1) Karma Corporation has total assets of $190,000 and total liabilities of $90,000. The

corporation’s debt-to-equity ratio is closest to:

A.0.47

B.0.90

C.0.53

D.0.32

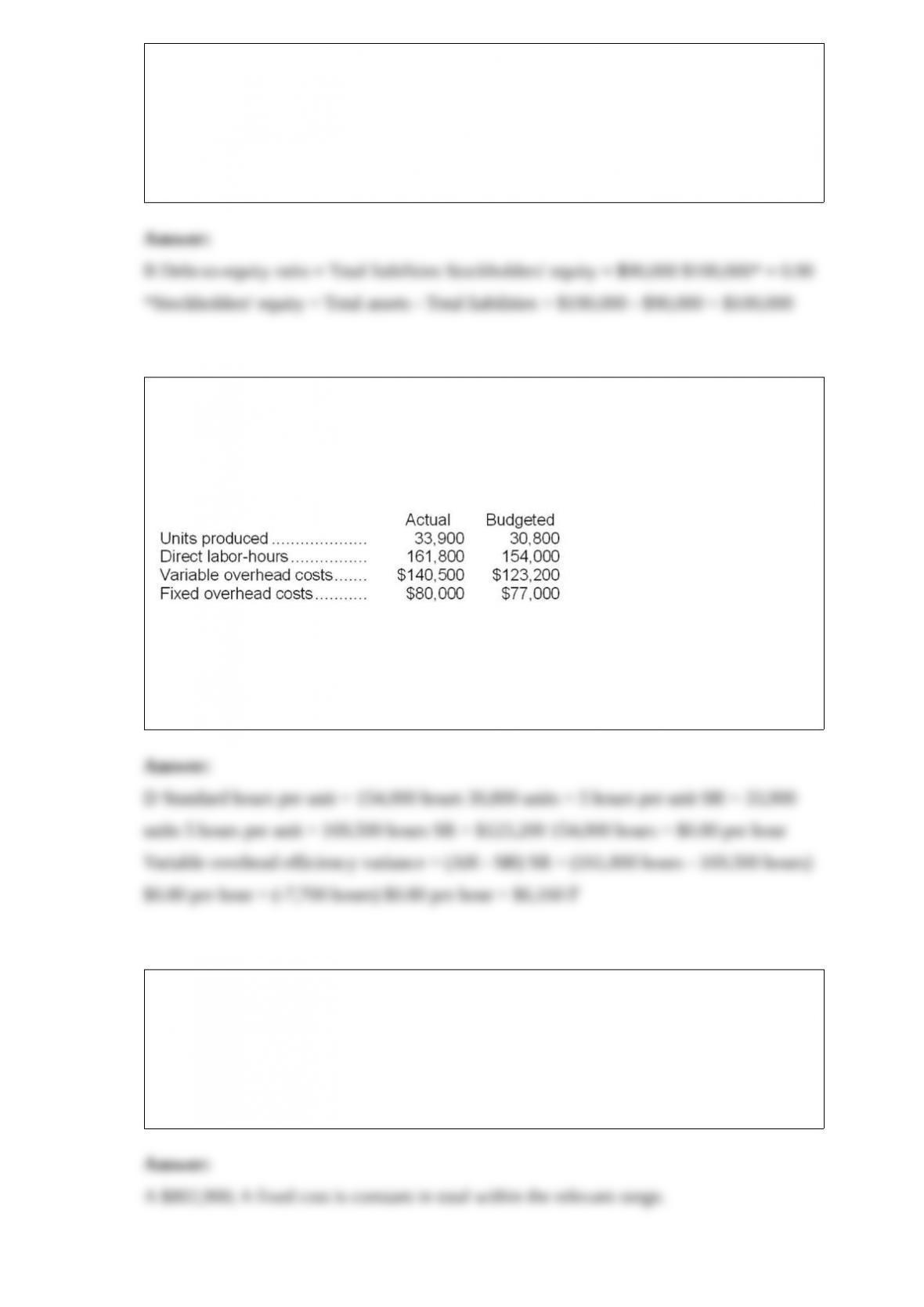

2) The Dillon Corporation makes and sells a single product. Overhead costs are applied

on the basis of standard direct labor-hours. The standard cost card shows that 5 direct

labor-hours are required per unit. The Dillon Corporation had the following budgeted

and actual data for March:

The variable overhead efficiency variance for March is:

A.$12,400 F

B.$6,160 U

C.$12,400 U

D.$6,160 F

3) To the nearest whole dollar, what should be the total property taxes at a sales volume

of 39,700 units? (Assume that this sales volume is within the relevant range.)

