1) The internal control environment is enhanced by the hiring and retention of

competent, honest employees.

2) All merchandising businesses are organized as corporations.

3) A voucher system is an example of an internal control procedure over cash payments.

4) Opportunity cost is the amount of increase or decrease in revenue that would result

from the best available alternative to the proposed use of cash or its equivalent.

5) The manager of a profit center does not make decisions concerning the fixed assets

invested in the center.

6) Information and communication are essential elements of an organization’s internal

control.

7) The cash budget presents the expected inflow and outflow of cash for a specified

period of time.

8) Credit memorandum is issued by the seller to customers for return of damaged or

defective merchandise.

9) The process by which management allocates available investment funds among

competing capital investment proposals is termed capital rationing.

10) When someone purchases merchandise and incurs the cost of transportation, these

costs of purchasing inventory are added to the cost of the inventory.

11) If paid-in capital in excess of par–preferred stock is $80,000, preferred stock is

$500,000, paid-in capital in excess of par–common stock is $50,000, common stock is

$1,000,000, and retained earnings is $230,000, the total stockholders’ equity is

$1,860,000.

12) The excess of cash flowing in from revenues over the cash flowing out for expenses

is termed net discounted cash flow.

13) If a company has current assets totaling $56,000 and current liabilities totaling

$40,500, then the companys working capital totals $15,500.

14) Operating expenses are subtracted from fees earned for a service business and from

gross profit for a merchandising business.

15) When evaluating a proposal by use of the net present value method, if there is an

excess of the present value of future cash inflows over the amount to be invested, the

rate of return on the proposal exceeds the rate used in the analysis.

