As of December 31, 2015, Gill Co. reported accounts receivable of $216,000 and an

allowance for uncollectible accounts of $8,400. During 2016, accounts receivable

increased by $22,000, and $7,800 of bad debts were written off. An analysis of Gill

Co.’s December 31, 2016, accounts receivable suggests that the allowance for

uncollectible accounts should be 3% of accounts receivable. Bad debt expense for 2016

would be:

a. $6,540.

b. $7,800.

c. $7,140.

d. None of these answer choices are correct.

Using straight-line depreciation for financial reporting purposes and MACRS for tax

purposes in the first year of an asset’s life creates a:

a. Future deductible amount.

b. Permanent difference not requiring inter-period tax allocation.

c. Deferred tax asset.

d. Deferred tax liability.

Red Corp. constructed a machine at a total cost of $70 million. Construction was

completed at the end of 2012 and the machine was placed in service at the beginning of

2013. The machine was being depreciated over a 10-year life using the straight-line

method. The residual value is expected to be $4 million. At the beginning of 2016, Red

decided to change to the sum-of-the-years’-digits method. Ignoring income taxes, what

will be Red’s depreciation expense for 2016?

a. $ 4.8 million.

b. $ 5.4 million.

c. $ 6.6 million.

d. $11.55 million.

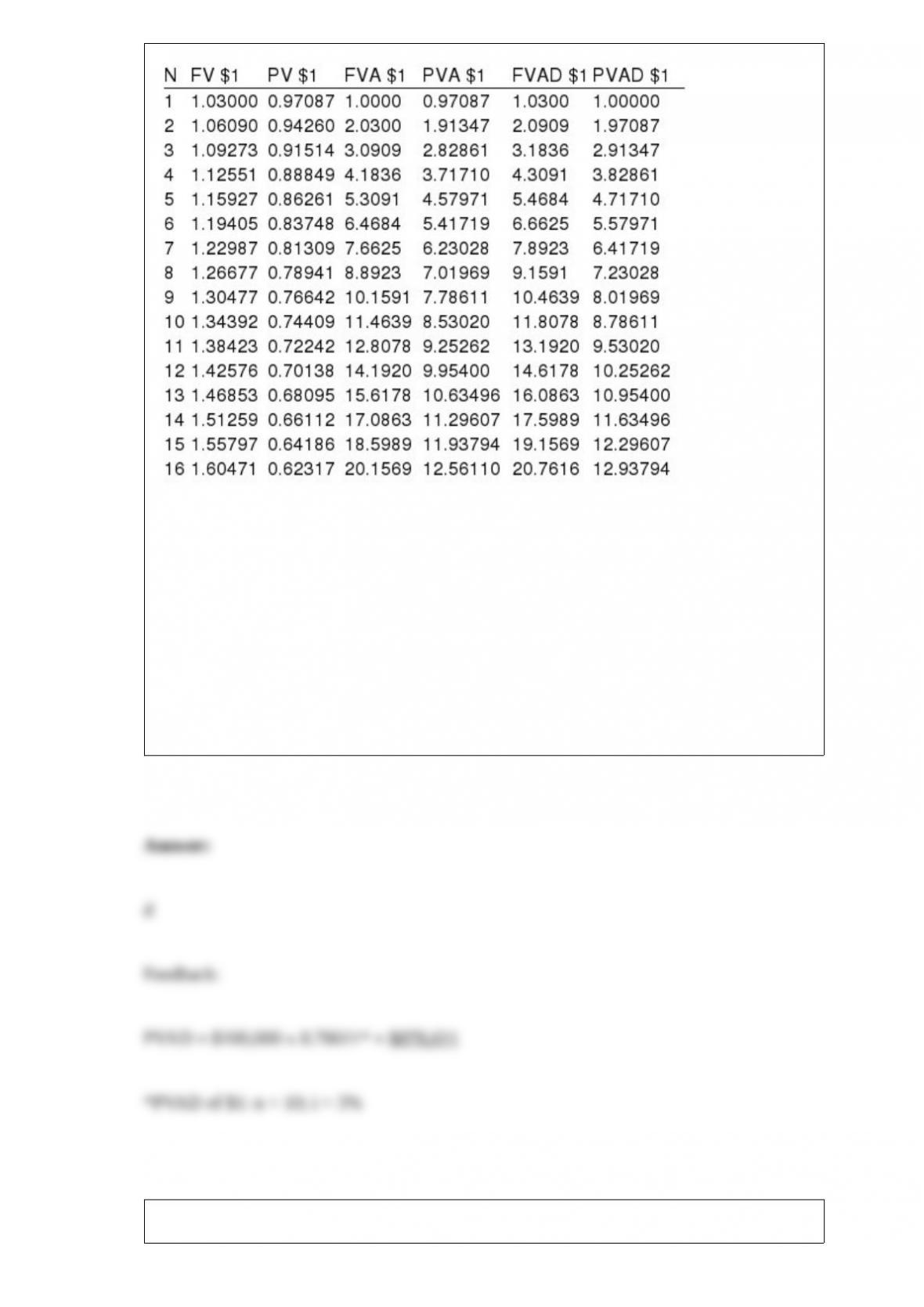

Present and future value tables of $1 at 3% are presented below:

Shelley wants to cash in her winning lottery ticket. She can either receive ten $100,000

semiannual payments starting today, or she can receive a lump-sum payment now based

on a 6% annual interest rate. What is the equivalent lump-sum payment?

a. $853,020.

b. $801,969.

c. $744,090.

d. $878,611.