A) $802,900

B) $748,295

C) $832,195

D) $861,490

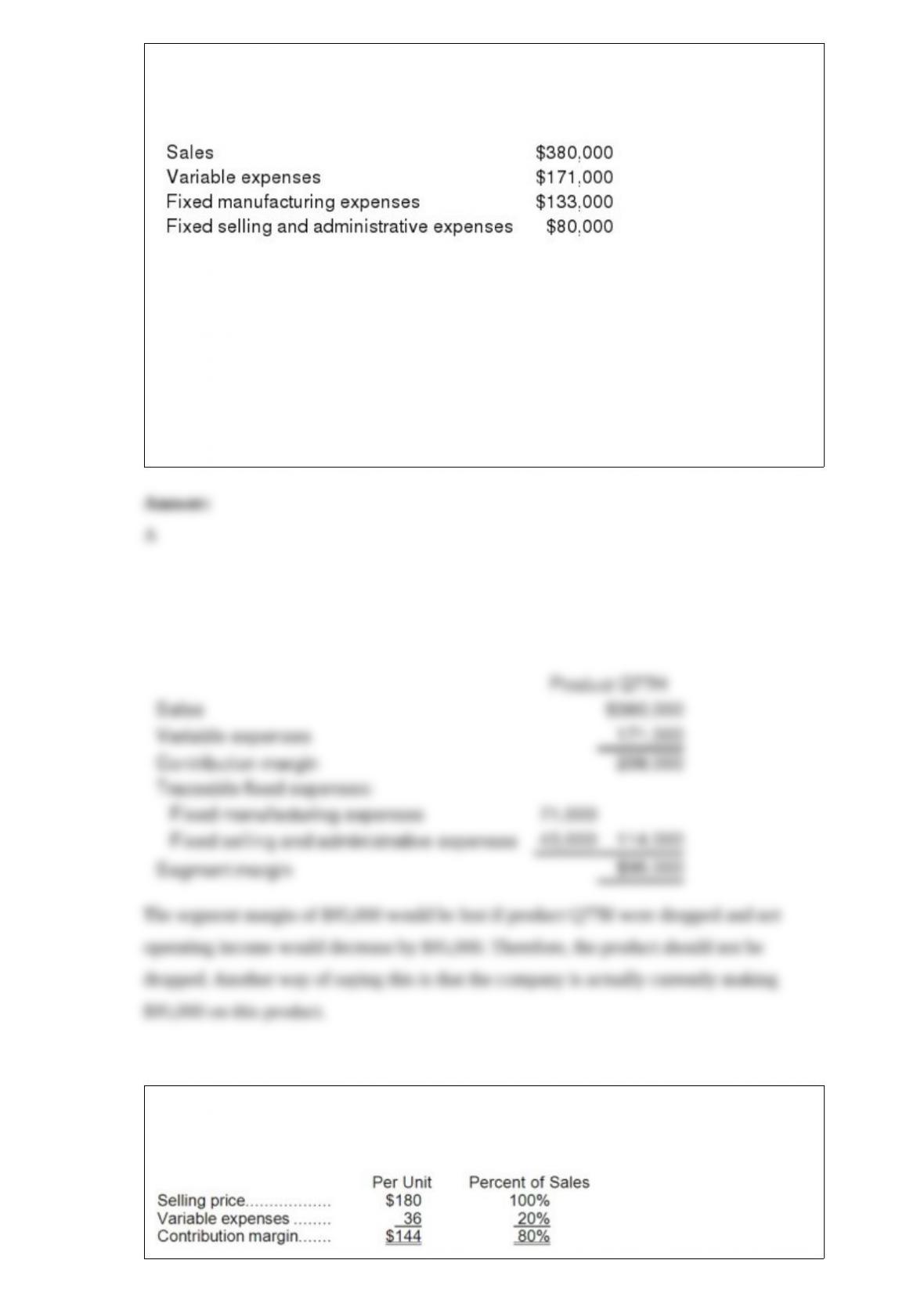

4) Product Q77H has been considered a drag on profits at Zenke Corporation for some

time and management is considering discontinuing the product altogether. Data from

the company’s accounting system appear below:

In the company’s accounting system all fixed expenses of the company are fully

allocated to products. Further investigation has revealed that $71,000 of the fixed

manufacturing expenses and $43,000 of the fixed selling and administrative expenses

are avoidable if product Q77H is discontinued. What would be the effect on the

company’s overall net operating income if product Q77H were dropped?

