1) Pisa, Inc. leased equipment from Tower Company under a four-year lease requiring

equal annual payments of $172,076, with the first payment due at lease inception. The

lease does not transfer ownership, nor is there a bargain purchase option. The

equipment has a 4-year useful life and no salvage value. Pisa, Inc.s incremental

borrowing rate is 10% and the rate implicit in the lease (which is known by Pisa, Inc.) is

8%. Pisa, Inc. uses the straight-line method to depreciate similar assets. What is the

amount of depreciation expense recorded by Pisa, Inc. in the first year of the assets life?

PV Annuity DuePV Ordinary Annuity

8%, 4 periods 3.57710 3.31213

10%, 4 periods 3.48685 3.16986

a.$0 because the asset is depreciated by Tower Company.

b.$142,484

c.$153,883

d.$150,000

2) __________ ratios measure how effectively a company uses its assets.

a.Liquidity

b.Activity

cProfitability

d.Coverage

3) Which of the following items should be included in a company’s inventory at the

balance sheet date?

a.Goods in transit which were purchased f.o.b. destination

b.Goods received from another company for sale on consignment

c.Goods sold to a customer which are being held for the customer to call for at his or

her convenience

d.None of these answer choices are correct

4) For Randolph Company, the following information is available:

Capitalized leases$560,000

Copyrights190,000

Long-term receivables210,000

In Randolphs balance sheet, intangible assets should be reported at

a.$190,000

b.$220,000

c.$750,000

d.$780,000

5) Under the installment-sales method,

a.revenue, costs, and gross profit are recognized proportionate to the cash that is

received from the sale of the product

b.gross profit is deferred proportionate to cash uncollected from sale of the product, but

total revenues and costs are recognized at the point of sale

c.gross profit is not recognized until the amount of cash received exceeds the cost of the

item sold

d.revenues and costs are recognized proportionate to the cash received from the sale of

the product, but gross profit is deferred until all cash is received

6) Which of the following disclosures is required for a change from LIFO to FIFO?

a.The cumulative effect on prior years, net of tax, in the current retained earnings

statement

b.The justification for the change

c.Restated prior year income statements

d.All of these are required

7) Which of the following organizations has been responsible for setting U.S.

accounting standards?

a.The Accounting Principles Board

b.The Committee on Accounting Procedure

c.The Financial Accounting Standards Board

d.All of the answer choices are correct

8) Davis Company purchased a new piece of equipment on July 1, 2014 at a cost of

$1,800,000. The equipment has an estimated useful life of 5 years and an estimated

salvage value of $150,000. The current year end is 12/31/15. Davis records depreciation

to the nearest month.

If, at the end of 2016, Davis Company decides the equipment still has five more years

of life beyond 12/31/16, with a salvage value of $150,000, what is straight-line

depreciation for 2016? (Assume straight-line used in all years.)

a.$180,000

b.$192,500

c.$217,500

d.$330,000

9) Which of the following items will not appear in the retained earnings statement?

