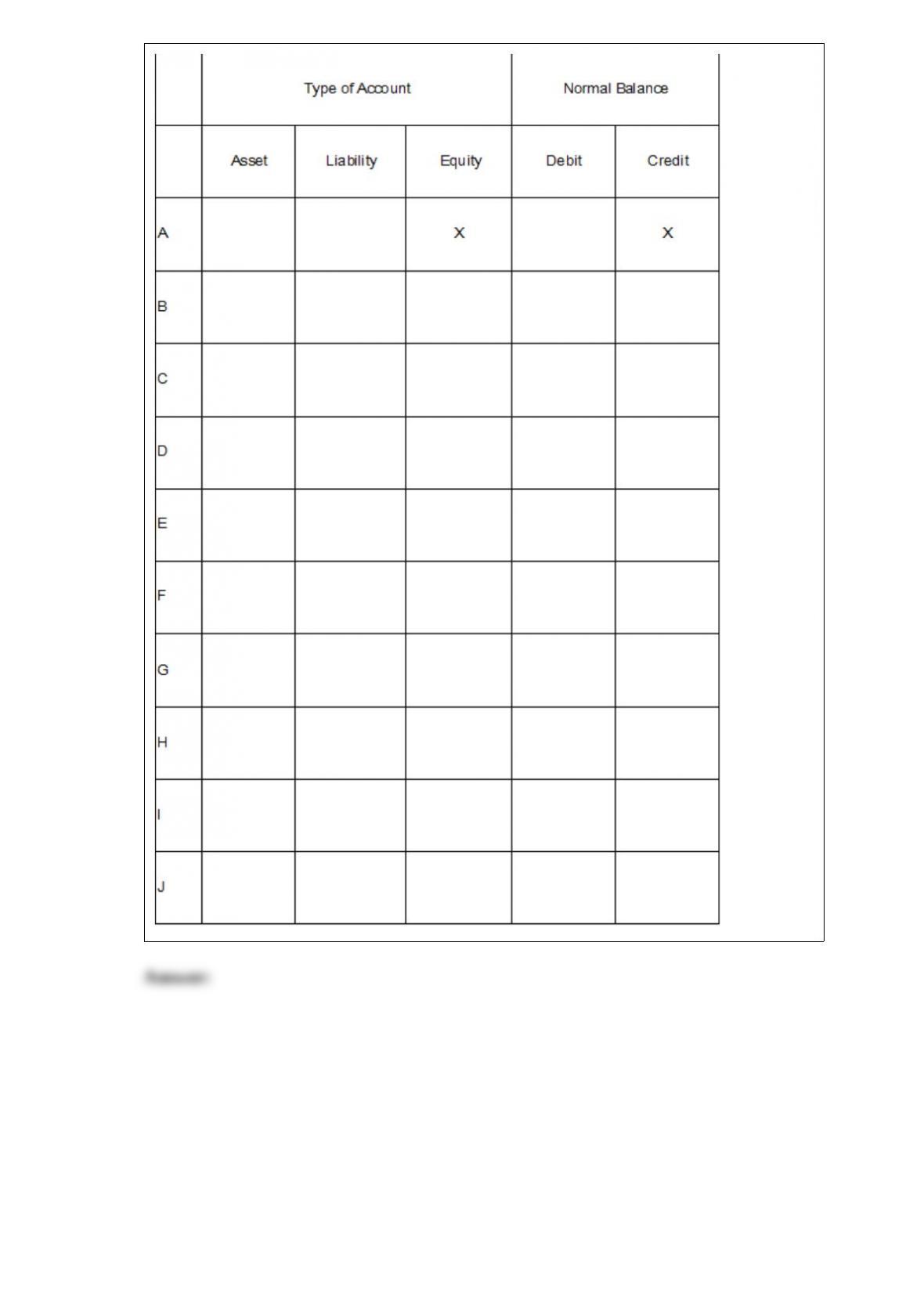

26) Using the following list of accounts and identification letters A through J for

Homer€s Management Co., enter the type of account and its normal balance into the

table below. The first item is filled in as an example:

