From a financial accounting perspective, the main purposes of a system of internal

control are to improve the accuracy and reliability of accounting information and to

safeguard assets.

Sellers recognize revenue for gift cards at the point in time control of the gift card is

transferred to the customer.

The transaction price should be adjusted to reflect the time value of money for interest

payable, but not for interest receivable.

On a sale-leaseback transaction, any gain on the ‘sale” portion of the transaction is

recognized immediately.

If the seller is an agent, the seller typically recognizes cost associated with the sale on

its own line in the income statement.

Under IAS No. 39, transfers of debt investments out of the FVPL category into AFS or

HTM are permitted under “rare circumstances.”

The right of return is a separate performance obligation, and a portion of the transaction

price needs to be allocated to it for revenue recognition.

Amounts held in cash equivalent investments must be reported separately from amounts

held as cash in the statement of cash flows.

The three factors in cost allocation of a depreciable asset are service life, allocation

base, and allocation method.

The monetary unit assumption requires that items in financial statements be measured

in a particular monetary unit.

Large, highly rated firms sometimes sell commercial paper:

a. To borrow funds at a lower rate than through a bank.

b. To earn a profit on the paper.

c. To avoid paperwork.

d. Because the interest rate is locked in by the Federal Reserve Board.

Which of the following is not a characteristic that defines a reportable operating

segment according to U.S. GAAP?

a. Operating results are regularly reviewed by the enterprise’s chief operating officer.

b. Discrete financial information is available.

c. Engages in business activities from which it may recognize revenues and incur

expenses.

d. Represents more than 20% of total company revenues, assets, or net income.

