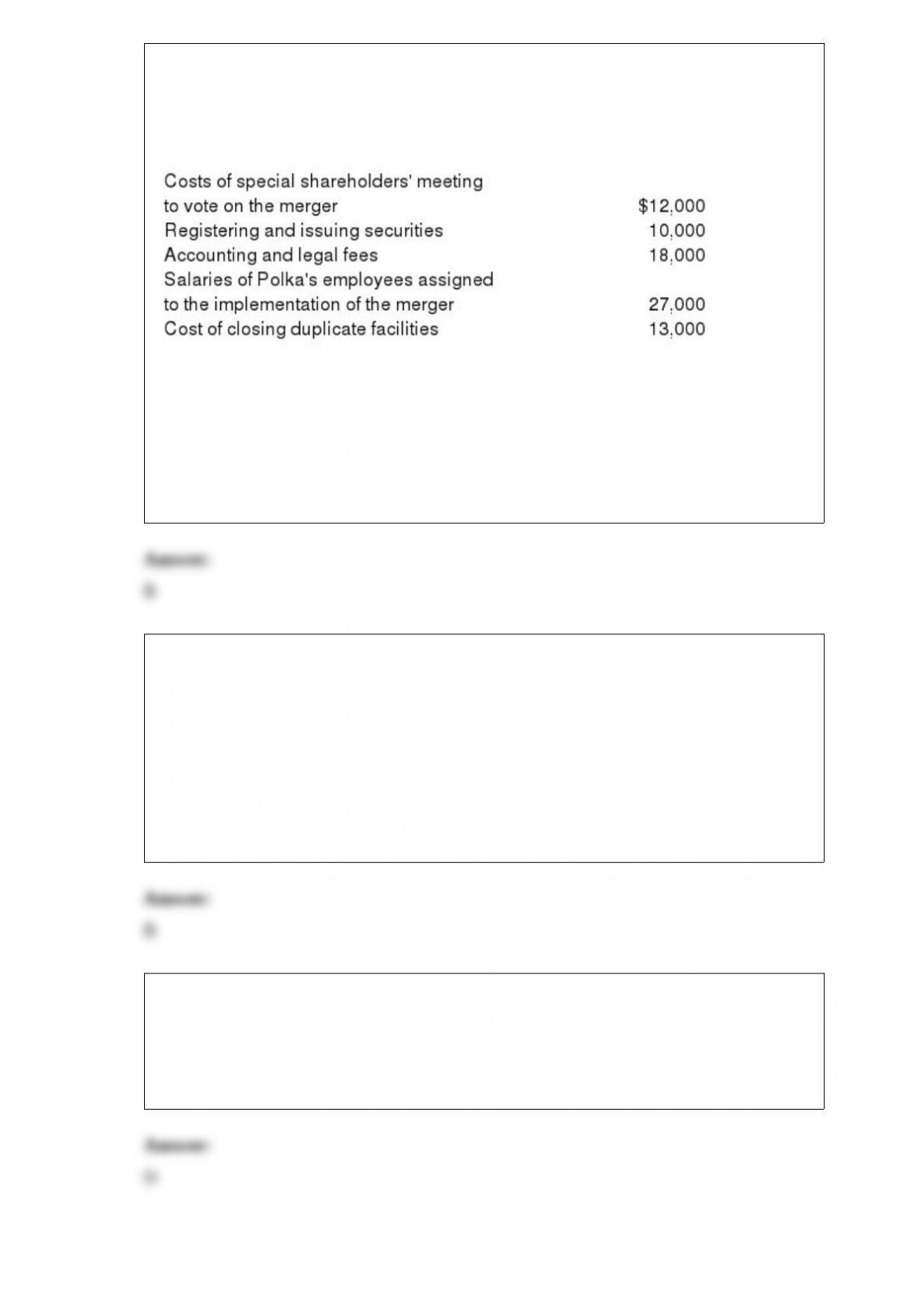

1) Polka Corporation exchanges 100,000 shares of newly issued $1 par value common

stock with a fair market value of $20 per share for all of the outstanding $5 par value

common stock of Spot Inc. and Spot is then dissolved. Polka paid the following costs

and expenses related to the business combination:

In the business combination of Polka and Spot

A) the costs of registering and issuing the securities are included as part of the purchase

price for Spot

B) the salaries of Polka’s employees assigned to the merger are treated as expenses

C) all of the costs except those of registering and issuing the securities are included in

the purchase price of Spot

D) only the accounting and legal fees are included in the purchase price of Spot

2) With respect to exchange rates, which of the following statements is true?

