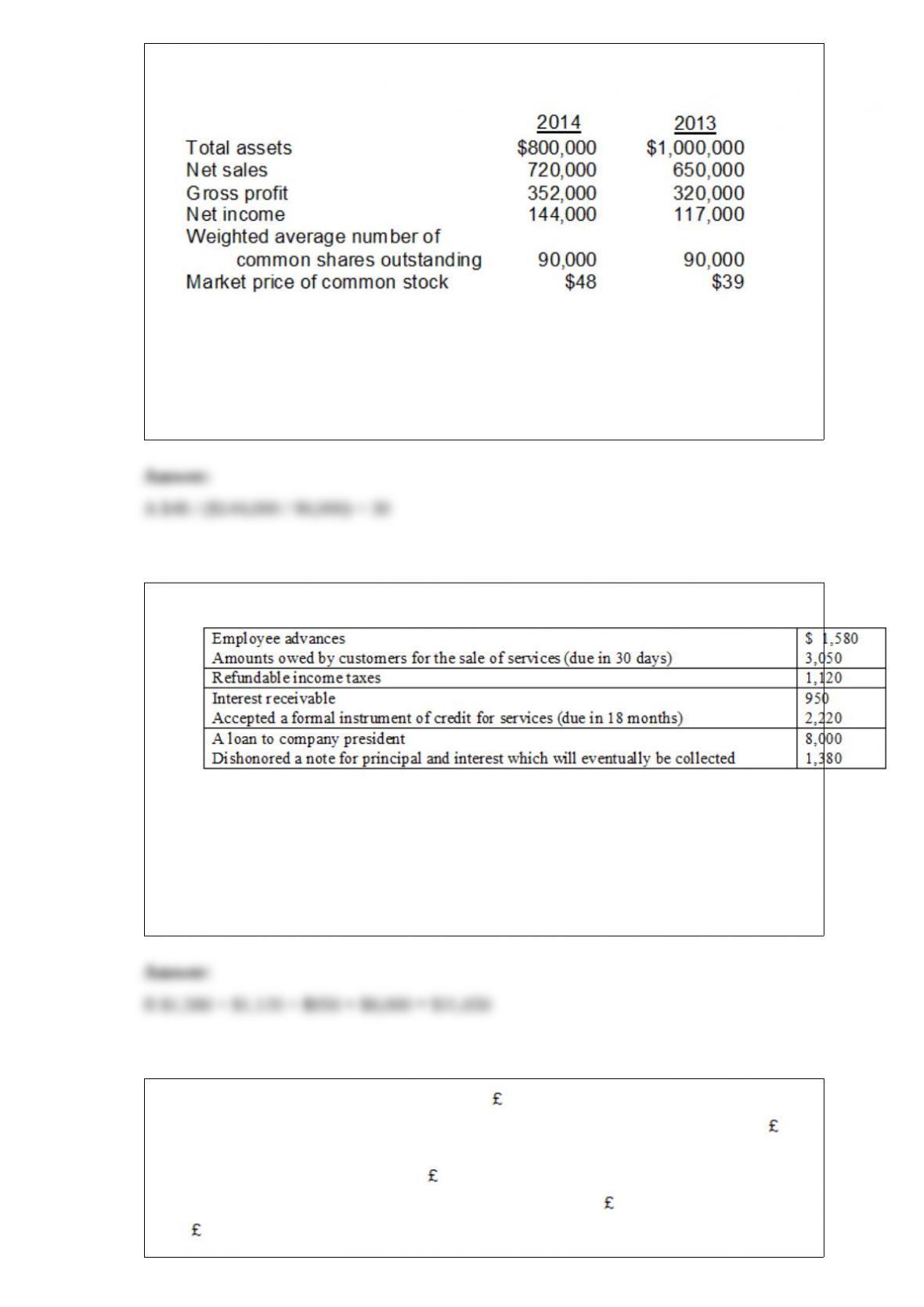

The following amounts were taken from the financial statements of Ando Company:

The price-earnings ratio for 2014 is

a.30 times.

b.25 times.

c.48 times.

d.3 times.