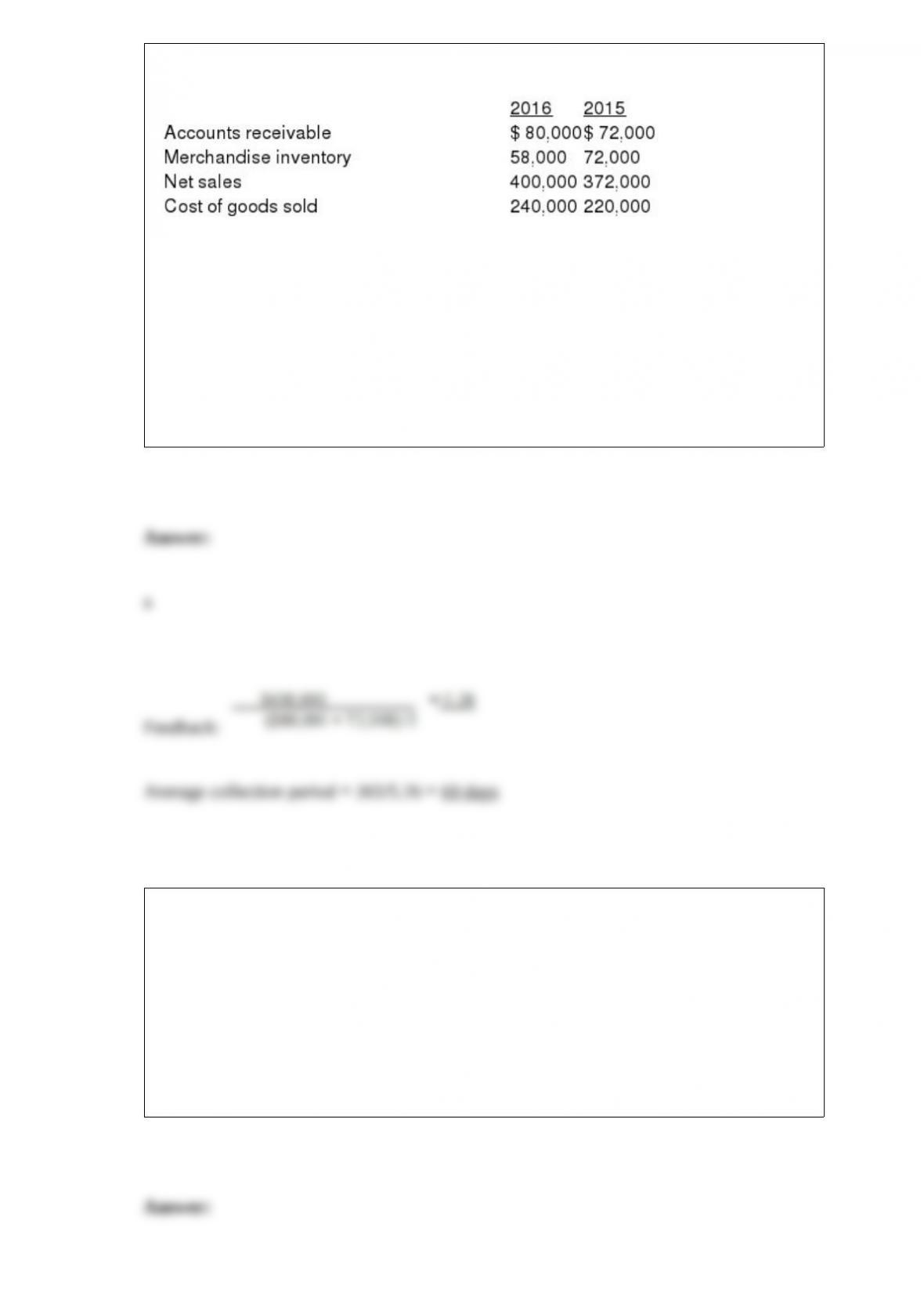

Excerpts from Huckabee Company’s December 31, 2016 and 2015, financial statements

are presented below:

Huckabee’s 2016 average collection period (rounded) is:

a. 69 days.

b. 116 days.

c. 111 days.

d. 73 days.

Of the following, which is not an investing activity?

a. Purchasing a new computer.

b. Buying treasury stock.

c. Selling a parcel of land.

d. Purchasing short-term investments.

Titan Corporation has a defined benefit pension plan. One of its employees has vested

benefits under the plan, which will pay her $30,000 annually for life starting with the

first $30,000 payment on the day she retires at the age of 65. The employee has just

reached the age of 45. Titan consulted standard mortality tables to come up with a life

expectancy of 80 for this employee. The implicit interest rate under the plan is 9%.

Required:

a. What will be the present value of the pension obligation at the time of the employee’s

retirement?

b. What is the present value of the pension obligation at the current time?

Since the lease payments under a lease agreement are normally paid at the beginning of

each period, the appropriate compound interest table to be used to determine the

amount at which the leased asset should be recorded is the:

a. Ordinary annuity table.

b. Present value of $1 table.

c. Present value of an annuity due table.

d. Future value of an annuity due table.

Which of the following would be an example of an investing activity on a statement of

cash flows?

a. Sale of equipment.

b. Issuance of long-term bonds.

c. Receipt of investment revenue.

d. Conversion of a cash equivalent into cash.

Under the retail method, in determining the cost-to-retail percentage for the current

year:

a. Net markups are included.

b. Net markdowns are excluded.

c. Net sales are included.

d. All of these answer choices are correct.

A purchase of equipment for cash is:

a. Reported as an operating activity in the statement of cash flows.

b. Reported as an investing activity in the statement of cash flows.

c. Reported as a financing activity in the statement of cash flows.

d. None of these answer choices is correct.

On June 1st, Lucy & Bros received an order for 500 cupcakes. Lucy delivered the

cupcakes to the client on June 25th. A $50 deposit was received on June 5th and the

remaining $450 was paid on June 30th. Lucy likely would recognize revenue on

a. June 1st

b. June 5th

c. June 25th

d. June 30th

Amortizing prior service cost for pensions and other postretirement benefit plans will:

a. Decrease retained earnings.

b. Increase assets.

c. Decrease assets.

d. Decrease shareholders’ equity.

Technoid Inc. sells computer systems. Technoid leases computers to Lone Star

Company on January 1, 2016. The manufacturing cost of the computers was $12

million.

This noncancelable lease had the following terms:

-Lease payments: $2,466,754 semiannually; first payment at January 1, 2016;

remaining payments at –June 30 and December 31 each year through June 30, 2020.

-Lease term: five years (10 semiannual payments).

-No residual value; no bargain purchase option.

-Economic life of equipment: five years.

-Implicit interest rate and lessee’s incremental borrowing rate: 5% semiannually.

-Fair value of the computers at January 1, 2016: $20 million.

Collectibility of the rental payments is reasonably assured, and there are no lessor costs

yet to be incurred.

What is the net book value of the lease liability in Lone Star’s June 30, 2016, balance

sheet? Round your answer to the nearest dollar.

a. $15,943,154.

b. $17,533,246.

c. $21,000,000.

d. None of these answer choices is correct.

Stock option plans give employees the option to purchase (a) a specified number of

shares of the firm’s stock, (b) at a specified price, (c) during a specified period of time.

