1) Budgeting is an informal plan for future business activities.

2) Obligations not due within one year or the company’s operating cycle, whichever is

longer, are reported as current liabilities.

3) An out-of-pocket cost requires a future outlay of cash and is relevant for current and

future decision making.

4) On May 1, Jorge Co. purchases 2,000 shares of Radiotech stock for $25,000. This

investment is considered to be an available-for-sale investment. On July 31 (Jorge’s

year-end), the stock had a market value of $28,000. Jorge should record a credit to

Unrealized Gain-Equity for $3,000.

5) If land is purchased as a building site, the cost of removing existing structures is not

charged to the Land account.

6) The management concept of customer orientation encourages a company to set up its

production system to produce large quantities of the same product for all customers.

7) The budgeted balance sheet and income statement are normally completed after

preparation of operating and capital expenditure budgets.

8) Reversing entries are recorded in response to external transactions that were created

in error during the prior accounting period.

9) A high merit rating for state unemployment taxes means that an employer has high

employee turnover or seasonal hiring.

10) The balanced scorecard aids in continuous improvement by augmenting financial

measures with information on the drivers or indicators of future financial performance.

11) The carrying value of a long-term note is computed as the present value of all

remaining future payments, discounted using the market rate at the time of issuance.

12) Trading securities are securities that are purchased by trading securities with other

companies rather than by paying cash.

13) Job order production systems would be appropriate for companies that produce

training films for a specific customer or custom-made furniture to be used in a new

five-star resort hotel.

14) The journal entry to record the declaration of dividends on common stock includes

a debit to Retained Earnings and a credit to Common Dividend Payable.

15) Standard costs can be used by management to assess the reasonableness of actual

costs incurred.

16) Which of the following statements is true?

A.Interest on bonds is tax deductible.

B.Interest on bonds is not tax deductible.

C.Dividends to stockholders are tax deductible.

D.Bonds do not have to be repaid.

E.Bonds always increase return on equity.