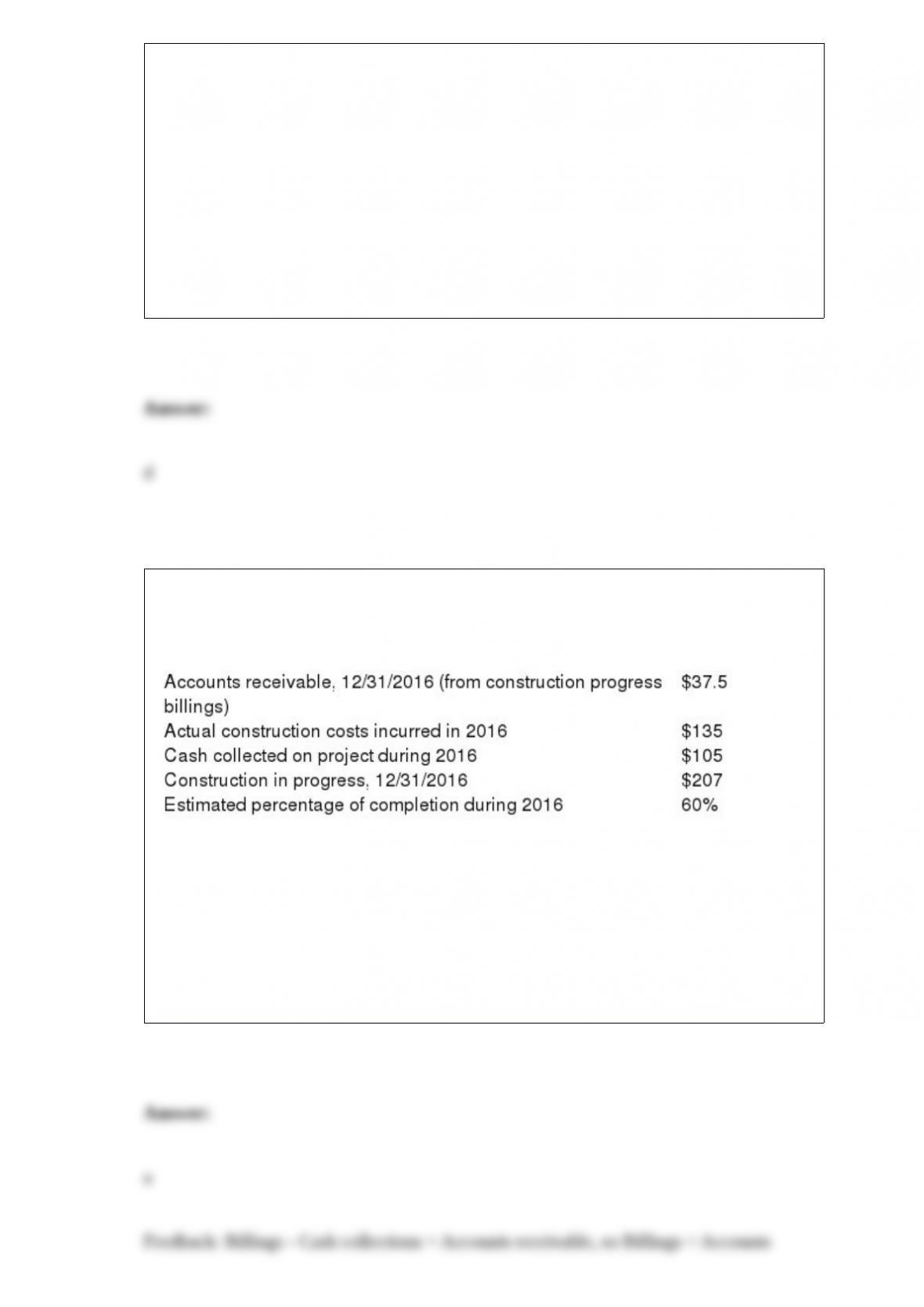

In 2016, Cupid Construction Co. (CCC) began work on a two-year fixed price contract

project. CCC recognizes revenue over time according to percentage of completion for

this contract, and provides the following information (dollars in millions):

What were the construction billings by CCC during 2016?

a. $142.5 million.

b. $67.5 million.

c. $37.5 million.

d. Cannot be determined from the given information.

Sanjeev enters into a contract offering variable consideration. The contract pays him

$1,000/month for six months of continuous consulting services. In addition, there is a

60% chance the contract will pay an additional $2,000 and a 40% chance the contract

will pay an additional $3,000, depending on the outcome of the consulting contract.

Sanjeev concludes that this contract qualifies for revenue recognition over time.

Assume that Sanjeev estimates variable consideration as the most likely amount. After

Sanjeev has recognized revenue for two months of the contract, he changes his

assessment of the chance the contract will pay him $3,000 to 70%. What adjustment to

revenue should Sanjeev recognize to account for that change in estimate?

a. Debit of $1,000

b. Debit of $334

c. Credit of $1,000

d. Credit of $334

One of the four criteria for a capital lease specifies that the lease term be equal to or

greater than:

a. 75% of the expected economic life of the leased property.

b. 90% of the expected economic life of the leased property.

c. 80% of the expected economic life of the leased property.

d. 50% of the expected economic life of the leased property.

Pierce Company issued 11% bonds, dated January 1, with a face amount of $800,000

on January 1, 2016. The bonds sold for $739,816 and mature in 2035 (20 years). For

bonds of similar risk and maturity the market yield was 12%. Interest is paid

semiannually on June 30 and December 31. Pierce determines interest at the effective

rate and elected the option to report these bonds at their fair value. On December 31,

2016, the fair value of the bonds was $730,000. The entire change in fair value was due

to a change in the general (risk-free) rate of interest. Pierce’s net income for the year

will include:

a. An unrealized gain from change in the fair value of debt of $10,617.

b. An unrealized loss from change in the fair value of debt of $10,617.

c. A gain from change in the fair value of debt of $10,204.

d. A loss from change in the fair value of debt of $10,204.

On January 1, 2016, Oliver Foods issued stock options for 40,000 shares to a division

manager. The options have an estimated fair value of $5 each. To provide additional

incentive for managerial achievement, the options are not exercisable unless Oliver

Foods’ stock price increases by 5% in four years. Oliver Foods initially estimates that it

is not probable the goal will be achieved. How much compensation will be recorded in

each of the next four years?

a. $10,000.

b. $45,000.

c. $50,000.

d. No effect.