A) An official exchange rate is the “market” rate resulting from the supply and demand

for a currency

B) A floating exchange rate is the “market” rate resulting from the supply and demand

for a currency

C) A government cannot set an exchange rate for their currency that is higher (weakens

their currency) than the quoted interbank market rate

D) A government cannot set an exchange rate for their currency that is lower

(strengthens their currency) than the quoted interbank market rate

3) Which of the following must approve a Chapter 11 plan?

A) The organization’s management and the assigned trustee

B) The assigned trustee and creditors

C) The assigned trustee and entity’s stockholders

D) The bankruptcy court and the creditors

4) Which of the following methods does the FASB consider the best indicator of fair

values in the evaluation of goodwill impairment?

A) Senior executive’s estimates

B) Financial analyst forecasts

C) Market value

D) The present value of future cash flows discounted at the firm’s cost of capital

5) The income from an equity method investee is reported on one line of the investor

company’s income statement except when

A) the cost method is used

B) the investee has extraordinary items

C) the investor company is amortizing cost-book value differentials

D) the investor company changes from the cost to the equity method

6) A key assumption in the segmented markets theory is that bonds of different

maturities

A) are not substitutes at all

B) are perfect substitutes

C) are substitutes only if the investor is given a premium incentive

D) are substitutes but not perfect substitutes

7) Jersey Company acquired 90% of York Company on April 1, 2011 . Both Jersey

Company and York Company have December 31 fiscal year ends. Under current GAAP,

which of the following statements is false?

A) The consolidated income statement in 2011 should not include York’s revenues and

expenses prior to April 1, 2011

B) When preparing consolidating work papers in 2011, York’s revenues prior to April 1,