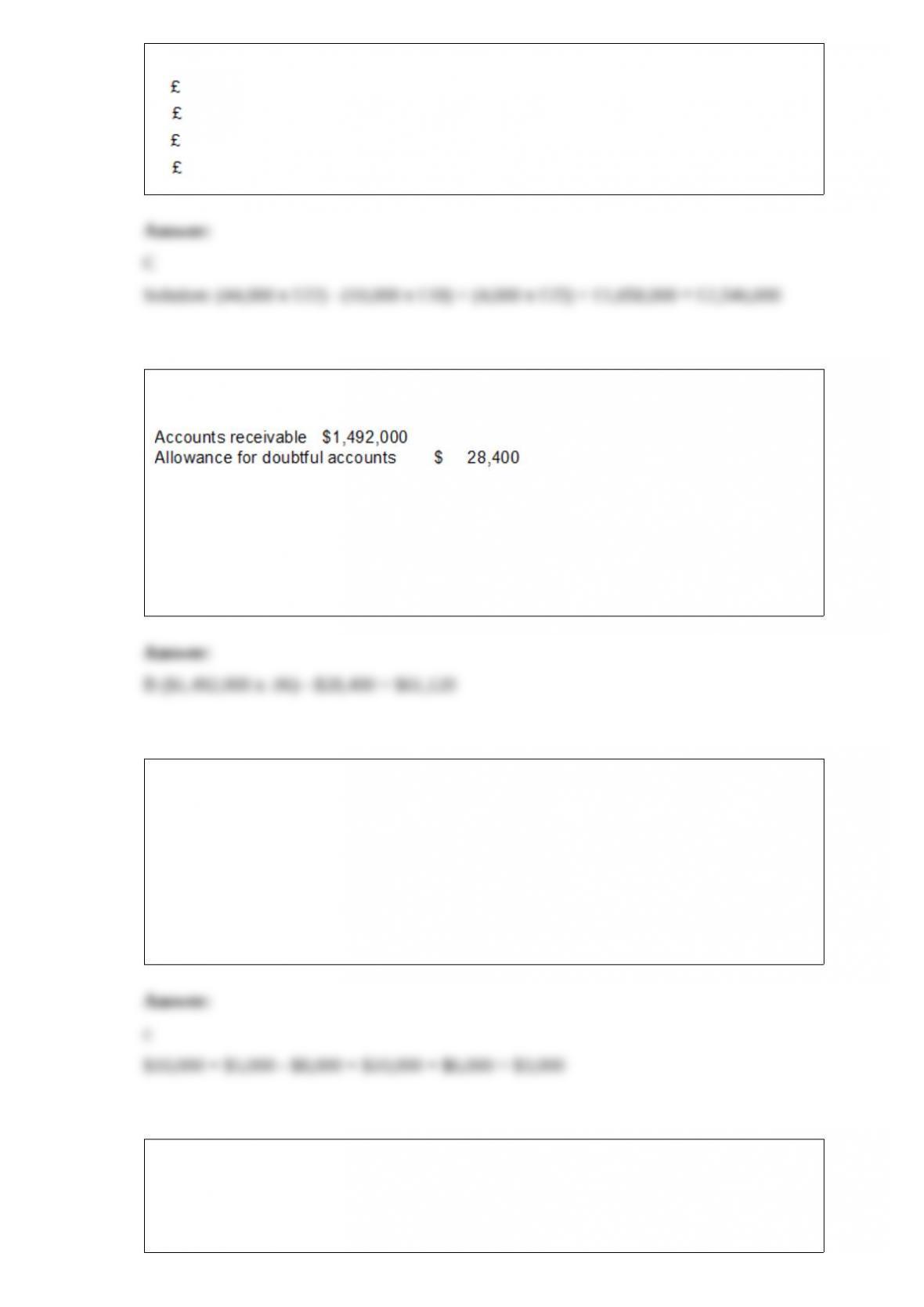

Dorman Company had the following items to report on its balance sheet:

Based on this information, what amount should appear in the “Other Receivables”

category?

a.$18,300

b.$11,650

c.$13,030

d.$15,250

Oxford Inc. was authorized to issue 100,000 10 par value ordinary shares. As of

December 31, 2014, the company had issued 44,000 shares at an average price of 22

per share. During 2014, the company felt that the shares were undervalued so it

purchased 10,000 treasury shares at 18 per share. When the share price rebounded

later in the year, the company sold 4,000 of the treasury for 25. Retained earnings

was 1,658,000 at December 31, 2014.

Total equity at December 31, 2014 is

a. 2,446,000.

b. 2,518,000.

c. 2,546,000.

d. 2,762,000.

Thompson Corporation’s unadjusted trial balance includes the following balances

(assume normal balances):

Bad debts are estimated to be 6% of outstanding receivables. What amount of bad debt

expense will the company record?

a.$89,520

b.$61,120

c.$59,416

d.$91,224

Catalina Company reported a net loss of $10,000 for the year ended December 31,

2014. During the year, accounts receivable decreased $5,000, inventory increased

$8,000, accounts payable increased by $10,000, and depreciation expense of $6,000

was recorded. During 2014, operating activities

a.used net cash of $3,000.

b.used net cash of $7,000.

c.provided net cash of $3,000.

d.provided net cash of $7,000.

