1) an error that overstates the ending inventory will also cause net income for the period

to be overstated.

2) the economic entity assumption states that economic events can be identified with a

particular unit of accountability.

3) sales minus operating expenses equals gross profit.

4) if an acquired franchise or license is for an indefinite time period, then the cost of the

asset should not be amortized.

5) when an account receivable that was previously written off is collected, it is first

necessary to reverse the entry to reinstate the customers account before recording the

collection.

6) any item that appears on the income statement would be considered as either a cash

inflow or cash outflow from operating activities.

7) gross profit rate is computed by dividing cost of goods sold by net sales.

8) if the ownership of merchandise passes to the buyer when the seller ships the

merchandise, the terms are stated as fob destination.

9) the process of determining the present value is referred to as discounting the future

amount.

10) at may 1, 2012, heineken company had beginning inventory consisting of 100 units

with a unit cost of $7. during may, the company purchased inventory as follows:

200 units at $7

300 units at $8

the company sold 500 units during the month for $12 per unit. heineken uses the average

cost method. the average cost per unit for may is

a.$7.00

b.$7.50

c.$7.60

d.$8.00

11) dividends appear on

a.the retained earnings statement only

b.the income statement only

c.both the retained earnings statement and the balance sheet

d.the balance sheet only

12) which statement is correct concerning the adjusted trial balance?

a.an adjusted trail balance eliminates the need for the preparation of financial

statements

b.the purpose of an adjusted trial balance is to prove the equality of the total debit

balances and the total credit balances in the ledger

c.an adjusted trial balance will contain only permanentbalance sheetaccounts

d.the adjusted trial balance is prepared after the adjusting entries have been journalized

but before they have been posted

13) the market adjustment account

a.is set up for each security in the company’s portfolio

b.relates to the entire portfolio of securities held by the company

c.is closed at the end of each accounting period

d.appears on the income statement as other expenses and losses

14) when authorizing bonds to be issued, the board of directors does not specify the

a.total number of bonds authorized to be sold

b.contractual interest rate

c.selling price

d.total face value of the bonds

15) walton company collected $7,200 in may of 2010 for 4 months of service which

would take place from october of 2010 through january of 2011. the revenue reported

from this transaction during 2010 would be:

