1) Which of the following phrases is frequently used to refer to estate or trust

accounting?

A) Non-profit accounting

B) Testamentary accounting

C) Fiduciary accounting

D) All of the above phrases are used to refer to estate or trust accounting.

2) With respect to goodwill, an impairment

A) will be amortized over the remaining useful life

B) is a two-step process which analyzes each business reporting unit of the entity

C) is a one-step process considering the entire firm

D) occurs when asset values are adjusted to fair value in a purchase

3) Bonds with relatively low risk of default are called ________ securities and have a

rating of Baa (or BBB) and above; bonds with ratings below Baa (or BBB) have a

higher default risk and are called ________

A) investment grade; lower grade

B) investment grade; junk bonds

C) high quality; lower grade

D) high quality; junk bonds

4) On June 1, 2011, Puell Company acquired 100% of the stock of Sorrell Inc. On this

date, Puell had Retained Earnings of $100,000 and Sorrell had Retained Earnings of

$50,000. On December 31, 2011, Puell had Retained Earnings of $120,000 and Sorrell

had Retained Earnings of $60,000. The amount of Retained Earnings that appeared in

the December 31, 2011 consolidated balance sheet was

A) $120,000

B) $130,000

C) $170,000

D) $180,000

5) A decrease in the riskiness of corporate bonds will ________ the price of corporate

bonds and ________ the price of Treasury bonds, everything else held constant

A) increase; increase

B) reduce; reduce

C) reduce; increase

D) increase; reduce

6) Pinata Corporation acquired an 80% interest in Smackem Inc. for $130,000 on

January 1, 2011, when Smackem had Capital Stock of $125,000 and Retained Earnings

of $25,000. Assume the fair value and book value of Smackem’s net assets were equal

on January 1, 2011 . Pinata’s separate income statement and a consolidated income

statement for Pinata and Subsidiary as of December 31, 2011, are shown below.

Pinata Consolidated

Sales revenue$145,850 $234,750

Income from Smackem 12,600

Cost of sales(60,000)(100,000)

Other expenses(20,000)(50,000)

Noncontrolling

interest share (3,150)

Net income$ 78,450 $ 81,600

Smackem’s separate income statement must have reported net income of

A) $13,750

B) $14,750

C) $15,750

D) $15,250

7) The General Fund transfers $50,000 cash to the Debt Service Fund to meet annual

interest payments. What entry did the Debt Service Fund prepare?

A) Debit Cash $50,000, Credit Revenue $50,000

B) Debit Cash $50,000, Credit Other Financing Sources-Transfer from General Fund

$50,000

C) Debit Encumbrance $50,000, Credit Due to General Fund $50,000

D) Debit Appropriation $50,000, Credit Reserve for Encumbrance $50,000

8) Because a fund is an accounting entity, each fund has

I.its own accounting equation.

II.its own journals, ledgers, and other accounting records.

III.its own separate auditor.

A) I only

B) II only

C) I and II

D) I, II and III

9) Government-wide financial statements include a

A) balance sheet, an income statement, and a statement of cash flows

B) statement of net assets, a statement of activities, and a statement of cash flows

C) statement of net assets and a statement of activities

D) statement of activities and a statement of cash flows

10) On January 1, 2011, Pansy Company acquired a 10% interest in Sunflower

Corporation for $80,000 when Sunflower’s stockholders’ equity consisted of $400,000

capital stock and $100,000 retained earnings. Book values of Sunflower’s net assets

equaled their fair values on this date. Sunflower’s net income and dividends for 2011

through 2013 were as follows:

2011 2012 2013

Net income$ 8,000$ 10,000$15,000

Dividends paid5,0005,0005,000

Assume that Pansy Incorporated used the cost method of accounting for its investment

in Sunflower. The balance in the Investment in Sunflower account at December 31,

2013 was

A) $76,700

B) $80,000

C) $83,300

D) $95,000

11) Alfred and Barne share profits and losses in a ratio of 2:3, respectively, after salary

allowances, interest allowances and bonus allocations. Alfred and Barne receive salary

allowances of $30,000 and $60,000, respectively, and both partners receive 10%

interest based upon the balance in their capital accounts on January 1 . Partners’

drawings are not used in determining the average capital balances. Total net income for

2011 is $180,000. If net income after deducting the interest and salary allocations is

more than $60,000, Barne receives a bonus of 5% of the original amount of net income.