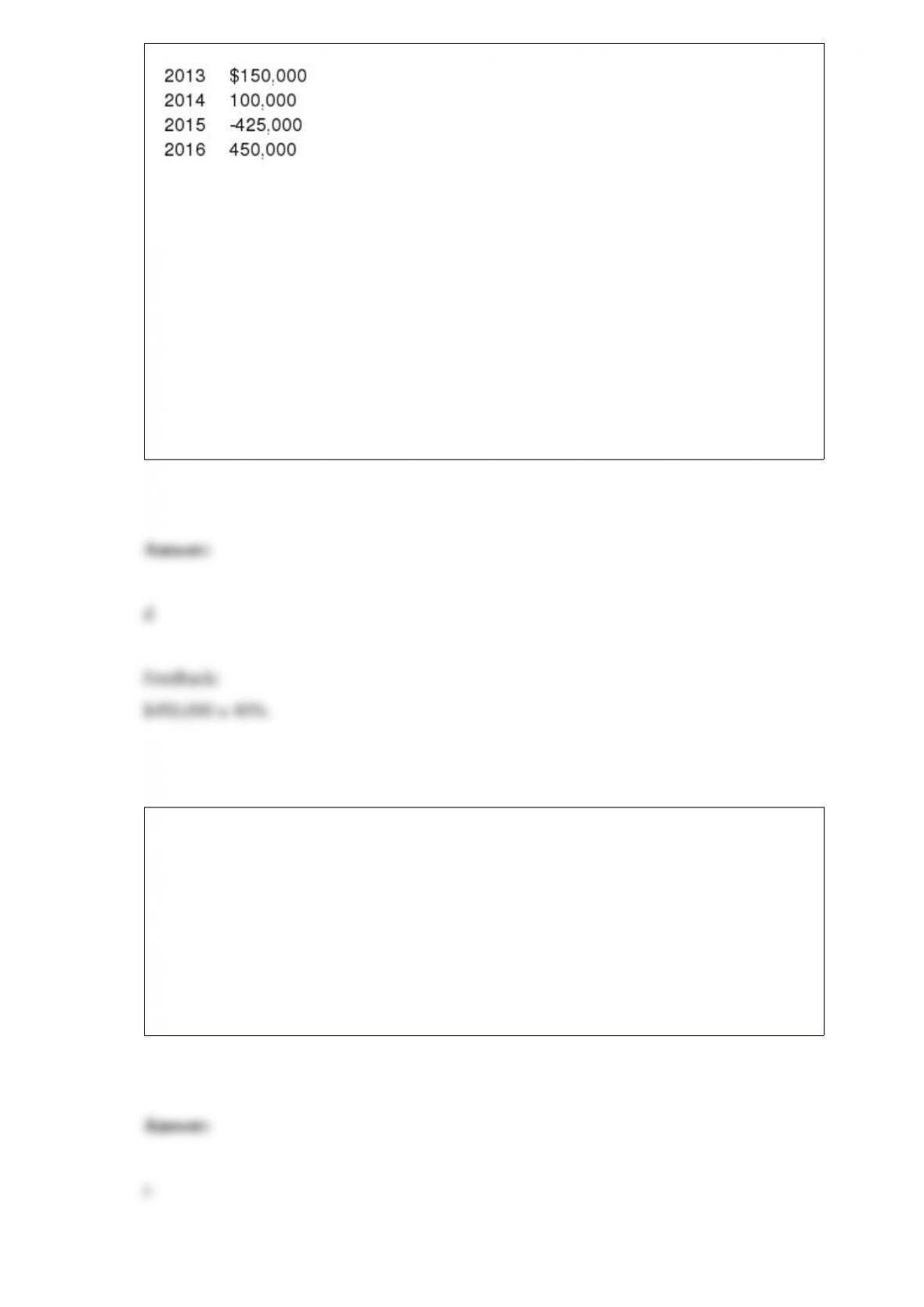

In its first four years of operations Peridot Jewelers reported the following operating

income (loss) amounts:

There were no other deferred income taxes in any year. In 2015, Peridot elected to carry

back its operating loss. The enacted income tax rate was 40%. In its 2016 income

statement, what amount should Peridot report as income tax expense?

a. $ 80,000.

b. $110,000.

c. $170,000.

d. $180,000.

Trading securities, by definition, are properly classified in the balance sheet as:

a. Shareholders’ equity.

b. Intangibles.

c. Current assets.

d. Other assets.

The following is the 2016 report of the independent registered public accounting firm

for The Great Food Company, Inc., a large supermarket chain:

In our opinion, the accompanying consolidated balance sheets and the related

consolidated statements of operations, stockholders’ deficit and comprehensive loss, and

cash flows present fairly, in all material respects, the financial position of The Great

Food Company, Inc. and its subsidiaries (debtor-in-possession) at December 31, 2016,

and December 31, 2015, and the results of their operations and their cash flows for each

of the three years in the period ended December 31, 2016, in conformity with

accounting principles generally accepted in the United States of America. In addition,

in our opinion, the financial statement schedule listed in Item 15(a)(2) presents fairly, in

all material respects, the information set forth therein when read in conjunction with the

related consolidated financial statements. Also in our opinion, the Company

maintained, in all material respects, effective internal control over financial reporting as

of December 31, 2016, based on criteria established in Internal Control – Integrated

Framework issued by the Committee of Sponsoring Organizations of the Treadway

Commission (COSO). The Company’s management is responsible for these financial

statements and financial statement schedule, for maintaining effective internal control

over financial reporting and for its assessment of the effectiveness of internal control

over financial reporting, included in Management’s Annual Report on Internal Control

over Financial Reporting appearing under Item 9A. Our responsibility is to express

opinions on these financial statements, on the financial statement schedule, and on the

Company’s internal control over financial reporting based on our integrated audits. We

conducted our audits in accordance with the standards of the Public Company

Accounting Oversight Board (United States). Those standards require that we plan and

perform the audits to obtain reasonable assurance about whether the financial

statements are free of material misstatement and whether effective internal control over

financial reporting was maintained in all material respects. Our audits of the financial

statements included examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements, assessing the accounting principles used and

significant estimates made by management, and evaluating the overall financial

statement presentation. Our audit of internal control over financial reporting included

obtaining an understanding of internal control over financial reporting, assessing the

risk that a material weakness exists, and testing and evaluating the design and operating

effectiveness of internal control based on the assessed risk. Our audits also included

performing such other procedures as we considered necessary in the circumstances. We

believe that our audits provide a reasonable basis for our opinions. The accompanying

financial statements have been prepared assuming that the Company will continue as a

going concern. However, the Company is currently operating pursuant to a Chapter 11

bankruptcy filing which, together with the uncertain outcomes of the matters discussed

in Note 1 to the consolidated financial statements, raise substantial doubt about the

