Companies within the same industry do not always use the same depreciation method,

but will use the same expected useful life for the same piece of equipment.

A retailer is a company that buys products from manufacturers and sells them to

wholesalers.

Because it is an expense account, the Sales Returns & Allowances account balance is

deducted from the Sales Revenue account balance in determining net sales.

The direct write-off method for uncollectible accounts is not allowed by either GAAP

or IFRS, but is required by the Internal Revenue Service (IRS) for tax purposes.

A healthy company typically shows positive cash flows in the financing activities

section of the statement of cash flows.

Assume the periodic inventory method is used. When LIFO is used, costs are assigned

to cost of goods sold using the most recent purchase at the time of the sale.

If inventory is sold with terms of FOB destination, the goods belong to the seller while

in transit.

When expenses exceed revenues in a period, stockholders’ equity will increase.

An adjusted trial balance is completed to check that debits still equal credits after the

income statement is prepared.

Building a new warehouse is an operating activity on the statement of cash flows.

When an asset is sold and its book value exceeds its selling price, net income will

increase.

Treasury stock purchases made with cash are classified as cash outflows from financing

activities on the statement of cash flows.

Interest revenue from notes receivable is typically reported on a multiple step income

statement as a part of Income from Operations.

If the Retained Earnings account is debited for $4,000 in the closing process, the

company had a net income of $4,000.

A company with a high inventory turnover requires a larger investment in inventory

than another company of similar sales with a lower inventory turnover.

Oats, Inc. has $14,000 in Cash, $37,000 in Accounts Receivable, $2,500 in Supplies,

$52,000 in Accounts Payable and $12,400 in Wages Payable. If Oats uses Cash to pay

off $8,000 of the Wages Payable, which of the following statements is correct?

A) The company ‘s current ratio will not change since current assets decreased by the

same amount that current liabilities increased.

B) The company will look more favorable to creditors.

C) The company has a greater ability to pay current liabilities.

D) The company ‘s current ratio will decrease.

Payroll taxes paid by employees include which of the following?