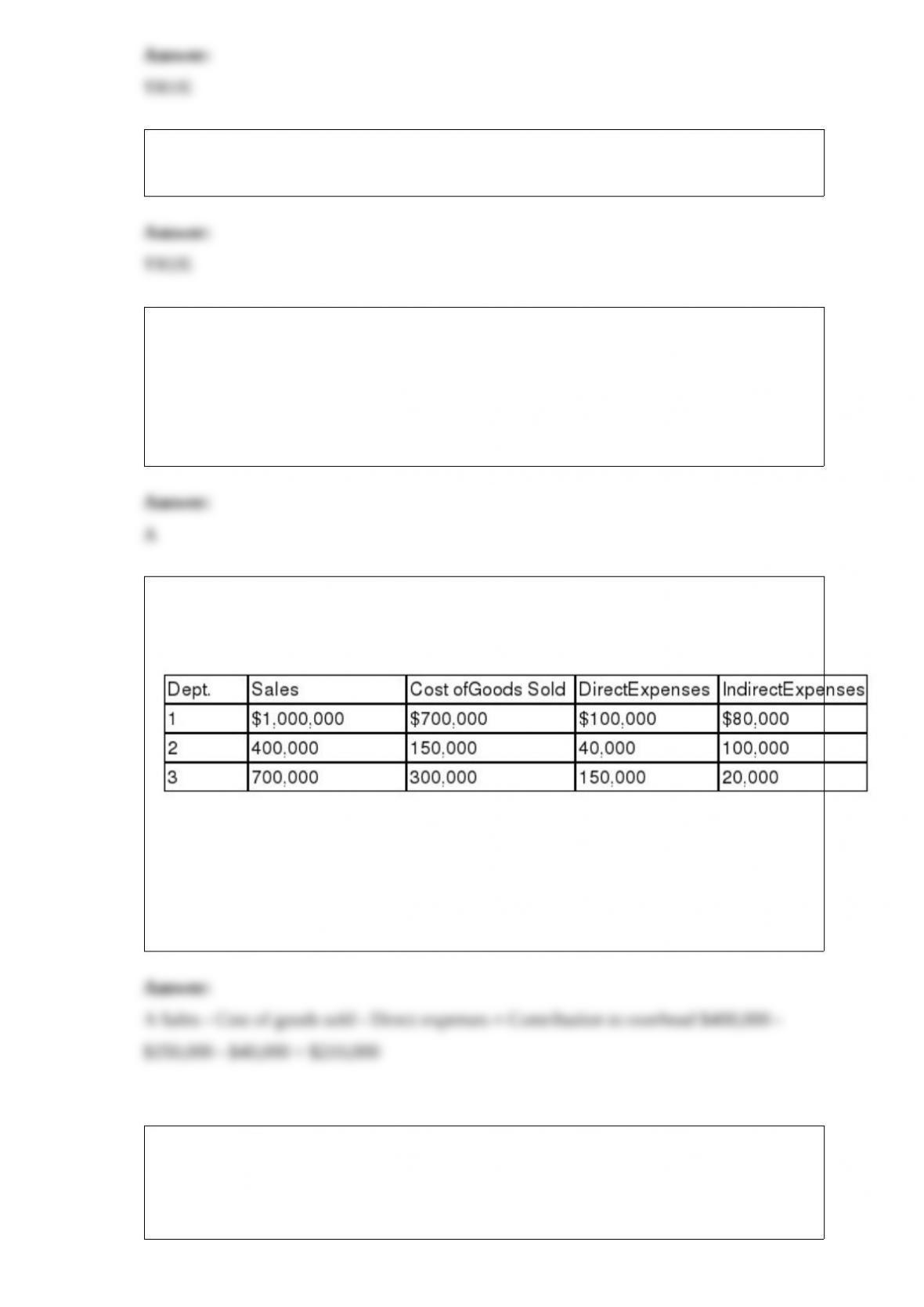

17) Ultimo Co. operates three production departments as profit centers. The following

information is available for its most recent year. Department 2’s contribution to

overhead in dollars is:

A.$210,000.

B.$350,000.

C.$10,000.

D.$260,000.

E.$150,000.

18) On January 1, a company issues bonds dated January 1 with a par value of

$400,000. The bonds mature in 5 years. The contract rate is 7%, and interest is paid

semiannually on June 30 and December 31. The market rate is 8% and the bonds are

sold for $383,793. The journal entry to record the first interest payment using

straight-line amortization is:

A.Debit Interest Payable $14,000.00; credit Cash $14,000.00.

B.Debit Interest Expense $14,000.00; credit Cash $14,000.00.

C.Debit Interest Expense $15,620.70; credit Discount on Bonds Payable $1,620.70;

credit Cash $14,000.00.

D.Debit Interest Expense $12,379.30; debit Discount on Bonds Payable $1,620.70;

credit Cash $14,000.00.

E.Debit Interest Expense $15,620.70; credit Premium on Bonds Payable $1,620.70;

credit Cash $14,000.00.

19) A corporation issued 6,000 shares of its $2 par value common stock in exchange for

land that has a market value of $84,000. The entry to record this transaction would

include:

A.A debit to Common Stock for $12,000.

B.A debit to Land for $12,000.

C.A credit to Land for $12,000.

D.A credit to Paid-in Capital in Excess of Par Value, Common Stock for $72,000.

E.A credit to Common Stock for $84,000.

20) All of the following regarding the current ratio are true except:

A.Current ratio is calculated by dividing current assets by current liabilities.

B.Current ratio helps to assess a company’s ability to pay its debts in the near future.

C.Current ratio does not affect a creditor’s decision on whether to allow a company to

buy on credit.

D.Current ratio can affect a creditor’s decision about whether to lend money to a

company.

E.Current ratio can reveal challenges in covering short-term obligations if it is less than

1.