One of the most heated controversies in standard-setting history has been the debate

over the amount of compensation to be recognized as expense for stock options. At

issue is how the value of stock options is measured, which for most options determines

whether any expense at all is recognized. The opposition included corporate executives,

auditors, members of Congress, and the SEC.

Required:

Describe the primary objections of critics of the FASB’s eventually successful attempt

to require expensing of the fair value of the options.

A company failed to report the $600,000 additional liability for its underfunded pension

plan. Its tax rate is 30%. As result of this error, retained earnings would be:

a. Unaffected.

b. Overstated by $600,000.

c. Overstated by $420,000.

d. Overstated by $180,000.

During the current year, Stern Company had pretax accounting income of $45 million.

Stern’s only temporary difference for the year was rent received for the following year

in the amount of $15 million. Stern’s taxable income for the year would be:

a. $30 million.

b. $60 million.

c. $50 million.

d. $45 million.

On June 30, 2016, Blair Industries had outstanding $80 million of 8% convertible bonds

that mature on June 30, 2017. Interest is payable each year on June 30 and December

31. The bonds are convertible into 6 million shares of $10 par common stock. At June

30, 2016, the unamortized balance in the discount on bonds payable account was $4

million. On June 30, 2016, half the bonds were converted when Blair’s common stock

had a market price of $30 per share. When recording the conversion, Blair should credit

paid-in capital-excess of par:

a. $6 million.

b. $8 million.

c. $10 million.

d. $12 million.

For the lessor to account for a lease as a capital lease, the lease must meet:

a. Any one of first four classification criteria and both of the last two additional

conditions specified by GAAP regarding accounting for leases.

b. Any one of the six criteria specified by GAAP regarding accounting for leases.

c. All four of the criteria specified by GAAP regarding accounting for leases.

d. Any one of the four criteria specified by GAAP regarding accounting for leases.

Consolidated financial statements are prepared when one company has:

a. Accounted for the investment using the equity method.

b. Accounted for the investment as securities available for sale.

c. Control over another company.

d. None of these answer choices is correct.

Harvey’s Wholesale Company sold supplies of $46,000 to Northeast Company on April

12 of the current year, with terms 1/15, n/60. Harvey uses the net method of accounting

for cash discounts.

What entry would Harvey’s make on June 10, assuming the customer made the correct

payment on that date?

During 2016, Quattro entered into the following transactions relating to shareholders’

equity. The corporation was authorized to issue 20 million common shares, $1 par per

share.

Net income for 2016 was $110 million.

Jan. 2: Issued 10 million common shares for cash.

Jan. 3 Entered an agreement with the company president to issue up to 2 million

additional shares of common stock in 2016 based on the earnings of Quattro in 2016. If

net income exceeds $100 million, the president will receive 1 million shares; 2 million

shares if net income exceeds $120 million.

Required:

Compute basic and diluted EPS for 2016.

In 2016, Cap City Inc. introduced a new line of televisions that carry a two-year

warranty against manufacturer’s defects. Based on past experience with similar

products, warranty costs are expected to be approximately 1% of sales during the first

year of the warranty and approximately an additional 3% of sales during the second

year of the warranty. Sales were $6,000,000 for the first year of the product’s life and

actual warranty expenditures were $29,000. Assume that all sales are on credit.

Required:

1> Prepare journal entries to summarize the sales and any aspects of the warranty for

2016.

2> What amount should Cap City report as a liability at December 31, 2016?