A) Federal income tax, federal unemployment tax, and Medicare

B) Social security, federal unemployment tax, and state unemployment tax

C) Social security, federal unemployment tax, and state unemployment tax

D) Federal income tax withheld, state income tax withheld, and Medicare

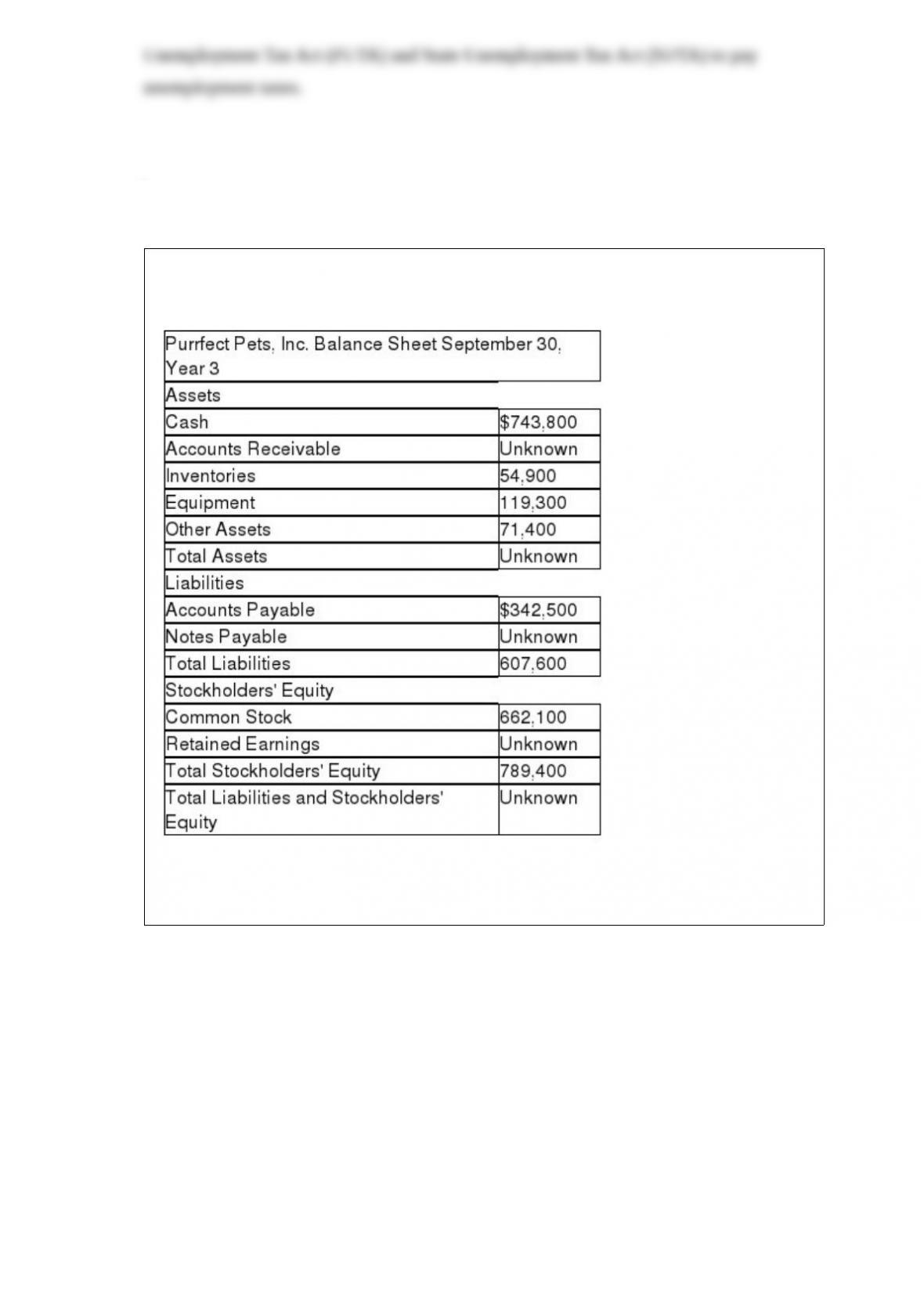

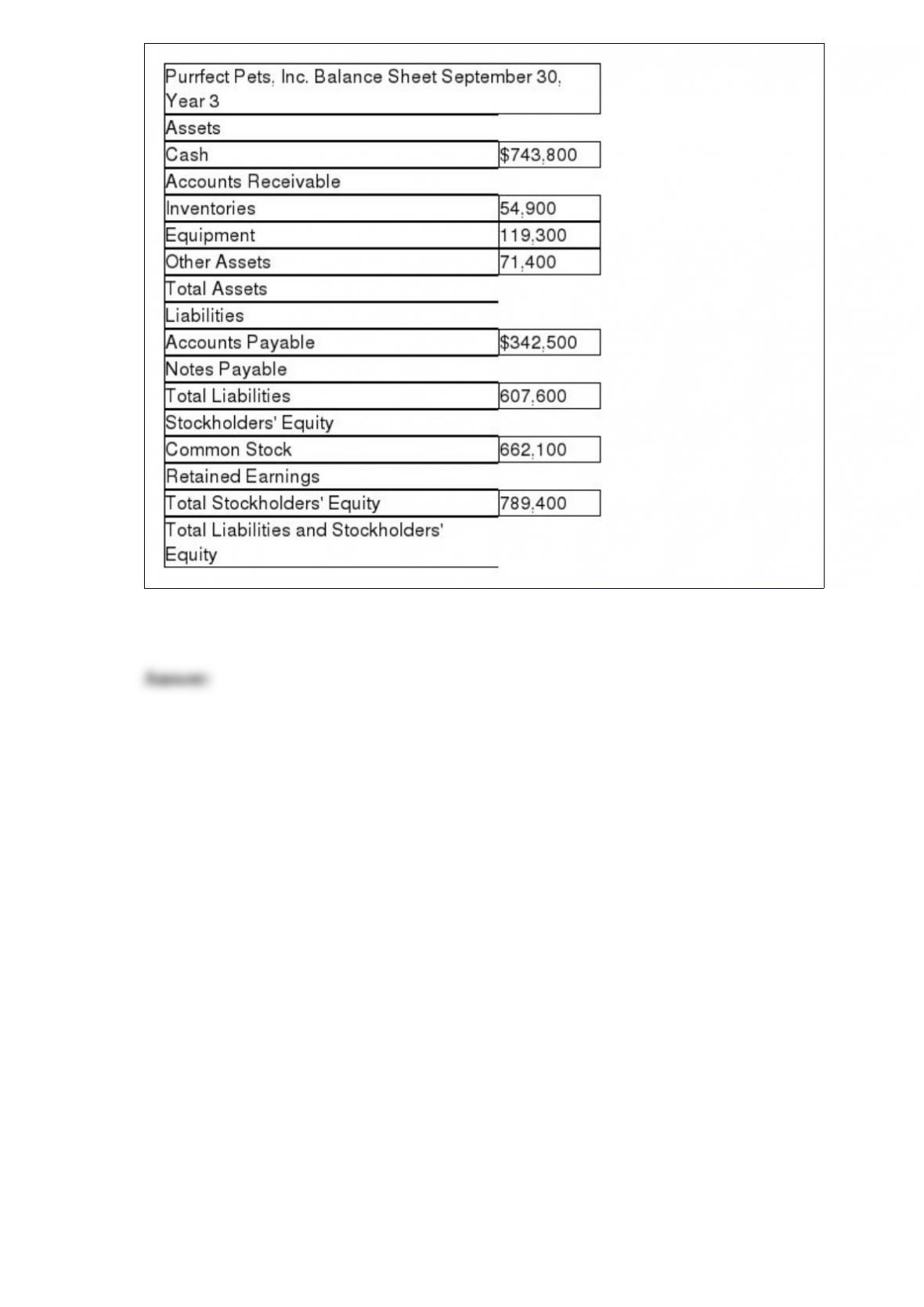

The following partially completed balance sheet is missing numerical data.

Required:

Fill in the missing amounts in the balance sheet.

An adjusted trial balance should be prepared immediately:

A) after the financial statements, but before closing.

B) before posting adjusting entries.

C) after posting adjusting entries.

D) after journalizing adjusting entries.

The receivables turnover ratio:

A) is calculated as the average number of days from the time a sale is made on account

to the time cash is collected.

B) is calculated as the average number of days from the time a sale is made on account

to the time payment is due.

C) measures how many times a year receivables go uncollected.

D) measures how many times, on average, the process of selling and collecting is

repeated during the period.

The effect of a stock dividend is to:

A) decrease total assets and stockholders’ equity.

B) change the composition of stockholders’ equity.

C) decrease total assets and total liabilities.

D) increase the market value per share of common shares.

Bobby Darling is the only employee of Atlantic Records, Inc. During the first week of

January, Darling earned $800 and had federal and state income tax withholdings of $40

and $15, respectively. FICA taxes are 7.65% on earnings up to $117,000. State and

federal unemployment taxes for the period are $50 and $8, respectively.

Use the information above to answer the following question. What would be the amount

of Darling’s payroll check for the first week of January?

A) $683.80

B) $741.80

C) $628.80

D) $625.80

Which of the following statements about the income statement of a company that was

formed 10 years ago is correct?

A) Reports a Net Loss for the year if expenses are more than revenues.

B) Reports the financial effects of activities that have occurred since the company’s

inception.

C) Reports the amount of the increase in stockholders’ equity this year as a result of the

company’s operations.

D) Reports Net Income which is not an account in the ledger.