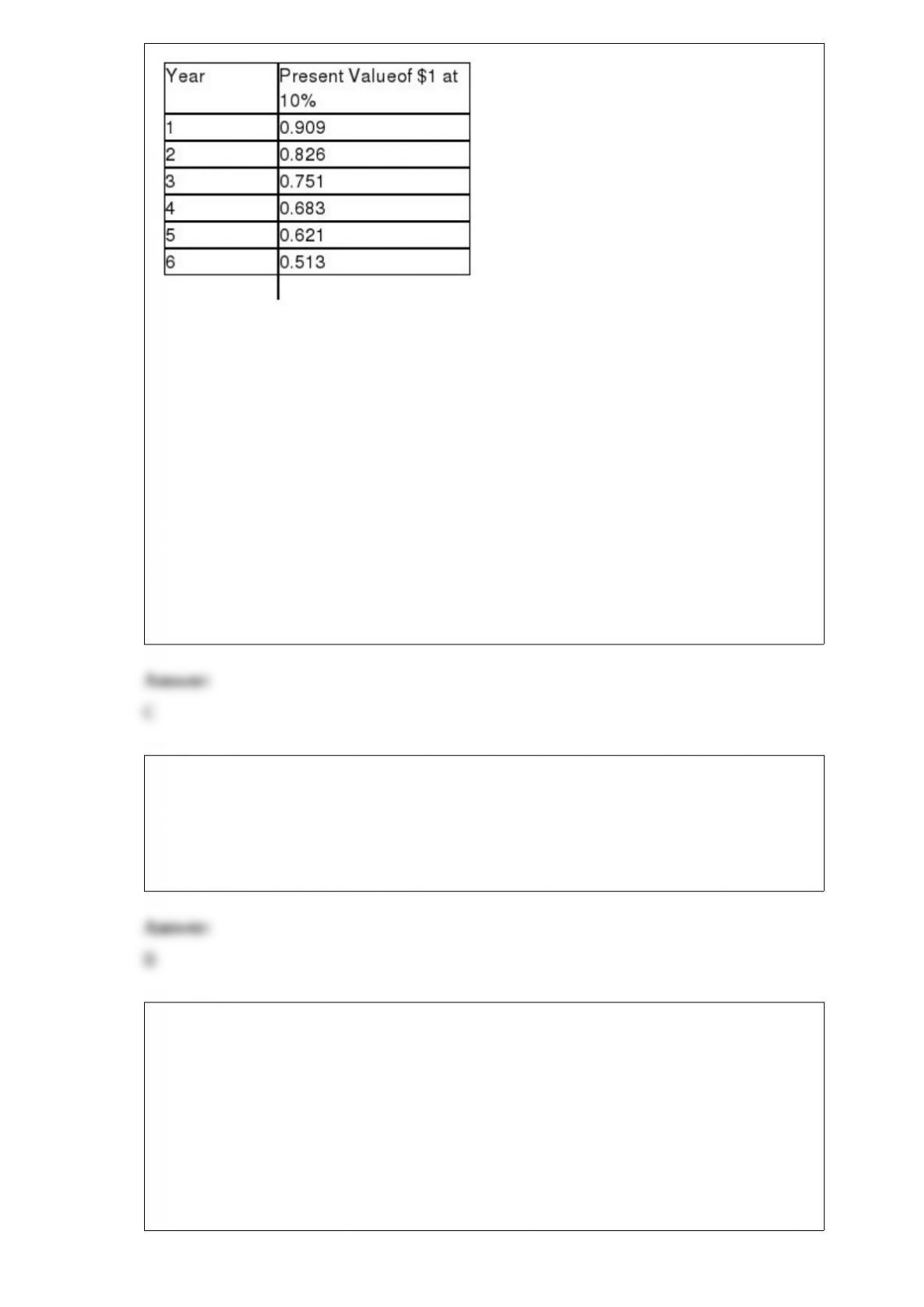

16) The management of Hence Corporation is considering the purchase of a new

machine costing $200,000. The company’s desired rate of return is 10%. The present

value factors for $1 at compound interest of 10% for 1 through 5 years are 0.909, 0.826,

0.751, 0.683, and 0.621, respectively. In addition to the foregoing information, use the

following data in determining the acceptability in this situation:

The present value index for this investment is:

A.0.88

B.1.45

C.1.14

D.0.70

17) Financing activities involve obtaining _____ to operate a business.