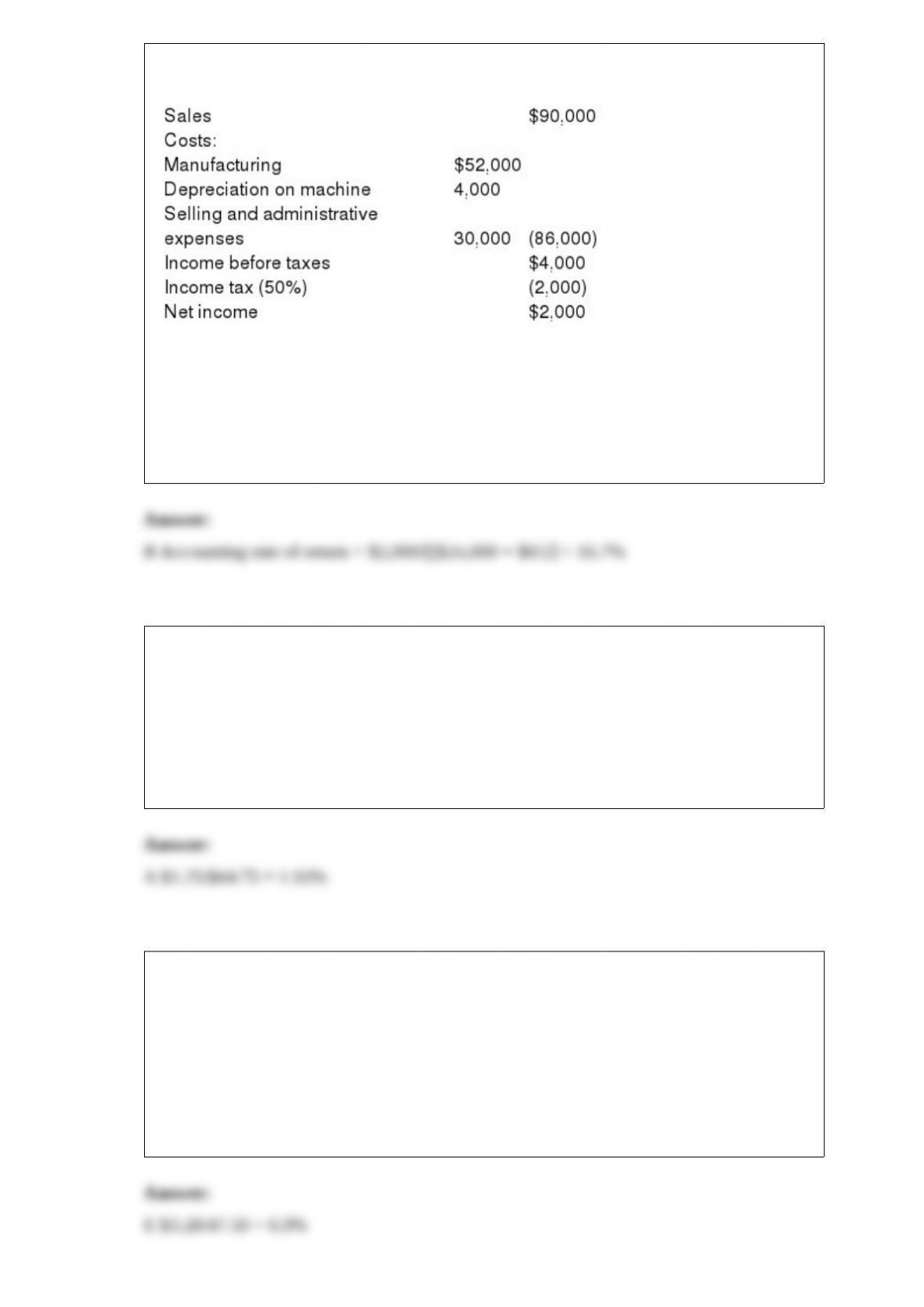

21) A company is planning to purchase a machine that will cost $24,000, have a

six-year life, and be depreciated over a three-year period with no salvage value. The

company expects to sell the machine’s output of 3,000 units evenly throughout each

year. A projected income statement for each year of the asset’s life appears below. What

is the accounting rate of return for this machine?

A.33.3%.

B.16.7%.

C.50.0%.

D.8.3%.

E.4%.

22) A company reports basic earnings per share of $3.50, cash dividends per share of

$1.25, and a market price per share of $64.75. The company’s dividend yield equals:

A.1.93%.

B.2.14%.

C.4.67%.

D.5.41%.

E.18.50%.

23) The market price of Horokhiv Corporation’s common stock at the start of 2014 was

$47.50 and it declared and paid cash dividends of $3.28 per share. The Dividend yield

ratio is:

A.14.5%.

B.7.4%.

C.6.5%.

D.144.8%.

E.6.9%.

24) A company borrowed $10,000 by signing a 180-day promissory note at 9%. The

total interest due on the maturity date is.

A.$900

B.$75

C.$450

D.$300

E.$1,800

25) After all activity costs are accumulated in an activity cost pool account, overhead

rates are computed and costs are allocated to cost objects based on:

A.Direct factors.

B.Indirect factors.

C.Cost drivers.

D.Joint cost principles.

E.Opportunity cost principles.

26) Horizontal analysis:

A.Is a method used to evaluate changes in financial data across time.

