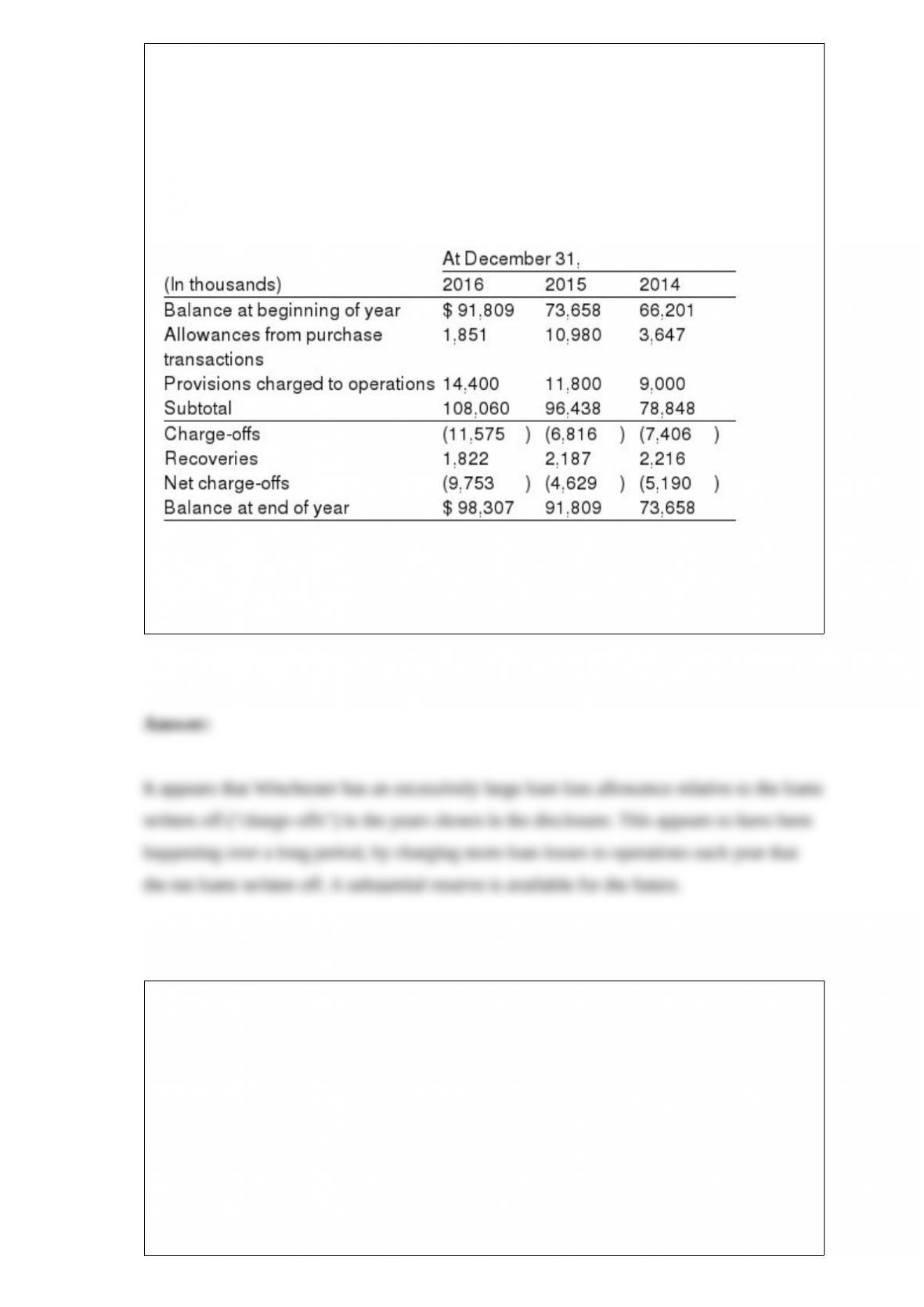

The following note disclosure is taken from the 2016 annual report to shareholders of

Winchester International Corporation. NOTE 5: ALLOWANCE FOR LOAN LOSSES

The allowance for loan loss is maintained at a level to absorb probable losses inherent

in the loan portfolio. This allowance is increased by provisions charged to operating

expense and by recoveries on loans previously charged off, and reduced by charge-offs

on loans. The following is a summary of the changes in the allowances for loan losses

for three years:

Winchester also reported (in thousands) in its comparative balance sheet that it held

Loans receivable, net, of $6,869,911 and $6,819,209 at December 31, 2016, and

December 31, 2015, respectively. Is there any evidence in Winchester’s disclosures

above that are consistent with earnings management?

On January 1, 2016, Field Company purchased 12% bonds, dated January 1, 2016, with

a face amount of $20 million. The bonds mature in 2025 (10 years). For bonds of

similar risk and maturity, the market yield is 10%. Interest is paid semiannually on June

30 and December 31.

Required:

1> Determine the price of the bonds at January 1, 2016.

2> Prepare the journal entry to record the bond purchase by Field on January 1, 2016.

3> Prepare the journal entry to record interest on June 30, 2016, using the straight-line

method.

4> Prepare the journal entry to record interest on December 31, 2016, using the

straight-line method.

Santa Cruz Oil is obligated to the State of Nevada to restore leased land to its original

condition after its oil drilling activities are over in four years. The cash flow

possibilities are probabilities for the restoration costs in four years are as follows:

The company’s credit-adjusted risk-free interest rate is 6%. Required:

Calculate the liability that Santa Cruz must record at the beginning of the project for the

restoration costs.

At the beginning of 2016, Scarlet Industries began providing a three-year warranty on

its products. The warranty program was expected to cost Scarlet 2% of net sales,

approximately equally over the three-year warranty period. Net sales made under

warranty in 2016 were $270 million. Thirteen percent of the units sold were returned in

2016 and repaired or replaced at a cost of $2 million. This amount was debited to

warranty expense as incurred.

Required:

Prepare the appropriate adjusting entry to adjust warranty expense on December 31,

2016. Show calculations.

The shareholders’ equity of Crystal Company includes the items shown below. The

board of directors of Crystal declared cash dividends of $3 million, $6 million, and $50

million in each of its first three years of operation: 2014, 2015, and 2016, respectively.

Common stock, $1 par, 50,000,000 shares outstanding

Preferred stock, 6%, $100 par, 1,000,000 shares outstanding

Required:

Determine the amount of dividends per share on preferred and common stock for each

of the three years. The preferred stock is cumulative and nonparticipating.

The components of postretirement benefit expense are similar to the components of

pension expense. How does the service cost component differ between the two

expenses?

Agasse Industries began construction of a new facility and took out a $1,500,000, 8%

construction loan on April 1, 2016. Agasse made payments to the general contractor of

$400,000 on April 1, $900,000 on August 31, and $500,000 on December 31.

Required:

Compute the amount of interest that Agasse would capitalize in 2016.

On September 1, 2016, Triton Entertainment borrowed $24 million cash to fund a new

Fun Park. The loan was made by Nevada Bank under a noncommitted short-term

financing arrangement. Triton issued a 9-month, 12% promissory note. Interest was

payable at maturity. Triton’s fiscal period is the calendar year. Required:

1> Prepare the journal entry for the issuance of the note by Triton.

2> Prepare the appropriate adjusting entry for the note by Triton on December 31, 2016.

3> Prepare the journal entry for the payment of the note at maturity.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

Listed below are 5 terms followed by a list of phrases that describe or characterize each

of the terms. Match each phrase with the number for the most correct term.