Company’s ability to continue as a going concern. Management’s plans in regard to

these matters are also described in Note 1. The consolidated financial statements do not

include any adjustments that might result from the outcome of these uncertainties. As

discussed in Note 1 to the consolidated financial statements, the Company changed the

manner in which it accounts for share lending arrangements during fiscal 2015. A

company’s internal control over financial reporting is a process designed to provide

reasonable assurance regarding the reliability of financial reporting and the preparation

of financial statements for external purposes in accordance with generally accepted

accounting principles. A company’s internal control over financial reporting includes

those policies and procedures that (i) pertain to the maintenance of records that, in

reasonable detail, accurately and fairly reflect the transactions and dispositions of the

assets of the company; (ii) provide reasonable assurance that transactions are recorded

as necessary to permit preparation of financial statements in accordance with generally

accepted accounting principles, and that receipts and expenditures of the company are

being made only in accordance with authorizations of management and directors of the

company; and (iii) provide reasonable assurance regarding prevention or timely

detection of unauthorized acquisition, use, or

disposition of the company’s assets that could have a material effect on the financial

statements.

Required. Interpret the main points indicated in this report by Great Food’s auditors.

On December 31, 2016, Wellstone Company reported net income of $70,000 and sales

of $210,000. The company also reported beginning and ending accounts receivable at

$20,000 and $25,000, respectively. Wellstone will report cash collected from customers

in its 2016 statement of cash flows (direct method) in the amount of:

a. $215,000.

b. $285,000.

c. $135,000.

d. $205,000.