Hopson Company incurred $600,000 of research and development costs in its

laboratory to develop a new product. It spent $80,000 in legal fees for a patent granted

on January 2, 2014. On July 31, 2014, Hopson paid $60,000 for legal fees in a

successful defense of the patent. What is the total amount that should be debited to

Patents through July 31, 2012?

a.$600,000.

b.$140,000.

c.$740,000.

d.Some other amount.

From the information below, compute the payout ratio for Kevin’s Trailers.

a.25%.

b.20%.

c.8%.

d.2%.

Atom Company just began business and made the following four inventory purchases

in June:

A physical count of merchandise inventory on June 30 reveals that there are 200 units

on hand. Using the LIFO inventory method, the value of the ending inventory on June

30 is

a.$1,105

b.$1,100

c.$1,170

d.$1,180

Collins Company borrowed $750,000 from BankTwo on January 1, 2013 in order to

expand its mining capabilities. The five-year note required annual payments of

$195,327 and carried an annual interest rate of 9.5%. What is the amount of expense

Collins must recognize on its 2014 income statement?

a.$71,250.

b.$59,463.

c.$52,693.

d.$46,555.

(a)Explain the control principle of independent internal verification?

(b)What practices are important in applying this principle?

Which of the following ratios indicates how efficiently a company uses it assets to

generate sales?

a.Profit margin

b.Asset turnover

c.Return on assets

d.Sustainability

Which one of the following is incorrect concerning the journal?

a.It provides a chronological record of transactions.

b.It helps prevent or locate errors.

c.It contains a record of each account maintained by the company.

d.It discloses in one place the complete effect of a transaction.

Herman Company received proceeds of ₤471,250 on 10-year, 8% bonds issued on

January 1, 2012. The bonds had a face value of ₤500,000, pay interest semi-annually

on June 30 and December 31, and have a call price of 101. Herman uses the

straight-line method of amortization.

Herman Company decided to redeem the bonds on January 1, 2014. What amount of

gain or loss would Herman report on its 2014 income statement?

a.₤23,000 gain

b.₤28,000 gain

c.₤28,000 loss

d.₤23,000 loss

Which of the following is a correct statement concerning the reporting of stockholders’

equity on the balance sheet?

a.Three classifications are reported in paid-in capital: capital stock, additional paid-in

capital, and treasury stock.

b.Additional paid-in capital represents the total amounts received from the issuance of

stock since the company began.

c.The paid-in capital section includes capital stock and additional paid-in capital.

d.Common stock is presented before preferred stock.

Gilkey Corporation began the year with retained earnings of $465,000. During the year,

the company issued $630,000 of common stock, recorded expenses of $1,800,000, and

paid dividends of $120,000. If Gilkey’s ending retained earnings was $495,000, what

was the company’s revenue for the year?

a.$1,830,000

b.$1,950,000

c.$2,460,000

d.$2,580,000

Which of the following relationships is true concerning the Sales Returns and

Allowances account? a.It is a contra account that is reported on the balance sheet as a

deduction from the related sales.

b.It can flag problems of inferior merchandise, inefficiencies in filling orders, and other

mistakes.

c.It represents the cost of merchandise returned by customers.

d.It has a normal credit balance and is added to sales to determine net sales.

Cash flows from operating activities can be calculated using the indirect or direct

method. Briefly describe how the two methods differ yet arrive at the same dollar

amount for net cash provided by operating activities.

On January 1, the Biddle & Biddle, CPAs received a $7,500 cash retainer for

accounting services to be provided rateably over the next 3 months. The full amount

was credited to the liability account Service Unearned Revenue. Assuming that the

revenue is recognized rateably over the 3 month period, what adjusting journal entry

should be made at January 31?

Mark Remington, the president and CEO of Earth Systems, Inc., a waste management

firm, was recently hospitalized, suffering from exhaustion and a heart ailment.

Immediately prior to his hospitalization, Earth Systems had experienced a sharp decline

in its stock price, and trading activity became almost nonexistent. The primary reason

for this was concern expressed in the media over a new untested waste management

system implemented by the company.

Mr. Remington had been unwilling to submit the procedure to testing before

implementation, but he reluctantly agreed to limited tests after the system was

operational. No problems have been identified by the tests to date.

The other members of management called a meeting to determine what they should do.