2011 are eliminated

C) York’s earnings prior to April 1, 2011 should appear as a deduction on the

consolidated income statement in 2011

D) The consolidated income statement in 2011 should include York’s revenues and

expenses after April 1, 2011

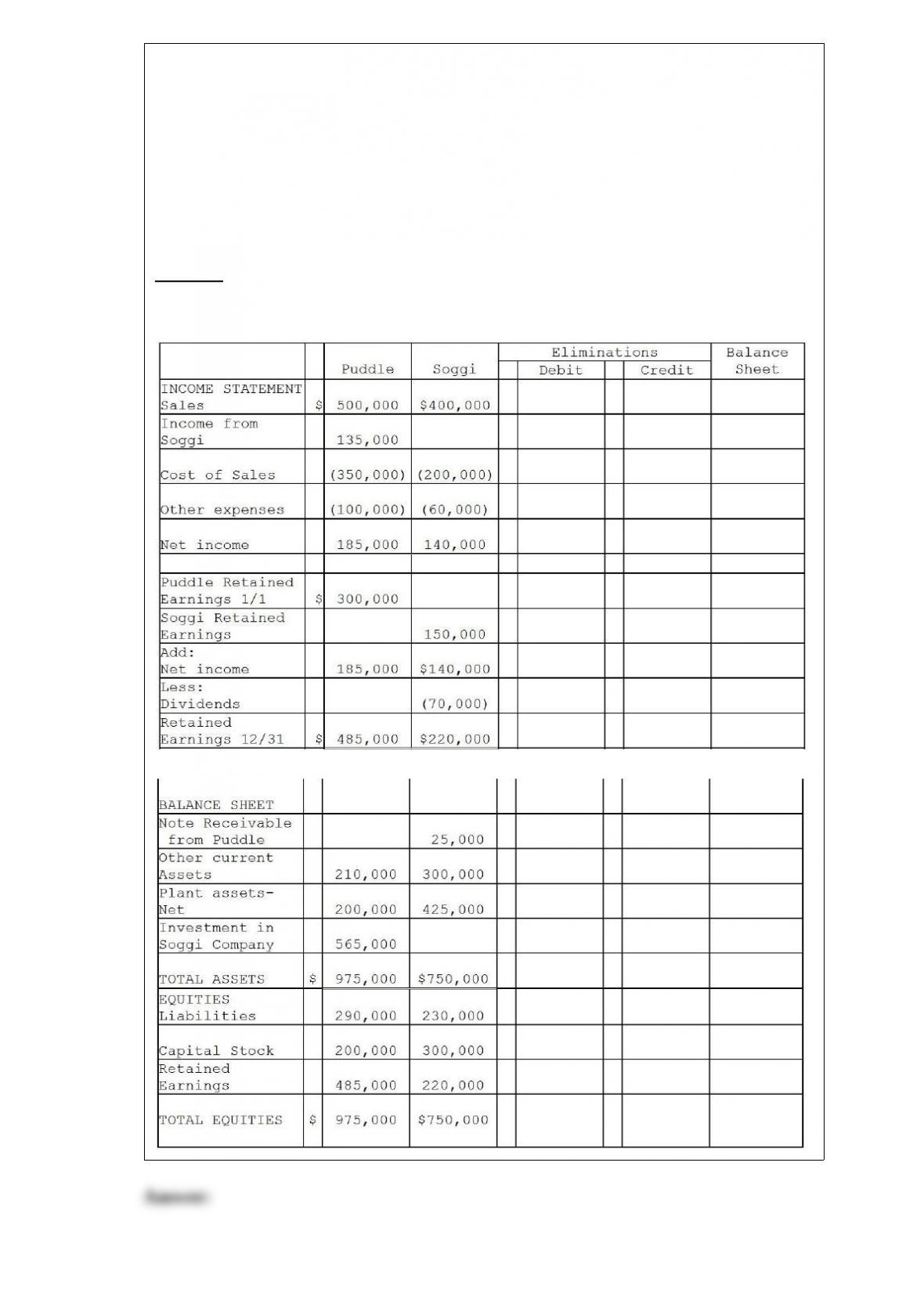

8) Puddle Corporation acquired all the voting stock of Soggi Company for $500,000 on

January 1, 2011 when Soggi had Capital Stock of $300,000 and Retained Earnings of

$150,000. The book value of Soggi’s assets and liabilities were equal to the fair value

except for the plant assets. The entire cost-book value differential is allocated to plant

assets and is fully depreciated on a straight-line basis over a 10-year period.

During 2011, Puddle borrowed $25,000 on a short-term non-interest-bearing note from

Soggi, and on December 31, 2011, Puddle mailed a check to Soggi to settle the note.

Soggi deposited the check on January 5, 2012, but receipt of payment of the note was

not reflected in Soggi’s December 31, 2011 balance sheet.

Required:

Complete the consolidation working papers for the year ended December 31, 2011 .

9) An increase in default risk on corporate bonds ________ the demand for these bonds,

but ________ the demand for default-free bonds, everything else held constant

A) increases; lowers

B) lowers; increases

C) does not change; greatly increases

D) moderately lowers; does not change

10) Paris Corporation purchased 80% of the outstanding voting common stock of

Sanders Corporation on January 1, 2011, at a cost of $400,000. The stockholders’ equity

of Sanders Corporation on this date consisted of $200,000 of Capital Stock and

$100,000 of Retained Earnings. Book values were equal to fair values except for land

and inventory. The book value of Sanders’ land was $10,000, and fair value was

$22,000. The book value of Sanders’ inventory was $30,000, and fair value was

$25,000.

Under the parent company theory, what amount of goodwill was reported on the

consolidated balance sheet at December 31, 2011?

A) $148,000

B) $153,000

C) $154,400

D) $160,000

11) Centralized data processing, central motor pools and garages, centralized

risk-financing activities, and central stores typically would be accounted for using what

type of fund?