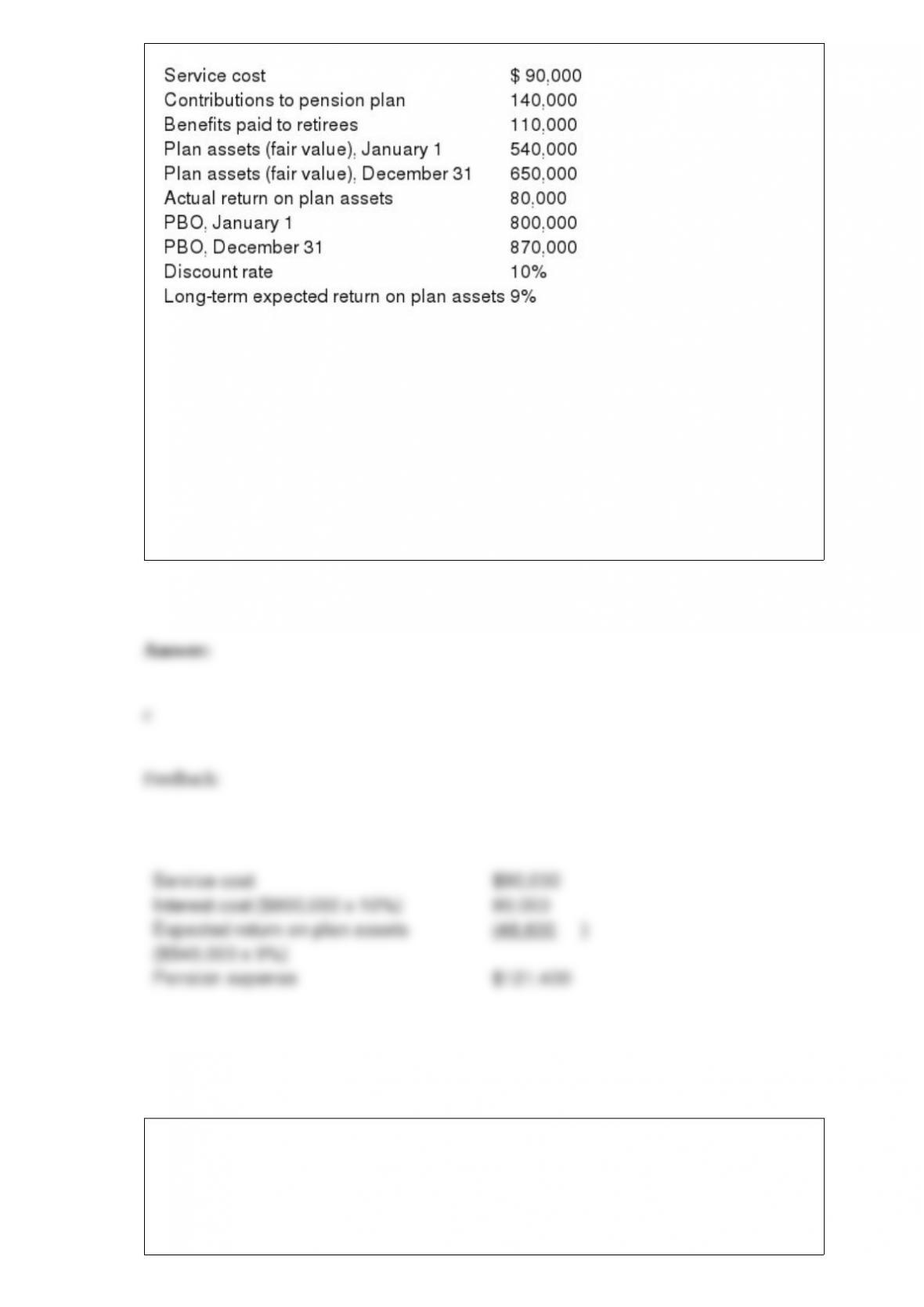

The following information is related to the defined benefit pension plan of Simpson

Company for the year:

Assuming no other relevant data exist, what is the pension expense for the year?

a. $ 90,000.

b. $230,600.

c. $121,400.

d. $154,000.

On January 1, 2016, Hobart Mfg. Co. purchased a drill press at a cost of $36,000. The

drill press is expected to last 10 years and has a residual value of $6,000. During its

10-year life, the equipment is expected to produce 500,000 units of product. In 2016

and 2017, 25,000 and 84,000 units, respectively, were produced. Required:

Compute depreciation for 2016 and 2017 and the book value of the drill press at

December 31, 2016 and 2017, assuming the sum-of-the-years’-digits method is used.