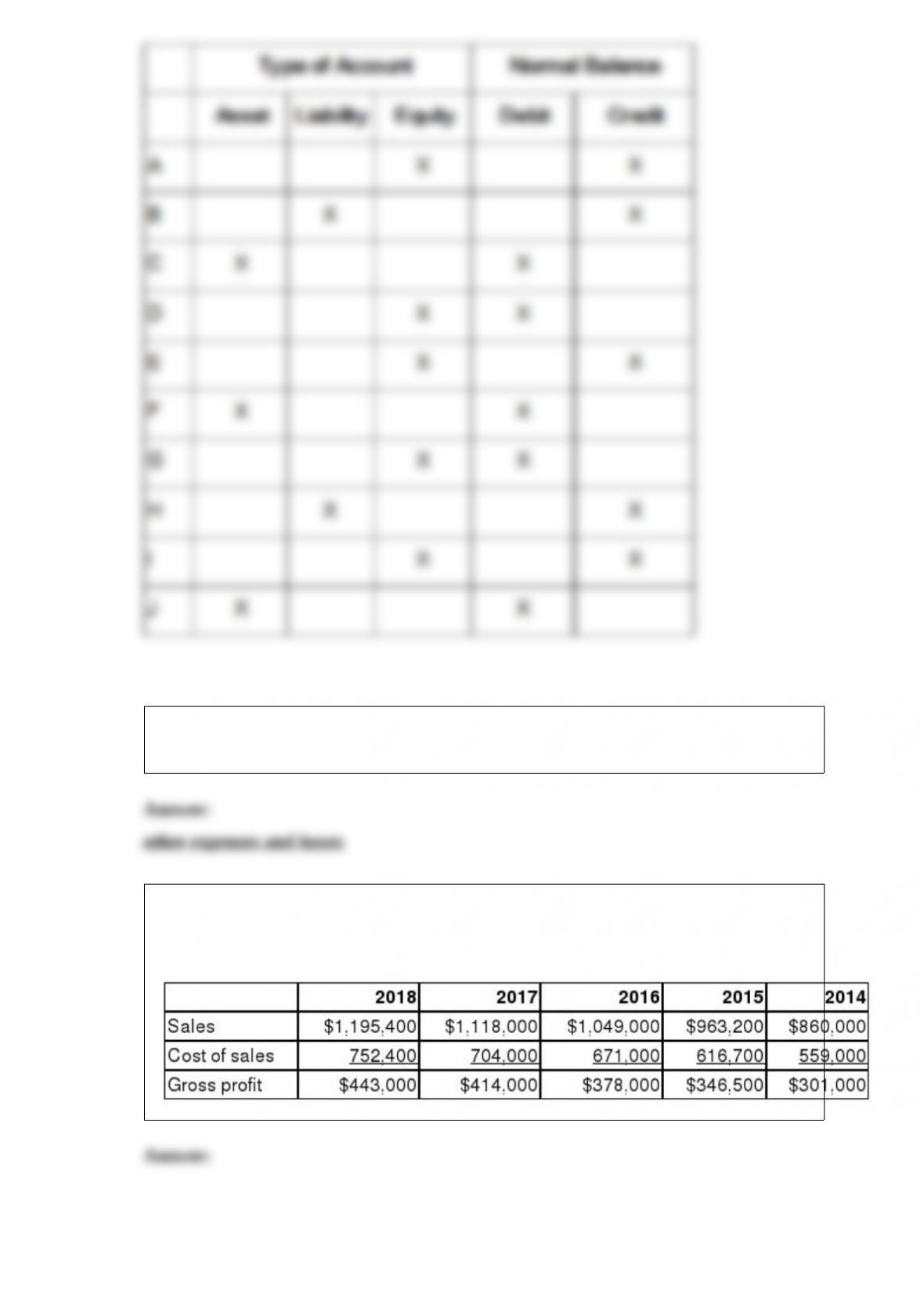

27) Non-operating activities that include interest expense, losses from asset disposals,

and casualty losses are reported as ____________________________.