A) An agency fund

B) An enterprise fund

C) An internal service fund

D) A trust fund

12) A bankruptcy petition filed by a firm’s creditors is

A) a Chapter 2 petition

B) a petition for liquidation

C) an involuntary petition

D) a voluntary petition

13) According to the segmented markets theory of the term structure

A) the interest rate on long-term bonds will equal an average of short-term interest rates

that people expect to occur over the life of the long-term bonds

B) buyers of bonds do not prefer bonds of one maturity over another

C) interest rates on bonds of different maturities do not move together over time

D) buyers require an additional incentive to hold long-term bonds

14) Pouch Corporation acquired an 80% interest in Shenley Corporation on January 1,

2012, when the book values of Shenley’s assets and liabilities were equal to their fair

values. The cost of the 80% interest was equal to 80% of the book value of Shenley’s

net assets. During 2012, Pouch sold merchandise that cost $70,000 to Shenley for

$86,000. On December 31, 2012, three-fourths of the merchandise acquired from Pouch

remained in Shenley’s inventory. Separate incomes (investment income not included) of

the two companies are as follows:

PouchShenley

Sales Revenue $180,000 $160,000

Cost of Goods Sold 120,00090,000

Operating Expenses 17,000 21,000

Separate incomes$ 43,000$ 49,000

What is Pouch’s income from Shenley for 2012?

A) $27,200

B) $29,600

C) $39,200

D) $49,000

15) If the expected path of 1-year interest rates over the next five years is 2 percent, 4

percent, 1 percent, 4 percent, and 3 percent, the expectations theory predicts that the

bond with the lowest interest rate today is the one with a maturity of

A) one year

B) two years

C) three years

D) four years

16) Separate income statements of Plantation Corporation and its 90%-owned

subsidiary, Savannah Corporation, for 2011 are as follows, prior to Plantation recording

any income related to its subsidiary:

PlantationSavannah

Sales Revenue$870,000 $230,000

Gain on equipment35,000

Gain on land20,000

Cost of sales(470,000)(90,000)

Other expenses(265,000)(60,000)

Separate incomes$170,000 $100,000

Additional information:

1>Plantation acquired its 90% interest in Savannah Corporation when the book values

were equal to the fair values.

2>The gain on equipment relates to equipment with a book value of $95,000 and a

7-year remaining useful life that Plantation sold to Savannah for $130,000 on January 1,

2011 . The straight-line depreciation method was used and the equipment has no

salvage value.

3>On January 1, 2011, Savannah sold land to an outside entity for $90,000. The land

was acquired from Plantation in 2009 for $70,000. The original cost of the land to

Plantation was $45,000.

4>Savannah did not declare or distribute dividends in 2011 .

Required:

1>Prepare elimination/adjusting entries on the consolidated worksheet for the year 2011

.

2>Prepare the consolidated income statement for the year ended December 31, 2011 .

