There is a universal chart of accounts that is applicable to all businesses.

a. True

b. False

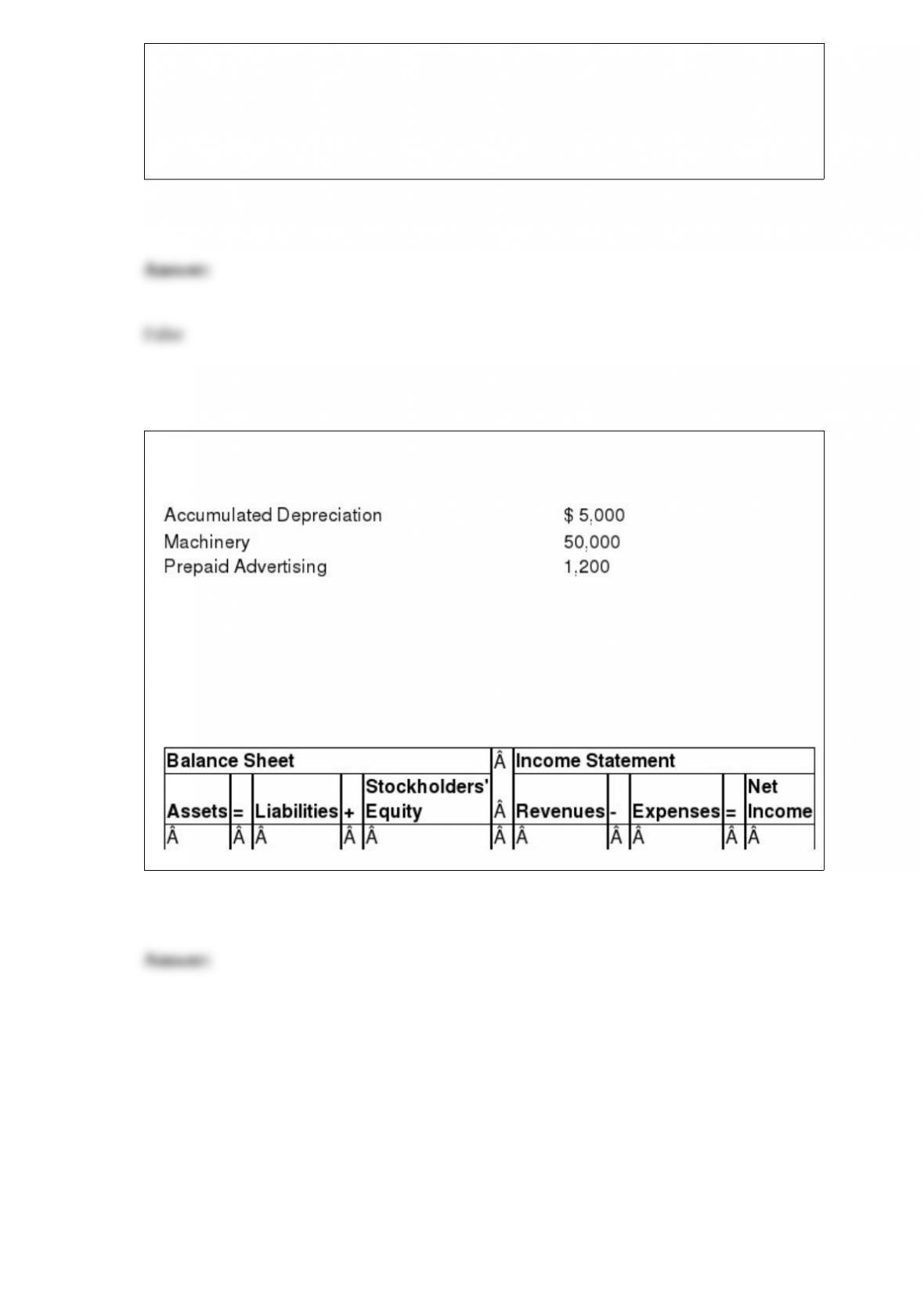

Marcus Roberts operates a small retail establishment. The following unadjusted

amounts were taken from Roberts’ accounting records at December 31, 2015:

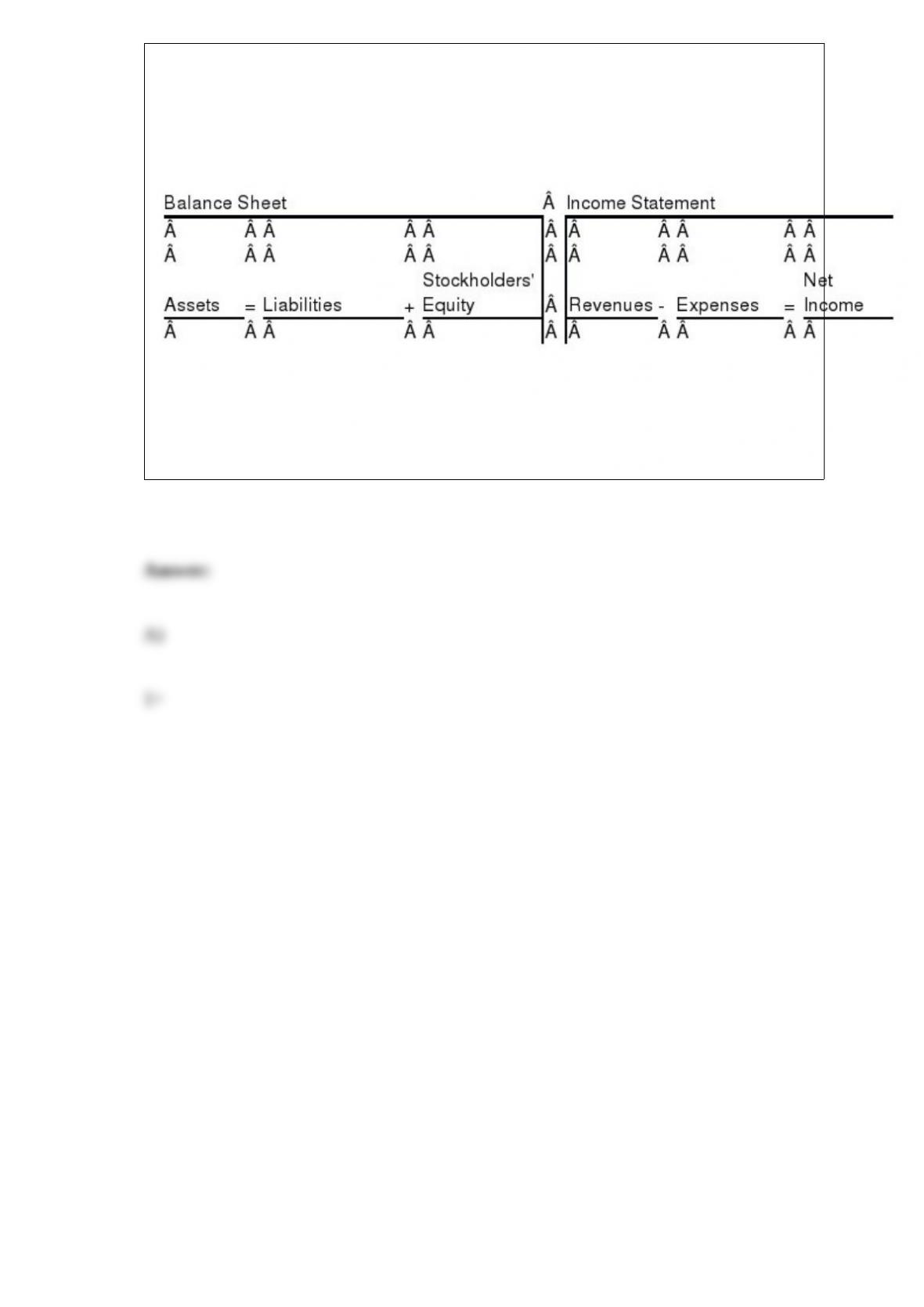

Determine the effect on the accounting equation of the adjusting entries at December