AlfredBarne

January 1 capital balances$600,000$900,000

Yearly drawings ($3,000 a month)36,00036,000

What is the total amount for the allocation of interest, salary, and bonus, and how much

over-allocation is present?

A) $180,000 and $0

B) $240,000 and $60,000

C) $249,000 and $0

D) $249,000 and $69,000

12) Pelga Company routinely receives goods from its 80%-owned subsidiary, Swede

Corporation. In 2011, Swede sold merchandise that cost $80,000 to Pelga for $100,000.

Half of this merchandise remained in Pelga’s December 31, 2011 inventory. This

inventory was sold in 2012 . During 2012, Swede sold merchandise that cost $160,000

to Pelga for $200,000. $62,500 of the 2012 merchandise inventory remained in Pelga’s

December 31, 2012 inventory. Selected income statement information for the two

affiliates for the year 2012 was as follows:

PelgaSwede

Sales Revenue$500,000$400,000

Cost of Goods Sold400,000320,000

Gross profit$100,000$80,000

Consolidated cost of goods sold for Pelga and Subsidiary for 2012 were

A) $512,000

B) $526,000

C) $522,500

D) $528,000

13) Oscar Lloyd is serving as the executor for the estate of Dixie Cooper, who passed

away on January 28, 2011, at the age of 98 . Dixie’s estate consisted of Treasury bonds

with a maturity value and fair market value of $1,400,000, $4,000 in her checking

account, and $50,000 in a Certificate of Deposit with First State Bank of Springfield.

Total accrued interest at the time of death was $44,000, made up of $2,000 from the CD

and $42,000 from the bonds.

Dixie left a valid will, which provided that most of her estate would be inherited by her

two nephews, Jimmy Johns and Joey Johns. In addition, Dixie provided that $200,000

be transferred to a trust account for her faithful cats, Petra and Hobbes. Income from the

trust would be used to care for Hobbes and Petra. Upon their passing, the remaining

funds would then transfer to Operation Kindness, an organization that cares for cats and

dogs.

Mr. Lloyd will also serve as the fiduciary for the trust. He has determined that no state

or federal inheritance taxes are due. The limited estate income is also free from any

federal or state income tax. The following transactions occurred during February.

1>On February 3, Oscar sold the treasury bonds for $1,460,000. $1,400,000 was for the

fair market value of the bonds, $42,000 was for interest accrued to the time of Dixie’s

death, and the remaining $18,000 was for accrued interest since Dixie’s death. Estate

income will be used to pay final medical expenses, and if anything is left, funeral

expenses.

2>On February 11, Oscar issued a check to pay Dixie’s final medical expenses of

$11,900.

3>On February 15, Oscar received a check in the amount of $52,000 from First State

Bank of Springfield. It is the maturity value and interest from a certificate of deposit in

the amount of $50,000. The CD matured on January 22, 2011 .

4>In Dixie’s will, she wanted to give $150,000 to the American Humane Society. After

examining the assets, Oscar determined that the estate’s assets will adequately cover all

expenses and specific devises, so on February 3, he issued a check to the organization

for $150,000.

5>On February 18, Oscar transferred $200,000 to a trust account at First State Bank to

fund the trust, to care for the cats.

6>On February 25, Oscar issued a check to pay Dixie’s funeral expenses of $9,800.

7>On February 26, Oscar paid himself the $4,000 executor’s fee specified in Dixie’s

will.

Assume that on February 28, 2011, Oscar finalized the estate and transferred the

balance of the estate assets to Dixie’s nephews, Jimmy Johns and Joey Johns. Each

received one-half of the residual estate.

Required:

1>Prepare the closing entry on February 28, 2011 .

2>Prepare the charge-discharge statement for the estate of Dixie Cooper for the period

January 28 through February 28, 2011 .

14) What is the dollar amount of the federal lifetime maximum gift tax exclusion?