A.products

B.customers

C.business incentives

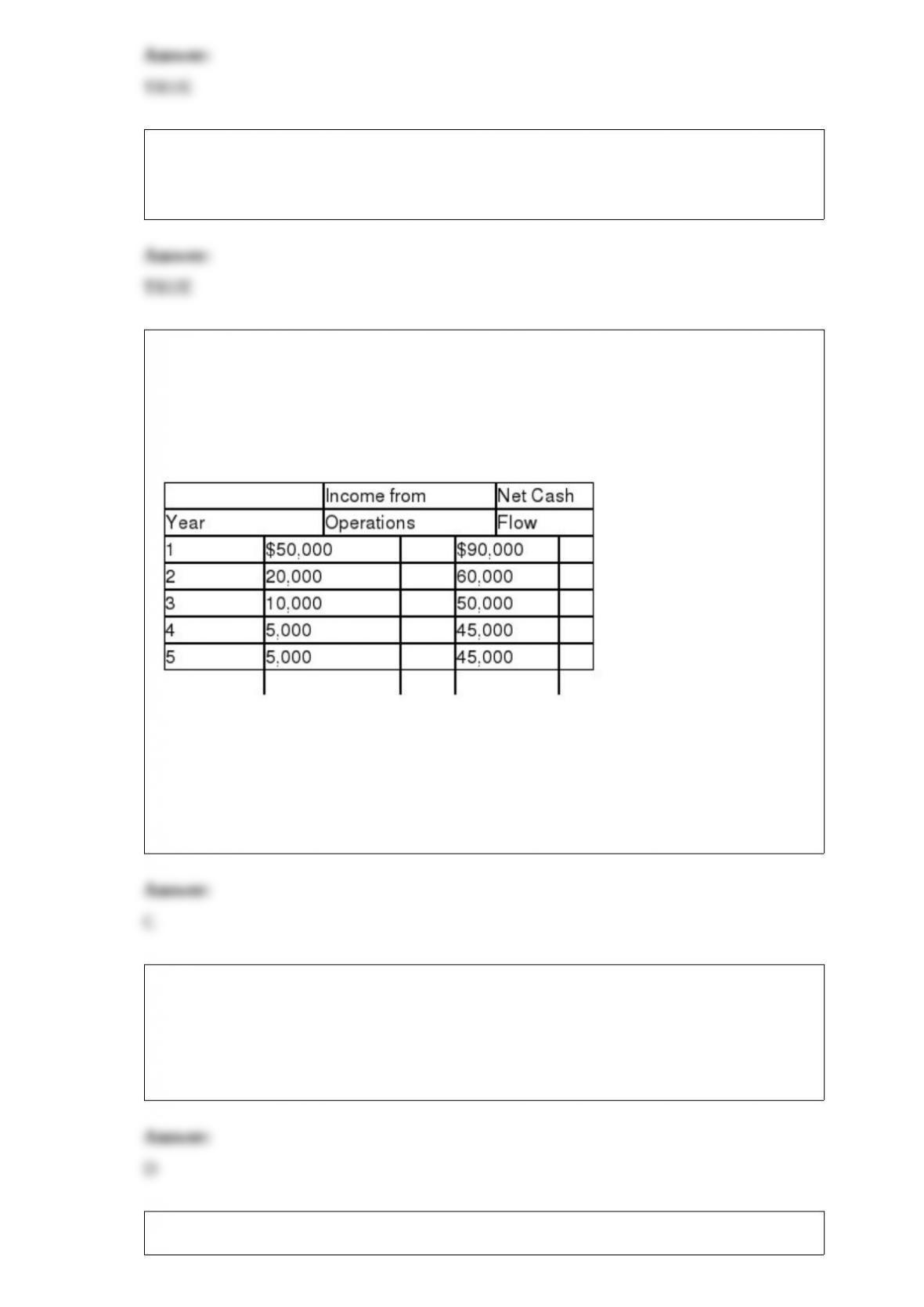

D.funds

18) A note receivable due in 18 months is listed on the balance sheet under the caption:

A.long-term liabilities

B.fixed assets

C.current assets

D.investments

19) Thomson Company reported the following on its income statement:

An analysis of the income statement revealed that interest expense was $40,000.

Thomson Company’s number of times interest charges are earned was:

A.8 times

B.7.5 times

C.9.5 times

D.11.5 times

20) Merchandise subject to terms 1/10, n/30, FOB shipping point, is sold on account to

a customer for $20,000. The seller issued a credit memorandum for $5,000 prior to

payment. What is the amount of the cash discount allowable?

A.$160

B.$150

C.$140

D.$100

21) One issue to consider when investing in assets in foreign countries is:

A.that local currency may weaken to the dollar causing adverse effects on the

investments return

B.that the dollar may weaken to the local currency causing adverse effects on the

investments return

C.that local currency may be difficult to exchange into dollars causing problems in

receiving a return on the investment

D.that dollars may be difficult to exchange into local currency causing problems in

receiving any return on investment

22) The profit margin is the ratio of:

A.income from operations to sales

B.income from operations to invested assets

C.assets to liabilities

D.sales to invested assets

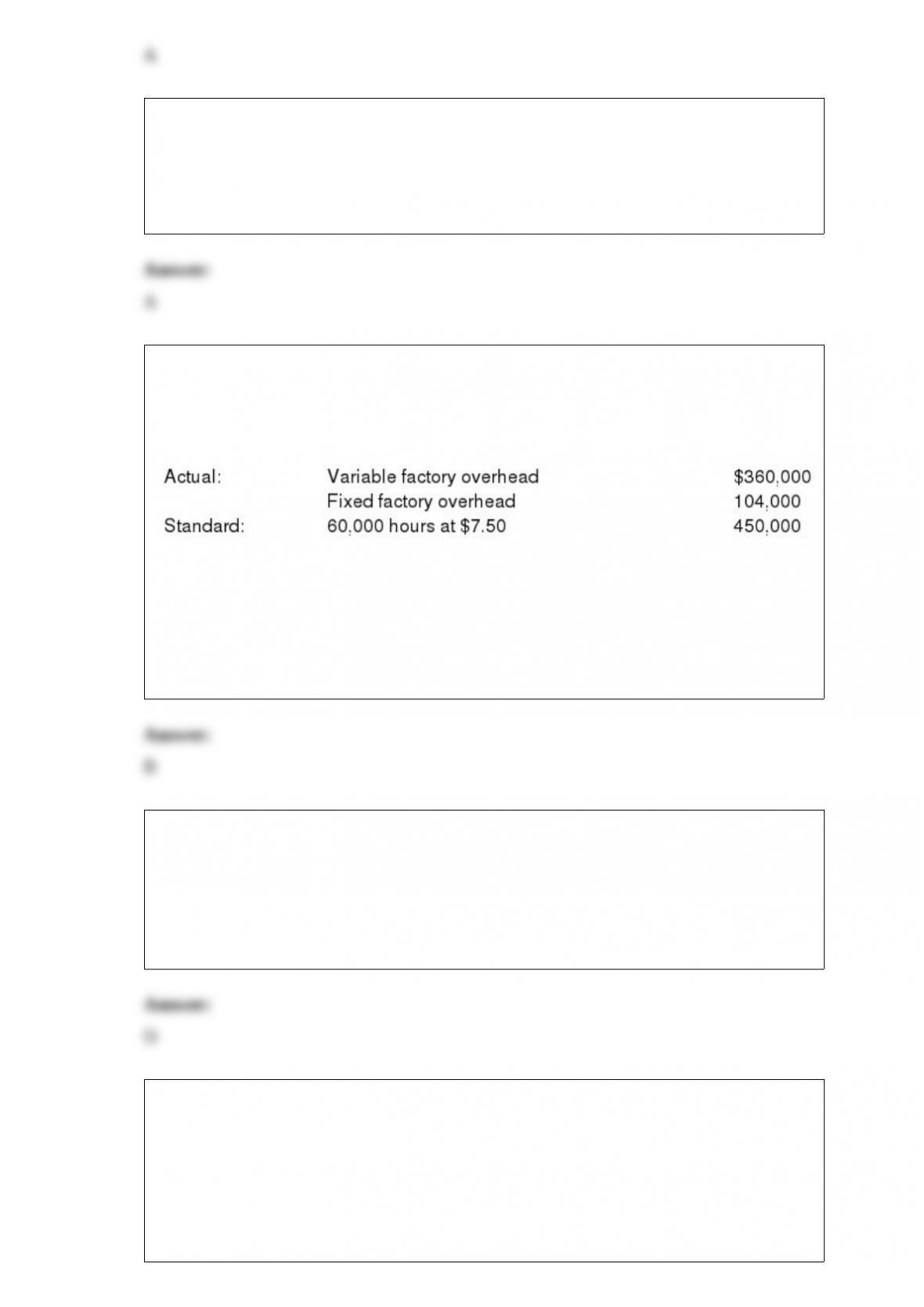

23) The standard factory overhead rate is $7.50 per machine hour ($6.20 for variable

factory overhead and $1.30 for fixed factory overhead) based on 100% capacity of

80,000 machine hours. The standard cost and the actual cost of factory overhead for the

production of 15,000 units during August were as follows:

What is the amount of the variable factory overhead controllable variance?

A.$12,000 unfavorable

B.$12,000 favorable

C.$14,000 unfavorable

D.$26,000 unfavorable

24) Which of the following elements of internal control focuses on locating weaknesses

and improving control effectiveness?

A.Control environment

B.Risk assessment

C.Control procedures

D.Monitoring

25) Blancher Corporation had $495,000 invested in assets, sales of $660,000, income

from operations amounting to $99,000, and a desired minimum rate of return of 15%.

The rate of return on investment for Blancher is:

A.16%

B.20%

C.18%

D.15%

26) Johnson, Inc. paid rent expense of $3,500 for the month of October. How are the

accounts affected due to this transaction?

A.Increase in cash $3,500 and increase in retained earnings $3,500

B.Increase in cash $3,500 and decrease in retained earnings $3,500

C.Decrease in cash $3,500 and decrease in retained earnings $3,500

D.Decrease in cash $3,500 and increase in retained earnings $3,500

27) Which of the following activity bases would be the most appropriate for gasoline

costs of a delivery service such as UPS?

A.Number of trucks employed

B.Number of miles driven

C.Number of trucks in service

D.Number of packages delivered

28) Using a perpetual inventory system, the return of merchandise purchased on

account includes a(n):

A.increase in Sales

B.increase in Merchandise Inventory

C.decrease in Merchandise Inventory

D.decrease in Sales

29) Stockholders Equity will be reduced by all of the following accounts except:

A.revenues

B.expenses

C.dividends

D.all of the above reduce Stockholders Equity

30) The process of a company selling its accounts receivable to another company is

referred as:

A.discounting

B.adjusting

C.assignment

D.factoring

31) Accompanying the bank statement was a credit memorandum for a short-term note

collected by the bank for the customer. What adjustment is required in the depositor’s

accounts?