A) Overall net operating income would decrease by $95,000.

B) Overall net operating income would increase by $95,000.

C) Overall net operating income would increase by $4,000.

D) Overall net operating income would decrease by $4,000.

5) Bohlen Corporation produces and sells a single product. Data concerning that

product appear below:

Fixed expenses are $716,000 per month. The company is currently selling 6,000 units

per month. Consider each of the following questions independently.

The marketing manager would like to introduce sales commissions as an incentive for

the sales staff. The marketing manager has proposed a commission of $16 per unit. In

exchange, the sales staff would accept a decrease in their salaries of $84,000 per month.

(This is the company’s savings for the entire sales staff.) The marketing manager

predicts that introducing this sales incentive would increase monthly sales by 600 units.

What should be the overall effect on the company’s monthly net operating income of

this change?

A.increase of $74,400

B.increase of $64,800

C.decrease of $103,200

D.increase of $928,800

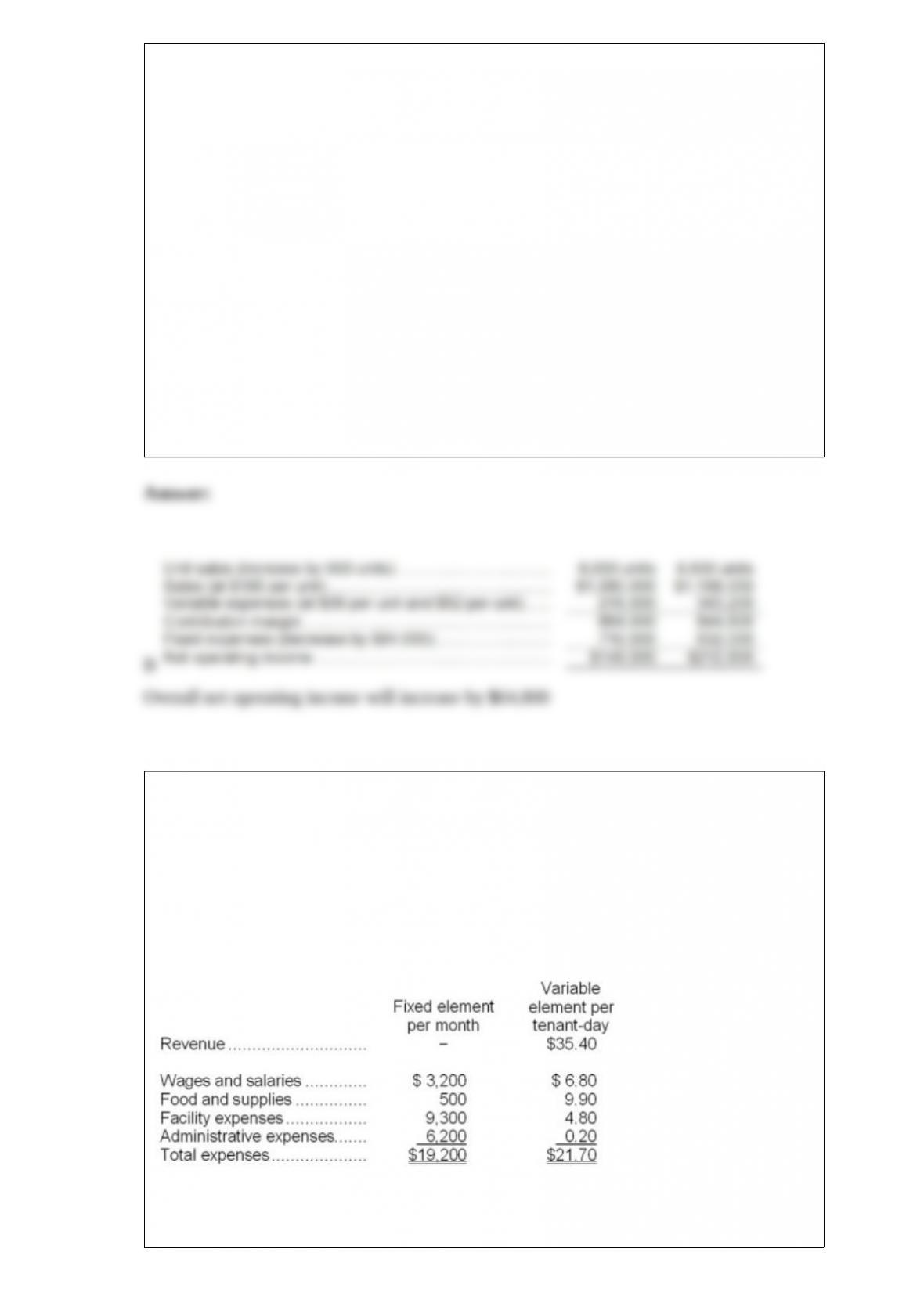

6) Ordway Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During June, the kennel budgeted for