A) $24,000

B) $600,000

C) $1,000,000

D) $2,000,000

15) Which of the following statements is not true with respect to the statement of cash

flows for a consolidated entity?

A) The statement may be prepared using either the direct or the indirect method

B) Noncontrolling interest share will be added back to cash flows from operating

activities under the indirect method

C) Payment of dividends from the subsidiary to the parent will appear on the statement

of cash flows as a financing activity

D) If the subsidiary does not use the same method (direct or indirect) as the parent, they

must convert their separate statement of cash flows first to the same method that the

parent uses, and then the two statements are consolidated

16) If 1-year interest rates for the next three years are expected to be 4, 2, and 3 percent,

and the 3-year term premium is 1 percent, than the 3-year bond rate will be

A) 1 percent

B) 2 percent

C) 3 percent

D) 4 percent

17) In a schedule of assumed loss absorptions

A) the partner with lowest loss absorption is eliminated last

B) it is necessary to have a cash distribution plan first

C) the least vulnerable partner is eliminated first

D) the most vulnerable partner is eliminated first

18) In reference to the FASB disclosure requirements about a business combination in

the period in which the combination occurs, which of the following is correct?

A) Firms are not required to disclose the name of the acquired company

B) Firms are not required to disclose the business purpose for a combination

C) Firms are required to disclose the nature, terms and fair value of consideration

transferred in a business combination

D) All of the above are correct

19) Which partner is considered the most vulnerable as a result of a computation of

vulnerability rankings?

A) The partner who has the lowest loss absorption potential

B) The partner who has the highest loss absorption potential

C) The partner with the highest capital account balance

D) The partner with the lowest capital account balance

20) On December 31, 2011, Pinne Corporation sold equipment with a three-year

remaining useful life and a book value of $21,000 to its 70%-owned subsidiary, Sull

Company, for a price of $27,000. Pinne bought the equipment four years ago for

$49,000. The salvage value is zero. Straight-line depreciation is used by both

companies.

After eliminating/adjusting entries are prepared, what was the intercompany sale impact

on the consolidated financial statements for the year ended December 31, 2011?

A) Consolidated Net IncomeConsolidated Net Assets

No effectNo effect

B) Consolidated Net IncomeConsolidated Net Asset

No effectIncreased

C) Consolidated Net IncomeConsolidated Net Asset

DecreasedDecreased

D) Consolidated Net IncomeConsolidated Net Asset

DecreasedNo effect

21) On January 1, 2011, Pailor Inc. purchased 40% of the outstanding stock of Saska

Company for $300,000. At that time, Saska’s stockholders’ equity consisted of $270,000

common stock and $330,000 of retained earnings. Saska Corporation reported net

income of $360,000 for 2011 . The allocation of the $60,000 excess of cost over book

value acquired is shown below, along with information relating to the useful lives of the

items:

Overvalued receivables (collected in 2011)$(5,000)

Undervalued inventories (sold in 2011)16,000

Undervalued building (4 years’ useful life remaining at January 1, 2011)24,000

Undervalued land8,000

Unrecorded patent (6 years’ economic life remaining at January 1, 2011)18,000

Undervalued accounts payable (paid in 2011) (4,000)

Total of excess allocated to identifiable assets and liabilities57,000

Goodwill 3,000

Excess cost over book value acquired $60,000

Required:

Determine Pailor’s investment income from Saska for 2011 .

22) At the end of 2010, the partnership of Piatta, Ragoo, and Sauss was dissolved. By

February 1, 2011, all assets had been converted into cash and all partnership liabilities

were paid. The partnership balance sheet on February 1, 2011 (with partner residual

profit and loss sharing percentages) was as follows:

Cash$220,000Piatta,capital (20%)$20,000

Ragoo, capital (40%)(180,000)

Sauss, capital (40%)380,000

Total assets$220,000Total equity$220,000

The value of partners’ personal assets and liabilities on February 1, 2011 were as

follows:

PiattaRagooSauss

Personal assets$86,000$310,000$210,000

Personal liabilities79,000250,000250,000

Required:

Prepare the final statement of partnership liquidation.