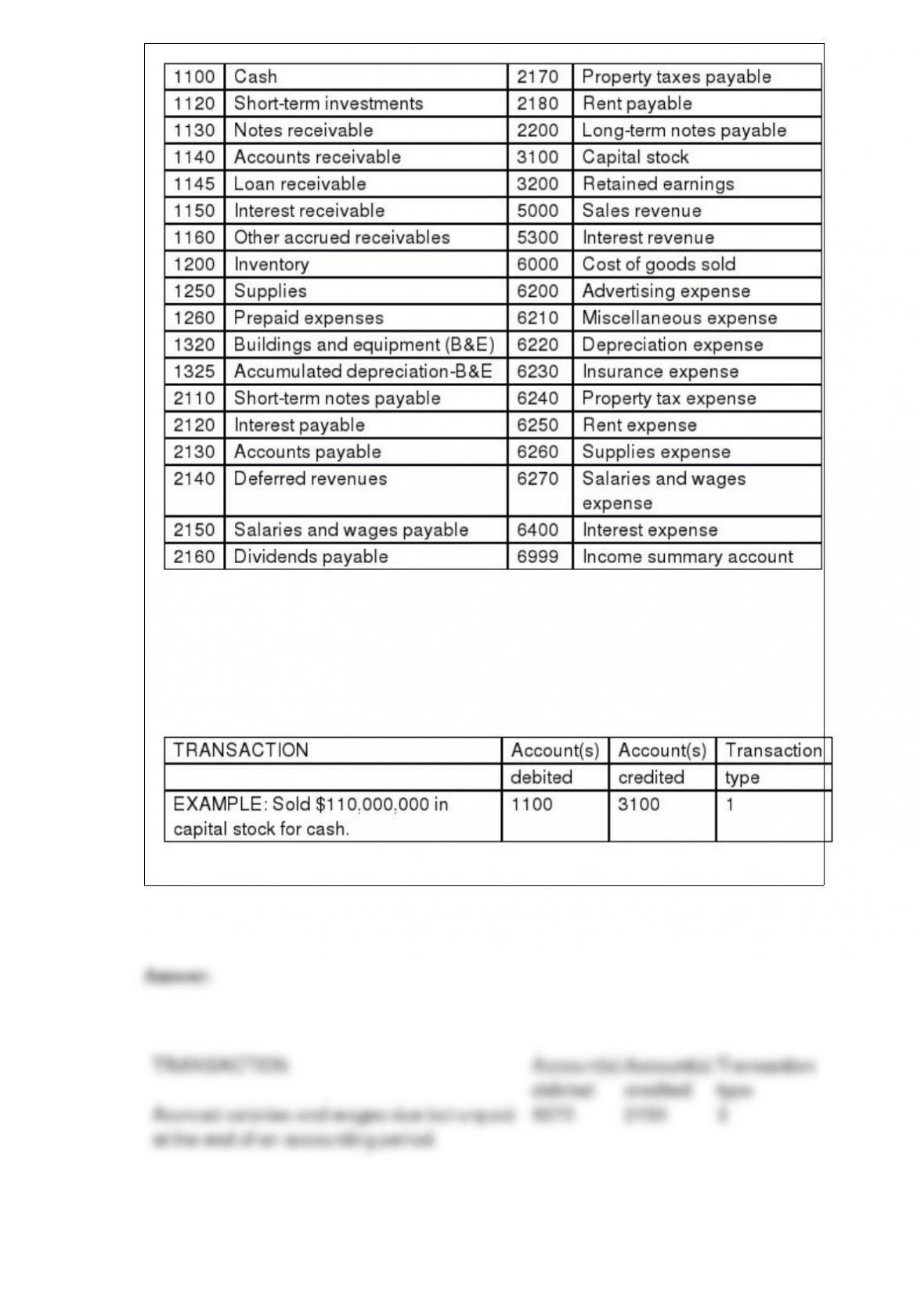

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Salaries and wages have been earned but are unpaid at the end of an accounting period.

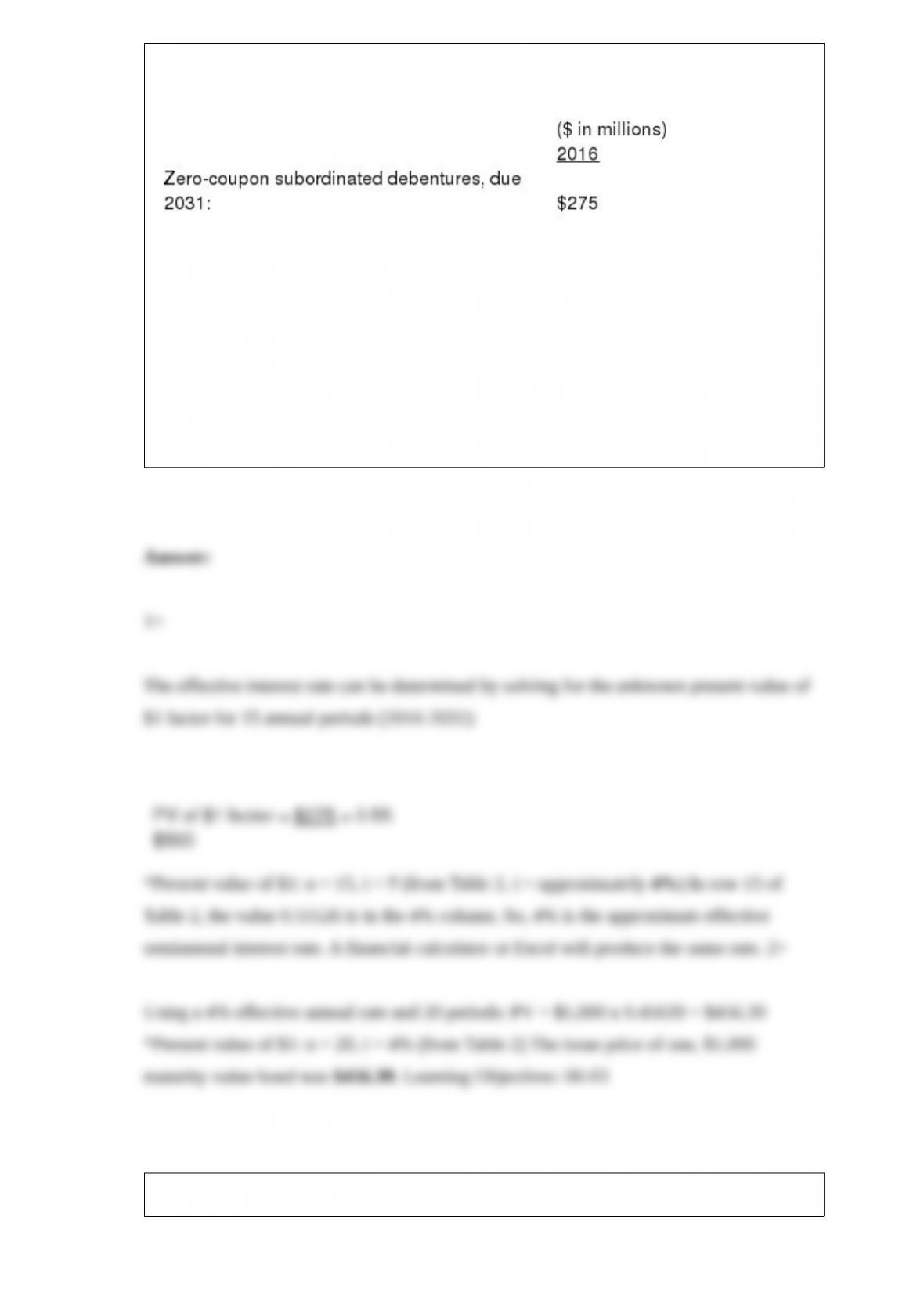

White & Decker Corporation’s 2016 financial statements included the following

information in the long-term debt disclosure note:

The disclosure note stated the debenture bonds were issued late in 2011 and have a

maturity value of $500 million. The maturity value indicates the amount that White &

Decker will pay bondholders in 2031. Each individual bond has a maturity value (face

amount) of $1,000. Zero-coupon bonds pay no cash interest during the term to maturity.