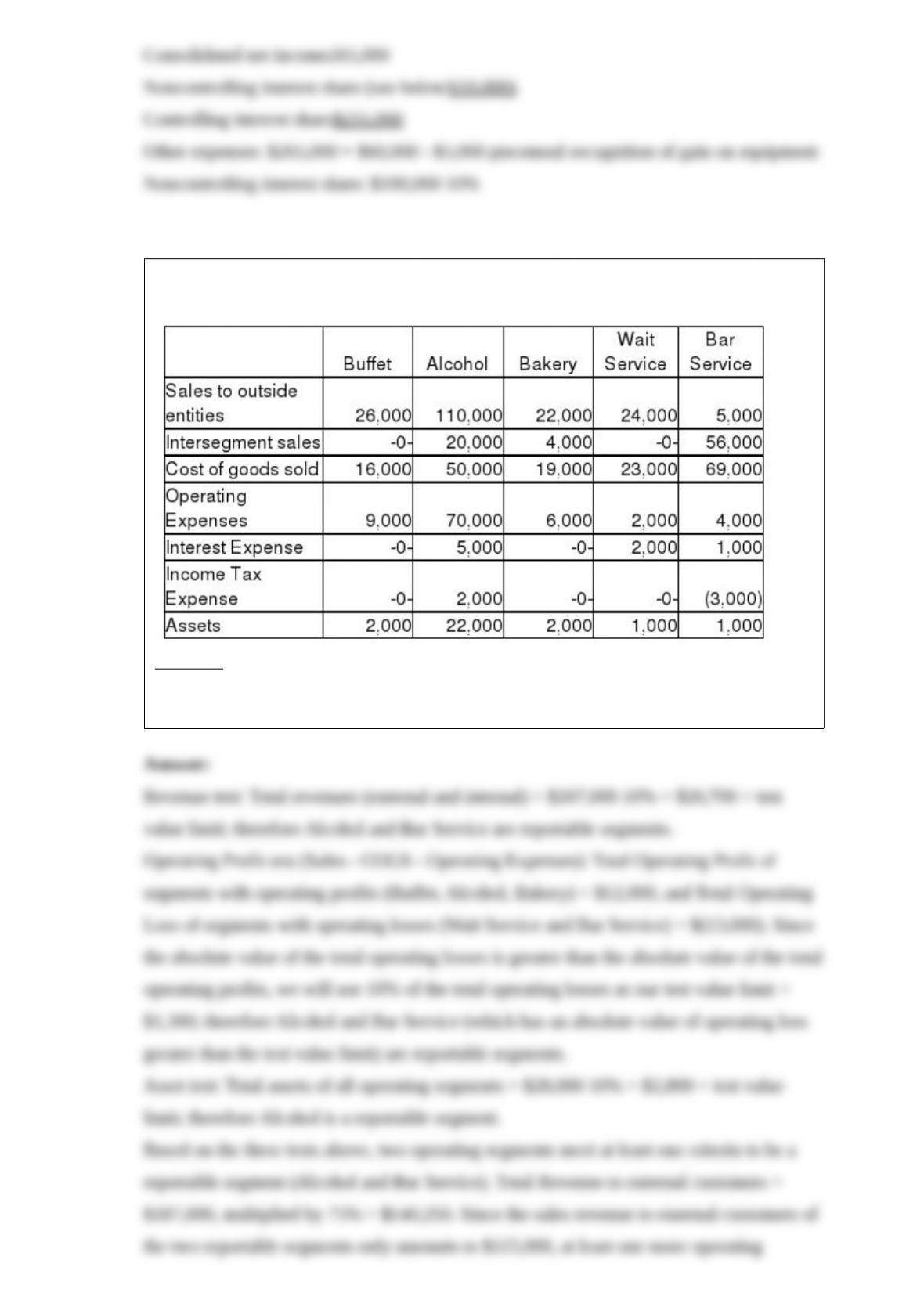

17) Snodberry Catering has five operating segments, as summarized below:

Required:

Determine which of the operating segments of Snodberry Catering are reportable

segments for the period shown.

18) Pane Corporation owns 100% of Alder Corporation, 85% of Ball Corporation, 70%

of Cake Corporation, 40% of Dash Corporation, and 10% of Eager Corporation. All of

these corporations are domestic corporations. Pane, Alder and Ball belong to an

affiliated group. Pane’s marginal income tax rate is 35%. All investees have paid out all

their net income in the form of dividends. During 2011, Pane Corporation received the

following cash dividends:

From Alder:$180,000

From Ball:$170,000

From Cake:$160,000

From Dash:$100,000

From Eager:$ 60,000

Required:

1> Compute the amount of the dividend income that would be excluded from taxation

under the current Internal Revenue Code.

2> Compute Pane’s current income tax liability for the dividend income received in

2011 .

19) Coats for Kids is a private, not-for-profit organization that provides free coats for

children in the suburbs of a large city. Coats for Kids had the following transactions in

2011 .

1>Unrestricted cash gifts that were received last year, but designated for use in the

current year, totaled $50,000. The cash gifts were used in 2011 .

2>Unrestricted pledges of $40,000 were received. They are expected to be collected in

2011 . Ten percent of the pledges typically prove uncollectible. Additional cash

contributions during the year totaled $65,000.