23) Several years ago, Peacock International purchased 80% of the outstanding stock of

Strutt Incorporated, at a time when Strutt’s book values were equal to its fair values. On

January 1, 2009, Strutt purchased a truck for $160,000 which had no salvage value with

a useful life of 8 years, depreciated on a straight-line basis. On January 1, 2012, Strutt

sold the truck to Peacock Corporation for $56,000. The equipment was estimated to

have a five-year remaining life on this date, with no salvage value. All affiliates use the

straight-line depreciation method.

Required:

Prepare the consolidation entries required for Peacock and subsidiary at:

1>December 31, 2012

2>December 31, 2013

3>December 31, 2014

4>December 31, 2015

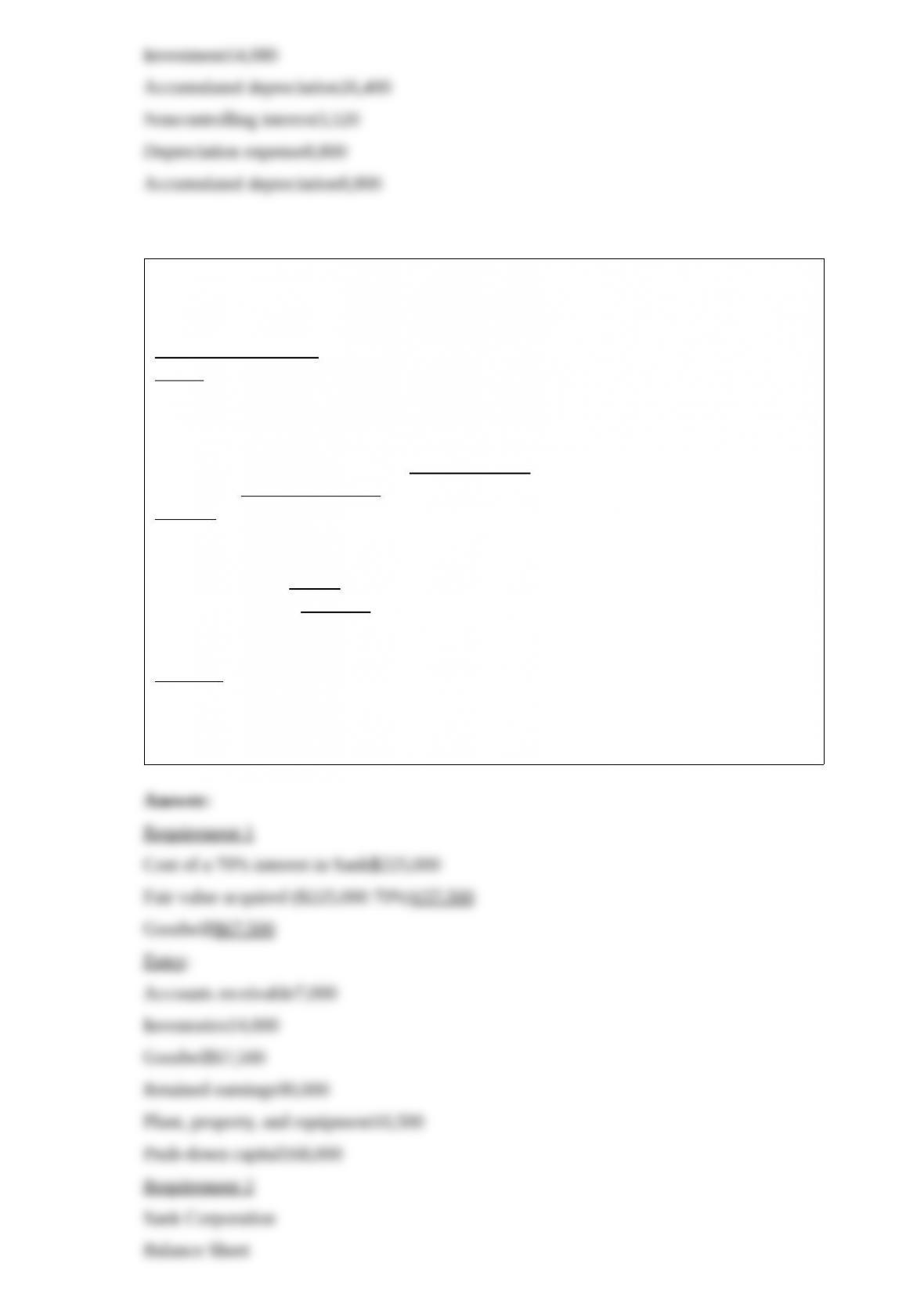

24) Pascal Corporation paid $225,000 for a 70% interest in Sank Corporation on

January 1, 2011 . On that date, Sank’s balance sheet accounts, at book value and fair

value, were as follows:

Book ValueFair Value

Assets

Cash$25,000$25,000

Accounts receivable-net45,00055,000

Inventories40,00060,000

Plant, property and equipment-net140,000125,000

Total assets$250,000$265,000

Equities

Accounts payable$40,000$40,000

Common stock120,000

Retained earnings90,000

Total liab. & equity$250,000

Both companies use the parent company theory. Push-down accounting is used for the

acquisition.

Required:

1> Prepare the journal entry on January 1, 2011 on Sank Corporation’s books.

2> Prepare a balance sheet for Sank Corporation immediately after the acquisition on

January 1, 2011 .

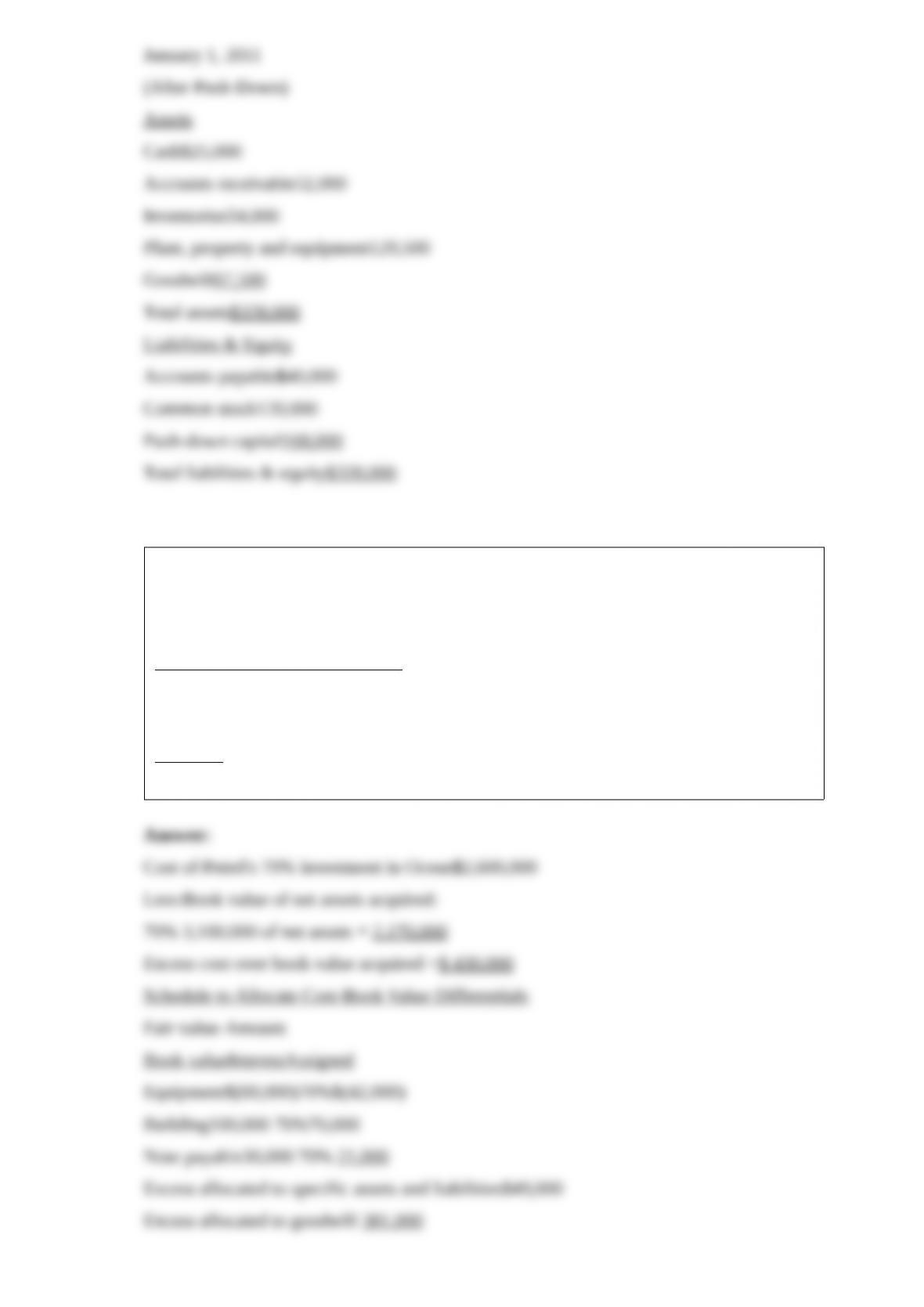

25) On January 1, 2010, Petrel, Inc. purchased 70% of the outstanding voting common

stock of Ocean, Inc., for $2,600,000. The book value of Ocean’s net equity on that date

was $3,100,000. Book values were equal to fair values except as follows:

BookFair

Assets & LiabilitiesValuesValues

Equipment$ 250,000$ 190,000

Building600,000700,000

Note payable270,000240,000

Required:

Prepare a schedule to allocate any excess purchase cost to specific assets and liabilities.