a.Net loss

b.Prior period adjustment

c.Discontinued operations

d.Dividends

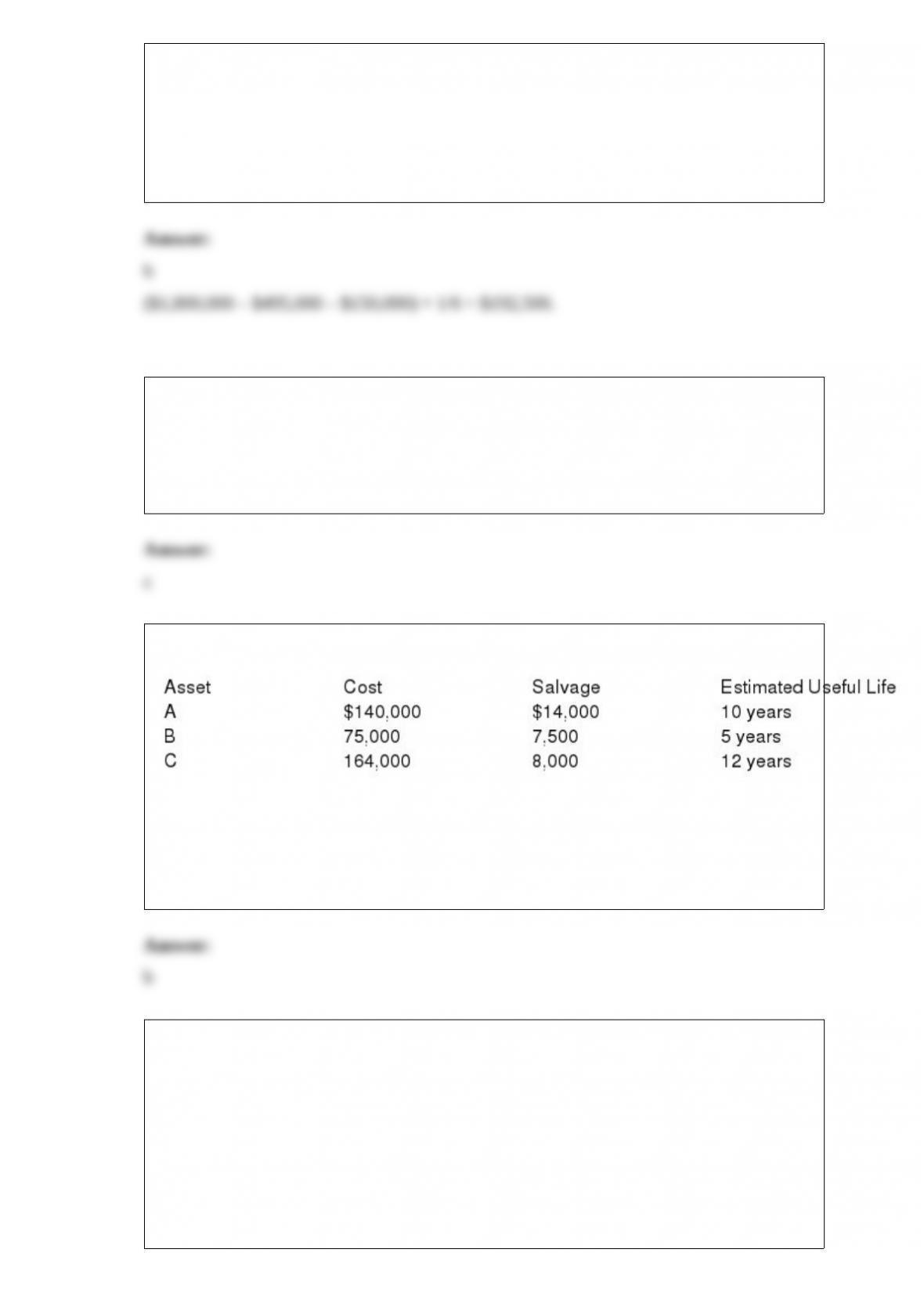

10) Exiter Inc. owns the following assets:

What is the composite depreciation rate of Exiter’s assets?

a.14.0%

b.10.3%

c.12.9%

d.11.1%

11) Various accounting assumptions, principles, constraints, and characteristics are

listed below. Select those which best justify the following accounting procedures and

indicate the corresponding letter(s) in the space(s) provided. A letter may be used more

than once or not at all.

a.Historical costf.Economic entityk.Revenue recognition

b.Relevanceg.Cost constraintl.Full disclosure

c.Monetary unith.Conservatismm.Faithful

d.Going concerni.Periodicityrepresentation

e.Consistencyj.Expense recognition

1> Chose the solution that will be least likely to overstate assets or income.

2> Describing the depreciation methods used in the financial statements.

3> Applying the same accounting treatment to similar accounting events.

4> The quality which helps users make predictions about present, past, and future

events.

5> Recording a transaction when goods or services are exchanged for cash or claims to

cash.

6> Preparing consolidated statements.

7> Information must make a difference or a company need not disclose it.

8> Provides the figure at which to record a liability.

9> The preparation of timely reports on continuing operations.

10> Accrual accounting (do not use “going concern”).

11> Reporting those items which are significant enough to affect decisions. Select two.

12> Additivity of financial statement figures relating to different time periods.

13> Ignoring the phenomenon of price-level changes (do not use “historical cost”).

14> Not reporting assets at liquidation prices (do not use “historical cost”).

15> Characterized by completeness, neutrality, and being free from error.

16> Establishment of an allowance for doubtful accounts.

17> Use of estimating procedures for amortization policies. Select two (do not use

“periodicity”) (17 and 18).

18> See item 17 above.

12) The reason for eliminating the price change in inventory is:

a.to measure the dollar increase in inventory

b.to inflate profits of a company

c.to increase the cost of inventory

d.to measure the real increase in inventory