The statement of cash flows for a company contained the following:

Cash flows from operating activities in the amount of $29,000

Cash flows from investing activities in the amount of$30,000

Cash flows from (used by) financing activities in the amount of ($45,000)

What was the change in cash for the period?

A) $14,000 increase

B) $15,000 increase

C) $14,000 decrease

D) $15,000 decrease

The requirement that transactions be recorded at their exchange price at the transaction

date is called the:

A) conservatism exception.

B) separate entity assumption.

C) cost principle.

D) monetary unit assumption.

A company reported a receivables turnover ratio of 8.0. Cost of goods sold was

$350,000 and net sales revenue was $480,000. The average net receivables must have

been

A) $45,000

B) $120,000

C) $60,000

D) $90,000

The Buddy Burger Corporation owes $1.5 million to the Texas Wholesale Meat

Company from whom Buddy Burger buys its burger meat. Which account would Buddy

Burger use to report the amount owed?

A) Cash

B) Accounts Payable

C) Notes Payable

D) Accounts Receivable

What are the differences between the periodic and the perpetual inventory systems?(Do

not address or list the actual journal entries made in each system.)

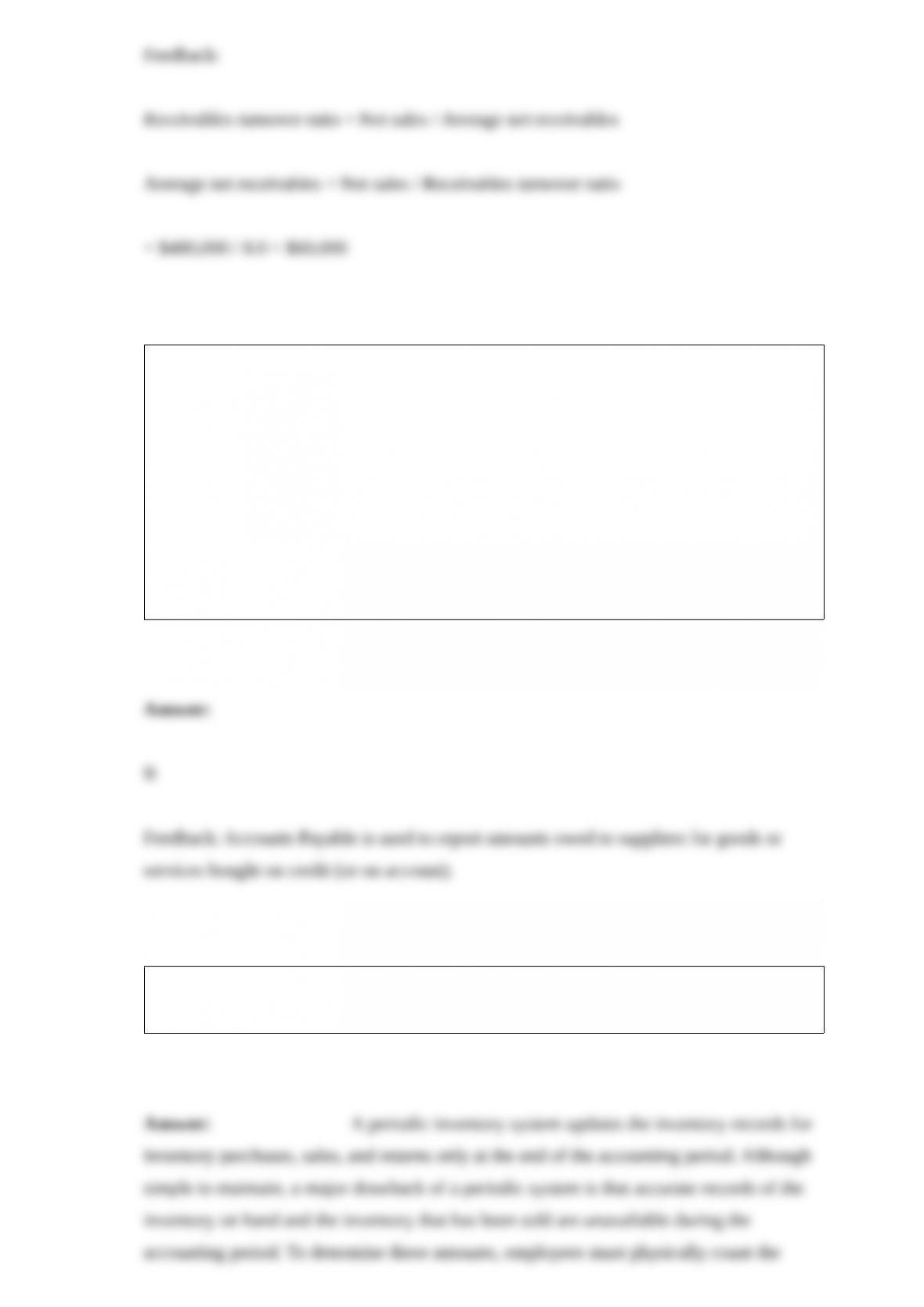

On January 1, 2016, a company issues 3-year bonds with a face value of $200,000 and a

stated interest rate of 8%. Because the market interest rate is higher than the stated

interest rate, the company receives $194,000 for the bond.

Required:

Fill in the table assuming the company uses the straight-line bond amortization.