31, 2015, for each of the transactions that follow: A. The advertising costs are for

television commercials to be aired equally throughout December, 2015, and January

and February, 2016. B. The machinery had an original cost of $50,000 and was

purchased during 2010. The estimated useful life is 6 years with an estimated salvage

value equal to $8,000. Roberts uses the straight-line method of depreciation.

a. A receivable arising from the sale of goods or services with a verbal promise to pay.

b. A form used to categorize the various individual accounts receivable according to the

length of time each has been outstanding.

c. A method of estimating bad debts on the basis of either the net credit sales of the

period or the accounts receivable at the end of the period.

d. A measure of the number of times receivables are collected in a period.

e. The general ledger account that is supported by a subsidiary ledger.

f. A contra-asset account used to reduce accounts receivable to its net realizable value.

g. The detail for a number of individual items that collectively make up a single general

ledger account.

h. The recognition of bad debts expense at the point an account is written off as

uncollectible. Allowance method

Your bookkeeper is off for the day and you are trying to figure out what her last entry in

the journal could be for. Unfortunately, she only recorded the debit side of the

transaction as $4,400 to Accounts Payable. It is possible that this debit could correspond

to:

a. A purchase of equipment costing $4,400 on credit.

b. A payment of $4,400 to a supplier to settle a balance due.

c. A $4,400 sale to a customer.

d. A $4,400 issuance of the company’s capital stock.

Select the ratio that each statement below most properly satisfies.

a. Dividend yield ratio

b. Cash flow from operations to capital expenditures ratio

c. Debt service coverage ratio

d. Return on common stockholders’ equity ratio

e. Times interest earned ratio

f. Asset turnover ratio

g. Debt-to-equity ratio

h. Dividend payout ratio

i. Price/earnings ratio

An income statement measure of the ability of a company to make its interest payments

Which of the following statements best describes the effects of recognizing revenue

earned by a business entity?

a. Assets increase only when cash sales are made.

b. Stockholders’ equity increases only when credit sales are made.

c. Assets and stockholders’ equity increase when either cash or credit sales are made.

d. Assets increase, but stockholders’ equity decreases, when either cash or credit sales

are made.

Which one of the following is a financing activity of a business?

a. Paying for purchases of inventory

b. Issuing stock for cash

c. Paying salaries

d. Purchasing a manufacturing plant

Match the following choices to the listed situation.

a. a deferred expense

b. a deferred revenue

c. an accrued liability

d. an accrued asset

A warehouse building was acquired for cash

Which of the following statements about current liabilities is true?

a. Current liabilities are listed in order of decreasing amounts in the current liability

section of the balance sheet.

b. The amount of current liabilities has little implication for a company’s liquidity.

c. The current liability section never contains any portion of long-term liabilities.

d. The current ratio is defined as current assets divided by current liabilities.