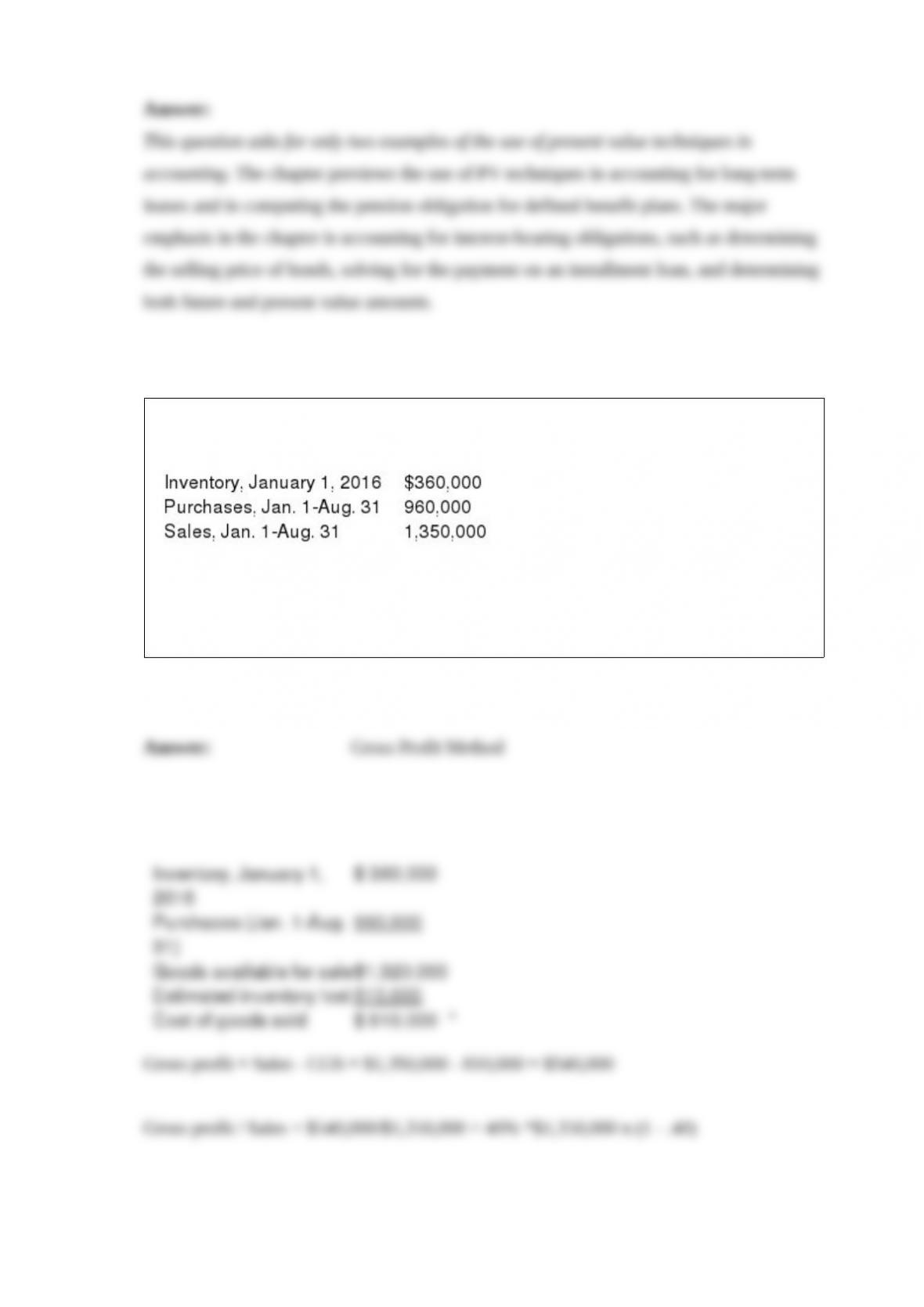

Provide two examples of the use of present value techniques in accounting.

On August 31, 2016, Hurricane Chuck destroyed Bedford Craft Mart’s entire inventory.

The following information is available from its accounting records:

Required:

Assuming that Bedford estimates the cost of destroyed inventory at $510,000, compute

gross profit margin % that Bedford uses in estimating inventory.

