Accounts receivable arise from credit sales to customers by both retailers and

wholesalers.

“Bookkeeping” is another term for “accounting”.

If the supplier pays freight charges, then ownership of inventory passes when goods

arrive at their destination.

A liability expressed by a written promise to make a future payment is usually called an

account payable.

There is no difference in the amount of inventory calculated by the periodic and

perpetual inventory systems when using the FIFO cost flow assumption.

Although, in a sole proprietorship, owner investments are not recorded as revenue, any

withdrawals are recorded as expenses.

It is acceptable to credit unearned revenues to revenue accounts when cash is received.

The accrual basis of accounting reflects the understanding that the economic effect of

revenue generally occurs when it is earned, not when cash is received.

Gallery Corp. performs 20 days’ work on a 30-day contract. The total contract is valued

at $6,000. The adjusting entry of $4,000 includes a credit to unearned revenue.

Salaries earned by employees, but unrecorded, are an example of an accrued expense.

Business events do not affect the accounting equation.

Private accountants work for several employers.

An unclassified balance sheet provides more information to users than a classified

balance sheet.

A contra account is an account the balance of which is added to the balance of an

associated account to show a more proper amount for the item recorded in the

associated account.

Each transaction recorded in the Sales Journal includes a debit to Accounts Receivable

and a credit to Sales Revenue.

Merchandise inventory refers to products a company owns for purposes of selling to

customers.

If the allowance method is used, the journal entry to record the reinstatement of an

account previously written off in the current period includes a debit to Accounts

Receivable and a credit to Bad Debt Expense.

On January 8, Gallery Corp. records $5,000 of accrued salaries. On January 15, $10,000

of salaries are paid. The entry on January 15 includes a debit to the Salaries Payable

account.

Merchandise inventory includes merchandise and office supplies.

During August, Gallery Corp. purchased $4,000 worth of supplies. At August 31 the

adjusted balance in the Supplies account was $2,800. The adjusting entry included a

$1,200 debit to Supplies Expense.

Before an adjusting entry for expired insurance is made, the amount in Prepaid

Insurance is overstated and Insurance Expense is overstated.

For a business, goods and services tax (GST) and/or Harmonized Sales Tax (HST) paid

is included in the amount recorded as an asset or an expense when a purchase is made.

Property, plant and equipment and intangible assets are long-term assets used to

produce or sell products and services.

Under the alternative method for recording prepaid expenses, the purchase of insurance

for cash would be recorded as a debit to Cash and a credit to Prepaid Insurance.

Phuong Vo borrowed $5,000 and signed a 3-month promissory note at 10%. The total

interest on the note is $125.

The assumption that a business will continue to operate until it can sell its assets to pay

its creditors underlies the going concern principle.

Gallery Corp. owes its employees $7,000 for the week ended March 31. The company

will pay the employees on April 5. The adjusting journal entry prepared on March 31

will include a debit to Salaries Expense and a credit to Cash.

Internal transactions often include cash payments.

To prepare the income statement all necessary numbers can be found in the income

statement columns of the work sheet, including the net income or net loss.

Posting is the process of copying the debit and credit amounts from a journal to the

ledger accounts.

Under the perpetual system, special journals are not required.

In a sole proprietorship, the Income Summary account is closed to the capital account

The balance sheet can be used in order to assess the creditworthiness of potential

customers.

Businesses normally get a full credit for the provincial sales tax (PST) they have paid.

The FIFO method assumes that costs for the most recently purchased items are

recovered first.

To prepare the balance sheet, all necessary numbers can be found in the balance sheet

columns of the work sheet, including ending capital.

The revenue recognition principle is the basis for making adjusting entries that pertain

to unearned and accrued revenues.

Liquidity measures how easily assets can be converted to another asset or be used to

pay for services or obligations.

The asset section of a classified balance sheet includes:

A. Current assets, long-term investments, property, plant and equipment, and intangible

assets.

B. Current assets, long-term assets, equity, and intangible assets.

C. Current assets, long-term investments, property, plant and equipment, and

withdrawals.

D. Current liabilities, long-term investments, property, plant and equipment, and

intangible assets.