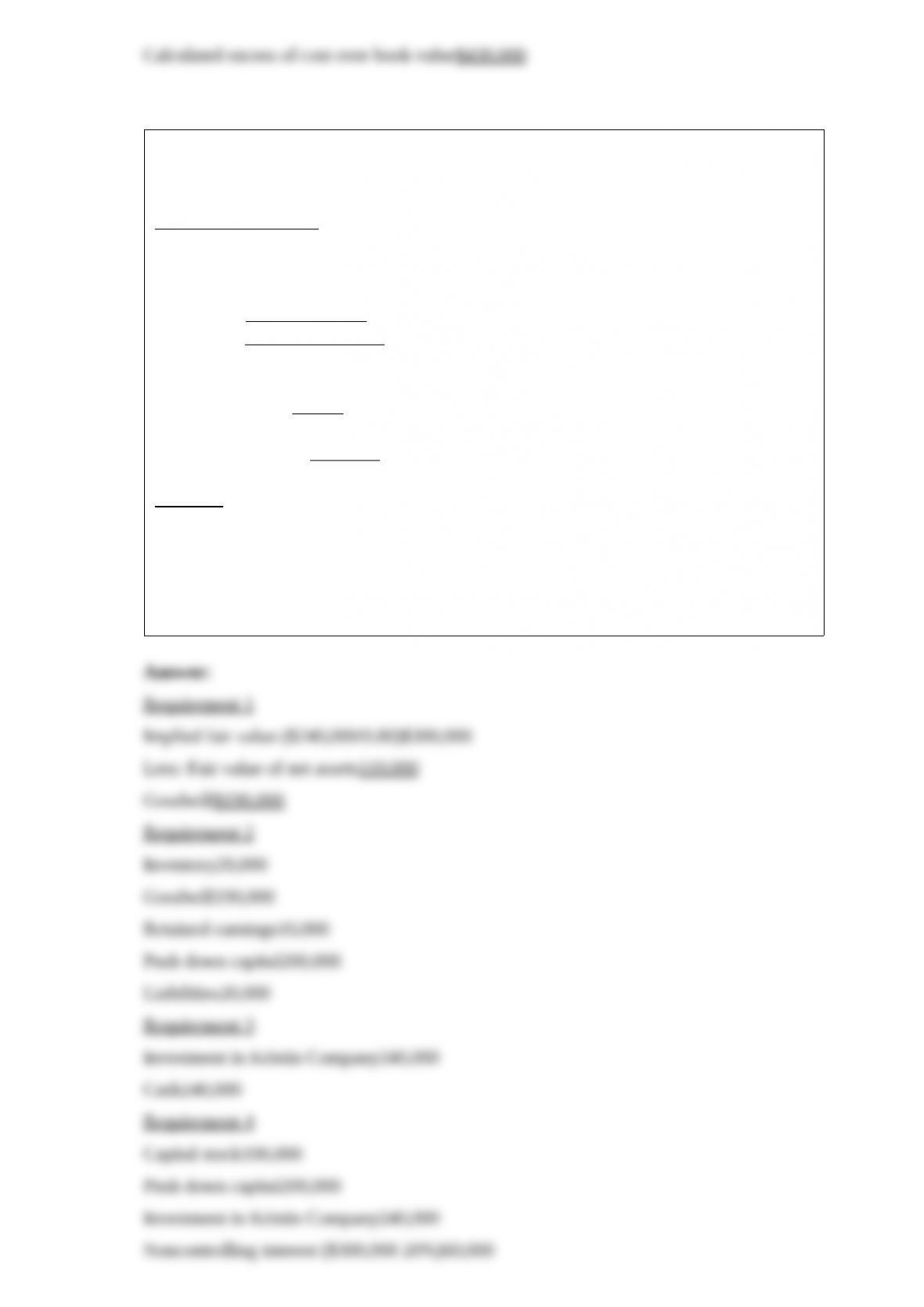

26) On January 1, 2011, Brody Company acquired an 80% interest in Kristin Company

for $240,000 cash. On January 1, 2011, Kristin Company had the following assets and

liabilities:

Book ValueFair Value

Cash$10,000$10,000

Accounts Receivable50,00050,000

Inventory50,00070,000

Plant Assets100,000100,000

Total Assets$210,000$230,000

Liabilities$100,000$120,000

Capital Stock100,000

Retained Earnings10,000

Total Liabilities &

Stockholders’ Equity$210,000

Push-down accounting is used for the acquisition. Both companies use the entity theory.

Required:

1> What is the goodwill associated with Kristin Company on January 1, 2011?

2> Prepare the journal entry(ies) on Kristin’s books on January 1, 2011 .

3> Prepare the journal entry(ies) on Brody’s books on January 1, 2011 .

4> Prepare the elimination entry(ies) on the consolidating working papers on January 1,

2011 .

27) Carousel Clothes is a voluntary health and welfare organization that provides

gently-used second-hand clothes to those in need. They had the following transactions

in 2011 .

1>Cash gifts were received in the amount of $60,000, of which $13,000 had been

pledged in the prior year.

2>Pledges made in the current year but not yet fulfilled amounted to $39,000. Ten

percent of the pledges typically prove to be uncollectible. Pledges are made for 2011 .

3>An office supply company donates office furniture to the VHWO. The fair value of

the furniture is $40,000. No restrictions were placed on the donation.