a.$0

b.$5,400

c.$7,200

d.$1,800

16) inventory becomes part of cost of goods sold when a company

a.pays for the inventory

b.purchases the inventory

c.sells the inventory

d.receives payment from the customer

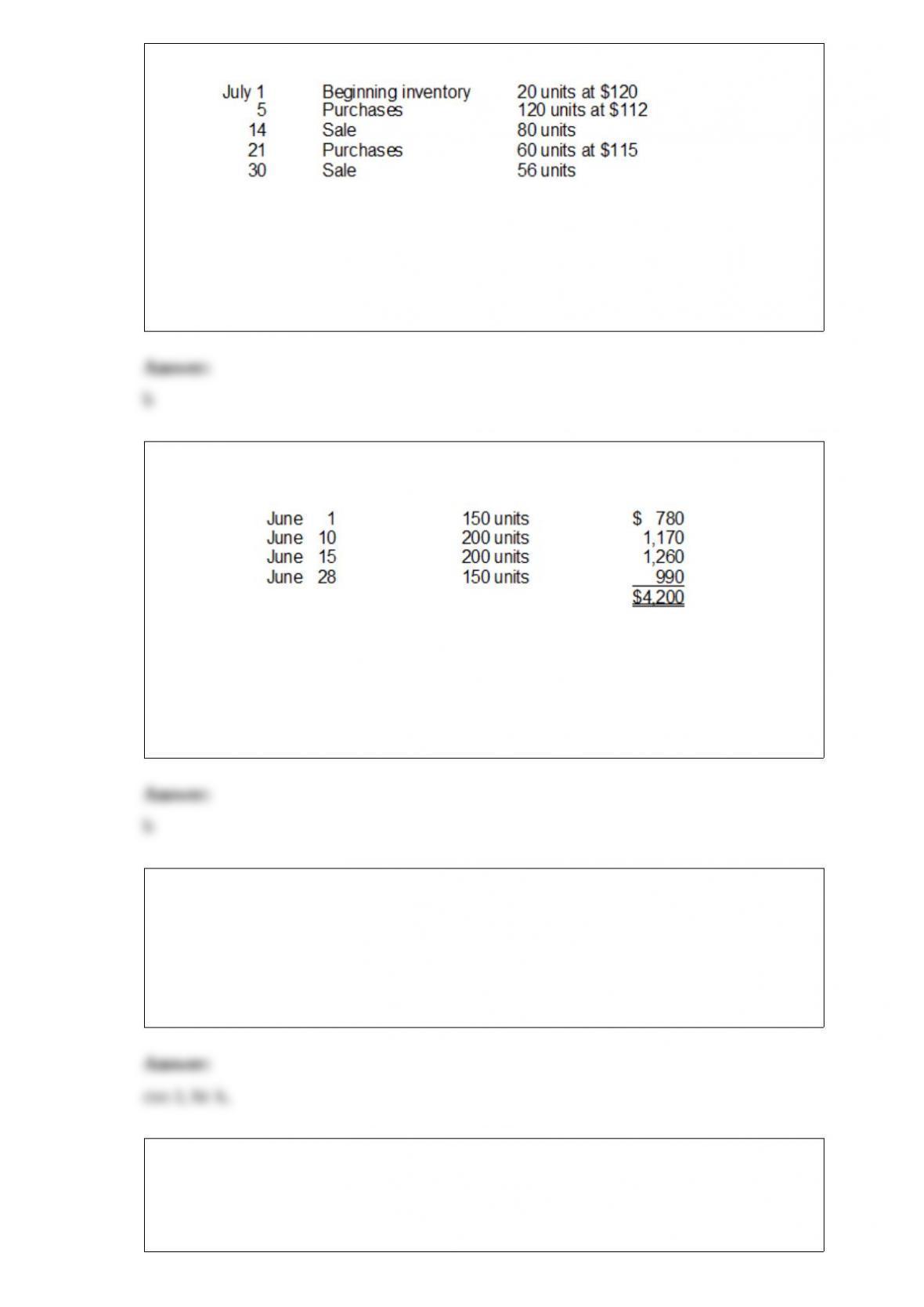

17) clear clarinets has the following inventory data:

assuming that a periodic inventory system is used, what is the amount allocated to

ending inventory on a fifo basis.

a.$7,288

b.$7,348

c.$15,392

d.$15,412

18) alpha first company just began business and made the following four inventory

purchases in june:

a physical count of merchandise inventory on june 30 reveals that there are 250 units on

hand. using the lifo inventory method, the value of the ending inventory on june 30 is

a.$1,300

b.$1,365

c.$1,650

d.$1,620

19) the primary difference between prepaid and accrued expenses is that prepaid

expenses have:

a.been incurred and accrued expenses have not

b.not been paid and accrued expenses have

c.been recorded and accrued expenses have not

d.not been recorded and accrued expenses have

20) unearned revenue is classified as a(n):

a.asset account

b.revenue account

c.contra revenue account

d.liability

21) stockholders of a corporation directly elect

a.the president of the corporation

b.the board of directors

c.the treasurer of the corporation

d.all of the employees of the corporation

22) if a company fails to adjust for accrued revenues:

a.liabilities will be understated and revenues will be understated

b.liabilities will be overstated and revenues will be understated

c.assets will be overstated and revenues will be understated

d.assets will be understated and revenues will be understated

23) cash generated from operations exceeds investing needs, and the company can

begin retiring debt during the

a.introductory phase

b.growth phase

c.maturity phase

d.decline phase

24) regions inc. pays its rent of $60,000 annually on january 1 and makes monthly

adjusting entries. if the february 28 monthly adjusting entry for prepaid rent is omitted,

which of the following are true?

a.failure to make the adjustment does not affect the february financial statements

b.expenses will be overstated by $5,000 and net income and stockholders’ equity will be

understated by $5,000

c.assets will be overstated by $10,000 and net income and stockholders’ equity will be

understated by $10,000

d.assets will be overstated by $5,000 and net income and stockholders’ equity will be

overstated by $5,000

25) dalton company was undergoing an end of year audit of its financial records. the

auditors were in the process of reviewing daltons inventory for year end, december 31,

2012. they completed an end of year inventory. the value of the ending inventory prior

to any adjustments was $192,000, but before finishing up they had a few questions.

discussion with daltons accountant revealed the following:

(a)dalton sold goods costing $60,000 to summey company fob shipping point on

december 28. the goods are not expected to reach summey until january 12. the goods

were not included in the physical inventory because they were not in the warehouse.

(b)the physical count of the inventory did not include goods costing $95,000 that were

shipped to dalton fob destination on december 27 and were still in transit at year-end.

(c)dalton received goods costing $25,000 on january 2. the goods were shipped fob

shipping point on december 26 by strong company. the goods were not included in the

physical count.

(d)dalton sold goods costing $40,000 to hampton company fob destination on december

30. the goods were received by hampton company on january 8. because the goods had

been shipped, they were excluded from the physical inventory count.

(e)dalton received goods costing $42,000 on january 2 that were shipped fob destination

on december 29. the shipment was a rush order that was suppose to arrive december 31.

this purchase was included in the ending inventory of $192,000.