A.Increase Notes Receivable; decrease Cash

B.Increase Cash; increase Miscellaneous Income

C.Increase Cash; decrease Notes Receivable

D.Increase Accounts Receivable; decrease Cash

32) On June 5, Glover Co. issued a $60,000, 6%, 120-day note payable to Jones Co.

How much will Glover Co. have to pay at maturity? (Assume 360 days in a year)

A.$63,600

B.$58,800

C.$60,000

D.$61,200

33) Decisions to install new equipment, replace old equipment, and purchase or

construct a new building are examples of:

A.sales mix analysis

B.variable cost analysis

C.cost-volume-profit analysis

D.capital investment analysis

34) A business is considering a cash outlay of $200,000 for the purchase of land, which

it could lease for $35,000 per year. If alternative investments are available that yield an

18% return, the opportunity cost of the purchase of the land is:

A.$35,000

B.$36,000

C.$1,000

D.$37,000

35) At the end of the fiscal year, if the balance in Factory Overhead is small, it would

normally be:

A.transferred to Work-in-Process

B.transferred to Cost of Goods Sold

C.transferred to Finished Goods

D.allocated between Work-in-Process and Finished Goods

36) Which one of the following is not a measure that management can use in evaluating

and controlling investment center performance?

A.Rate of return on investment

B.Negotiated price

C.Residual income

D.Income from operations

37) Basic analytical method in which all items are expressed only in relative terms

(percentages of a common base) and are often useful for comparing one company with

another or for comparing a company with industry averages are:

A.horizontal analysis

B.percentage statements

C.profitability analysis

D.common-sized statements

38) All amounts paid to get an asset in place and ready for use are referred to as:

A.deferred expenditures

B.revenue expenditures

C.residual value

D.cost of an asset

39) When purchases of merchandise are made for cash, under the perpetual inventory

system, the transaction:

A.increases Cash; decreases Merchandise Inventory

B.increases Merchandise Inventory; decreases Cash

C.increases Merchandise Inventory; decreases Cash Discounts

D.increases Merchandise Inventory; decreases Purchases

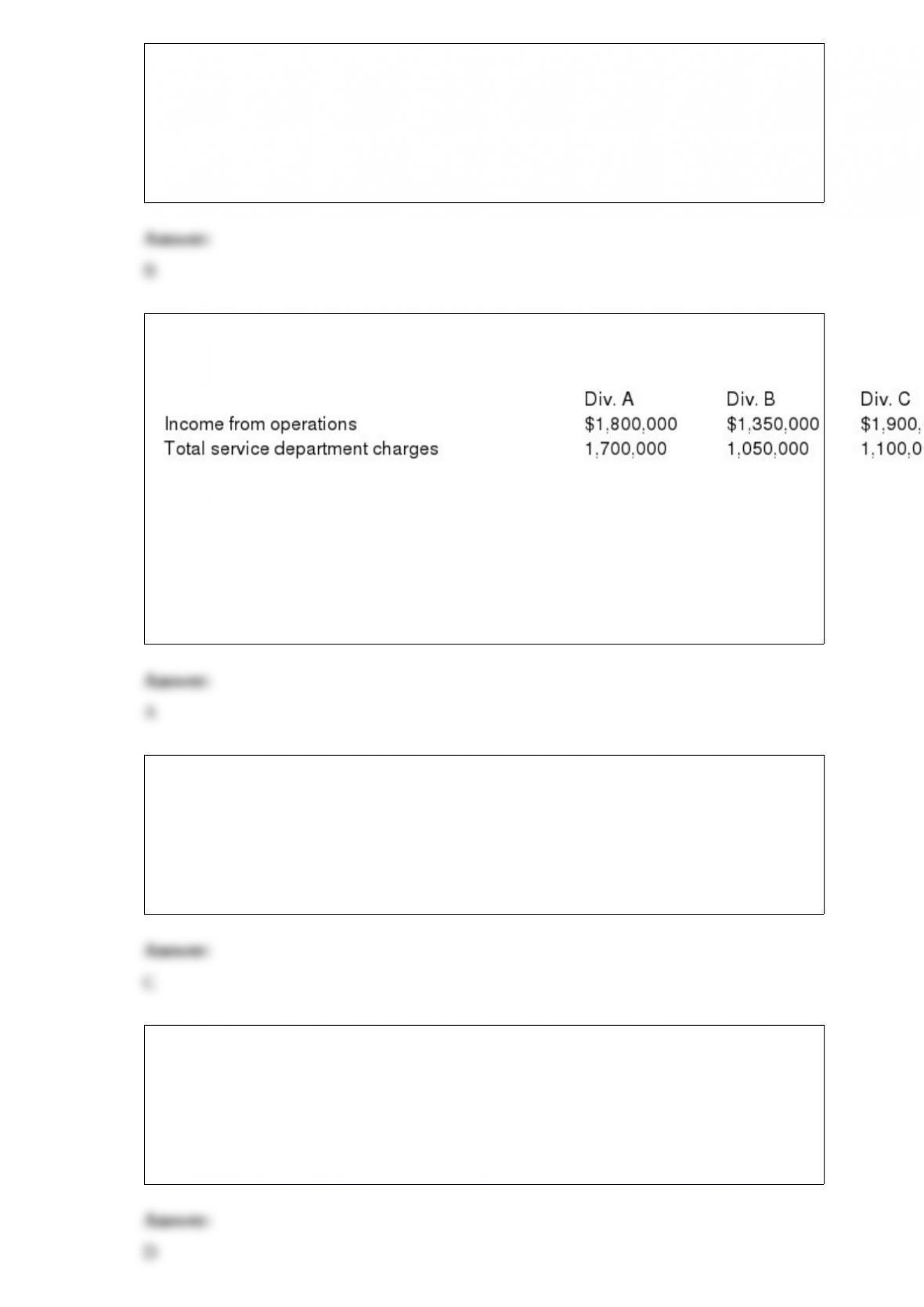

40) The following data are taken from the management accounting reports of Dancer

Co.:

If an incentive bonus is paid to the manager who achieved the highest income from

operations before service department charges, it follows that

A.division A’s manager is given the bonus

B.division B’s manager is given the bonus

C.division C’s manager is given the bonus

D.the managers of Divisions B and C divide the bonus

41) If fixed costs are $850,000 and variable costs are 60% of the sales, what is the

break-even point (in dollars)?

A.$1,416,667

B.$1,983,333

C.$2,125,000

D.$2,550,000

42) If the cost of direct materials is not a significant portion of the total product cost, it

may be classified as:

A.direct labor costs

B.selling and administrative costs

C.miscellaneous costs

D.factory overhead costs

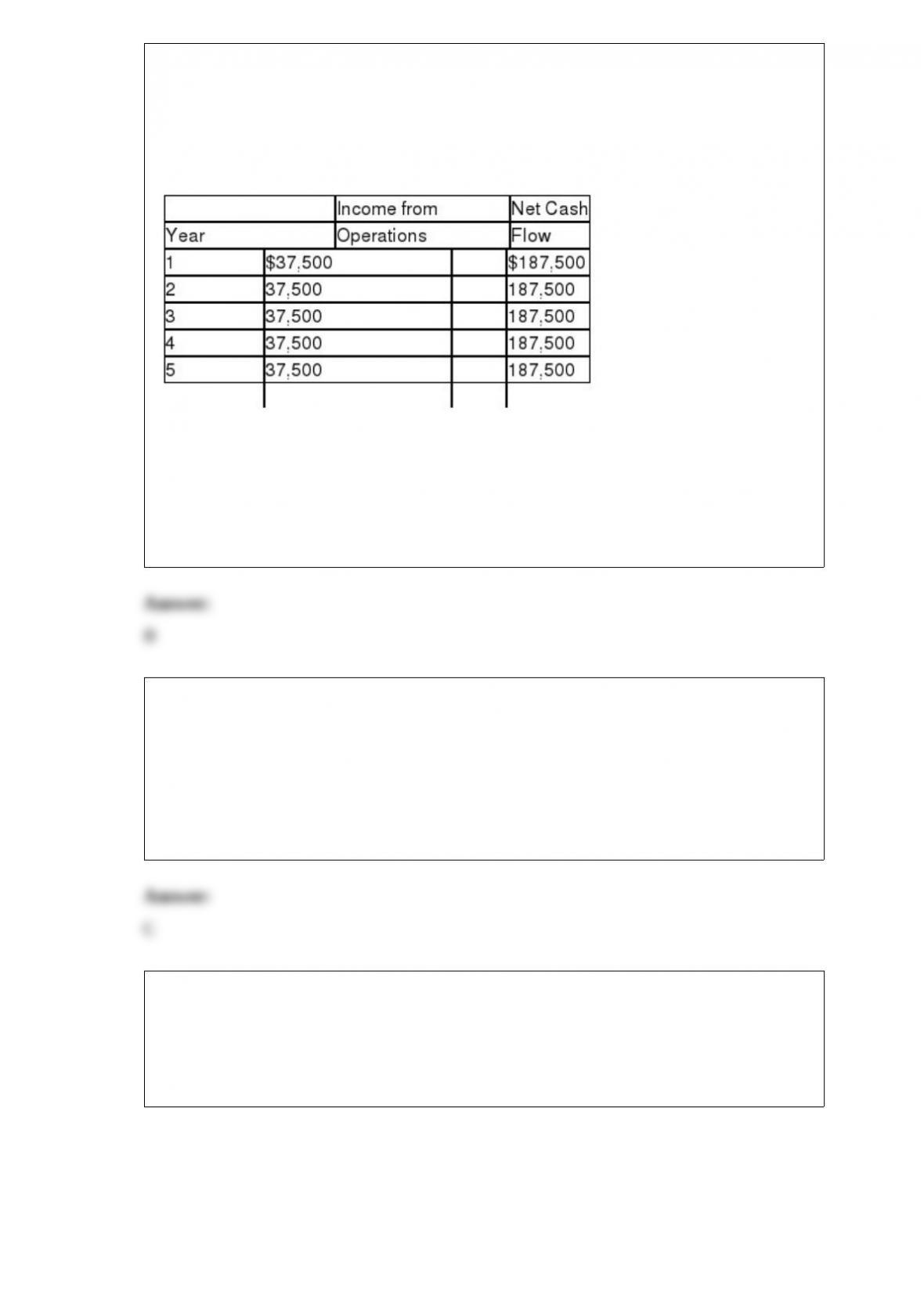

43) The management of London Corporation is considering the purchase of a new

machine costing $750,000. The company’s desired rate of return is 6%. The present

value factors for $1 at compound interest of 6% for 1 through 5 years are 0.943, 0.890,

0.840, 0.792, and 0.747, respectively. In addition to this information, use the following

data in determining the acceptability in this situation:

The average rate of return for this investment is:

A.5%

B.10%

C.25%

D.15%

44) Merchandise with an invoice price of $6,000 is purchased subject to terms of 2/10,

n/30, FOB destination. Transportation costs paid by the seller totaled $125. What is the

net cost of the merchandise?

A.$6,125

B.$6,005

C.$5,880

D.$5,755

45) Mars Corp. is choosing between two different capital investment proposals.

Machine A has a useful life of 4 years, and Machine B has a useful life of 6 years. Each

proposal requires an initial investment of $200,000, and the company desires a rate of

return of 10%. Although Machine B has a useful life of 6 years, it could be sold at the

end of 4 years for $35,000.

Machine A will generate net cash flow of $70,000 in each of the four years. Machine B

will generate $80,000 in year 1, $70,000 in year 2, $60,000 in year 3, and $40,000 per

year for the remaining 3 years of its useful life.

Which of the following statements portrays the most accurate analysis between the two

proposals?

A.Mars should invest in Machine A because the net present value of Machine A after 4

years is higher than the net present value of Machine B after 4 years

B.Mars should invest in Machine B because the net present value of Machine A after 4

years is lower and the net present value of Machine B after 6 years

C.Mars should invest in Machine B because the net present value of Machine A after 4

years is lower than the net present value of Machine B after 4 years

D.Mars should invest in Machine A because the net present value of Machine A after 4

years is higher than the net present value of Machine B after 6 years

46) A fully depreciated asset must be:

A.removed from the books

B.kept on the books until sold or discarded

C.disclosed only in the notes to the financial statements

D.recognized on the income statement as a loss

47) Machine with a useful life of 5 years and a residual value of $6,000 was purchased

on January 3, 2007, for $48,500. The machine was sold on January 5, 2012, for

$13,000.

(a) What is the book value of the machine on January 5, 2012, assuming straight-line

depreciation is used?

(b) Illustrate the effects on the accounts and the financial statements of the sale of the

machine on January 5, 2012 .