28) For the following financial statement items, calculate trend percentages using 2014

as the base year:

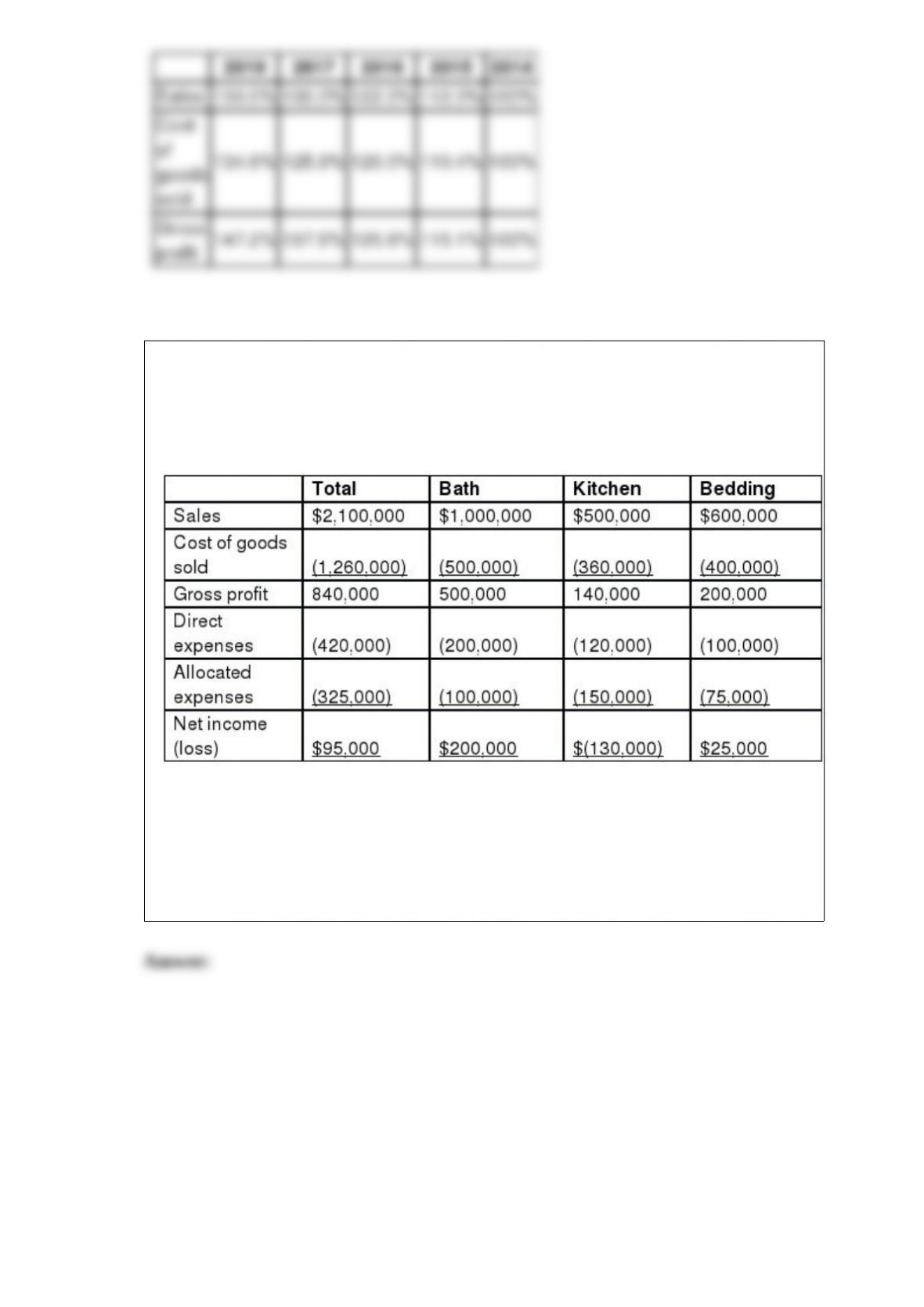

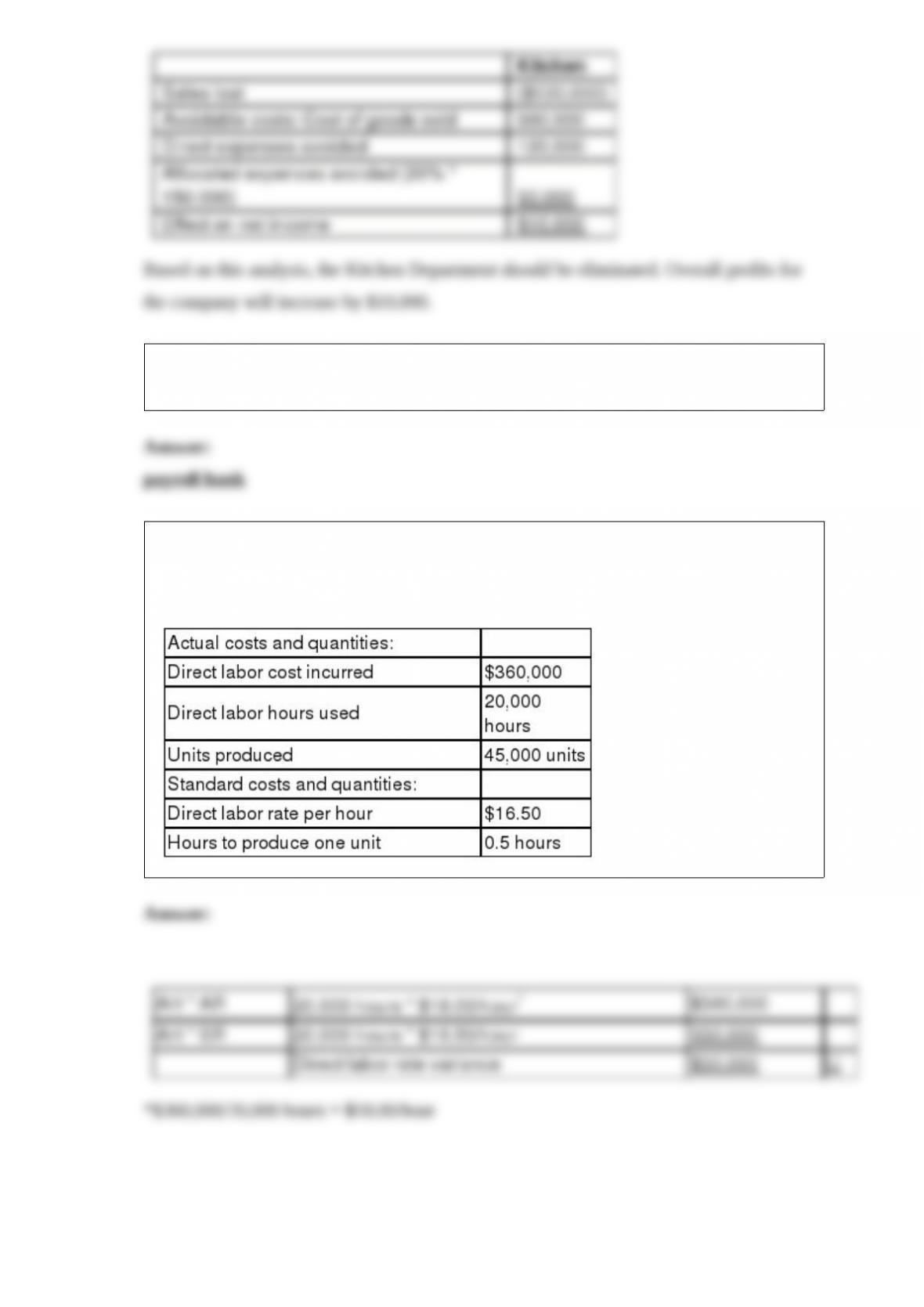

29) Luxury Linens has three departments: Bath, Kitchen, and Bedding. The most recent

income statement, showing the total operating profit and departmental results is shown

below:

Based on this income statement, management is considering eliminating the Kitchen

department. If the Kitchen department is eliminated, the other departments will expand

to fill the space but sales are not expected to change. Twenty percent of Kitchen’s

allocated expenses will be avoided due to restructuring and the remainder reallocated

equally to Bath and Bedding. Show an analysis indicating whether the Kitchen

department should be eliminated.

30) Companies with many employees often use a special ____________________

account to pay employees.

31) Use the following cost information to calculate the direct labor rate and efficiency

variances and indicate whether they are favorable or unfavorable.

32) When purchase costs regularly rise, the ___________________ method of

inventory valuation yields the lowest gross profit and net income, providing a tax

advantage.

33) Nutley Company uses a job order cost system and last period incurred $70,000 of

overhead and $100,000 of direct labor. Nutley estimates that its overhead next period

will be $65,000. The company also expects to incur $100,000 of direct labor. If Nutley

bases its overhead applied on direct labor cost, what should be the overhead rate for the

next period?