Terry Jackson, the marketing manager, suggested that the company purchase a large

number of shares of treasury stock. In that way, investors might notice that activity had

picked up, and might decide to buy some more shares. This plan would use up most of

the company’s available cash, so that there will be no money available for a cash

dividend. Earth Systems has paid cash dividends every quarter for over ten years.

1)Is Mr. Jackson’s suggestion ethical? Explain.

2)Is it ethical to discontinue the cash dividend? Explain.

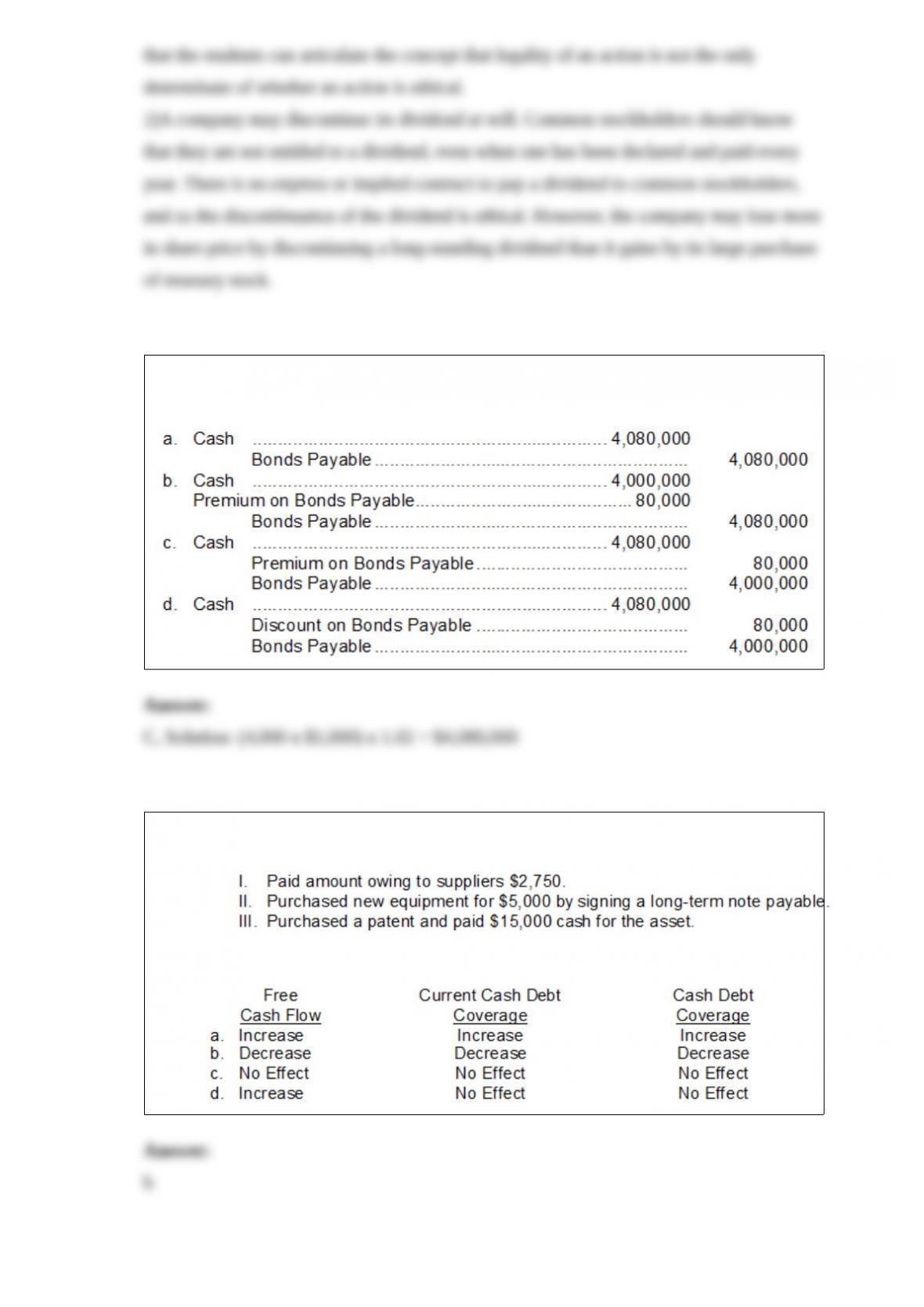

Four thousand bonds with a face value of $1,000 each, are sold at 102. The entry to

record the issuance is

Authentic Exposure Company had the following transactions that took place during the

year:

How what is the total effect of these transactions on Free Cash Flow, Current Cash Debt

Coverage, and Cash Debt Coverage respectively?