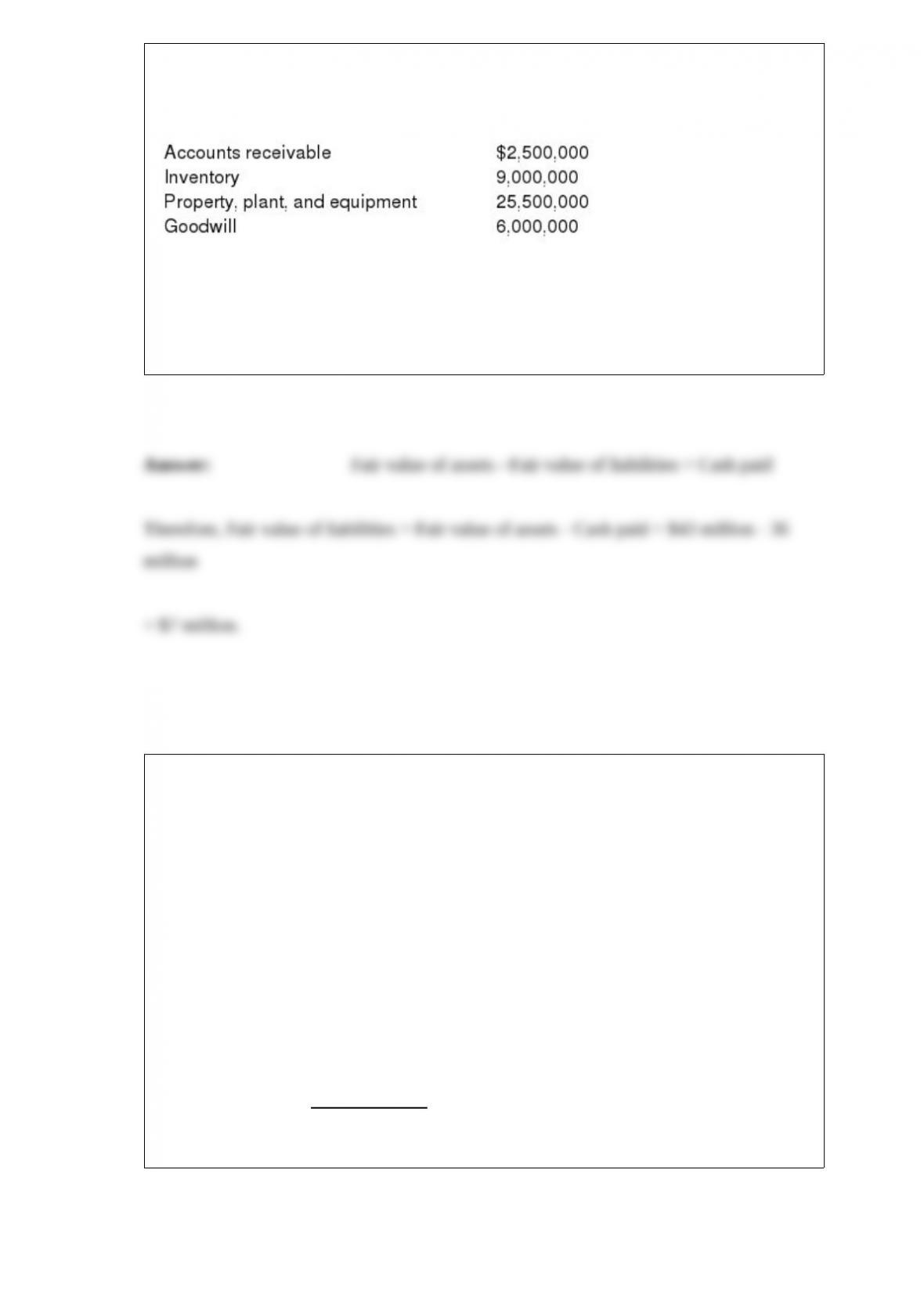

During the current year, Peterson Data Corporation acquired all of the outstanding

common stock of Junior Jackson Inc. (JJI), paying $36 million in cash. Peterson

recorded the assets acquired as follows:

The book value of JJI’s assets and owners’ equity before the acquisition were $22

million and $18 million, respectively.

Required: Compute the fair value of JJI’s liabilities that Peterson assumed in the

acquisition.

Terra Bus Transportation provides on-campus bus services for universities. On January

1, it enters into a one-year contract with Moose University to operate five bus lines

traveling throughout the campus. Under the contract, Terra will be paid $100,000 on the

last day of each month. In addition, Terra will receive an additional $120,000 at the end

of each six-month period, provided it remains free of accidents. – On January 1, based

on historical experience, Terra estimated that there is a 75% chance that it will remain

free of accidents for the entire year.

– On March 20, three of the most senior drivers at Terra abruptly left. As a result, Terra

had to hire inexperienced drivers to fill the vacant positions. Consequently, Terra

revised its estimate to a 30% chance that it would earn the semiannual bonus.

– On June 30, Moose confirmed that there was no accident between January and June,

so Terra would be entitled to the semiannual bonus. Terra bases estimates of variable

consideration on the expected value it expects to receive. Prepare Terra’s June 30

journal entry to account for the revenue earned from June 1 – June 30, as well as any

necessary adjustments to revenue.