(f)dalton company, as the consignee, had goods on consignment that cost $3,000.

because these goods were on hand as of december 31, they were included in the

physical inventory count.

analyze the above information and calculate a corrected amount for the ending

inventory. explain the basis for your treatment of each item.

26) determine the interest on the following notes:

(a)$4,000 at 6% for 90 days.

(b)$800 at 9% for 5 months.

(c)$3,000 at 8% for 60 days

(d)$1,600 at 7% for 6 months

27) there are usually how many closing journal entries?

a.5

b.4

c.3

d.2

28) bank errors

a.occur because of time lags

b.must be corrected by debits

c.are infrequent in occurrence

d.are corrected by making an adjusting entry on the depositor’s books

29) at december 31, 2012 keen company had retained earnings of $1,092,000. during

2012 they issued stock for $49,000, and paid dividends of $17,000. net income for 2012

was $201,000. the retained earnings balance at the beginning of 2012 was:

a.$1,276,000

b.$908,000

c.$957,000

d.$1,227,000

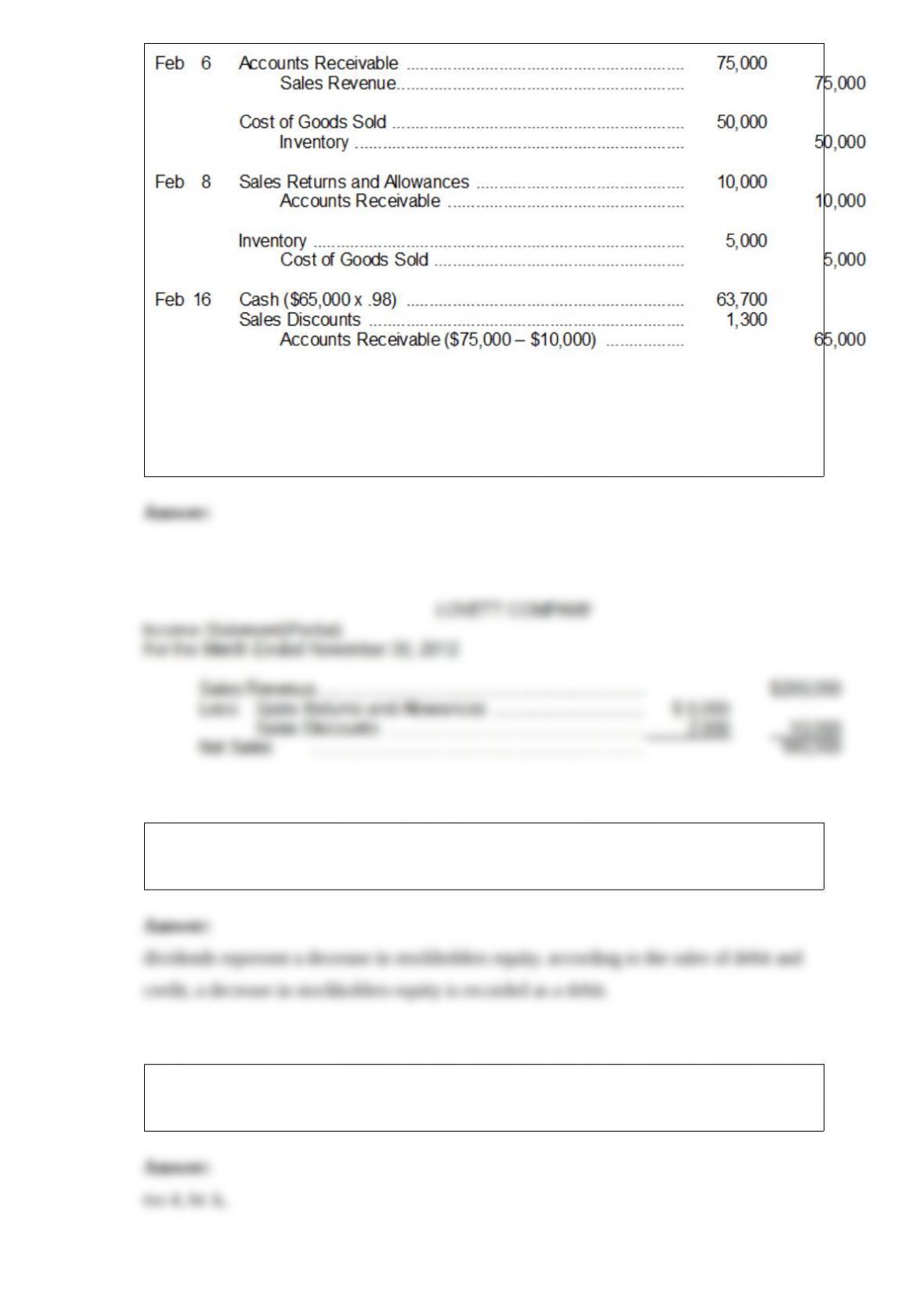

30)

lovett company provides this information for the month of november, 2012: sales on

credit $150,000; cash sales $50,000; sales discount $2,000; and sales returns and

allowances $8,000. prepare the sales revenues section of the income statement based on

this information.