4>The following expenses were incurred and paid: director’s salary, $15,000; facility

rental, $18,000; cleaning and repair costs for clothes, $29,000; and purchase of supplies

consumed in tagging and distribution of clothes, $5,000. The director’s salary is

categorized as Support Services and the rest of the costs are Program Services.

5>Restricted pledges were received during the year for $450,000. The pledges are

restricted for the construction of a new facility.

Required:

Prepare the journal entries for Carousel for 2011 .

28) On December 31, 2011, Maria Corporation has the following stockholders’ equity:

Common stock, $10 par$100,000

Additional paid-in capital20,000

Retained earnings80,000

Total stockholders’ equity$200,000

On January 1, 2012, Maria Corporation declared and issued a 10% stock dividend when

the market price per share was $50.

On January 2, 2012, James Corporation purchased an 80% interest in Maria

Corporation for $160,000 from the open market. On January 2, 2012, the fair value of

Maria’s individual assets and liabilities was equal to book value.

Required:

1> Prepare the journal entry(ies) for Maria Corporation on January 1, 2012 .

2> Prepare the journal entry(ies) for James Corporation on January 2, 2012 .

3> Prepare the elimination entry(ies) for consolidating work papers on January 2, 2012 .

4> Prepare the elimination entry(ies) for consolidating work papers on January 2, 2012

if the 10% stock dividend is not declared and issued on January 1, 2012 .