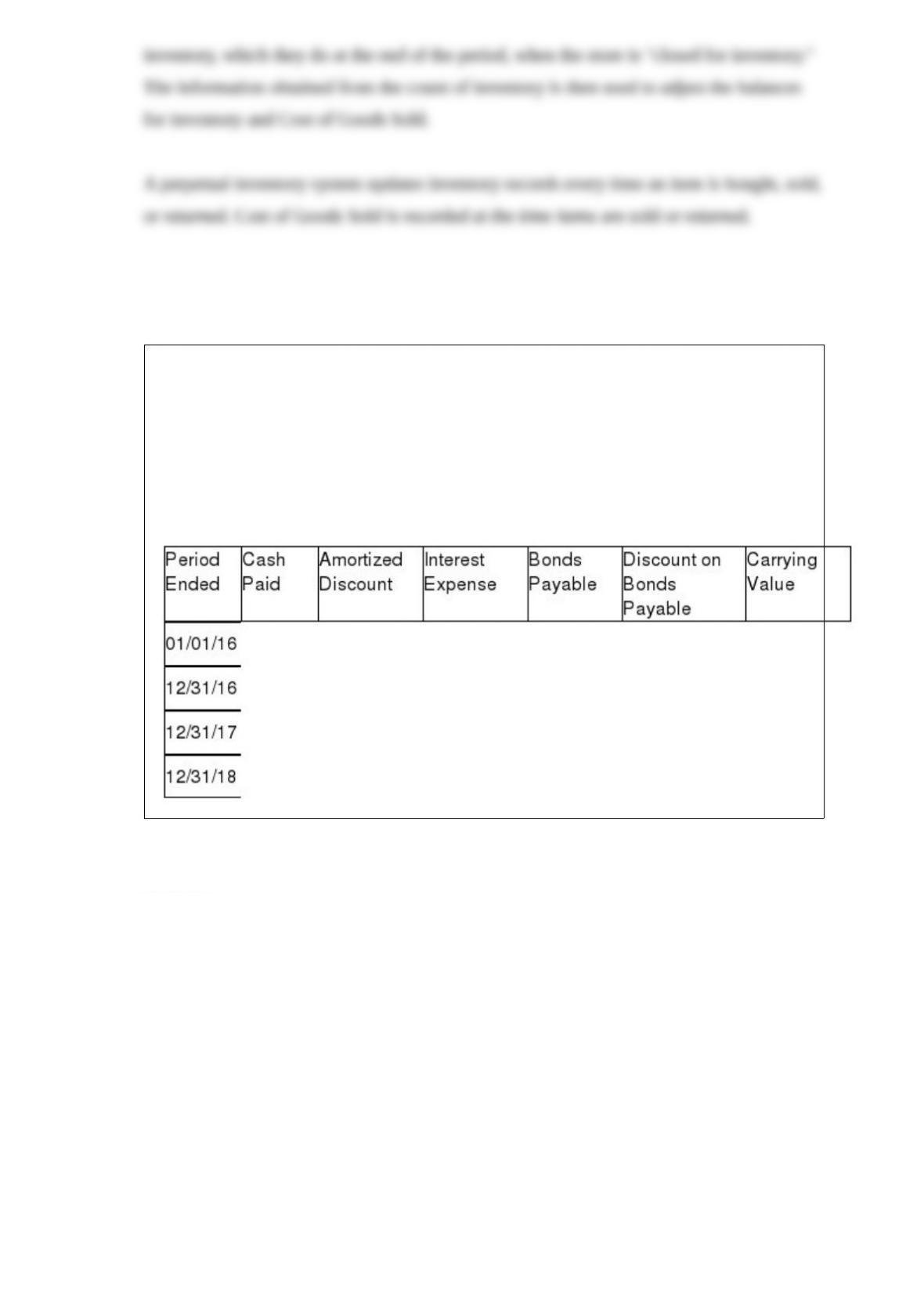

Darlington Inc. reported the following amounts on their financial statements for Year 1,

Year 2 and Year 3:

It was discovered early in Year 4 that the ending inventory at the end of Year 1 was

overstated by $6,000 and the ending inventory at the end of Year 2 was understated by

$2,500. The ending inventory at the end of Year 3 was correctly reported.

Required:

Ignoring income taxes, determine the correct amounts of cost of goods sold and net

income for each of the three years and total assets at the end of each the three years and

complete the table below. Show your work.

Supporting calculations:

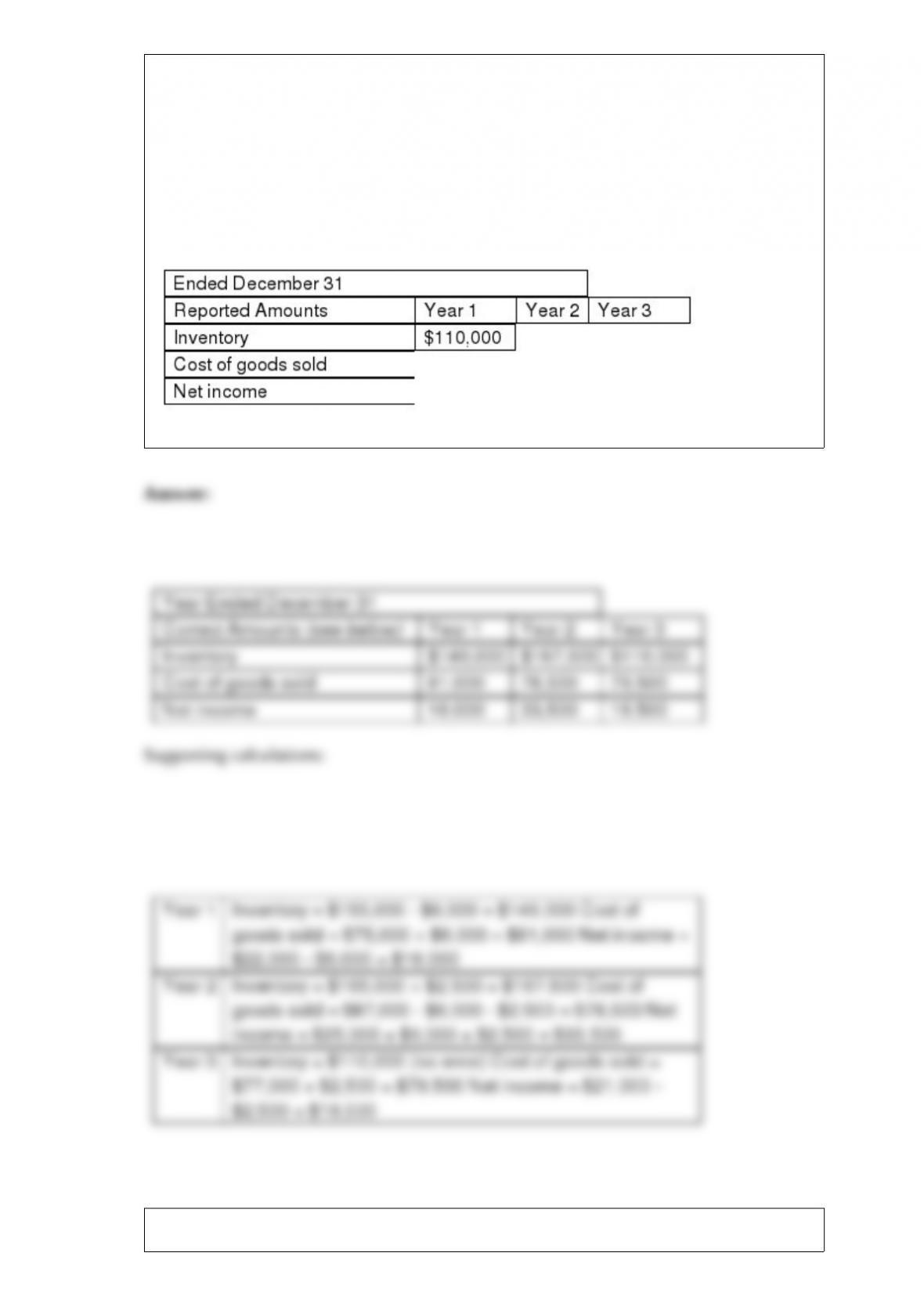

On January 1, 2016, a company issues 3-year bonds with a face value of $50,000 and a

stated interest rate of 7%. Because the market interest rate is 5%, the company receives

$52,723 for the bonds.

Required:

Fill in the table assuming the company uses effective-interest bond amortization.

The following information is available for the Tierney Company for the month of

November.

On November 30, after all transactions have been recorded, the balance in the

company’s Cash account has a balance of $27,202.

The company’s bank statement shows a balance on November 30 of $29,279.

Outstanding checks at November 30 include check #3030 in the amount of $1,525 and

check #3556 in the amount of $1,459.

Included with the bank statement was a credit memo in the amount of $770 for an EFT

in payment of a customer ‘s account.

The bank deducted $67 for an NSF check from a customer deposited on November 22.

A deposit placed in the bank’s night depository on November 30 totaled $1,675 and did

not appear on the bank statement.

Examination of the checks on the bank statement with the entries in the accounting

records reveals that check #3445 for the payment of an account payable was correctly

written for $2,450, but was recorded in the accounting records as $2,540.

Included with the bank statement was a debit memorandum in the amount of $25 for

bank service charges.

Required:

Prepare the journal entries for the items that would appear on the company ‘s bank

reconciliation as of November 30. (Do not prepare the bank reconciliation.)