3>A donor donated investments with a fair value of $10,000. The investments can be

sold and used only for the purchase of coats for children.

4>The following expenses were incurred and paid: Salary of director, $15,000,

classified as supporting services. The remaining expenses of $47,500 were classified as

program services.

5>Pledges of $250,000 were received during the year. The pledges were restricted for

use in purchasing new delivery vans. All of these pledges are expected to be collected

in the next fiscal year. Ten percent are estimated to be uncollectible.

Required:

Prepare the journal entries for the aforementioned transactions.

20) For each of the following transactions relating to the startup of a community pool,

determine the fund(s) being affected and prepare the appropriate journal entry for each.

Be sure to note the fund type with each journal entry prepared.

1>General obligation bonds are issued at face value of $500,000 to construct a new

community pool.

2>Cash of $100,000 is received from a state grant. Grant is set up to support the

construction of the community pool.

3>A community fund-raiser by a citizens’ group raises $50,000 which is donated to the

pool fund, with the restriction placed on it that only earnings are to be used for lifeguard

wages, and the principal may not be used until such time as the pool ceases to operate,

at which time the principal will revert to the general fund.

4>Construction is completed and the contractors invoices received, totaling $578,000.

The invoices are paid within 60 days.

5>The balance of funds from the general obligation bonds and state grant that was not

used is transferred to the General Fund.

21) Childrens Hospital is a private, not-for-profit hospital. The following information is

available about the operations.

1>Gross patient services charges totaled $6,400,000.

2>Included in the above revenues are: charity services, $210,000; contractual

adjustments, $2,400,000; and courtesy allowances, $37,000.

3>Received a donation of marketable securities with a fair value of $165,000 for the

purchase of new diagnostic equipment.

4>The marketable securities were sold for $182,000 and diagnostic equipment was

purchased at a cost of $210,000.

5>Revenue from the hospital gift shop was $58,000 and from the cafeteria revenues

were $227,000. Received cash from both enterprises.

6>Incurred and paid nursing service costs of $1,700,000 and general service costs of

$400,000.

Required:

Prepare journal entries for the aforementioned transactions.

22) Albatross University, a not-for-profit, nongovernmental university, had the

following transactions in 2011 .

1>Tuition bills were sent amounting to $8,000,000, with 70% collected before the end

of the fiscal year; tuition waivers were granted on the total amount of $400,000, and

$220,000 was expected to be uncollectible.

2>Cafeteria sales, all cash, were $1,400,000.

3>Salaries and wages were paid amounting to $5,500,000, of which $370,000 was for

cafeteria staff.

4>Long-term debt payments were made from general funds amounting to $800,000, of

which $130,000 was for interest.

5>Equipment was purchased for the engineering department with funds previously set

aside for that purpose, amounting to $180,000.

Required:

Prepare the journal entries for 2011 for Albatross University.