B.Is also called vertical analysis.

C.Is the presentation of financial ratios.

D.Is a tool used to evaluate financial statement items relative to industry statistics.

E.Evaluates financial data across industries.

27) Frisco Company’s Merchandise Inventory account at the end of year 2015 has a

balance of $62,115, but a physical count reveals that only $61,900 of inventory exists.

The adjusting entry to record this $215 of inventory shrinkage is:

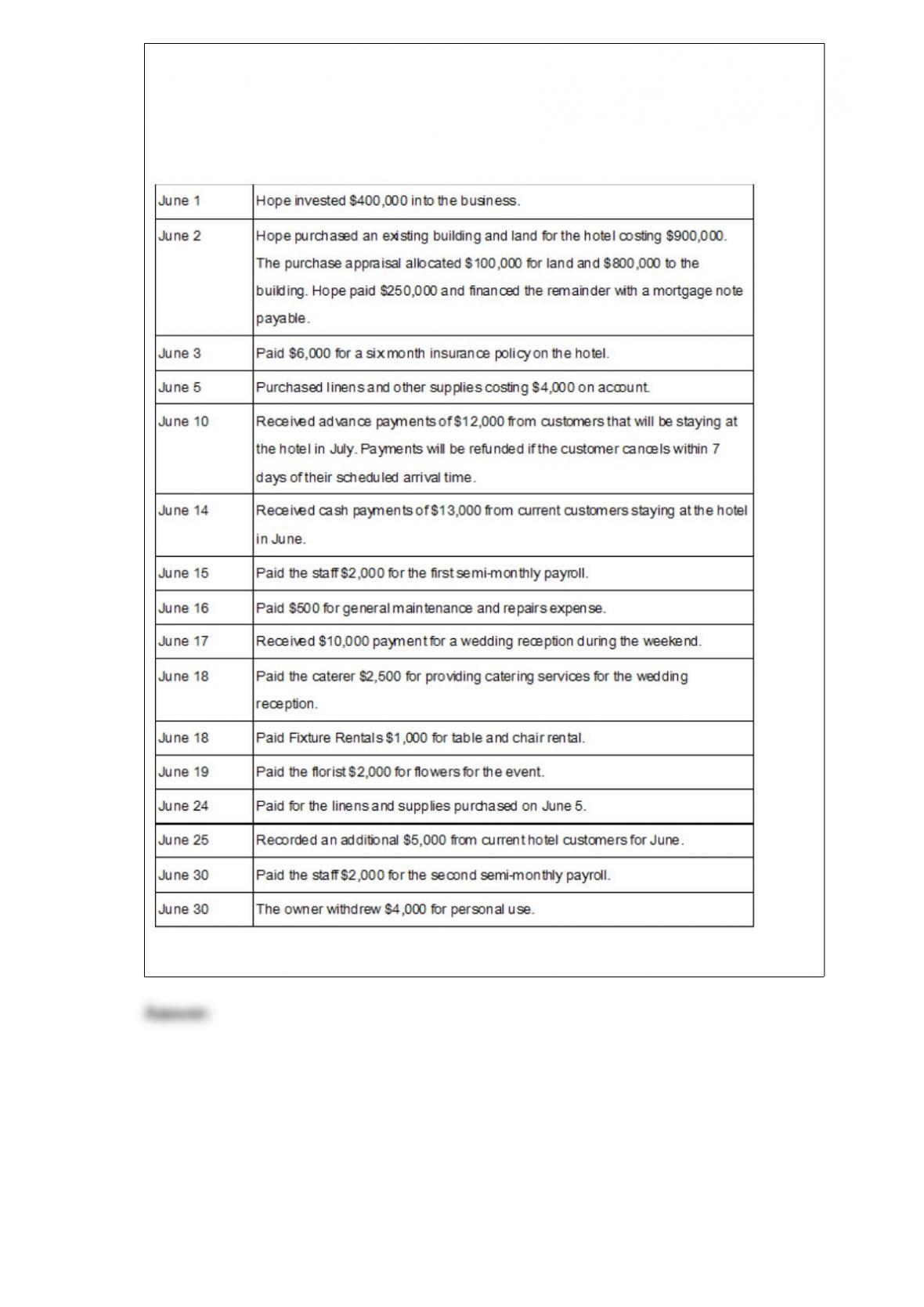

28) Jason Hope decided to open a hotel in his hometown. Prepare journal entries to

record the following transactions. Hope uses the accounts Room Rental Revenue and

Event Revenue. All expenses for special events are recorded as Event Expense.