2,100 tenant-days, but its actual level of activity was 2,070 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for June:

Data used in budgeting:

Actual results for June:

The wages and salaries in the planning budget for June would be closest to:

A.$17,480

B.$17,116

C.$17,364

D.$17,276

7) The income tax expense in year 2 is:

A.$14,000

B.$3,500

C.$7,000

D.$10,500

8) Cervetti Corporation has two major business segments-East and West. In July, the

East business segment had sales revenues of $220,000, variable expenses of $125,000,

and traceable fixed expenses of $29,000. During the same month, the West business

segment had sales revenues of $890,000, variable expenses of $472,000, and traceable

fixed expenses of $169,000. The common fixed expenses totaled $246,000 and were

allocated as follows: $123,000 to the East business segment and $123,000 to the West

business segment.

The contribution margin of the West business segment is:

A.$418,000

B.-$57,000

C.$513,000

D.$66,000

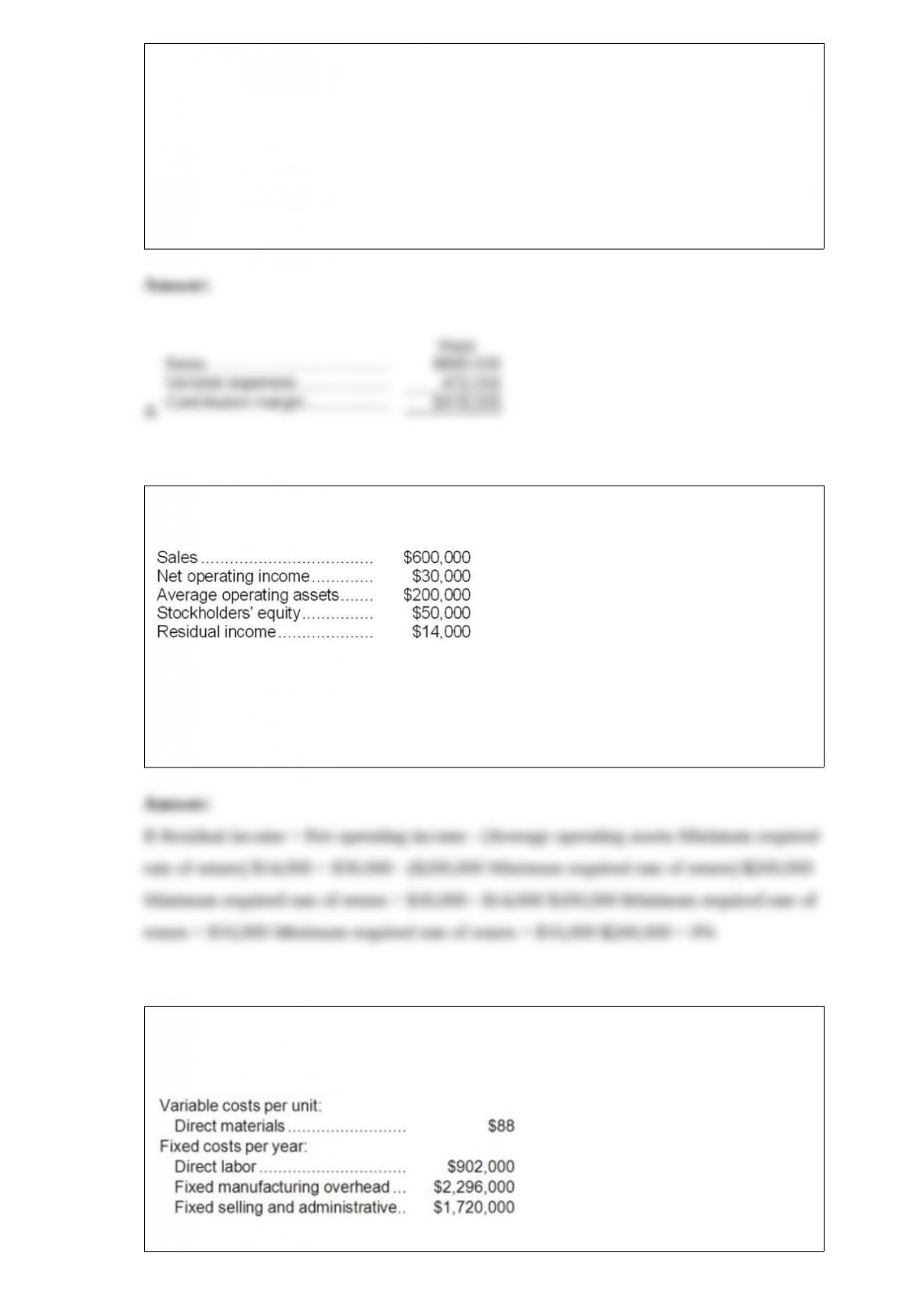

9) The Jenkins Division recorded operating data as follows for the past year:

For the past year, the minimum required rate of return was:

A.7%

B.8%

C.16%

D.14%

10) Phoeuk Corporation manufactures and sells one product. The following information

pertains to the company’s first year of operations:

The company does not have any variable manufacturing overhead costs or variable

selling and administrative costs. During its first year of operations, the company

produced 41,000 units and sold 40,000 units. The company’s only product is sold for

$231 per unit.

Assume that the company uses a variable costing system that assigns $22 of direct labor

cost to each unit that is produced. The net operating income under this costing system

is:

A.$714,000

B.$824,000

C.$802,000

D.$880,000

11) Routit Corporation had the following sales and production for the past four years:

Selling price per unit, variable cost per unit, and total fixed cost are the same each year.

There were no beginning inventories in Year 1. Which of the following statements is

correct?

A.Under variable costing, net operating income for Year 3 and Year 4 would be the

same.

B.Under variable costing, net operating income for Year 2 and Year 3 would be the

same.

C.Variable costing net income would exceed absorption costing net income in Year 1.

D.Absorption costing net income would exceed variable costing net income in Year 4.

12) How much will the company’s profits be increased or (decreased) if it prices the 100

units at $7 each?

A.$(30)

B.$150

C.$0

D.$310