(c) Illustrate the effects on the accounts and the financial statements of the sale of the

machine if it had been sold for $18,000 instead.

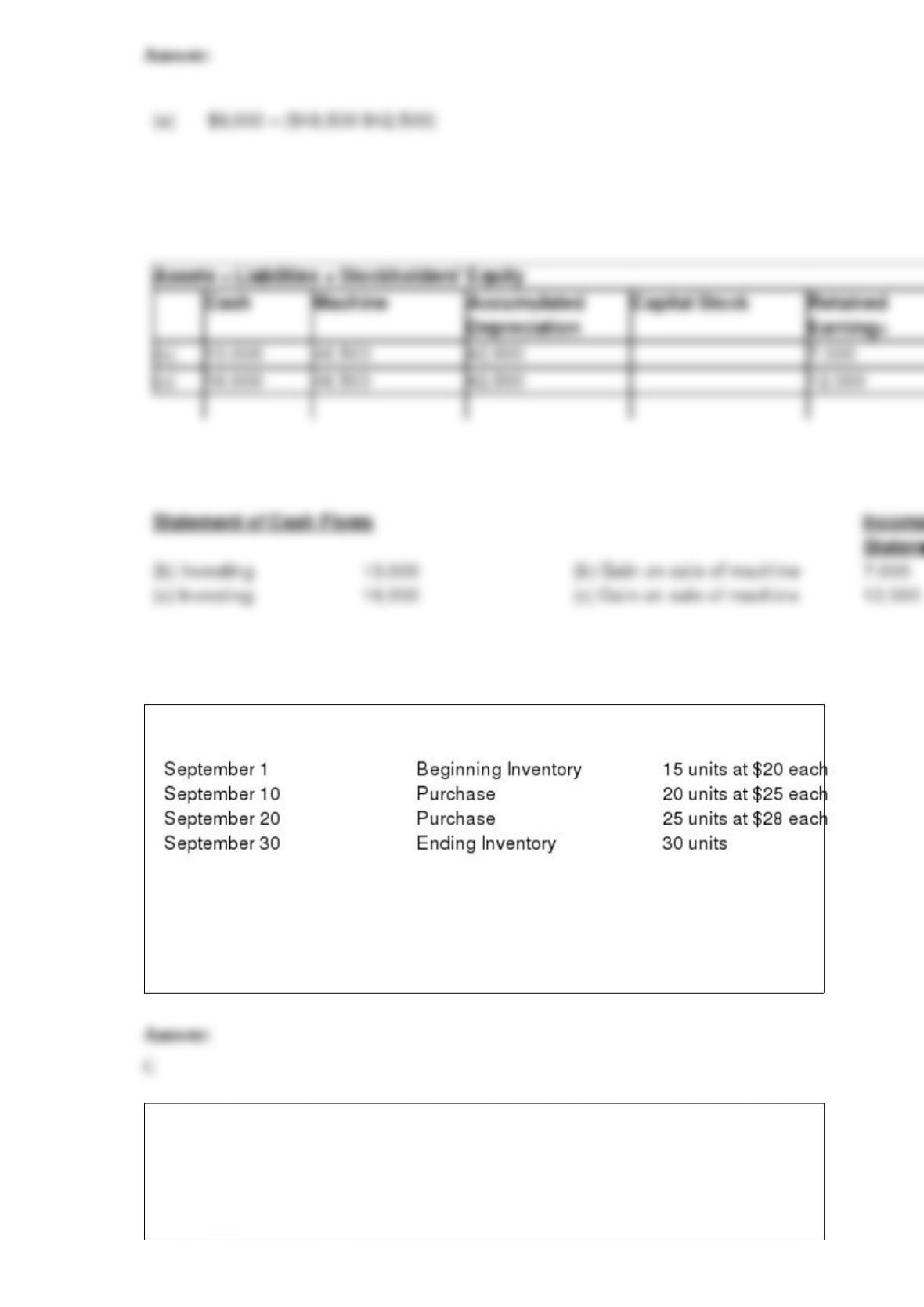

48) Use the following data to calculate cost of merchandise sold under FIFO method.

A.$825

B.$750

C.$675

D.$600

49) Payroll taxes levied against employees become liabilities:

A.on the first of the following month

B.at the time the liability for the employees wages is paid

C.when earned by the employee

D.at the end of an accounting period