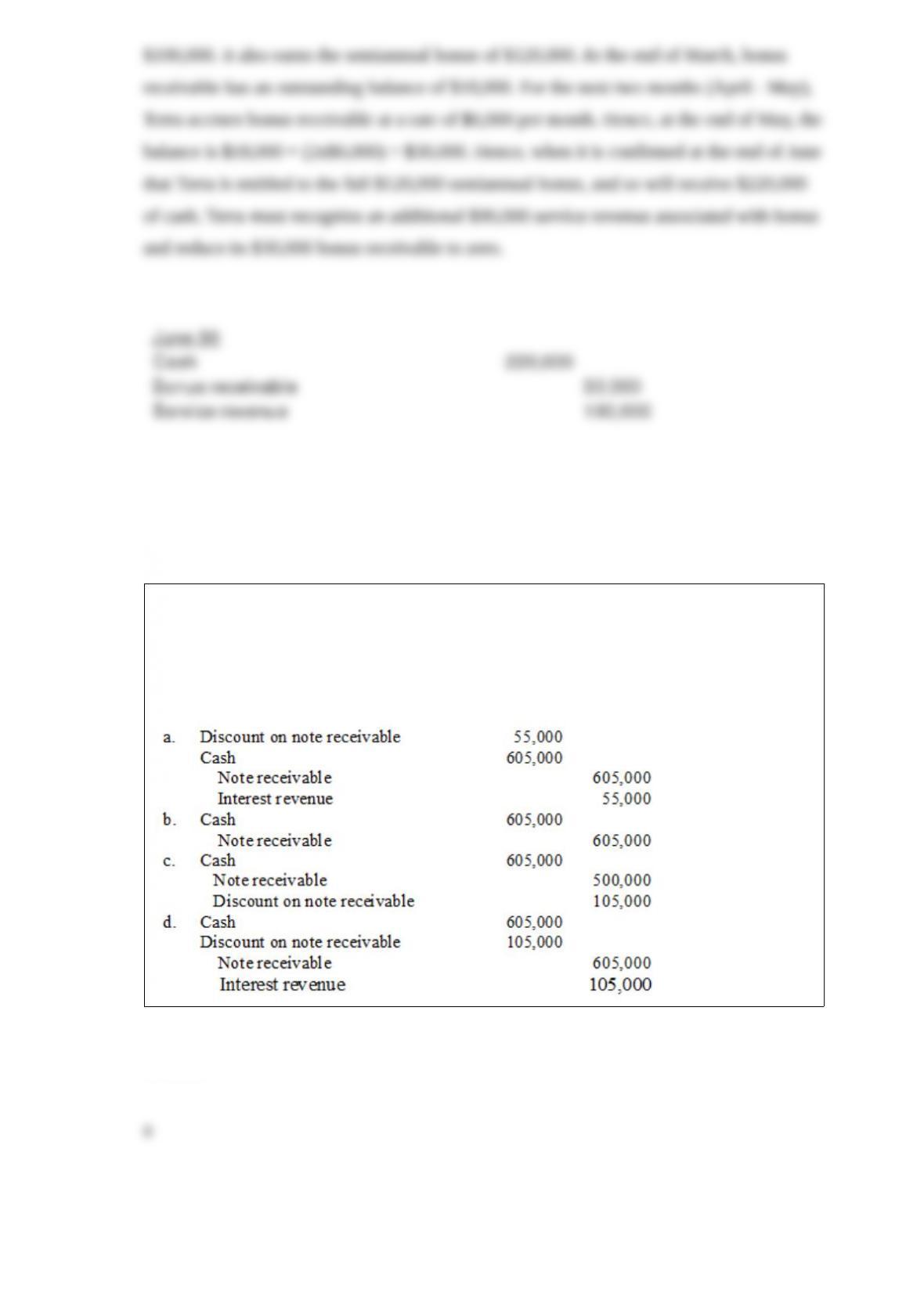

Chen Inc. accepted a two-year noninterest-bearing note for $605,000 on January 1,

2016. The note was accepted as payment for merchandise with a fair value of $500,000.

The effective interest rate is 10%. The cash collection on December 31, 2017, would be

recorded as:

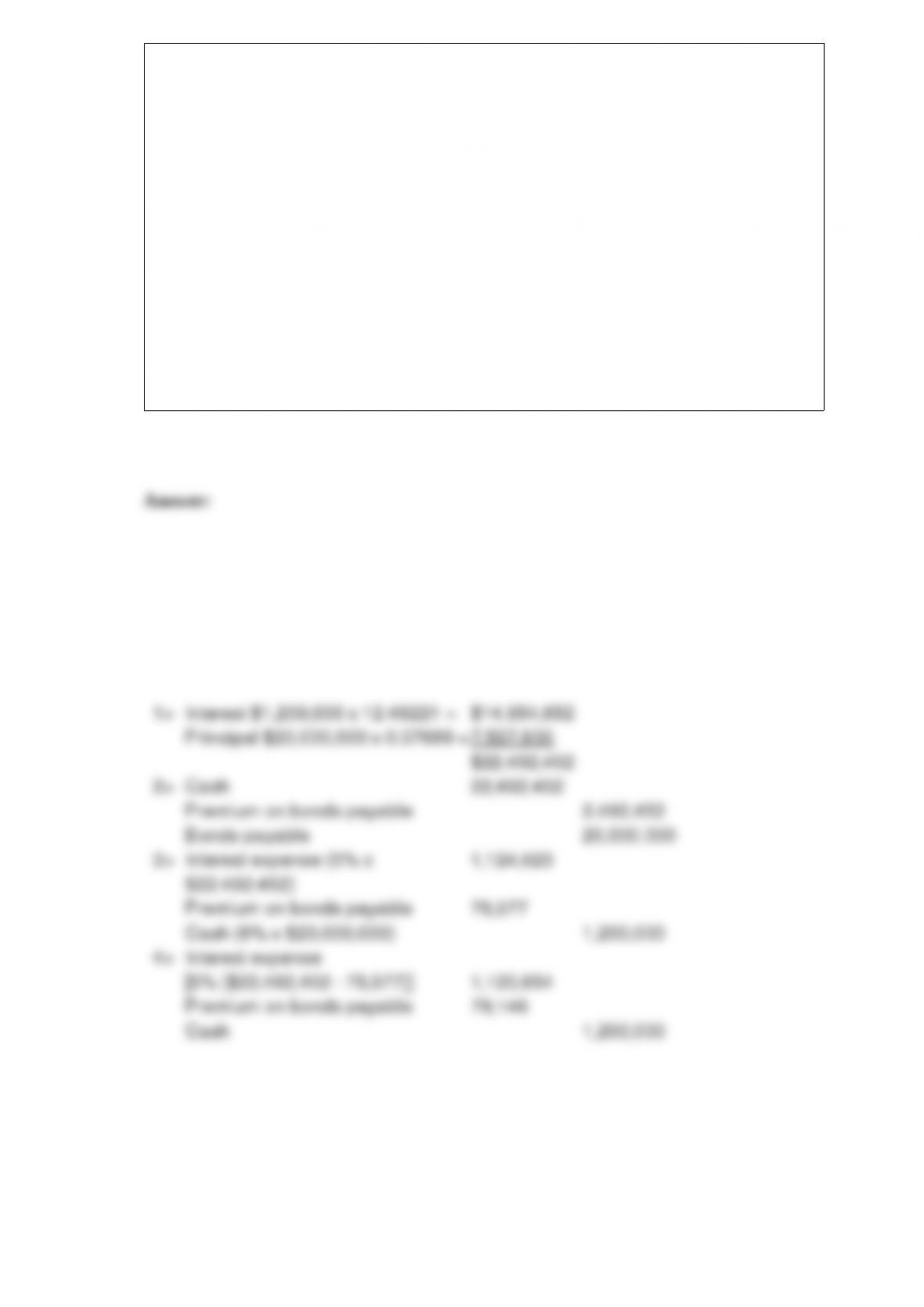

On January 1, 2016, Mania Enterprises issued 12% bonds dated January 1, 2016, with a

face amount of $20 million. The bonds mature in 2025 (10 years). For bonds of similar

risk and maturity, the market yield is 10%. Interest is paid semiannually on June 30 and

December 31.

Required:

1> Determine the price of the bonds at January 1, 2016.

2> Prepare the journal entry to record the bond issuance by Mania on January 1, 2016.

3> Prepare the journal entry to record interest on June 30, 2016, using the effective

interest method.

4> Prepare the journal entry to record interest on December 31, 2016, using the

effective interest method.