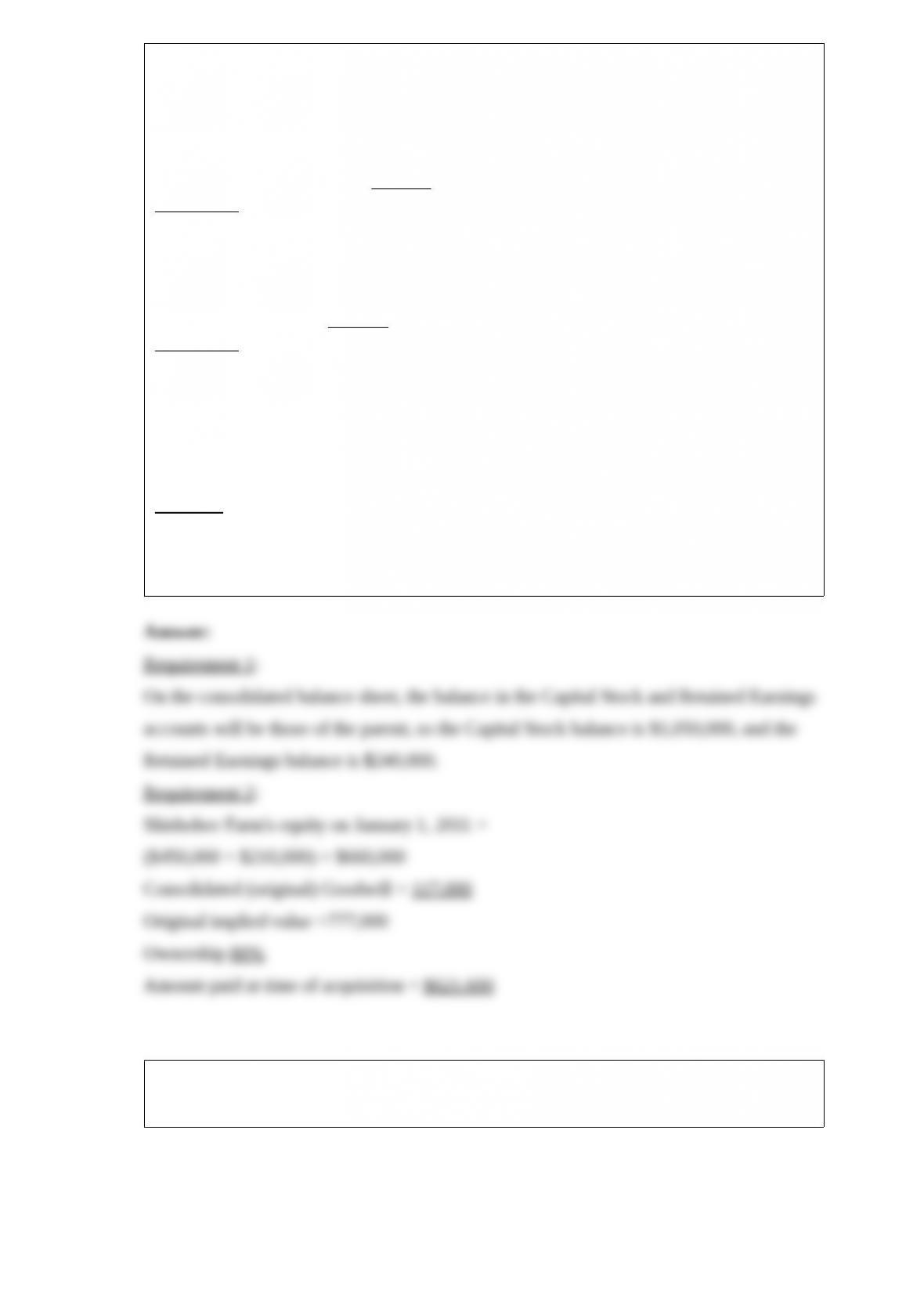

23) The consolidated balance sheet of Pasker Corporation and Shishobee Farm, its 80%

owned subsidiary, as of December 31, 2011, contains the following accounts and

balances:

Pasker Corporation and Subsidiary

Consolidated Balance Sheet

at December 31, 2011

Balances

Cash$57,000

Accounts receivable-net210,000

Inventories330,000

Other current assets255,000

Plant assets-net870,000

Goodwill from consolidation117,000

$1,839,000

Accounts payable$219,000

Other liabilities210,000

Capital stock1,050,000

Retained earnings240,000

Noncontrolling interest120,000

$1,839,000

Pasker Corporation acquired its interest in Shishobee Farm on January 1, 2011, when

Shishobee Farm had $450,000 of Capital Stock and $210,000 of Retained Earnings.

Shishobee Farm’s net assets had fair values equal to their book values when Pasker

acquired its interest. No changes have occurred in the amount of outstanding stock

since the date of the business combination. Pasker uses the equity method of accounting

for its investment.