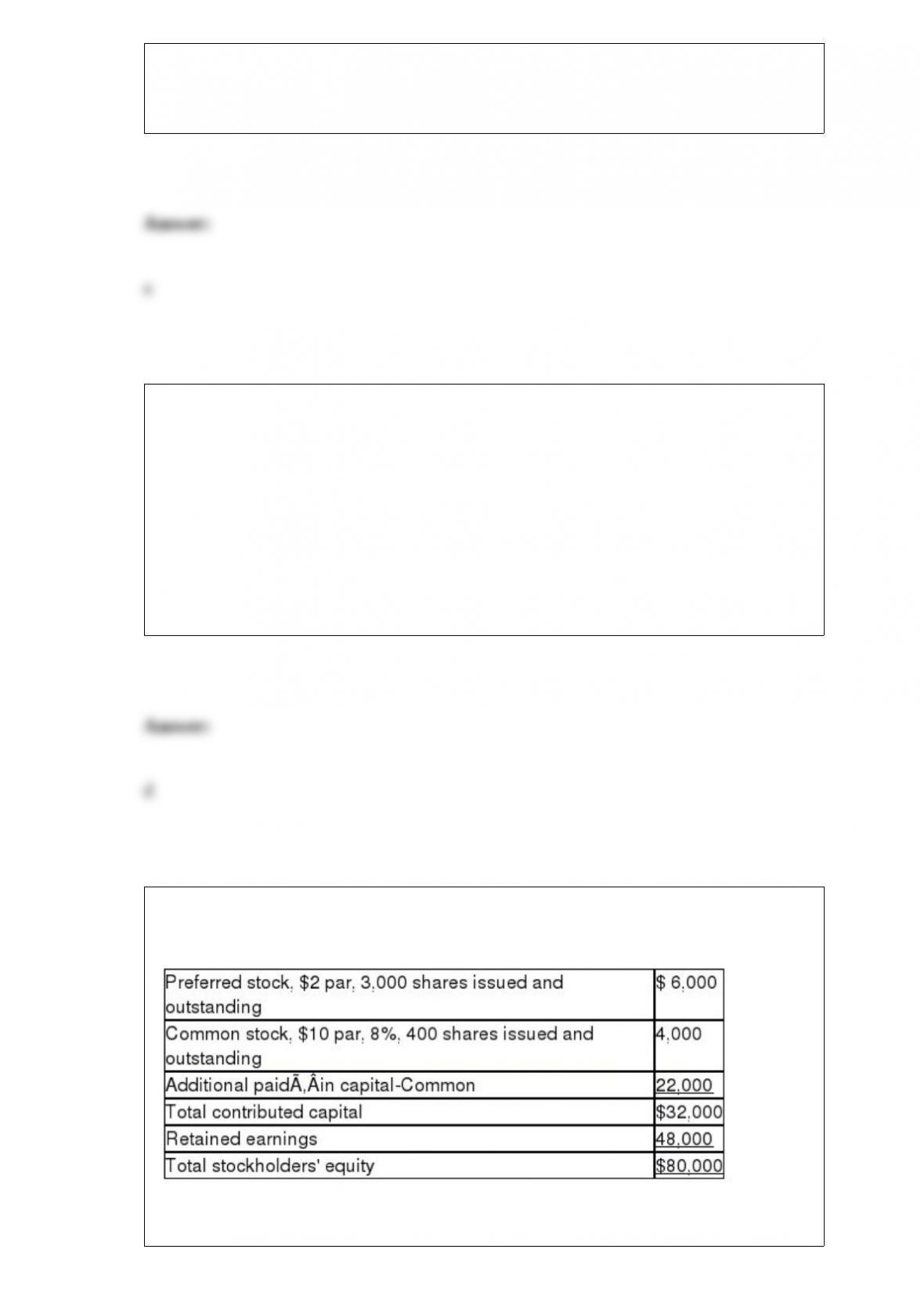

Lakeview Company reported the following amounts on its balance sheet at December 1,

2015:

The following transactions occurred during December: 1> Declared a 20% stock

dividend on comnon stock on December 3, when the stock was selling at $12 per share.

The stock dividend will be distributed on December 20, 2015.

2> Distributed the common stock dividend on December 20. 3> Approved a 2-for-1

stock split of the common stock on December 28, when the stock was selling for $20

per share. A) Show the effect of the transactions on the accounting equation.

B) Answer the following questions:

1> How many common shares are outstanding at December 31, 2015?

2> What effect will the stock split have on the stock’s market value?

Match the following business forms with their characteristics below.

a. Sole proprietorship

b. Partnership

c. Corporation

Usually owned and operated by the same person