E. Current assets, liabilities, property, plant and equipment, and intangible assets.

Special journals include:

A. Sales journal.

B. Cash receipts journal.

C. Purchases journal.

D. Cash disbursements journal.

E. All of these answers are correct.

The merchandise turnover ratio:

A. Is used to analyze profitability.

B. Is used to measure solvency.

C. Measures how quickly a firm sells its merchandise inventory.

D. Validates the acid-test ratio.

E. Depends on the type of inventory valuation method.

A merchandising company:

A. Earns net income from buying and selling merchandise.

B. Buys products from manufacturers and sells to retailers.

C. Buys products from manufacturers and sells them to consumers.

D. Reports cost of goods sold on the income statement.

E. All of these answers are correct.

A column in journals and accounts used to cross reference journal and ledger entries is

called the:

A. Account balance.

B. Debit.

C. Posting reference.

D. Credit.

E. Description.

If throughout an accounting period the fees for legal services paid in advance by clients

are recorded in an account called Unearned Legal Fees, the end-of-period adjusting

entry to record the portion of these fees that has been earned is:

A. Debit Cash and credit Legal Fees Earned.

B. Debit Cash and credit Unearned Legal Fees.

C. Debit Unearned Legal Fees and credit Legal Fees Earned.

D. Debit Legal Fees Earned and credit Unearned Legal Fees.

E. Some other entry.

Understatement of beginning inventory causes:

A. Cost of goods sold to be understated and net income to be understated.

B. Cost of goods sold to be understated and net income to be overstated.

C. Cost of goods sold to be overstated and net income to be overstated.

D. Cost of goods sold to be overstated and net income to be understated.

E. Cost of goods sold to be overstated and net income to be accurate.

The following information is available for Isla Company for last May. How much is the

net income for the month?

A. $0

B. $10,000.

C. $20,000.

D. $30,000.

E. $35,000.

Accrued revenues:

A. Are paid in advance.

B. At the end of one accounting period often result in cash receipts from customers in

the next period.

C. At the end of one accounting period often result in cash payments in the next period.

D. Are also called unearned revenues.

E. Are listed on the balance sheet as liabilities.

Sales returns and allowances:

A. Provide information about dissatisfied customers and the possibility of lost future

sales.

B. Are usually recorded in separate contra-revenue accounts.

C. Are omitted from published statements.

D. Represent a reduction of the customer’s account receivable.

E. All of these answers are correct.

Generally accepted accounting principles require that the inventory of a company be

reported at:

A. Net realizable value.

B. Historical cost.

C. Lower of cost and net realizable value.

D. Replacement cost.

E. Purchase price.

The J. Dawson, Capital account has a credit balance of $1,200 before closing entries are

made. If total revenues for the year are $65,200, total expenses $49,800, and

withdrawals are $2,400, what is the ending balance in the J. Dawson, Capital account

after all closing entries have been made?

A. $5,200.

B. $7,600.

C. $14,200.

D. $16,600.

E. $23,200.

Patel Packing had the following information for its inventory:

Beginning inventory: cost $107,000; retail $130,000

Net purchases: cost $58,000; retail $120,000

Sales at retail: $145,000

What is the estimated cost of the ending inventory?

A. $44,188.

B. $57,102.

C. $57,750.

D. $69,300.

E. $105,000.

A list of all accounts used by a company, including the identification number assigned

to each account, is called a:

A. Ledger.

B. Journal.

C. Trial balance.

D. Chart of accounts.

E. General Journal.

The merchandise turnover ratio:

A. Is cost of goods sold divided by average merchandise inventory.

B. Is average merchandise inventory divided by cost of goods sold.

C. Is ending inventory divided by cost of goods sold.

D. Is cost of goods sold divided by ending inventory.

E. Is cost of goods sold divided by ending inventory times 365.

On December 31 of the current year, TechCom’s unadjusted trial balance included the

following items: Accounts Receivable, debit balance of $107,250; Allowance for

Doubtful Accounts, credit balance of $1,900. What amount should be debited to Bad

Debt Expense, assuming 6% of outstanding accounts receivable as of December 31 of

the current year, are estimated to be uncollectible?