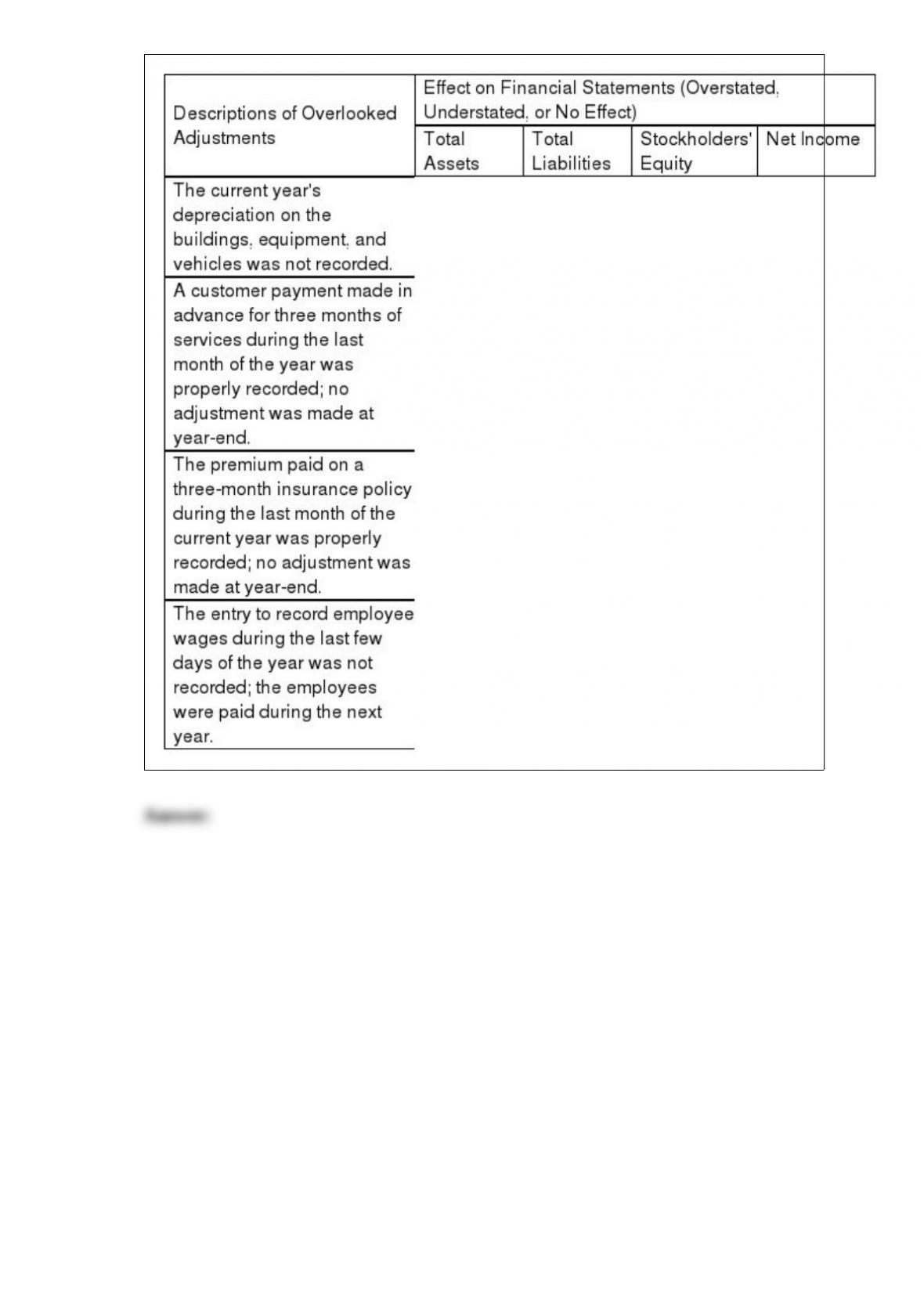

Assume that the accountant neglected to analyze the company’s accounts and did not

prepare any adjusting entries at the end of the year. The adjusting entries that should

have been made are described in the table below.

Required:

For each overlooked adjusting entry, indicate how each error impacted the amounts of

total assets, total liabilities, and total stockholders’ equity that were reported on the

balance sheet and the amount of net income reported on the income statement.

On January 1, 2016, a company issues 3-year bonds with a face value of $200,000 and a

stated interest rate of 8%. Because the market interest rate is lower than the stated

interest rate, the company receives $209,000 for the bond.

Required:

Fill in the table assuming the company uses the straight-line bond amortization.