The company is ‘œaccreting’ (gradually increasing) the issue price to maturity value

using the bonds’ effective interest rate computed on an annual basis. Required:

1> Determine the effective interest rate on the bonds.

2> Determine the issue price in late 2011 of a single, $1,000 maturity-value bond.

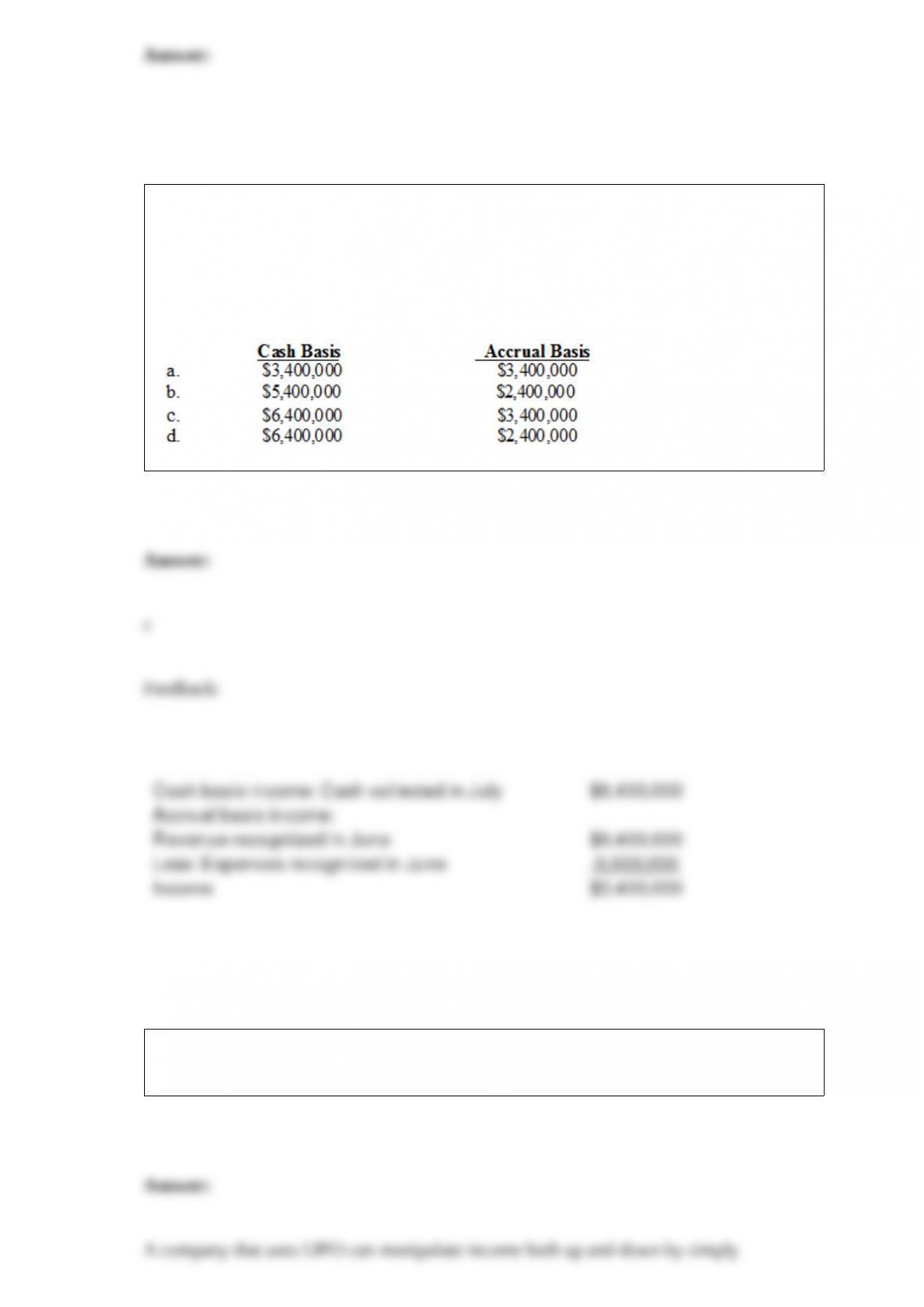

On June 1, Royal Corp. began operating a service company with an initial cash

investment by shareholders of $2,000,000. The company provided $6,400,000 of

services in June and received full payment in July. Royal also incurred expenses of

$3,000,000 in June that were paid in August. During June, Royal paid its shareholders

cash dividends of $1,000,000. What was the company’s income before income taxes for

the two months ended July 31 under the following methods of accounting?

Briefly explain how companies that use LIFO can both increase and decrease reported

earnings by “managing” ending inventories.