A. $2,835.

B. $3,755.

C. $4,535.

D. $6,435.

E. $8,335.

The timeliness principle assumes that an organization’s activities can be divided into

specific time periods including:

A. One month.

B. Quarters.

C. Fiscal year.

D. Calendar year.

E. Any of the above.

Throughout an accounting period, the fees for legal services paid in advance by clients

are recorded in an account called Unearned Legal Fees. If the accountant fails to make

the end-of-period adjusting entry to record the portion of these fees that has been

earned, one effect will be:

A. An overstatement of equity.

B. An understatement of equity.

C. An understatement of assets.

D. An understatement of liabilities.

E. An overstatement of net income.

An internal control system is the policies and procedures that managers use to:

A. Protect assets.

B. Ensure reliable accounting.

C. Promote efficient operations.

D. Encourage adherence to company policies.

E. All of these answers are correct.

Reese’s Company reported equity of $22,000 on its December 31, 2014 balance sheet.

The following information is available for the year ended December 31, 2015:

What are the total assets of Reese’s Company at December 31, 2015?

A. $14,000.

B. $25,000.

C. $35,000.

D. $47,000.

E. $57,000.

In reimbursing the petty cash fund:

A. Cash is debited.

B. Petty Cash is credited.

C. Petty Cash is debited.

D. Expense accounts are debited.

E. Petty Cash is credited and expense accounts are debited.

An account balance is:

A. The total of the credit side of the account.

B. The total of the debit side of the account.

C. The difference between the increases (including the beginning balance) and

decreases recorded in the account.

D. The same as the balance sheet equation.

E. Not used in the real world.

Today, Cedar Park Company paid $600 of its accounts payable in cash. What is the

effect on the accounting equation?

A. Assets, $600 increase; liabilities, no effect; equity, $600 increase.

B. Assets, $600 decrease; liabilities, $600 decrease; equity, no effect.

C. Assets, $600 decrease; liabilities, $400 increase; equity, $200 decrease.

D. Assets, no effect; liabilities, $600 decrease; equity, $400 increase.

E. No effect.

A credit sale of $2,500 to a customer would result in:

A. A credit to the Accounts Receivable account in the general ledger and a credit to the

customer’s account in the Accounts Receivable Ledger.

B. A debit to the Accounts Receivable account in the general ledger and a debit to the

customer’s account in the Accounts Receivable Ledger.

C. A debit to the Accounts Receivable account in the general ledger and a credit to the

customer’s account in the Accounts Receivable Ledger.

D. A credit to the Accounts Receivable account in the general ledger and a debit to the

customer’s account in the Accounts Receivable Ledger.

E. A credit to Sales and a credit to the customer’s account in the Accounts Receivable

Ledger.

The accounting cycle begins with:

A. Preparing financial statements and other reports.

B. Analysis of economic events and recording their effects.

C. Posting to the ledger.

D. Presentation of financial information to decision makers.

E. None of these answers is correct.

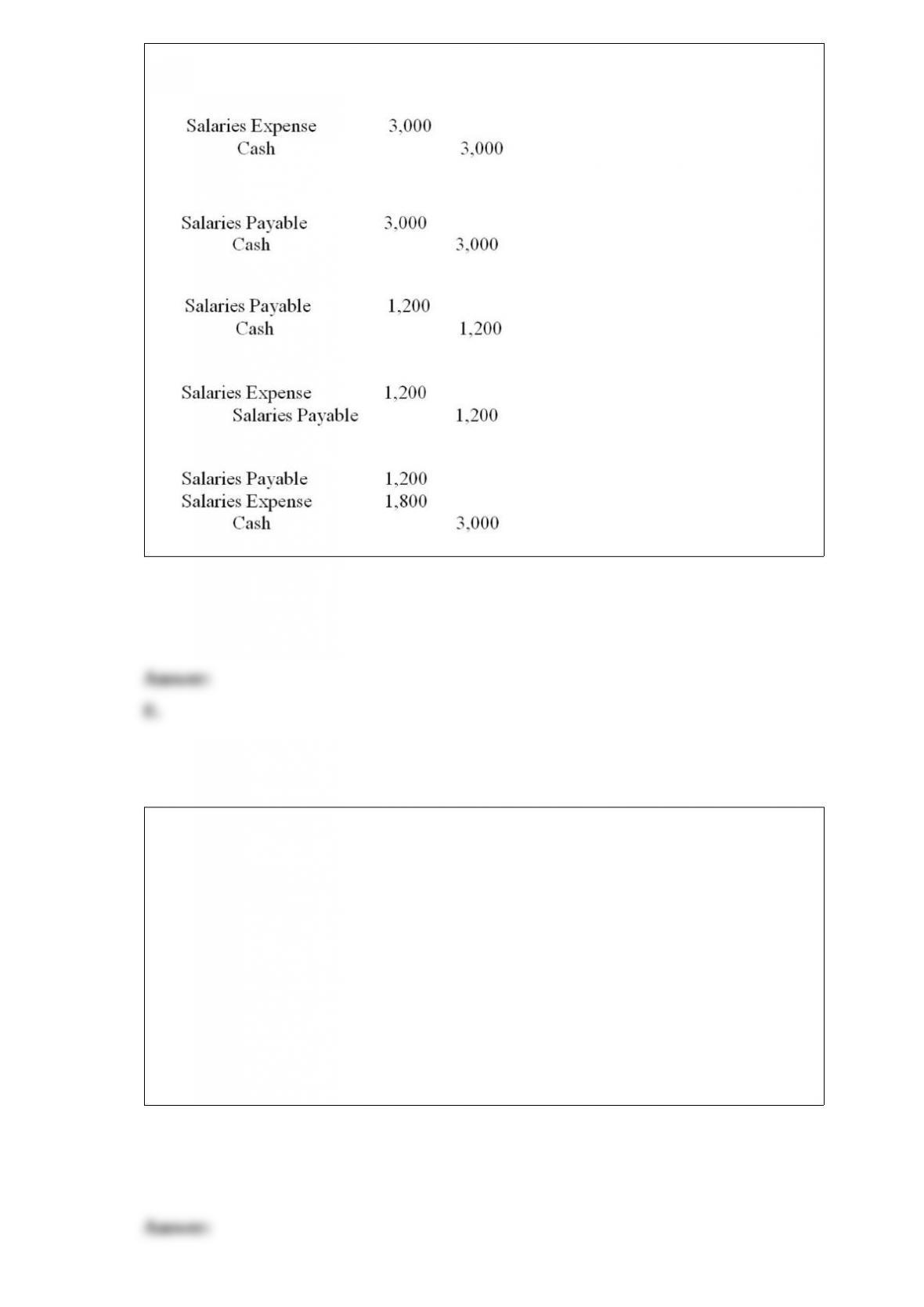

An adjusting entry was made on December 31, 2015, to accrue salaries expense of

$1,200. Which of the following entries would be prepared to record the next payment of

salaries, on January 5, 2016, in the amount of $3,000?

A.

B.

C.

D.

E.

Welder Company purchases supplies from Plumber Company on account. The entry for

this transaction will include a:

A. Debit to Accounts Payable for Welder Company.

B. Debit to Accounts Receivable for Welder Company.

C. Debit to Accounts Receivable for Plumber Company.

D. Credit to Accounts Payable for Plumber Company.

E. Credit to Accounts Receivable for Welder Company.

Retailers:

A. Buy products from manufacturers and sell to wholesalers.

B. Buy products from wholesalers and sell to other wholesalers.

C. Buy products from manufacturers and wholesalers and sell to consumers.

D. Buy only from wholesalers.

E. All of these answers are correct.

A summary of the ledger that lists the accounts and their balances, in which the total

debit balances should equal the total credit balances, is called a(n):

A. Account balance.

B. Trial balance.

C. Ledger.

D. Chart of accounts.

E. General Journal.

Gross profit is:

A. The same as net income.

B. Subtracted from operating income to get net income.

C. Net sales less cost of goods sold.

D. A special general ledger account.

E. Only calculated when using the perpetual inventory system.

After posting is completed, there may be an error if:

A. The sum of the customer account balances does not equal the total in the sales

journal.

B. The sum of the accounts receivable ledger does not equal the balance in the sales

account.

C. The sum of the customer account balances does not equal the accounts receivable

controlling account balance.

D. The balance in the sales journal does not equal the accounts receivable controlling

account balance.

E. The sum of the accounts receivable ledger does not equal the balance in the sales

journal.

Explain why temporary accounts are closed each period.

The ______________ of a note is the time from the note’s date to its maturity date.

_______________ expenses support the overall operations of a company.

Explain the effect of an error in inventory valuation on financial statements.

Z-Mart had net sales of $741,800. Its cost of goods sold was _____________ and its

resulting gross profit was $282,884.

What is the main motivation for retailers to accept credit cards or debit cards?

Explain the current ratio. Describe how it is used to evaluate a company.

Using the perpetual system, what are the three types of inventory cost flow

assumptions?

Discuss how accrual accounting adds usefulness to financial statements.