29) Companies promoting continuous improvement strive to achieve _____________

standards by eliminating inefficiencies and waste.

30) The second step in the analyzing and recording process is to record the transactions

and events in the book of original entry, called the ______________.

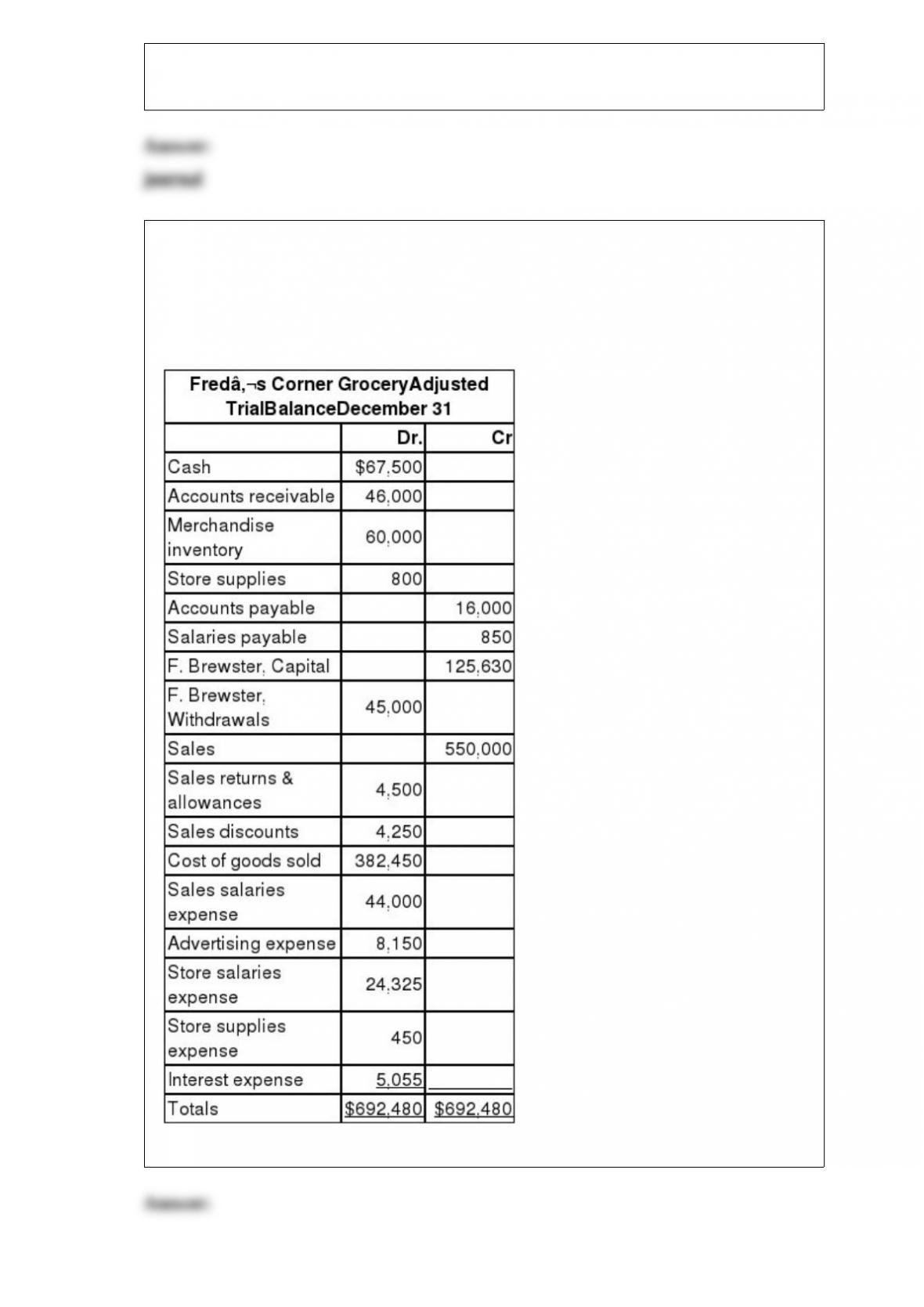

31) Following is the year-end adjusted trial balance for Fred’s Corner Grocery for the

current year:

Prepare the closing entries at December 31 for the current year.