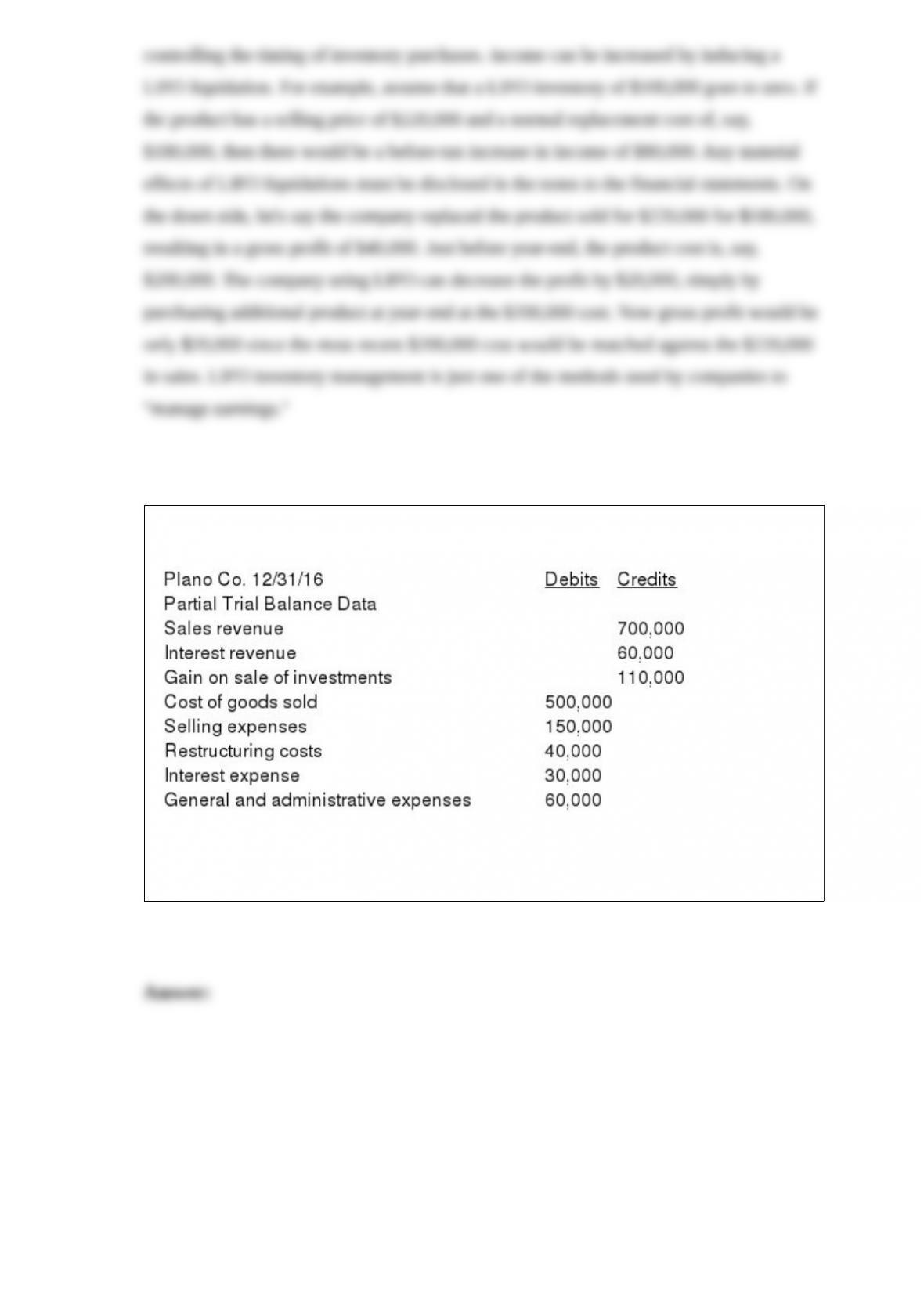

Plano had 50,000 shares of stock outstanding throughout the year. Income tax expense

has not yet been accrued. The effective tax rate is 30%.

Required: Prepare a single-step income statement with earnings per share disclosure.

Provide an example of a liability that would not require the payment of cash.

Summerhill Construction builds luxury houses in remote areas. On June 1, 2016, the

company signed a contract to build a house in an undeveloped section of a

mountainside, and received $2 million in advance for the job. To complete the project,

the company must construct a pathway leading to the building lot, clear a large hillside,

and construct a wooden house. Normally, the company would charge $400,000,

$1,400,000, and $500,000, respectively, for each of these tasks if done separately.

Required: Given the information above, how many performance obligations are

included in this contract?

Over time, accounting standards have developed to reflect changes in the business

world as well as changes in our ability to account for such changes. Using the example

of marking assets and liabilities to their fair value, explain why you would expect

accounting standards to change.