31) why is the dividends account increased by a debit? explain in terms of its

relationship to stockholders equity.

32) the cost of a depreciable asset less accumulated depreciation reflects the book value

of the asset.

33) an _______________ is an individual accounting record of increases and decreases

in specific assets, liabilities, and stockholders equity items.

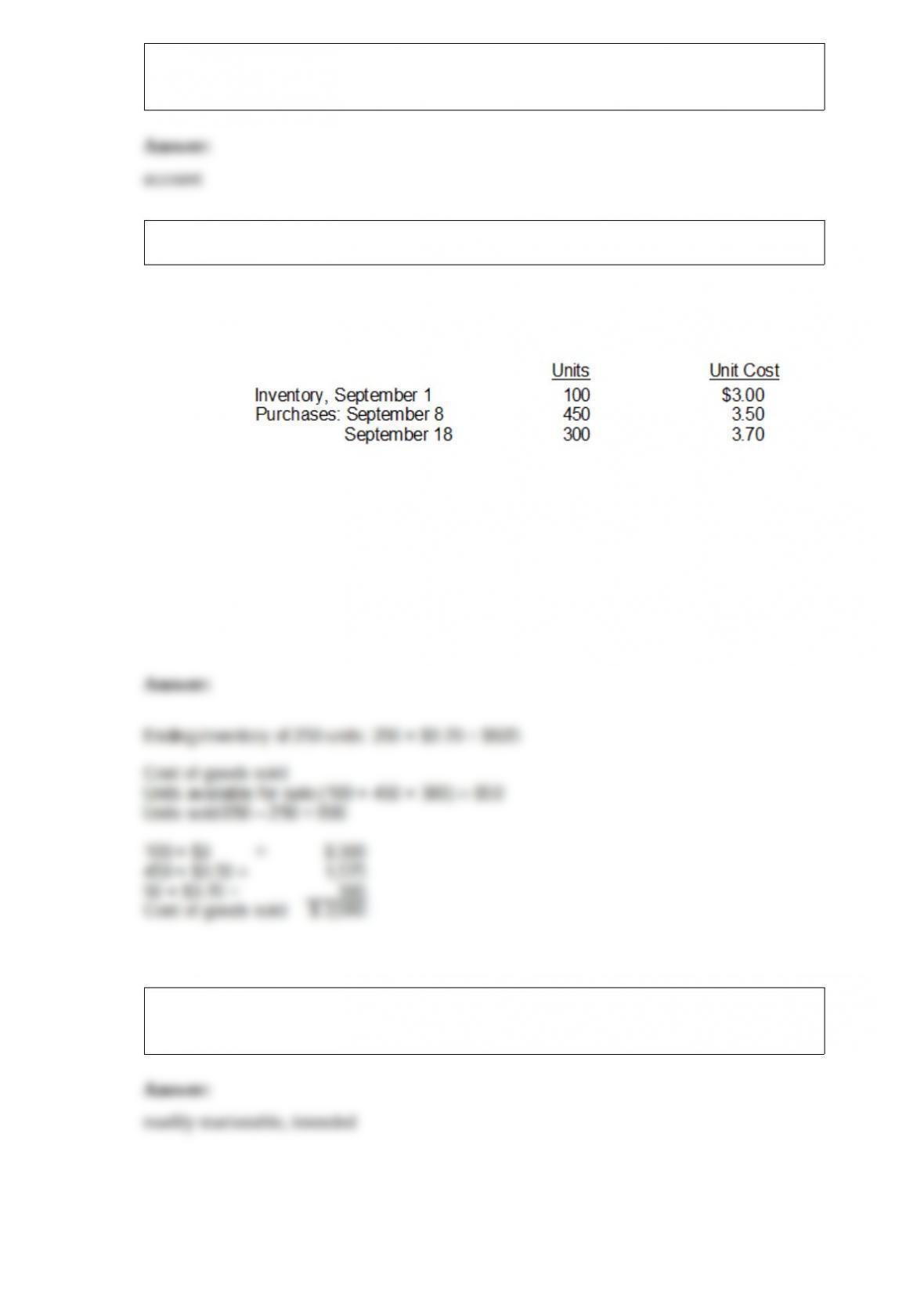

34)

hess company’s inventory records show the following data for the month of september:

a physical inventory on september 30 shows 250 units on hand.

calculate the value of ending inventory and cost of goods sold if the company uses fifo

inventory costing and a periodic inventory system.

35) short-term investments are securities that are _____________ and ______________

to be converted into cash within the next year.