Required: Determine the following amounts:

1>The balance of Pasker’s Capital Stock and Retained Earnings accounts at December

31, 2011

2>Cost of Pasker’s purchase of Shishobee Farm on January 1, 2011

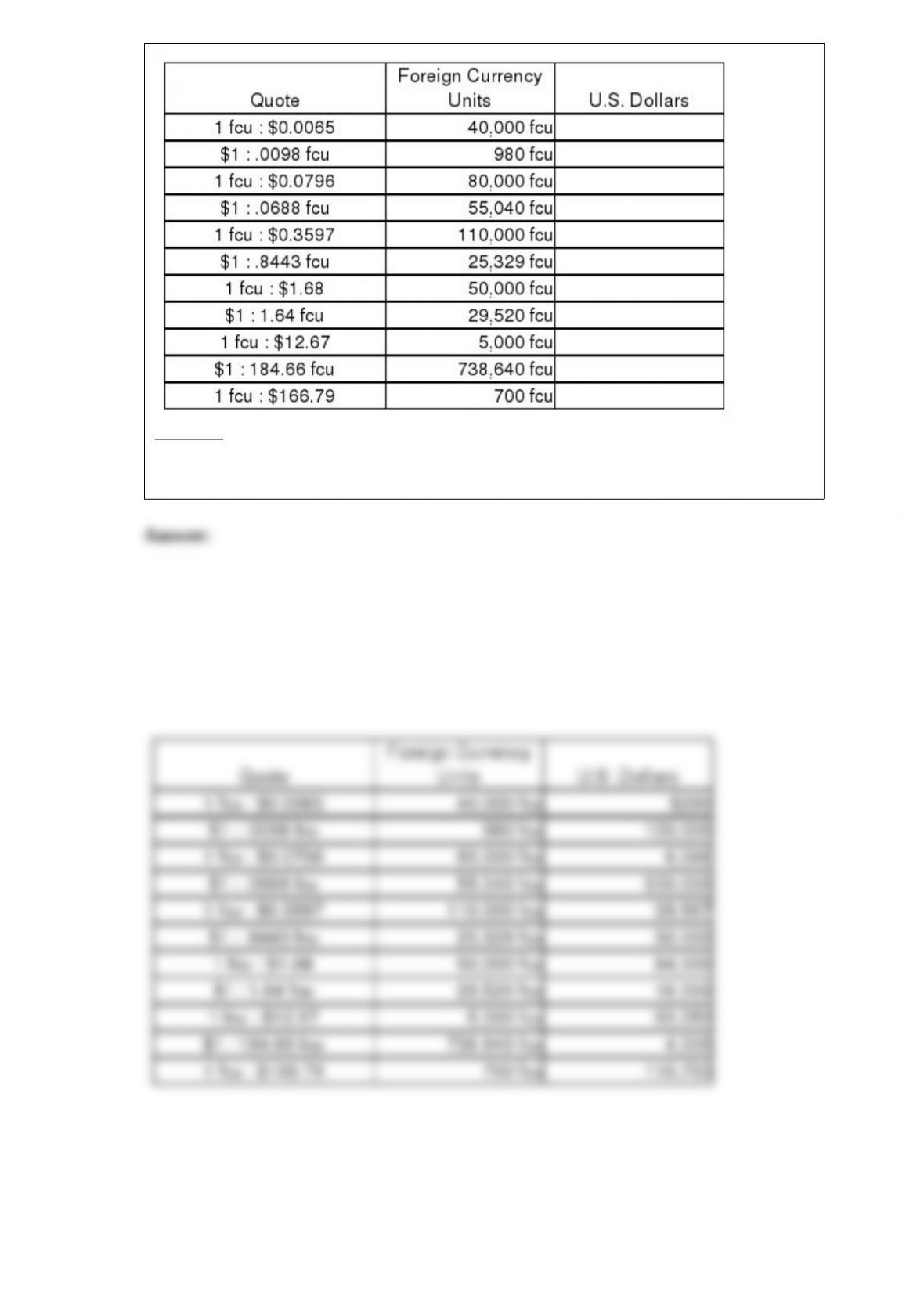

24) The table below provides either a direct or indirect quote for a given foreign

currency unit, and the related units of that foreign currency.

Required:

Complete the table, indicating the amount of U.S. Dollars that is the equivalent of the

foreign currency shown, based on the direct or indirect quote provided.