13) How much profit (loss) does the company make by processing the intermediate

product cane juice into molasses rather than selling it as is?

A) $(43)

B) $(17)

C) $10

D) $(3)

14) Machain Corporation applies manufacturing overhead to products on the basis of

standard machine-hours. The company’s standard variable manufacturing overhead rate

is $2.90 per machine-hour. The actual variable manufacturing overhead cost for the

month was $15,270. The original budget for the month was based on 5,000

machine-hours. The company actually worked 5,090 machine-hours during the month.

The standard hours allowed for the actual output of the month totaled 5,200

machine-hours. What was the variable overhead efficiency variance for the month?

A.$580 Unfavorable

B.$190 Unfavorable

C.$509 Unfavorable

D.$319 Favorable

15) Lartey Corporation’s cost formula for its selling and administrative expense is

$22,200 per month plus $27 per unit. For the month of December, the company planned

for activity of 5,300 units, but the actual level of activity was 5,270 units. The actual

selling and administrative expense for the month was $168,150.

The selling and administrative expense in the planning budget for December would be

closest to:

A.$169,107

B.$165,300

C.$168,150

D.$164,490

16) The Claus Corporation makes and sells a single product and uses standard costing.

During January, the company actually used 8,700 direct labor-hours (DLHs) and

produced 3,000 units of product. The standard cost card for one unit of product includes

the following:

Variable factory overhead: 3.0 DLHs @ $4.00 per DLH.

Fixed factory overhead: 3.0 DLHs @ $3.50 per DLH.

For January, the company incurred $22,000 of actual fixed manufacturing overhead

costs and recorded a $875 favorable volume variance.

The denominator level of activity in direct labor-hours (DLHs) used by Claus in setting

the predetermined overhead rate for January is:

A.9,500 DLHs

B.9,250 DLHs

C.8,750 DLHs

D.10,500 DLHs

17) The company’s return on equity for Year 2 is closest to:

A.71.44%

B.4.72%

C.2.97%

D.1.93%

18) Beakins Corporation produces a single product. The standard cost card for the

product follows:

During a recent period the company produced 1,200 units of product. Various costs

associated with the production of these units are given below:

The company records all variances at the earliest possible point in time. Variable

manufacturing overhead costs are applied to products on the basis of standard direct

labor-hours.

The labor rate variance for the period is:

A.$3,150 U

B.$2,700 F

C.$2,700 U

D.$3,150 F